Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

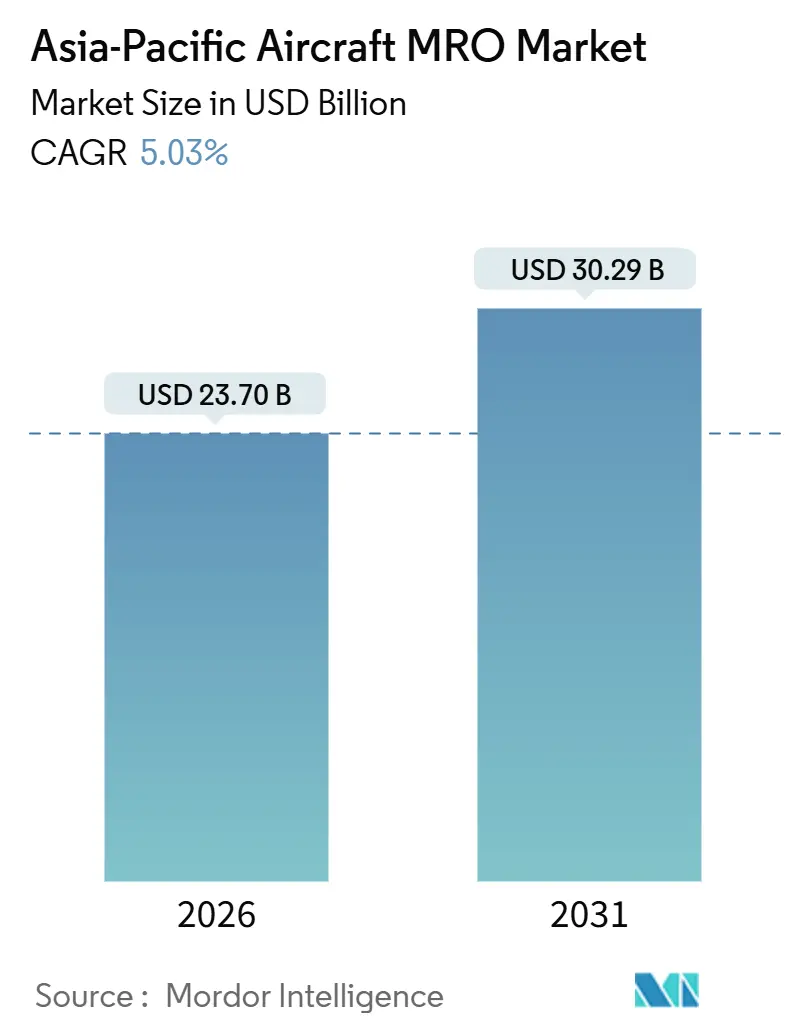

| Market Size (2026) | USD 23.70 Billion |

| Market Size (2031) | USD 30.29 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Aircraft MRO Market Analysis by Mordor Intelligence

The Asia-Pacific aircraft MRO market was valued at USD 23.70 billion in 2026 and is expected to reach USD 30.29 billion by 2031, growing at a CAGR of 5.03%. Key factors driving this growth include increased deliveries of single-aisle aircraft, maintenance demands for aging in-service fleets, and extended engine shop visits associated with the Pratt & Whitney GTF recall. OEM-airline joint ventures are altering the competitive landscape by redirecting high-margin work from independent providers. However, the market faces challenges, including a 15-20% rise in labor, parts, and logistics costs, as well as shortages of titanium and semiconductors, which are impacting profit margins. Facilities capable of ensuring turnaround times are commanding a higher price premium. Additionally, sustainability regulations, such as Singapore’s 1% SAF blend requirement starting in 2026, are driving demand for retrofit packages that combine fuel-system checks with cabin reconfigurations, boosting the modifications sub-segment. Independent providers are responding by expanding predictive-maintenance platforms, which can reduce unscheduled events by up to 30%. This shift in focus is moving the competitive landscape from labor-cost advantages to data-driven availability solutions.

Key Report Takeaways

- Engine MRO accounted for 43.24% of the Asia-Pacific aircraft MRO market share in 2025, while the modifications and upgrades segment is projected to grow at the fastest rate, with a CAGR of 7.59% through 2031.

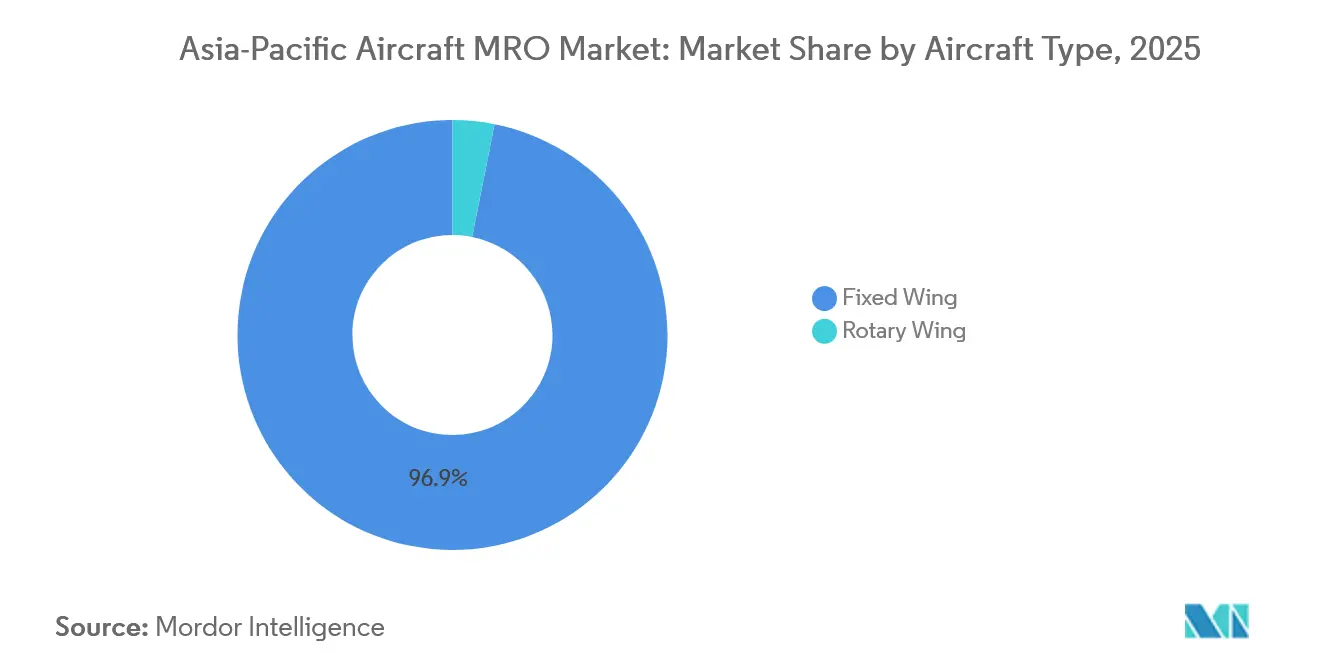

- Fixed-wing aircraft represented 96.87% of the spending in 2025; however, rotary-wing maintenance is expected to grow at a CAGR of 6.01%, driven by increased utilization of offshore and EMS helicopters.

- Passenger aircraft contributed 57.89% of the market value in 2025, while maintenance for cargo and freighter aircraft is anticipated to grow at a CAGR of 6.7%, supported by the expansion of e-commerce logistics.

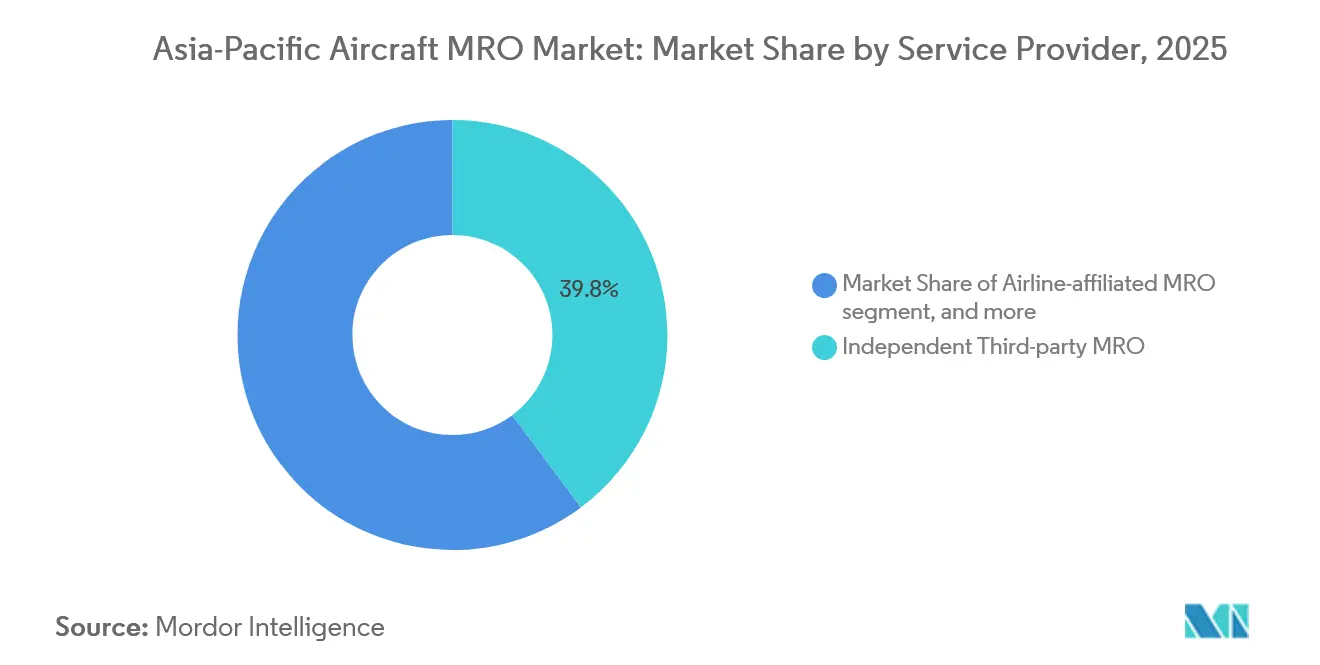

- Independent third-party providers held 39.8% of the revenue share in 2025 and are forecast to grow at a CAGR of 5.4%, surpassing the growth rates of airline-affiliated shops and OEM-captive providers.

- China dominated the Asia-Pacific aircraft MRO market with a 33.51% share in 2025, while India is the fastest-growing market, with a projected CAGR of 7.9%, driven by record fleet orders and supportive policy incentives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Aircraft MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet expansion of narrow-body and LCC fleets | +1.80% | Asia-Pacific core, strongest in India, Southeast Asia, China | Medium term (2–4 years) |

| Aging aircraft creating heavy-check backlog | +1.10% | Global, acute in Australia, Japan, mature Asia-Pacific markets | Short term (≤ 2 years) |

| OEM-airline JVs accelerating aftermarket capture | +0.90% | China, India, Thailand; spill-over to Southeast Asia | Long term (≥ 4 years) |

| Sustainability retrofits and SAF-ready conversions | +0.50% | Singapore, Japan, China; regulatory-driven adoption | Medium term (2–4 years) |

| AI-driven predictive maintenance and digital twins | +0.60% | Singapore, India, China; early adopters in premium carriers | Medium term (2–4 years) |

| On-shoring to hedge supply-chain/geopolitical risk | +0.40% | China, India; spill-over to Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fleet Expansion of Narrow-Body and LCC Fleets Drives Baseline Demand

Airbus projects 19,500 aircraft deliveries to Asia-Pacific operators between 2024 and 2043, with 75% being single-aisle jets. These aircraft typically perform 10-12 flights daily, leading to compressed maintenance intervals. IndiGo’s fleet, currently at 350 aircraft, is expected to exceed 500 aircraft by 2027. By 2027-28, IndiGo plans to add 12 bays at Bangalore Airport for MRO, aiming to triple its total available simultaneous aircraft MRO bays. Despite this expansion, the airline will remain dependent on MRO capacities outside India for another decade, until its new facility becomes fully operational.

Similar capacity constraints are observed with VietJet, AirAsia, and Cebu Pacific, which keep line-maintenance slots limited and favor providers with EASA Part-145 approvals. Meanwhile, China Eastern’s new twelve-widebody mega-hangar in Shanghai highlights efforts to expand infrastructure and shift maintenance work to lower-cost domestic bases. These developments contribute to sustained baseline growth in the Asia-Pacific aircraft MRO market, further supported by delivery delays that extend the service life of older jets.

Aging Aircraft Creating Heavy-Check Backlog Elevates Demand

Delays in aircraft deliveries from Boeing and Airbus are expected to increase the average fleet age in the Asia-Pacific region to 11.4 years by 2026. This aging fleet will require more frequent D-checks, costing USD 3-5 million each and consuming up to 50,000 labor hours. Qantas has reported unscheduled corrosion repairs that sidelined 737-800s for six weeks, reflecting a broader backlog affecting maintenance facilities in Bangkok, Kuala Lumpur, and Jakarta. ST Engineering’s airframe slots in Singapore are fully booked until mid-2027, with overflow routed to Jinan. Providers are prioritizing higher-margin engine work, leaving a gap in heavy-check capacity. Additionally, landing-gear overhauls face 18-month queues due to the limited number of authorized stations in the region, driving premium pricing for incumbents.[1]Qantas, “Annual Report 2024,” qantas.com Mandatory inspections under CAAC CCAR-145 and JCAB regulations ensure continued demand for structural maintenance in the Asia-Pacific aircraft MRO market.

OEM-Airline Joint Ventures Redefine Aftermarket Capture

Joint ventures between OEMs and airlines are reshaping the aftermarket landscape. Examples include Rolls-Royce and Air China’s USD 315 million overhaul facility in Beijing, Airbus-Thai Airways’ component venture in Bangkok, and GE’s expanded engine cell in Singapore. These partnerships aim to secure lifecycle margins traditionally captured by independent providers. Total-care contracts offer airlines predictable costs while limiting third-party access to maintenance work. Safran’s ventures in Suzhou and Xian integrate proprietary repairs within joint-venture frameworks, adhering to ITAR restrictions. Independent providers are responding by scaling predictive analytics, as seen with Lufthansa Technik’s AVIATAR platform, which reduces AOG events by 25%. The Asia-Pacific aircraft MRO market is evolving into a hybrid structure, with OEM-captive facilities focusing on new-technology engines and independent specialists catering to legacy fleets.

AI-Driven Predictive Maintenance and Digital Twins

Air India’s USD 200 million agreement with GE Digital aims to reduce unscheduled maintenance events by 30% through the use of sensor analytics and digital twins. Singapore Airlines is deploying digital twins for its A350 and 787 fleets to extend engine time-on-wing and defer costly shop visits. Lufthansa Technik and ST Engineering report 20-40% reductions in diagnostic time using AI to identify failure precursors, allowing technicians to focus on revenue-generating tasks.[2]ST Engineering, “Investor Presentation 2025,” stengg.com However, smaller maintenance providers in Southeast Asia lack the capital to adopt such technologies, widening the competitive gap in turnaround guarantees. As OEM health-monitoring platforms remain exclusive to in-network facilities, digital adoption is further polarizing the Asia-Pacific aircraft MRO market, creating clear distinctions between leaders and laggards.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Licensed-technician talent crunch | -1.00% | Global, acute in China, India, Southeast Asia | Long term (≥ 4 years) |

| Global parts and materials shortages | -0.70% | Global, severe in component and engine segments | Medium term (2–4 years) |

| GTF and LEAP reliability issues stretch TATs | -0.50% | India, Southeast Asia; spill-over to China, Australia | Short term (≤ 2 years) |

| Inflation and FX volatility pressuring costs | -0.60% | Japan, India, Southeast Asia; currency-dependent markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Licensed-Technician Talent Crunch Constrains Capacity Expansion

IATA estimates that the Asia-Pacific region will require 189,000 licensed technicians by 2032, but is projected to produce only 127,000, resulting in a 33% shortfall. China alone will need 121,900 additional technicians, while India requires 45,000 by 2027. However, DGCA-approved schools in India graduate fewer than 2,000 engineers annually. Salaries in Manila and Bangkok have risen by 8-12% annually as Gulf carriers attract experienced staff with 30-40% higher tax-free pay, squeezing MRO margins tied to fixed-price contracts. Automation helps Air India reduce manual inspection hours by 25%, but the high capital investment required sidelines smaller providers. Certification timelines under EASA Part-66 and FAA Part 65 remain rigid, limiting the ability to address labor shortages despite physical hangar expansions, thereby constraining the growth of the Asia-Pacific aircraft MRO market.

GTF and LEAP Reliability Issues Stretch Turnaround Times

Pratt & Whitney has identified powder-metal contamination in 1,400 GTF engines, doubling shop visit durations to 250-300 days and grounding over 70 IndiGo jets. This has forced IndiGo to lease replacement aircraft at rates 40% higher than those in 2019.[3]Pratt & Whitney, “GTF Fleet Update 2024,” pratt-whitney.com Go First’s collapse, attributed to similar grounding incidents, underscores the financial risks associated with idle assets. CFM LEAP engine parts shortages have extended maintenance durations by 30-50 days, pushing engine shop utilization to 95-100% across facilities in Singapore, Zhuhai, and Hyderabad. While ST Engineering is expanding GTF capacity, Pratt & Whitney does not anticipate full resolution until late 2026. These prolonged turnaround times and increased spare-engine leasing costs are expected to continue restraining schedules, profitability, and overall growth in the Asia-Pacific aircraft MRO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By MRO Type: Engine Overhauls Anchor Revenue, Modifications Accelerate

Engine services accounted for 43.24% of the 2025 market value, driven by USD 3-5 million shop visits and the intensive OEM tooling requirements that few independent providers can meet. Prolonged GTF and LEAP engine events have increased parts consumption, pushing segment revenues higher despite reduced throughput. Consequently, the Asia-Pacific aircraft MRO engine market is growing faster than flight hours, underscoring the need for additional test cells in locations such as Singapore and Zhuhai.

Modifications and upgrades represent the fastest-growing segment, with a 7.59% CAGR, as airlines retrofit cabins, install winglets, and certify systems for 1-5% SAF blends under CAAS regulations. Airlines often combine these projects with heavy maintenance checks to optimize downtime, generating incremental revenue of approximately USD 1 million per aircraft. ST Engineering reported a 40% increase in retrofit inquiries in 2025, reflecting demand from operators seeking immediate fuel-efficiency improvements. This trend positions modifications as a strategic buffer for providers against fluctuations in airframe maintenance workloads within the Asia-Pacific aircraft MRO market.

By Aircraft Type: Fixed-Wing Dominance Masks Rotary-Wing Acceleration

Fixed-wing aircraft accounted for 96.87% of 2025 expenditures, led by A320 and 737 families, which log 3,500-4,500 flight hours annually and require A-checks every 500-750 hours. Widebody D-checks, which can cost up to USD 7 million and require 60,000 labor hours, have made Singapore, Hong Kong, and Shanghai critical hubs. The Asia-Pacific aircraft MRO market for fixed-wing services remains stable, driven by mandated inspections, despite fluctuations in traffic.

Helicopter maintenance, which accounts for only 3.13% of spending, is growing at an annual rate of 6.01%. This growth is driven by offshore energy, EMS, and tourism operators in Australia, Indonesia, and Thailand, who are refreshing AW139, H225, and Bell 412 fleets. Extended lead times of 12-18 months for dynamic components, combined with limited authorized repair shops, have created pricing power for providers. Expanding rotary-wing maintenance capabilities allows providers to diversify revenue streams and mitigate seasonal demand fluctuations in the Asia-Pacific aircraft MRO market.

By Application: Passenger Segment Leads, Cargo Surges on E-Commerce Logistics

Passenger operations contributed 57.89% of the 2025 market value, as full-service carriers operate complex wide-body fleets and low-cost carriers (LCCs) drive high-cycle, narrow-body utilization. IndiGo, for instance, conducts over 1,000 line-maintenance events daily, highlighting the revenue model driven by frequency. Consequently, the Asia-Pacific aircraft MRO market is closely tied to passenger operations, scaling in line with both flight hours and cycles.

Cargo and freighter maintenance is expanding at a 6.7% annual growth rate, fueled by operators such as SF Airlines, Cainiao, and DHL, whose intra-Asia networks rely on dependable 737BCF and 757F fleets. Passenger-to-freighter conversions, costing USD 6-8 million, extend the economic life of aircraft by 15-20 years, keeping ST Engineering’s conversion lines fully booked through 2027. This trend has increased demand for structural modifications and cargo door kits, thereby diversifying revenue streams within the Asia-Pacific aircraft MRO market.

By Service Provider: Independent Third-Parties Lead, OEM-Captives Gain

Independent service providers accounted for 39.8% of the 2025 market revenue and are projected to grow at 5.4% annually, benefiting from multi-airline portfolios and geographic reach. ST Engineering’s 2025 acquisition of StandardAero doubled its engine capacity and added business-jet capabilities, underscoring the impact of consolidation. However, the market share of independents faces pressure from OEM vertical integration.

OEM-captive providers and joint ventures are increasingly capturing warranty and long-term care contracts for new-technology engines, diverting work from airline-affiliated shops that face capital-constrained budgets. Investments such as GE’s USD 75 million test-cell upgrade in Singapore and Rolls-Royce’s Beijing joint venture highlight a shift toward OEM dominance. Independent providers are expected to focus on legacy fleets, landing gear, and avionics to remain competitive in the Asia-Pacific aircraft MRO market.

Geography Analysis

China accounted for 33.51% of the Asia-Pacific aircraft MRO market share in 2025, supported by major players such as AMECO, GAMECO, and HAECO, which handle wide-body heavy checks that were previously outsourced to Hong Kong or Singapore. Shanghai’s new twelve-widebody hangar and Hainan’s duty-free zone have reduced logistics costs by up to 20%, aligning with Beijing’s efforts to localize value. Joint ventures such as MTU Maintenance Zhuhai, which focuses on CFM56 and V2500 engines, are operating at 95% capacity, indicating strong demand for additional facilities.

India is the fastest-growing market, with a 7.9% CAGR, driven by fleet expansions from IndiGo and Air India, as well as a reduction in the GST rate on MRO services from 18% to 5%. Air India’s planned USD 500 million mega-facility in Delhi will enable domestic widebody D-checks, while Air Works and Lufthansa Technik are scaling component shops under the “Make in India” initiative. However, challenges such as technician shortages and limited widebody maintenance bays persist. Despite these issues, favorable policies are attracting new investments, boosting India’s contribution to the Asia-Pacific aircraft MRO market.

Japan, South Korea, and Australia maintain mature, high-skill ecosystems. JAL Engineering derived 22% of its 2024 revenue from third-party customers, while Korea Aerospace Industries secured USD 1.2 billion for F-16 upgrades, strengthening its defense workload. Australia’s F-35 sustainment hub at RAAF Williamtown is projected to generate AUD 1.5 billion (USD 1.01 billion) annually by 2028, anchoring high-complexity work in the region. Southeast Asian hubs such as Singapore, Malaysia, and Thailand continue to benefit from competitive labor costs but face challenges with technician attrition to Gulf carriers, prompting investments in training and retention programs.

Competitive Landscape

The top five providers, ST Engineering, Lufthansa Technik, HAECO, SIA Engineering, and AAR, accounted for approximately 38% of the projected 2025 revenue, leaving a significant portion of the market to specialized providers in line maintenance and component repair. ST Engineering’s acquisition of StandardAero and GE’s expansion in Singapore demonstrate ongoing consolidation and increased vertical integration by OEMs. Lufthansa Technik’s AVIATAR platform, now utilized by 300 airlines, reflects a shift toward data-driven services that prioritize availability over cost, altering the pricing dynamics in the Asia-Pacific aircraft MRO market.

Growth opportunities are concentrated in areas such as modifications, component overhauls, and rotary-wing support, where existing capability gaps allow for premium pricing. Safran Landing Systems reported an 18% year-on-year increase in landing-gear overhaul volumes in the Asia-Pacific region. However, with only six authorized stations, lead times have extended to 18 months. Meanwhile, digital-native startups offering parts-procurement algorithms are collaborating with traditional MRO providers, reducing quote cycles from days to hours and attracting venture capital focused on improving operational efficiency.

Capacity expansions in China and India are challenging established hubs in Singapore and Hong Kong, compelling incumbents to differentiate through faster turnaround times, SAF-ready conversions, and substantial regulatory compliance. Adherence to ISO 9001 and EASA Part-145 standards remains essential for cross-border operations, with recent audits in India and China highlighting regulatory efforts to oversee the growing number of new facilities. As a result, competition in the Asia-Pacific aircraft MRO market is shifting from labor-cost advantages to proprietary data, OEM collaborations, and comprehensive lifecycle service offerings.

Asia-Pacific Aircraft MRO Industry Leaders

Singapore Technologies Engineering Ltd.

Lufthansa Technik AG

Hong Kong Aircraft Engineering Company Limited

SIA Engineering Company

AAR CORP.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ST Engineering finalized the USD 1.1 billion acquisition of StandardAero's engine MRO business, effectively doubling its engine overhaul capacity. This acquisition expanded its capabilities to include Pratt & Whitney PT6 turboprops and Rolls-Royce BR725 business-jet engines, enabling the company to cater to both commercial and general aviation markets in the Asia-Pacific region. The full press release from ST Engineering is available for reference.

- September 2025: GE Aerospace has announced an investment of USD 75 million in its Maintenance, Repair, and Overhaul (MRO) and component repair facilities across the Asia-Pacific (APAC) region, with completion expected by the end of 2025. This announcement was made during the event “Advancing MRO for a Resilient Aerospace Industry in Asia-Pacific,” hosted in Singapore by The Business Times. The investment is part of the company’s global, multi-year USD 1 billion MRO spending plan, initially announced in 2024. The initiative aims to enhance the capacity of MRO facilities in APAC’s expanding aviation market to meet the increasing demand for services across the GE Aerospace and CFM installed base, building on a USD 45 million investment made in the previous year.

Asia-Pacific Aircraft MRO Market Report Scope

Aircraft maintenance, repair, and overhaul (MRO) is the process of inspecting, servicing, or restoring airframes, engines, systems, and components to keep aircraft compliant with Asia-Pacific safety and airworthiness standards. The study of the aircraft MRO market encompasses all scheduled and unscheduled line checks, heavy airframe visits, engine shop work, component repairs, and modification programs performed on fixed-wing and rotary-wing platforms across commercial, military, and general aviation fleets operating in the region. Component-level tasks, such as avionics calibration, landing gear overhauls, and cabin retrofits, are included within the market scope.

The Asia-Pacific aircraft MRO market is segmented by MRO type, aircraft type, application, service provider, and geography. By MRO type, the market is segmented into engine, airframe heavy maintenance, component, line and routine checks, and modifications and upgrades. By aircraft type, the market is segmented into fixed-wing and rotary-wing aircraft. By application, the market is segmented into commercial aviation (passenger and cargo/freighter), military aviation, and general aviation. Service providers segment the market into airline-affiliated MRO, independent third-party MRO, OEM-captive MRO, and military depots. By geography, the market is segmented into China, India, Japan, South Korea, and the rest of Asia-Pacific. Market sizing and forecasts are presented in value terms (USD billion) for every segment and sub-segment listed above.

By MRO Type

| Engine |

| Airframe Heavy Maintenance |

| Component |

| Line and Routine Checks |

| Modifications and Upgrades |

By Aircraft Type

| Fixed Wing |

| Rotary Wing |

By Application

| Commercial Aviation | Passenger |

| Cargo/Freighter | |

| Military Aviation | |

| General Aviation |

By Service Provider

| Airline-affiliated MRO |

| Independent Third-party MRO |

| OEM-Captive MRO |

| Military Depots |

By Country

| China |

| India |

| South Korea |

| Japan |

| Singapore |

| Malaysia |

| Indonesia |

| Rest of Asia-Pacific |

| By MRO Type | Engine | |

| Airframe Heavy Maintenance | ||

| Component | ||

| Line and Routine Checks | ||

| Modifications and Upgrades | ||

| By Aircraft Type | Fixed Wing | |

| Rotary Wing | ||

| By Application | Commercial Aviation | Passenger |

| Cargo/Freighter | ||

| Military Aviation | ||

| General Aviation | ||

| By Service Provider | Airline-affiliated MRO | |

| Independent Third-party MRO | ||

| OEM-Captive MRO | ||

| Military Depots | ||

| By Country | China | |

| India | ||

| South Korea | ||

| Japan | ||

| Singapore | ||

| Malaysia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How big is the Asia-Pacific aircraft MRO market in 2026?

The Asia-Pacific aircraft MRO market size reached USD 23.70 billion in 2026 and is on track for USD 30.29 billion by 2031.

Which MRO segment dominates spending?

Engine services dominate, holding 43.24% of 2025 value owing to capital-intensive overhauls and longer shop visits during the GTF recall.

Why is India the fastest-growing geography?

Fleet orders from IndiGo and Air India, GST cuts from 18% to 5%, and a USD 500 million widebody facility near Delhi are propelling a 7.9% CAGR.

What is driving demand for modifications and upgrades?

Airlines are bundling cabin reconfigurations, winglets, and SAF-readiness checks with heavy maintenance, pushing this sub-segment to a 7.59% CAGR.

How are OEMs reshaping the competitive landscape?

OEM-airline joint ventures and captive shops in Beijing, Bangkok, and Singapore secure lifecycle revenue, pressuring independents to specialize.

What talent challenges face Asia-Pacific MROs?

The region will be 33% short of licensed technicians by 2032, pushing wages up 8-12% annually and limiting effective capacity despite new hangars.

Page last updated on: