Neurotechnology Brain Computer Interface Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

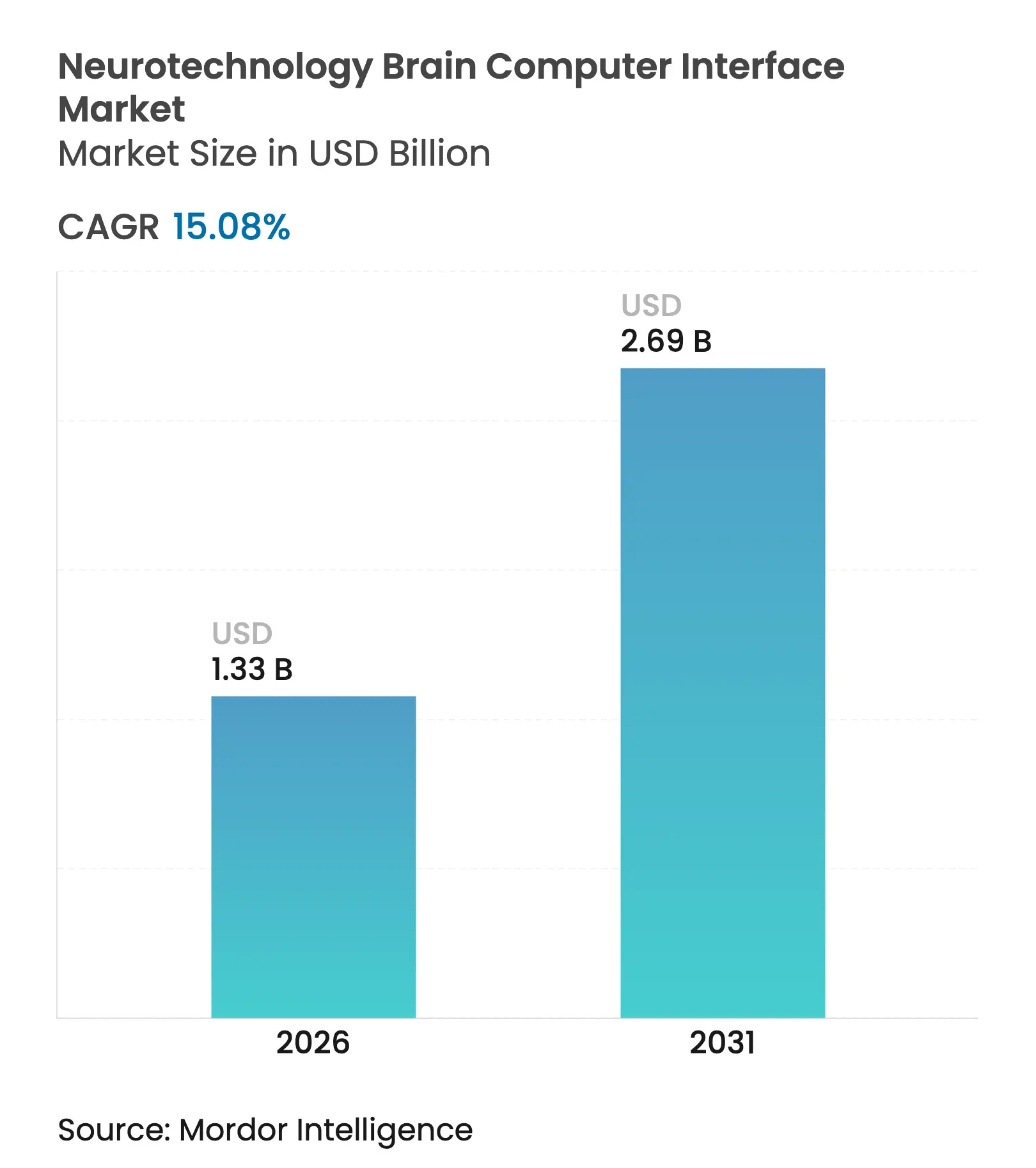

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 15.08 % CAGR |

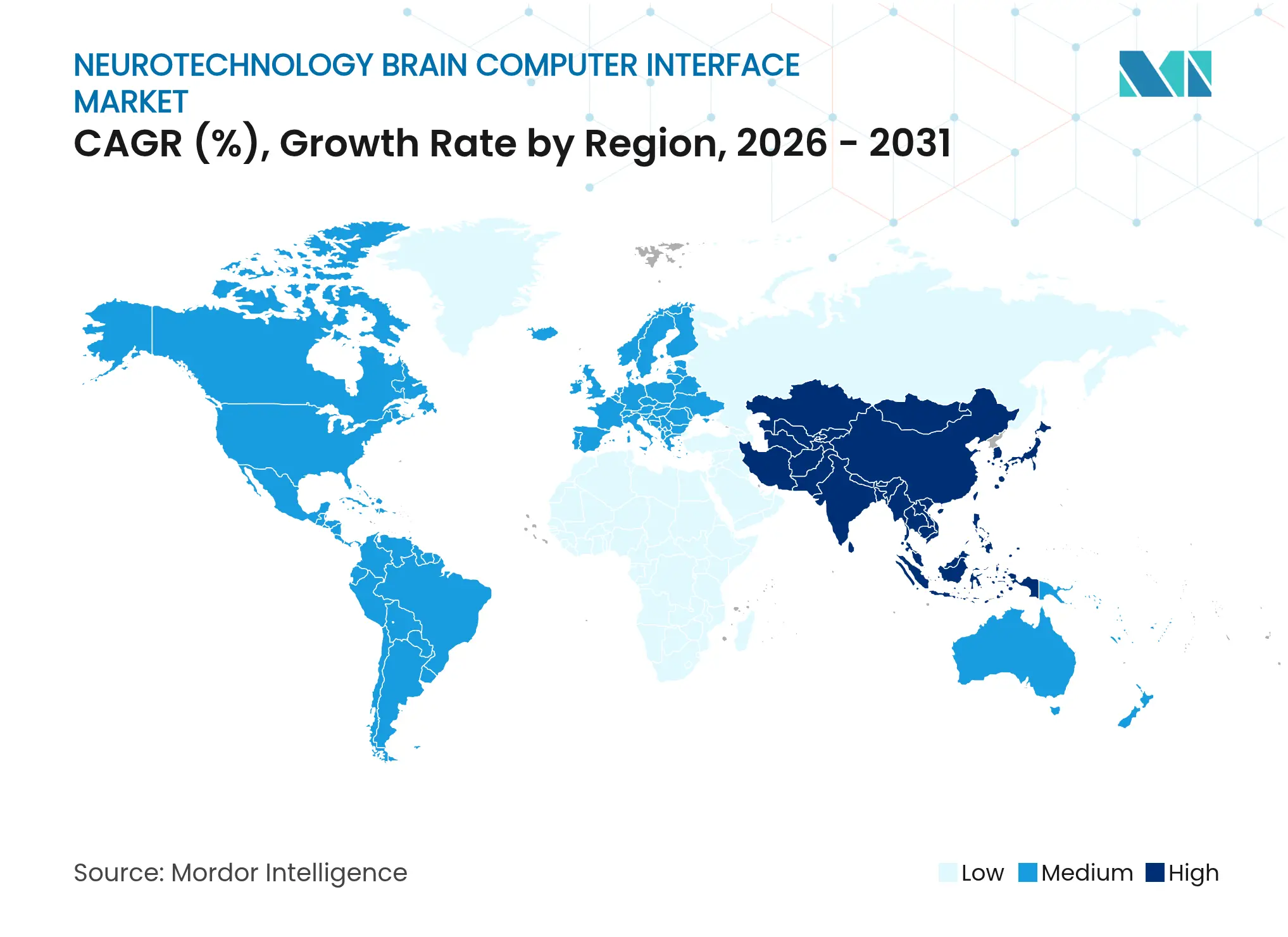

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

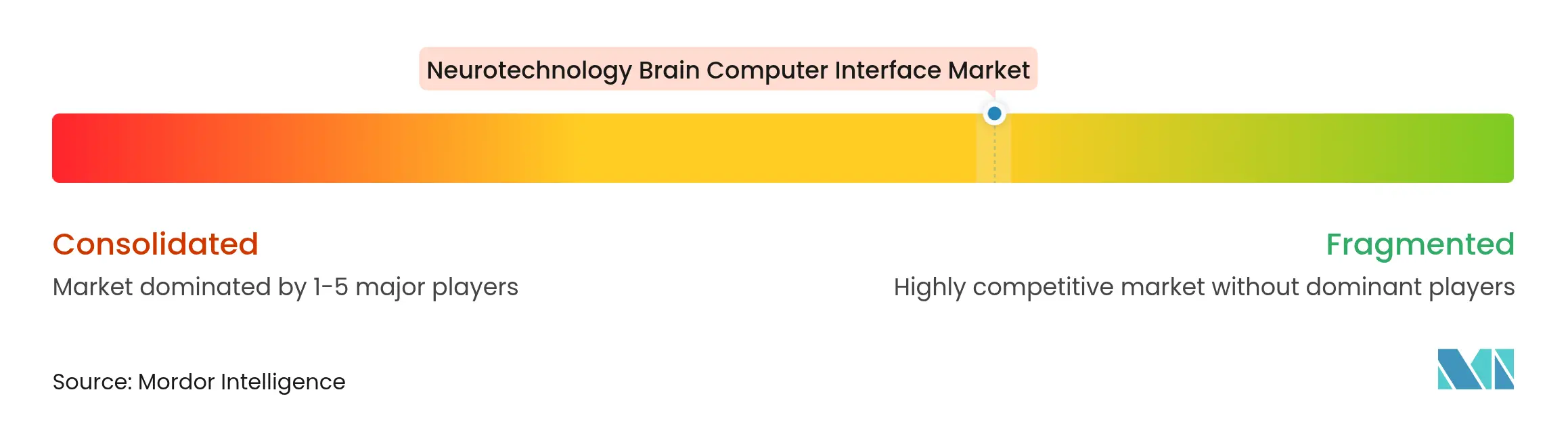

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Neurotechnology Brain Computer Interface Market Analysis by Mordor Intelligence

neurotechnology brain computer interface market size in 2026 is estimated at USD 1.33 billion, growing from 2025 value of USD 1.16 billion with 2031 projections showing USD 2.69 billion, growing at 15.08% CAGR over 2026-2031. Expanding neurological disorder prevalence, rapid FDA Breakthrough Device clearances, and maturing neural signal-processing techniques are building a clear commercial pathway for the neurotechnology brain computer interface market. Hardware maintains dominance because implant arrays, amplifiers, and wireless telemetry require sizable capital spending, yet software is becoming the prime growth engine as artificial intelligence improves decoding accuracy and shortens calibration time. Non-invasive modalities continue to hold a sizeable clinical footprint, but partially invasive systems are now scaling quickly thanks to minimally invasive electrode formats that raise recording quality without imposing extensive surgical risks. Investment momentum remains strong, with venture funding surpassing USD 850 million in 2025 and multiregional public projects accelerating translational research. North America supplies the largest revenue pool, however Asia Pacific is closing the gap as China, Japan, and South Korea fund national neurotechnology programs that shorten development cycles.

Key Report Takeaways

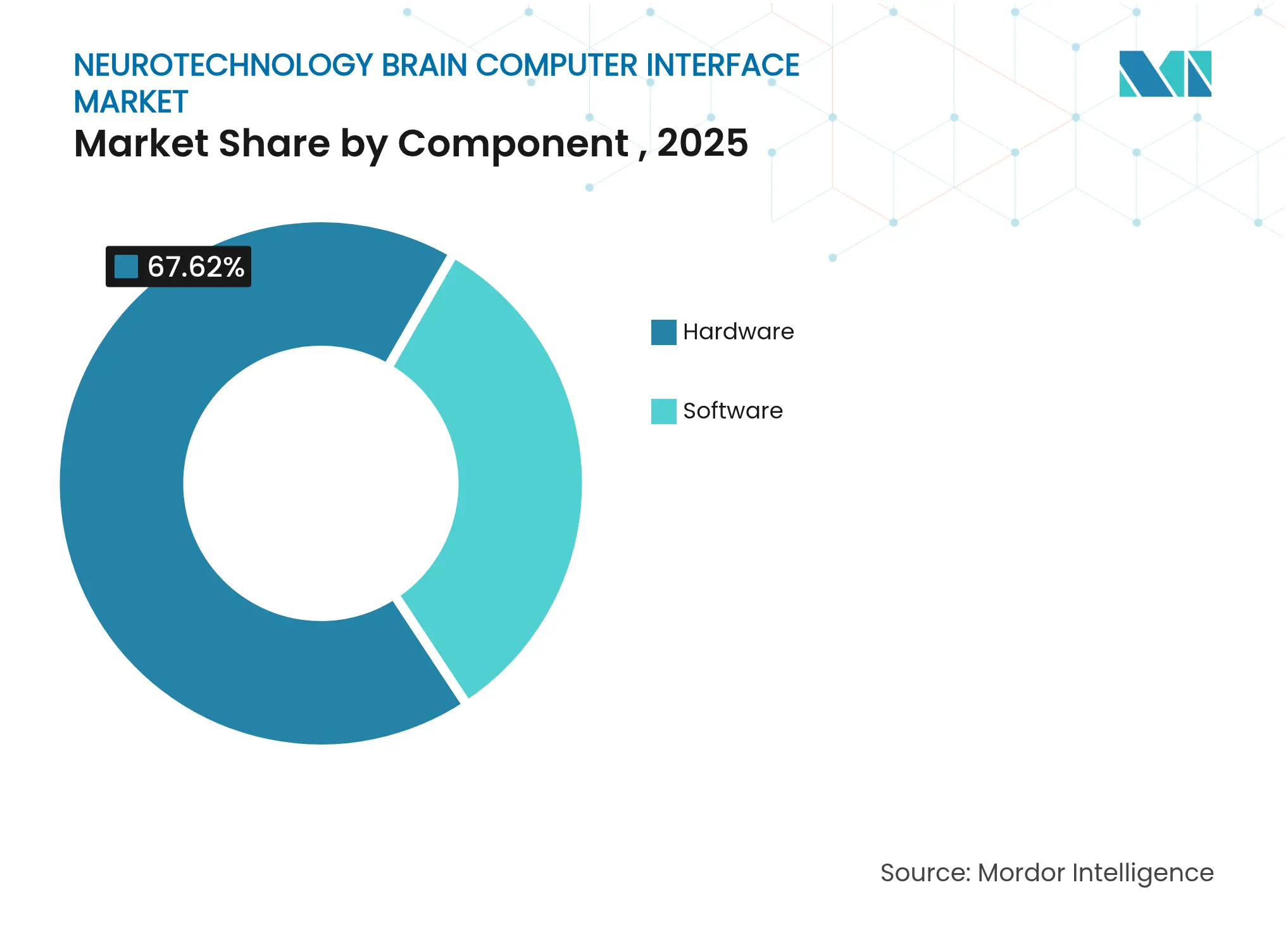

- By component, hardware held 67.62% of neurotechnology brain computer interface market share in 2025, whereas software is projected to post a 16.12% CAGR through 2031.

- By interface type, non-invasive systems controlled 71.35% revenue in 2025; partially invasive formats are on track for the fastest 16.35% CAGR to 2031.

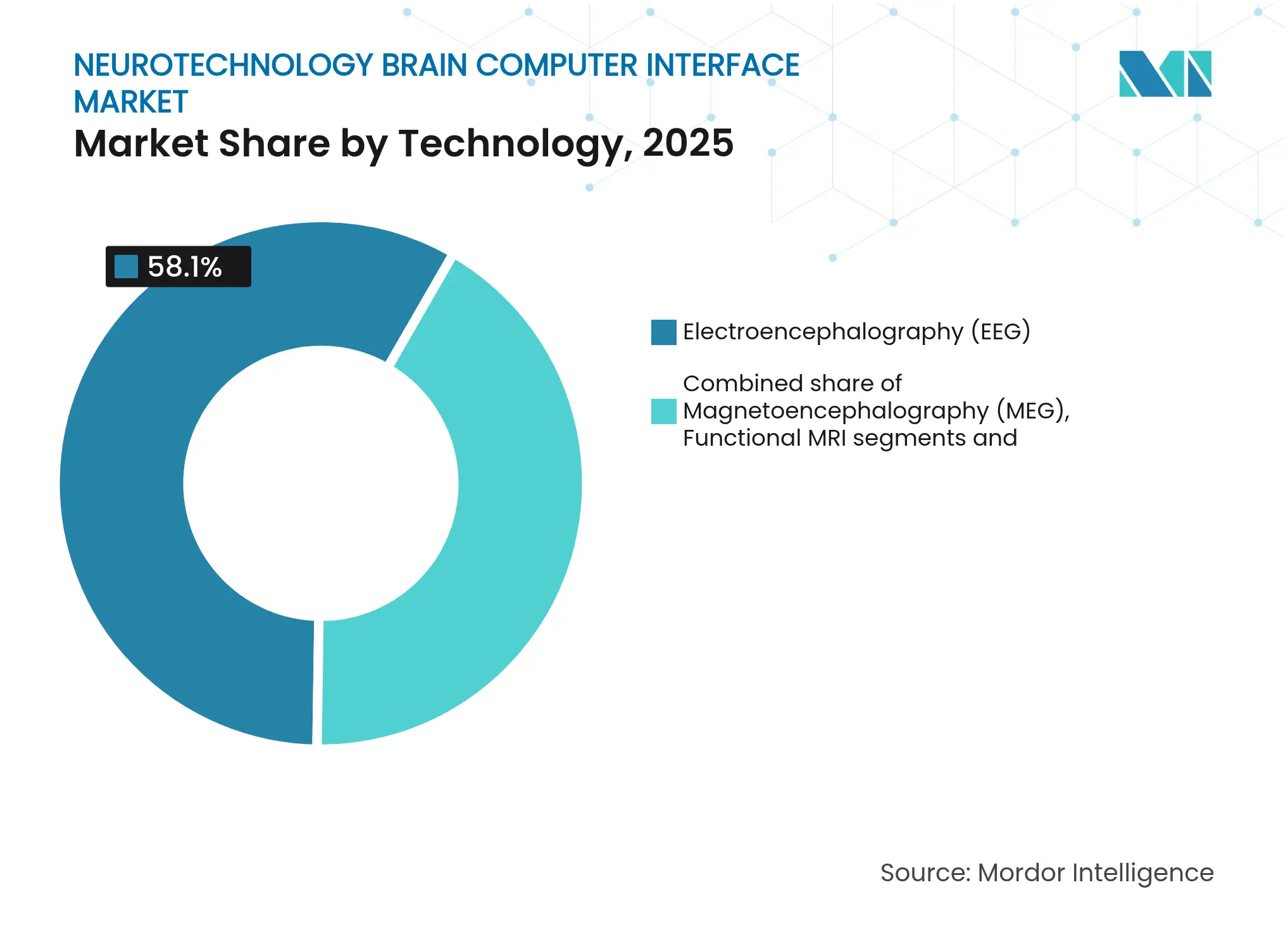

- By technology, electroencephalography captured 58.10% of the neurotechnology brain computer interface market size in 2025, while real-time functional MRI is expected to grow at 15.91% CAGR between 2026 and 2031.

- By end user, hospitals and clinics accounted for 54.66% share of the neurotechnology brain computer interface market size in 2025 and rehabilitation centers are set for a 15.54% CAGR through 2031.

- By geography, North America led with 40.92% revenue in 2025 and Asia Pacific is advancing at 16.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurotechnology Brain Computer Interface Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging prevalence of neurological disorders

Surging prevalence of neurological disorders

| +4.2% | Global, with highest burden in low- and middle-income countries | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+4.2%

|

Geographic Relevance

:

Global, with highest burden in low- and middle-income

countries

|

Impact Timeline

:

Long term (≥ 4 years)

|

Escalating R&D investments and venture funding

Escalating R&D investments and venture funding

| +3.8% | North America & EU, expanding to Asia Pacific | Medium term (2-4 years) | |||

Advances in non-invasive neuro-imaging and AI decoding

Advances in non-invasive neuro-imaging and AI decoding

| +2.9% | Global, led by US and China research institutions | Medium term (2-4 years) | |||

Mainstream consumer wearables adoption

Mainstream consumer wearables adoption

| +1.7% | North America, Western Europe, urban Asia Pacific | Short term (≤ 2 years) | |||

FDA Breakthrough Device designations accelerating

approvals

FDA Breakthrough Device designations accelerating

approvals

| +1.9% | US market with spillover to international regulatory harmonization | Short term (≤ 2 years) | |||

Integration of BCIs with XR productivity ecosystems

Integration of BCIs with XR productivity ecosystems

| +0.8% | North America, Northern Europe, tech-forward Asian markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surging Prevalence of Neurological Disorders

Neurological conditions affect more than 3.4 billion people, making them the leading global cause of illness and disability. Incidence rates for stroke, dementia, and diabetic neuropathy have risen sharply, widening the clinical population that cannot be served adequately by pharmaceuticals alone. The neurotechnology brain computer interface market benefits directly because BCIs restore lost communication and motor pathways and reduce long-term care costs. As healthcare systems prioritize quality-of-life outcomes, reimbursement frameworks are beginning to recognize the value of neural prosthetics. In turn, clinicians are incorporating BCI options into multidisciplinary care plans for patients with advanced motor impairment.

Escalating R&D Investments and Venture Funding

Neuralink,[1]Source: CNBC, “Neuralink Raises USD 650 Million in Series E Funding,” cnbc.com Precision Neuroscience, and Blackrock Neurotech collectively raised more than USD 1 billion between 2024 and 2025, reflecting high investor confidence in the neurotechnology brain computer interface industry. Government programs such as the NIH BRAIN Initiative and China’s national neurotech agenda are providing non-dilutive capital, shortening time to pivotal trials. The funding upturn has increased the number of investigational devices in first-in-human studies, aligning commercial milestones with rising patient demand. As capital shifts from proof-of-concept toward scale-up, suppliers of electrodes, ASICs, and low-power wireless modules gain forward revenue visibility.

Advances in Non-Invasive Neuro-Imaging and AI Decoding

Large-language-model integration with EEG data sets has improved thought-to-text accuracy to 75%, which is 2.6 times better than earlier benchmarks. Chinese research teams demonstrated two-way adaptive BCIs that deliver 100-fold efficiency improvements and 20% accuracy gains through neuromorphic hardware.[2]Source: Interesting Engineering, “World’s First Two-Way Brain-Computer Interface with 100-Fold Efficiency,” interestingengineering.com These breakthroughs neutralize long-standing constraints around low signal-to-noise ratios, opening the neurotechnology brain computer interface market to consumer wellness and industrial productivity applications. As algorithms advance, device makers can reduce electrode counts and simplify form factors, lowering cost of goods and broadening patient eligibility.

FDA Breakthrough Device Designations Accelerating Approvals

The FDA has granted Breakthrough Device status to multiple BCI systems, including Neuralink’s visual prosthesis. Breakthrough status shortens feedback cycles and formalizes clinical outcome measures, a key step toward payer coverage. Expedited reviews also set harmonization templates for other agencies, notably in Canada, Australia, and Japan. The clearer regulatory outlook reduces due-diligence risk, spurring additional institutional investment and strategic partnerships across the neurotechnology brain computer interface market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High device, procedure & maintenance costs

High device, procedure & maintenance costs

| -3.1% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-3.1%

|

Geographic Relevance

:

Global, most pronounced in emerging markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Signal fidelity & reliability limitations

Signal fidelity & reliability limitations

| -2.4% | Global, affecting all BCI modalities | Long term (≥ 4 years) | |||

Neuro-privacy regulations raising compliance burdens

Neuro-privacy regulations raising compliance burdens

| -1.8% | US states, EU, expanding globally | Short term (≤ 2 years) | |||

Global shortage of implant-qualified neurosurgeons

Global shortage of implant-qualified neurosurgeons

| -1.2% | Most severe in Africa and Southeast Asia | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Device and Procedural Costs

Current implantation packages range from USD 10,500 to USD 40,000, which limits access in both public and private pay systems. Device manufacturing relies on high-precision microfabrication, clean-room packaging, and bespoke surgical robots, pushing capital expenses well above typical neurostimulation implants. Insurance coverage remains narrow because long-term outcomes data are still emerging. Vendors are pursuing automated implantation and polymer electrode arrays to push system prices toward the USD 2,000 range, yet this goal hinges on volume scale and streamlined supply chains.

Signal Fidelity and Reliability Limitations

Scar tissue formation, electrode corrosion, and motion artifacts degrade recording quality over time, which in turn forces frequent recalibration. Non-invasive EEG faces environmental noise and variable skin contact, while invasive arrays encounter gliosis that increases impedance. Average information transfer rates remain below 50 words per minute, restricting real-world communication use cases. Research on graphene and soft polymer electrodes shows promise for lower inflammatory response, yet multiyear stability data are still limited. Sustained reliability is vital for payer adoption and will dictate the usable lifetime of implanted hardware within the neurotechnology brain computer interface market.

Segment Analysis

By Component: Hardware dominance continues while AI software accelerates

Hardware captured 67.62% revenue in 2025 because every clinical workflow requires electrodes, amplifiers, and power modules that meet rigorous biocompatibility standards. The neurotechnology brain computer interface market size for hardware reached USD 0.78 billion in 2025. Sophisticated Utah arrays, endovascular stents, and kirigami-folded 3D probes underline continuing capital intensity. Component suppliers are now integrating wireless power links that remove percutaneous connectors, improving infection control and patient comfort. The convergence of ASIC miniaturization with biocompatible polymers is extending implant life cycles.

Software is advancing at a 16.12% CAGR through 2031 as deep learning models refine spike sorting and reduce calibration to minutes rather than hours. Real-time adaptation to signal drift cuts clinical setup costs and supports at-home use. Open-source training data and federated learning encourage algorithm portability across different electrode formats, further spurring uptake. Over the forecast horizon, integrated neuromorphic chips may tilt value capture toward software-defined architectures, but hardware innovation will still anchor market entry barriers for new competitors.

Note: Segment shares of all individual segments available upon report purchase

By Interface Type: Non-invasive leadership with minimally invasive surge

Non-invasive solutions generated 71.35% of neurotechnology brain computer interface market revenue in 2025 as EEG caps and dry electrodes dominate hospital outpatient and consumer wellness channels. Adoption benefits from low regulatory hurdles and absence of neurosurgical requirements. However, partially invasive systems that place electrodes under the skull or within cortical vessels are registering a 16.35% CAGR and could narrow the gap by 2031. Signal-to-noise ratios in sub-scalp EEG now rival surface electrocorticography, broadening application beyond simple cursor control.

Clinical decision making increasingly weighs safety against decoding precision. For communication prostheses restoring speech in ALS, fully invasive arrays remain preferred. For motor recovery, non-invasive systems enable extended home rehabilitation sessions without surgical risk. Surgical robotics and image-guided catheter placement are shrinking procedure times, reducing hospital costs, and supporting outpatient implantation models that will raise overall neurotechnology brain computer interface market share for minimally invasive formats.

By Technology: EEG stays ahead while real-time fMRI moves up the curve

Electroencephalography accounted for 58.10% of segment revenue in 2025, benefitting from a century of hardware refinement and straightforward reimbursement pathways. Dry electrodes and in-ear form factors have improved wearability and cut setup time to under five minutes. The neurotechnology brain computer interface market share for EEG is likely to moderate slightly as hybrid modalities mature.

Real-time functional MRI exhibits a 15.91% CAGR on the strength of millimeter-scale spatial resolution and deep-brain imaging. Neurofeedback protocols for depression and chronic pain are generating promising outcomes in controlled trials. Cost and scanner availability restrict widespread use, yet portable low-field MRI designs are in development. Electrocorticography and magnetoencephalography address niche requirements for high bandwidth and deep-structure recordings. Hybrid EEG-fMRI pipelines deliver temporal and spatial completeness, a trend that could define future clinical standard-of-care once integrated software workflows mature.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals dominate but rehabilitation centers expand quickly

Hospitals and clinics commanded 54.66% revenue in 2025 because BCI implantation, tuning, and acute monitoring require surgical theaters and neurologist oversight. The neurotechnology brain computer interface market size for hospital deployments is projected to grow steadily in line with procedural volumes. Health systems regard BCIs as adjunct technologies for complex neurological care, fostering multidisciplinary neuro-prosthetic teams that manage pre-operative planning through to chronic support.

Rehabilitation centers display a robust 15.54% CAGR. Evidence from randomized studies shows BCI-guided motor imagery combined with functional electrical stimulation can improve upper-extremity Fugl-Meyer scores, motivating insurers to trial bundled payment models. Tele-rehabilitation toolkits that stream EEG data over secure cloud links reduce travel burdens for stroke survivors, opening a new service line for rural clinics. Consumer wellness studios and educational labs form a small but rising sub-segment as non-medical applications gain mind-share.

Geography Analysis

North America generated 40.92% of neurotechnology brain computer interface market revenue in 2025. The United States anchors that lead through FDA Breakthrough Device pathways, deep venture pools, and a concentration of academic medical centers running first-in-human trials. Canada augments regional capability with favorable research tax credits and provincial grants that fund translational engineering programs. Upcoming Medicare coverage assessments for adaptive deep brain stimulation could unlock public reimbursement, reinforcing market momentum in 2026 and beyond.

Asia Pacific is the growth frontrunner at 16.84% CAGR. China channels state funding into national neurotech laboratories and offers accelerated device review through its NMPA Special Review Procedure, which mirrors FDA priority review but with broader accepted surrogate endpoints. Home-grown innovators such as NeuroXess have demonstrated 71% speech decoding accuracy for Mandarin syllables, narrowing the performance gap with Western pioneers. Japan leverages robotics strengths to refine lead placement, while South Korea advances semiconductor supply chains that decrease implant costs.

Europe continues steady expansion driven by the EU Medical Device Regulation that provides a single certification regime. Horizon Europe grants and the Human Brain Project sustain cross-border academic-industrial consortia. Post-Brexit, the United Kingdom is piloting a flexible approvals sandbox that allows conditional market entry for neurotechnology start-ups. Emerging markets in Latin America and Africa remain constrained by low neurosurgeon density, yet telehealth enabled EEG and non-surgical sub-scalp systems present viable near-term entry points, particularly where mobile broadband penetration is high.

Competitive Landscape

Market Concentration

The sector shows moderate concentration as leading firms pursue differentiated design philosophies rather than converging on a single architecture. Neuralink focuses on ultra-high-density invasive arrays implanted by proprietary surgical robots, aiming for more than 1,000 channels per device and bandwidth suitable for full-hand prosthetic control. Synchron follows an endovascular path that leverages standard neuro-interventional tools, thereby shortening learning curves for surgeons and reducing procedure cost. Precision Neuroscience offers a thin-film cortical surface implant designed for 30-day recording that lowers tissue trauma risk.

Strategic collaborations are multiplying. Synchron’s agreement with Apple allows thought-based control of Vision Pro headsets, expanding beyond the medical niche and signaling a future in consumer electronics interfaces. Paradromics partnered with NEOM Investment Fund to build a dedicated Middle East neurotechnology innovation hub, illustrating geographic diversification strategies. Suppliers of ASICs, graphene electrodes, and wireless power modules are entering co-development pacts to secure design-win positions inside flagship implants.

Patent filings show a surge in claims covering soft polymer electrodes, bi-directional stimulation, and closed-loop machine learning algorithms that adapt decoding in real time. White-space opportunities exist in pediatric neuroprosthetics and ultrasound-based BCIs, where device sizing, skull thickness, and acoustic safety thresholds differ markedly from adult implants. Companies with expertise in material science and energy-efficient neuromorphic chips are well placed to capture share as product portfolios widen across therapeutic and non-medical verticals.

Neurotechnology Brain Computer Interface Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: UC Berkeley and UCSF scientists demonstrated near-real-time thought-to-speech conversion, enabling voice restoration for locked-in patients.

- February 2025: Subsense exited stealth with USD 17 million to advance non-surgical BCI headsets, underscoring sustained investor appetite.

- September 2024: Neurable and Master & Dynamic launched MW75 Neuro headphones, the first consumer-grade audio device with integrated BCI functions, broadening market visibility.

- May 2024: Neurotechnology updated BrainAccess HALO to an 8-hour battery life, lifting daily usability for portable EEG monitoring.

Table of Contents for Neurotechnology Brain Computer Interface Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Surging prevalence of neurological disorders

- 4.2.2Escalating R&D investments and venture funding

- 4.2.3Advances in non-invasive neuro-imaging and AI decoding

- 4.2.4Mainstream consumer wearables adoption

- 4.2.5FDA Breakthrough Device designations accelerating approvals

- 4.2.6Integration of BCIs with XR productivity ecosystems

- 4.3Market Restraints

- 4.3.1High device, procedure & maintenance costs

- 4.3.2Signal fidelity & reliability limitations

- 4.3.3Neuro-privacy regulations raising compliance burdens

- 4.3.4Global shortage of implant-qualified neurosurgeons

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Component

- 5.1.1Hardware

- 5.1.2Software

- 5.2By Interface Type

- 5.2.1Invasive

- 5.2.2Partially Invasive

- 5.2.3Non-Invasive

- 5.3By Technology

- 5.3.1Electroencephalography (EEG)

- 5.3.2Magnetoencephalography (MEG)

- 5.3.3Electrocorticography (ECoG)

- 5.3.4Functional MRI

- 5.3.5Other Technologies

- 5.4By End User

- 5.4.1Hospitals and Clinics

- 5.4.2Rehabilitation Centers

- 5.4.3Other End Users

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Neuralink Corp.

- 6.3.2Blackrock Neurotech

- 6.3.3Synchron Inc.

- 6.3.4Precision Neuroscience

- 6.3.5Advanced Brain Monitoring, Inc.

- 6.3.6EMOTIV, Inc.

- 6.3.7Neurable Inc.

- 6.3.8g.tec medical engineering GmbH

- 6.3.9OpenBCI

- 6.3.10Brain Products GmbH

- 6.3.11CorTec GmbH

- 6.3.12Ripple Neuro

- 6.3.13Paradromics Inc.

- 6.3.14Cognixion

- 6.3.15MindMaze SA

- 6.3.16Kernel

- 6.3.17Nexstem

- 6.3.18NeuroPace Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the brain-computer interface market as the global revenue generated by hardware and core software that capture, translate, and transmit human neural signals to external devices in order to restore, augment, or replace motor, sensory, and cognitive functions. All interface types, non-invasive, partially invasive, and fully invasive, are in scope alongside enabling electroencephalography, electrocorticography, magnetoencephalography, fMRI, and related signal-processing platforms.

Scope exclusion: consumer wearables that use basic electro-dermal or optical sensors without true neural acquisition lie outside this assessment.

Segmentation Overview

- By Component

- Hardware

- Software

- Hardware

- By Interface Type

- Invasive

- Partially Invasive

- Non-Invasive

- Invasive

- By Technology

- Electroencephalography (EEG)

- Magnetoencephalography (MEG)

- Electrocorticography (ECoG)

- Functional MRI

- Other Technologies

- Electroencephalography (EEG)

- By End User

- Hospitals and Clinics

- Rehabilitation Centers

- Other End Users

- Hospitals and Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with neurosurgeons, rehabilitation therapists, procurement leads at leading hospitals, and product managers at neurotech start-ups across North America, Europe, and Asia helped us validate typical device pricing, hospital adoption hurdles, and regional reimbursement timelines. Structured surveys among academic labs experimenting with invasive BCI clarified likely clinical trial success rates and timing, plugging gaps that secondary data could not address.

Desk Research

We began with publicly available datasets from agencies such as the U.S. National Institutes of Health, Eurostat, and the World Health Organization, each offering incidence figures for stroke, spinal cord injury, and neurodegenerative disorders that frame potential patient pools. Trade associations like the IEEE Brain Initiative and the International Neuroinformatics Coordinating Facility provide technology adoption timelines, while customs and tender portals, including Volza and Tenders Info, reveal shipment volumes and contract values for EEG headsets and implant components. Company filings and FDA 510(k) summaries supply selling prices and pipeline counts, and Dow Jones Factiva tracks venture funding and merger activity feeding our demand assumptions. The sources cited are illustrative, not exhaustive, of the material reviewed by Mordor analysts during data collection and validation.

Market-Sizing & Forecasting

We applied a top-down incidence-to-treatment model that scales candidate patient populations by procedure eligibility, reimbursement penetration, and device utilization rates, and we corroborated totals through selective bottom-up supplier roll-ups of sampled average selling price multiplied by unit shipments. Key variables include annual ischemic stroke cases, ALS prevalence, average EEG headset ASP, number of active BCI clinical trials, and venture capital inflows. A multivariate regression with adoption-curve dummies and GDP-per-capita controls projects each variable through 2030; scenario analysis then adjusts for technology breakthroughs or regulatory delays. Where supplier data were missing, substitution with regional proxy pricing was flagged and peer-reviewed before inclusion.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, anomaly checks against external benchmarks, and management sign-off. Our models refresh every twelve months, with interim revisions triggered by major funding rounds, pivotal trial results, or material regulatory changes to ensure clients always receive an up-to-date view.

Why Our Neurotechnology Brain Computer Interface Baseline Commands Confidence

Benchmark comparison

Published estimates often diverge because firms mix assistive software revenues with device sales, assume aggressive reimbursement roll-outs, or use narrow product cut-offs.

Key gap drivers here include differing inclusion of consumer EEG wearables, one-time service revenues counted as recurring sales, and varied refresh cadences that leave some models two years out of date.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.16 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 2.94 B (2025) | Global Consultancy A | Adds gaming headsets and neuro-adaptive software platforms | ||

USD 2.40 B (2025) | Industry Forecast B | Bundles installation services and neuro-prosthetic consumables | ||

USD 0.26 B (2024) | Regional Study C | Limits scope to non-invasive diagnostics devices only |