Dental Milling Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

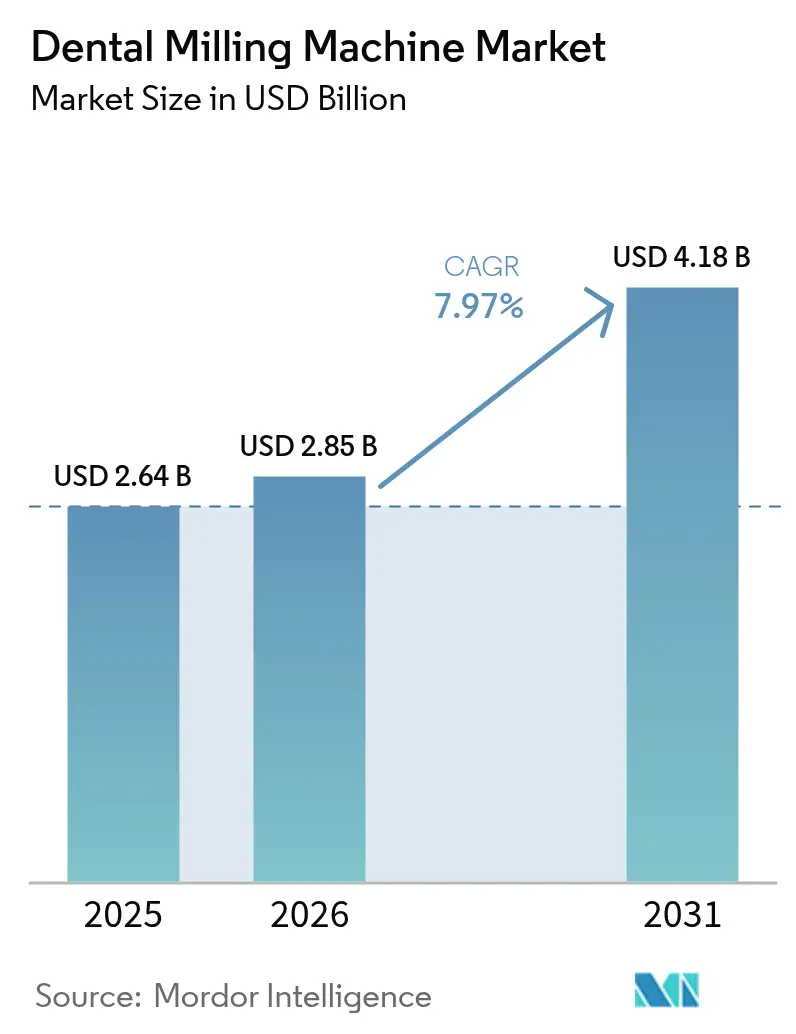

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 4.18 Billion |

| Growth Rate (2026 - 2031) | 7.97% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Milling Machine Market Analysis by Mordor Intelligence

The dental milling machine market size in 2026 is estimated at USD 2.85 billion, growing from 2025 value of USD 2.64 billion with 2031 projections showing USD 4.18 billion, growing at 7.97% CAGR over 2026-2031. Growth stems from the shift toward fully digital workflows that shorten chair-time and improve restoration precision. Demand for zirconia and other high-aesthetic ceramics is pulling five-axis technology into the mainstream, while cloud-based design platforms let laboratories and clinics collaborate in real time. Asia-Pacific shows the steepest trajectory as rising healthcare spending and dental tourism increase equipment orders, whereas North America retains leadership because of early CAD/CAM adoption and a consolidated service-organization structure. Subscription and leasing models are emerging to soften the high upfront costs that still hinder smaller practices.

Key Report Takeaways

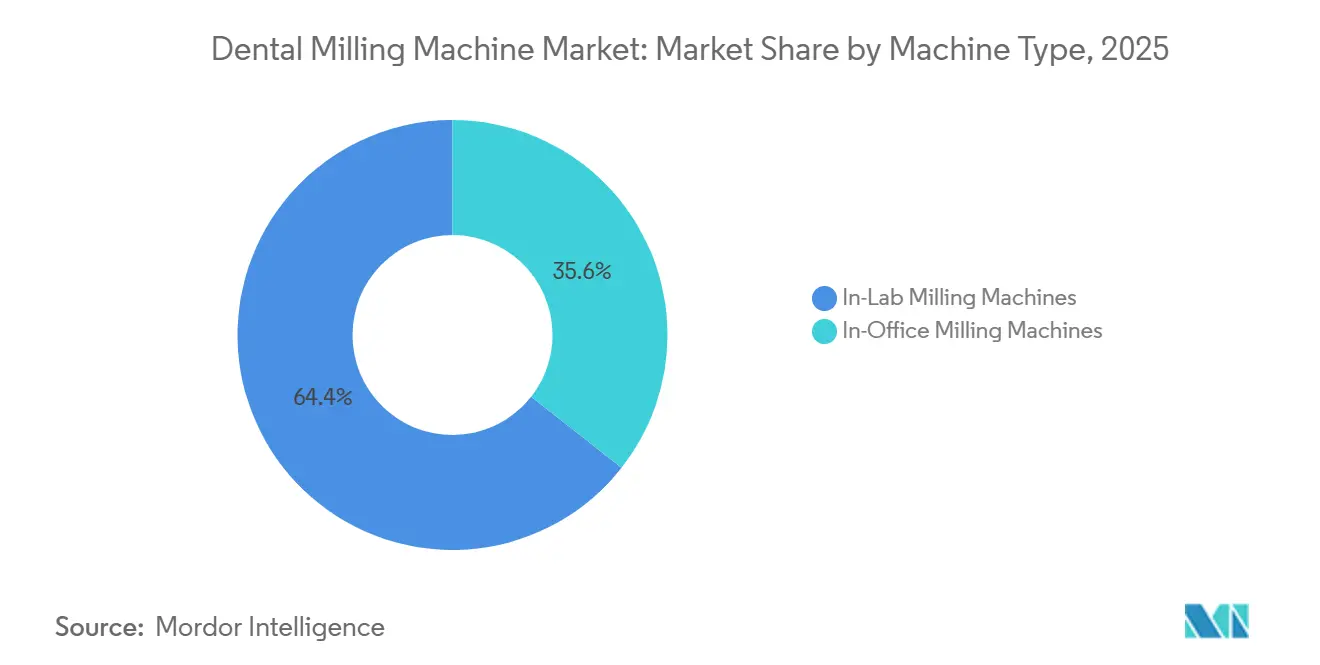

- By machine type, In-Lab systems led with 64.40% revenue share in 2025, while In-Office units are projected to expand at a 10.36% CAGR through 2031.

- By axis configuration, 4-axis platforms held 55.30% of the dental milling machine market share in 2025; 5-axis units are advancing at an 11.55% CAGR.

- By size, bench-top units accounted for 40.40% of the dental milling machine market size in 2025; stand-alone systems are forecast to grow 12.05% per year to 2031.

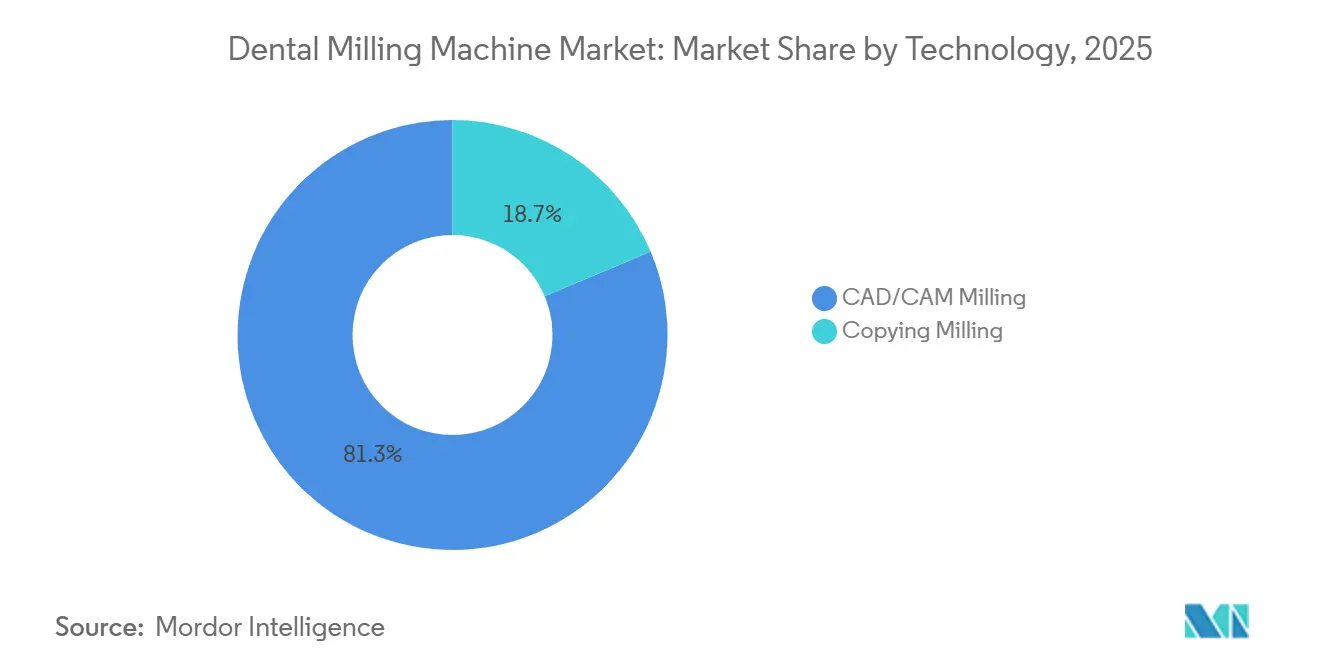

- By technology, CAD/CAM captured 81.35% of 2025 revenue and is set to post a 9.45% CAGR during the outlook period.

- By end-user, laboratories commanded 72.20% share of the dental milling machine market size in 2025, whereas clinics record the fastest growth at 12.44% CAGR.

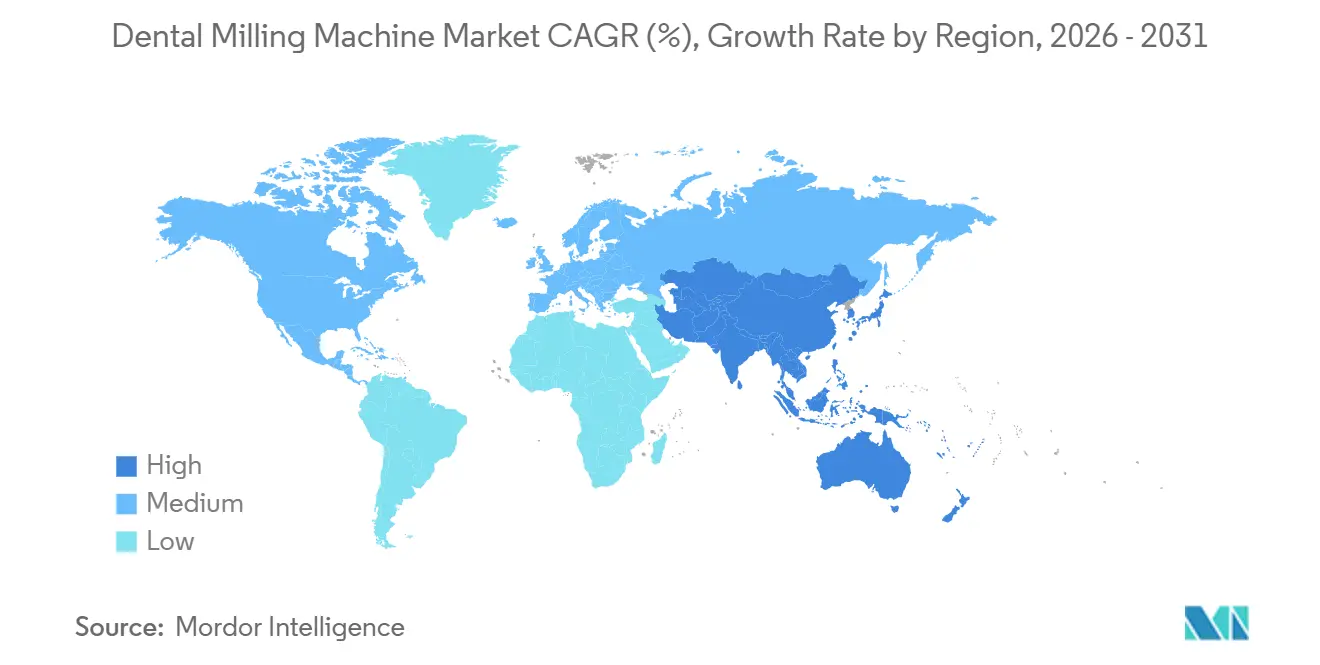

- By geography, North America contributed 37.60% of global revenue in 2025, while Asia-Pacific is on track for a 12.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Milling Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Burden of Untreated Dental Caries & Tooth Loss | +2.5% | Global, with highest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Rapid Digitization of Dental Workflows (Scanner–CAD–Mill–Sinter) | +2.2% | Global, led by North America and Europe | Short term (≤2 years) |

| Expansion of Dental Service Organizations & Centralized Milling Hubs | +1.8% | North America & EU, with emerging impact in APAC core | Medium term (2-4 years) |

| Escalating Demand for High-Aesthetic Materials (Zirconia, Li-disilicate) Requiring Precision Milling | +1.5% | Global, with highest impact in developed markets | Short term (≤2 years) |

| Government-Backed Insurance Expansion for Prosthetic Restorations | +1.3% | North America & EU, with spill-over to APAC core | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Untreated Dental Caries & Tooth Loss

An estimated 2.3 billion people live with untreated caries, and clinicians increasingly choose milled restorations because they can be delivered in a single visit and achieve long-term survival rates above 95% for zirconia crowns. The workflow efficiency is critical as case volumes grow, with practices reporting up to 60% chair-time reduction when milling replaces conventional lab work. Developing economies feel the greatest impact because a growing middle class now seeks aesthetic prosthetics rather than extractions. Clinics that adopted same-day solutions report measurable patient preference and willingness to pay premium fees, reinforcing revenue potential for providers.

Rapid Digitization of Dental Workflows

Scanner-to-mill connectivity has accelerated due to cloud platforms that move design files in seconds instead of minutes, allowing remote designers to finalize crowns and bridges while patients remain in the chair[1]Rune Fisker, “2025’s Five Big Digital Dentistry Trends You Need to Know,” 3Shape, 3shape.com. Automated design tools now achieve a 94% acceptance rate for crown proposals, slashing the CAD learning curve and widening access among non-specialist teams. Integrated quality-control routines inside the mill reduce remakes and create a data feedback loop that refines preparations over time. Consequently, clinics view digital transformation less as a discretionary upgrade and more as a requirement for competitive parity.

Expansion of Dental Service Organizations & Centralized Milling Hubs

Consolidation is reshaping production economics. Larger dental service organizations invest in regional centers equipped with industrial-grade five-axis lines that run multiple materials around the clock. Smaller affiliated clinics forward scans through secure portals and receive completed work within twenty-four hours, often by subscription that bundles hardware, software, and logistics. These arrangements lower the capital threshold, allowing practices in cost-sensitive areas to offer premium prosthetics without owning a mill. The hub-and-spoke model also improves throughput consistency by centralizing maintenance and calibration under dedicated teams.

Escalating Demand for High-Aesthetic Materials Requiring Precision Milling

Multi-layer zirconia blocks that blend opacity and translucency now dominate anterior cases, eliminating the esthetic compromises once associated with monolithic crowns. Cutting these materials within 10 microns demands five-axis kinematics and high-stability spindles. Manufacturers answer with auto-tool changers and closed-loop calibration, so even chairside units can mill full-contour bridges. Innovation continues with glass-ceramic hybrids that mimic enamel fluorescence while remaining grindable, further widening the indications possible in a single session.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front & Maintenance Costs of Multi-Axis Mills | -1.6% | Global, with highest impact in developing regions | Short term (≤2 years) |

| Digital Workflow Integration & Training Barriers for Small Clinics | -1.2% | Global, with highest impact in regions with fragmented dental practices | Medium term (2-4 years) |

| Competition from Additive Manufacturing and Outsourced Labs | -0.9% | Global, with early gains in North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Up-Front & Maintenance Costs of Multi-Axis Mills

Entry-level chairside packages start near USD 100,000 before software, training, and facility upgrades are added. Diamond bur replacements can equal 20% of running costs each year, pressuring return-on-investment calculations for low-volume clinics. Leasing and pay-per-restoration schemes are gaining traction, but residual value uncertainties and service commitments still deter some buyers. Capital shortages are more acute in emerging markets, where financing rates remain higher and currency volatility raises import costs. Vendors respond with modular designs that let practices add spindles or tool magazines over time, aligning cash flow with growing case loads.

Digital Workflow Integration & Training Barriers for Small Clinics

Surveys show 68% of dentists find software overlap and data-format conflicts to be primary hurdles. Staff turnover deepens the problem because each new technician faces a three-to-six-month learning curve. Cloud-based design outsourcing partly offsets the skills gap, yet ongoing subscription fees reduce cost savings. Chairside protocol also requires modified preparations to optimize milling accuracy, so dentists must retrain on margin placement and occlusal reduction. These workflow adjustments demand team-wide coordination, which some owner-operators struggle to implement alongside daily patient loads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: In-Lab Systems Retain Volume Leadership while In-Office Segment Accelerates

In-Lab platforms generated 64.40% of 2025 revenue, underscoring their central role in high-capacity laboratories that supply multiple clinics. The typical installation supports multi-material carousels, continuous spindle operation, and automatic disc management, enabling daily output far above chairside units. Laboratories leverage this scale to deliver consistent restorations for broad patient groups, keeping the dental milling machine market anchored in centralized production.

The In-Office category expands at 10.36% CAGR because same-day dentistry improves scheduling and increases case acceptance. Modern compact mills now handle zirconia bridges alongside single crowns, closing the gap with laboratory systems. Practices report that monthly production doubles within four months of adoption as teams gain confidence in digital steps. This productivity spike strengthens the economic case for ownership, sustaining robust demand.

By Axis Configuration: Five-Axis Precision Drives Complex Indications

Four-axis equipment held 55.30% of the dental milling machine market share in 2025 due to affordability and ease of use, offering sufficient articulation for standard crowns and inlays. Users appreciate straightforward toolpaths and shorter setup times that support lean laboratory operations.

Five-axis solutions, however, expand at 11.55% CAGR because they cut undercuts, screw-access channels, and full-arch frameworks without repositioning. The extra degrees of freedom improve cervical fit and margin integrity, reducing chairside adjustments after delivery. Laboratories that incorporate five-axis stations secure more implant and aesthetic work, a profitable niche that propels equipment upgrades across the dental milling machine industry.

By Size: Stand-Alone Units Power High-Volume Hubs

Bench-top units captured 40.40% of sales in 2025 because they blend performance with manageable footprints, fitting easily into most laboratories. Their modular chassis accepts multiple material holders, covering everyday clinical indications.

Stand-alone mills drive the fastest growth at 12.05% CAGR, particularly inside regional hubs serving dental service organizations. These floor-standing machines run simultaneously with twin spindles and integrated loaders, pushing throughput to industrial levels. Operators value the unattended night-shift capability that leverages lower energy tariffs, supporting cost-efficient scaling of the dental milling machine market.

By Technology: CAD/CAM Remains the Core of Digital Dentistry

CAD/CAM maintained 81.35% revenue share in 2025 and is forecast to grow 9.45% each year as digital impressions become the default record. The integration of artificial intelligence into design modules means a single technician can now finalize dozens of cases daily with consistent quality.

Copying milling continues its gradual retreat, limited to regions with minimal scanner penetration. Even hold-out users acknowledge the convenience of digital storage and instant case duplication across multiple sites. Connectivity priorities now sit at the software layer, where open-architecture platforms let clinics pair any scanner with any mill, expanding the accessible base for the dental milling machine market.

By End-User: Laboratories Dominate yet Clinics Gain Momentum

Laboratories processed 72.20% of total case volume in 2025, benefiting from specialized staffing and round-the-clock operation. Many labs differentiate through exotic materials such as multilayer zirconia or lithium-disilicate sub-structures and maintain direct ties to material suppliers for updates.

Clinics post a 12.44% CAGR by integrating chairside milling into routine workflows that enhance patient convenience. Real-time communication between scanners, mills, and ovens shortens appointment cycles, encouraging practitioners to offer premium restorations without external collaboration. Hybrid models emerge, with laboratories installing chairside devices inside partner clinics to secure volume while reducing courier costs, further broadening the dental milling machine market.

Geography Analysis

North America contributed 37.60% of global revenue in 2025, supported by sophisticated insurance reimbursement and early CAD/CAM rollout. Approximately 15% of clinics perform in-office milling, and service organizations have standardized equipment procurement to streamline support contracts. Capital spending also benefits from favorable leasing conditions that make hardware renewal predictable every five years.

Europe stands as the second-largest region, with regulatory harmonization accelerating product launches. German and Scandinavian manufacturers pioneer multi-layer zirconia and energy-efficient spindles that appeal to laboratories focused on sustainability. Strict data-privacy rules encourage vendors to build secure cloud connectors, improving adoption among practice networks that exchange designs across borders. The dental milling machine market here is shaped by independent labs that stress craft quality, creating demand for precision upgrades rather than outright capacity expansion.

Asia-Pacific records a 12.95% CAGR, the fastest worldwide, fueled by rising disposable income and vibrant dental tourism in Thailand and India. China quickly scales domestic production, narrowing the technology gap with Western incumbents, while Japan applies its expertise in precision engineering to develop compact five-axis mills tailored for small urban clinics. Public health initiatives in several countries now reimburse CAD/CAM crowns, spurring clinics to add mills. Middle East and Africa and South America show moderate growth; Brazil leads South America due to its established dental manufacturing cluster, whereas Gulf Cooperation Council nations invest heavily in modern clinics aimed at medical tourists.

Competitive Landscape

The dental milling machine market shows moderate concentration as large conglomerates integrate scanner-to-mill ecosystems through acquisitions, yet niche entrants continue to innovate. Product roadmaps emphasize automation; automatic tool changers, intelligent spindle torque control, and integrated vision systems reduce manual intervention. Material compatibility has become a differentiator, with some vendors optimizing firmware for hybrid ceramics while others partner with zirconia disc producers to guarantee shade match.

Open-architecture strategies gain momentum because laboratories and clinics demand flexibility across scanners, CAD packages, and furnaces. Vendors offering locked ecosystems face pushback unless they offset constraints with value-added services such as remote diagnostics and guaranteed uptime. Subscription finance reshapes access: monthly bundles that combine hardware, software, updates, and service lower entry barriers for smaller operations and simplify budgeting for large service organizations.

Competitive dynamics now focus on workflow analytics. Machines that collect spindle load, bur wear, and job timing feed cloud dashboards that managers use to predict consumable orders and schedule preventive maintenance. Companies leveraging this data layer differentiate on operational insights rather than raw hardware speed, carving a defensible niche in the evolving dental milling machine market.

Dental Milling Machine Industry Leaders

Dentsply Sirona

Institut Straumann AG

Planmeca Oy.

Solventum Corporation

Roland DG Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Roland DGA’s DGSHAPE Americas introduced the DWX-43W wet mill featuring filter-free coolant management and faster cycle times.

- February 2025: Amann Girrbach partnered with Panthera to distribute Fusion Bar solutions, enabling Ceramill users to access validated titanium workflows.

- October 2024: Roland DGA launched the DWX-53D dry mill with productivity and precision upgrades over its predecessor.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the dental milling machine market as all computer-guided, subtractive devices that carve prosthetic restorations from digital design files in laboratories or chairside settings, measured only by the sale value of new units and related manufacturer software licenses. Machines dedicated to ceramics, polymers, or metal blocks and discs, across 4- and 5-axis configurations, are covered while refurbished equipment and standalone CAD design stations remain outside scope.

Scope Exclusion: used or refurbished mills, as well as purely additive dental printers, are not included.

Segmentation Overview

- By Machine Type

- In-Lab Milling Machines

- In-Office Milling Machines

- By Axis Configuration

- 4-Axis Machines

- 5-Axis Machines

- By Size

- Table-top

- Bench-top

- Stand-alone

- By Technology

- CAD/CAM Milling

- Copying Milling

- By End-User

- Dental Laboratories

- Dental Clinics (Chair-side)

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Conversations with dental lab owners, chairside-focused clinicians, and regional distributors spanning North America, Europe, and high-growth Asian cities helped us verify typical selling prices, 4-axis to 5-axis migration rates, and country-specific reimbursement triggers. Follow-up surveys captured expected replacement intent and average units per multi-site dental support organization.

Desk Research

Mordor analysts began with public datasets from agencies such as the US FDA 510(k) database, Eurostat's Prodcom codes for dental machinery, and UN Comtrade HS-codes that capture exports of CN 845811 products. Trade-group white papers from the American Dental Association and the German VDDI detailed unit replacement cycles, while peer-reviewed work in the Journal of Prosthetic Dentistry guided average spindle-hour utilization. Company 10-Ks, investor decks, and patent landscapes from Questel added pricing and technology lifecycles. D&B Hoovers supplied revenue splits for privately held milling vendors. This list is illustrative; many other open and paid sources were reviewed for cross-checks.

Market-Sizing & Forecasting

We rebuilt 2024 country revenue using a top-down "production + net trade" reconstruction, then validated totals with bottom-up spot checks of supplier shipments and sampled average selling price × volume. Key variables include i) installed chairside scanner base, ii) prosthetic crown volumes, iii) CAD/CAM penetration in labs, iv) import tariff shifts on precision machinery, and v) 5-axis price premiums. Forecasts to 2030 employ multivariate regression where crown volumes, scanner base growth, and GDP per capita explained over 90% of variance, with ARIMA smoothing for short-term shocks. Where distributor roll-ups under-reported by >10%, values were gap-filled using regional ASP medians and shipment trends.

Data Validation & Update Cycle

Outputs are compared with independent shipment indices and ADA equipment surveys; anomalies trigger a senior analyst review before sign-off. Mordor refreshes each model annually, issuing interim updates for material recalls or merger events, ensuring clients receive the latest vetted baseline.

Why Mordor's Dental Milling Machine Baseline Commands Confidence

Published estimates often diverge because firms select different device classes, refresh cadences, and pricing stacks.

Key gap drivers include whether chairside mills are grouped with broader CAD/CAM systems, currency conversion years, and the use of aggressive unit growth multipliers that our interviews did not corroborate. Mordor reports the base-year 2025 value at USD 2.64 billion [mordorintelligence.com].

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.64 bn (2025) | Mordor Intelligence | - |

| USD 2.16 bn (2024) | Global Consultancy A | Excludes chairside mills and applies 2020 ASPs |

| USD 0.98 bn (2025) | Industry Journal B | Counts only North America & Europe, then projects globally |

| USD 2.98 bn (2025) | Regional Consultancy C | Uses shipment growth without adjusting for falling ASPs |

In sum, by aligning scope strictly to new units, triangulating trade data with field pricing, and revisiting assumptions each year, Mordor Intelligence delivers a balanced, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the dental milling machine market and its growth outlook?

The market is valued at USD 2.85 billion in 2026 and is projected to reach USD 4.18 billion by 2031, reflecting a 7.97% CAGR.

Why are five-axis milling machines gaining popularity?

They deliver sub-10-micron accuracy for complex geometries, enabling full-arch restorations and implant components that require undercut machining.

Which end-user segment adopts milling technology most rapidly?

Dental clinics are the fastest-growing segment, expanding at a 12.44% CAGR as same-day dentistry becomes a key differentiator.

How do subscription and leasing models influence market adoption?

These financing options reduce up-front capital requirements, helping smaller practices access digital workflows without large cash outlays.

Which region shows the highest growth rate through 2031?

Asia-Pacific leads with a forecast 12.95% CAGR, driven by expanding healthcare infrastructure and dental tourism.

What are the main barriers stopping small clinics from installing mills?

High equipment costs, ongoing maintenance expenses, and the learning curve for digital design and workflow integration remain primary hurdles.

Page last updated on: