Medium Voltage Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 43.47 Billion |

| Market Size (2031) | USD 55.08 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

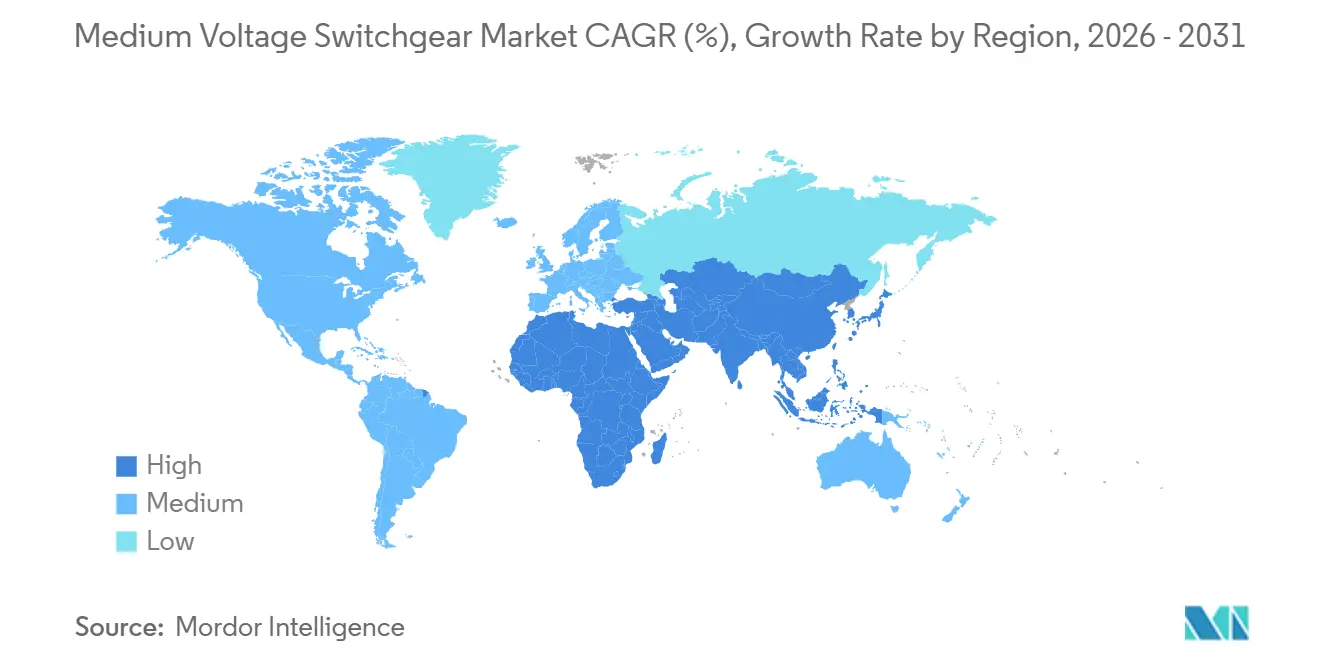

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

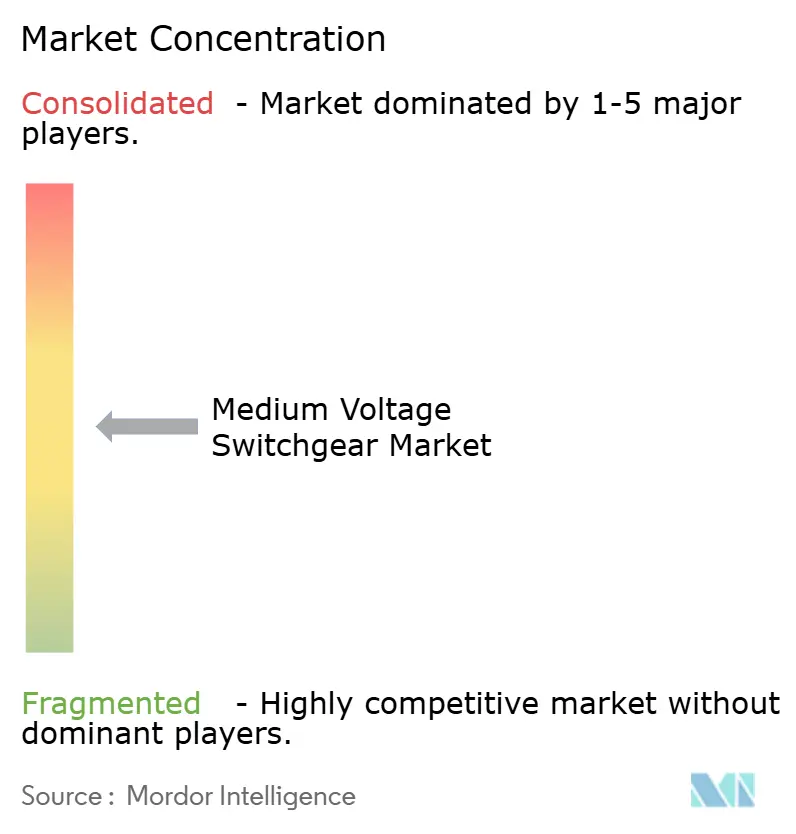

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medium Voltage Switchgear Market Analysis by Mordor Intelligence

The Medium Voltage Switchgear Market size is expected to grow from USD 41.62 billion in 2025 to USD 43.47 billion in 2026 and is forecast to reach USD 55.08 billion by 2031 at 4.85% CAGR over 2026-2031.

Transmission and distribution modernization programs, mandates to integrate renewable generation, and the rapid uptake of compact gas-insulated equipment in space-constrained assets such as data centers and urban micro-substations are shaping demand. Although air-insulated designs retained a 43.1% medium-voltage switchgear market share in 2025, the strongest growth is shifting toward solid-dielectric, vacuum, and fluoronitrile-based “clean-air” systems as the European Union phases out SF₆ in stages. Direct-current architectures are also gaining traction, especially in hyperscale computing facilities moving to 48 VDC and 380 VDC distribution. Asia-Pacific remains pivotal, accounting for 40.3% of 2025 revenue and benefiting from multi-billion-dollar grid investments across China, India, and the ASEAN bloc. Indoor installations led with 61.5% of deployments thanks to urban land pressures, while the residential segment is the fastest-growing end-user as rooftop solar, home storage, and neighborhood microgrids proliferate.

Key Report Takeaways

- By insulation, air-insulated switchgear held 43.1% of 2025 revenue; SF₆-free alternatives are forecast to advance at a 10.5% CAGR through 2031.

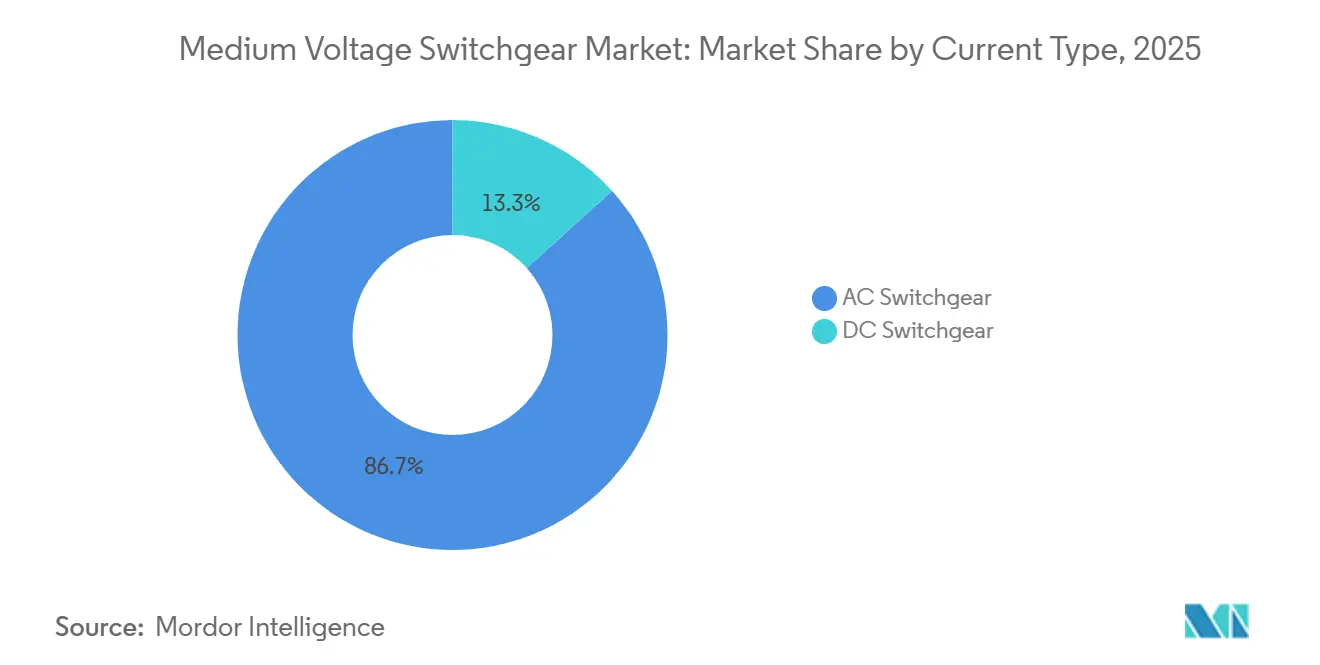

- By current type, AC equipment captured 86.7% of the 2025 medium-voltage switchgear market size, while DC variants are rising at a 6.3% CAGR to 2031.

- By installation, indoor configurations represented 61.5% of 2025 revenue and are set to expand at a 5.7% CAGR over the forecast period.

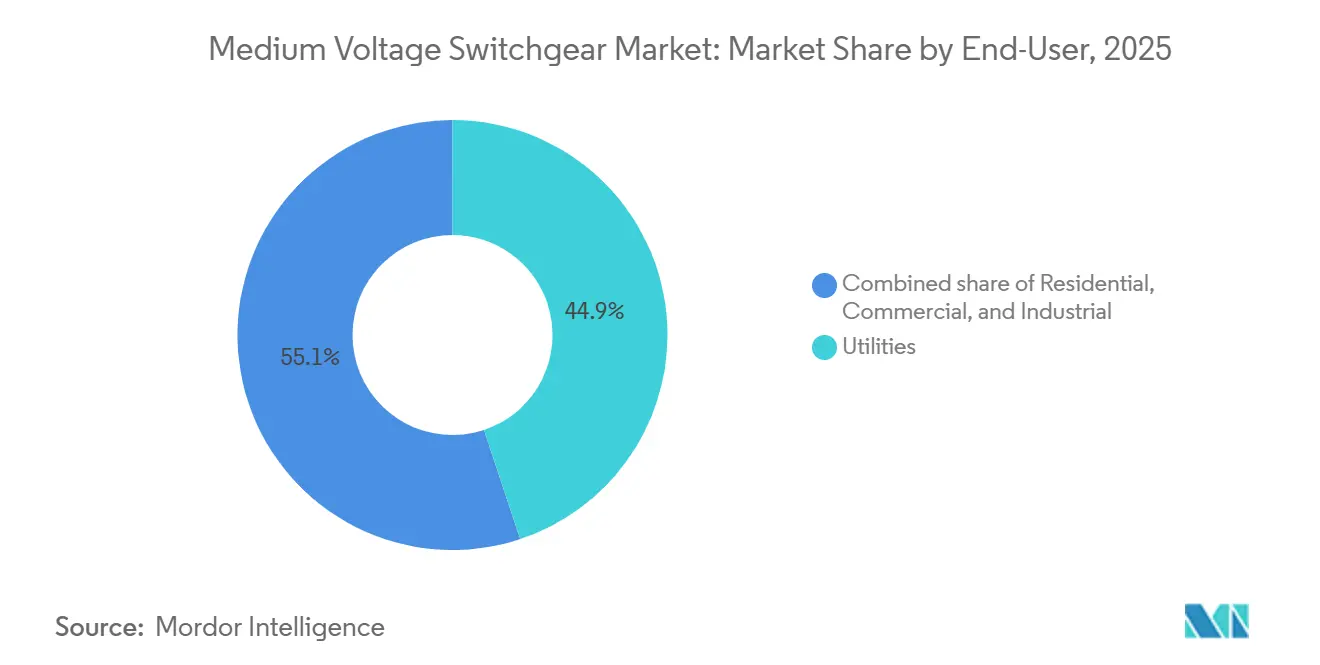

- By end-user, utilities controlled 44.9% of 2025 spending; the residential segment is accelerating at a 7.2% CAGR on the back of distributed energy resources.

- By geography, Asia-Pacific generated 40.3% of global revenue in 2025 and is projected to grow at a 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medium Voltage Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| T&D infrastructure investments | +1.2% | North America, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Renewable-integration upgrade cycle | +1.0% | Asia-Pacific, Europe, South America | Long term (≥ 4 years) |

| Urban reliability & micro-substation build-out | +0.6% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Smart-grid & digital substation roll-outs | +0.5% | North America, Europe, early adoption in South Korea, Japan | Medium term (2-4 years) |

| Data-center-led demand for compact GIS | +0.4% | North America, Europe, Singapore, Hong Kong | Short term (≤ 2 years) |

| Undergrounding projects in dense cities | +0.3% | Europe, North America, select Asia-Pacific metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

T&D Infrastructure Investments

Utilities are ramping up capital outlays to replace aging assets and ease capacity bottlenecks. The U.S. spent USD 50.9 billion on distribution assets in 2023, with substation equipment absorbing USD 6.1 billion.[1]U.S. Energy Information Administration, “Electric Power Annual 2023,” eia.gov Washington followed with USD 10 billion for grid hardening and another USD 12.7 billion across GRIP and transmission facilitation programs in 2024. ASEAN members have earmarked USD 290 billion for cross-border interconnections through 2035.[2]ASEAN Centre for Energy, “ASEAN Energy Infrastructure Outlook,” aseanenergy.org Because each new substation typically installs 4-12 medium-voltage bays, these allocations funnel directly into the medium-voltage switchgear market. Modular factory-built yards are shortening construction schedules by 20-30%, allowing owners to energize capacity sooner and cut overrun risk.

Renewable-Integration Upgrade Cycle

Variable renewables now compel grid operators to handle bidirectional power and quicker fault clearing. India’s cumulative renewable base hit 203 GW in 2024, and meeting its 500 GW 2030 target requires INR 5.75 trillion (USD 69 billion) of grid upgrades. China installed 300 GW of new renewables in 2024 and budgeted USD 546 billion for network expansion.[3]State Grid Corporation of China, “Annual Report 2024,” sgcc.com.cn IEEE-2800 is pushing for IEC 61850-ready protection schemes, while Europe’s 111 GW offshore wind fleet requires marine-rated gear. The International Energy Agency foresees 1,200 GW of variable renewables on grids by 2030, translating into a 40% rise in medium-voltage switchgear at collection points.[4]International Energy Agency, “Renewable Energy Market Update 2024,” iea.org

Urban Reliability & Micro-Substation Build-Out

Dense cities are installing micro-substations to curb outages and hide equipment. Con Edison’s USD 5 billion plan in New York deploys 27 kV and 13.8 kV compact yards inside buildings. London has invested GBP 3 billion (USD 3.8 billion) in underground cables and secondary substations. Singapore mandates 24 kV and 36 kV GIS in land-scarce zones. Seismic-resilient underground stations in Tokyo further highlight urban demand. Each micro-facility usually needs only a handful of bays, but the high number of sites aggregates to meaningful volumes in the medium-voltage switchgear market.

Smart-Grid & Digital Substation Roll-Outs

IEC 61850 process-bus architectures cut commissioning time by up to 40% and enable predictive maintenance that reduces unplanned outages by 20-30%. The United States has earmarked USD 96 billion over five years for smart-grid deployments. Siemens Energy’s Blue GIS embeds sensors that watch gas density, temperature, and partial discharge in real time. Schneider Electric links switchgear to cloud analytics to detect failure patterns months in advance. South Korea has already digitized 40% of its distribution network, trimming outage duration by 25%. Cyber-secure communication per IEC 62351 now adds roughly 8% to system cost but is rapidly becoming mandatory for critical infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SF₆ environmental restrictions | -0.8% | Europe (immediate), North America & Asia-Pacific (phased) | Short term (≤ 2 years) |

| High capex of GIS vs AIS | -0.5% | Global, acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Supply-chain lead-time spikes post-2023 | -0.3% | Global, lingering in North America and Europe | Short term (≤ 2 years) |

| Solid-state protection cannibalizing MV bays | -0.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SF₆ Environmental Restrictions

The EU bans SF₆ in ≤24 kV gear from January 2026 and in 24-52 kV equipment by 2030. ABB’s AirPlus and Siemens Energy’s Blue GIS reduce global-warming potential 99% but add 8-12% to cost. Vacuum interrupters, dominant in Japan, remove gas altogether yet top out at 40.5 kV. The United States still relies on voluntary SF₆ curbs, letting OEMs ship legacy designs to unregulated regions.

High Capex of GIS vs AIS

A 24 kV GIS bay costs USD 80,000-120,000 versus USD 50,000-70,000 for AIS, curbing uptake in price-sensitive grids. However, lifecycle studies show GIS can be 15-20% cheaper in dense cities once land and downtime are priced in. Rural electrification in India and sub-Saharan Africa still favors AIS despite larger footprints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insulation: SF₆-Free Alternatives Reshape Competitive Dynamics

Alternative insulation platforms are expanding at a 10.5% CAGR, far faster than the mature gas-insulated and the cost-oriented air-insulated lines. The European SF₆ prohibition for ≤24 kV gear from 2026 and for up to 52 kV by 2030 is the primary catalyst. Solid-dielectric and vacuum technologies eliminate gas leakage and double maintenance intervals to every 10 years. Vacuum circuit breakers already command 70% of Japan’s medium-voltage market.

Air-insulated gear keeps its cost edge, especially in rural or industrial lots where footprint is secondary. Gas-insulated lines remain the choice for data centers, offshore installations, and dense cities because they occupy up to 40% less floor space. Clean-air GIS, launched by Hitachi Energy in 2024, secured its first 145 kV order in Germany. The premium for SF₆-free designs is shrinking as economies of scale build, but capital-tight utilities in developing regions still rely on AIS. Even so, the ongoing substitution means the medium-voltage switchgear market will see rapid share shifts toward clean alternatives over the forecast horizon.

By Current Type: DC Architectures Gain Traction in Data Centers and Renewables

AC equipment retained 86.7% share of the 2025 medium-voltage switchgear market size, reflecting its entrenched role in long-distance transmission. Yet DC switchgear is rising 6.3% annually as hyperscale cloud firms adopt 380 VDC buses to eliminate conversion losses. The U.S. NEVI program’s 500,000 fast chargers also require medium-voltage DC interface gear.

Solar-plus-storage developers are coupling PV arrays with batteries on a shared DC bus, improving round-trip efficiency 3-5 percentage points. India’s 15 GW of DC-coupled solar-storage illustrates the opportunity. Though DC bays cost 15-20% more than AC, efficiency savings and smaller footprints offset the premium in data centers, EV charging hubs, and renewables. Eaton’s 1,500 VDC portfolio with 2-millisecond solid-state interruption lowers a past technical barrier.

By Installation: Indoor Configurations Dominate Urbanization and Digitalization

Indoor switchgear represented 61.5% of 2025 revenue and is on track for a 5.7% CAGR through 2031. Compact GIS saves up to 40% of floor space, critical where land costs top USD 500 per m². Singapore’s regulator requires indoor substations for new urban developments, pushing 24 kV and 36 kV GIS as de facto standards.

Outdoor AIS, still cheaper upfront, holds sway in rural electrification drives. India’s village program continues to specify outdoor line-ups at USD 50,000-70,000 per bay. Nevertheless, urban planners prefer indoor yards because IEC 61850 servers, fiber gateways, and cybersecurity hardware need climate-controlled environments. Schneider Electric’s edge devices now ship IP54-rated enclosures bundled with switchgear, reinforcing the indoor pivot.

By End-User: Residential Segment Leads Growth Amid Electrification Wave

Utilities commanded 44.9% of 2025 spending, but residential demand is advancing 7.2% annually, the fastest among segments. U.S. households added 6.8 GW of rooftop solar and 10.6 GWh of battery storage in 2024, a 55% increase year-on-year. Community microgrids that aggregate dozens of homes behind a shared medium-voltage lineup are multiplying.

Commercial campuses adopt onsite solar and storage to cut demand charges, while mines in Australia, Chile, and South Africa electrify heavy equipment, boosting orders for robust 11 kV and 33 kV switchgear. Codelco’s USD 1.5 billion electrification drive illustrates mining’s pull. The distributed trend shifts capex from central substations toward neighborhood and facility-level switchgear, underpinning medium-voltage switchgear market growth despite emerging volume-reduction technologies.

Geography Analysis

Asia-Pacific generated 40.3% of 2025 revenue and is forecast to grow at a 6.8% CAGR through 2031. China’s USD 546 billion grid plan covers everything from ultra-high-voltage lines to district-level automation. India is channeling INR 5.75 trillion (USD 69 billion) into evacuation corridors for its 500 GW renewable ambition. ASEAN is investing USD 290 billion to stitch together a regional supergrid.

Washington’s USD 13 billion modernization package, plus Canada’s net-zero-electricity goal by 2035, gives the region strong forward visibility. Data-center clustering in Northern Virginia and the Pacific Northwest adds a concentrated pocket of demand for SF₆-free GIS. Europe’s roadmap revolves around integrating 300 GW of offshore wind by 2050 and decarbonizing distribution networks per the Green Deal. Germany alone earmarked EUR 20 billion for north-south corridors, while the United Kingdom plans GBP 58 billion in network upgrades.

The Middle East and Africa are smaller but are accelerating. Saudi Arabia’s USD 500 billion NEOM project and the UAE’s USD 163 billion grid program prioritize compact, digital gear for smart-city campuses. South America benefits from Brazil’s 7,000 km transmission expansion and Chile’s mining electrification initiatives, while Australia integrates 5 GW of new renewables annually and scales battery storage to balance its high variable-renewable system.

Mordor Intelligence provides coverage of the medium voltage switchgear market across other key regional markets, including Europe, Middle East and Africa, North America, and Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The five largest suppliers, Siemens Energy, Schneider Electric, Hitachi Energy, ABB, and Eaton, control about half of global revenue, with regional challengers such as CHINT, Hyosung, and CG Power adding another 15-20%. The strategic battleground spans SF₆-free technology, digital substations, and emerging DC platforms. Siemens Energy’s Blue GIS, certified to IEC 62271-1, posted more than 50 European installs by late-2024. ABB lifted Electrification revenue 16% year-on-year in Q3 2024 on data-center and renewable orders. Schneider Electric’s cloud-linked monitoring reduces unplanned downtime by up to 30% and has become a key differentiator.

Eaton’s xEnergy 1,500 VDC gear is among the first utility-grade DC offerings, landing contracts with hyperscale operators. NOJA Power is finding success with reclosers for rural fault isolation, while Ormazabal tailors compact stations for Latin America at a cost of 15-20% below European imports. IEC 62351 cybersecurity compliance raises R&D hurdles, favoring incumbents with deeper engineering benches and certification pipelines.

Medium Voltage Switchgear Industry Leaders

Schneider Electric SE

Siemens AG

Hitachi ABB Power Grids Ltd

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: In 2025, Hyosung Heavy Industries secured a KRW 120 billion (approximately USD 82 million) contract to supply ultra-high-voltage transformers to the UK. The deal with SP Energy Networks, part of ScottishPower, supports a wind power project aligned with the UK’s carbon neutrality goals.

- September 2025: Eaton introduced its xEnergy medium-voltage DC platform with 2 ms solid-state interruption capability and booked early hyperscale data-center orders.

- June 2024: CG Power secured a USD 120 million contract from Power Grid Corporation of India for 145 kV and 245 kV switchgear supporting renewable corridors.

- June 2024: Hitachi Energy committed USD 300 million to expand its South Carolina plant for SF₆-free GIS production, targeting a 2027 ramp-up.

- March 2024: CHINT Group announced a USD 200 million switchgear hub in Saudi Arabia to meet Vision 2030 localization mandates.

Global Medium Voltage Switchgear Market Report Scope

A medium voltage switchgear is a collection of electrical equipment housed in a predominantly metal structure. This centralized set contains numerous switches, transformers, fuses, and circuit breakers. Electrical panels are used to better safeguard, control, and isolate electrical equipment. The global medium voltage switchgear market report includes:

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Insulation | Gas Insulated Switchgear (GIS) | |

| Air Insulated Switchgear (AIS) | ||

| Others | ||

| By Current Type | AC Switchgear | |

| DC Switchgear | ||

| By Installation | Indoor | |

| Outdoor | ||

| By End-User | Utilities | |

| Residential | ||

| Commercial | ||

| Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the medium-voltage switchgear market in 2031?

It is expected to reach USD 55.08 billion, reflecting a 4.85% CAGR from 2026 to 2031.

Which insulation technology is growing fastest?

SF₆-free options using solid dielectrics, vacuum, and fluoronitrile-based clean air are expanding at a 10.5% CAGR as regulators restrict SF₆ use.

Why is Asia-Pacific the largest regional contributor?

Massive grid investments in China and India, coupled with rapid urbanization and renewable additions, give Asia-Pacific a 40.3% revenue share and the highest growth rate.

How is the residential segment influencing demand?

Rooftop solar and battery adoption are driving a 7.2% CAGR for residential installations, shifting switchgear spending toward neighborhood microgrids.

What role does digitalization play in market growth?

IEC 61850-compliant digital substations cut commissioning time up to 40% and enable predictive maintenance, reinforcing demand for intelligent switchgear.

How are SF₆ bans shaping product development?

The EU’s phased ban compels OEMs to commercialize clean-air and fluoronitrile-based GIS, accelerating the shift to low-GWP equipment worldwide.

Page last updated on: