Digital Map Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 32.79 Billion |

| Market Size (2031) | USD 61.19 Billion |

| Growth Rate (2026 - 2031) | 13.29% CAGR |

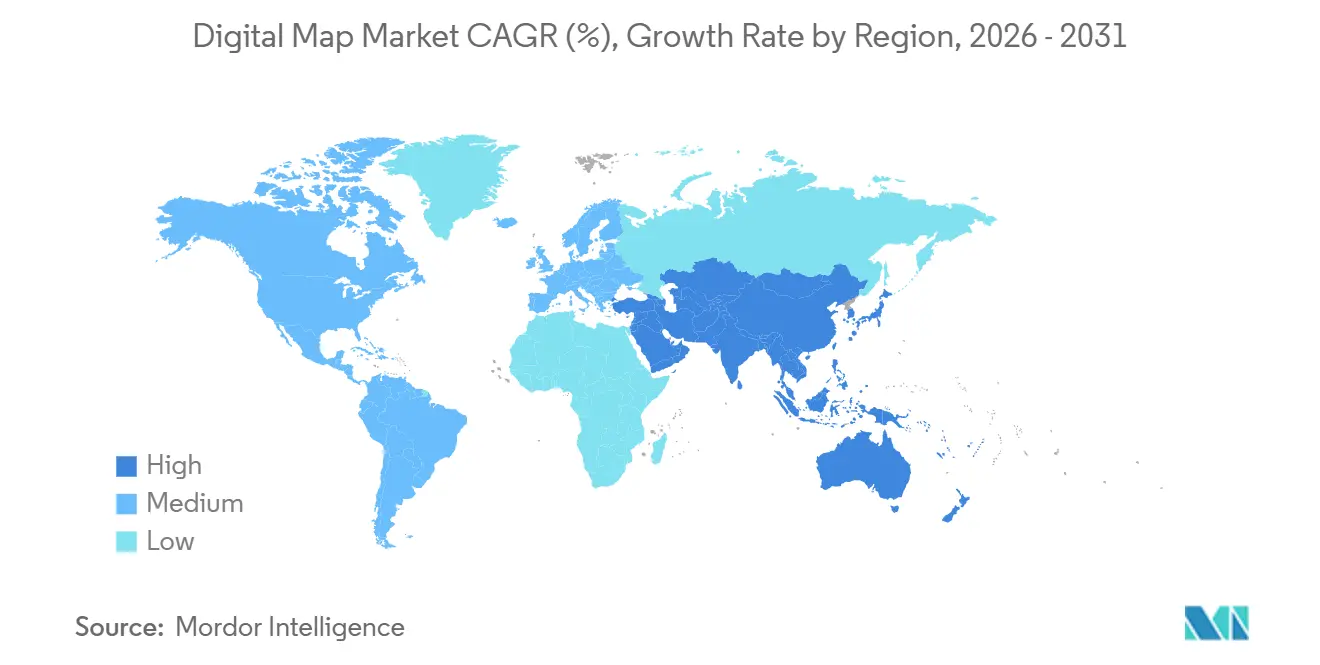

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

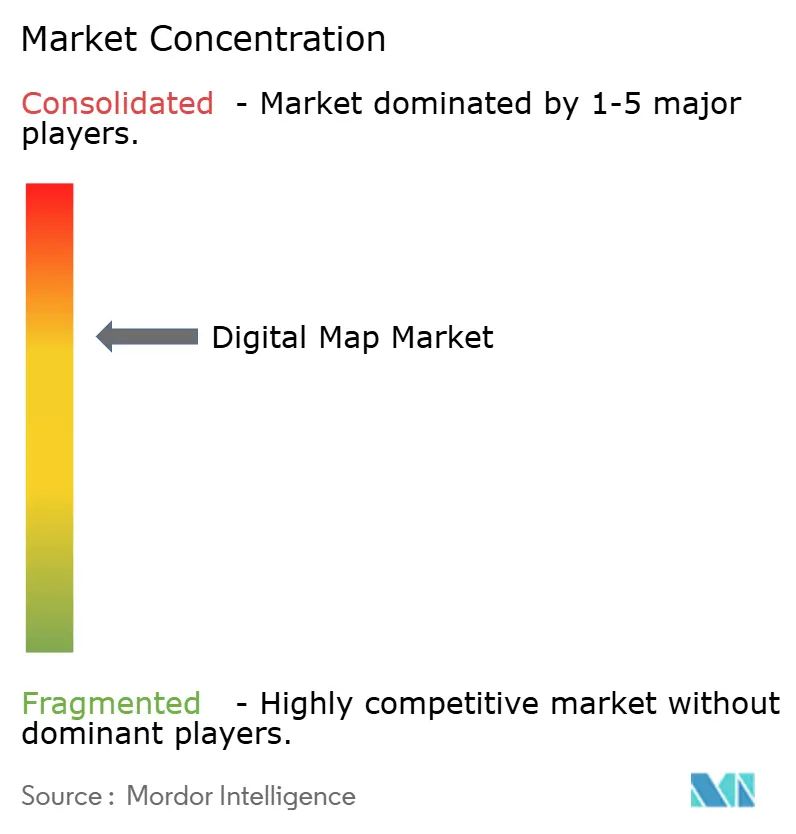

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Map Market Analysis by Mordor Intelligence

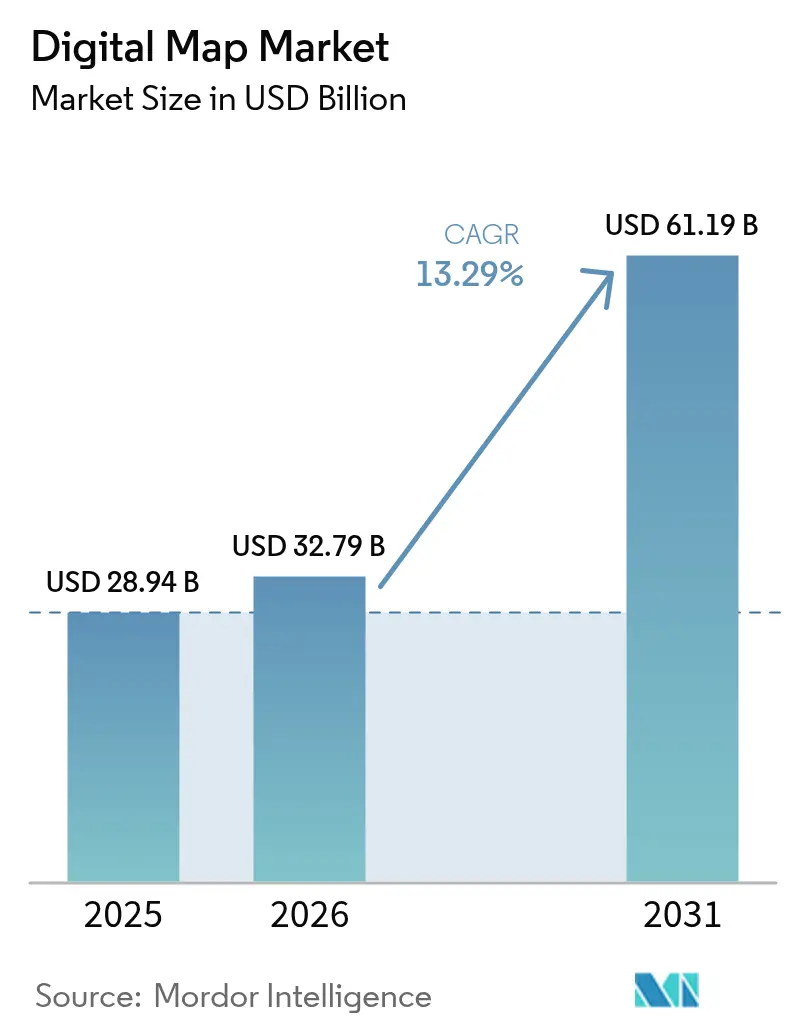

The digital map market size is projected to be USD 28.94 billion in 2025, USD 32.79 billion in 2026, and reach USD 61.19 billion by 2031, growing at a CAGR of 13.29% from 2026 to 2031. Demand is shifting from static cartography toward dynamic, sensor-fused platforms that feed autonomous driving systems, city-scale digital twins, and corporate carbon-accounting workflows. Software continued to dominate revenue in 2025, but multiyear refresh contracts and cloud-integration projects are steering incremental spending into services. Cloud deployment already captures more than two-thirds of spending and is reinforced by hyperscaler programs that bundle real-time layers into AWS Location Service, Azure Maps, and Google Earth Engine. Automotive remains the largest end-use industry, yet public-sector and defense agencies are scaling geospatial-intelligence modernization at the fastest clip. Competitive intensity is mounting as cloud-native specialists use open standards and modular APIs to undercut traditional perpetual-license models.

Key Report Takeaways

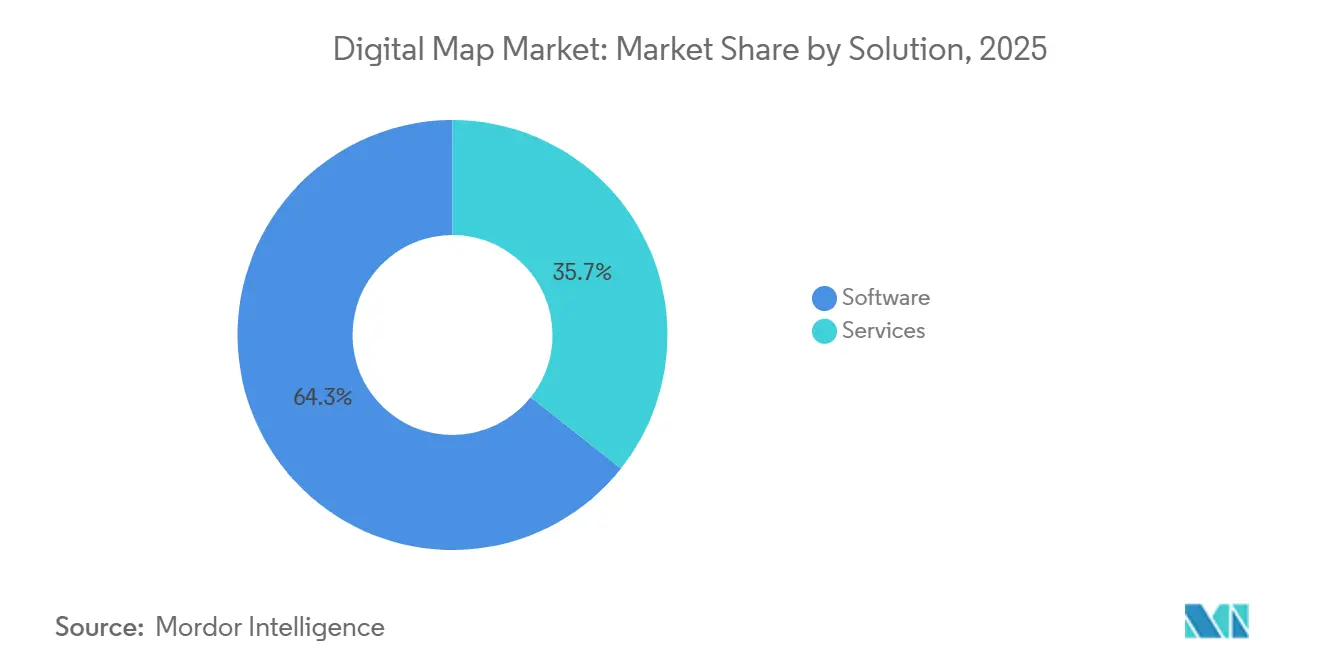

- By solution, software led with 64.33% of 2025 revenue, while services are growing at a 13.71% CAGR through 2031.

- By deployment, cloud held 71.42% of the 2025 digital map market share and is forecast to sustain a 13.66% CAGR to 2031.

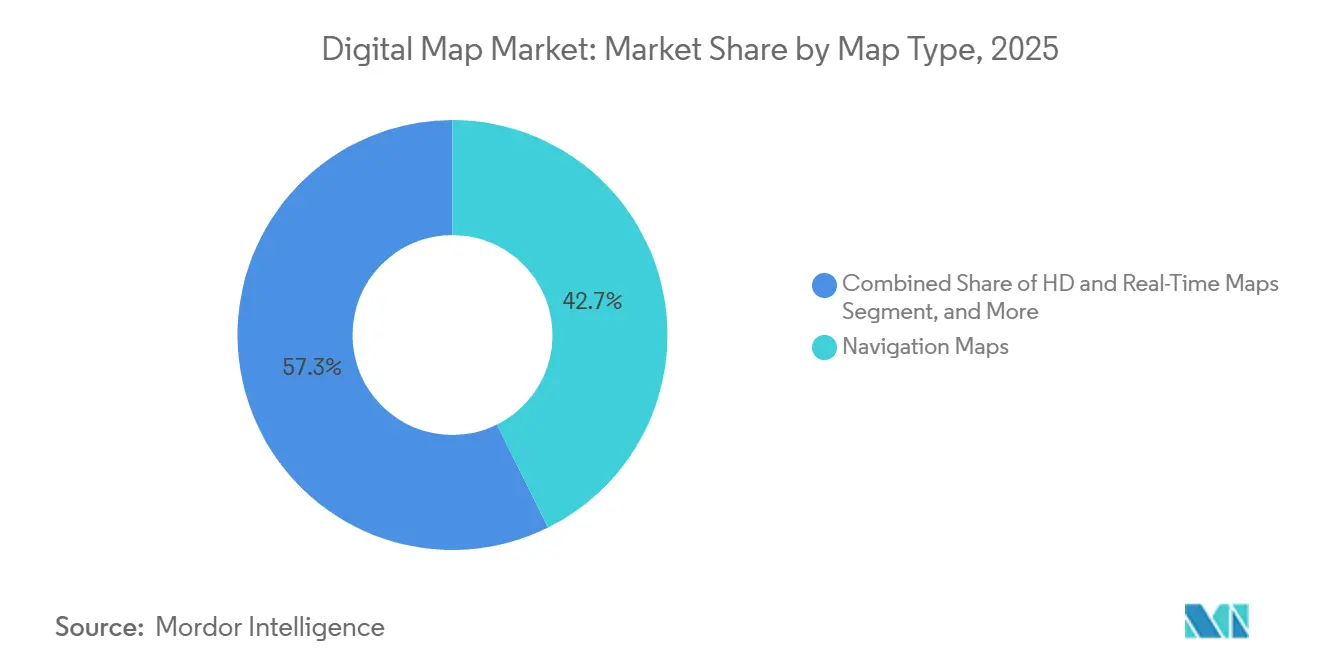

- By map type, navigation maps accounted for 42.67% of 2025 sales, whereas HD and real-time maps are advancing at a 14.07% CAGR to 2031.

- By end-use industry, automotive accounted for 39.17% of the digital map market share in 2025, but the public sector and defense are expanding fastest at a 14.47% CAGR through 2031.

- By geography, North America accounted for 36.83% of 2025 spending, while Asia-Pacific is projected to grow at a 14.24% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Map Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of HD Maps for ADAS and Autonomous Vehicles | +2.8% | Global, concentrated in North America, Europe, and China | Medium term (2-4 years) |

| Explosive Growth of Connected-Car OTA Map-Update Ecosystems | +2.3% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Mainstream Adoption of Cloud-Native GIS Platforms | +2.1% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Smart-City Digital-Twin Programs Scaling Globally | +1.7% | Global, early gains in Singapore, Dubai, Barcelona, and Chinese tier-1 cities | Long term (≥ 4 years) |

| Mandatory EU eCall and Next-Gen Road-Safety Regulations | +1.4% | Europe, with spillover to Middle East and Asia-Pacific | Short term (≤ 2 years) |

| Corporate Scope-3 Carbon Mapping Requirements | +1.2% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of HD Maps for ADAS and Autonomous Vehicles

Automakers rolling out SAE Level 3 and Level 4 features now treat centimeter-grade HD basemaps as non-negotiable safety equipment. Mercedes-Benz activated Drive Pilot in California and Nevada using HERE’s HD Live Map, which fuses sensor data from more than 5 million vehicles to keep lane markings accurate within 10 centimeters. BMW and Volkswagen’s Dynamic Map Platform processes 15 terabytes of probe data each day to refresh a 1.2-million-kilometer European–Japanese network, revealing the high cost of pure LiDAR surveys. A 2025 SAE technical paper showed that overlaying crowd-sourced updates on a static HD layer can trim refresh expense by roughly 40% without losing accuracy.[1]SAE International Editorial Board, “Hybrid HD Mapping Architectures for Autonomous Vehicles,” SAE International, sae.org This hybrid model is steering investment toward providers that pair on-board sensor fusion with cloud analytics rather than rely on periodic drive-outs.

Explosive Growth of Connected-Car OTA Map-Update Ecosystems

Over-the-air delivery has moved from a premium add-on to a regulatory baseline as drivers and safety agencies demand up-to-the-minute road data. Ford pushed 63 million delta-compressed map packages in 2024, cutting cellular payloads 85% and slashing data costs. Stellantis embedded Snapdragon Ride Flex chips so updates run automatically while vehicles charge, eliminating the latency that once delayed critical patches.[2]Qualcomm Newsroom, “Qualcomm and Stellantis Partner to Deliver Next-Generation Software-Defined Vehicles,” Qualcomm, qualcomm.com Tesla ingests 1.5 billion fleet miles each month, refreshing lane geometry without third-party royalties and proving the margin upside of vertical integration. Map vendors unwilling to offer lightweight APIs that integrate seamlessly with diverse telematics stacks risk losing share to OEMs writing their own pipelines.

Mainstream Adoption of Cloud-Native GIS Platforms

Consumption-based cloud GIS is eroding the pricing power of perpetual desktop suites while expanding the total user base. Esri’s ArcGIS Online crossed 15 million seats in 2025 as agencies migrated to pay-as-you-go tiers that scale with data volume.[3]Esri Newsroom, “ArcGIS Online Reaches 15 Million Users,” Esri, esri.com Google Earth Engine added commercial real-time change-detection APIs that let retailers and contractors audit sites without field visits. AWS Location Service now hooks directly into SageMaker, so data scientists can train location-aware models on embedded map layers instead of building custom ETL flows. As hyperscalers commoditize storage and rendering, legacy GIS suppliers must pivot toward vertical analytics and advisory services to defend margins.

Smart-City Digital-Twin Programs Scaling Globally

City planners are promoting pilot twins into full production systems that couple dense sensor grids with authoritative 3D basemaps. Singapore’s Virtual Singapore ingests data from more than 100,000 IoT nodes to simulate flood scenarios and transit flows at 1-meter resolution. Dubai now requires ISO 19650-compliant BIM files for all new construction, feeding its national twin for automated permitting and infrastructure scheduling. Barcelona overlays live air-quality and traffic feeds on its Sentilo platform to test low-emission zones before rollout. Map providers that supply modular, standards-based base layers are best placed to win these multi-vendor municipal contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Costs of Continuous, Centimeter-Level Map Refresh | -1.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Heightened Data-Privacy and Localization Statutes (GDPR, PIPL) | -1.5% | Europe and China, with spillover to Asia-Pacific | Medium term (2-4 years) |

| IP-Licensing Disputes Among Data Providers and OEMs | -1.1% | Global, concentrated in automotive sector | Medium term (2-4 years) |

| Algorithmic Bias and Liability Concerns in AI-Generated Maps | -0.9% | Global, regulatory frameworks emerging in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Costs of Continuous, Centimeter-Level Map Refresh

Sub-10-centimeter accuracy across continental road networks demands heavy LiDAR fleets, aerial imagery, and cloud processing that only global incumbents can afford. HERE’s 200-vehicle LiDAR armada cut gross margin on HD services by 320 basis points when refresh cycles tightened from quarterly to weekly. TomTom trimmed survey cadence in secondary markets and pivoted to satellite change detection, lowering costs 30% but stretching update latency from days to weeks. Smaller challengers rely on dash-cam computer vision yet still struggle to meet Level 4 precision targets. The economics widen incumbents' moats and slow competitive churn.

Heightened Data-Privacy and Localization Statutes (GDPR, PIPL)

New privacy regimes are splintering the global data fabric into regional silos, raising compliance costs and complicating cross-border services. GDPR requires any geospatial trail linked to an identifiable person to remain within EU borders, prompting providers to spin up sovereign clouds in Frankfurt and Amsterdam. China’s 2024 revisions to the Personal Information Protection Law bar the outbound transfer of domestic map data without state sign-off, compelling foreign vendors to enter joint ventures with local players. India’s 2023 Digital Personal Data Protection Act empowers regulators to audit foreign map providers’ handling practices, delaying several market entries by more than a year. These overlapping rules strain smaller specialists that lack capital for duplicate infrastructure and favor incumbents with regional partners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Services Rise on Recurring Refresh Contracts

Software accounted for 64.33% of the digital map market share in 2025, a position built on decades of desktop GIS licenses and embedded navigation stacks. Even so, service revenues, ranging from continuous map-refresh subscriptions to cloud-integration consulting, are forecast to climb at a 13.71% CAGR through 2031, adding the largest slice of the incremental digital map market over the period. Enterprises now favor predictable operating expense models over one-time capital outlays; Trimble’s 2024 purchase of Transporeon, which bundles routing APIs with logistics consulting, produced a 28% year-over-year lift in subscription lines during 1H 2025. Esri and Maxar report the same pattern in municipal digital-twin engagements, where customers insist on outcome-based contracts tied to refresh frequency rather than seat counts.

The tilt toward services is also a talent play. Few enterprises employ in-house geospatial experts, so they outsource data fusion, custom cartography, and API governance to suppliers that can guarantee service-level agreements. Software will remain the larger revenue pool in absolute terms, but licensing growth is decelerating as cloud-native open-source stacks undercut pricing power. Vendors that fail to build substantial consulting and managed-hosting arms risk ceding wallet share to systems integrators or hyperscalers that already command the customer relationship.

By Deployment: Cloud Becomes the Default Geospatial Platform

Cloud installations accounted for 71.42% of 2025 revenue and are projected to maintain a 13.66% CAGR through 2031, reinforcing a cloud-first stance across the digital map market. With AWS Location Service exposing HERE, Esri, and Grab tiles behind a single pay-as-you-go endpoint, enterprises avoid the complexity of multiple negotiations. Microsoft went further in March 2025, embedding Azure Maps inside Power BI so analysts can overlay sales territories without writing code. These moves slash deployment friction and accelerate adoption among non-GIS specialists, driving new chunks of the digital map market size into the cloud column.

On-premises servers persist in defense, critical infrastructure, and heavily regulated utilities where sovereign data or air-gap mandates remain immovable. Esri disclosed at its 2025 user conference that roughly 30% of ArcGIS Enterprise seats still run on customer metal, down from 55% in 2020. As sovereign cloud regions open in Europe, India, and the Middle East, even some of those workloads are expected to migrate. By 2031, analysts see on-premises stabilizing at 20-25% of the digital map market share, anchoring a specialized but profitable niche for vendors able to meet zero-connectivity requirements.

By Map Type: HD and Real-Time Layers Outpace Commodity Navigation

Navigation products retained a 42.67% share of 2025 revenue, yet HD and real-time layers are set to outgrow them at a 14.07% CAGR through 2031, expanding their contribution to the digital map market. Waymo’s sixth-generation driver localizes against 5-centimeter HD tiles to maintain reliability in dense urban cores. General Motors’ Ultra Cruise consumes 2 GB of HD data per driving hour, prompting the automaker to secure redundant feeds to avoid single-vendor risk. These premium requirements place a pricing floor well above standard routing layers.

By contrast, commodity navigation faces a margin squeeze as gig-economy platforms and mid-tier OEMs pivot to open-source alternatives such as OpenStreetMap or government basemaps. Topographic and thematic sets will continue to serve defense, maritime, and environmental monitoring, but track macroeconomic growth rather than the double-digit rates seen in HD. Providers that cannot fund the sensor-fusion pipelines and centimeter-grade refresh cadences demanded by Level 3+ autonomy may be relegated to low-margin consumer navigation or niche thematic verticals.

By End-Use Industry: Public Sector Budgets Accelerate Past Automotive

Automotive generated 39.17% of 2025 sales on the strength of embedded navigation, ADAS, and forthcoming autonomy layers. Yet the public sector and defense segment is projected to be the fastest-growing, advancing at a 14.47% CAGR and absorbing an increasing share of the digital map market. The U.S. Department of Defense awarded Maxar USD 476 million in 2024 for high-resolution 3D terrain, a 40% budget bump over the prior cycle. NGA plans to automate feature extraction so battlefield maps refresh in near real time, driving fresh demand for analytics services.

Commercial verticals are following suit. Engineering and construction firms overlay BIM models with live survey data to trim rework costs by 12% on hundreds of projects. Telecom operators use geospatial AI to fine-tune 5G tower placement, cutting site-acquisition expenses by 18%. Retailers rely on demographic polygons to prioritize store locations and avoid cannibalization, an application that Esri’s Business Analyst now delivers to more than 3,000 chains. Collectively, these non-automotive uses deepen and diversify the revenue base, cushioning suppliers against any slowdown in vehicle sales cycles.

Geography Analysis

North America accounted for 36.83% of 2025 revenue, giving the region the largest share of the digital map market in the base year. Autonomous-vehicle pilots in California and Nevada drive uptake, Tesla’s high-volume fleet telemetry, and robust U.S. defense geospatial budgets. The Federal Communications Commission’s 2024 allocation of Cellular Vehicle-to-Everything spectrum accelerated connected-car deployments and boosted demand for real-time traffic and hazard layers. Canada benefits from Natural Resources Canada's open basemaps, which lower entry barriers for start-ups, while Mexico lags because rural broadband gaps limit cloud GIS adoption. As connected-vehicle penetration nears saturation, regional growth is expected to trail the 13.29% global CAGR, but absolute spending will still expand as defense agencies refresh HD terrain data.

Asia-Pacific is projected to post the fastest 14.24% CAGR through 2031 and will add the largest share of the incremental digital map market over the forecast window. China’s Baidu Maps recorded 650 million monthly active users in Q4 2024 after integrating EV-charger availability and autonomous-taxi routing. India’s Smart Cities Mission requires all 100 designated municipalities to deploy GIS platforms for waste, mobility, and water management, feeding multiyear contracts to MapmyIndia and Esri India. Japan’s Zenrin–Toyota partnership is building HD maps for Level 3 Lexus Teammate, while South Korea earmarked KRW 500 billion (USD 375 million) to digitize its road grid at 10-centimeter resolution ahead of the 2027 Busan World Expo. These programs, combined with rapid 5G rollout, underpin sustained double-digit regional growth.

Europe captured a mid-20s share in 2025, supported by the EU’s eCall mandate and improvements in Galileo satellite accuracy. The Digital Markets Act now obliges Apple and Google to open mapping APIs, a rule that could redirect traffic to regional specialists such as HERE and TomTom. Strict GDPR localization favors vendors with sovereign clouds in Frankfurt and Amsterdam, reinforcing incumbent positions. In the Middle East and Africa, the United Arab Emirates and Saudi Arabia bankroll smart-city twins, yet sub-Saharan African adoption is constrained by limited cadastral databases. South American demand is centered on Brazil and Argentina, where urban logistics platforms need reliable routing, but currency volatility tempers long-horizon infrastructure investment.

Competitive Landscape

Alphabet, HERE Technologies, and TomTom together control an estimated 55-60% of automotive contracts and consumer navigation revenue, giving the sector a moderate concentration profile. Alphabet monetizes Google Maps and Waze through advertising rather than per-vehicle royalties, allowing aggressive pricing that squeezes fee-based rivals. HERE, backed by German OEMs, shifted its focus to HD Live Map and real-time traffic, lifting automotive sales by 18% in 2024 even as consumer navigation slipped by 7%. TomTom exited personal navigation devices in 2025 to focus on B2B APIs, a pivot that stabilized revenue but narrowed gross margins as the firm scaled its cloud infrastructure.

Cloud-native specialists are fragmenting the field. Mapbox uses an OpenStreetMap foundation and vector-tile compression, which cuts bandwidth consumption by 80%, attracting high-traffic customers such as Snap and Meta. CARTO’s spatial SQL engine on BigQuery lets analysts run geospatial queries without desktop GIS, expanding the addressable user pool among retail and logistics clients. Esri invested USD 150 million to add data centers in Singapore, Dubai, and São Paulo, reducing latency for smart-city and utility workloads while deepening its vertical analytics playbook. These moves chip away at incumbent share by lowering switching costs and broadening developer access.

Regulatory compliance has become a key competitive lever. Providers with ISO 27001 certification and sovereign cloud capacity qualify for sensitive contracts in Europe, India, and China, where foreign data hosting can disqualify bids. Partnerships such as TomTom–Microsoft Azure and HERE–Mercedes-Benz combine data residency with centimeter-grade refresh cycles, creating high barriers for late entrants. Meanwhile, intellectual-property disputes are prompting some automakers to internalize mapping stacks, as General Motors did for its Cruise fleet, thereby pressuring third-party royalties. The net result is a market where incumbents defend their share through deep compliance and high-precision assets, while nimble API vendors seize greenfield enterprise workloads.

Digital Map Industry Leaders

Alphabet Inc.

HERE Global B.V.

TomTom International B.V.

Mapbox, Inc.

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: HERE Technologies and Mercedes-Benz expanded their HD mapping partnership to cover an additional 500,000 kilometers of roads across North America and Europe, enabling Level 3 functionality in 15 new metropolitan areas.

- December 2025: Trimble completed the USD 285 million acquisition of Geodetics Inc., adding real-time kinematic GNSS corrections to its construction and agriculture mapping suite.

- November 2025: Maxar Technologies won a USD 320 million National Geospatial-Intelligence Agency contract for satellite imagery and automated 3D terrain extraction through 2030.

- October 2025: Baidu Maps integrated its HD layer with more than 200,000 EV charging stations across China, providing real-time availability via API.

Global Digital Map Market Report Scope

The Digital Map Market Report is Segmented by Solution (Software, and Services), Deployment (On-Premise, and Cloud), Map Type (Navigation Maps, HD and Real-Time Maps, Topographic and Thematic Maps), End-Use Industry (Automotive, Engineering and Construction, Telecommunications, Public Sector and Defense, Retail and Geomarketing, Other End-Use Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-Premise |

| Cloud |

| Navigation Maps |

| HD and Real-Time Maps |

| Topographic and Thematic Maps |

| Automotive |

| Engineering and Construction |

| Telecommunications |

| Public Sector and Defense |

| Retail and Geomarketing |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Solution | Software | ||

| Services | |||

| By Deployment | On-Premise | ||

| Cloud | |||

| By Map Type | Navigation Maps | ||

| HD and Real-Time Maps | |||

| Topographic and Thematic Maps | |||

| By End-Use Industry | Automotive | ||

| Engineering and Construction | |||

| Telecommunications | |||

| Public Sector and Defense | |||

| Retail and Geomarketing | |||

| Other End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is spending on high-definition maps growing?

HD and real-time layers are forecast to expand at a 14.07% CAGR through 2031 as autonomous-vehicle programs scale.

Which region will add the most incremental revenue by 2031?

Asia-Pacific, led by China, India, and Japan, is projected to post the fastest 14.24% CAGR and contribute the largest share of new spending.

What drives the shift from software licenses to services?

Enterprises increasingly favor continuous map-refresh subscriptions and cloud-integration consulting, pushing services to a 13.71% CAGR through 2031.

Why are cloud deployments overtaking on-premise installations?

Elastic scaling, integrated security, and bundled APIs from AWS, Azure, and Google Cloud make cloud the default choice, already holding 71.42% of 2025 revenue.

How do data-privacy laws affect global providers?

GDPR, China’s PIPL, and India’s data-localization rules force vendors to maintain regional clouds, raising compliance costs and limiting cross-border data flows.

Which companies are challenging the established leaders?

Mapbox, CARTO, and Esri are winning enterprise deals with open standards, vector-tile compression, and spatial SQL services that lower switching costs.

Page last updated on: