DC Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 22.07 Billion |

| Market Size (2031) | USD 31.03 Billion |

| Growth Rate (2026 - 2031) | 7.06% CAGR |

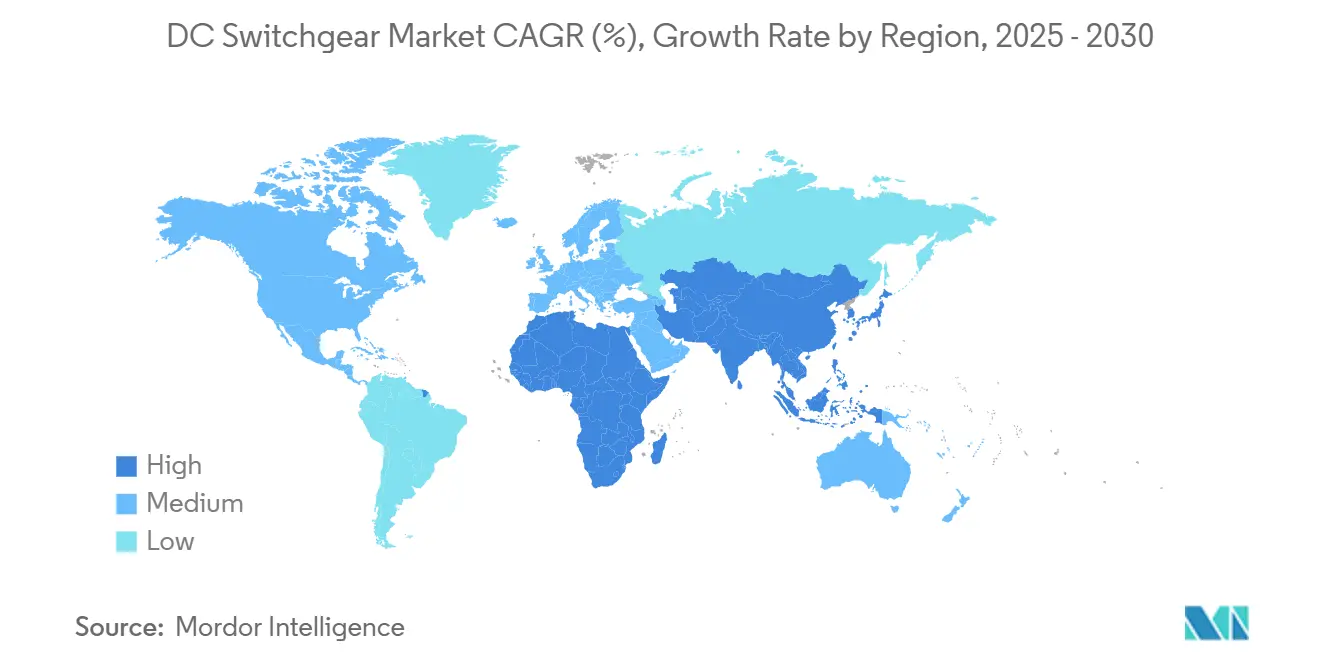

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DC Switchgear Market Analysis by Mordor Intelligence

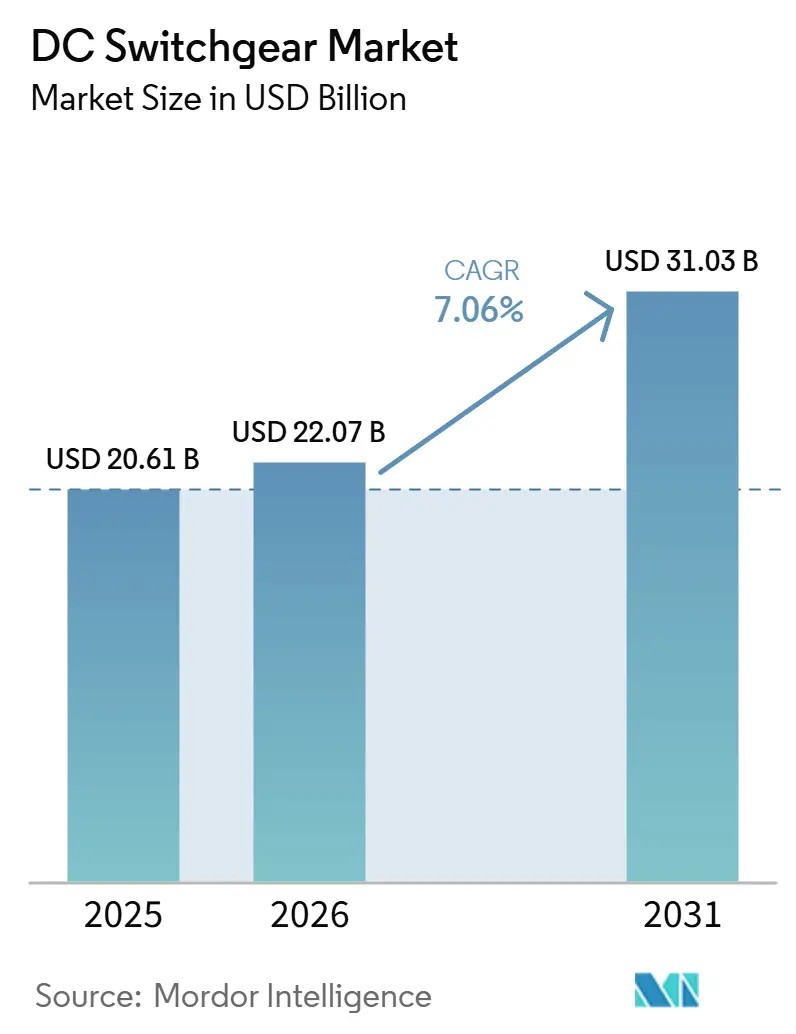

The DC Switchgear Market size is projected to be USD 20.61 billion in 2025, USD 22.07 billion in 2026, and reach USD 31.03 billion by 2031, growing at a CAGR of 7.06% from 2026 to 2031.

Accelerating investment in high-efficiency direct-current infrastructure, rapid renewable energy deployments, and the proliferation of data center, rail, and EV charging applications underpin the expansion of the DC switchgear market. Rising grid modernization budgets in the Asia-Pacific and Europe, coupled with the need to curb AC-DC conversion losses, keep demand momentum strong despite widening supply chain lead times. Medium-voltage equipment—and, increasingly, solid-state and hybrid technologies—give manufacturers room for product differentiation, while regulatory pushes to phase out SF6 spur innovation in greener insulation media. However, high upfront capital costs, vacuum-interrupter shortages, and fragmented global standards temper near-term growth prospects.

Key Report Takeaways

- By voltage, medium voltage captured 39.5% of the DC switchgear market share in 2025, and is projected to expand at a 7.9% CAGR through 2031.

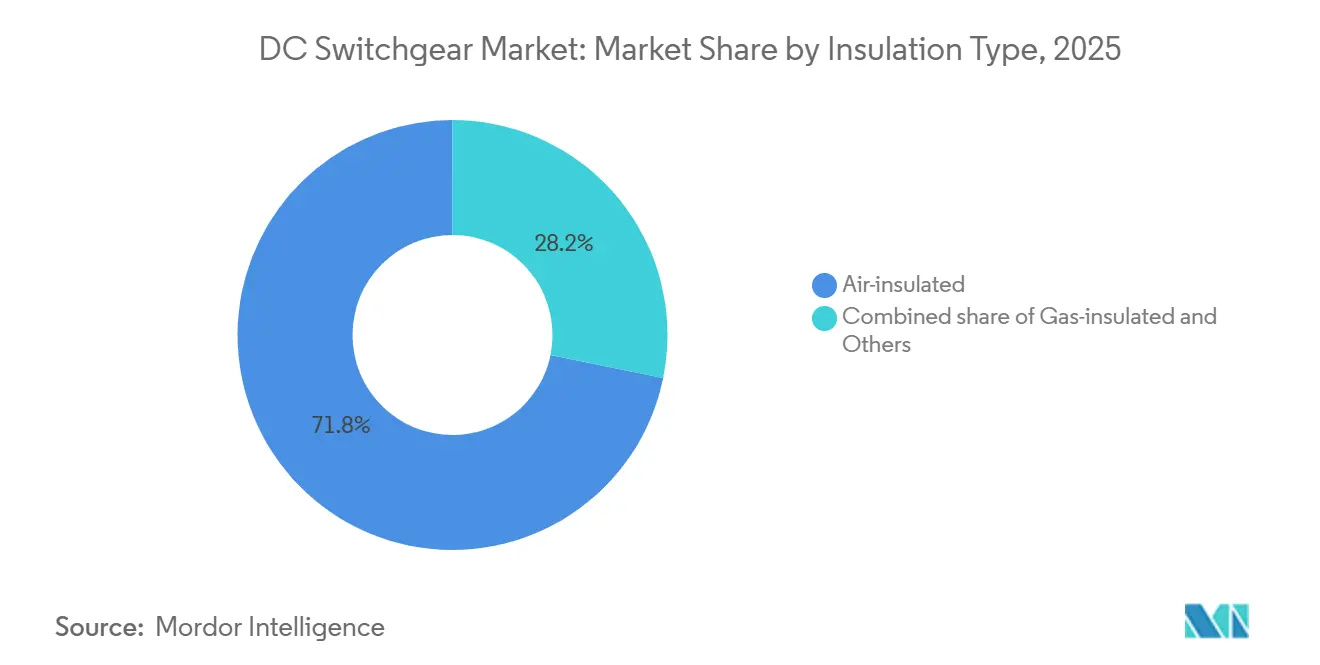

- By insulation type, air-insulated switchgear led with a 71.8% revenue share in 2025; the “Others” category, solid-state and hybrid, is expected to record the highest projected CAGR of 9.5% from 2026 to 2031.

- By installation, indoor systems accounted for a 59.2% share of the DC switchgear market size in 2025, and outdoor equipment is set to advance at an 8.2% CAGR.

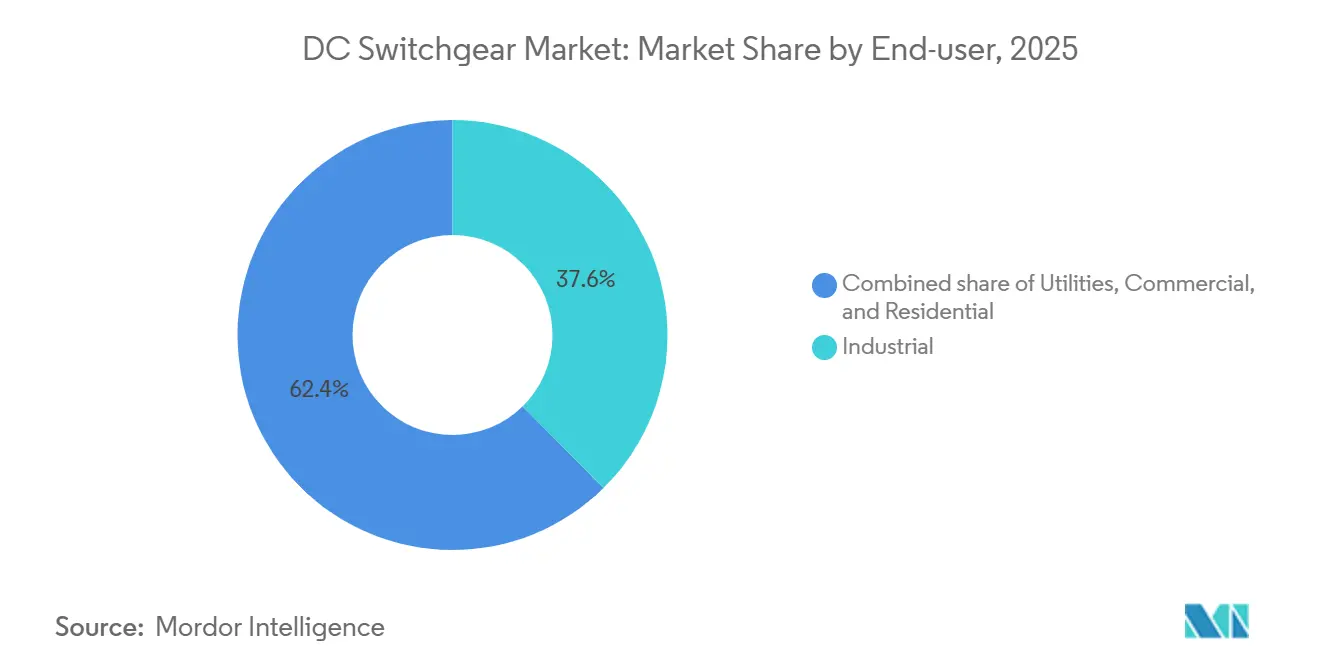

- By end-user, industrial deployments held a 37.6% share in 2025, whereas residential installations are expected to post the fastest CAGR at 8.8% through 2031.

- By geography, the Asia-Pacific region dominated with a 45.4% share in 2025 and is expected to maintain the region’s fastest growth rate of 7.7% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global DC Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy capacity additions | 1.80% | Global, APAC & Europe | Long term (≥ 4 years) |

| Rail & metro electrification surge | 1.20% | APAC core, spill-over to North America & Europe | Medium term (2-4 years) |

| Data-center DC power architectures | 1.50% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| EV fast-charging roll-outs | 0.90% | Global, led by China & Europe | Medium term (2-4 years) |

| Defence micro-grids demand | 0.40% | North America, selective APAC | Long term (≥ 4 years) |

| Offshore wind-to-hydrogen hubs | 0.70% | Europe, North Sea focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy Capacity Additions

Global wind and solar installations inherently generate direct current, eliminating AC-DC conversion losses and creating sustained demand for high-voltage DC switchgear. Offshore North Sea developers, in collaboration with Siemens Energy, GE Vernova, and Hitachi Energy, are constructing multiterminal hubs designed to integrate 70 GW of wind capacity into the EU's grids.[1]Siemens Energy, “North Sea HVDC Hubs for 70 GW Offshore Wind,” tdworld.com In India, a planned ±800 kV, 6 GW HVDC link will transmit power from the Khavda renewable complex to Nagpur, utilizing advanced switchgear.[2]Hitachi Energy, “Khavda-Nagpur ±800 kV HVDC Contract,” hitachienergy.com Similar requirements arise in the Netherlands' PosHYdon integrated wind-to-hydrogen pilot, where compact, corrosion-resistant units protect offshore electrolyzers.[3]Riviera Maritime Media, “PosHYdon Offshore Hydrogen Pilot,” rivieramm.com Legislators continue to earmark grid funds that accelerate DC switchgear uptake, as the EU targets a 45% renewables share by 2030.

Rail & Metro Electrification Surge

Mass transit agencies are phasing out diesel locomotion in favor of electric traction, a shift that relies on robust DC distribution networks. Washington’s WMATA reserved USD 99.1 million in FY 2024 for traction-power upgrades, with sizable allocations for DC switchgear replacement.[4]Washington Metropolitan Area Transit Authority, “FY 2024 Budget,” wmata.com The U.S. DOT identifies DC traction at 1,500 V-3,000 V as cost-effective for high-frequency services. Hitachi Energy’s turnkey power-supply packages illustrate the integrated approach, combining static frequency converters, isolation transformers, and high-speed breakers to manage regenerative braking currents. Safety codes specific to rail—ranging from electromagnetic-compatibility limits to fire-hardening push OEMs to design application-tailored enclosures and monitoring.

Data-Center DC Power Architectures

Operators striving to trim energy bills are redesigning white-space distribution in favor of 380 V DC buses. Eltek’s studies show 4.2% annual savings for a midsize facility switching from AC to DC. Siemens has agreed with Compass Datacenters to supply modular medium-voltage skids that incorporate DC switchgear, debuting on a Chicago-area campus during the second half of 2025. ABB’s SACE Emax 3 breaker targets AI loads with IEC 62443 cybersecurity, arc-flash detection, and DC trip units. Given a projected 16% CAGR for datacenter power systems from 2023 to 2030, demand for compact breakers, busways, and conversion hardware is expected to intensify.

EV Fast-Charging Roll-Outs

High-power public chargers operate at up to 1,500 V DC and 350 kW, placing stringent demands on switchgear regarding interruption and overheating. ABB’s DC disconnect portfolio supports continuous currents of up to 1,000 A within compact footprints, making them well-suited for curbside pedestals. Eaton’s USD 750 million factory expansion in the Dominican Republic specifically targets components for EV chargers and renewable projects. European regulators project 30 million EVs by 2030, a milestone that will multiply charger installations and reinforce the DC switchgear market. Bidirectional vehicle-to-grid designs introduce additional complexity, requiring ultrafast solid-state devices capable of safely reversing current.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex versus AC switchgear | -1.10% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Absence of global DC standards | -0.80% | Global, varying by region | Medium term (2-4 years) |

| Thermal-runaway risk in solid-state breakers | -0.50% | Advanced markets | Medium term (2-4 years) |

| Vacuum-interrupter supply bottlenecks | -0.90% | Global, high-demand regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex Versus AC Switchgear

DC projects still command a noticeable premium over comparable AC builds, an obstacle largely dominated by the high cost of converter stations and specialized protection equipment. Electrical Engineering Portal data indicate that cost parity typically emerges on routes exceeding 600 km or in undersea links. NREL modeling highlights the limited economies of scale for DC components, as global production volumes remain modest. Escalating lead times now beyond 92 weeks for breakers—inflate contingency budgets and discourage early adopters in emerging regions. Developers often oversize AC alternatives to hedge parts shortages, further delaying DC uptake.

Absence of Global DC Standards

While IEC 60947-2:2024 covers devices up to 1,500 V DC, higher ranges lack universal protocols, compelling OEMs to craft site-specific designs and swelling project engineering hours. CIGRE working groups stress that multivendor MVDC systems will not scale until hardware and communication layers are harmonized. IEEE initiatives aimed at codifying DC-building wiring practices remain incomplete, prolonging uncertainty for contractors. The READY4DC consortium underlines interoperability risks for European HVDC grids if manufacturers continue to apply proprietary protection algorithms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: Medium Voltage Commands Growth Leadership

The medium-voltage segment accounted for a 39.5% share of the DC switchgear market in 2025 and is forecast to post a 7.9% CAGR through 2031, thereby playing a significant role in overall market expansion. The DC switchgear market size for medium voltages benefits from its sweet spot balance of current-handling capability and cost, making it ideal for industrial plants, renewable energy feeders, and urban rail networks. Siemens Energy’s MVDC PLUS platform claims 20-80% transmission-capacity gains over comparable AC alternatives, bolstering its value proposition. Demand is further reinforced by battery-energy-storage systems that increasingly standardize on 1.5-35 kV link voltages to simplify containerized designs.

Low-voltage equipment, below 1.5 kV, enjoys a broad installed base in data centers and residential solar, but shows slower growth as penetration matures. High-voltage (>52 kV) projects are accelerating in tandem with UHVDC corridor investments in China and large offshore wind link contracts in Europe. Although high-voltage projects drive marquee order values, the technological complexity and lengthy permitting processes temper year-to-year shipment volumes. As a result, medium-voltage remains the principal revenue stream for most OEMs and the primary competitive arena for solid-state innovation.

By Insulation Type: Air-Insulated Dominance Faces Solid-State Disruption

Air-insulated assemblies retained a 71.8% share in 2025, owing to their proven designs and low initial costs. Yet the category recorded only moderate expansion as buyers pilot solid-state and hybrid solutions promising significant loss reductions. “Others,” which includes ABB’s IEC-certified SACE Infinitus solid-state breaker, is projected for a 9.5% CAGR, the fastest within the DC switchgear market. Gas-insulated units are used in premium applications aboard offshore platforms and urban substations, where their compact footprints offset higher capital expenses.

Global efforts to eliminate SF6 accelerate demand for vacuum-based or alternative-gas designs, prompting air-insulated and gas-insulated manufacturers to retrofit with greener media. Hitachi Energy delivered the first 550 kV SF6-free GIS to China in May 2025, a milestone that will influence future tender requirements. Conversely, solid-state adoption is hindered by thermal-management hurdles and higher prices, yet its maintenance-free operation appeals to data centers and semiconductor plants.

By Installation: Indoor Applications Lead Despite Outdoor Acceleration

Indoor installations accounted for 59.2% of deployments in 2025, supported by factory floors, hyperscale data centers, and commercial buildings that require climate-controlled environments. Vendors tout lower lifetime cost, cleaner operating conditions, and easier serviceability to maintain dominance. The DC switchgear market size for indoor setups remains sizable, but expansion slows as major industrial users finish multi-year modernization cycles.

Outdoor-rated switchgear, including pad-mounted metal-clad assemblies and containerized modular rooms, is on track for an 8.2% CAGR. Solar and wind plants, public EV hubs, and remote microgrids prefer outdoor designs that simplify civil works and resist dust, salt spray, and ultraviolet exposure. Advances in enclosure coatings, IP67 sealing, and space-optimized GIS chambers enable quicker commissioning in rugged climates. The trend also spurs hybrid “semi-indoor” offerings, where weather-tight e-houses house DC equipment adjacent to process areas.

By End-user: Industrial Dominance with Residential Emergence

Industrial processes captured a 37.6% share in 2025, using DC for variable-speed drives, electrolysis, and advanced robotics. Growth moderates as penetration levels off among early-moving sectors, such as metals and chemicals. Nonetheless, brownfield modernization and process electrification keep replacement demand resilient. The data-center and commercial segments add fresh volume as cloud operators build 100 MW-class campuses, requiring thousands of breaker poles.

Although starting from a small base, residential adoption is expected to exhibit the highest 8.8% CAGR, driven by rooftop solar, battery storage, and bidirectional home fast chargers. DOE programs that subsidize smart-home upgrades encourage builders to pre-wire dwellings for DC plugs and USB-C outlets, boosting shipment visibility through 2031. Transportation, encompassing rail, marine, and EV infrastructure, also posts double-digit gains, but order timing swings with public-funding cycles. Defense and mining remain niche but profitable, commanding specialized ruggedization and cybersecurity features.

Geography Analysis

The Asia-Pacific’s gravitational pull in the DC switchgear market is driven by unparalleled capital-investment cycles and supportive industrial policies. State Grid’s documented spending spree and India’s transmission PPP initiatives funnel multibillion-dollar tenders to global and domestic OEMs. Technology transfer agreements linked to these projects provide regional suppliers with new competencies, further solidifying DC ecosystems.

Europe continues to champion SF6-free regulations and promote the development of cross-border HVDC corridors. The North Sea Wind Power Hub envisions interconnected energy islands, each demanding multiterminal switchgear rated well above 300 kV. Funding mechanisms under the EU’s TEN-E framework prioritize such projects, assuring predictable procurement pipelines.

North American deployments focus on data-center clusters in the Midwest and renewable intertie expansions in Texas and California. Federal tax incentives enacted under the Inflation Reduction Act prolong the order cycle for grid-scale batteries, catalyzing demand for medium-voltage DC switchgear with energy-storage-optimized protection logic.

South America’s adoption pivots on utility-scale solar in Chile and Brazil. Currency volatility and constrained public budgets temper the broader diffusion, yet multilateral bank financing sustains landmark HVDC corridor builds. The Middle East & Africa see spot demand tied to desalination plants, onshore wind in Egypt, and oil-and-gas electrification in Saudi Arabia, each requiring corrosion-resistant, high-ambient-temperature housings.

Competitive Landscape

Market leadership remains contested among ABB, Siemens Energy, and Schneider Electric, each leveraging broad portfolios and digital-asset management suites. ABB’s IEC-approved solid-state breaker represents a first-mover advantage in low-loss, maintenance-free switching. Siemens Energy foregrounds SF6-free gas-insulated lines, aligning with EU decarbonization mandates. Schneider Electric integrates EcoStruxure analytics to manage predictive maintenance and optimize asset lifecycles.

Eaton, Mitsubishi Electric, and Hitachi Energy are expanding their manufacturing footprints in the United States and Europe to reduce 90-week lead times and meet Buy-America thresholds. Powell Industries leverages its high domestic content to secure investor-owned utility frame contracts, while Fuji Electric and Toshiba maintain strong positions in Japanese transit electrification.

Specialist entrants, such as Meidensha, LS Electric, and Zhenfa Hi-tech, chase solid-state and modular e-house niches, often collaborating with semiconductor firms to overcome thermal runaway challenges. Supply-chain resilience, notably vacuum-interrupter access, emerges as a decisive differentiator; firms with captive ceramics lines enjoy superior schedule control.

Digital twins, cybersecurity accreditation, and lifecycle-service guarantees now weigh heavily in bid evaluations. Vendors coupling hardware with cloud monitoring clinch multiyear service revenues, offsetting margins eroded by raw-material inflation.

DC Switchgear Industry Leaders

ABB Ltd.

Siemens Energy

Schneider Electric

Eaton Corporation

Mitsubishi Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hitachi Energy announced a USD 70 million expansion in Pennsylvania to produce EconiQ SF6-free high-voltage switchgear and breakers.

- March 2025: ABB completed the acquisition of Siemens’ wiring accessories business in China, adding USD 150 million in revenue in 2024.

- March 2025: ABB confirmed USD 120 million U.S. production capacity expansion, including a new 320,000 sq ft Tennessee facility.

- February 2025: Eaton committed USD 340 million to a South Carolina transformer factory, creating 700 jobs.

Global DC Switchgear Market Report Scope

| Low Voltage (Up to 1.5 kV) |

| Medium Voltage (1.5 to 52 kV) |

| High Voltage (Above 52 kV) |

| Air-insulated |

| Gas-insulated |

| Others |

| Indoor |

| Outdoor |

| Utilities |

| Commercial |

| Residential |

| Industrial |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Voltage | Low Voltage (Up to 1.5 kV) | |

| Medium Voltage (1.5 to 52 kV) | ||

| High Voltage (Above 52 kV) | ||

| By Insulation Type | Air-insulated | |

| Gas-insulated | ||

| Others | ||

| By Installation | Indoor | |

| Outdoor | ||

| By End-user | Utilities | |

| Commercial | ||

| Residential | ||

| Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the DC switchgear market in 2025?

The DC Switchgear Market size is projected to be USD 20.61 billion in 2025, USD 22.07 billion in 2026, and reach USD 31.03 billion by 2031, growing at a CAGR of 7.06% from 2026 to 2031.

Which voltage class grows fastest?

Medium-voltage assemblies, covering 1.5-52 kV, lead expansion at a 7.9% CAGR thanks to utility, industrial, and transit projects.

Why are solid-state breakers gaining attention?

They slash energy losses by up to 70%, enable microsecond switching, and cut maintenance, although higher cost and heat management still limit adoption.

What role does Asia-Pacific play?

Asia-Pacific commands 45.4% of 2025 revenue and sustains the highest 7.7% regional CAGR, driven by massive Chinese and Indian grid investment.

How are SF6-free regulations influencing the market?

EU and Chinese mandates to phase out SF6 are steering buyers toward vacuum and alternative-gas options, prompting rapid product redesigns among leading OEMs.

What are current supply-chain challenges?

Vacuum-interrupter shortages and transformer bottlenecks push delivery times for medium-voltage switchgear past 90 weeks, forcing buyers to pre-order and vendors to onshore capacity.

Page last updated on: