Denmark Software As A Service (SaaS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

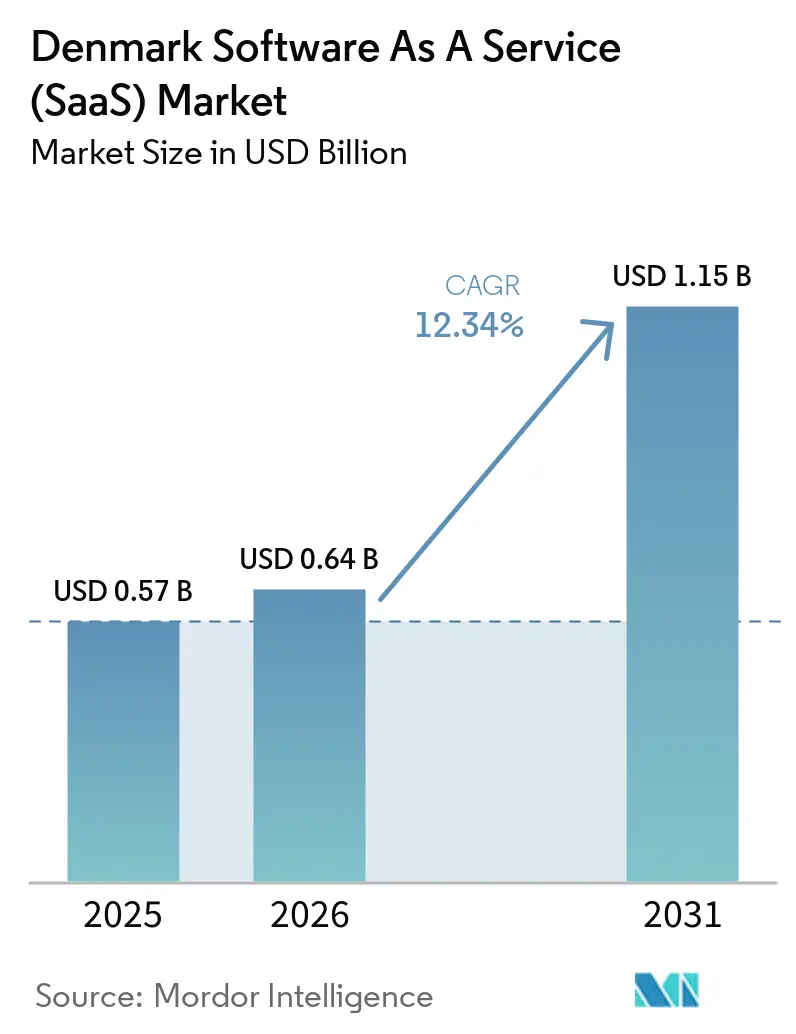

| Base Year Market Size (2025) | USD 0.57 Billion |

| Market Size (2026) | USD 0.64 Billion |

| Market Size (2031) | USD 1.15 Billion |

| Growth Rate (2026 - 2031) | 12.34% CAGR |

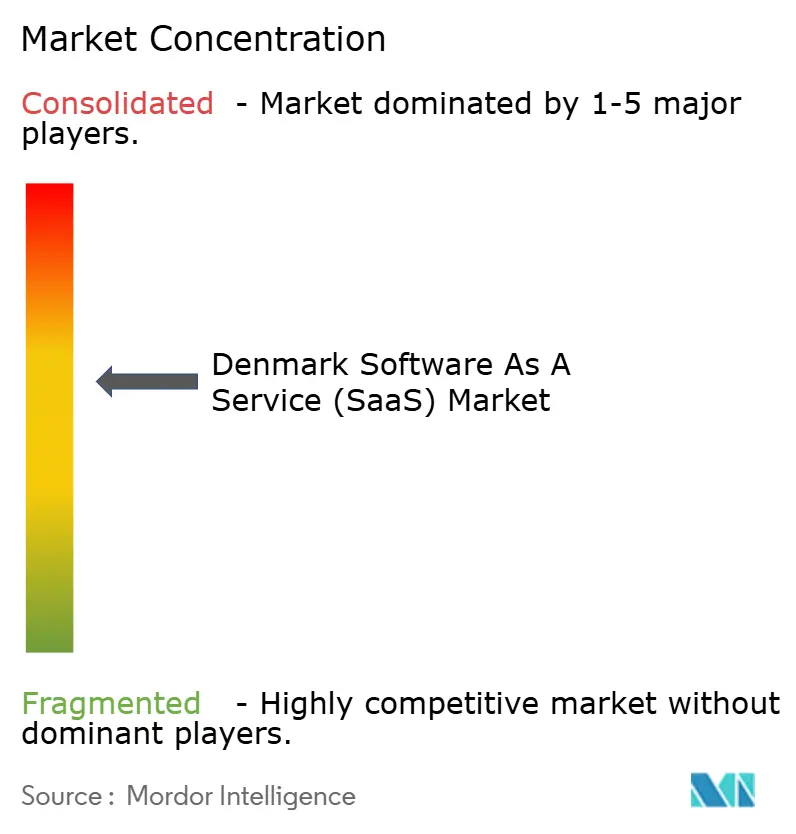

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Software As A Service (SaaS) Market Analysis by Mordor Intelligence

Denmark SaaS market size in 2026 is estimated at USD 0.64 billion, growing from 2025 value of USD 0.57 billion with 2031 projections showing USD 1.15 billion, growing at 12.34% CAGR over 2026-2031. Rising demand for data-sovereign cloud services, regulatory tailwinds such as mandatory PEPPOL e-invoicing, and heavy public-sector digital spending are accelerating adoption across all enterprise sizes. Copenhagen’s emergence as a green data-center hotspot, coupled with Denmark’s advanced e-government infrastructure, is drawing both domestic and international vendors to localize offerings. Increasing venture capital inflows into Danish cloud-native start-ups, together with EU-wide privacy mandates, continue to widen the addressable base for subscription software. Simultaneously, concerns over vendor lock-in, high Nordic electricity costs, and a looming IT-skills gap are reshaping buying behaviors and sparking consolidation among well-capitalized players.

Key Report Takeaways

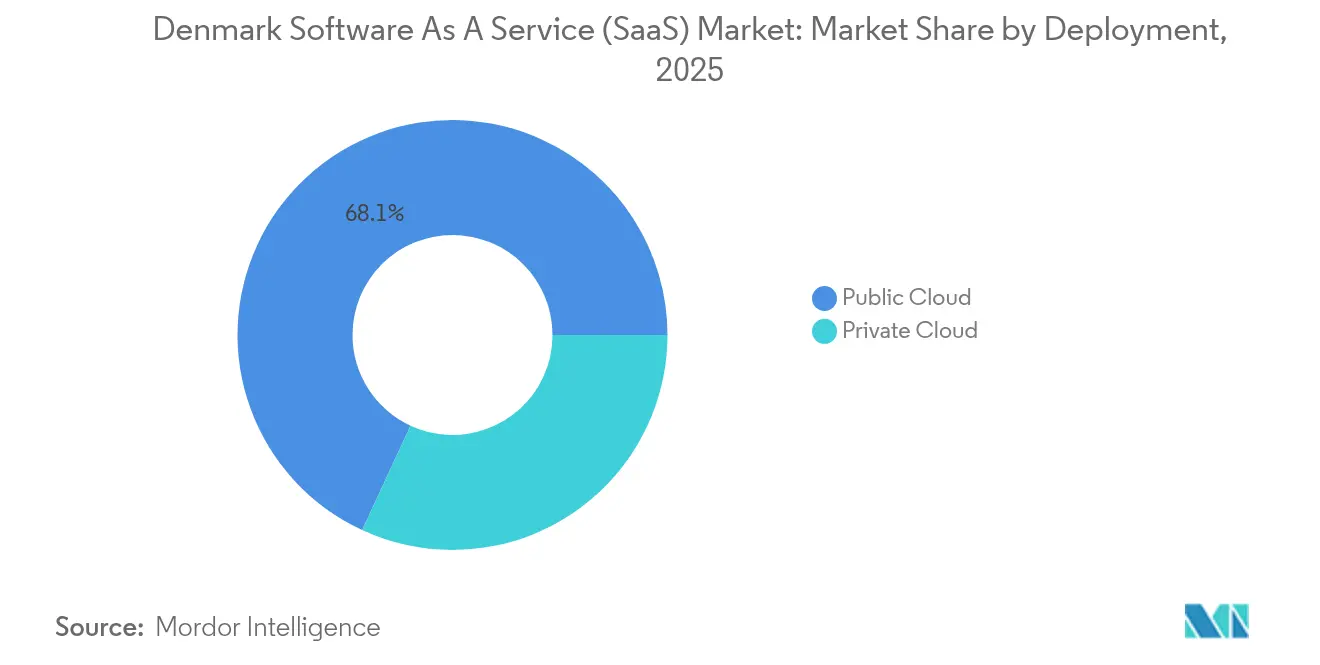

- By deployment, the public cloud held a 68.10% revenue share of the Denmark SaaS market in 2025, while the private-cloud model is forecast to expand at an 17.89% CAGR through 2031.

- By enterprise size, SMEs accounted for 58.35% of the Denmark SaaS market share in 2025; the same cohort is set to grow at 16.1% CAGR to 2031.

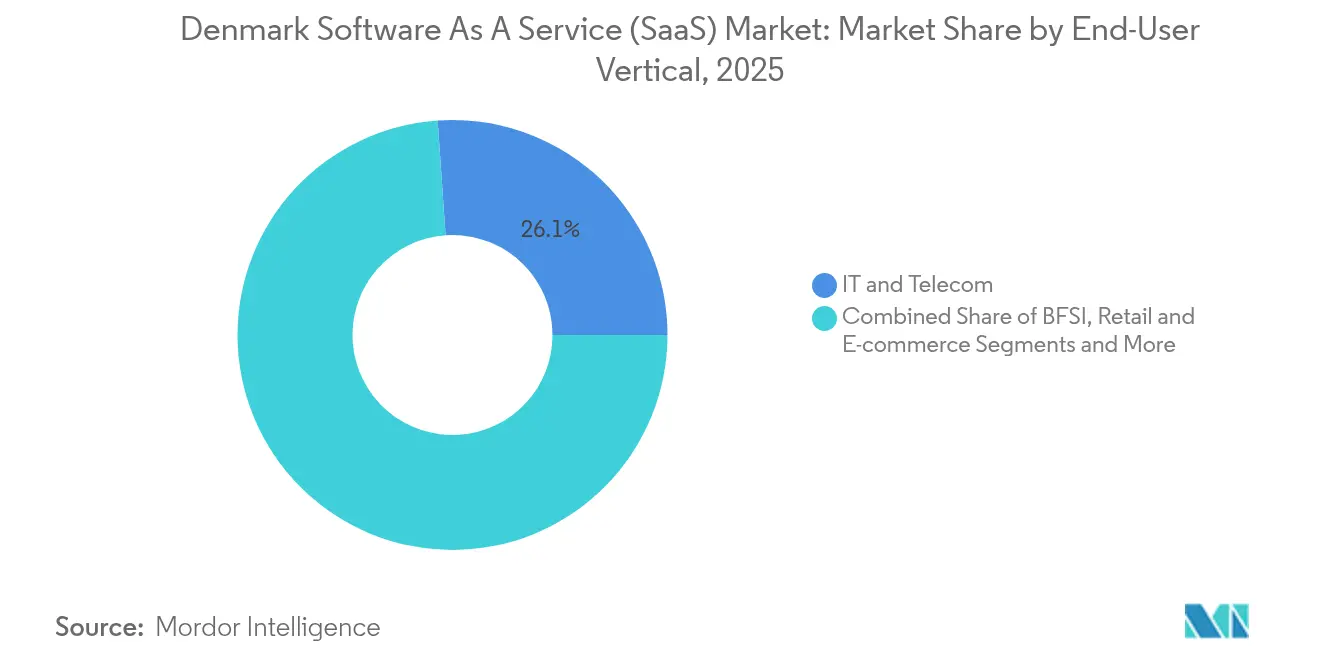

- By end-user vertical, IT and Telecom captured 26.10% revenue share in 2025, whereas Healthcare and Life Sciences is advancing at 17.45% CAGR through 2031.

- By functional application, Customer Experience and CRM generated 22.10% of the Denmark SaaS market size in 2025, while Cybersecurity and Backup solutions are projected to rise at 18.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Denmark representing one among them. The global report on software as a service market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Denmark Software As A Service (SaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mobile-first digitisation across Danish SMEs | +2.1% | National, concentrated in Copenhagen and Aarhus | Medium term (2-4 years) |

| Rapid growth of cloud-native start-ups and VC inflows | +1.8% | National, with spillover to Nordic region | Short term (≤ 2 years) |

| National "Digital Denmark" e-government programmes | +2.3% | National, public sector led | Long term (≥ 4 years) |

| EU GDPR-driven demand for compliance-focused SaaS | +1.6% | EU-wide, early adoption in Denmark | Medium term (2-4 years) |

| Fast-track permitting for green data-centre builds | +1.4% | National, rural areas prioritized | Long term (≥ 4 years) |

| Mandatory PEPPOL/B2B e-invoicing rollout | +2.2% | National, phased by company size | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile-First Digitisation Across Danish SMEs

Denmark's SME sector is experiencing a fundamental shift toward mobile-first SaaS adoption, driven by the country's 96% smartphone penetration rate and government initiatives that mandate digital-by-default interactions with public authorities.[1]“Denmark in Figures – Smartphone Penetration,” Ministry of Foreign Affairs, denmark.dk This transformation extends beyond basic digitalization to encompass sophisticated workflow automation, with companies like Dynaccount reporting a 43% increase in customer acquisition in 2024 as businesses seek integrated accounting and automation solutions. The mobile-first approach is particularly pronounced in the retail and service sectors, where Danish companies are leveraging SaaS platforms to bridge physical and digital customer touchpoints. SMEs are increasingly adopting cloud-native solutions that eliminate the need for on-premise infrastructure, with mobile accessibility becoming a non-negotiable requirement rather than a value-added feature.

National "Digital Denmark" E-Government Programmes

Denmark's position as the world's second-most digital government creates a unique market dynamic where public sector digitalization requirements cascade into private sector SaaS demand patterns. The government's Digital Growth Strategy allocates USD 138 million through 2027 specifically for enhancing digital services, cybersecurity infrastructure, and SME digital capabilities, creating a multiplier effect that extends far beyond direct government procurement. This comprehensive approach includes 28 specific initiatives ranging from personalized data permission management to digital powers of attorney, establishing Denmark as a testing ground for advanced digital governance models that other EU nations are likely to replicate. The e-government programs are particularly significant because they establish technical standards and security requirements that become de facto market requirements for SaaS providers serving Danish enterprises. The ripple effect extends to B2B relationships, where companies must adopt compatible SaaS solutions to maintain seamless interactions with government systems, creating a network effect that accelerates overall market adoption.

EU GDPR-Driven Demand for Compliance-Focused SaaS

The intersection of GDPR compliance requirements and Denmark's data sovereignty initiatives is creating a distinct market segment for privacy-first SaaS solutions that can operate within strict European regulatory frameworks. Danish companies are increasingly prioritizing SaaS providers that offer built-in compliance features, data residency controls, and transparent audit trails, moving beyond basic GDPR compliance to embrace privacy-by-design architectures. This trend is amplified by the upcoming EU AI Act, which requires Danish businesses to implement AI literacy programs and governance frameworks, creating demand for SaaS solutions that integrate compliance monitoring and risk management capabilities. The regulatory landscape is driving consolidation among SaaS providers, as smaller vendors struggle to maintain compliance across multiple jurisdictions while larger platforms invest heavily in regulatory technology capabilities. Danish enterprises are willing to pay premium pricing for SaaS solutions that reduce compliance risk, with many companies viewing regulatory adherence as a competitive advantage rather than a cost center.

Mandatory PEPPOL/B2B E-Invoicing Rollout

Denmark's phased implementation of mandatory B2B e-invoicing represents one of Europe's most comprehensive digital transformation mandates, affecting approximately 118,000 entities by January 2026 and creating immediate demand for compliant SaaS solutions. The requirement for OIOUBL format compliance and Peppol BIS Billing 3.0 standards is driving rapid adoption of integrated financial management SaaS platforms that can handle complex invoicing workflows while maintaining audit trails.[2]“Data Act and GDPR Guidance,” European Commission, ec.europa.eu This mandate extends beyond simple invoicing to encompass comprehensive digital bookkeeping requirements, forcing traditional paper-based businesses to adopt cloud-based financial management systems within compressed timeframes. The rollout is creating opportunities for SaaS providers that can offer seamless integration with existing ERP systems while ensuring compliance with both Danish national standards and broader EU regulations. Companies that delay compliance face significant operational disruptions, creating a captive market for SaaS solutions that can accelerate implementation timelines and reduce regulatory risk.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vendor lock-in and limited customisation for mid-market buyers | -1.9% | National, affecting mid-market enterprises | Medium term (2-4 years) |

| Heightened data-sovereignty and cybersecurity concerns | -1.7% | National, with EU regulatory influence | Long term (≥ 4 years) |

| Scarcity of Danish-language Gen-AI talent | -1.3% | National, concentrated in tech hubs | Short term (≤ 2 years) |

| High Nordic electricity prices squeezing SaaS gross margins | -1.1% | Nordic region, affecting infrastructure costs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vendor Lock-In and Limited Customisation for Mid-Market Buyers

Mid-sized Danish companies deploy an average of 110 cloud apps, yet many find exit clauses, data-portability options, and API extensibility inadequate. Rising subscription fees outpacing inflation are prompting procurement teams to negotiate multi-vendor frameworks and favour open-standards architectures. Systems integrators now market “composable” SaaS stacks that decouple data storage from application logic, but such designs often demand stronger in-house DevOps skills than mid-market firms possess. This restraint tempers Denmark SaaS market expansion rates, especially in verticals with legacy ERP footprints that are expensive to migrate.

Scarcity of Danish-Language Gen-AI Talent

Projections show a 19,000 IT-specialist shortfall by 2030, with AI and machine-learning roles hardest hit.[3]“Denmark Is Facing a 19,000 IT Specialist Shortage,” Grid Dynamics, griddynamics.com Only 5% of large enterprises have progressed beyond AI pilot projects, largely because few data scientists can fine-tune models for Danish grammar and cultural context. Vendors embedding multilingual chatbots or document-automation engines therefore struggle to guarantee accuracy in Danish, slowing feature roadmaps. Although universities are ramping applied-AI curricula, meaningful relief is unlikely within two years, restraining the pace at which advanced capabilities permeate the Denmark SaaS market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Private Cloud Gains Momentum

Private-cloud subscriptions are expanding at an 17.89% CAGR, despite public-cloud installations capturing 68.10% of 2025 revenue within the Denmark SaaS market. Municipal moves to eliminate US-hosted productivity suites and the prevalence of sensitive workloads in finance and healthcare explain the shift toward sovereign hosting models. Energy-efficient data centres in Fredericia and other rural zones allow enterprises to localise data without forfeiting scalability, underpinning sustained private-cloud demand through 2031.

Hybrid patterns are also on the rise: firms keep regulated datasets in private clusters while bursting seasonal analytics jobs to hyperscale clouds powered by Danish wind energy. Edge locations near offshore wind farms further lower latency for industry-4.0 use cases. As EU-level data-transfer rules tighten, Danish CIOs view private-cloud enclaves as strategic insurance, reinforcing their allocation within overall Denmark SaaS market spending.

By Enterprise Size: SMEs Drive Market Expansion

SMEs generated 58.35% of 2025 revenue and will grow at 16.1% CAGR, making them the principal engine of Denmark SaaS market expansion. Digital-first public services force micro-businesses to submit tenders, payroll, and tax filings online, pushing even the smallest shops onto subscription platforms. Cloud-based tools with preset workflows appeal to firms lacking in-house IT and enable instant compliance with archiving and audit rules.

Large enterprises remain influential reference customers, piloting AI-enabled modules and negotiating volume-licence discounts that later trickle down through reseller channels. As firms like Novo Nordisk publicly share ROI metrics from ERP-modernisation projects, smaller suppliers adopt the same SaaS suppliers to align data formats for seamless B2B interaction. Government vouchers covering up to 50% of onboarding costs further widen SME access to advanced SaaS suites, deepening market penetration.

By End-User Vertical: Healthcare Leads Innovation

Healthcare and Life Sciences is set to post 17.45% CAGR through 2031, leveraging consolidated electronic health records that ease SaaS integration with national portals such as Sundhed.dk. Telehealth scheduling, e-prescription fulfillment, and AI-assisted diagnostics rank among top procurement priorities, lifting vertical demand for secure APIs and real-time analytics. IT and Telecom keeps overall revenue leadership at 26.10% due to self-consumption of DevOps and collaboration suites that underpin broader digital infrastructure.

Banking and fintech spending is accelerating as new capital adequacy and anti-money-laundering directives require continuous monitoring and reporting. Manufacturing plants adopt SaaS-based OEE dashboards to predict downtime, while retail chains deploy unified commerce platforms with embedded payments. Diverse adoption patterns collectively reinforce the Denmark SaaS market’s resilience across macro cycles.

By Functional Application: Security Solutions Accelerate

Cybersecurity and Backup applications will grow at 18.55% CAGR, fueled by USD 226 million of national cybersecurity funding and Europe-wide upticks in ransomware incidents microsoft.com. Zero-trust access, immutable backups, and continuous compliance scanning top CIO shopping lists. Customer Experience and CRM retained 22.10% share of the Denmark SaaS market size in 2025, as omnichannel engagement remains central to revenue diversification.

Spend-management tools gain relevance from mandatory e-invoicing, while HR suites expand via skills-gap analytics modules that help businesses forecast recruitment needs in tight labor markets. Content-automation vendors integrate e-signature, redaction, and archival features to support both GDPR and local bookkeeping statutes. The functional mix demonstrates heightened buyer sophistication, moving beyond single-purpose apps toward integrated, compliance-ready platforms.

Geography Analysis

Denmark’s SaaS activity clusters around Copenhagen and Aarhus, which together host roughly 60% of domestic cloud development and engineering roles. Dense talent pools shorten release cycles and nurture peer networks that accelerate best-practice diffusion across the Denmark SaaS market. Yet government incentives for rural data-centre build-outs are starting to distribute workloads more evenly, mitigating urban congestion and lowering real-estate overheads.

International connectivity is another geographic asset. Sub-sea cables linking Jutland to Germany, the Netherlands, and Norway give Danish vendors low-latency access to 100-million-plus potential users, turning the domestic market into a launchpad for broader EU expansion. EU Digital Single Market rules further simplify cross-border subscription sales, so Danish ISVs increasingly architect products with multilingual interfaces and VAT-compliant pricing engines from day one.

The presence of hyperscale, renewable-powered facilities by Google and Microsoft strengthens Denmark’s branding as a green cloud corridor. The expansion of Denmark Data Center infrastructure are supported by renewable-powered hubs and sovereign cloud investments. This stature attracts foreign SaaS firms to establish regional points of presence, enriching local ecosystems with new partnerships and second-tier suppliers. However, energy-price volatility across the Nordic grid remains a watch item, as higher utility bills could erode the cost advantages of domestic hosting over time.

Competitive Landscape

The Denmark SaaS market displays moderate concentration, with local scale-ups rapidly approaching unicorn status while global acquirers scout for compliance-ready assets. Visma’s acquisition of Penneo solidifies digital-signing dominance and signals continued Nordic roll-ups, whereas Acquia’s purchase of Monsido extends accessibility tooling deeper into enterprise CMS workflows. Valuations of Pleo (USD 4.7 billion) and Siteimprove (USD 112 million revenue) underscore investor confidence in Danish product-led growth models.

Competitive strategy splits along two paths. Deep vertical specialists like Factbird double down on domain expertise, embedding AI to boost manufacturing OEE metrics. Horizontal platform builders such as Visma and Ageras leverage cash reserves to consolidate fragmented functions—ranging from payroll to KYC—into single login experiences. In turn, smaller vendors differentiate through native Danish language support or industry-specific compliance blueprints, hoping to retain niche segments before platform giants broaden coverage.

Denmark Software As A Service (SaaS) Industry Leaders

Zendesk, Inc.

Siteimprove A/S

Pleo Technologies ApS

Templafy A/S

Falcon.io A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Visma completed its acquisition of Penneo with >90% shareholder approval at DKK 16.50 per share, bolstering Nordic digital-signing capabilities.

- January 2025: Acquia finalized its purchase of Danish SaaS firm Monsido, integrating accessibility analytics into its digital-experience platform.

- April 2024: Ageras raised EUR 82 million to fund acquisitions that expand its SME software suite across banking, accounting, and payroll in Northern Europe.

- January 2024: Keepit secured USD 40 million in refinancing from HSBC Innovation Banking to scale its data-protection and backup services globally.

Denmark Software As A Service (SaaS) Market Report Scope

Software as a service (SaaS) is a cloud computing service model where the provider offers use of application software to a client and manages all needed physical and software resources. Any kind of SaaS business including subscription-based service, web-based software, and hosted software application can benefit from this marketing strategy.

The denmark software as a service (SaaS) market is segmented by deployment (public cloud, private cloud, hybrid cloud), by enterprises (SMEs, large enterprises), by end-user vertical (IT and telecom, BFSI, retail, healthcare, manufacturing, other end-user verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Public Cloud |

| Private Cloud |

| SMEs |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Manufacturing |

| Others (Education, Public Sector, Media) |

| Customer Experience and CRM |

| Finance and Spend Management |

| HR and Talent Management |

| Content and Document Automation |

| Cyber-security and Backup |

| Marketing Automation and Analytics |

| By Deployment | Public Cloud |

| Private Cloud | |

| By Enterprise Size | SMEs |

| Large Enterprises | |

| By End-user Vertical | IT and Telecom |

| BFSI | |

| Retail and E-commerce | |

| Healthcare and Life Sciences | |

| Manufacturing | |

| Others (Education, Public Sector, Media) | |

| By Functional Application | Customer Experience and CRM |

| Finance and Spend Management | |

| HR and Talent Management | |

| Content and Document Automation | |

| Cyber-security and Backup | |

| Marketing Automation and Analytics |

Key Questions Answered in the Report

What is the current value of the Denmark SaaS market?

The market is valued at USD 0.64 billion in 2026 and is forecast to reach USD 1.15 billion by 2031.

Which deployment model is growing fastest in Denmark?

Private-cloud subscriptions lead growth at an 17.89% CAGR due to data-sovereignty and compliance priorities.

Why are Danish SMEs pivotal to future SaaS adoption?

SMEs hold 58.35% revenue share and benefit from government digital mandates and subsidies that lower onboarding costs.

How will mandatory PEPPOL e-invoicing affect SaaS demand?

Approximately 118,000 firms must adopt compliant invoicing software by January 2026, making SaaS bookkeeping platforms indispensable.

Page last updated on: