Desktop Virtualization In Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.51 Billion |

| Market Size (2030) | USD 3.71 Billion |

| Growth Rate (2025 - 2030) | 8.15% CAGR |

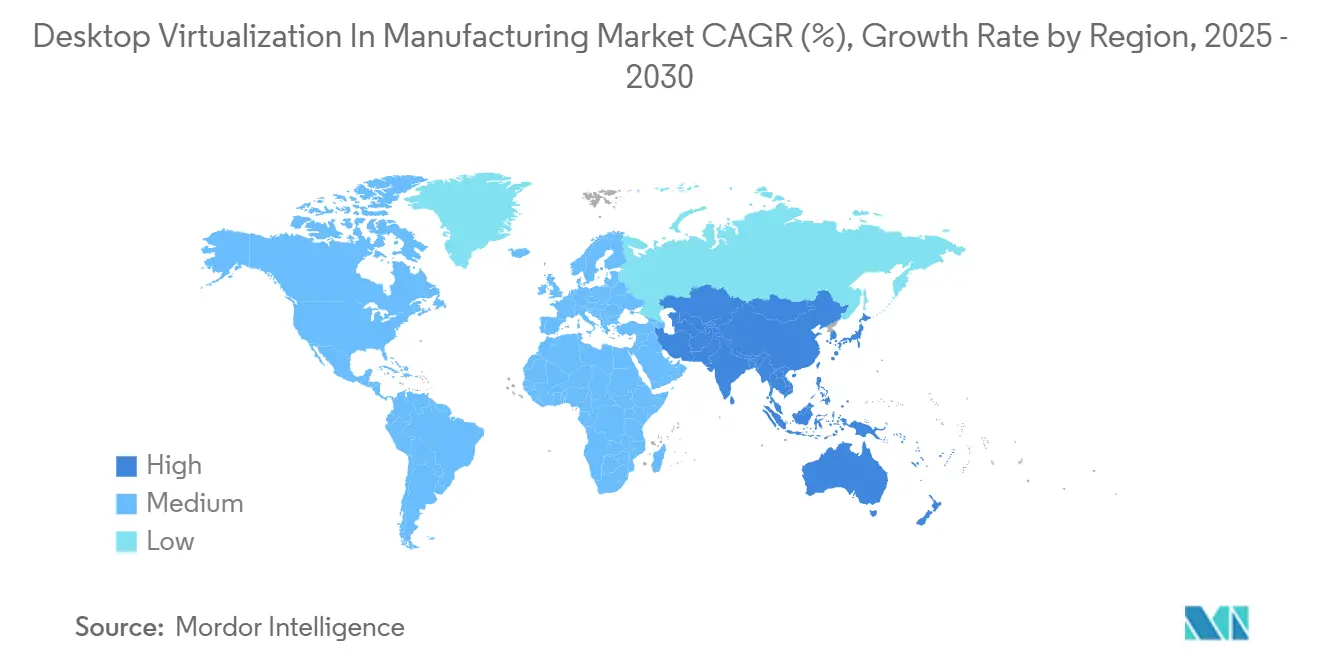

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Desktop Virtualization In Manufacturing Market Analysis by Mordor Intelligence

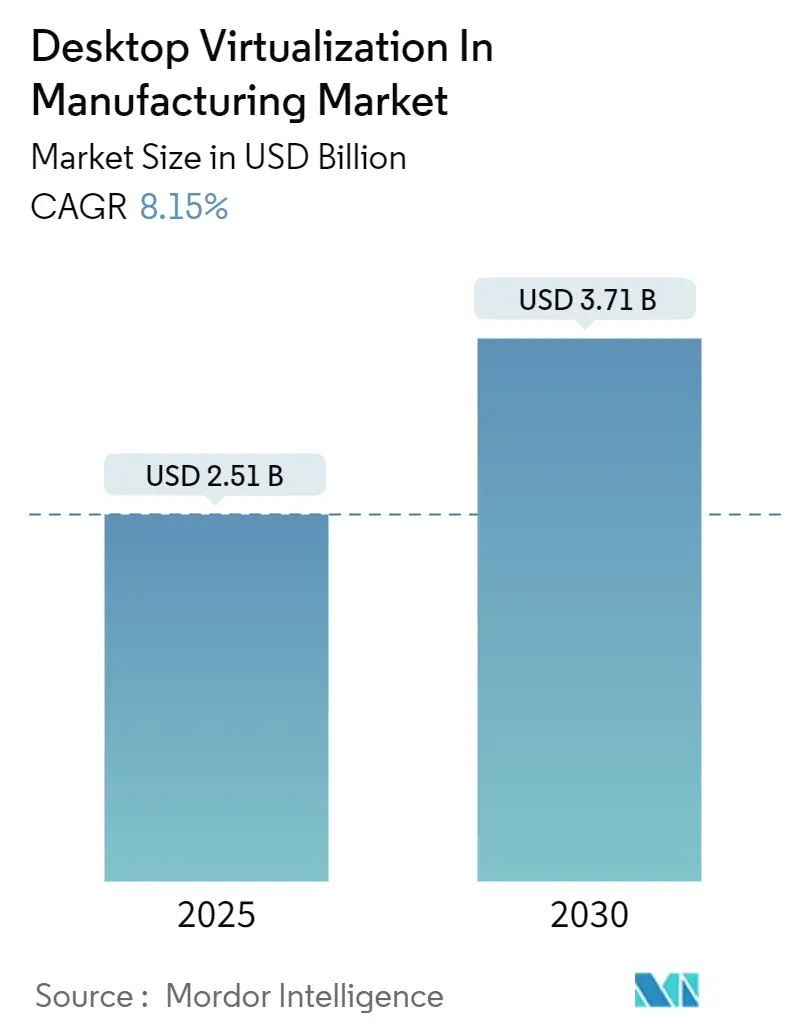

The desktop virtualization in the manufacturing market size was valued at USD 2.51 billion in 2025 and is on track to reach USD 3.71 billion by 2030, advancing at an 8.2% CAGR. This expansion reflects factories’ shift toward centralized, secure, and remotely accessible workstations that unify operational-technology and information-technology workloads. High demand for hybrid work models, stricter cybersecurity mandates, and the growing use of compute-heavy CAD/CAE workloads over virtual channels fuel adoption. Vendors are also layering artificial-intelligence features onto platforms to automate provisioning and predict performance bottlenecks, creating new value levers for buyers. Simultaneously, manufacturers are balancing on-premise control with selective cloud offloading to keep intellectual property safe while still cutting infrastructure costs.

Key Report Takeaways

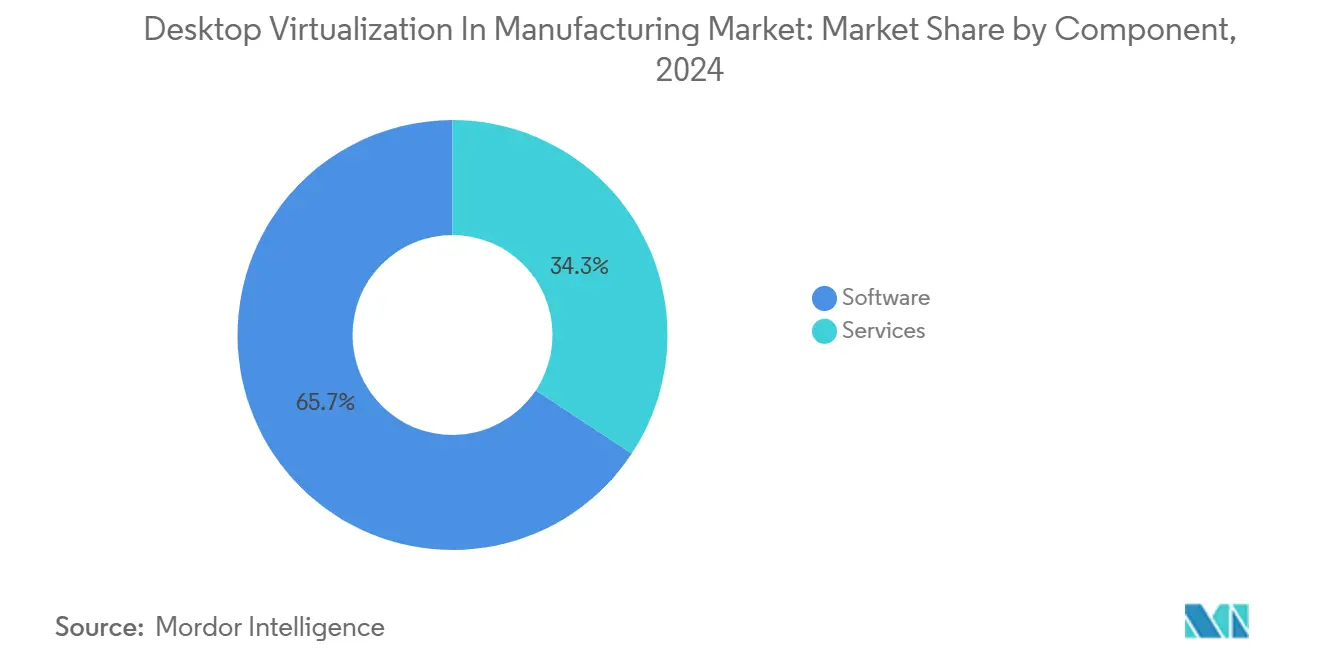

- By component, software led with 65.7% revenue share in 2024, whereas services are forecast to expand at a 9.8% CAGR through 2030.

- By desktop-delivery platform, Hosted Virtual Desktop held 59.2% of the desktop virtualization in manufacturing market share in 2024, while Desktop-as-a-Service is projected to grow at 8.8% CAGR to 2030.

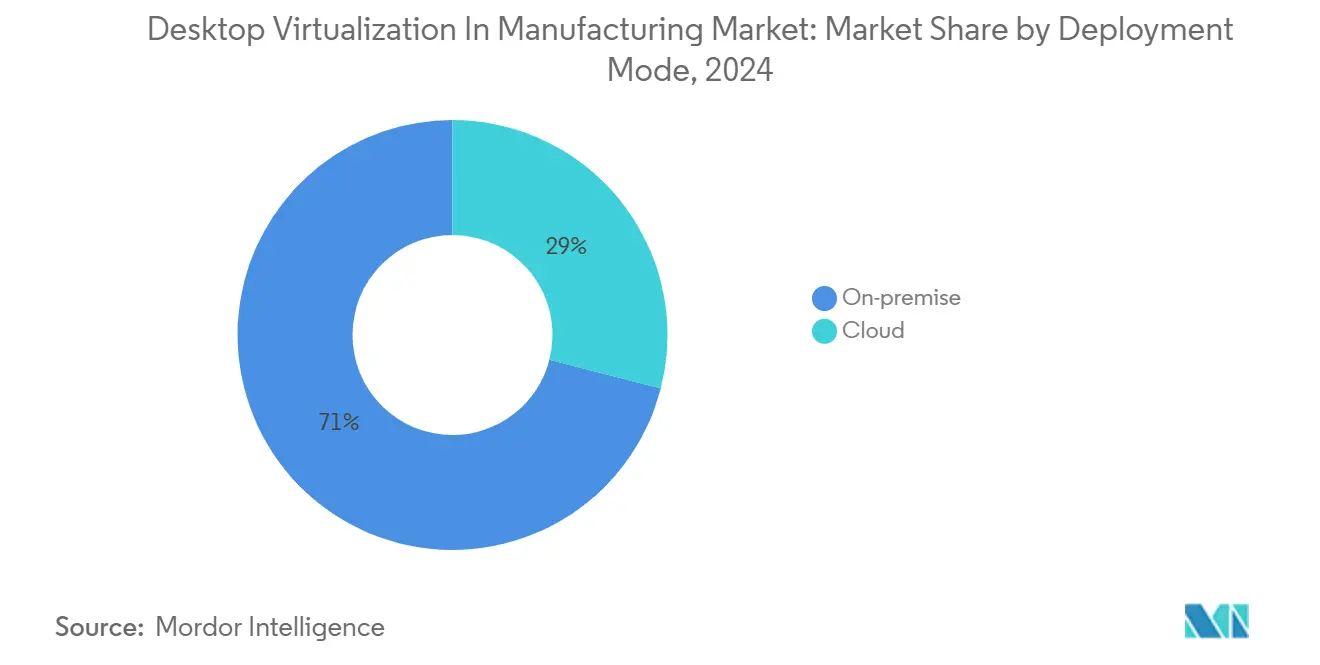

- By deployment mode, on-premise solutions commanded 71.0% share of the desktop virtualization in manufacturing market size in 2024; cloud deployments are set to rise at a 10.0% CAGR.

- By organization size, large enterprises accounted for 69.4% of revenue in 2024, but small and medium enterprises will post the fastest 9.4% CAGR.

- By geography, North America led with 39.8% share in 2024, whereas Asia-Pacific is the fastest-growing region at 8.6% CAGR.

Global Desktop Virtualization In Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to hybrid and remote workforces | +1.8% | North America, Europe | Medium term (2-4 years) |

| Need to secure OT–IT convergence endpoints | +1.5% | Asia-Pacific, global tier-1 hubs | Long term (≥ 4 years) |

| Cloud cost-optimised GPU instances for 3-D CAD/CAE | +1.2% | North America, European advanced-manufacturing corridors | Short term (≤ 2 years) |

| Predictive maintenance via virtual-desktop logging | +0.9% | Asia-Pacific core, MEA spill-over | Medium term (2-4 years) |

| Energy-efficient thin clients for ESG goals | +0.6% | European Union, expanding to North America | Long term (≥ 4 years) |

| Government “sovereign cloud” mandates | +0.8% | China, India, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Hybrid and Remote Manufacturing Workforces

Digital-twin platforms allow production managers to oversee lines from anywhere, as shown in BMW’s smart factory and Unilever’s Brazil plant deployments. Virtual desktops supply engineers with secure, high-performance access to CAD, MES, and SCADA tools regardless of location, keeping projects on schedule when travel or site access is limited. A new cadre of “sky-blue-collared” employees, operators proficient in data visualization and machine-learning dashboards, needs flexible desktops that evolve with shifting skill sets. Manufacturers also rely on virtualization to maintain business continuity during supply-chain shocks, quickly rerouting workloads to alternate sites. Collectively, these factors amplify demand for desktop virtualization in the manufacturing market.

Need to Secure OT–IT Convergence Endpoints

Honeywell notes that tighter connectivity between plant-floor devices and corporate networks expands the threat surface, making unified endpoint control vital.[1]Honeywell, “Industrial Cybersecurity and OT–IT Convergence,” honeywell.com Virtual-desktop infrastructure (VDI) underpins zero-trust frameworks by centralizing authentication, patching, and logging while isolating production data. Compliance with IEC 62443 and similar standards further accelerates uptake. As manufacturers integrate Industrial-IoT feeds with enterprise resource systems, VDI creates the secure bridge required for real-time visibility without exposing controllers to the public internet. Consequently, security mandates remain a primary catalyst for the desktop virtualization in manufacturing market.

Cloud Cost-Optimised GPU Instances for 3-D CAD/CAE

NVIDIA’s virtual-GPU licensing and leading hyperscalers’ on-demand GPU tiers let small design teams spin up high-power workstations without buying physical cards. Automotive and aerospace firms run complex crash or airflow simulations entirely in the cloud, yet deliver frames interactively to users thousands of miles away. Pay-as-you-go economics shrink capex, making the technology accessible to tier-2 suppliers and thereby broadening the desktop virtualization in the manufacturing market’s addressable base. Lower entry barriers translate into faster proof-of-concept cycles and more rapid production roll-outs.

Predictive Maintenance Enabled by Virtual Desktop Logging

Microsoft Azure’s predictive-maintenance toolkit links VDI session data, IoT sensor streams, and machine-learning models to forecast failures with high accuracy. Operators can visualize anomalies inside their virtual desktops in real time, triggering just-in-time part replacements and reducing downtime. Brownfield plants benefit because legacy control interfaces can be wrapped within new virtual sessions that capture granular user actions, enriching training data for algorithms. As reliability gains become measurable, more factories allocate budgets to virtualization, reinforcing growth for the desktop virtualization in the manufacturing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High LAN latency in brown-field plants | –1.4% | Emerging-market brownfield facilities | Short term (≤ 2 years) |

| Persistent software-licence stacking costs | –1.1% | North America, Europe | Medium term (2-4 years) |

| OT cyber-safety standards slow roll-outs | –0.8% | Global | Long term (≥ 4 years) |

| Skilled-labour gap for VDI image engineering | –0.6% | Asia-Pacific and other developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High LAN Latency in Brown-Field Plants

Citrix performance guidelines warn that session quality declines sharply past 300 ms latency, a threshold often exceeded in older factories relying on daisy-chained switches. Retrofitting networks during active production is complex and expensive, delaying many projects. Until connectivity upgrades complete, organizations cap VDI roll-outs to non-critical zones, tempering near-term growth of the desktop virtualization in manufacturing market.

Persistent Software-Licence Stacking Costs

Autodesk’s virtualization policies stipulate separate licenses for virtual deployments, and GPU passthrough adds further fees.[2]Autodesk Inc., “Software Licensing for Virtual Deployments,” autodesk.com These cumulative costs can double total ownership, especially for SMEs. Consequently, some firms postpone upgrades or adopt open-source alternatives, muting revenue expansion despite technical readiness. Vendors are responding with usage-based billing and bundled service tiers, but cost friction remains a restraint on the desktop virtualization in manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Software Dominance

The software layer secured 65.7% revenue of desktop virtualization in the manufacturing market in 2024, thanks to perpetual and subscription licenses required for CAD, MES, and endpoint-security add-ons. Concurrently, the services category is projected to rise at 9.8% CAGR as plants seek integration experts to merge virtual desktops with PLC networks and industrial-control protocols. Implementation, managed hosting, and compliance audits make up the bulk of the spend. A sizeable share of contracts now bundle AI-driven monitoring, pushing managed-services demand higher. This shift toward expertise-heavy engagements reveals how desktop virtualization in manufacturing market is evolving from tool purchase to lifecycle partnership.

Manufacturers obligated to adhere to IEC 62443 and NIST 800-82 increasingly outsource configuration validation and continuous patching. In parallel, platform vendors introduce reference architectures that still need on-site tuning for real-time constraints such as motion-control latency. As a result, service providers capture incremental margins, and their influence over vendor choice grows. The desktop virtualization in the manufacturing market size for services is forecast to account for a larger slice of overall spend by 2030, even as licensing remains the single biggest line item.

By Desktop Delivery Platform: DaaS Disrupts Traditional HVD Leadership

Hosted Virtual Desktop retained a 59.2% share in 2024, capitalizing on existing data-center footprints within large automotive and electronics conglomerates. However, Desktop-as-a-Service is scaling at 8.8% CAGR as line-of-business heads embrace opex models and faster deployment cycles. Cloud-native orchestration now auto-scales GPU resources during peak design sprints, eliminating over-provisioning. The desktop virtualization in manufacturing market thus sees a pronounced pivot toward SaaS-like consumption without losing the deterministic performance controls that engineers demand.

In regulated segments such as medical-device fabrication, hybrid architectures prevail: blueprints place the broker and authentication stack in the cloud while image repositories stay on-premise. This architecture satisfies data-residency rules yet still grants remote collaboration benefits. As hyperscalers expand regional availability zones near industrial clusters, network jitter falls, further encouraging DaaS uptake. Analysts expect HVD dominance to erode steadily, though it will remain relevant for ultra-low-latency assembly-line consoles that cannot risk public-cloud outages.

By Deployment Mode: Cloud Acceleration Despite On-Premise Preference

On-premise deployments owned 71.0% of revenue in 2024 because intellectual property, tooling recipes, and robotics parameters are viewed as crown jewels. That said, cloud instances are growing at 10.0% CAGR as zero-trust postures mature. Hyper-converged edge appliances now cache golden-image updates locally but replicate logs to the cloud for analytics. This reconciles autonomy with centralized oversight, supporting the desktop virtualization in manufacturing market’s hybrid trajectory.

Microsoft’s USD 349 Windows 365 Link thin client bridges secure local peripherals and Azure-hosted desktops.[3]Microsoft Corporation, “Predictive Maintenance Using Azure,” microsoft.com Early adopters in discrete electronics fabrication report 40% shorter onboarding time for contractors. Vendors are also shipping “sovereign cloud” variants that restrict telemetry export, meeting China’s and India’s localization statutes. Over the forecast horizon, hybrid patterns are expected to dominate new roll-outs, while pure on-premise estates continue shrinking as hardware refresh cycles lapse.

By Organization Size: SME Adoption Accelerates Despite Enterprise Dominance

Large enterprises still contributed 69.4% revenue in 2024, leveraging scale to negotiate volume discounts and multi-year service agreements. Yet SMEs are registering the fastest 9.4% CAGR, propelled by pay-as-you-go cloud plans and packaged managed services. DaaS eliminates the need for full-time VDI administrators, erasing a capacity gap that once kept smaller firms on traditional PCs. As a result, the desktop virtualization in manufacturing market witnesses democratization, with tier-2 suppliers gaining secure access to the same design toolchains used by OEMs.

ISVs such as VMware streamlined Horizon licensing bundles for firms under 1,000 seats, cutting procurement complexity. Channel partners now offer “virtual-desktop-in-a-box” kits with pre-configured GPU nodes delivered as operating leases. These shifts lower adoption barriers, translating into higher aggregate seat counts even if initial ticket sizes remain modest. Over time, SMEs’ cumulative demand will counterbalance the large-enterprise plateau, sustaining healthy market growth.

Geography Analysis

North America controlled 39.8% of 2024 revenue due to early migration toward zero-trust frameworks and substantial automotive, aerospace, and semiconductor verticals. The region’s installations emphasize deep integration with MES and quality-inspection cameras. General Motors’ collaboration with NVIDIA Omniverse to optimize body-in-white robotics lines underscores the powerful synergy between real-time simulation and virtual desktops. As reshoring incentives prompt companies to reconstruct supply chains, virtualization enables remote commissioning of new lines before physical equipment arrives, anchoring the desktop virtualization in manufacturing market trajectory in North America.

Asia-Pacific is expanding at an 8.6% CAGR, spearheaded by China’s and India’s digital-manufacturing drives. Sovereign-cloud mandates require data to remain in-country, giving rise to domestic DaaS offerings built on local hyperscale regions. Government-backed electronics and semiconductor parks adopt virtualization to pool scarce CAD/EDA licenses, shortening design cycles. NVIDIA’s planned joint facilities with Foxconn and Wistron further lift regional compute capacity, opening pathways for small suppliers to migrate workloads previously out of reach. In parallel, ASEAN nations channel Industry 4.0 grants into network upgrades, mitigating latency constraints that once hindered adoption.

Europe follows with steady gains as GDPR, the Cyber-Resilience Act, and the NIS 2 Directive tighten cybersecurity obligations for critical sectors. Audi’s Edge Cloud 4 Production program virtualizes PLCs and worker stations on VMware Cloud Foundation to cut physical-controller counts by 30%.[4]Broadcom Inc., “Audi and Broadcom Launch Edge Cloud 4 Production,” broadcom.com Meanwhile, energy-efficiency imperatives drive uptake of thin clients that slash endpoint power draw, aiding ESG scorecards. Pan-European manufacturers also favor cross-border engineering hubs, where virtual desktops ease talent sharing without relocating staff. The Middle East and Africa market, while nascent, benefits from national diversification agendas that prioritize advanced manufacturing. New green-field plants incorporate VDI from day one, skirting legacy networking pitfalls. Regional telcos partner with platform providers to launch low-latency edge zones, creating an infrastructural springboard for the desktop virtualization in manufacturing market.

Competitive Landscape

Industry concentration is moderate. Broadcom’s 2024 acquisition of VMware and the spin-out of the End-User Computing division (now Omnissa) reshuffled the field, but it did not create a near-monopoly. Omnissa, Citrix (Cloud Software Group), Microsoft, and NVIDIA dominate core platform revenues, collectively accounting for roughly 60% of global spend. Citrix augmented its stack with DeviceTrust and Strong Network to embed context-aware access controls, cementing a security-first value proposition. Microsoft courts cloud-native workloads through Azure Virtual Desktop and Windows 365, bundling services like Defender for Endpoint to deliver an integrated offer.

NVIDIA differentiates with vGPU acceleration and AI-driven resource orchestration, appealing to simulation-heavy use cases. Start-ups such as Sangfor Technologies compete on cost and mid-market simplicity, bundling hyper-converged infrastructure, managed cloud, and VDI under a single pane. Meanwhile, hyperscalers insert native DaaS services into their marketplaces, compressing margins for traditional license vendors. To stay relevant, incumbents layer machine-learning models that predict host saturation and auto-heal user sessions, shrinking administration overhead.

Strategic alliances illustrate the race for vertical depth. Broadcom and Audi debuted a joint Edge Cloud initiative that virtualizes PLCs, validating industrial-grade latency performance. Rockwell Automation’s Emulate3D on NVIDIA Omniverse enables simulation-guided factory acceptance tests before hardware ships, shortening initial ramp-up. Looking forward, vendors that embed OT protocols, AI-enabled troubleshooting, and regulatory controls into their platforms are poised to win share in the desktop virtualization in manufacturing market.

Desktop Virtualization In Manufacturing Industry Leaders

IBM Corp.

Microsoft Corporation

Cisco Systems Inc.

Oracle Corporation.

Amazon Web Services Inc. (Amazon WorkSpaces)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Broadcom and Audi rolled out Edge Cloud 4 Production, relying on VMware Cloud Foundation to virtualize PLCs and worker stations, trimming hardware footprint and elevating efficiency.

- March 2025: Rockwell Automation showcased Emulate3D Factory Test with NVIDIA Omniverse APIs, allowing pre-deployment validation of automation systems through immersive simulation.

- March 2025: Omnissa launched a three-tier partner program featuring performance-based incentives and an AI assistant named Omni to streamline hybrid-work deployments.

- February 2025: KION Group, Accenture, and NVIDIA unveiled “Mega,” an Omniverse blueprint for smart-warehouse digital twins that balance robot fleets and labor assignments.

Global Desktop Virtualization In Manufacturing Market Report Scope

| Software |

| Services |

| Hosted Virtual Desktop (HVD) |

| Hosted Shared Desktop (HSD) |

| Desktop-as-a-Service (DaaS) |

| Remote Desktop Services (RDS) |

| On-premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Desktop Delivery Platform | Hosted Virtual Desktop (HVD) | ||

| Hosted Shared Desktop (HSD) | |||

| Desktop-as-a-Service (DaaS) | |||

| Remote Desktop Services (RDS) | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current market value of desktop virtualization in manufacturing?

The desktop virtualization in manufacturing market reached USD 2.51 billion in 2025 and is projected to hit USD 3.71 billion by 2030.

Which component segment is growing fastest?

Services, covering consulting, integration, and managed offerings, is set to grow at a 9.8% CAGR through 2030 as factories seek specialized expertise.

Why are SMEs increasingly adopting virtual desktops?

Pay-as-you-go cloud plans and packaged managed-service bundles remove the need for in-house VDI specialists, enabling SMEs to leverage enterprise-grade security and CAD performance.

How does virtualization improve predictive maintenance?

Virtual desktops aggregate session logs with IoT sensor data, feeding machine-learning models that forecast equipment failures and schedule maintenance before downtime occurs.

What role do cloud GPUs play in manufacturing design?

Cost-optimized cloud GPU instances deliver high-fidelity CAD/CAE rendering to engineers without the capital expense of workstation-grade hardware, accelerating product development cycles.

Page last updated on: