DC Circuit Breaker Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.72 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

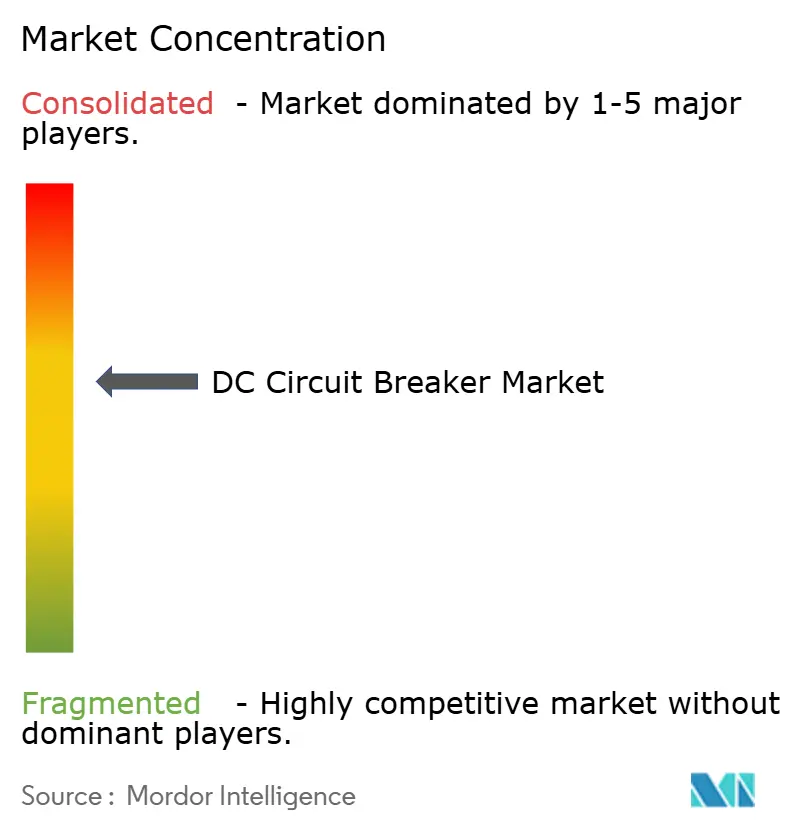

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DC Circuit Breaker Market Analysis by Mordor Intelligence

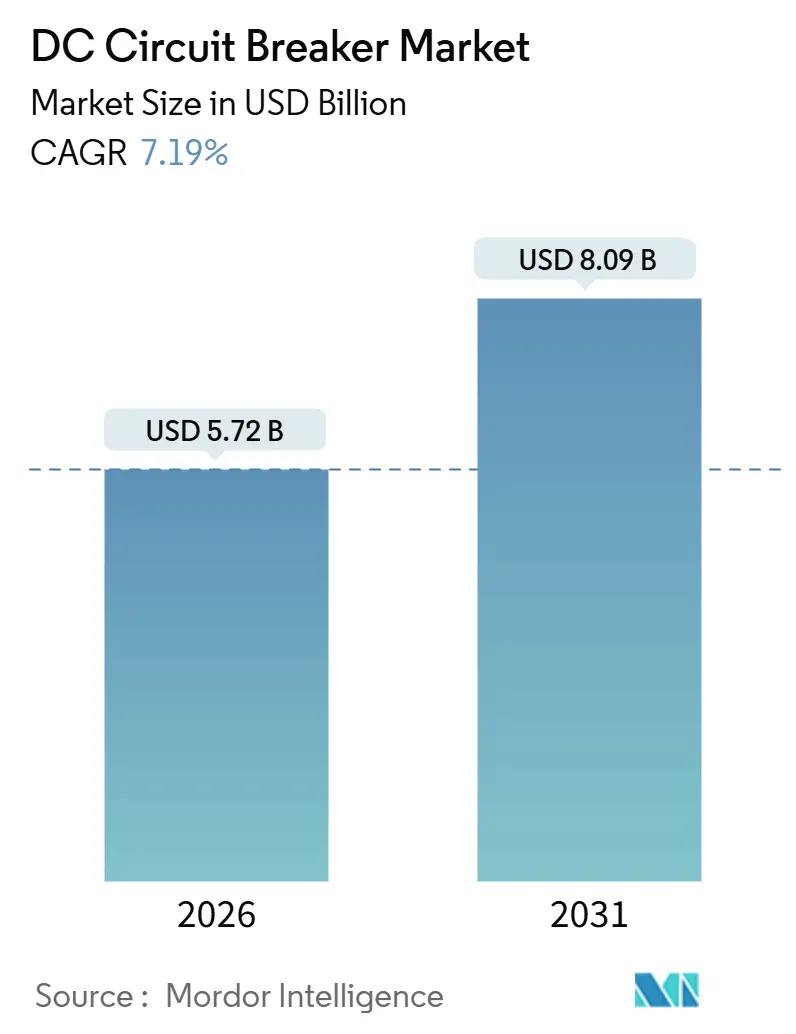

The DC Circuit Breaker Market size is estimated at USD 5.72 billion in 2026, and is expected to reach USD 8.09 billion by 2031, at a CAGR of 7.19% during the forecast period (2026-2031).

Growth is propelled by ultra-high-voltage direct-current (HVDC) transmission corridors, rapid rail electrification, and the data-center pivot toward 800 VDC busways, each of which requires fault-clearing speeds unattainable with legacy alternating-current devices.[1]ABB, “SafeRing Fluoronitrile Switchgear,” abb.com The European Union’s phased ban on sulfur-hexafluoride (SF₆) insulation, effective January 2026 for equipment up to 24 kV, is accelerating the shift to vacuum and solid-state technologies.[2]European Commission, “Regulation (EU) 2024/573,” ec.europa.eu Asia-Pacific leads adoption as China, India, and Vietnam commission new HVDC links and metro lines, while North America and Europe see retrofit demand as utilities replace oil-filled switchgear. Competitive strategies now concentrate on securing silicon-carbide wafer supply, embedding proprietary breaker modules into converter stations, and achieving IEC 62271-100 certification for SF₆-free gases.[3]Siemens Energy, “blue GIS Portfolio,” siemens-energy.com

Key Report Takeaways

- By type, solid-state units held 76.3% revenue share in 2025, whereas hybrid designs are forecast to expand at an 8.8% CAGR through 2031.

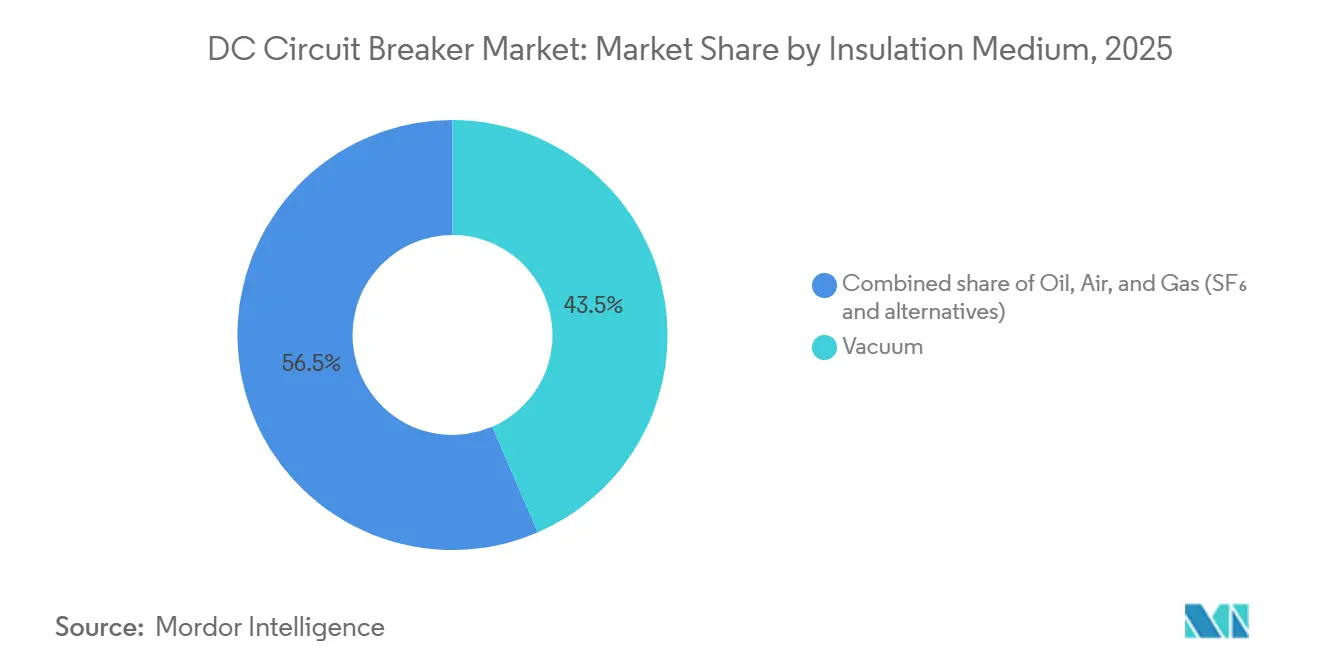

- By insulation medium, vacuum breakers captured 43.5% of the DC circuit breaker market share in 2025 and will grow at a 7.7% CAGR to 2031.

- By voltage rating, medium-voltage products led with 48.1% of the DC circuit breaker market size in 2025, while the high-voltage segment is advancing at a 10.5%.

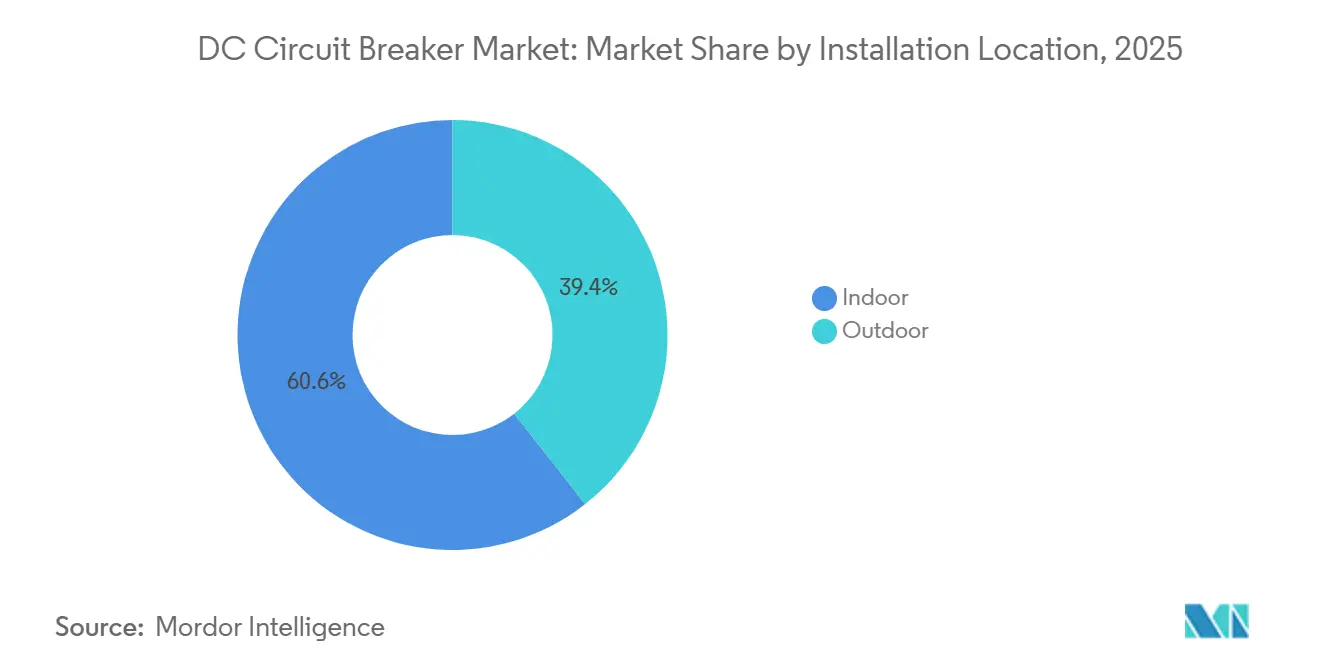

- By installation location, indoor units dominated with a 60.6% share in 2025; outdoor models are projected to grow the fastest at a 9.2% CAGR.

- By operating mechanism, mechanical designs controlled a 44.9% share in 2025, whereas solid-state-actuated breakers will register an 11.6% CAGR through 2031.

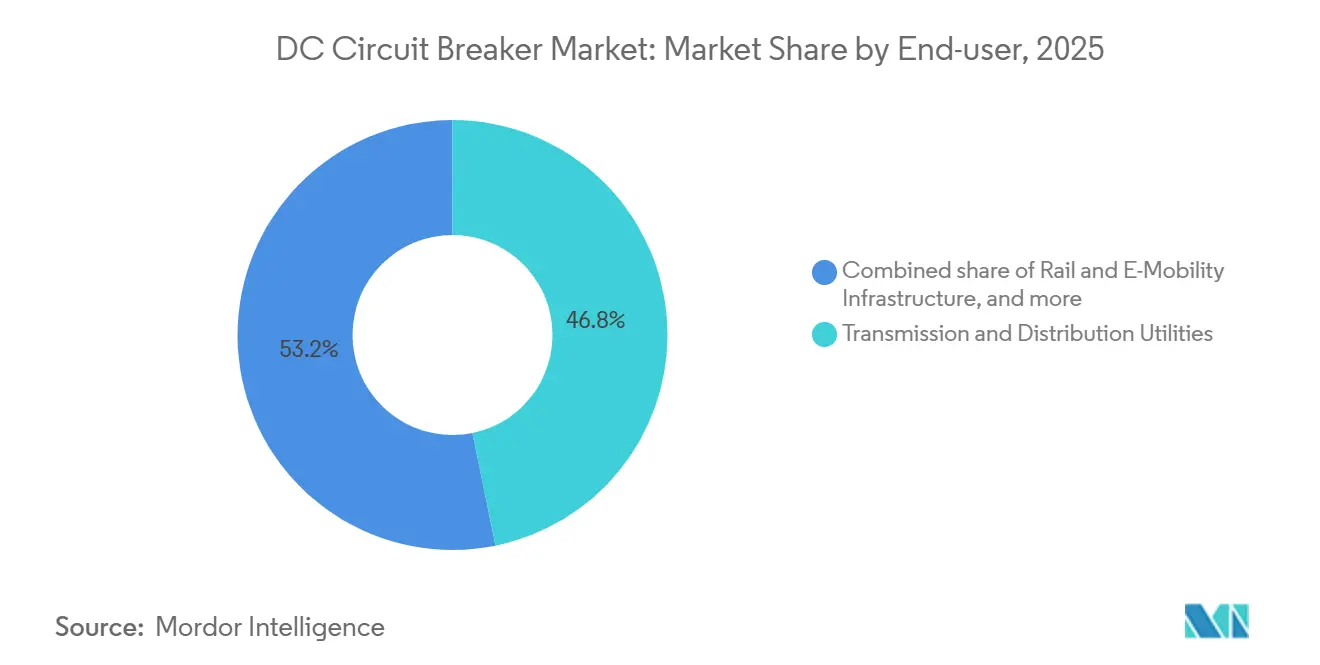

- By end-user, transmission and distribution utilities accounted for 46.8% of 2025 revenue, yet rail and e-mobility are the fastest-growing segments at an 11.1% CAGR.

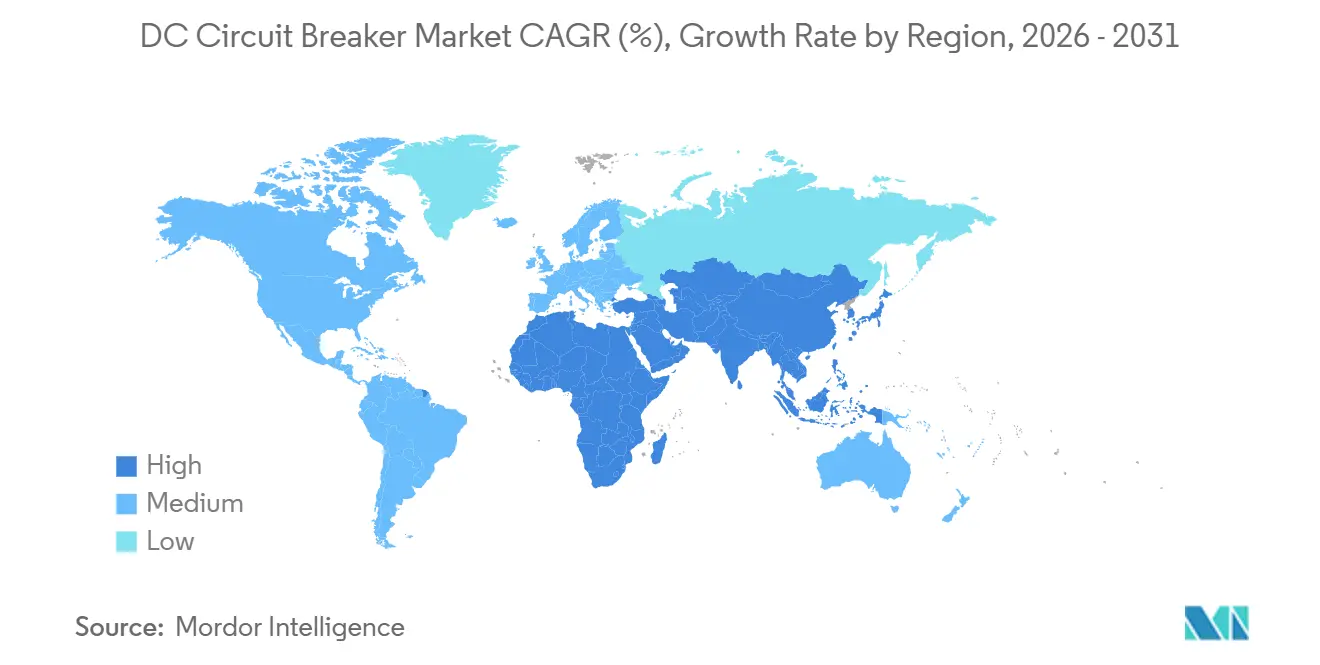

- By geography, Asia-Pacific commanded a 39.7% share in 2025 and is set to maintain the highest regional CAGR of 9.4% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global DC Circuit Breaker Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in renewable-linked DC networks | 1.40% | China, India, EU offshore wind | Medium term (2-4 years) |

| Rapid build-out of HVDC transmission corridors | 1.60% | Asia-Pacific, Europe, Brazil | Long term (≥ 4 years) |

| Grid-modernization programs in ageing T&D fleets | 1.10% | North America, Europe | Medium term (2-4 years) |

| Rail & metro DC electrification pipelines | 0.80% | Vietnam, India, China, Europe | Medium term (2-4 years) |

| Data-center shift toward on-prem LVDC busways | 0.70% | United States, Europe, Singapore | Short term (≤ 2 years) |

| Policy bans on SF₆ insulation | 0.90% | EU-27, United Kingdom, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Renewable-Linked DC Networks

Utility-scale solar and offshore wind farms increasingly export power on DC collection grids, producing fault currents that exceed the capability of AC switchgear. China reported that 68% of solar farms commissioned in 2025 used 1,500 VDC string inverters with embedded breakers, trimming balance-of-system costs by 12%.[4]National Energy Administration China, “2025 Solar Deployment Statistics,” nea.gov.cn India tendered 15 GW of DC-coupled storage, requiring 3 kV vacuum breakers to secure lithium-ion arrays. North Sea developers now specify 320 kV collection platforms with hybrid breakers capable of 40 kA interruption in 2 milliseconds to avert cascade trips. The IEC draft amendment proposed in December 2025 will, once ratified, shorten certification cycles and spur broader uptake. Collectively, these investments strengthen the demand outlook for the DC circuit breaker market.

Rapid Build-Out of HVDC Transmission Corridors

HVDC lines are displacing long-distance AC corridors thanks to lower resistive losses. The Hami-Chongqing ±800 kV link, energized in 2024, uses 12 hybrid breakers at each terminal to isolate faults within 3 milliseconds. Hitachi Energy supplies breaker modules pairing a mechanical disconnect with silicon-carbide thyristors for 25 kA duties. Europe’s Celtic Interconnector began construction in March 2025 and specifies vacuum breakers at both ends to enable black-start capability. Brazil’s Madeira project will employ ±600 kV solid-state breakers to guard a 2,400 km corridor that exports 4 GW of hydropower. Such mega-projects underpin high-voltage revenue streams within the DC circuit breaker market.

Grid-Modernization Programs in Ageing T&D Fleets

North American and European utilities are phasing out oil-filled switchgear installed in the 1970s. The U.S. Department of Energy allocated USD 3.5 billion in 2024-2025 for distribution upgrades, earmarking 22% for DC microgrids. Germany now bans SF₆ gear above 10 kV in new substations, accelerating the replacement of 18,000 legacy breakers by 2028. ABB’s SafeRing, launched in April 2025, employs a fluoronitrile-CO₂ blend and captured 14% of Europe’s retrofit orders within nine months. Collectively, these programs refresh demand for medium-voltage solutions and reinforce long-term growth in the DC circuit breaker market.

Rail & Metro DC Electrification Pipelines

Urban transit authorities standardize on 750 VDC and 1,500 VDC systems that need breakers capable of clearing inductive loads without arc reignition. Vietnam approved USD 61 billion for metro expansion through 2035, specifying vacuum breakers in traction substations. India’s rail network electrification mandates 3 kV breakers, with a USD 180 million contract awarded in August 2024. East Japan Railway retrofitted 320 substations with solid-state breakers during 2025, recouping 9% energy via regenerative braking. On-board storage trams such as Alstom’s Citadis X05 impose 15 kA peaks, which only hybrid designs can interrupt. These projects support double-digit growth in rail applications inside the DC circuit breaker market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital premium of solid-state & hybrid designs | -0.5% | Global, with acute sensitivity in price-competitive markets (India, Southeast Asia, Africa, Latin America) | Short term (≤ 2 years) |

| Complex fault-clearing in multi-terminal DC grids | -0.3% | Europe (North Sea wind hubs), China (provincial HVDC meshes), North America (planned offshore wind interconnectors) | Medium term (2-4 years) |

| Absence of universal DC-protection standards | -0.4% | Global, with pronounced impact in multi-vendor HVDC projects and cross-border interconnectors requiring interoperability | Medium term (2-4 years) |

| Wide-band-gap semiconductor supply bottlenecks | -0.3% | Global, with supply concentration in U.S. (Wolfspeed), Japan (Rohm, Mitsubishi), and Europe (Infineon, STMicroelectronics) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital Premium of Solid-State & Hybrid Designs

Solid-state and hybrid breakers carry a 3-5× cost multiple versus mechanical vacuum units. A 52 kV hybrid pole can cost up to USD 580,000, stretching payback periods beyond 12 years for regulated utilities. India deferred solid-state deployment at three HVDC projects in 2025 due to capital constraints. Silicon-carbide wafer shortages pushed 2025 lead-times to 52 weeks and spot prices 35% above contract levels. Chinese suppliers now market mechanical-vacuum hybrids at USD 180,000-240,000, trading speed for affordability and winning 22% of Asia’s medium-voltage orders in 2025.

Complex Fault-Clearing in Multi-Terminal DC Grids

Meshes lack natural fault isolation, forcing protection to act within 2 milliseconds. The North Sea Wind Power Hub saw a 14-month delay as integrators refined algorithms for five-terminal coordination. IEC standards still cover only point-to-point links, inflating engineering costs by up to 40%. China’s Zhangbei four-terminal grid suffered three outages in 2025 due to mis-coordination, requiring USD 38 million in firmware retrofits. CIGRE simulations indicate stability requires sub-1.5-millisecond clearing, achievable only with poles costing USD 1.2-1.8 million.

Segment Analysis

By Type: Hybrid Designs Gain Traction Despite Solid-State Dominance

Solid-state breakers held 76.3% of the DC circuit breaker market in 2025, owing to sub-microsecond commutation paths that meet stringent HVDC grid requirements. The segment’s continuous 0.3-0.5% conduction loss, however, equates to USD 180,000-280,000 in annual energy waste for a 25 kA unit, encouraging utilities to evaluate alternatives. Hybrid products route steady-state current through a zero-resistance vacuum contact and invoke a semiconductor path only during faults, cutting losses to 0.08%. ABB’s installation along the Hami-Chongqing link in 2024 validated a 3-millisecond interruption time and demonstrated 15-year life expectancy.

Hybrid designs will expand at an 8.8% CAGR, 1.6 points above the overall DC circuit breaker market, as field-upgradeable modules lower first-cost barriers. Hitachi Energy’s cartridge concept, launched in March 2025, lets operators add silicon-carbide stacks later, deferring up to USD 450,000 in capital. Eaton’s wafer supply deal with Wolfspeed promises 22% cost reductions by 2027. Mechanical-only breakers remain relevant in low-voltage rail traction where 10-millisecond clearing suffices and pricing undercuts hybrids by 60%.

By Insulation Medium: Vacuum Leads Amid SF₆ Phase-Out

Vacuum units controlled 43.5% of 2025 revenue and will grow at a 7.7% CAGR as regulators ban SF₆ in new installations. The DC circuit breaker market size tied to vacuum products is forecast to improve sharply once the EU restriction starts in 2026. Utilities value the vacuum’s maintenance-free design and rapid dielectric recovery. ABB’s SafeRing landed 1,800 orders within five months of its April 2025 debut.

Gas-insulated breakers, 24.5% of the mix in 2025, cling to high-voltage outdoor niches, but fluoronitrile-and-ketone blends now rival SF₆ performance. Siemens Energy’s blue GIS secured 12 converter-station contracts in 2025. Oil-filled designs declined to 18% share due to fire risk, and air-insulated units lost ground to vacuum units in data-center retrofits. Mitsubishi Electric’s 84 kV vacuum interrupter, undergoing trials at Tokyo Electric, signals vacuum’s upward voltage migration.

Note: Segment shares of all individual segments available upon report purchase

By Voltage Rating: High-Voltage Segment Accelerates on HVDC Demand

Medium-voltage devices up to 52 kV captured 48.1% share in 2025, yet high-voltage units above 52 kV will expand at a 10.5% CAGR, fuelled by ±800 kV corridors in China and offshore interconnectors in Europe. The high-voltage DC circuit breaker market size for multi-terminal grids is projected to rise fastest as fault energy scales with voltage. Interrupting 25 kA at ±800 kV dissipates 40 GJ in 3 milliseconds, a feat hybrid designs now achieve.

Low-voltage equipment to 1 kV enjoys a steady 6.8% CAGR through data-center LVDC adoption. Schneider Electric’s Premset switchgear posted 4,200 unit sales in 2025, 62% DC-rated, demonstrating medium-voltage resilience. High-voltage deployments such as the Zhangbei grid employ modules costing USD 1.4 million apiece, underscoring the premium potential of this tier.

By Installation Location: Outdoor Breakers Surge on Renewable Integration

Indoor models dominated with a 60.6% share in 2025, reflecting use in data centers, substations, and rail facilities. Outdoor installations, however, will grow at a 9.2% CAGR as wind farms and desert corridors expand. The Qinghai-Henan ±800 kV route employs outdoor hybrids with ceramic-composite insulators to survive high-altitude deserts. Offshore wind platforms demand weatherproof enclosures with pressurized nitrogen that adds 30% to cost but is indispensable for salt-fog resilience.

Indoor adoption remains strong where climate control lowers maintenance. Microsoft’s 180 indoor breakers at 800 VDC showcase compact footprints and high power density. East Japan Railway’s retrofit shrank equipment rooms by 40%, freeing urban real estate. Outdoor containerized systems like ABB’s PCS100 ESS, deployable in 72 hours, will widen addressable markets even in remote sites.

Note: Segment shares of all individual segments available upon report purchase

By Operating Mechanism: Solid-State Actuated Breakers Outpace Mechanical Designs

Mechanical actuators retained 44.9% revenue share in 2025 thanks to spring-charged reliability and low upfront pricing. Yet the solid-state-actuated sub-segment will climb at 11.6% CAGR as HVDC grids mandate sub-millisecond clearing. ABB’s hybrid HVDC breaker at Hami-Chongqing uses silicon-carbide devices that trigger within 500 microseconds. Eaton’s 800 VDC rack breaker interrupts 20 kA in 300 microseconds, protecting lithium-ion UPS banks.

Hybrid electromechanical mechanisms claim a 33% share, offering a balance between loss and speed. Hitachi Energy shipped 1,200 units in 2025 across HVDC and rail, proving scalability. Mechanical timelines of 8-12 milliseconds are impractical for emerging multi-terminal meshes, so migration toward semiconductor-assisted actuation is inevitable.

By End-User: Rail & E-Mobility Infrastructure Leads Growth

Transmission and distribution utilities dominated 46.8% of 2025 revenue, underpinning the DC circuit breaker market with grid-scale orders. Rail and e-mobility infrastructure, however, will grow the fastest at 11.1% CAGR, driven by USD 61 billion in Vietnamese metro builds and India’s 45,000-km electrification target. ChargePoint deployed 2,400 U.S. fast-charging sites integrating 1,000 VDC solid-state breakers, signaling rising demand beyond rail.

Renewable and storage plants held a 22% share in 2025 as DC-coupled batteries gained traction. Commercial and industrial facilities captured an 18% share with a 7.9% CAGR by rolling out LVDC microgrids for energy savings. Marine and telecoms remain niche at 7% share but value sealed, maintenance-free designs for harsh settings.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific led the DC circuit breaker market with 39.7% share in 2025 and is forecast to register a 9.4% CAGR through 2031. China energized three ±800 kV corridors in 2024, each requiring 25 kA hybrids and a cumulative equipment spend above USD 180 million. India’s 500 GW renewable target drives demand for 3 kV vacuum breakers at solar-storage nodes, while Vietnam’s metro expansion stipulates 1,500 VDC protection across two major cities. Japan’s 320-substation retrofit saved 9% traction energy and deferred USD 240 million in upgrades.

Europe secured a 28% share in 2025 and will rise at a 7.8% CAGR under SF₆ bans and offshore wind interconnectors. Regulation 2024/573 boosts vacuum orders by 34%, and Germany’s substation rule accelerates the removal of 18,000 legacy units. The Celtic Interconnector, valued at EUR 930 million, specifies vacuum breakers for black-start capability. Nordic HVDC links such as Hansa PowerBridge employ ±525 kV hybrids to stabilize continental flows.

North America held a 19% share in 2025 and is expected to post a 6.9% CAGR. The U.S. Grid Resilience Partnership carved out USD 770 million for DC microgrids, while California’s SF₆ limits bring forward vacuum retrofits. Hyperscale clusters in Virginia and Oregon now standardize 800 VDC racks, lifting low-voltage demand. South America, the Middle East, and Africa together accounted for a 13.3% share and will grow at an 8.1% CAGR, supported by Brazil’s Madeira HVDC project and Saudi Arabia’s NEOM renewable hub.

Competitive Landscape

Innovation and Adaptability Drive Market Success

The top five suppliers, ABB, Siemens Energy, Hitachi Energy, Schneider Electric, and Eaton, controlled roughly 58% of DC circuit breaker revenue in 2025. Their integrated portfolios span power semiconductors, vacuum-interrupter fabrication, and HVDC engineering, enabling turnkey contracts that bundle breakers with converter stations. ABB’s 2024 acquisition of GE Industrial Solutions added 1,200 hybrid patents and boosted capacity 18%, helping secure China’s ±800 kV projects. Siemens Energy leverages its installed GIS base to cross-sell fluoroketone-insulated breakers compliant with EU regulations.

Cost pressure intensifies as wide-bandgap wafers remain scarce. Eaton’s five-year Wolfspeed deal locks 150 mm supply, promising 22% cost cuts and 1,200 hybrid units annually by 2027. Chinese challengers Chint and GEYA underprice low-voltage offerings by up to 40%, prompting incumbents to focus on high-margin outdoor and solid-state segments. Specialty vendors carve niches: Powell sells ruggedized breakers for offshore oil platforms rated for 25-year maintenance-free life. Technology leadership remains the decisive lever as suppliers race to certify SF₆-free gases and sub-2-millisecond hybrids under pending IEC amendments.

White-space opportunities include multi-terminal grid protection and 350 kW fast-charging stations that need 300 microsecond isolation. Early movers embed proprietary communication links that lock customers into multidecade service arrangements, raising switching costs. Market entrants must navigate the absence of harmonized standards, but successful pilot projects could reshape share allocation within the DC circuit breaker market.

DC Circuit Breaker Industry Leaders

ABB Ltd

Mitsubishi Electric Corporation

Fuji Electric Co Ltd

Siemens AG

Eaton Corporation PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The Open Compute Project ratified ORv3, mandating 500-microsecond DC protection in 800VDC racks.

- July 2025: ABB launched SafeRing medium-voltage switchgear with fluoronitrile-CO₂ insulation and booked 1,800 European orders within five months.

- June 2025: Hitachi Energy will supply HVDC circuit breakers for the Gansu-Zhejiang ±800 kV UHVDC Transmission project, developed by SGCC. This project supports renewable energy generation in China’s Gobi Desert and other arid regions, addressing rising power demands from economic growth in the Yangtze River Delta.

- June 2025: The State Grid Corporation of China (SGCC) has launched the ±800 kV Hami–Chongqing UHVDC project, integrating 10,200 MW of wind and solar power in Xinjiang. The project enhances energy transmission reliability and efficiency using advanced DC circuit breaker technology.

Global DC Circuit Breaker Market Report Scope

DC circuit breakers are used to protect devices operating on direct current (DC). Its primary function is to automatically shut off power when a circuit is overloaded due to voltage fluctuations and other power quality issues, thus protecting sensitive equipment from getting damaged and preventing short circuits.

The DC circuit breaker market is segmented by type, insulation, voltage, operating mechanism, end-user, and geography. By type, the market is segmented into solid-state and hybrid. By insulation, the market is segmented by gas and vacuum. By operating mechanism, the market is divided into mechanical, solid-state actuated, and hybrid electrochemical. By end-user, the market is segmented by transmission and distribution, renewables and energy storage systems, commercial, and others. The report also covers the market size and forecasts for the DC circuit breaker market across major regions, such as Asia-Pacific, North America, Europe, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Solid-state |

| Hybrid |

| Oil |

| Air |

| Vacuum |

| Gas (SF₆ & alternatives) |

| Low Voltage (Up to 1 kV) |

| Medium Voltage (1 to 52 kV) |

| High Voltage (Above 52 kV) |

| Indoor |

| Outdoor |

| Mechanical |

| Solid-State Actuated |

| Hybrid Electromechanical |

| Transmission and Distribution Utilities |

| Renewable and Energy-Storage Plants |

| Rail and E-Mobility Infrastructure |

| Commercial and Industrial Facilities |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Solid-state | |

| Hybrid | ||

| By Insulation Medium | Oil | |

| Air | ||

| Vacuum | ||

| Gas (SF₆ & alternatives) | ||

| By Voltage Rating | Low Voltage (Up to 1 kV) | |

| Medium Voltage (1 to 52 kV) | ||

| High Voltage (Above 52 kV) | ||

| By Installation Location | Indoor | |

| Outdoor | ||

| By Operating Mechanism | Mechanical | |

| Solid-State Actuated | ||

| Hybrid Electromechanical | ||

| By End-User | Transmission and Distribution Utilities | |

| Renewable and Energy-Storage Plants | ||

| Rail and E-Mobility Infrastructure | ||

| Commercial and Industrial Facilities | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the DC circuit breaker market in 2026?

The DC circuit breaker market size is estimated at about USD 5.7 billion in 2026.

Which region leads demand for DC breakers?

Asia-Pacific accounts for the largest share at 39.7% thanks to extensive HVDC and rail investments in China, India, and Vietnam.

What drives the shift toward vacuum insulation?

EU and state-level bans on SF? push utilities to adopt vacuum and fluoronitrile-gas alternatives that meet the same performance without greenhouse impact.

Why are hybrid breakers gaining popularity?

Hybrid designs cut continuous losses versus full solid-state units while still clearing faults in about 3 milliseconds, balancing performance with lifecycle cost.

How fast can solid-state DC breakers interrupt faults?

Data-center and HVDC units with silicon-carbide or gallium-nitride devices achieve isolation in under 500 microseconds, preventing equipment damage and outages.

What is the key challenge in multi-terminal DC grids?

Coordinating protection across several nodes in less than 2 milliseconds remains difficult due to the absence of unified IEC standards, driving up engineering costs.