Market Overview

| Study Period | 2021 - 2031 |

|---|---|

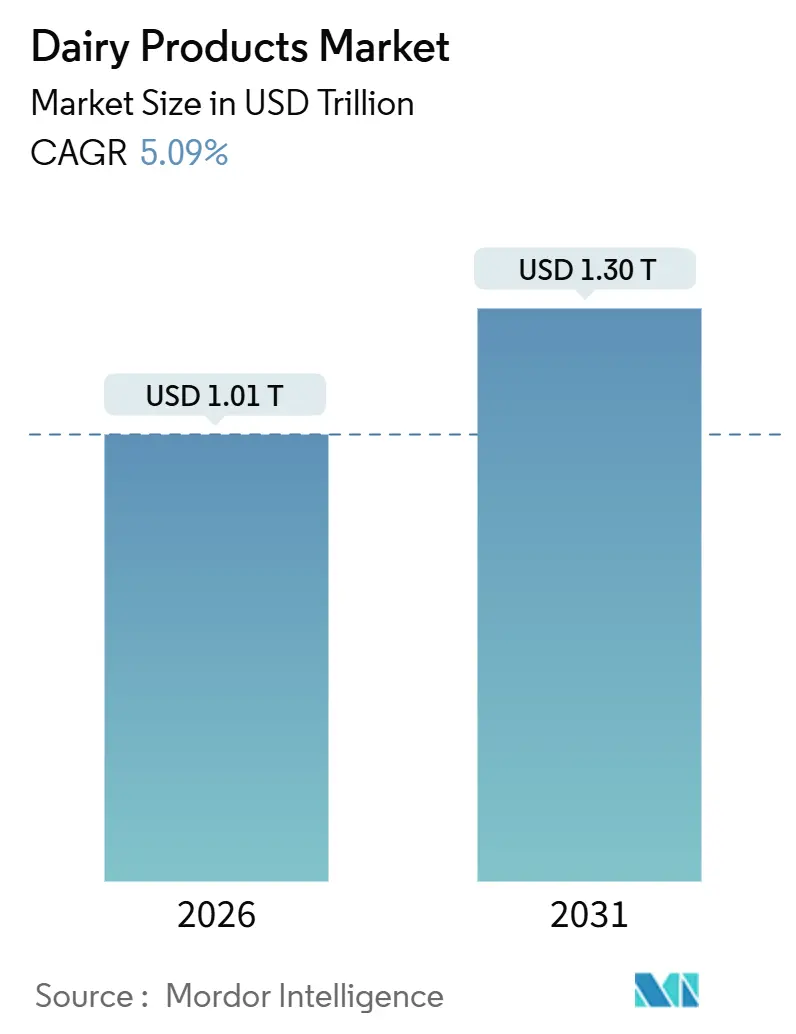

| Market Size (2026) | USD 1.01 Trillion |

| Market Size (2031) | USD 1.30 Trillion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dairy Products Market Analysis by Mordor Intelligence

The dairy products market, valued at USD 1.01 trillion in 2026, is set to reach USD 1.30 trillion by 2031, marking a projected CAGR of 5.09%. The market's medium-term growth is bolstered by rising demand for fortified offerings, government programs stabilizing farm-gate prices, and technological advancements catering to lactose-sensitive consumers. Multinational cooperatives are strategically merging upstream milk procurement with their branded portfolios, allowing them to capture margins and shield themselves from raw-milk price fluctuations. As urbanization surges in Asia-Pacific and Latin America, it's expanding cold-chain infrastructures. Concurrently, Europe's sustainability mandates are driving investments in methane-reducing feed additives, creating lucrative carbon-credit income streams. However, the rise of plant-based substitutes has heightened competition, pushing dairy processors to emphasize gut-health benefits, protein density, and sourcing from regenerative farms.

Key Report Takeaways

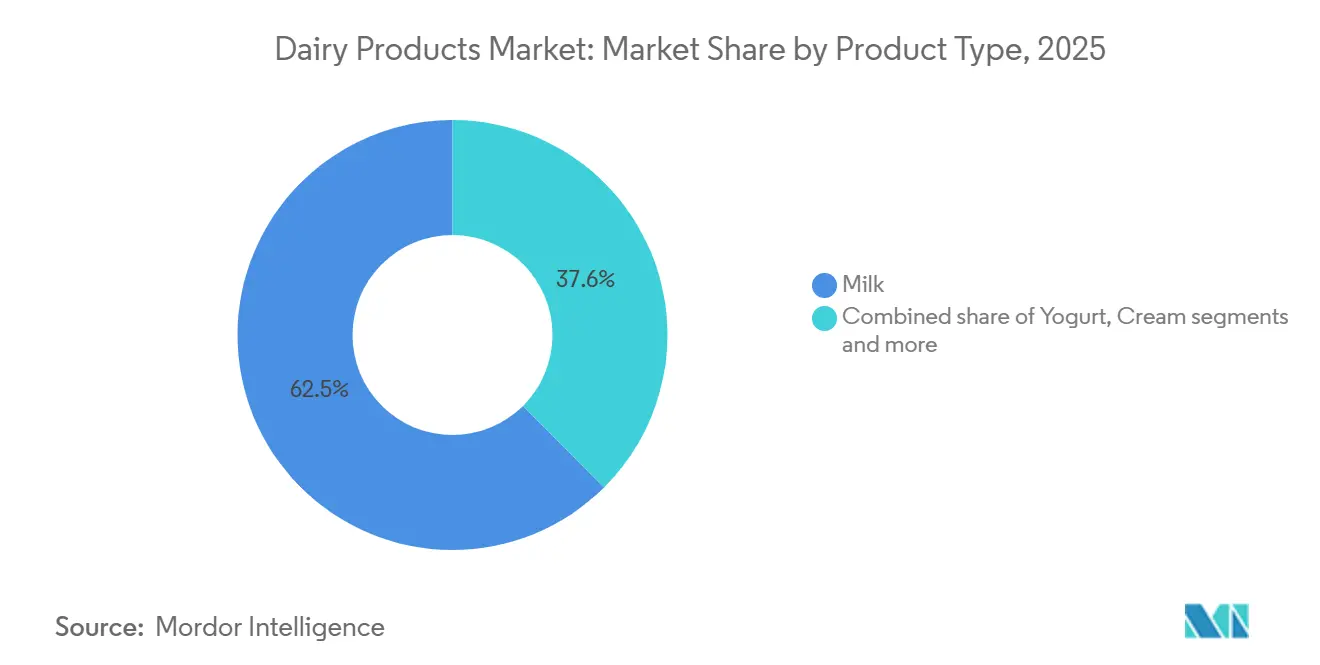

- By product type, milk led with 62.45% revenue share of the dairy products market in 2025, whereas yogurt is forecast to post the fastest 5.73% CAGR to 2031.

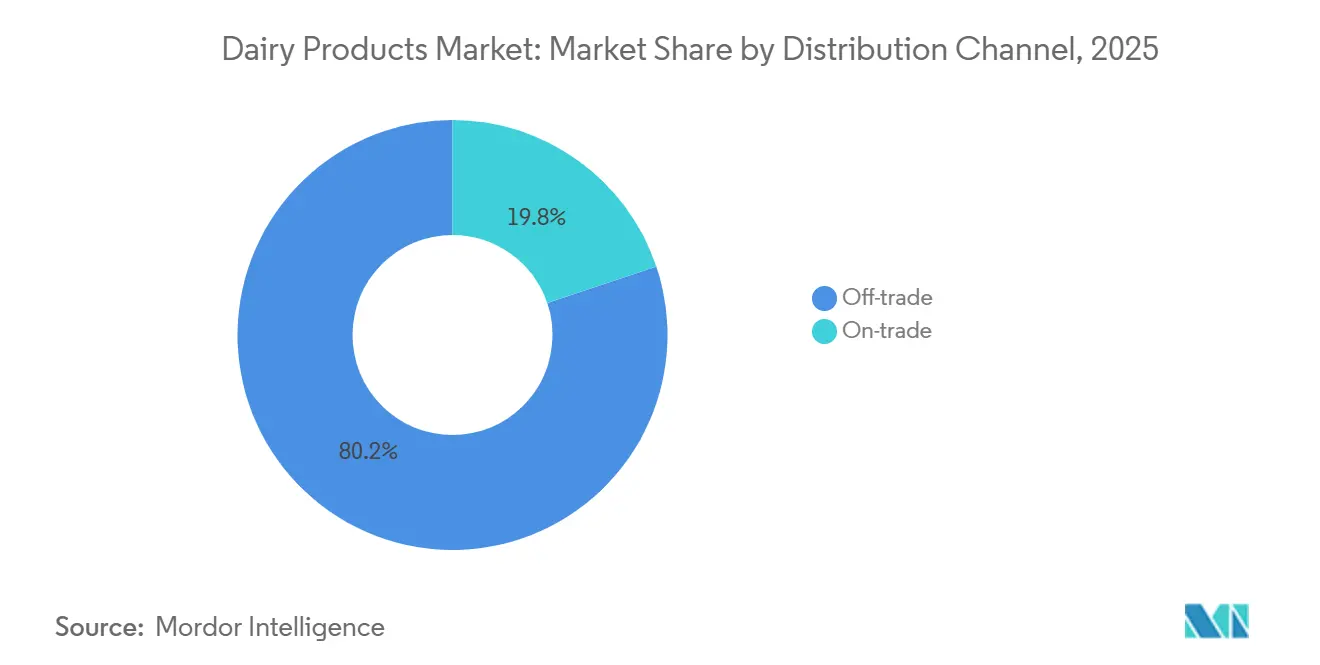

- By distribution channel, off-trade outlets captured 80.17% of the dairy products market in 2025; on-trade is projected to grow at a 5.81% CAGR through 2031.

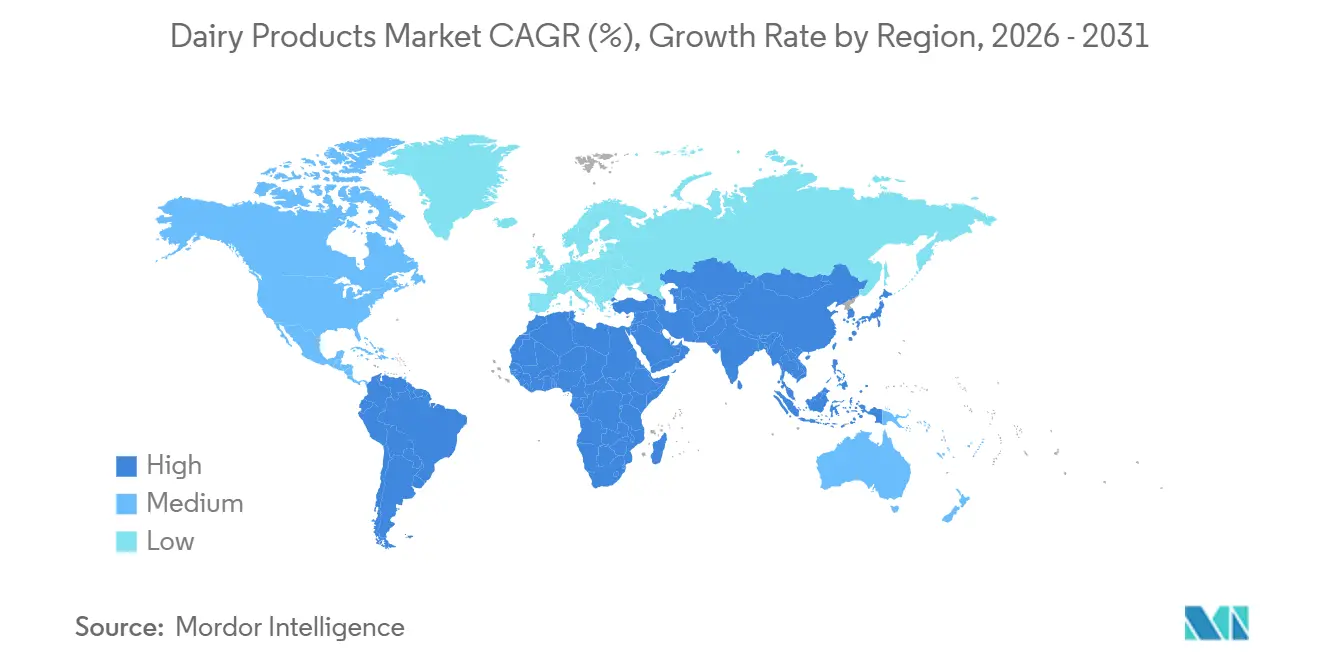

- By geography, Asia-Pacific accounted for 36.72% of the dairy products market size in 2025, while North America is poised for the quickest 6.16% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dairy Products Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for probiotic and functional dairy | +1.2% | Global, with North America and Europe leading regulatory approvals | Medium term (2-4 years) |

| Growing availability of dairy variants for dietary needs | +0.9% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Rising use of dairy ingredients in packaged foods | +0.8% | Global, particularly North America and Europe for sports nutrition and infant formula | Medium term (2-4 years) |

| Government support for dairy development and supply stability | +0.7% | India, China, United States, European Union | Long term (≥ 4 years) |

| Increasing adoption of sustainable and ethical dairy options | +0.5% | Europe, North America, Australia | Long term (≥ 4 years) |

| Expansion of lactose-digestive aids supporting dairy intake | +0.4% | Asia-Pacific, Latin America, Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing demand for probiotic and functional dairy

Consumers are increasingly focusing on preventive nutrition, particularly for improving gut health, maintaining metabolic balance, and boosting immunity. This shift is transforming dairy products from being seen as everyday staples to being recognized as functional, health-focused options. In March, 2024, the Food and Drug Administration issued a qualified health claim stating that consuming yogurt regularly at least 2 cups per week may help lower the risk of developing Type 2 diabetes[1]Source: Food and Drug Administration, "FDA Announces Qualified Health Claim for Yogurt and Reduced Risk of Type 2 Diabetes", fda.gov. As a result, manufacturers are reformulating their products to include clinically proven probiotic strains, higher protein content to appeal to health-conscious consumers. For example, Activia plans to launch its Proactive yogurt line in 2025, which will feature live probiotics, prebiotic fiber, and increased protein levels. This innovation reflects how brands are adapting to meet growing consumer interest in products that support digestive health and overall metabolic wellness.

Growing availability of dairy variants for dietary needs

The increasing availability of dairy products designed for specific dietary needs is expanding the global consumer base and driving demand for specialized milk options. Products such as lactose-free milk, A2 milk, grass-fed milk, and protein-fortified milk have become common in supermarkets, offering consumers choices that cater to digestive health, ethical preferences, and targeted nutritional benefits. For instance, while countries like DR Congo, Vietnam, and South Korea show about 1% lactose intolerance, according to World Population Review in 2025, the demand for these specialized dairy products is more influenced by lifestyle choices, perceived health benefits, and premium quality rather than widespread medical necessity[2]Source: World Population Review, "Lactose Intolerance by Country 2025", worldpopulationreview.com. In August 2025, the Karnataka Milk Federation announced the launch of lactose-free buffalo milk under its Nandini brand by September 2025. This marked a significant step in India, combining the traditional richness of buffalo milk with the convenience of lactose-free options.

Government support for dairy development and supply stability

Governments across major dairy-producing regions are actively investing in initiatives to boost dairy development and ensure a stable supply chain. In India, the government allocated INR 2,790 crore to upgrade milk-collection centers in March 2025 according to the Press Information Bureau[3]Source: Press Information Bureau, "Cabinet approves Revised National Program for Dairy Development (NPDD)", pib.gov.in. These efforts aim to strengthen cooperative procurement systems and minimize post-harvest losses, ensuring better efficiency in the supply chain. Similarly, Canada has committed to implement methane digesters and precision-feeding systems in September 2025. These technologies not only improve dairy production efficiency but also align with the country’s climate goals by reducing greenhouse gas emissions. In the European Union, the Common Agricultural Policy now ties payments to pasture preservation. This approach supports cooperatives that share resources for agronomic assistance and compliance with sustainability standards.

Increasing adoption of sustainable and ethical dairy options

Consumers are increasingly prioritizing environmental sustainability and animal welfare, prompting dairy producers to implement more eco-friendly and ethical practices across their operations. There is a rising demand for products such as grass-fed, pasture-raised, and low-carbon-certified dairy. These products are supported by transparent verification systems that confirm grazing practices, the origin of animal feed, and efforts to maintain biodiversity on farms. To meet stricter climate goals and appeal to environmentally conscious consumers, companies are investing in renewable energy for farms, technologies to reduce water usage during processing, and methods to lower methane emissions from livestock. Ethical sourcing is also gaining importance, with cooperatives ensuring that farmers receive fair compensation and that supply chains remain transparent. These initiatives not only build consumer trust but also help brands position themselves as premium and socially responsible options in the market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising lactose intolerance and dairy sensitivities | -0.8% | Asia-Pacific, Latin America, sub-Saharan Africa | Short term (≤ 2 years) |

| High volatility in raw milk prices | -0.6% | Global, with acute effects in North America and Europe | Short term (≤ 2 years) |

| Increasing competition from plant-based alternatives | -0.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Frequent quality and adulteration issues | -0.3% | India, China, emerging markets in Africa and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing competition from plant-based alternatives

The growing popularity of plant-based alternatives is posing a significant challenge to the dairy products market. As of June 2025, the global vegan population was estimated to reach approximately 88 million, accounting for about 1.1% of the world’s population, as per the World Animal Foundation[4]Source: World Animal Foundation, "How Many Vegans Are in the World in 2025? Latest Vegan Stats", worldanimalfoundation.org. This expanding demographic is driving increased demand for dairy substitutes. For instance, in October 2024, Maizly introduced a plant-based milk product in the United States, highlighting how new players are intensifying competition in the retail dairy segment. Plant-based options like oat and almond milk, which now offer similar foam stability and texture to traditional dairy, are gaining popularity in cafés and home coffee routines. Hybrid cheese products, which combine dairy with plant-based ingredients, are also attracting flexitarian consumers by delivering the familiar qualities of melt and stretch while offering a lower environmental impact.

Frequent quality and adulteration issues

Quality issues and adulteration present significant challenges for the dairy products market, undermining consumer trust and creating obstacles for both domestic sales and exports. A report by The Times of India in August 2024 highlighted that nearly 22% of milk and milk product samples tested in the Punjab, Haryana, and Himachal Pradesh regions between 2021 and 2024 did not meet safety standards. This underscores persistent gaps in quality control measures. Previous incidents, such as the melamine contamination in China, continue to impact consumer confidence, especially in the infant formula segment. In response to these concerns, producers are increasingly focusing on enhancing traceability and conducting independent audits. Additionally, risks such as aflatoxin contamination from moldy animal feed and antibiotic residues from mastitis treatments pose significant challenges, particularly when exporting to countries with strict safety regulations.

Segment Analysis

By Product Type: Yogurt Growth Outpaces a Mature Milk Base

In 2025, milk accounted for 62.45% of product-type revenue, driven by its role as a dietary staple and its versatility in beverages, cooking, and as an ingredient. Ultra-high-temperature processing extended its shelf life to 6-9 months without refrigeration, enabling wider access in rural areas of India and sub-Saharan Africa, where cold-chain infrastructure is limited. Per-capita fluid-milk consumption in the U.S. stabilized at 56 liters in 2025, reversing a decade of decline as lactose-free and organic options attracted consumers. Powdered milk exports from New Zealand and the European Union reached 2.4 million metric tons, serving infant formula, bakery, and confectionery markets in Asia and the Middle East. Condensed milk maintained niche demand in Latin America and Southeast Asia for desserts, while flavored milk, chocolate, strawberry, and coffee, captured 8% of North American sales, targeting children and adolescents through school programs.

Yogurt is projected to grow at a 5.73% CAGR through 2031, the fastest among all product categories, driven by probiotics addressing digestive health and immunity. Drinkable yogurt, led by brands like Yakult and Danone's Actimel, grew 21% in Asia-Pacific in 2025, appealing to busy consumers seeking convenience and health benefits. Spoonable yogurt expanded with Greek, Icelandic skyr, and Australian-style options, offering 15-20 grams of protein per serving and positioning as a healthier snack alternative. In 2025, Europe saw 340 new yogurt SKUs featuring plant-based ingredients, collagen peptides, and prebiotic fibers to stand out in a crowded market. Regulatory approvals for Lactobacillus and Bifidobacterium health claims in the U.S. and EU supported probiotic marketing, enabling premium pricing and boosting yogurt profitability despite lower volumes compared to milk.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Off-Trade Dominates but On-Trade Accelerates

In 2025, off-trade channels accounted for 80.17% of distribution revenue, reflecting consumer preference for buying dairy products during regular grocery trips. Supermarkets and hypermarkets contributed 52% of off-trade sales by offering private-label dairy products priced 15-20% lower than branded options, supported by partnerships with regional processors. Convenience stores in Japan and South Korea expanded refrigerated dairy sections to 18% of shelf space, featuring single-serve yogurt, flavored milk, and cheese snacks for impulse purchases. Online retail captured 7% of off-trade sales, with platforms like Amazon Fresh, Alibaba's Hema, and Instacart offering subscription models for milk and yogurt, reducing stockouts and encouraging repeat purchases. Specialist retailers, such as organic grocers and health-food stores, secured 4% of revenue by selling premium products like grass-fed butter, artisan cheese, and A2 milk, which commanded 30-50% higher prices than standard options.

On-trade channels are projected to grow at a 5.81% CAGR through 2031, driven by foodservice innovation and expanded dairy-based offerings in coffee chains. In 2025, quick-service restaurants in North America increased cheese usage in burgers and sandwiches to meet clean-label demands. Coffee chains like Starbucks and Costa Coffee introduced premium options, including oat milk, lactose-free milk, and organic whole milk, adding USD 0.50-0.80 surcharges to boost revenue while catering to dietary preferences. Full-service restaurants in Europe highlighted cheese and butter through tableside presentations and curated cheese boards, positioning dairy as a premium offering to justify higher prices. Institutional foodservices, including hospitals, schools, and corporate cafeterias, adopted portion-controlled dairy packaging in 2025, with single-serve yogurt cups and individually wrapped cheese slices gaining popularity for reducing waste and ensuring food safety.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, Asia-Pacific led the global dairy market, contributing 36.72% of global revenue. China and India were key players, producing 480 million metric tons and 210 million metric tons of milk, respectively, accounting for 52% of the region's output. China's Ministry of Agriculture and Rural Affairs launched a dairy revitalization plan in February 2025, aiming to mechanize 70% of dairy farms by 2028 and subsidize Holstein genetics imports to enhance herd productivity. India expanded Operation Flood 4.0, installing 2,400 bulk milk coolers in Uttar Pradesh and Rajasthan, reducing post-harvest losses by 18% and connecting smallholder farmers to organized procurement networks. Rising incomes, urbanization, and Western dietary trends, driven by multinational quick-service restaurants, boosted dairy consumption in Indonesia and Thailand, making them high-growth markets.

North America is projected to grow at a 6.16% CAGR through 2031, the fastest among all regions. The U.S. Department of Agriculture's Dairy Margin Coverage program stabilized raw-milk prices and encouraged investments in value-added products. In 2025, the U.S. produced 102 million metric tons of milk, with Wisconsin, California, and Idaho contributing 48% of the total. Organic dairy sales reached USD 8.2 billion, representing 6% of total revenue, driven by consumer demand for antibiotic-free and pasture-raised products certified under the USDA National Organic Program. In Canada, the Canadian Dairy Commission maintained stable farm-gate prices through production quotas, protecting processors from margin pressures seen in deregulated markets.

Europe's dairy sector faced challenges from the European Green Deal's Farm to Fork strategy, which targets 25% organic farming by 2030 and mandates methane emission reductions requiring feed and manure management improvements. Germany, France, and the Netherlands produced 68 million metric tons of milk in 2025, supported by cooperatives like FrieslandCampina and Arla Foods, which helped small farmers scale processing and marketing. The European Union exported 1.1 million metric tons of cheese and 780,000 metric tons of milk powder, mainly to China, Japan, and the Middle East, leveraging premium certifications like Protected Designation of Origin for products such as Parmigiano-Reggiano. The Middle East and Africa remained net importers, with Gulf Cooperation Council nations investing in cold-chain infrastructure to reduce spoilage. Nigeria attracted foreign investments from Danone and FrieslandCampina to expand local processing capacity.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The dairy products market is moderately fragmented, with competition from multinational corporations and regional cooperatives. Companies like Nestlé SA, Danone SA, and Groupe Lactalis use their strong marketing, Research and Development, and global supply chains to maintain an edge. Regional cooperatives such as GCMMF, Fonterra, and Dairy Farmers of America focus on their local presence and farmer-owned models to build trust. To meet changing consumer preferences, companies are prioritizing high-value products like whey protein, precision-fermented dairy alternatives, and hybrid blends. For instance, Arla Foods strengthened its sports nutrition and infant formula portfolio by acquiring Volac Whey Nutrition, while Leprino Foods partnered with Fooditive to develop animal-free casein, reflecting the industry's focus on innovation and sustainability.

Sustainability and advanced technologies are becoming key differentiators in the market. Companies adopting regenerative grazing and leveraging carbon credits gain a competitive advantage as retailers demand lower supply chain emissions. Larger players use artificial intelligence to optimize milk collection and predict price trends, while smaller farmers in Asia and Africa adopt mobile tools to reduce losses and improve efficiency. Innovations like digestion-resistant probiotic encapsulation, shelf-stable lactase enzymes, and recyclable packaging highlight the industry's dual focus on nutrition and environmental impact.

Entering the dairy market is challenging due to high costs for processing facilities, cold-chain logistics, and strict food safety regulations. However, precision fermentation is disrupting traditional dairy production. Startups like Remilk, with FDA-approved animal-free whey protein, are creating opportunities by eliminating the need for cows in production. Established dairy companies are investing in or partnering with these startups to share growth potential while minimizing risks. This approach helps legacy players stay competitive and adapt to evolving consumer demands and technologies.

Dairy Products Industry Leaders

-

Danone SA

-

Nestlé SA

-

Dairy Farmers of America

-

Fonterra Co-operative Group

-

Groupe Lactalis

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Country Delight has launched a new high-protein cow milk product to meet India's increasing demand for improved daily nutrition. This product contains twice the protein of regular milk, aiming to serve health-conscious consumers looking for better dietary options.

- August 2025: Danone has launched Oikos yogurt drink, specifically designed for users of GLP-1 receptor agonists. This product introduction highlights the company's strategic commitment to meeting the nutritional needs of individuals who use these medications, which are often prescribed for managing diabetes and promoting weight loss.

- June 2025: Yogurt Factory has announced its plans to expand into the Indian market through a strategic collaboration with FranGlobal, the international business division of Franchise India.

- March 2025: Paras Dairy, operated by VRS Foods Limited, is a leading name in India's dairy industry. During the Aahar 2025 exhibition, the company launched its premium cheese brand, Galacia. This introduction marks a strategic effort to meet the increasing demand for high-quality cheese products in the Indian market.

Global Dairy Products Market Report Scope

The dairy products market is segmented by Product Type, Distribution Channel, and Geography. Based on Product Type, the market is segmented into butter, cheese, cream, dairy desserts, milk, yogurt, sour milk drinks and others. Based on the distribution channel, the market studied is segmented into on-trade and off-trade. Based on geography, the market studied is segmented into North America, South America, Europe, Asia-Pacific, and Middle East and Africa.

Product Type

| Butter | Salted Butter | |

| Unsalted Butter | ||

| Cheese | Natural Cheese | Cheddar |

| Cottage | ||

| Feta | ||

| Parmesan | ||

| Others | ||

| Processed Cheese | ||

| Cream | Fresh Cream | |

| Cooking Cream | ||

| Whipping Cream | ||

| Others | ||

| Dairy Desserts | Ice Cream | |

| Cheesecakes | ||

| Frozen Desserts | ||

| Others | ||

| Milk | Condensed milk | |

| Flavored Milk | ||

| Fresh Milk | ||

| UHT Milk (Ultra-High Temperature Milk) | ||

| Powdered Milk | ||

| Others | ||

| Yogurt | Drinkable | |

| Spoonable | ||

| Sour Milk Drinks | ||

| Others | ||

Distribution Channel

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets/Hypermarkets | |

| Online Retail | |

| Others |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Butter | Salted Butter | |

| Unsalted Butter | |||

| Cheese | Natural Cheese | Cheddar | |

| Cottage | |||

| Feta | |||

| Parmesan | |||

| Others | |||

| Processed Cheese | |||

| Cream | Fresh Cream | ||

| Cooking Cream | |||

| Whipping Cream | |||

| Others | |||

| Dairy Desserts | Ice Cream | ||

| Cheesecakes | |||

| Frozen Desserts | |||

| Others | |||

| Milk | Condensed milk | ||

| Flavored Milk | |||

| Fresh Milk | |||

| UHT Milk (Ultra-High Temperature Milk) | |||

| Powdered Milk | |||

| Others | |||

| Yogurt | Drinkable | ||

| Spoonable | |||

| Sour Milk Drinks | |||

| Others | |||

| Distribution Channel | On-trade | ||

| Off-trade | Convenience Stores | ||

| Specialist Retailers | |||

| Supermarkets/Hypermarkets | |||

| Online Retail | |||

| Others | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Butter - Butter is a yellow-to-white solid emulsion of fat globules, water, and inorganic salts produced by churning the cream from cows’ milk

- Dairy - Dairy product include milk and any of the foods made from milk, including butter, cheese, ice cream, yogurt, and condensed and dried milk.

- Frozen Desserts - Frozen dairy dessert means and includes products containing milk or cream and other ingredients which are frozen or semi-frozen prior to consumption, such as ice milk or sherbet, including frozen dairy desserts for special dietary purposes, and sorbet

- Sour Milk Drinks - Sour milk is thick, curdled milk, with a sour taste, obtained from the fermentation of milk. Sour milk drinks such as kefir, laban, buttermilk have been considered in the study

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF