Digital MRO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

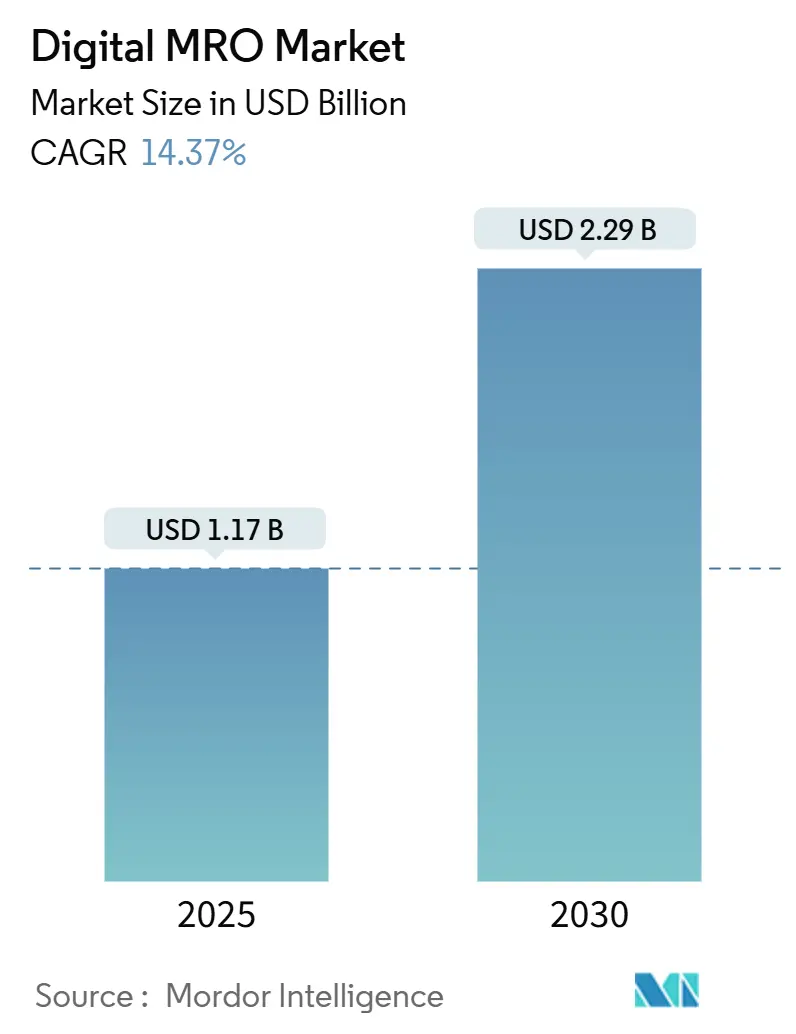

| Market Size (2025) | USD 1.17 Billion |

| Market Size (2030) | USD 2.29 Billion |

| Growth Rate (2025 - 2030) | 14.37% CAGR |

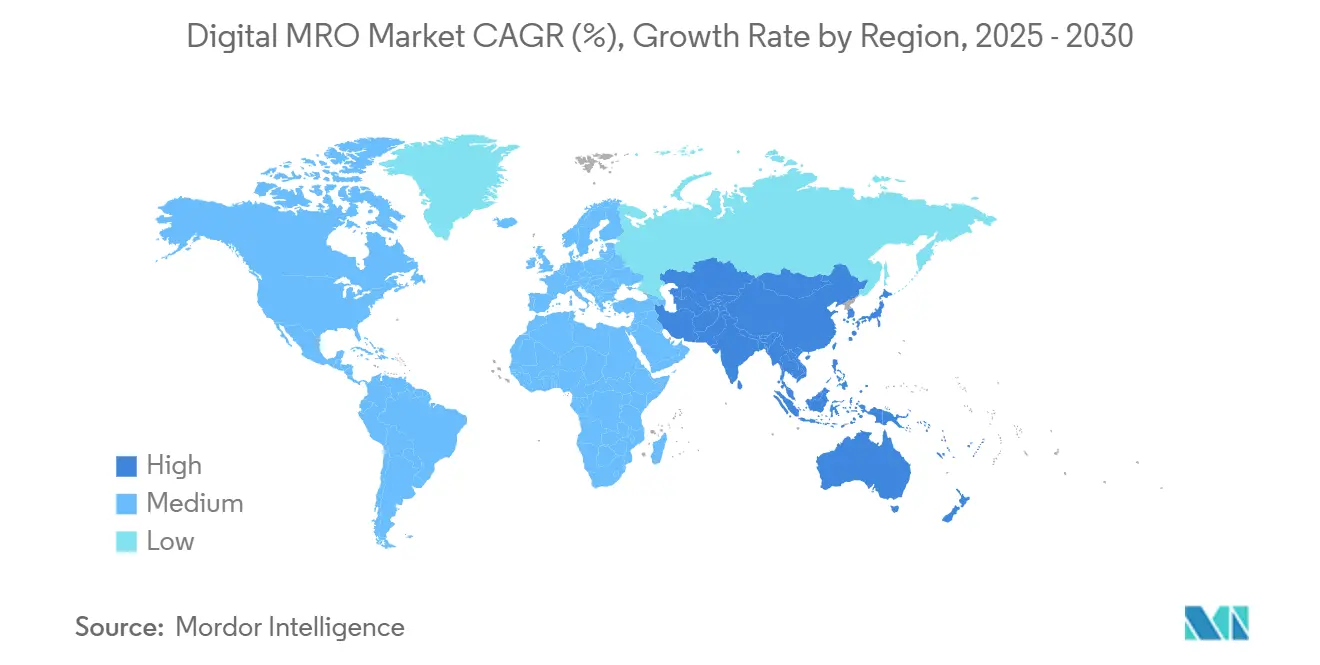

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital MRO Market Analysis by Mordor Intelligence

The digital MRO market size is valued at USD 1.17 billion in 2025 and is projected to reach USD 2.29 billion by 2030, reflecting a 14.37% CAGR over the forecast period. A shift from reactive fixes toward data-driven, predictive maintenance anchors this growth as airlines seek higher aircraft availability and lower lifecycle costs. Widespread sensor retrofits, the maturation of cloud-based data exchanges, and OEM programs that bundle hardware with analytics services strengthen market adoption. Growing fleet sizes in emerging economies fuel demand, while rising sustainability mandates encourage digital tracking of carbon impacts within maintenance workflows. Competitive momentum intensifies as airframe and engine makers extend beyond parts sales into integrated digital platforms that promise faster turnarounds and new recurring-revenue streams.

Key Report Takeaways

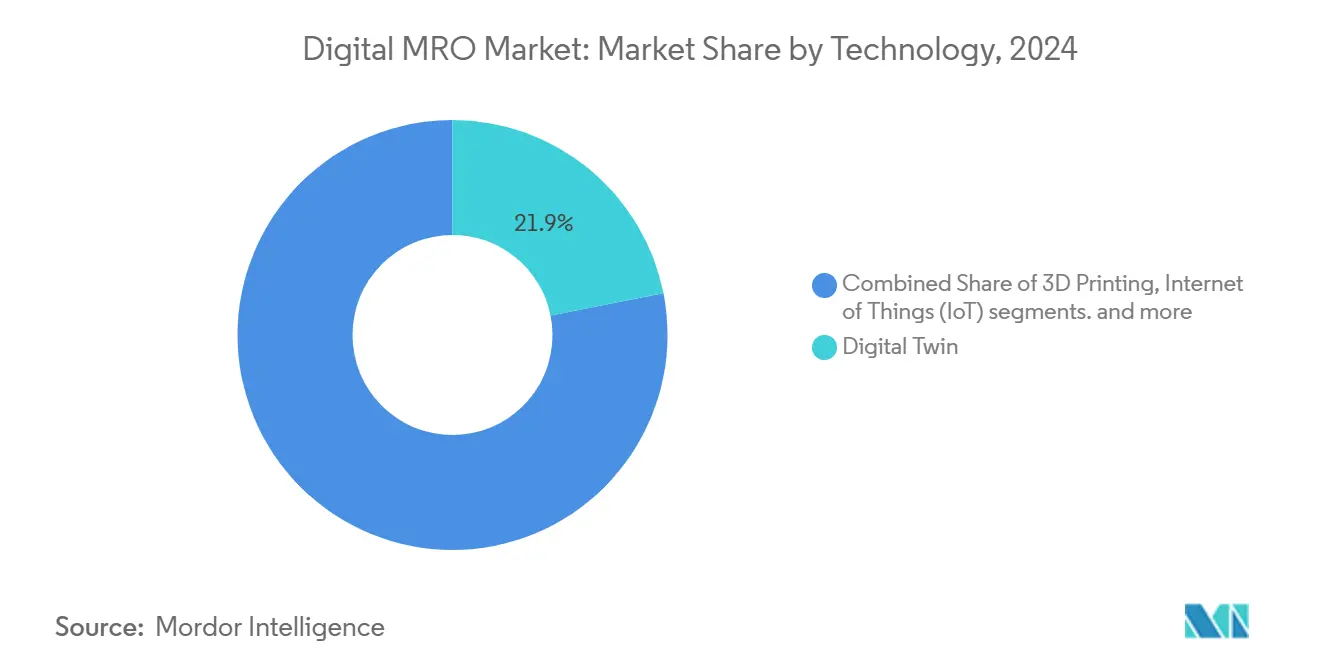

- By technology, digital twin tools captured 21.89% of the digital MRO market share in 2024 and are forecasted to expand at a 17.65% CAGR to 2030.

- By application, the inspection and damage assessment segment led with a 24.76% revenue share in 2024; predictive analysis is projected to grow at a 16.57% CAGR through 2030.

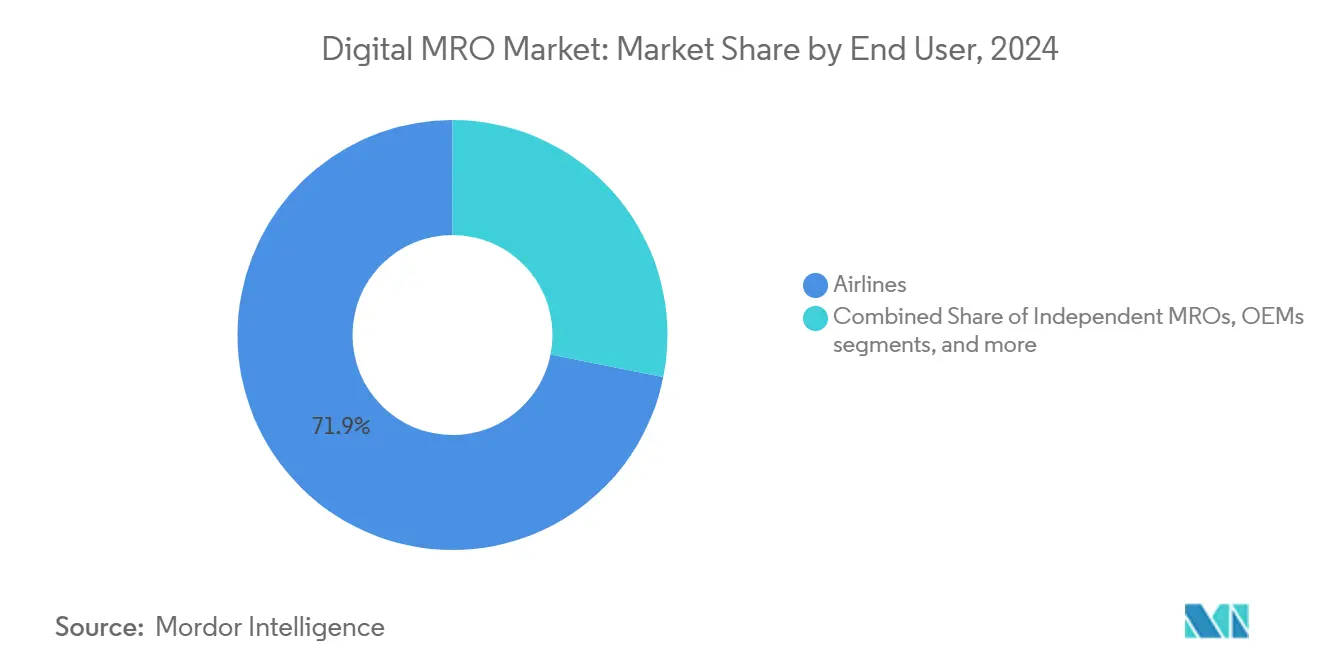

- By end user, airlines held a 71.87% share of the digital MRO market in 2024, while aircraft lessors show the highest projected CAGR at 15.45% between 2025 and 2030.

- By geography, North America commanded a 34.80% share in 2024, while Asia-Pacific advanced at a 16.76% CAGR through 2030.

Global Digital MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption of predictive maintenance solutions | +2.8% | Global, North America and Europe | Medium term (2-4 years) |

| Growth of connected aircraft data lake ecosystems | +2.1% | Global, led by Airbus Skywise | Long term (≥ 4 years) |

| OEM-led initiatives to digitize aftermarket operations | +1.9% | Global aerospace hubs | Medium term (2-4 years) |

| Deployment of mobile XR-enabled maintenance workstations | +1.6% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Leasing-sector adoption of digital twin models for asset remarketing | +1.4% | Global leasing centers | Medium term (2-4 years) |

| Integration of real-time carbon tracking tools for ESG compliance audits | +1.2% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Predictive Maintenance Solutions

Rolls-Royce’s IntelligentEngine program streams data from more than 25,000 sensors per engine, allowing operators to cut unscheduled events by up to 30% and redeploy aircraft faster. Airlines now run terabytes of flight data through machine-learning models that flag subtle degradations long before traditional inspections. Inventory planners order parts only when algorithms predict an imminent need, trimming excess stock and freeing working capital. Early adopters report higher block-hour utilization that flows straight to profitability, particularly on high-frequency narrow-body fleets. As predictive accuracy improves, insurers consider lower maintenance-related premiums, creating another financial incentive. The digital MRO market benefits because each successful case drives peer airlines to accelerate similar deployments to remain cost-competitive.

Growth of Connected Aircraft Data Lake Ecosystems

Airbus Skywise aggregates operational data from 11,000 aircraft and 180 operators, enabling cross-fleet learning that individual airlines could not replicate alone.[1]Airbus, “Skywise,” airbus.com Smaller carriers gain predictive insights from larger peers, shortening their learning curves. Delta Air Lines used the ecosystem to refine maintenance schedules and save USD 6 million in 2024 through reduced component failures. Yet participation hinges on trust: operators fear losing competitive advantage if proprietary operating profiles become visible to rivals. Governance frameworks that anonymize data while preserving analytic value remain a linchpin for further ecosystem expansion. As data-lake maturity grows, suppliers integrate weather, flight profile, and supply chain signals to improve parts-availability forecasts, strengthening the digital MRO market’s network effects.

OEM-Led Initiatives to Digitize Aftermarket Operations

GE Aerospace earmarked USD 1 billion for global MRO upgrades, including AI-guided borescope inspections and blockchain-verified parts tracking. Boeing’s service suite bundles Airplane Health Management with electronic flight-bag apps, giving airlines a turn-key route to digital maintenance and flight-operations alignment. These programs shift OEM revenues toward subscription-like service contracts that smooth earnings and deepen customer lock-in. Independent MROs must respond with niche specialization or partnerships that plug their know-how into wider OEM platforms. The resulting consolidation concentrates technical data within OEM ecosystems, accelerating standards adoption and heightening concerns over data sovereignty.

Deployment of Mobile XR-Enabled Maintenance Workstations

Boeing’s ATOM initiative showed 30% faster task completion when technicians accessed holographic instructions via smart glasses instead of paper manuals. Lufthansa Technik’s AR-based training reduced new-hire certification time by 40%. Real-time overlays of wiring diagrams and torque specs cut errors, raising first-time-right rates. XR also captures experienced workers’ knowledge as interactive guides, easing the industry’s retirement-driven skills gap. Network reliability and device ruggedness remain key adoption hurdles, but telecom operators see value in dedicated private-5G hangar networks that guarantee latency and cybersecurity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity vulnerabilities and intellectual property ownership concerns | -2.3% | Global, North America and Europe | Short term (≤ 2 years) |

| High capital investment required for legacy system digitization | -1.8% | Global, smaller operators | Medium term (2-4 years) |

| Shortage of skilled, data-proficient maintenance technicians | -1.5% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Data sovereignty conflicts between airlines and OEMs | -1.1% | Global with regional regulation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Vulnerabilities and Intellectual-Property Ownership Concerns

The EU Part-IS rule obliges every aviation entity to implement ISO 27001-aligned processes, imposing new audit and encryption costs. Airlines demand clear contractual terms on data ownership before integrating with OEM clouds, yet OEMs rely on aggregated fleet insights for product development. Fear of ransomware targeting maintenance software discourages smaller operators from moving critical functions offline. US Federal Aviation Administration proposals would require tamper-resistant partitions between safety-critical and business networks on transport aircraft.[2]Federal Aviation Administration, “Equipment, Systems, and Network Information Security Protection,” federalregister.gov Compliance expenses delay or scale down digital MRO projects, especially in regions with thin profit margins.

High Capital Investment Required for Legacy System Digitization

Retro-fitting sensors to aging wide-bodies can exceed USD 1 million per aircraft, an outlay many low-cost carriers judge unrecoverable before retirement. Mixed-fleet operators juggle multiple OEM portals with divergent data schemas, forcing pricey middleware to normalize feeds. Independent MRO shops must procure AI tools and train staff while margins hover in single digits, spurring consolidation as well-funded peers buy distressed facilities. Finance-leasing structures sometimes restrict liened aircraft modifications, adding yet another barrier. As a result, digital MRO market penetration lags in regions dominated by older aircraft despite proven efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Digital Twin Dominance Drives Innovation

Digital twins held 21.89% of the digital MRO market share in 2024, and their segment is set to grow at a 17.65% CAGR, adding more than USD 600 million to the digital MRO market size by 2030. Airlines model entire airframes and engines to simulate stress loads and fuel-burn impacts, converting these insights into optimized work-scope packages. AI and big-data analytics follow closely, parsing billions of sensor points to refine twin accuracy and generate failure probabilities. AR/VR overlays translate model outputs into step-by-step guidance, while IoT networks stream live inputs that continuously update the virtual replica. Blockchain secures part pedigrees inside the twin, mitigating counterfeit risk. 3D-printed spares shorten lead times for low-volume components, further reinforcing the twin ecosystem. These tools create a self-learning loop that pushes the digital MRO market toward autonomous maintenance scheduling.

Second-tier technologies expand addressable use cases. AI-enabled image recognition accelerates composite fuselage inspections; predictive supply-chain algorithms flag at-risk inventory and auto-launch purchase orders. Cyber-resilient edge devices mirror critical data within aircraft to maintain diagnostics when connectivity falters. Vendors bundle these capabilities to differentiate platforms, turning individual technologies into interlocking value propositions.

By Application: Predictive Analysis Transforms Traditional Practices

Inspection and damage assessment remained the largest slice at 24.76% in 2024, yet predictive analysis is on track for a 16.57% CAGR, lifting its contribution to the digital MRO market size through 2030. Performance-monitoring dashboards provide real-time system health views that empower dispatchers to reroute aircraft before faults ground them. Remote-assistance apps let engineers share live video with OEM experts, cutting troubleshooting time. Digital documentation modules auto-log task completion for regulatory audits, driving near-paperless hangar floors. Inventory systems tie into predictive engines to balance stock levels against failure probabilities, freeing warehouse space. Mobility features deliver all these functions to tablets and wearables, letting technicians update work cards in situ. As each function feeds data back into the predictive core, applications converge, locking users into comprehensive suites and powering continued digital MRO market growth.

By End User: Aircraft Lessors Drive Dynamic Growth

Airlines own 71.87% of the current user base, but lessors post the fastest 15.45% CAGR, magnifying their influence over digital MRO market adoption. Twin-supported remarketing reports detail component health and projected maintenance reserves, commanding better lease rates. Independent MROs pursue tailored analytics to defend niche work scopes against OEM encroachment. OEMs blur lines between manufacturing and services, bundling health monitoring with power-by-the-hour deals. Military operators require air-gapped architectures and sovereign data hubs, prompting specialized secure-cloud offerings. These varied user needs collectively spur providers to design modular platforms adaptable to vastly different governance and performance criteria.

Geography Analysis

North America retained 34.80% digital MRO market share in 2024, underpinned by large fleets, mature IT infrastructure, and supportive regulatory initiatives such as forthcoming FAA cybersecurity rules. Delta Air Lines leveraged Skywise analytics to save USD 6 million in maintenance costs, setting a benchmark for peers. Canada contributes via Bombardier’s digital service packages, while Mexico grows as a near-shore MRO hub, supplying US airlines seeking cost efficiencies.

Europe EASA Part-IS will create a harmonized security baseline that accelerates platform rollout.[3]European Union Aviation Safety Agency, “EASA Published Updated Easy Access Rules for Information Security,” easa.europa.eu GE Aerospace’s USD 130 million facility upgrades in Poland and Hungary add AI tools that cut engine turnaround times by 20%. France anchors R&D through Airbus headquarters, while Germany funds hydrogen-ready maintenance research aligning digital twins with alternative-fuel performance modeling.

Asia-Pacific advances at 16.76% CAGR, outpacing all regions. China’s COMAC program spurs domestic supply-chain digitization, and India’s government-backed DigiYatra initiative feeds aviation-sector IT expertise into maintenance applications. Japan pilots robotics-assisted inspections that link to digital twins, and Australia integrates satellite connectivity for remote-based fleet maintenance. Diverse fleet ages and rapid traffic growth create fertile conditions for leapfrogging legacy workflows and embedding digital MRO market practices from day one.

Competitive Landscape

The digital MRO market remains moderately fragmented as no vendor exceeds a 25% revenue share. The Boeing Company, Airbus, and GE Aerospace exploit installed-base data privileges to market vertically integrated platforms. GE Aerospace’s AI-enhanced borescope reduced inspection time for LEAP engines by 50%, bolstering customer retention.

SITA and IBM position themselves as neutral data orchestrators across mixed fleets, emphasizing interoperability. Oracle targets parts logistics optimization through blockchain modules. Start-ups focus on carbon accounting and mobile XR; many will likely become acquisition targets as incumbents seek specialized capabilities. White-label platform partnerships emerge, enabling smaller MROs to deploy branded digital services without heavy R&D spend. The race now centers on end-to-end workflow coverage and proven ROI rather than isolated feature rollouts.

Digital MRO Industry Leaders

The Boeing Company

Lufthansa Technik AG

Airbus

Honeywell International Inc.

GE Aerospace (General Electric Company)

Airbus SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE Aerospace and Lufthansa Technik AG established XEOS, a maintenance facility in Poland, focusing on CFM LEAP‑1A and ‑1B engine repair and overhaul. The facility enhances regional maintenance capabilities through lean operations, training programs, and expanded test infrastructure.

- February 2025: GE Aerospace deployed an AI-enabled inspection tool to enhance accuracy and consistency in examining narrowbody aircraft engine components, reducing maintenance time and supporting increased air travel demand.

Global Digital MRO Market Report Scope

| Digital Twin |

| Augmented Reality/ Virtual Reality (AR/VR) |

| 3D Printing |

| Internet of Things (IoT) |

| Artificial Intelligence (AI) and Big-Data Analytics |

| Blockchain |

| Inspection and Damage Assessment |

| Performance Monitoring |

| Predictive Analysis |

| Inventory and Part Replacement |

| Mobility and Functionality |

| Training and Remote Assistance |

| Documentation and Compliance |

| Airlines |

| Independent MROs |

| OEMs |

| Aircraft Lessors |

| Military and Defence Operators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Technology | Digital Twin | ||

| Augmented Reality/ Virtual Reality (AR/VR) | |||

| 3D Printing | |||

| Internet of Things (IoT) | |||

| Artificial Intelligence (AI) and Big-Data Analytics | |||

| Blockchain | |||

| By Application | Inspection and Damage Assessment | ||

| Performance Monitoring | |||

| Predictive Analysis | |||

| Inventory and Part Replacement | |||

| Mobility and Functionality | |||

| Training and Remote Assistance | |||

| Documentation and Compliance | |||

| By End User | Airlines | ||

| Independent MROs | |||

| OEMs | |||

| Aircraft Lessors | |||

| Military and Defence Operators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the digital MRO market expected to grow through 2030?

It is projected to advance at a 14.37% CAGR, rising from USD 1.17 billion in 2025 to USD 2.29 billion by 2030.

Which technology currently holds the largest share of digital maintenance spending?

Digital twin solutions lead with 21.89% share in 2024, thanks to their predictive-maintenance value.

Why are aircraft lessors investing heavily in digital MRO tools?

Digital twins improve asset-remarketing efficiency and boost residual values, supporting the segment’s 15.45% CAGR.

What is the biggest regional opportunity for digital MRO vendors?

Asia-Pacific, forecasted to expand at 16.76% CAGR, offers the fastest fleet growth and supportive digitization policies.

How are security regulations shaping digital MRO adoption?

EU Part-IS and proposed FAA rules mandate robust cyber safeguards, increasing compliance costs but standardizing best practices.

Which recent innovation cuts engine inspection times in half?

GE Aerospace and Waygate Technologies’ AI-enhanced borescope, launched in November 2024, reduces borescope task duration by 50%.

Page last updated on: