Degaussing Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

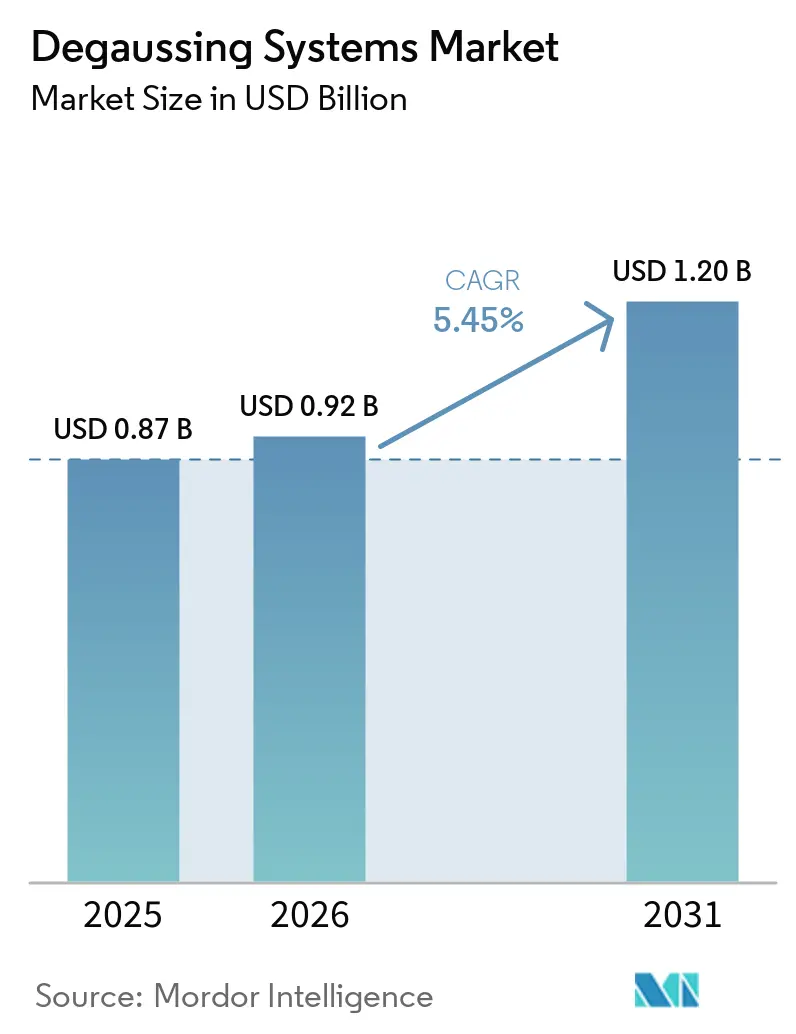

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.20 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Degaussing Systems Market Analysis by Mordor Intelligence

The degaussing systems market size is expected to grow from USD 0.87 billion in 2025 to USD 0.92 billion in 2026 and is forecasted to reach USD 1.2 billion by 2031 at a 5.45% CAGR over 2026-2031. Momentum rests on two counter-vailing forces. First, the expansion of magnetic-influence sea mines across contested chokepoints pushes navies to cut their magnetic signatures. Second, constrained capital budgets encourage life-extension upgrades on proven hulls instead of commissioning entirely new ships. The degaussing systems market, therefore, expands each time a fleet commander selects a cost-effective retrofit over a new-build destroyer or submarine. Growth also concentrates around software-driven control suites that use real-time data to fine-tune coil output, raising suppression efficiency while trimming power demand. Regionally, North America leads current revenue, yet Asia-Pacific adds hulls fastest as China, India, and South Korea push signature-management mandates across every new surface combatant.

Key Report Takeaways

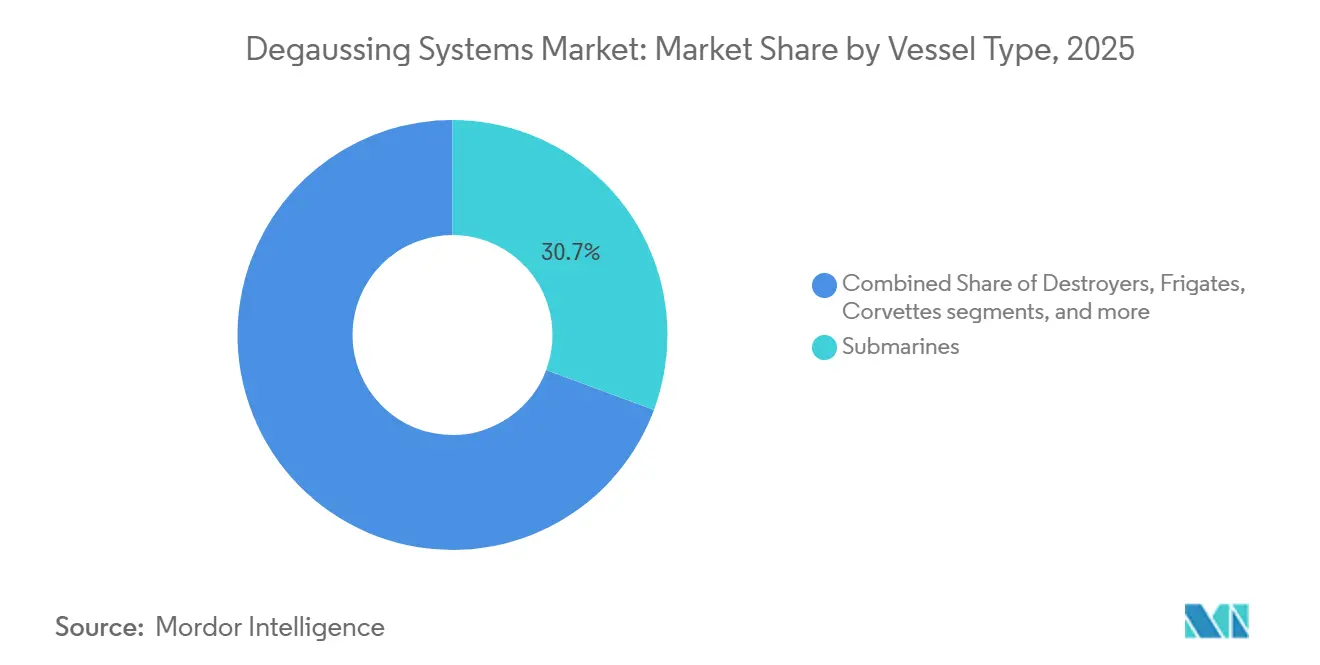

- By vessel type, submarines led with 30.67% revenue share in 2025, while mine countermeasure vessels are forecast to expand at a 7.65% CAGR through 2031.

- By solution, degaussing commanded a 61.25% share in 2025, while deperming is forecast to advance at a 6.27% CAGR through 2031.

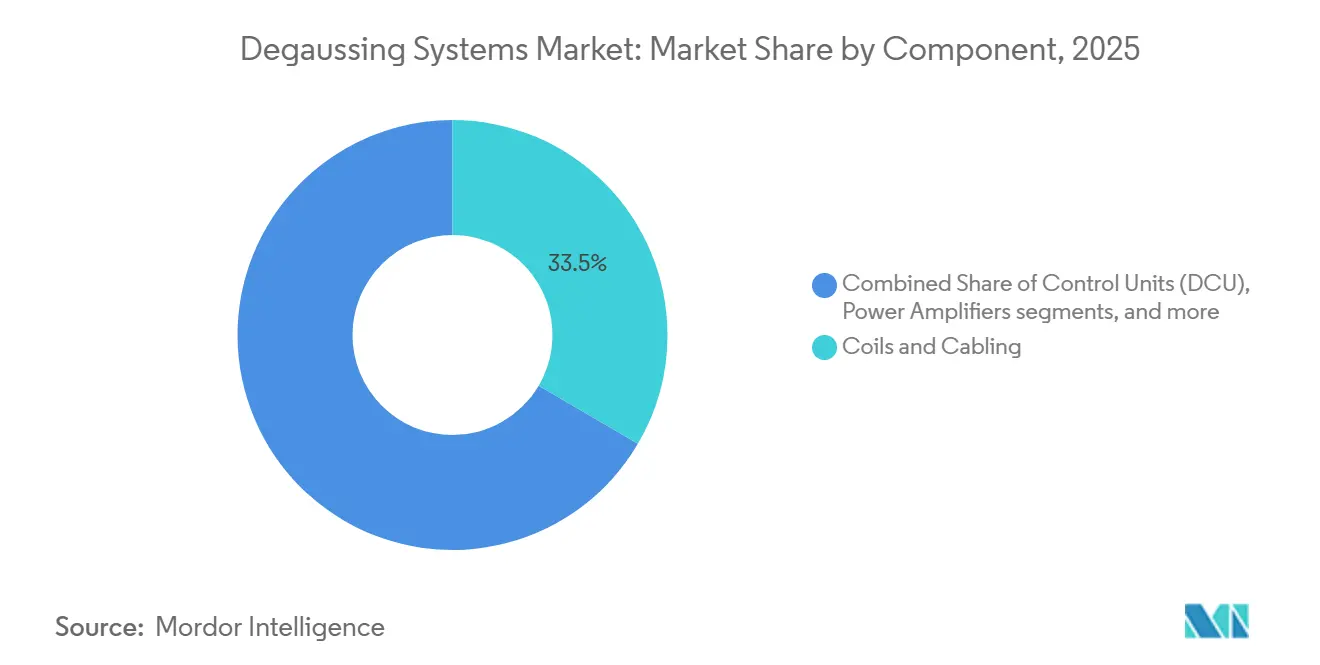

- By component, coils and cabling accounted for 33.45% in 2025, while software and analytics are forecast to grow at a 7.87% CAGR through 2031.

- By installation, retrofit held a 53.76% share in 2025 and is projected to grow at a 7.38% CAGR through 2031.

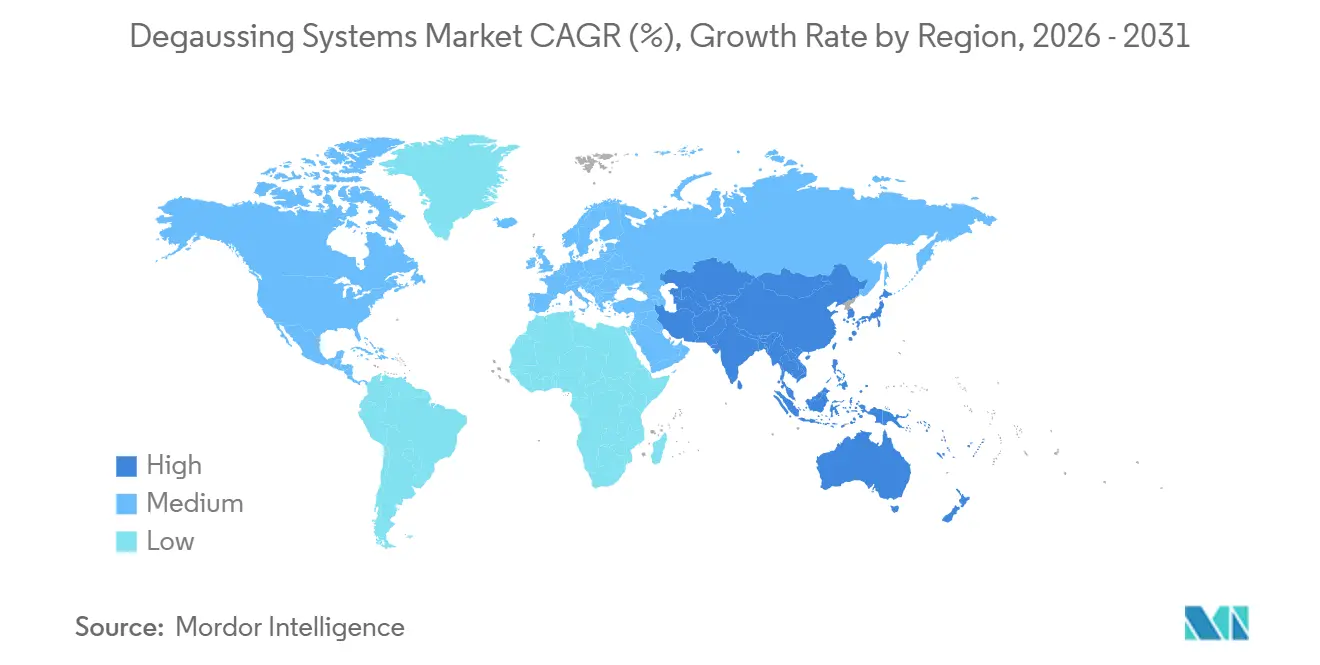

- By geography, North America held 35.65% in 2025, while Asia-Pacific is projected to grow at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Degaussing Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising naval modernization budgets accelerating investment in degaussing systems | +1.2% | Global, concentrated in North America, Asia-Pacific | Medium term (2-4 years) |

| Increased deployment of magnetic-influence sea mines driving demand for magnetic signature control | +0.9% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Expansion of retrofit initiatives targeting older surface vessels for degaussing upgrades | +0.8% | Global, early gains in North America, Europe | Medium term (2-4 years) |

| Emergence of high-temperature superconducting (HTS) coil technology enabling compact and efficient systems | +0.7% | North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Integration of AI-powered adaptive algorithms for real-time signature management | +0.6% | Asia-Pacific, North America | Medium term (2-4 years) |

| Growing requirement for micro-degaussing systems in stealthy unmanned surface and underwater vehicles | +0.5% | Global, concentrated in Asia-Pacific, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Naval Modernization Budgets Accelerate Procurement

Higher defense investment is reinforcing multi-year shipbuilding and sustainment programs that bundle degaussing upgrades with combat-system refresh. The US allocates USD 384.3 billion for FY2026 defense investment, with USD 65 billion directed to shipbuilding and maritime systems, including survivability and signature-management work on surface combatants.[1]US Department of Defense, “Fiscal Year 2026 Budget Materials,” comptroller.defense.gov Canada’s 2026 defense industrial strategy emphasizes a build-partner-buy approach, aligning national shipbuilding roadmaps with electromagnetic-compatibility standards for surface ships. NATO members are also introducing AI-enabled capabilities around ship platforms, signaling that modernizations increasingly combine hardware and software for real-time field control. The degaussing systems market benefits as navies move more hulls through upgrade docks and sync ranging, deperming, and onboard-coil recalibration with other mission package work. Near-term buys in North America and faster growth in Asia-Pacific are the central volume drivers for the degaussing systems market through 2031.

Magnetic-Influence Sea Mines Propel Signature Control Demand

The Defense Intelligence Agency has evaluated that North Korea possesses a significant stockpile of naval mines, which include influence mines equipped with magnetic fuzes, which can cause imminent danger to surface warships in restricted areas. The threat from mines is equally present in the South China Sea, where shallow waters can enhance the effectiveness of bottom- and moored-mine hazards. To address these mine risks, the US Navy awarded contracts to RTX Corporation and Textron Inc. in 2025 for mine countermeasure payloads through the Naval Sea Systems Command, which is part of modular mine-sweeping equipment carried by Littoral Combat Ships, where it is critical to control magnetic signatures from these vessels. At the same time, Chinese research and development activities, as noted in various studies, on rubidium-based quantum magnetometers highlight the importance of controlling magnetic signatures, even from degaussing-equipped vessels.

Expansion of Retrofit Initiatives Targeting Older Surface Vessels for Degaussing Upgrades

Retrofit programs outpace new-build installations because they deliver faster, cheaper resilience on ships that remain in service for decades. Government reviews continue to highlight acquisition timelines that span many years, pushing fleets to extract more value from existing hulls through mid-life upgrades. In that context, navies schedule degaussing refresh during planned maintenance windows to lower risk and cost while achieving measurable signature gains at sea. Retrofit dominance is also linked to ranging and calibration cycles that can be planned around deployments, reducing operational downtime compared to waiting for a new-build delivery slot. Vendors have refined modular coil kits and compact controllers to minimize structural changes and speed on-ship installation, strengthening the case for updates to aging frigates and destroyers. This advantage keeps retrofits at the center of the degaussing systems market during the forecast period.

Emergence of High-Temperature Superconducting Coil Technology Enabling Compact and Efficient Systems

High-temperature superconducting technology remains a strategic avenue for weight and efficiency gains on large combatants. Defense and energy supply chains continue to invest in HTS magnet technology, which supports naval applications that benefit from compact geometry and lower electrical loss.[2]Tokamak Energy, “TE Magnetics Division Launch,” tokamakenergy.co.uk As production capacity scales and more partners enter the ecosystem, qualification paths for shipboard coils will widen across allied programs. North America leads early adoption, while spillover into Asia-Pacific is likely as partners align on standards and thermal-management approaches compatible with at-sea operations. HTS also pairs well with model-based design and digital twins, which shorten validation cycles for next-generation coil layouts. These attributes help the degaussing systems market as programs plan future-proof builds that can carry more mission systems without exceeding displacement or power limits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated capital expenditure and long-term maintenance costs limit broader adoption | -0.9% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Extended acquisition timelines due to complex defense procurement procedures | -0.7% | Global, US and EU procurement cycles | Medium term (2-4 years) |

| Resource reallocation toward emerging railgun and directed-energy weapon systems reduces funding availability | -0.6% | North America, Europe | Medium term (2-4 years) |

| Supply-chain vulnerabilities for HTS tape and rare-earth-based magnetic sensors hinder production scalability | -0.5% | Global, materials concentration risk | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Capital Expenditure and Long-Term Maintenance Costs Limit Broader Adoption

Budget planners face trade-offs among survivability investments, lethality, and readiness, which can slow the pace of degaussing upgrades in some fleets. Total cost of ownership includes installation, periodic maintenance, and ranging, and these line items compete with other line items in procurement plans. Programs in emerging markets are the most sensitive to upfront and lifecycle costs, which can push degaussing work into later phases. Decision makers often choose retrofit packages that combine degaussing with other mid-life tasks to secure savings on labor and dock time. This cost calculus keeps adoption steady, yet it can delay deployment across lower-priority hulls in any given year.

Supply-Chain Vulnerabilities for HTS Tape and Rare-Earth-Based Magnetic Sensors Hinder Production Scalability

The materials stack that supports superconducting coils and advanced magnetometers is limited to a small supplier base. Industrial initiatives are underway to reduce reliance on specific rare-earth inputs, including next-generation HTS magnet designs that require fewer scarce materials. Even with these efforts, scaling output to naval volumes takes time as vendors qualify production lines for maritime requirements. Lead times and concentration risk can create scheduling pressure on ship programs that aim to adopt HTS coils or quantum-grade sensors. These constraints, therefore, temper the upside for the degaussing systems market in the forecast's out-years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vessel Type: Submarines Drive Stealth Imperatives

Submarines accounted for 30.67% of segment revenue in 2025 as undersea fleets embedded magnetic-signature control into new builds and through-class upgrades. Mine countermeasure vessels are advancing at a 7.65% CAGR through 2031, which reflects a doctrine that relies on low-field motherships and unmanned craft to hunt and neutralize mines. Procurement in North America centers on life-extension plans for Asia-Pacific growth, which is tied to contested littorals and new undersea programs that specify signature control at the blueprint stage. As unmanned systems take on more minehunting roles, motherships and support vessels also standardize lower magnetic baselines to reduce operational risk in influence fields. The degaussing systems industry benefits from this balanced mix as navies sequence upgrades by mission need and hull age.

Surface combatants, including destroyers and frigates, continue to sustain demand as fleets calibrate real-time control for low-signature patrols and transits. Mine warfare requirements extend to patrol craft and auxiliary vessels that support expeditionary missions, broadening the installed base for smaller coil sets and compact controllers. Allied shipbuilding roadmaps in 2026 emphasize higher survivability standards and tighter electromagnetic compatibility, which makes degaussing a core requirement rather than an optional retrofit. The result is stable volume from large hulls and faster growth in specialized vessels that operate in mine-threatened zones. This two-speed pattern anchors forecast demand and shapes vendor strategies across vessel classes within the degaussing systems market.

By Solution: Degaussing Dominance Faces Deperming Growth

Degaussing solutions led with 61.25% of segment spend in 2025 as navies prioritized onboard coil systems that suppress signatures during routine operations. Ranging and calibration remain central to commissioning and refit workflows because they set and validate field targets for both degaussing and deperming. Software-defined control adds resilience by learning how hulls behave across headings and latitudes, thereby reducing crew workload and shortening time to goal fields in port and at sea. Procurement teams integrate these capabilities within broader survivability scopes so modernization timelines align with ship availability windows. The degaussing systems industry is responding with modular amplifiers, smart controllers, and digital twins that compress design and acceptance testing.

Deperming is growing at a 6.27% CAGR through 2031 as navies increase the cadence of permanent magnetism resets to support lower day-to-day field levels. Portable and pierside approaches that minimize transit time to fixed facilities are gaining traction, keeping ships on station and reducing schedule risk. Since deperming improves the effectiveness of onboard coils by reducing remanence drift, many fleets pair deperming cycles with ranging updates to lock in gains. Model-based design is also improving coil layouts and deperming profiles, which supports more repeatable results between treatments. Together, these practices reinforce solution diversity and maintain real-time degaussing's leadership in the degaussing systems market.

By Component: Software Analytics Accelerate Intelligence Integration

Coils and cabling accounted for 33.45% of 2025 component revenue, supported by replacement cycles and design-in on new hulls. Demand spans copper-based loops and emerging superconducting architectures that aim to reduce weight and power draw on large ships. Vendors support these needs with modular harnessing and routing kits that simplify installation around propulsion and mission systems. Control electronics continue to evolve, with higher reliability and stronger cyber safeguards, which are essential as more ships network with combat systems. These shifts keep hardware investment steady while opening the door to software-centric differentiation in the degaussing systems market.

Software and analytics are the fastest-growing components at a 7.87% CAGR through 2031, driven by AI-enabled control and model-based tuning. A 2026 partnership between Naval Group and Thales highlights the move to industrialize AI for ship platforms, including algorithms that optimize coil currents in real time using sensor feedback. Digital twins shorten design iterations and reduce range cycles by validating coil layouts before launch, and predictive maintenance modules help forecast cable or amplifier service needs before failure. As fleets add unmanned assets, scalable software control spanning motherships and USVs becomes increasingly valuable for coordinated operations. These factors explain why software is the performance lever and growth engine across components in the degaussing systems market.

By Installation Type: Retrofit Modernization Dominates Market

Retrofit installations held 53.76% of 2025 revenue and are projected to grow at a 7.38% CAGR through 2031, reflecting lifecycle economics and procurement realities. Navies align degaussing refresh with other mid-life packages to minimize dry-dock time and integrate calibrations with broader mission system upgrades. Oversight reporting on delivery timelines reinforces why fleets maximize value from existing hulls while new builds progress through longer qualification paths.[3]US Government Accountability Office, “Defense Acquisitions Oversight Publications,” gao.gov Retrofit scope also adapts to platform constraints, keeping costs and time in check across a range of surface combatants. These attributes make retrofit the center of gravity for the degaussing systems market through the forecast.

New-build installations account for the remaining share and reflect strategic programs where magnetic-signature control is embedded at the blueprint stage. Shipbuilding budgets in North America provide durable funding for destroyers, amphibious ships, and undersea platforms that standardize signature management and electromagnetic compatibility. Asia-Pacific programs concentrate growth as partners advance submarine and surface combatant lines that plan for low-field operations in contested waters. Even so, long qualification cycles and supply-chain considerations temper the near-term ramp and preserve the retrofit advantage. As a result, both paths remain active, with retrofit driving volume and new-builds setting the technology baseline for the degaussing systems market.

Geography Analysis

North America held 35.65% of the degaussing systems market size in 2025, supported by sustained US shipbuilding and modernization outlays and Canadian industrial policy that prioritizes domestic capability. The US FY2026 portfolio directs USD 65 billion to shipbuilding and maritime systems and maintains funding for mine countermeasures and survivability enablers. Canada’s 2026 defense industrial strategy formalizes a pathway to strengthen naval production capacity and align suppliers with long-term platform needs, including electromagnetic compatibility readiness for future surface ships. The US Navy’s MCM USV program advances distributed mine warfare, bridging platform procurement with mission demand for low-field operations. These conditions secure a stable base for the degaussing systems market in the region.

Asia-Pacific is projected to grow at an 8.12% CAGR through 2031 as naval expansion aligns with contested sea lanes and broader adoption of autonomous mine countermeasures. Unmanned programs across the region place a premium on micro-degaussing and software-defined control, enabling USVs and motherships to operate in influence-mine areas with lower field strength. Partners continue to align technical choices with survivability goals, which reinforces model-based design and calibration discipline. Software innovation is likely to scale quickly as suppliers tailor algorithms to local operating environments and range datasets. These elements underpin Asia-Pacific's outperformance in the degaussing systems market.

Europe sustains steady adoption, anchored in its mine warfare legacy and in standardization within NATO frameworks. Member states invest in autonomous mine countermeasures and associated degaussing coordination, and 2026 supplier announcements confirm AI engineering resources dedicated to ship platforms and signature management. Procurement cycles remain deliberate to align with electromagnetic compatibility and shock requirements, which keeps throughput consistent across near-term budgets. European priorities mirror the global mix of retrofit volume and selective new-build adoption, with an emphasis on modular and software-defined control. This stance supports predictable opportunities for the degaussing systems market without the volatility seen in other defense categories.

Competitive Landscape

The degaussing systems market centers on a focused set of naval-qualified suppliers that combine onboard coils, control electronics, and calibration tools with software-defined control. Global primes and specialist vendors anchor positions by meeting stringent military standards for electromagnetic compatibility, shock, and reliability. Partnerships in 2026 indicate greater investment in AI for ship platforms, raising the bar for real-time coil-current optimization at sea. Control stack evolution and digital twin support both new-build and retrofit pathways, expanding serviceable opportunities in the near term. These qualities point to moderate concentration shaped by qualification depth and installed base strength.

Strategy execution in 2026 spotlights software and autonomy as differentiators. Thales and Naval Group formalized a sovereign-AI collaboration to accelerate industrialization of algorithms for onboard decision support and real-time field management, a move designed to scale across national fleets. Exail expanded its Middle East presence by opening a Riyadh office in 2026 and confirmed allied procurement of mine-neutralization systems that align with autonomous MCM concepts of operation, thereby increasing the relevance of coordinated signature control across motherships and unmanned assets. The US Navy’s MCM USV program continues to shape requirements for micro-degaussing and modular integration around autonomous payloads. These examples highlight a shift to software-centric approaches that benefit platforms of all sizes in the degaussing systems market.

Ecosystem dynamics also reflect how autonomy and AI are crossing from aviation into naval applications. In 2024, Shield AI partnered with the US Navy to integrate its Hivemind AI pilot software into an aerial target as a testbed for autonomous decision loops. This pathway informs future integration of maritime control software. Vendors that demonstrate interoperable, cyber-hardened control stacks and verifiable performance gains in calibration and at-sea operations are likely to consolidate share. Defense buyers reward proof points tied to mission outcomes, which positions companies that blend qualified hardware with adaptive software to lead growth. This focus continues to shape competition and underpins adoption decisions across the degaussing systems market.

Degaussing Systems Industry Leaders

Wärtsilä Corporation

Polyamp AB

ESCO Technologies Inc.

American Superconductor Corporation

L3Harris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Royal Navy integrated three autonomous SWEEP mine countermeasure systems under a GBP 25 million (USD 34.1 million) contract with TKMS Atlas UK. These systems, equipped with USVs towing magnetic, acoustic, and electric influence payloads, reflect the growing strategic focus on magnetic signature management and mine threat mitigation.

- February 2025: ESCO Technologies completed the USD 550 million acquisition of Ultra Maritime's signature management and power division, integrating Ultra's degaussing, ranging, and power-conditioning lines.

- February 2024: Babcock received a five-year contract from the UK Ministry of Defence (MoD) to provide in-service support for the Royal Navy's Ships Protective System equipment, delivering degaussing, cathodic protection, and active shaft grounding services to reduce vessel vulnerability to magnetic mines.

Global Degaussing Systems Market Report Scope

Naval degaussing systems are critical technologies designed to manage and reduce the magnetic signatures of maritime vessels, thereby minimizing risks associated with magnetic and influence mines. This report examines solutions such as degaussing, deperming, and magnetic ranging, along with the necessary hardware and software components.

The market is segmented by vessel type, solution, component, installation type, and geography. By vessel type, the market is segmented into aircraft carriers, destroyers, frigates, corvettes, submarines, mine countermeasure vessels, and other vessel types. By solution, the market is segmented into degaussing, deperming, and ranging. By component, the market is segmented into control units (DCU), power amplifiers, coils and cabling, magnetometers, sensors, and software analytics. By installation type, the market is segmented into new-build installations or retrofits. The report also covers the market sizes and forecasts for the degaussing systems market in major countries across different regions. For each segment, the market size and forecast are provided in terms of value (USD).

| Aircraft Carriers |

| Destroyers |

| Frigates |

| Corvettes |

| Submarines |

| Mine Countermeasure Vessels |

| Other Vessel Types |

| Degaussing |

| Deperming |

| Ranging |

| Control Units (DCU) |

| Power Amplifiers |

| Coils and Cabling |

| Magnetometers and Sensors |

| Software and Analytics |

| New-Build Installation |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Vessel Type | Aircraft Carriers | ||

| Destroyers | |||

| Frigates | |||

| Corvettes | |||

| Submarines | |||

| Mine Countermeasure Vessels | |||

| Other Vessel Types | |||

| By Solution | Degaussing | ||

| Deperming | |||

| Ranging | |||

| By Component | Control Units (DCU) | ||

| Power Amplifiers | |||

| Coils and Cabling | |||

| Magnetometers and Sensors | |||

| Software and Analytics | |||

| By Installation Type | New-Build Installation | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the degaussing systems market size in 2026 and the growth outlook to 2031?

The degaussing systems market size is valued at USD 921.3 million in 2026 and is projected to reach USD 1,201.26 million by 2031 at a 5.45% CAGR.

Which vessel types are leading demand for naval degaussing?

Submarines led with 30.67% of segment revenue in 2025, and mine countermeasure vessels are the fastest growing at a 7.65% CAGR through 2031.

Which regions are driving growth for naval degaussing through 2031?

North America held 35.65% in 2025, while Asia-Pacific is projected to grow at 8.12% CAGR through 2031 on rising mine-warfare and autonomy investments.

What solutions and components are gaining the most traction?

Degaussing led with 61.25% share in 2025, deperming is growing at 6.27% CAGR, and software and analytics is the fastest component at 7.87% CAGR.

Why are retrofit installations so prominent in naval degaussing programs?

Retrofit held 53.76% share in 2025 and is growing at 7.38% CAGR because bundled mid-life upgrades deliver faster results than new-build cycles with long qualification timelines.

How are AI and autonomy influencing demand for naval degaussing?

Naval AI partnerships are moving real-time field optimization into production, and unmanned mine countermeasures programs require micro-degaussing on USVs to operate safely near influence mines.

Page last updated on: