Long-chain Dicarboxylic Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

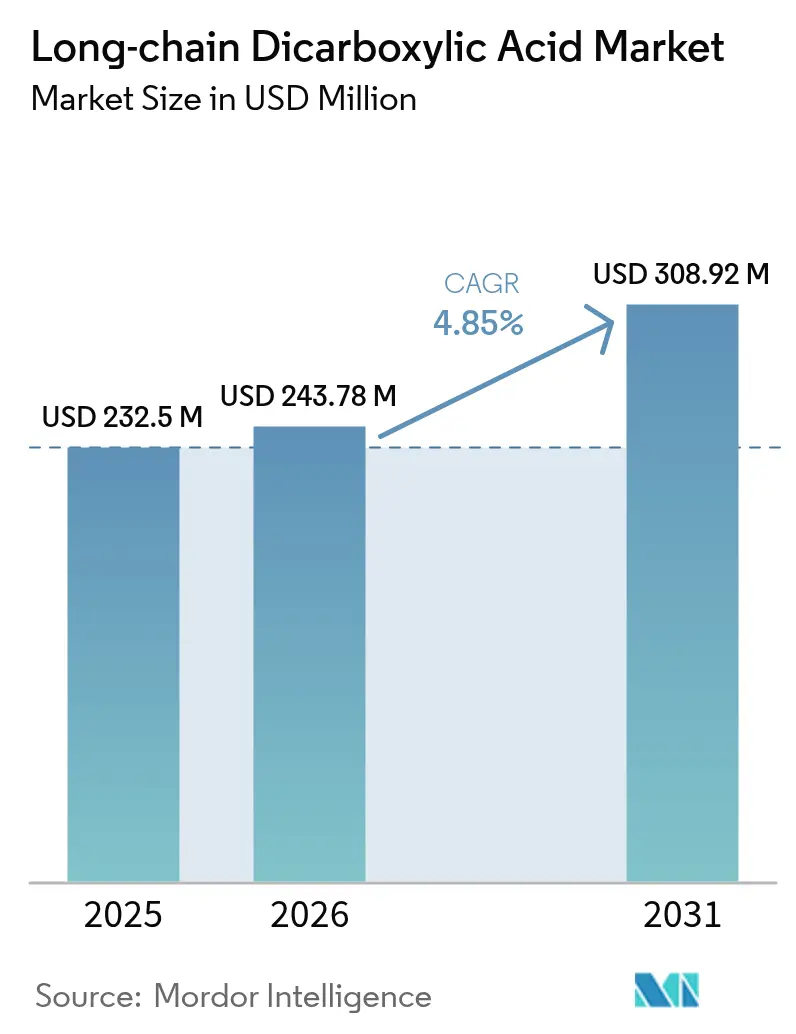

| Market Size (2026) | USD 243.78 Million |

| Market Size (2031) | USD 308.92 Million |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Long-chain Dicarboxylic Acid Market Analysis by Mordor Intelligence

The Long-chain Dicarboxylic Acid market size is expected to grow from USD 232.5 Million in 2025 to USD 243.78 Million in 2026 and is forecast to reach USD 308.92 Million by 2031 at 4.85% CAGR over 2026-2031. Strong demand from high-performance coatings, specialty polyamides, and implant-grade polymers is elevating both volume and value creation. Powder-coated electric‐vehicle battery casings, high-temperature nylons for e-mobility, and bio-based capacity additions in Asia-Pacific are the primary engines of growth. Elevated qualification hurdles in aerospace and medical applications lend pricing power to incumbent suppliers, while tightening sustainability regulations push formulators toward bio-based routes that cut greenhouse-gas emissions by up to 90%. Raw-material volatility, notably in tall-oil feedstocks, keeps cost structures under pressure and spurs diversification of bio-based supply chains.

Key Report Takeaways

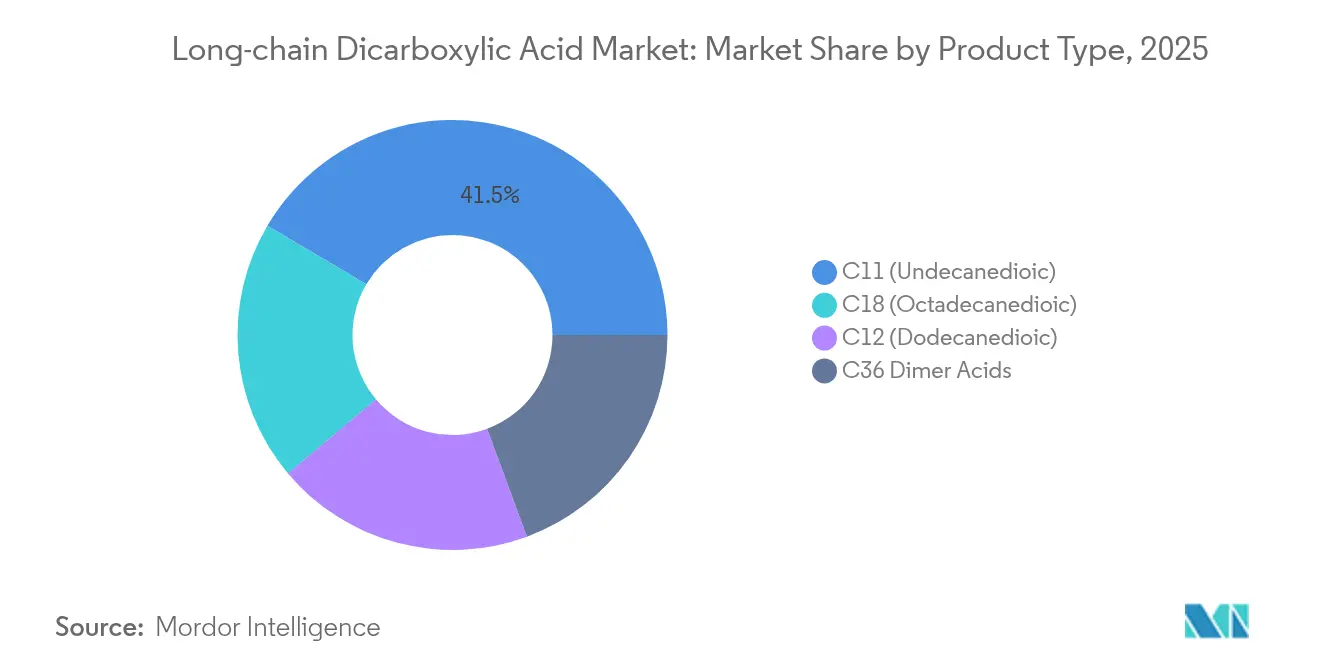

- By product type, C11 (undecanedioic) acid led with the largest share of 41.51% in the Long-chain Dicarboxylic Acid market in 2025. However, C18 (octadecanedioic) acid is projected to expand with the fastest CAGR of 5.22% through 2031.

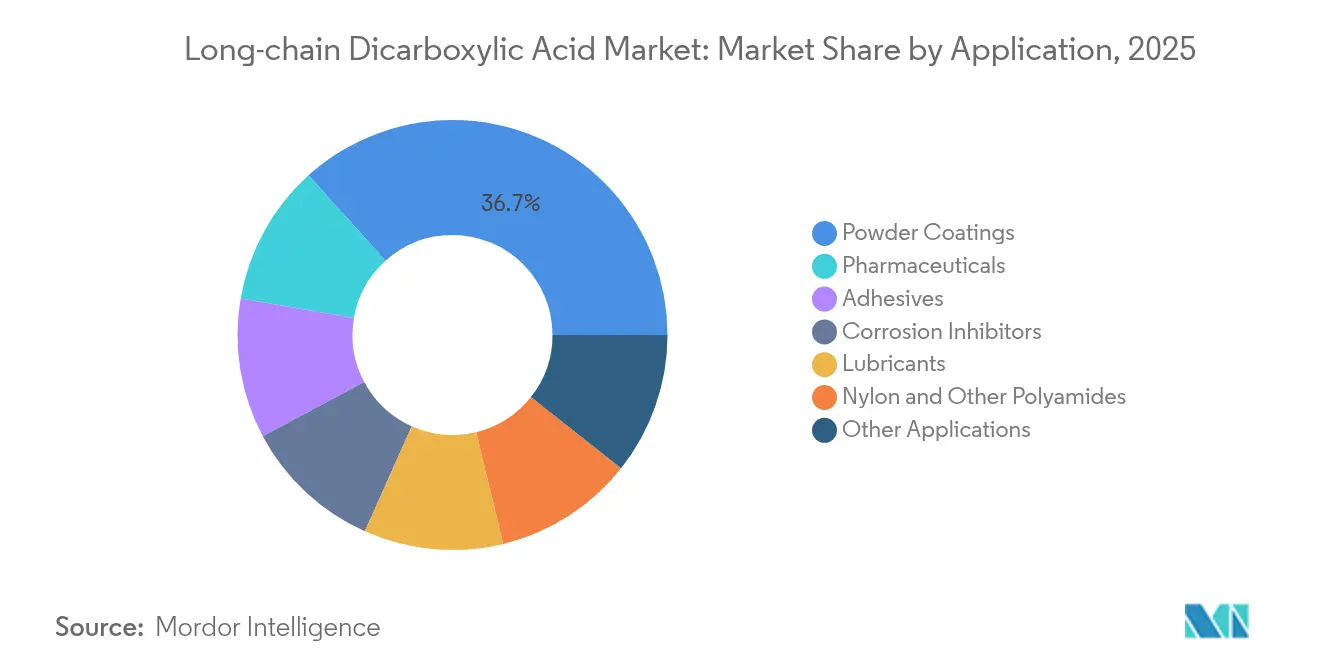

- By application, powder coatings accounted for the largest share of 36.68% in the Long-chain Dicarboxylic Acid market revenue. However, pharmaceuticals application is forecasted to grow the fastest CAGR of 5.63% by 2031.

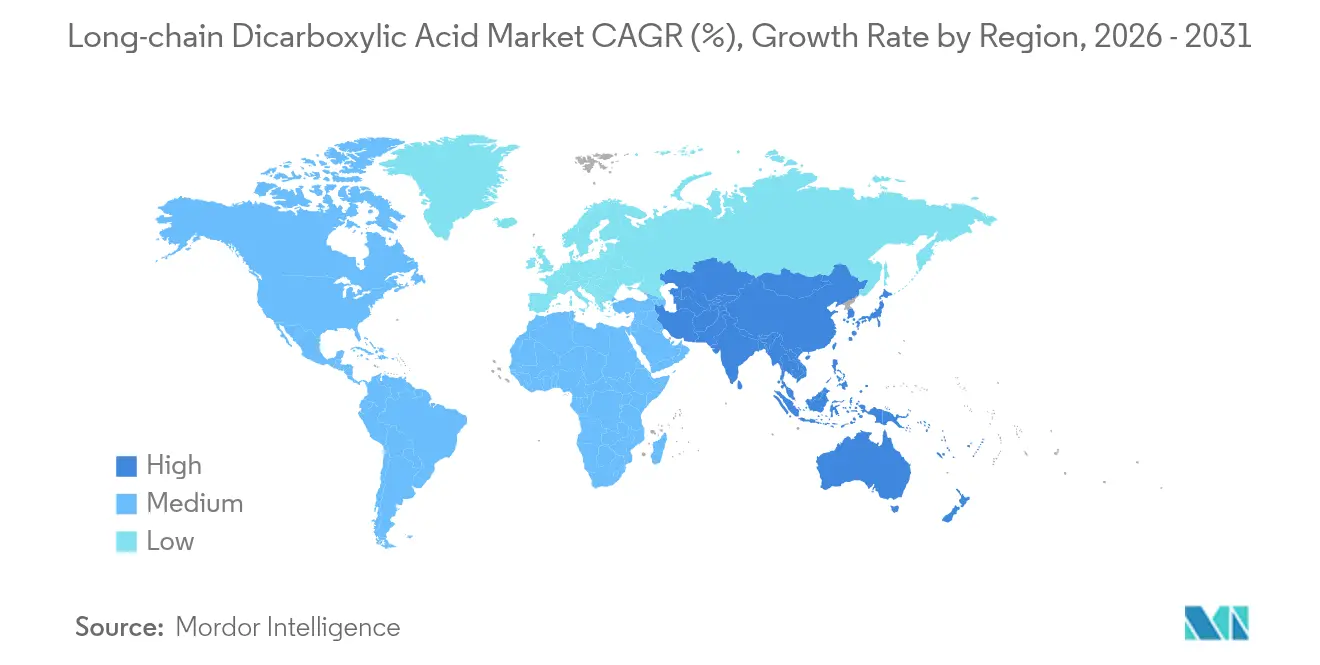

- By geography, Asia-Pacific contributed 43.98% revenue share in 2025, growing at a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Long-chain Dicarboxylic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Powder Coatings for EV Battery Casings | +1.2% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Demand for High-Temperature Nylon in E-mobility | +0.9% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Expanding Aerospace Use of Corrosion-resistant Polyamides | +0.7% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Asia-Pacific's Specialty Polyamide Capacity Additions | +0.8% | APAC core, global supply impact | Short term (≤ 2 years) |

| Niche Medical Demand for LCDA-based Implants | +0.5% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Powder Coatings for EV Battery Casings

Safety-critical electric-vehicle battery housings increasingly specify powder coatings formulated with long-chain dicarboxylic acids for dielectric strength, corrosion resistance, and thermal-shock durability. AkzoNobel introduced a single-spray coating line in 2024 that meets Importer Exporter Code (IEC) battery insulation norms while reducing process steps [1]AKZONOBEL Staff, “Battery-Safe Powder Coatings for EV Platforms,” AkzoNobel, akzonobel.com. Automakers now treat coating performance as a functional component of battery safety, bolstering premium demand for C11-rich crosslinkers. The addressable market widens as commercial-vehicle fleets scale electrification and stationary energy-storage systems demand robust enclosures. Regulatory tightening in China, the United States, and the European Union on battery-fire risk further underpins this driver.

Demand for High-Temperature Nylon in E-mobility

Motor housings, inverter connectors, and fast-charging components in electrified drivetrains operate above 200°C, outstripping the thermal ceilings of legacy polyamides. Long-chain dicarboxylic acids impart molecular flexibility, allowing nylon 6T and 9T to sustain mechanical integrity at 230°C continuous service. BASF’s Ultramid ENDURE platform illustrates the commercial traction for such resins, combining weight savings with chemical resistance to glycol coolants. Broader charging-infrastructure build-out pushes demand into grid-scale enclosures and heat-management systems, sustaining double-digit volume growth for lauric diacid (LCDA)-modified polyamides.

Expanding Aerospace Use of Corrosion-Resistant Polyamides

Composite air-frame parts and cabin-interior panels increasingly substitute metal sub-assemblies with flame-smoke-toxicity compliant polyamides derived from long-chain dicarboxylic acids. Qualification cycles lasting 2-4 years create high switching costs, so suppliers that clear Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) testing secure multi-decade revenue streams. The materials deliver weight reductions and resistance to hydraulic fluids, while retaining strength after salt-spray exposure. New flame, smoke, and toxicity (FST)-rated grades are expanding addressable use in seat structures and galley fittings, widening aerospace pull-through over the forecast horizon.

Asia-Pacific Specialty Polyamide Capacity Additions

Cathay Industrial Biotech’s USD 500 Million investment at Wusu doubles regional LCDA output to meet rising domestic and export demand. China’s five-year plan endorses bio-based chemical self-sufficiency, accelerating additional projects in Jiangsu and Shandong. Near-term capacity growth eases supply bottlenecks for nylon compounds and powder coatings, allowing formulators to design new applications without rationing constraints. Nevertheless, customer concerns over single-country dependency stimulate interest in alternative production hubs across India and Southeast Asia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Tall-oil Supply Impacting Cost Base | -0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Slow Qualification Cycles in Aerospace and Medical | -0.6% | North America & Europe primarily | Long term (≥ 4 years) |

| Limited Global Production Capacity Concentration | -0.4% | Global, with acute impact in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Tall-oil Supply Impacting Cost Base

Tall oil supply volatility creates significant cost pressures for long-chain dicarboxylic acid producers, as this kraft pulping byproduct is a primary feedstock for bio-based production routes. The global production of tall oil approximates 1.2 Million tonnes annually, with supply fluctuations directly tied to paper industry dynamics and forest product demand cycles. Supply chain disruptions in the forestry sector, particularly in North America and Scandinavia, create cascading effects on tall oil fatty acid availability and pricing, directly impacting production costs for downstream dicarboxylic acids. This constraint becomes more pronounced as producers shift toward bio-based feedstocks to meet sustainability requirements, creating increased competition for limited tall oil supplies. The challenge intensifies during periods of reduced paper production, when tall oil generation decreases while demand for bio-based chemicals continues growing.

Slow Qualification Cycles in Aerospace and Medical

Extended qualification timelines in aerospace and medical applications create market entry barriers that constrain rapid adoption of new long-chain dicarboxylic acid formulations. Aerospace material qualification processes typically require 2-4 years of testing and documentation, with requirements for extensive environmental exposure testing and mechanical property validation under various conditions NASA. Medical device applications face similar constraints, with biocompatibility testing and regulatory approval processes extending development timelines and increasing market entry costs. These qualification requirements create a dual constraint: they limit the speed at which innovative formulations can reach market while simultaneously creating barriers for new suppliers seeking to establish relationships with aerospace and medical customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: C11 Dominance Drives Crosslinking Innovation

C11 acid accounted for 41.51% of the Long-chain Dicarboxylic Acid market in 2025, anchoring its status as the go-to crosslinker for powder coatings and reactive adhesives. This chain length delivers optimal melt viscosity and crosslink density, translating into hard yet flexible films for EV battery enclosures. The long-chain dicarboxylic acids market size for C11 applications will advance steadily as automakers widen electric vehicle (EV) portfolios and industrial original equipment manufacturers (OEMs) phase out solvent-borne paints. C18 acid, though only 19.62% of 2025 volume, leads incremental gains at a 5.22% CAGR owing to its role in high-temperature polyamide fibers that service e-mobility and aerospace wire harnesses.

Bio-fermentation technology tilts the competitive field: Cathay Industrial Biotech and several Chinese start-ups operate proprietary yeast strains that yield C11 and C12 diacids at 30% lower unit energy, securing contracts with coating majors and compounders . Western producers respond by improving petrochemical oxidation routes and seeking licensing deals for fermentation know-how. Intellectual-property depth and consistent product purity remain decisive competitive levers across the product spectrum.

By Application: Pharmaceuticals Accelerate Despite Powder-Coating Leadership

Powder-coating formulations consumed 36.68% of 2025 volumes, reinforcing the application’s dominant place in the Long-chain Dicarboxylic Acid market. Robust demand from electrified mobility, architectural cladding, and general-industrial components sustains mid-single-digit growth, even as formulators extract higher functionality per kilogram. Pharmaceuticals captured just 10.60% volume in 2025 but posted a leading 5.63% CAGR, leveraging LCDA-based polyesters that biodegrade without acidic by-products, a key attribute for resorbable sutures and drug-eluting stents. As clinical evidence accumulates, the Long-chain Dicarboxylic Acids market share of pharmaceuticals will double by 2031.

Nylon and other polyamide uses remain the second-largest application block, supported by automotive lightweighting mandates and the shift to metal-replacement in electrical connectors. Adhesives and lubricants combine niche technical requirements, chemical resistance, high-temperature stability, and hydrophobicity, which LCDA chemistries meet uniquely. Corrosion-inhibitor demand gathers momentum in offshore wind foundations and marine shipping, where legacy chromate systems face regulatory phase-out.

Geography Analysis

Asia-Pacific generated 43.98% of global sales in 2025, sustaining the fastest regional CAGR at 6.05% through 2031. The region hosts integrated value chains from tall-oil derivatives to EV and smartphone assembly, ensuring captive demand for C11-C18 diacids. Cathay Industrial Biotech’s USD 500 million doubling of Wusu output exemplifies government-backed capacity build-outs that de-risk supply security for downstream users. India and Vietnam are deploying fermentation hubs tied to sugar-ethanol corridors, widening regional diversification beyond China.

North America represents an innovation-driven hub where aerospace and medical OEMs adopt LCDA-based materials under rigorous performance protocols. INVISTA is re-commissioning hexamethylene-diamine assets with a USD 23 million CAD upgrade to ensure backward integration into high-temperature nylon franchises. Eastman Chemical’s USD 375 million Department of Energy grant for a second methanolysis site illustrates federal incentives harnessed to circular-economy objectives. Such moves reinforce domestic supply resilience amid a growing policy emphasis on strategic materials.

Europe contends with energy-price inflation that compresses margins for oxidation-based LCDA routes, but regulatory leadership on sustainability favors bio-based imports and local biotech collaborations. Croda International’s partnership with the United Kingdom universities aims to unlock biodegradable polymer platforms that embed undecanedioic acid for home-care and crop-care formulations. The European Commission’s biotechnology roadmap targets higher-value niches, encouraging corporate alignment toward specialty LCDA derivatives. Emerging markets in South America and the Middle East & Africa are building demand off low bases, centered on lubricants for mining fleets and corrosion inhibitors for infrastructure expansion.

Competitive Landscape

The Long-chain Dicarboxylic Acid market is moderately consolidated with major players, such as Cathay Biotech Inc., INVISTA, dsm-firmenich, Zibo Guangtong Chemical Co., Ltd., and Henan Junheng Industrial Group Biotechnology Co., Ltd. INVISTA and Eastman Chemical command entrenched positions in nylon intermediates, leveraging integrated monomer streams and multi-regional production footprints. Cathay Biotech Inc. possesses cost-efficient fermentation, shipping C11 diacid at benchmark quality while pioneering C12 production with a greenhouse-gas advantage. Investment patterns highlight a pivot to sustainability. Eastman’s USD 2.25 billion circular-chemistry program and Hyosung’s USD 1 billion Vietnamese plant underline capital re-allocation toward low-carbon intermediates. Qualification moats in aerospace and medical create durable revenue streams for incumbents, yet high entry costs hinder diversification, keeping overall market concentration moderate.

Long-chain Dicarboxylic Acid Industry Leaders

Cathay Biotech Inc.

INVISTA

Henan Junheng Industrial Group Biotechnology Co., Ltd.

Zibo Guangtong Chemical Co., Ltd.

dsm-firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Hyosung announced an investment of USD 1 billion in a Vietnam fermentation facility to produce biobased products 50,000 metric tonnes annually by 2026. The investment aligns with Asia-Pacific's growing focus on bio-based chemical production and potential synergies with long-chain dicarboxylic acids.

- March 2024: Eastman Chemical Company received a grant worth USD 375 Million from the Department of Energy to build a second methanolysis facility in Longview, Texas. The development aims to enhance molecular recycling and sustainable chemical production for long-chain dicarboxylic acids in recycled polymer applications.

Global Long-chain Dicarboxylic Acid Market Report Scope

The scope of the long-chain dicarboxylic acid market report includes:

| C11 (Undecanedioic) |

| C12 (Dodecanedioic) |

| C18 (Octadecanedioic) |

| C36 Dimer Acids |

| Powder Coatings |

| Nylon and Other Polyamides |

| Adhesives |

| Lubricants |

| Pharmaceuticals |

| Corrosion Inhibitors |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of APAC | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Chain Length) | C11 (Undecanedioic) | |

| C12 (Dodecanedioic) | ||

| C18 (Octadecanedioic) | ||

| C36 Dimer Acids | ||

| By Application | Powder Coatings | |

| Nylon and Other Polyamides | ||

| Adhesives | ||

| Lubricants | ||

| Pharmaceuticals | ||

| Corrosion Inhibitors | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of APAC | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the Long-chain Dicarboxylic Acid market by 2031?

The Long-chain Dicarboxylic Acid market size is forecast to reach USD 308.92 Million by 2031, driven by a 4.85% CAGR.

Which region leads demand and growth for long-chain dicarboxylic acids?

Asia-Pacific commands 43.98% of 2025 revenue and is expanding fastest at 6.05% CAGR thanks to large-scale bio-based capacity additions.

Why are long-chain dicarboxylic acids critical to EV battery casings?

They enable powder-coating formulations with high dielectric strength and corrosion resistance, improving battery safety and longevity.

Which product type dominates the market today?

C11 (undecanedioic) acid holds 41.51% market share due to its optimal crosslinking performance in coatings and adhesives.

What is the main constraint on market growth?

Volatile tall-oil feedstock supply raises production costs, clearing 0.8% points off forecast CAGR.

Page last updated on: