Die Casting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

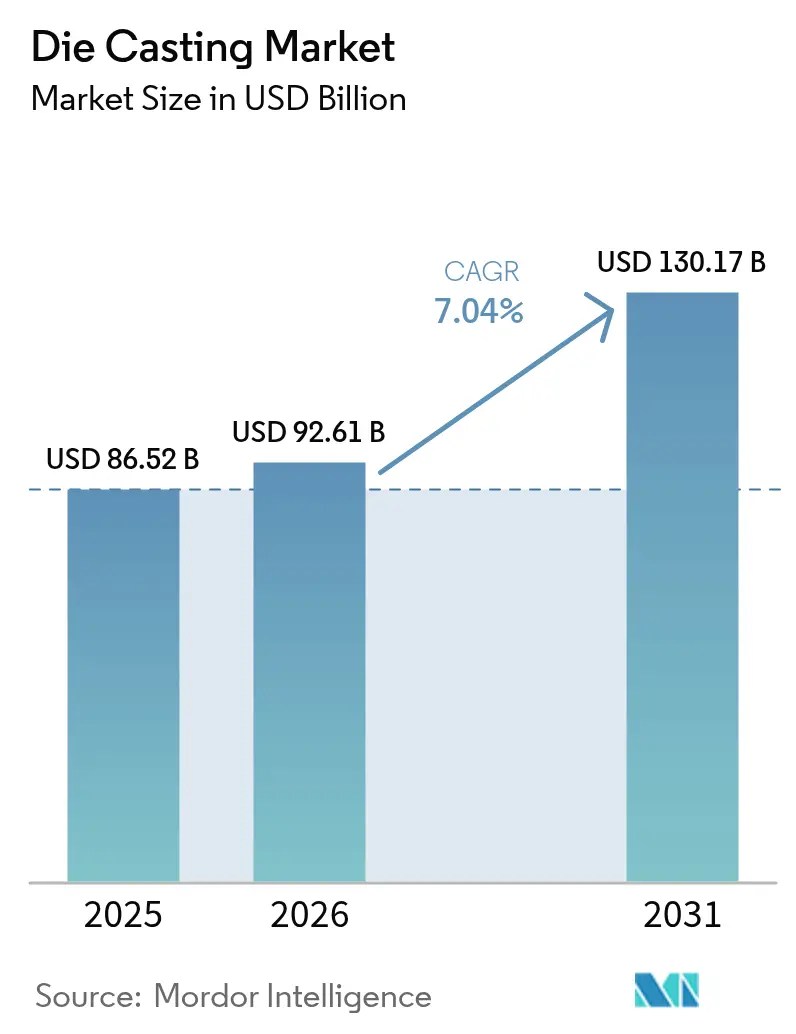

| Market Size (2026) | USD 92.61 Billion |

| Market Size (2031) | USD 130.17 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Die Casting Market Analysis by Mordor Intelligence

The die casting market size was valued at USD 86.52 billion in 2025 and estimated to grow from USD 92.61 billion in 2026 to reach USD 130.17 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031). As electrification reshapes power-train needs, OEMs are replacing multi-piece stamp-and-weld assemblies with single, high-integrity castings that cut weight and part counts while preserving structural rigidity. This pivot keeps the die casting market resilient even as internal-combustion volumes plateau, because the content-per-vehicle in electric cars rises on the back of battery trays, motor housings, and under-body megacastings. Outside mobility, renewable-energy infrastructure, 5G rollouts, and automation programs sustain demand for complex, near-net-shape components. Competitive intensity tightens as tier-1 suppliers, pure-play foundries, and vertically integrating automakers race to master giga-press technology, deploy on-site renewables for cost control, and navigate looming PFAS bans in mold lubricants.

Key Report Takeaways

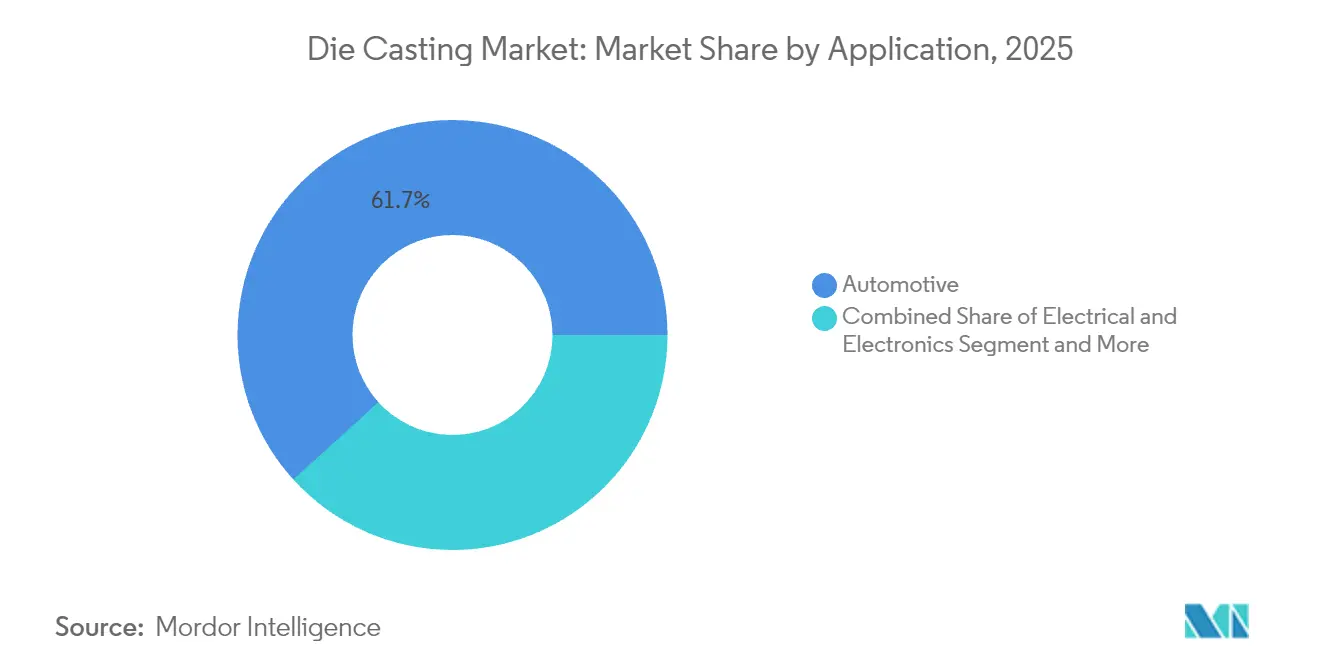

- By application, automotive held 61.73% of the die casting market share in 2025 and is expected to grow at an 8.02% CAGR during the forecast period (2026-2031).

- By process, pressure casting retains 55.02% revenue share in 2025, while vacuum casting is forecast to expand at a 8.93% CAGR during the forecast period (2026-2031).

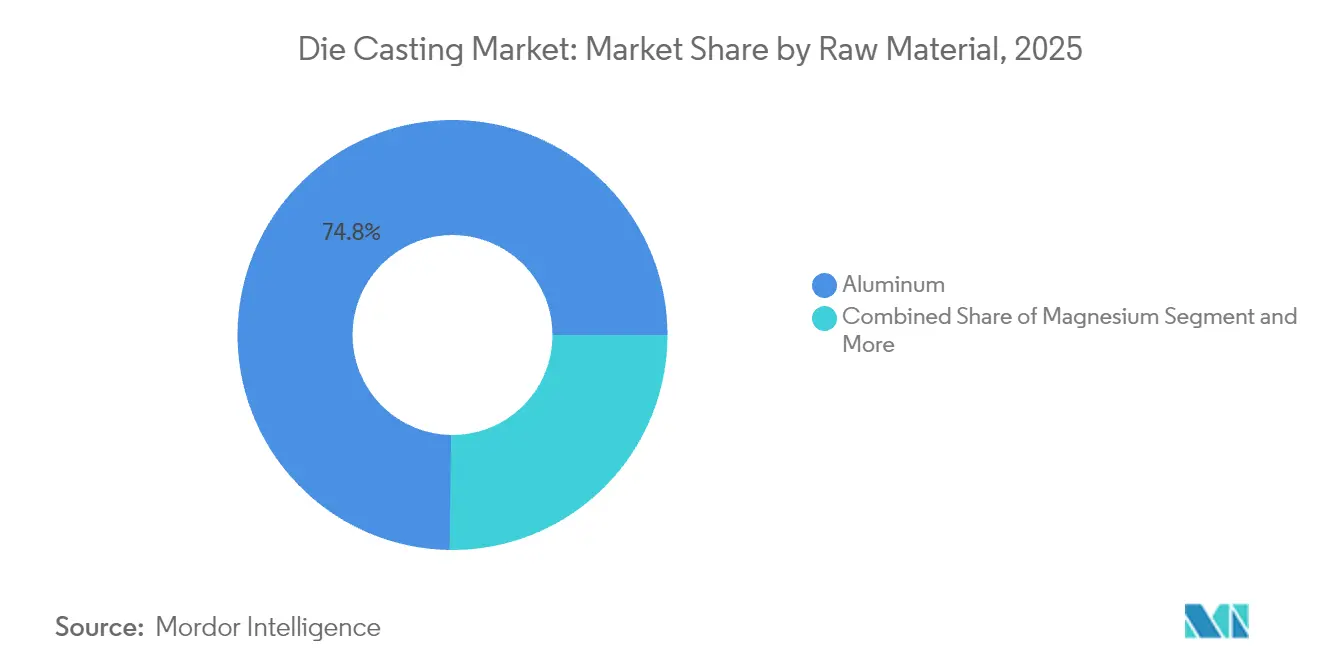

- By raw material, aluminum commanded a 74.78% share of the die casting market size in 2025; magnesium is growing at a 9.53% CAGR during the forecast period (2026-2031).

- By casting-machine clamping force, 4,001-10,000 kN machines accounted for 53.08% share of the die casting market in 2025, whereas the ver 10,000 kN segment is projected to expand at 9.61% CAGR during the forecast period (2026-2031).

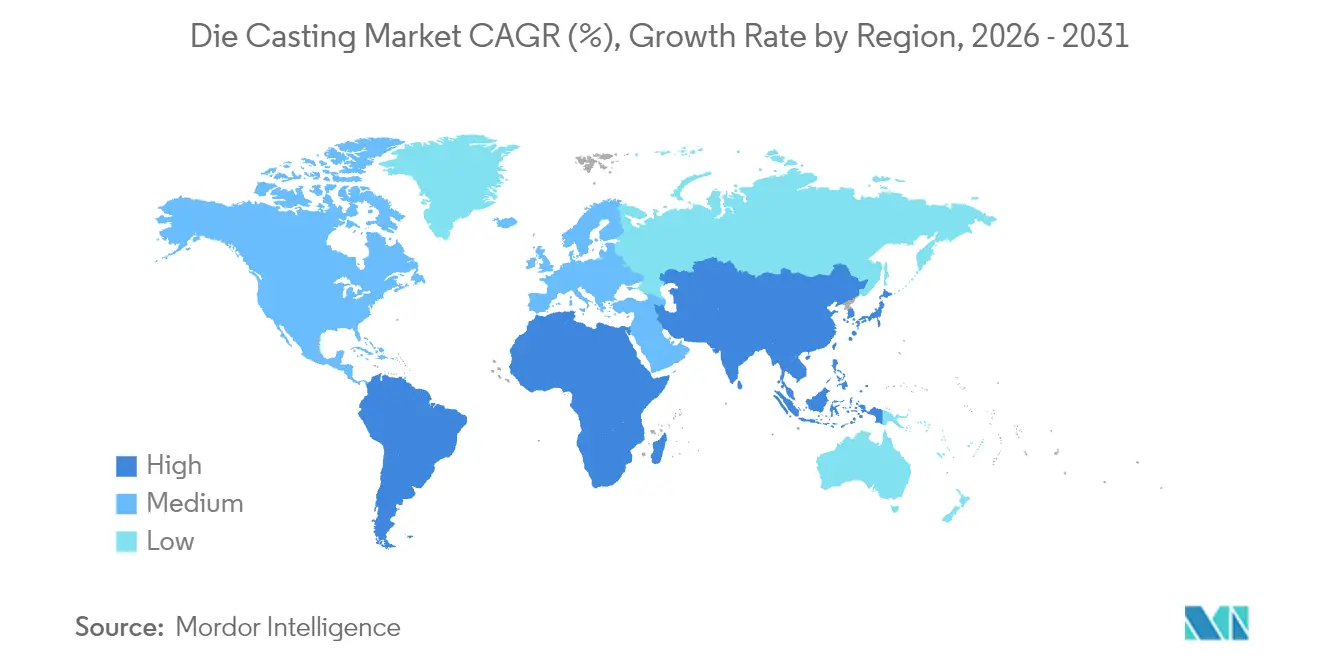

- By geography, Asia-Pacific captured 56.21% share of the die casting market in 2025; the Middle East & Africa region is poised to grow at 8.42% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Die Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE-to-EV Lightweighting Push | +1.8% | Global (early China, North America, Europe) | Medium term (2-4 years) |

| Near-Net-Shape Giga-Press Body | +1.2% | North America and China; spill-over to Europe | Long term (≥4 years) |

| Sensors For Zero-Defect First-Shot | +0.8% | APAC core, spreading to North America and Europe | Medium term (2-4 years) |

| Aluminum Recycling Mandates | +0.7% | Europe leading, North America and APAC trailing | Medium term (2-4 years) |

| On-Site Renewables Hedging Energy | +0.6% | High electricity-cost regions worldwide | Short term (≤2 years) |

| 3D-Printed Sand Cores for EV | +0.5% | Early use in North America and Europe; APAC following | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

ICE-to-EV Structural-Parts Lightweighting Push

Battery-electric vehicles streamline their design with fewer components, yet they demand larger, integrated castings for essential structures such as battery housings, motor frames, and unified chassis sections. A prime example is Tesla's rear underbody megacasting, which consolidates several stamped parts. This underscores the rising strategic significance and value of die casting in each vehicle, regardless of fluctuations in overall production volumes. Studies indicate structural megacasting can reduce curb weight by 10-15%, bringing critical range benefits while lowering assembly complexity [1]Organization for Economic Co-operation and Development, “Electric Vehicle Lightweighting Strategies,” oecd.org.

Near-Net-Shape Pressure-Die-Casting for Giga-Press Body-in-White

Ultra-large giga-presses now create single-piece structures, a feat that once demanded multiple welded components. While traditional automakers are integrating these presses into their new electric vehicle platforms, smaller foundries grapple with challenges like high initial scrap rates and expensive die adjustments. Meanwhile, advanced equipment lines are achieving quicker cycle times, a move that mitigates hefty capital costs and pushes the die-casting industry towards consolidating into fewer, yet significantly larger, production cells.

In-Mold Sensors Enabling Zero-Defect “First-Shot” Quality

AI-driven models now leverage real-time data on pressure, temperature, and flow to forecast defects before solidification concludes. This proactive approach not only curtails scrap rates more effectively than traditional high-pressure lines but also protects profit margins amidst rising alloy costs and the trend of larger components. Additionally, it enhances operational efficiency by enabling manufacturers to optimize production processes and reduce downtime. As a result, this technology is swiftly emerging as a crucial tool for tier-1 suppliers aiming to meet rigorous automotive quality standards.

Circular-Economy Aluminum-Recycling Mandates Spur Secondary HPDC Demand

Major regions are now mandating minimum recycled content levels in aluminum components for both automotive and consumer goods, thanks to circular-economy regulations. These regulations aim to reduce environmental impact and promote sustainable practices. As a result, there's been a notable uptick in the demand for secondary high-pressure die-casting capacity, which is essential for meeting these new requirements. Recycled aluminum cuts energy consumption versus primary smelting, so OEMs use it to meet Scope 3 carbon-reduction targets while shielding themselves from volatile ingot prices[2]“Circular Economy Action Plan: Aluminium Recycling Requirements,” European Commission, europa.eu. Foundries respond by installing advanced sort-and-melt lines that separate post-consumer scrap, feed clean billets into cold-chamber cells, and certify traceability under ISO 14021 guidelines. The process yields cost savings, enabling competitive bids on large structural EV castings that previously relied on virgin alloy feedstock.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-2026 China Magnesium Controls | −1.1% | Global, the highest effect in North America and Europe | Medium term (2-4 years) |

| PFAS-Based Lubricant Restrictions | −0.9% | Strictest in North America and Europe | Short term (≤2 years) |

| OEM Insourcing via Giga-Pressing | −0.8% | North America and China core | Long term (≥4 years) |

| EU Carbon Border Taxes | −0.6% | Direct in Europe, spill-over worldwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Post-2026 Magnesium Supply Risk from China Export Controls

China continues to lead as the primary source of magnesium. However, recent export licensing measures from the country hint at tighter supply controls. Such moves could potentially disrupt downstream casting contracts. Western smelters, taking years to ramp up, are grappling with price volatility, complicating long-term vehicle platform planning. Programs in the automotive and aerospace sectors, which have relied on magnesium's lightweight benefits over aluminum, now confront difficult decisions: redesigning components or stockpiling the material.

Tightening PFAS Emissions Norms on Lubricants

The United States EPA now requires full PFAS usage disclosure under TSCA Section 8(a)(7). Fluorinated mold-release agents deliver unmatched thermal stability above 300 °C, but replacement formulations often need more frequent spraying, raising labor cost and cycle time. Compliance spending—testing, worker training, and new spray equipment—can consume up to 5% of a mid-size foundry’s annual budget[3]“PFAS Reporting Rule under TSCA Section 8(a)(7),” U.S. Environmental Protection Agency, epa.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Automotive Megacasting Reshapes Demand

Automotive applications contributed 61.73% of 2025 revenues and will deliver an 8.02% CAGR to 2031, illustrating how EV structural content offsets ICE decline. The die casting market size for battery enclosures, motor housings, and under-body castings will grow significantly by the end of the forecast period. Automakers are consolidating dozens of stamped components into just a few large castings, leading to a shift in sourcing strategies. They're now favoring suppliers adept at giga-press operations, especially those with flawless startup cycles. Beyond the automotive realm, sectors like renewable energy and telecom are witnessing a steady uptick in demand.

Meanwhile, the aerospace industry is showing heightened interest in titanium and high-strength aluminum, eyeing them for next-generation airframes. This industry-wide transition is spurring intensified R&D efforts into ductile alloys and vacuum-assisted filling, all in a bid to meet stringent crash safety standards. Tier-1 suppliers, previously centered on engine parts, are now pivoting. They're retrofitting furnaces and setting up massive casting cells, focusing on structural components and battery trays. Such trends are elevating entry barriers for smaller foundries and nudging the industry towards integrated hubs, seamlessly blending machining and assembly close to OEM body shops.

By Process: Vacuum Technology Gains Ground

While pressure casting still owns 55.02% of 2025 billings, vacuum casting will clock a 8.93% CAGR as safety-critical EV structures require heat-treatable, weldable parts. When pore content falls 60-80%, automakers can T6-treat aluminum parts without blow-out risk and laser-weld them into multi-material frames. That capability lifts price realizations by up to 30% per kilogram, keeping margin potential high even where alloy cost rises. Consequently, the die casting market sees plants adding vacuum chambers or converting cold-chamber cells to hybrid configurations.

Longer term, squeeze casting and semi-solid processes address niche aerospace and heavy-truck steering knuckles that need forged-like microstructures. Yet their cycle times remain slower, so high-volume industries still favor pressure or vacuum options supplemented by in-die cooling and intensified process monitoring.

By Raw Material: Aluminum Still Rules, Magnesium Accelerates

Aluminum retained 74.78% command in 2025 owing to robust secondary supply chains that slash carbon output 95% versus new smelting. Regulatory targets for recycled content help aluminum hold ground, yet the 9.53% CAGR in magnesium volumes underscores a quest for deeper weight savings. The die casting market size for aluminum parts in electric SUVs will expand in the coming years, whereas magnesium’s lightweight advantage keeps attracting aerospace cabin and seat suppliers despite supply-chain risk.

Zinc sustains hardware and consumer goods where its fluidity and dimensional stability shine, while copper alloys serve thermal-management bases in power-electronics modules. Rising EU circular-economy thresholds, however, push OEMs to audit alloy provenance, rewarding cast houses that certify recycled inputs.

By Casting-Machine Clamping Force: High-Tonnage Cells Surge

Cells rated 4,001-10,000 kN contributed 53.08% of 2025 turnover because they balance flexibility with capacity. Even so, presses above 10,000 kN will post a 9.61% CAGR to 2031 as megacasting reshapes assembly lines. Notable number of giga-presses have been booked worldwide, and each installation, often costing at the higher-end, triggers adjacent investment in robots, quench tanks, and X-ray quality stations. Foundries that secure long-term EV platform awards commit to single-supplier press strategies to ensure die-to-die consistency, cementing deeper OEM-foundry partnerships within the die casting market.

Small machines under 4,000 kN continue serving electronics, medical, and precision-pump components where tighter wall-thickness tolerances outrank sheer volume. These cells also evolve, adopting in-machine temperature mapping and automated quick-die-change tables to limit downtime.

Geography Analysis

Asia-Pacific generated 56.21% of global sales in 2025, anchored by China’s vast auto, appliance and electronics clusters. Decades of cumulative know-how, high scrap-aluminum availability, and vertically integrated tool-steel ecosystems keep cost positions sharp. Korea and Japan contribute control-system innovation, while India rides production-linked incentives that fund new lightweight-component lines. As OEMs diversify sourcing, Southeast Asia gains share for low-complexity parts and back-up capacity, broadening the die casting market footprint across ASEAN.

The Middle East & Africa region is the fastest riser at 8.42% CAGR. Gulf Cooperation Council states use Vision 2030 funds to manufacture solar inverters, wind housings, and EV chargers domestically. Megaprojects like NEOM draw demand for high-tonnage presses able to cast aluminum façade nodes and structural connectors. Turkey’s auto exports and Egypt’s industrial-park policies further energize regional orders, though upstream ingot supply relies on imports until smelters scale.

North America and Europe grow chiefly through technology shifts rather than plant count. United States tax credits favor domestic battery and drivetrain sourcing, causing OEMs to localize megacasting next to assembly plants in Ohio, Alabama, and Ontario. Europe’s Carbon Border Adjustment Mechanism boosts competitive standing for regional shops running recycled aluminum furnaces on renewable power. Both regions further the die casting market by enforcing PFAS phase-outs and lifecycle carbon audits, spurring capital upgrades and digital traceability modules.

Mordor Intelligence provides coverage of the die casting market across other key regional markets. Detailed country-level analysis extends to South Korea incorporating local coverage and market participation, as required.

Competitive Landscape

The die casting market remains moderately fragmented, yet megacasting’s capital demands push consolidation. Large diversified groups have acquired niche foundries to secure vacuum capacity and giga-press know-how. Meanwhile, automakers insource signature structures to lock in IP and shorten supply chains, pressuring tier-1 volume.

Strategic moves include a major North American supplier installing 9,000-ton presses adjacent to an OEM body shop, while a European lightweight specialist divested conventional engine block lines to focus on EV battery trays. Technology edge is decisive. Suppliers offering design-for-casting co-engineering, 3D-printed sand cores, and AI-driven defect prediction win longer, higher-margin contracts.

Sustainability credentials matter too: plants powered 50% or more by on-site renewables secure premium OEM score-card ratings. Finally, additive-manufacturing entrants print intricate core inserts that cut tooling lead times by weeks, nudging incumbents to form alliances or licensing deals.

Die Casting Industry Leaders

Form Technologies Inc. (Dynacast)

Nemak S.A.B. de C.V.

Georg Fischer Ltd

Pace Industries Inc.

Endurance Technologies Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Nemak agreed to acquire GF Casting Solutions’ automotive division for USD 336 million, with USD 160 million paid upfront from long-term credit lines.

- June 2025: Uno Minda approved a greenfield aluminum die casting plant in Maharashtra, India, targeting EV two- and four-wheeler demand.

- February 2025: Sundaram Clayton commissioned a new plant near Chennai and installed a 4,400-ton press in the United States to supply engine and EV structural castings.

- October 2024: Handtmann has successfully commissioned a Carat 610, extended from Bühler AG, marking its entry into the production of large structural parts. The Carat 610 boasts a clamping force of 61,000 kN and can handle a shot weight of up to 128 kg of aluminum.

Global Die Casting Market Report Scope

Die casting is an automated casting process for producing metal parts of a particular shape are produced by pouring molten material into a mold under pressure.

The Die Casting Market is Segmented by Application (Automotive, Electrical and Electronics, Industrial, and Other Applications), Process (Pressure Die Casting, Vacuum Die Casting, Squeeze Die Casting, and Other Processes), Raw Material (Aluminum, Magnesium, and Zinc), and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa).

| Automotive |

| Electrical and Electronics |

| Industrial Machinery |

| Aerospace and Defense |

| Consumer Appliances |

| Others |

| Pressure Die Casting |

| Vacuum Die Casting |

| Squeeze Die Casting |

| Gravity Die Casting |

| Aluminum |

| Magnesium |

| Zinc |

| Copper |

| Others (Lead, Tin Alloys) |

| ≤4,000 kN |

| 4,001-10,000 kN |

| Above 10,000 kN |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Malaysia | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Automotive | |

| Electrical and Electronics | ||

| Industrial Machinery | ||

| Aerospace and Defense | ||

| Consumer Appliances | ||

| Others | ||

| By Process | Pressure Die Casting | |

| Vacuum Die Casting | ||

| Squeeze Die Casting | ||

| Gravity Die Casting | ||

| By Raw Material | Aluminum | |

| Magnesium | ||

| Zinc | ||

| Copper | ||

| Others (Lead, Tin Alloys) | ||

| By Casting-Machine Clamping Force | ≤4,000 kN | |

| 4,001-10,000 kN | ||

| Above 10,000 kN | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the die casting market in 2026?

The die casting market size is USD 92.61 billion in 2026, on track for USD 130.17 billion by 2031.

Which segment grows fastest through 2031?

Machines above 10,000 kN clamping force post the quickest rise at 9.61% CAGR as megacasting gains scale.

Why is automotive demand still rising in die casting?

Electric vehicles need large, integrated aluminum castings for battery and chassis structures, so content-per-vehicle climbs even while ICE components decline.

Which region leads die casting production?

Asia-Pacific holds 56.21% of global revenue thanks to mature supply chains and high aluminum recycling capacity.

Page last updated on: