Digital Vault Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

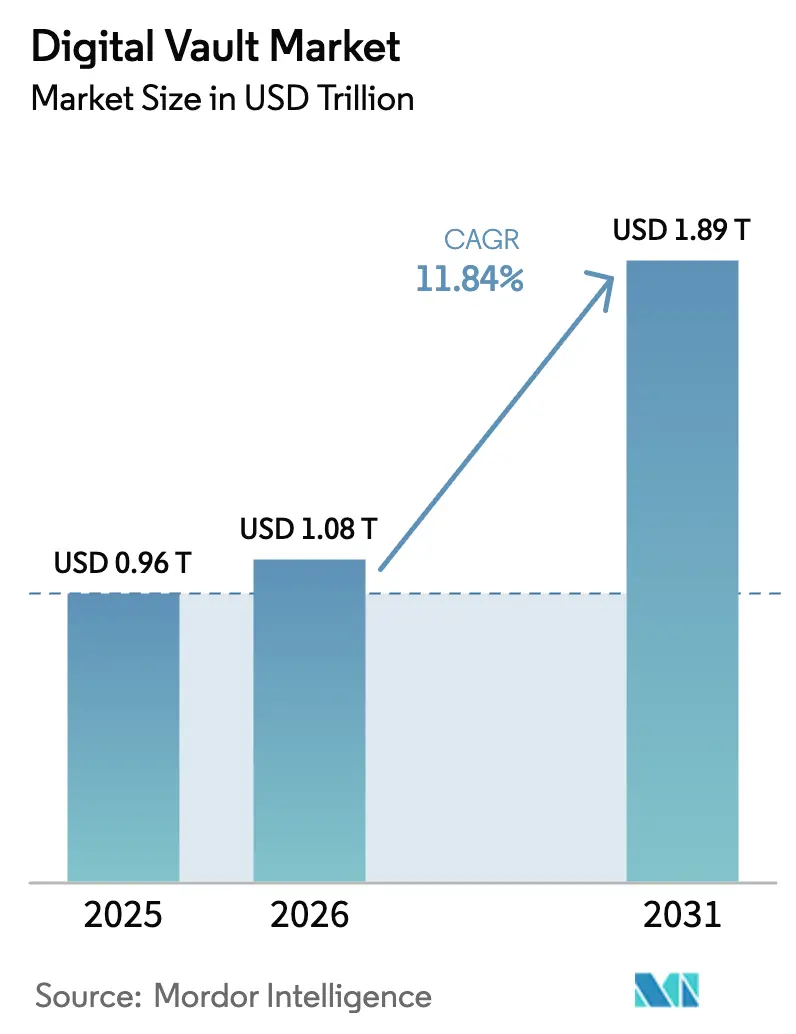

| Market Size (2026) | USD 1.08 Trillion |

| Market Size (2031) | USD 1.89 Trillion |

| Growth Rate (2026 - 2031) | 11.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Vault Market Analysis by Mordor Intelligence

The Digital Vault Market size is projected to be USD 0.96 trillion in 2025, USD 1.08 trillion in 2026, and reach USD 1.89 trillion by 2031, growing at a CAGR of 11.84% from 2026 to 2031. Demand is rising as enterprises face monetary penalties that surpassed EUR 1.2 billion (USD 1.3 billion) for sub-par data protection in 2024. Quantum-computing roadmaps that could break legacy encryption within the decade have accelerated the adoption of post-quantum modules. At the same time, United States breach costs climbed to USD 9.36 million in 2024, nearly double the global average, prompting buyers to adopt zero-trust architectures centered on vault isolation. Vendors are differentiating themselves through cryptographic agility, automated compliance dashboards, and anomaly detection that targets ungoverned artificial intelligence workloads. White-space opportunities are emerging in decentralized custody of tokenized assets, while cloud-centric price competition is squeezing niche specialists but lowering entry barriers for small and medium enterprises.

Key Report Takeaways

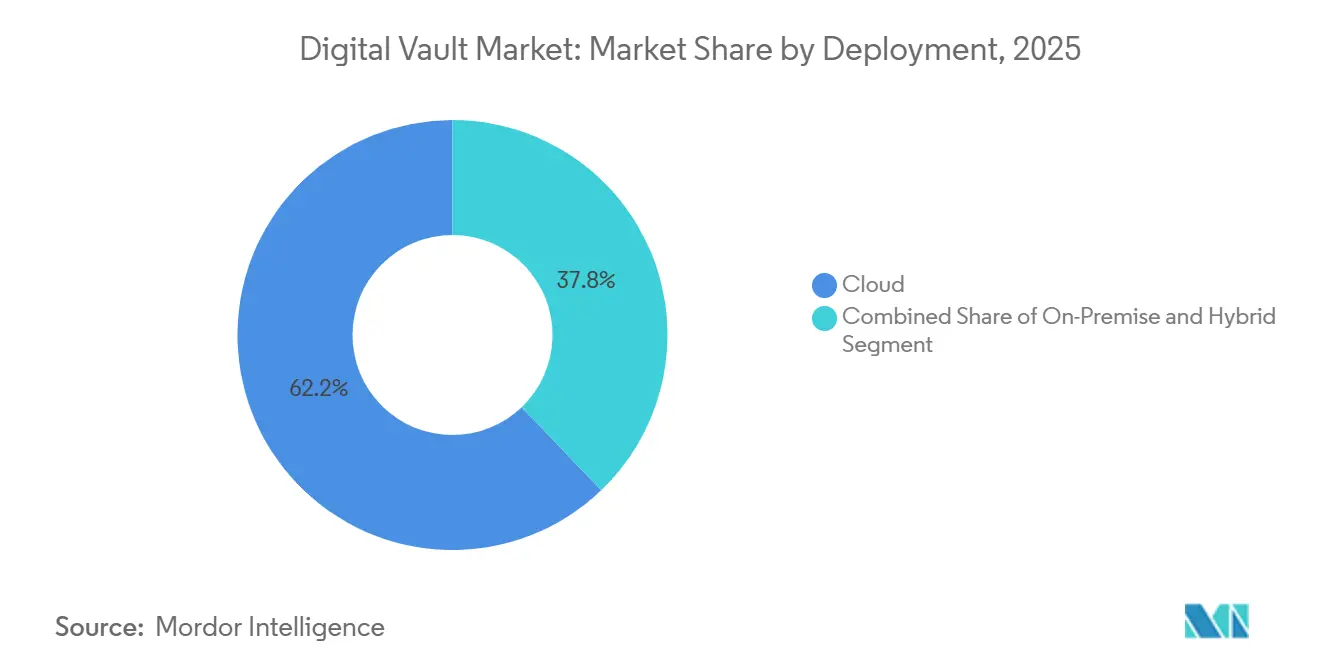

- By deployment, cloud configurations held 62.17% revenue share in 2025; hybrid models are forecast to grow at a 12.19% CAGR through 2031.

- By component, solutions commanded 72.48% of 2025 spending, whereas services are projected to expand at a 12.07% CAGR to 2031.

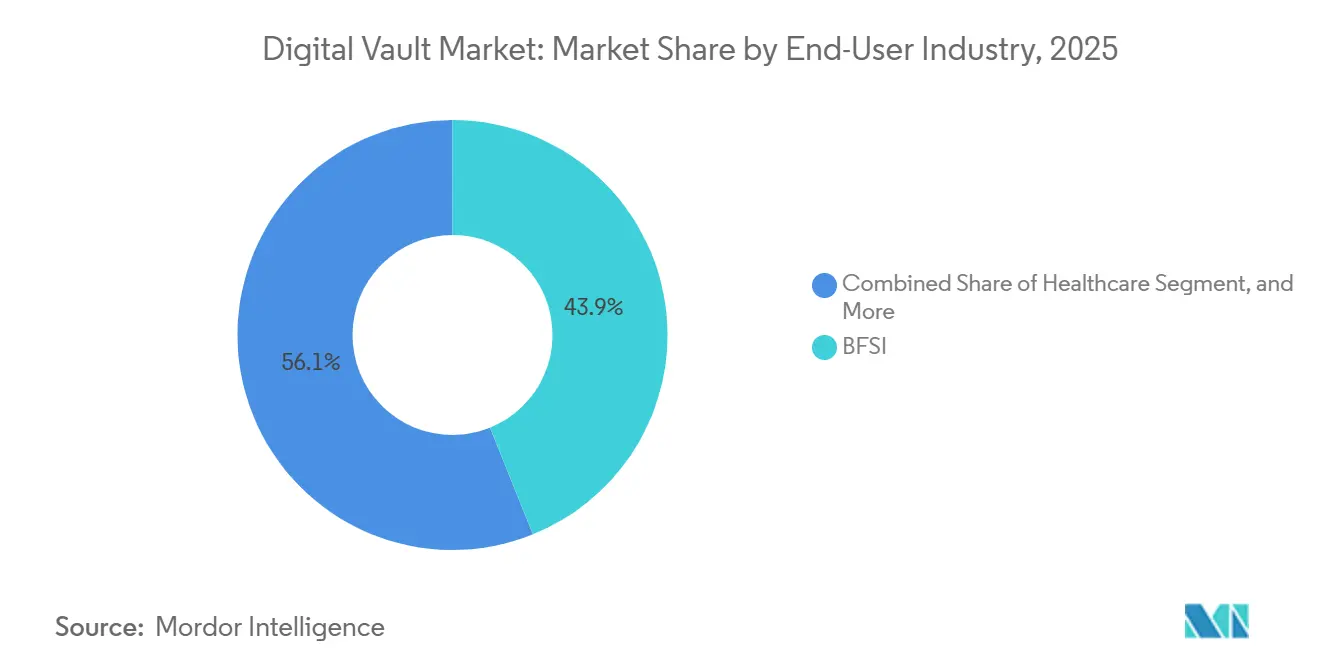

- By end-user industry, banking, financial services, and insurance accounted for 43.89% of the 2025 demand; healthcare is projected to have the fastest growth at a 12.83% CAGR through 2031.

- By organization size, large enterprises accounted for 59.18% of the adoption in 2025, while small and medium enterprises are advancing at a 12.11% CAGR through 2031.

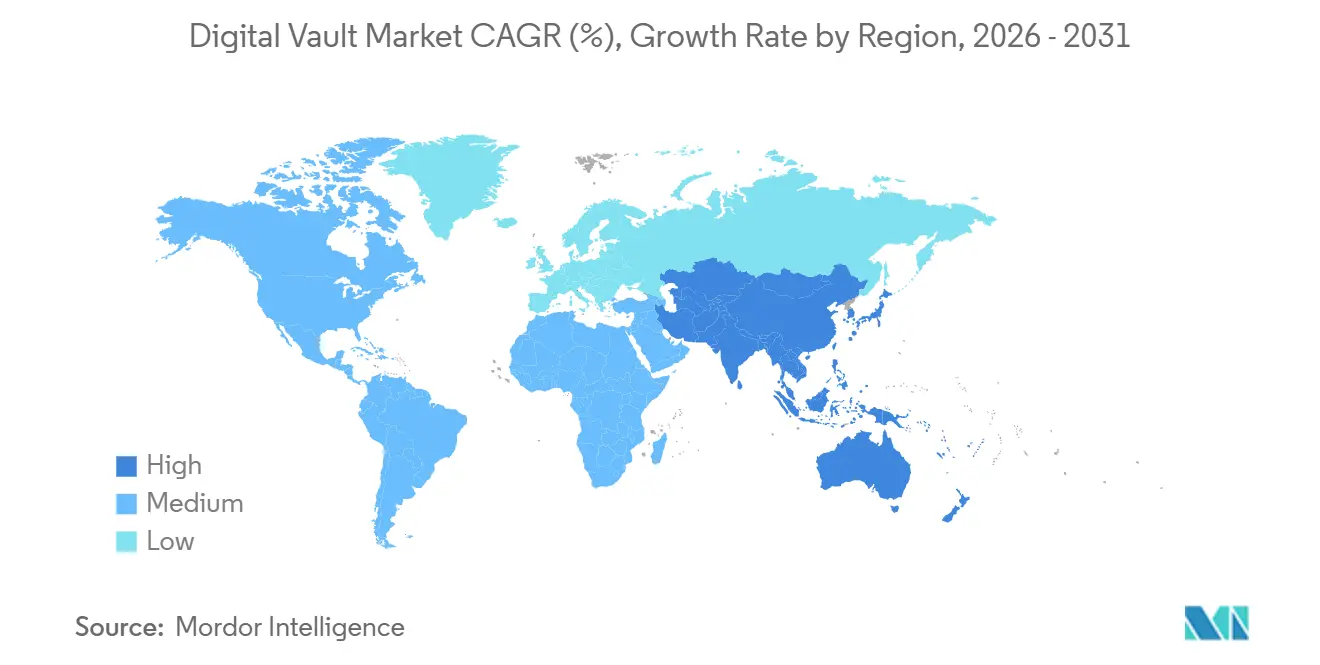

- By geography, North America generated 39.73% of 2025 revenue, whereas Asia-Pacific is expected to register the highest regional growth with a 12.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Vault Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Data-Breach Litigation Risk | +2.4% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Expanding Zero-Trust Architecture Adoption | +2.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Handling of Data Generated Through Connected Devices | +1.8% | Global, with Asia-Pacific leading IoT deployments | Medium term (2-4 years) |

| Decentralised Digital-Asset Custody in BFSI | +1.6% | North America, Europe, Singapore, Switzerland | Medium term (2-4 years) |

| Quantum-Ready Encryption Roll-outs | +1.5% | Global, with early adoption in BFSI and government sectors | Long term (≥ 4 years) |

| Venture Funding for Reg-Tech Start-ups | +1.3% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Data-Breach Litigation Risk

Average United States breach costs climbed to USD 9.36 million in 2024, and European regulators issued EUR 1.2 billion (USD 1.3 billion) in fines for weak encryption, leading security officers to prioritize vaults with immutable audit trails and rapid incident reporting.[1]IBM Security, “Cost of a Data Breach Report 2024,” ibm.com Shadow artificial-intelligence projects inflated remediation outlays by USD 670,000 per incident, elevating demand for discovery engines embedded in vault layers. Enterprises are inserting indemnification clauses that obligate partners to use vault-grade encryption, extending compliance pressure across supply chains. Litigation exposure is, therefore, pushing even mid-market organizations to adopt the digital vault market’s advanced feature sets.

Expanding Zero-Trust Architecture Adoption

NIST Special Publication 1800-35 mapped 19 federal zero-trust implementations in 2025, offering reference designs that commercial buyers are now emulating.[2]National Institute of Standards and Technology, “Post-Quantum Cryptography Standardization,” nist.gov Continuous authentication and micro-segmentation make vaults the authoritative source for policy enforcement, shrinking procurement cycles from 18 to 9 months. CISA found that agencies are 78% complete on encryption yet only 52% complete on data governance, a gap that vault classification engines directly address. Financial institutions reported that vault isolation blocked lateral movement in 83% of simulated ransomware events, validating the architecture’s risk-reduction value.

Handling of Data Generated Through Connected Devices

Connected devices are forecast to surpass 30 billion units by 2027, flooding enterprises with telemetry that requires real-time encryption and long-term archival. Healthcare genomic files often exceed 200 gigabytes per patient, forcing providers to offload encryption to hardware security modules to avoid clinical latency. Automotive firms encrypt telematics streams to comply with GDPR location data rules.[3]European Data Protection Board, “Annual Report 2024,” edpb.europa.eu Telecom operators in China and India deploy edge vaults to meet localization mandates while minimizing backhaul. These use cases position the digital vault market as the linchpin for secure IoT scale-up.

Decentralised Digital-Asset Custody in BFSI

Central banks and commercial lenders validated lattice-based encryption for tokenized bond settlement during Project Leap in 2025. Switzerland’s regulator permits distributed-ledger custody provided that multi-signature vaults manage key recovery. India’s central bank published a quantum-readiness roadmap in 2025, urging pilot deployments to begin in 2026. These moves are driving banks to select platforms that bridge traditional rails with blockchain and support post-quantum cryptography, a capability still limited to a handful of vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Dependence on Physical Vaults | -1.2% | Global, with higher impact in tier-2 banks across North America and Europe | Short term (≤ 2 years) |

| High Switching Costs for Tier-2 Banks | -1.0% | North America, Europe, and Asia-Pacific regional banks | Medium term (2-4 years) |

| Fragmented Global Data-Sovereignty Mandates | -0.9% | Global, with acute friction in Europe, China, India, and Brazil | Medium term (2-4 years) |

| Skills Gap in Post-Quantum Cryptography | -0.7% | Global, with concentration in markets lacking specialized training programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Dependence on Physical Vaults

Tier-2 banks allocate up to 40% of security budgets to maintain physical archives, and audits in some jurisdictions still request paper records. Migrations, therefore, require dual operations for up to two years, doubling overhead. Institutions in regions with intermittent connectivity also hesitate to rely on cloud vaults, fearing service disruptions that could delay customer transactions. This inertia slows penetration of the digital vault market among mid-sized lenders.

High Switching Costs for Tier-2 Banks

Migration from 1990s-era core systems can cost more than USD 50 million once licensing, data conversion, and downtime are tallied. Proprietary file formats often force manual validation, consuming thousands of labor hours. Vendors prioritize Fortune 500 accounts, leaving regional banks with fewer customization options and less favorable pricing. The result is a bifurcated digital vault market, where leading banks adopt quantum-ready vaults, while their smaller peers lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Configurations Gain Traction

Hybrid architectures are advancing at a 12.19% CAGR, as buyers balance sovereignty mandates with cloud scalability. Cloud controlled 62.17% of 2025 revenue, yet enterprises in China and Russia route sensitive fields to on-premise tiers to navigate cross-border audits. For high-frequency trading, keeping order data on collocated servers while archiving history in cloud vaults cuts per-terabyte storage by 80%. Disaster-recovery planning improves because snapshots can replicate across multiple regions without requiring additional hardware. Telecommunications carriers deploy edge vault nodes for subscriber data, illustrating how hybrid models underpin the digital vault market’s versatility.

Hybrid vaults reduce latency, support multi-region compliance, and align with NIST zero-trust guidance, which endorses distributed authentication without single points of failure. By transitioning predictable workloads to consumption pricing, this design alleviates pressures on capital budgets in the digital vault market. It enables organizations to manage costs more effectively, providing flexibility and scalability while addressing CFO concerns about significant upfront spending.

By Component: Services Surge on Integration Complexity

Services are growing at a 12.07% CAGR as enterprises discover that vault projects entail connectors for legacy databases, identity providers, and security information and event management platforms. Engagements often run 6-12 months, explaining why services are narrowing the revenue gap with solutions, which captured 72.48% of the market in 2025. Consulting teams conduct cryptographic agility audits that map encryption inventories and prioritize post-quantum upgrades, commanding fees exceeding USD 500,000 at major banks. Managed-services bundles now include 24/7 monitoring and incident response, a draw for mid-market firms lacking security operations centers.

While licensing encryption engines and compliance dashboards continues to drive solutions revenue, vendors are progressively transitioning to usage-based models. This shift underscores that, even as professional services expand the digital vault market due to integration complexities, the demand for core software remains robust. The adoption of usage-based models allows vendors to align pricing with customer consumption patterns, offering greater flexibility and potentially increasing customer retention. Additionally, the growing reliance on professional services highlights the need for expertise in managing and integrating these solutions, further contributing to market growth.

By End-User Industry: Healthcare Accelerates Adoption

Healthcare is projected to log a 12.83% CAGR, the fastest among end users, as genomic sequencing and telemedicine amplify sensitive data volumes. In 2024, United States regulators clarified that genomic data falls under HIPAA, prompting retrofits of biobanks with vault-grade encryption. Telemedicine platforms encrypt consultation streams both at rest and in transit, with keys that patients can revoke, thereby safeguarding privacy in home-care scenarios. Banking, financial services, and insurance retained 43.89% of the 2025 demand through long-standing mandates, such as PCI DSS.

Hospitals are integrating vaults with medical devices, making firmware updates tamper-proof. Such measures not only bolster the digital vault market share in healthcare but also underscore the necessity for attribute-based access. This access mechanism ensures secure and efficient monitoring of clinician roles and permissions across federated networks, enhancing operational security and compliance with regulatory standards.

By Organization Size: SMEs Embrace Consumption Pricing

Small and medium-sized enterprises are advancing at a 12.11% CAGR, narrowing the gap with large enterprises, which held a 59.18% adoption rate in 2025. Cloud-native vendors offer vault subscriptions for under USD 1,000 per month, eliminating the need for large upfront licenses. Global privacy laws impose uniform penalties regardless of size, prompting SMEs to adopt rigorous encryption standards. Managed services providers supply turnkey packages that include migration and compliance reporting, removing talent barriers.

Large enterprises leverage volume discounts and customize vault workflows for legacy mainframes, maintaining their dominant spending position. Consumption pricing is expanding the digital vault market's reach, making enterprise-grade encryption accessible to smaller firms. This pricing model allows businesses with limited budgets to adopt robust security measures, replacing their reliance on makeshift file protection with more reliable and scalable solutions.

Geography Analysis

North America captured 39.73% of 2025 revenue, buoyed by United States breach-notification rules and sectoral statutes such as HIPAA. Hyperscalers embed vault functionality into infrastructure services, undercutting niche vendors on price. Canada’s PIPEDA applies extraterritorial reach, compelling cross-border operators to encrypt data that flows south. Mexico’s fintech law requires encrypted transaction records, prompting traditional banks to modernize their systems.

The Asia-Pacific region is forecast to post the fastest growth at a 12.89% CAGR. China enforces fines up to CNY 50 million (USD 7 million) or 5% of revenue for unauthorized transfers, driving demand for domestic vault instances. India’s data-protection act grants citizens data-portability rights, leading enterprises to deploy self-service vault portals. Japan tightened consent rules in 2022, while Australia recorded 527 notifiable breaches in fiscal 2024, with 60% occurring in healthcare and finance, signaling an urgent need for stronger data-protection controls.

Europe wields global influence through GDPR, with EUR 1.2 billion in 2024 fines steering multinationals toward encryption that renders data unusable to unauthorized parties. The Middle East accelerates the rollout of vaults under Saudi Vision 2030's e-government goals. Brazil's LGPD, which is similar to the GDPR, requires firms operating in South America to establish local data vault instances to ensure compliance with data protection regulations. This regulation emphasizes the importance of safeguarding personal data within the region.

Competitive Landscape

In 2025, the top 10 suppliers commanded a revenue share of approximately 55%-60%, signaling a moderate market concentration. This level of concentration reflects a competitive environment where a few key players hold significant influence. Hyperscalers, by bundling vaults into broader cloud contracts, are compelling specialists to emphasize certifications and niche modules, like post-quantum custody tailored for banking. These strategies are crucial for specialists to differentiate themselves and address the evolving demands of specific verticals.

Vendors rush to comply with NIST post-quantum standards, which were released in 2024, as financial institutions set 2027 deadlines for algorithm migration. Patent filings in homomorphic encryption and secure multi-party computation illustrate interest in enabling analytics on encrypted data. Startups differentiate through usage pricing and drag-and-drop connectors, lowering switching costs for SMEs.

Mergers and acquisitions focus on folding identity management and vault technology into unified zero-trust suites. Meanwhile, pilots in Switzerland and Singapore are validating decentralized custody for tokenized real-world assets, a niche that is expected to mature once other regulators issue guidance. Overall, the digital vault market rewards suppliers that combine cryptographic agility, compliance dashboards, and flexible deployment models.

Digital Vault Industry Leaders

International Business Machines Corporation

CyberArk Software Ltd.

Hitachi, Ltd.

Fiserv, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: BIS expanded Project Leap to include the Monetary Authority of Singapore, widening decentralized custody trials for government bonds.

- July 2025: The Reserve Bank of India released a quantum-readiness whitepaper outlining phase-wise vault migration timelines through 2030.

- June 2025: NIST Special Publication 1800-35 detailed 19 federal zero-trust implementations, offering blueprints for commercial vault rollout.

- January 2025: The European Data Protection Board reported EUR 1.2 billion in GDPR fines for 2024, with 40% tied to inadequate encryption.

Global Digital Vault Market Report Scope

The Digital Vault Market Report is Segmented by Deployment (On-Premise, Cloud, Hybrid), Component (Solutions, and Services), End-User Industry (BFSI, Government, IT and Telecommunication, Healthcare, Other End-User Industries), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud |

| Hybrid |

| Solutions |

| Services |

| BFSI |

| Government |

| IT and Telecommunication |

| Healthcare |

| Other End-User Industries |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Component | Solutions | ||

| Services | |||

| By End-User Industry | BFSI | ||

| Government | |||

| IT and Telecommunication | |||

| Healthcare | |||

| Other End-User Industries | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How fast is the digital vault market expected to grow through 2031?

It is forecast to expand from USD 1.08 trillion in 2026 to USD 1.89 trillion by 2031 at an 11.84% CAGR, driven by regulatory pressure and quantum-security readiness.

Which region will register the highest growth in digital vault adoption?

Asia-Pacific is projected to log the fastest regional growth with a 12.89% CAGR, propelled by China’s and India’s strict data-localization laws.

Why are hybrid deployments gaining popularity?

Hybrid vaults balance data-sovereignty rules with cloud scalability, cut disaster-recovery spending, and align with NIST zero-trust guidance.

What makes healthcare the fastest-growing end-user segment?

Genomic sequencing, telemedicine, and stricter HIPAA interpretations boost demand for vaults that secure large sensitive datasets and support granular patient consent.

How are small and medium enterprises entering the digital vault space?

Cloud-native vendors offer consumption pricing under USD 1,000 per month and managed-services bundles, allowing SMEs to meet regulatory encryption requirements without large capital outlays.

Page last updated on: