Cumene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

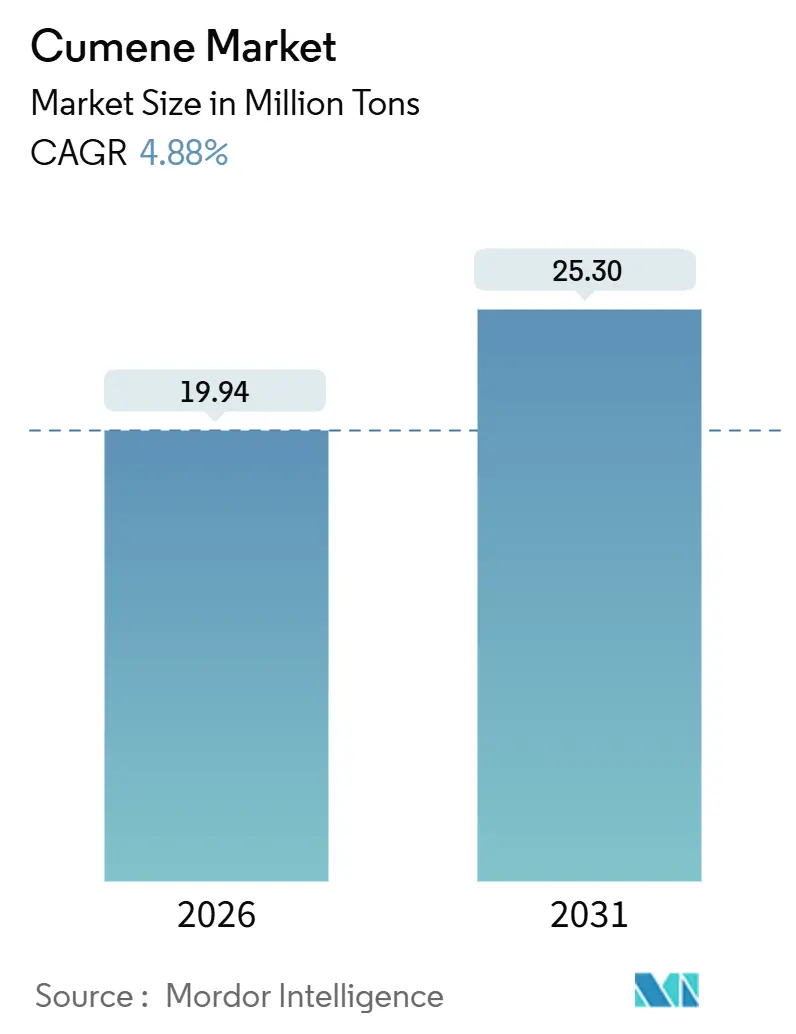

| Market Volume (2026) | 19.94 Million tons |

| Market Volume (2031) | 25.30 Million tons |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

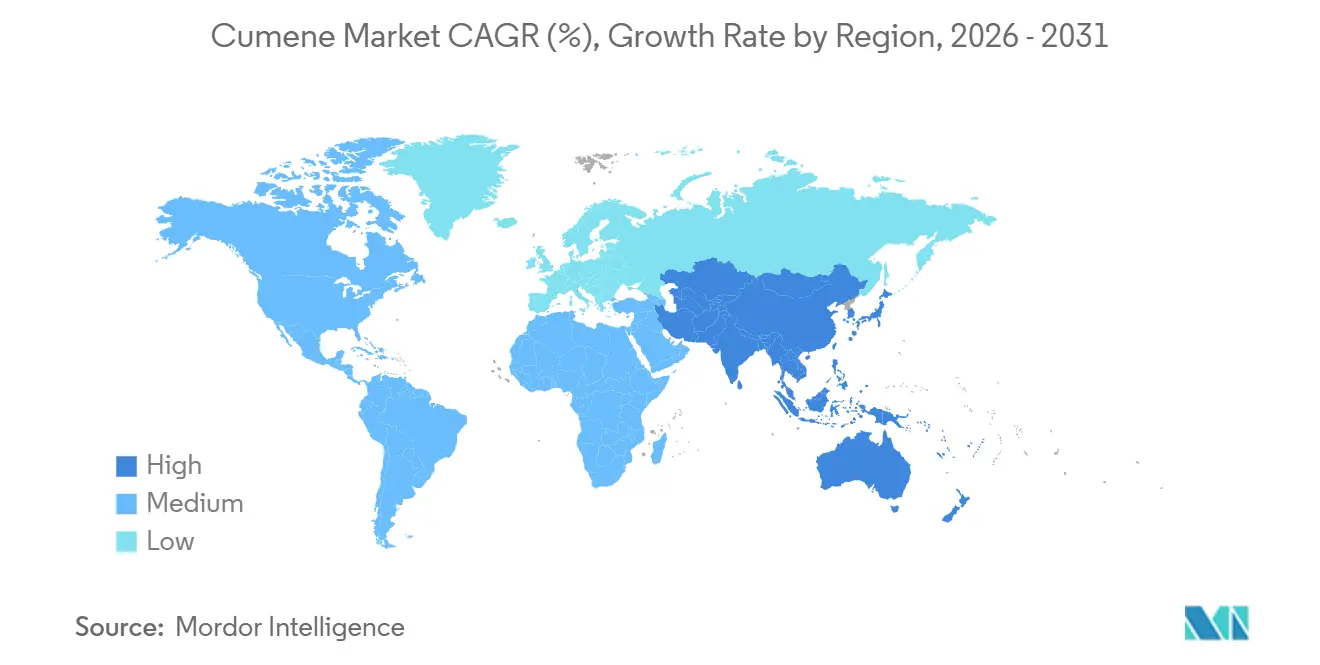

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cumene Market Analysis by Mordor Intelligence

The Cumene Market size is estimated at 19.94 million tons in 2026, and is expected to reach 25.30 million tons by 2031, at a CAGR of 4.88% during the forecast period (2026-2031). Current dynamics reflect how integrated refinery-petrochemical complexes and high-selectivity zeolite catalysts are lifting yields, trimming by-product costs, and driving down unit emissions. Suppliers with access to in-house benzene and propylene streams continue to post margin resilience even when crude-linked feedstock spreads widen. The cumene market also benefits from sustained phenol demand in polycarbonate glazing for electric vehicles and epoxy resins used in wind blades and aerospace composites. Stricter emission norms, such as the EPA's 40 CFR 60.112c and OSHA's 50 ppm exposure cap, are pushing plants to adopt closed-loop handling, vapor recovery, and real-time monitoring systems. These upgrades are significantly impacting the budget of new constructions.

Key Report Takeaways

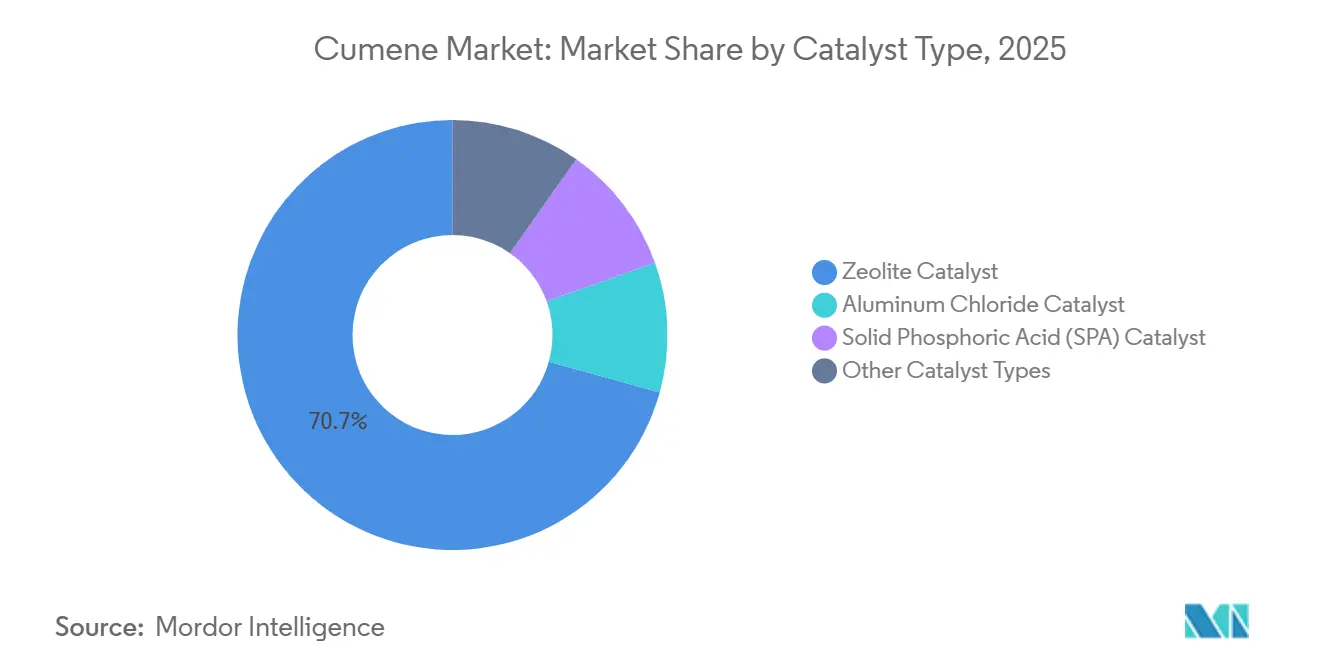

- By catalyst type, zeolite catalysts led with 70.68% cumene market share in 2025; they are forecast to advance at a 6.17% CAGR through 2031.

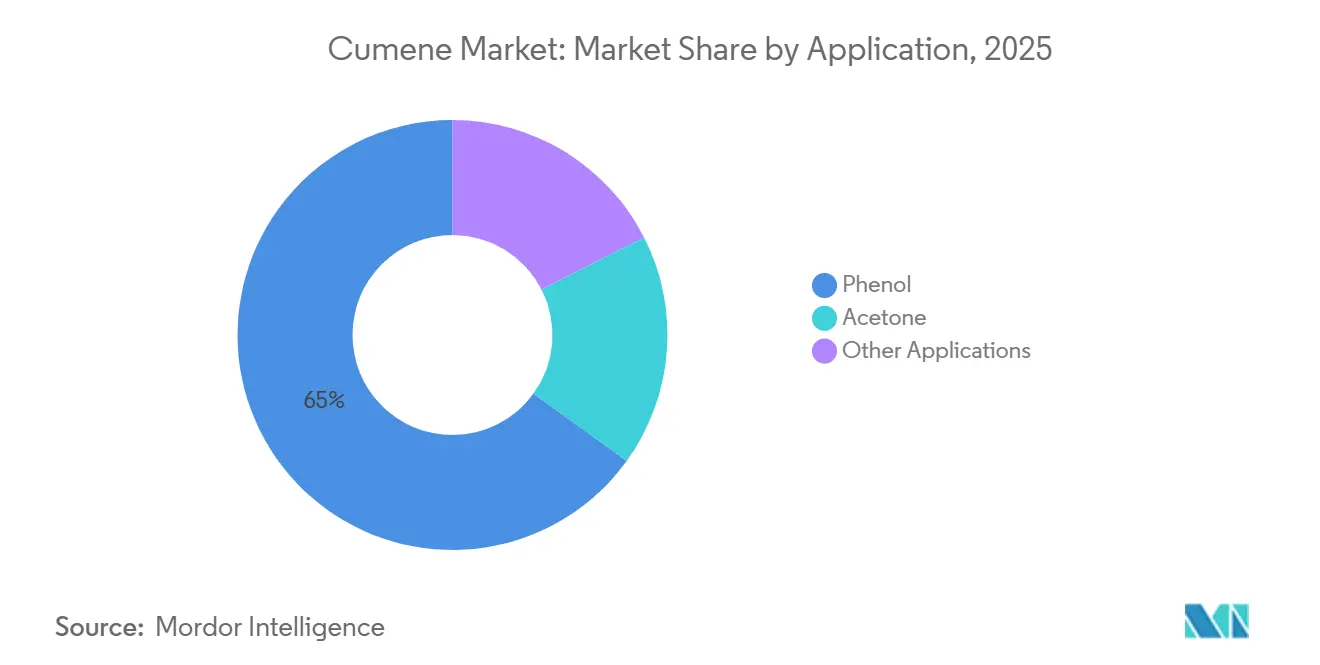

- By application, phenol accounted for 65.04% of the cumene market size in 2025 and is poised to grow at a 5.05% CAGR to 2031.

- By geography, Asia-Pacific held 61.26% of the cumene market size in 2025 and is expanding at a 5.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cumene Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for phenol-based polycarbonates and epoxy resins | +1.2% | Global, with concentration in Asia-Pacific automotive hubs (China, Japan, South Korea), North American electronics clusters, and European wind energy markets | Medium term (2-4 years) |

| Expanding use of acetone in solvents and MMA | +0.6% | Asia-Pacific core (China, India, Southeast Asia), North America industrial coatings sector, Europe specialty chemicals | Medium term (2-4 years) |

| Integrated refinery-petchem complexes improving cumene economics | +0.9% | Middle East (Saudi Arabia, Qatar, UAE), China coastal provinces (Zhejiang, Jiangsu, Shandong), US Gulf Coast | Long term (≥ 4 years) |

| Rapid adoption of high-selectivity zeolite catalysts | +0.7% | Global, with early adoption in Europe and North America, accelerating deployment in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Increasing demand for phenol from the plastic industry | +1.0% | Asia-Pacific core (China, India, Japan, South Korea), spill-over to Middle East downstream integration and North America automotive lightweighting | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Phenol-Based Polycarbonates and Epoxy Resins

Electric vehicles are trimming their mass with the use of polycarbonate glazing, aiding in their range extension goals. As general construction demand levels off, electronics manufacturers are turning to optically clear resins for high-resolution displays, boosting phenol off-take. Offshore wind blades and primary structures in aerospace requiring high fatigue resistance are driving a rise in epoxy resin consumption. In automotive braking systems, phenolic binders are increasingly replacing metallic friction materials, leading to reductions in both weight and noise. While backward-integrated players in China have linked cumene, phenol, and bisphenol A units on single sites to mitigate supply risks, this strategy has inadvertently led to regional overcapacity.

Integrated Refinery-Petrochemical Complexes Improving Cumene Economics

Crude-to-chemicals projects pair mixed-feed crackers with aromatics units, giving operators internal benzene and propylene streams at transfer prices unaffected by spot swings. The Yasref refinery expansion in Saudi Arabia will add benzene for downstream phenol-acetone chains by 2029, and the Ras Laffan cracker in Qatar is scheduled to start up in 2026 with on-purpose propylene dehydrogenation to balance light-feed cracking yields[1]Saudi Aramco, “Yasref Expansion Framework Agreement,” ARAMCO.COM. Such complexes eliminate inter-plant logistics, shorten working-capital cycles, and enable rapid swings between cumene and other aromatics when margin signals shift.

Rapid Adoption of High-Selectivity Zeolite Catalysts

ExxonMobil's MCM-22 framework drives over half of the world's capacity, achieving high selectivity rates and significantly reducing di-isopropylbenzene formation. INEOS's Marl unit demonstrates a notable reduction in CO₂ emissions when compared to traditional solid phosphoric acid technology. UOP's Q-Max system boasts an extended catalyst lifespan, leading to decreased downtime and regeneration costs. This industry shift is further bolstered by regulatory pressures, as zeolites not only meet VOC-capture thresholds but also do so with more straightforward abatement hardware, outpacing the SPA or aluminum chloride methods.

Increasing Demand for Phenol in the Plastics Value Chain

Phenol serves as a precursor for polycarbonate, phenolic resins, and nylon-6 intermediates, establishing a direct link between the cumene market and sectors like electric vehicles, wind energy, and engineered textiles. China relies on imports to meet its phenol demand, and India is poised to address this gap through new projects at Haldia and Deepak Chem Tech. Meanwhile, caprolactam producers in Southeast Asia are expanding their cyclohexanone capacity, indirectly boosting the demand for phenol, even as styrene accounts for nearly half of the global benzene consumption.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and environmental hazards of cumene exposure | -0.5% | Global, with acute regulatory pressure in North America (EPA, OSHA) and Europe (ECHA, REACH), gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| Crude oil/benzene-propylene price volatility | -0.8% | Global, with acute impact in import-dependent regions (India, Southeast Asia, Europe), moderate impact in integrated Middle East and North America | Short term (≤ 2 years) |

| Stricter emission norms raising compliance costs | -0.6% | North America and EU (EPA 40 CFR 60.112c, EU ETS, CBAM), with gradual adoption in China and other Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude Oil, Benzene, and Propylene Price Volatility

In April–May 2024, Northeast Asia saw benzene–naphtha spreads fluctuate. In contrast, Western Europe experienced a significant drop during the same period. This decline was driven by LPG cracking, which displaced pygas-derived benzene. Propylene, closely tied to Brent, sees its margins tighten sharply whenever benchmark crude prices rise. North American ethane crackers produce minimal propylene. As a result, cumene producers are turning to on-purpose PDH supplies, but at a premium. Asian plants that aren't integrated are feeling the brunt of the pressure, as their reliance on imports makes them vulnerable to fluctuations in freight and currency.

Stricter Emission Norms Raising Compliance Costs

Following the National Toxicology Program's classification of cumene as "reasonably anticipated to be a human carcinogen," the EPA has tightened limits on fugitive emissions from storage tanks and loading operations. Under OSHA's regulations, with a 50 ppm permissible exposure ceiling, operators are now mandated to implement closed-loop transfer systems equipped with leak-free pumps. Additionally, real-time VOC monitoring and flare-gas recovery have increased greenfield capex budgets[2]Occupational Safety and Health Administration, “Cumene Chemical Data,” OSHA.GOV. European plants are also grappling with rising EU-ETS carbon prices. Furthermore, the CBAM will impose these carbon costs on imports starting in 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Catalyst Type: Zeolite Retains a Commanding Lead

Zeolite systems captured 70.68% of the cumene market share in 2025, and their output is growing 6.17% yearly to 2031. Zeolite technology is poised to boost its contribution to the cumene market in the coming years. At INEOS’s Marl complex, the adoption of zeolite technology has led to a notable reduction in off-spec streams and a decrease in CO₂ emissions per ton. Meanwhile, ExxonMobil's MCM-22 units boast yields that solid phosphoric acid systems can't match, especially given their added caustic-neutralization costs.

Aluminum chloride methods now represent a small portion of the total installed capacity, predominantly in older Chinese facilities that are either set for retrofitting or imminent closure. In a nod to the national low-carbon targets unveiled before COP28, greenfield projects in the Middle East are predominantly opting for zeolite frameworks. Demonstrating a commitment to self-sufficiency, China's Wanhua Chemical has successfully enhanced its in-house zeolite catalyst, boosting cumene capacity. However, operators still using SPA units find themselves at a disadvantage: EPA 40 CFR 60.112c mandates a stringent control efficiency, leading to significant capital investments for vapor recovery.

By Application: Phenol Extends Its Dominance

Phenol commanded 65.04% of the cumene market share in 2025 amid growing demand for electric-vehicle glazing and high-performance composites. Segment revenue is expanding at a 5.05% CAGR. Wind projects, consistently setting new length records, are driving the production of epoxy resin. Each turbine blade, after all, demands several tons of bisphenol-A-based resin.

In China, acetone, which is co-generated with phenol, is facing an oversupply. This surplus has not only depressed unit margins but has also led some phenol units to reduce their rates. Integrated refiners, like SABIC, which have downstream lines in MMA or BPA, are in a position to absorb the excess. In contrast, independent sellers frequently turn to export arbitrage, targeting Southeast Asia. While other smaller outlets, such as aviation fuel additives and inks, account for a minor share of cumene offtake, their growth remains stagnant.

Geography Analysis

Asia-Pacific retained 61.26% of the cumene market in 2025, and is expected to register a 5.97% CAGR through 2031. Between 2025 and 2027, China introduced significant phenol-acetone capacity to the market, including projects like Rongsheng’s Jintang line. However, with benzene overcapacity increasing, bisphenol A run rates were curtailed. Mitsui Chemical announced the closure of its Ichihara phenol plant by FY 2026, attributing the decision to a structural oversupply. In contrast, India grapples with a phenol deficit. Haldia Petrochemicals ramped up its phenol output in 2026, and Deepak Chem Tech is pushing forward with new projects set to debut in 2027. Meanwhile, PTTGC, a key player in Southeast Asia, operates a phenol facility, catering to the region's packaging and electronics sectors.

North America capitalizes on its low-cost ethane, achieving high yields in ethylene production. However, this process yields weaker propylene streams. As a result, the US cumene market relies on feedstock sourced from refinery FCCs or PDH units, often at a premium price. In 2024, benzene prices reflected a tight supply scenario, especially with styrene's increasing consumption. Since 2021, capacity expansions on the US Gulf Coast, notably by Baystar and GCGV, have enhanced the availability of integrated propylene. Yet, this progress is often overshadowed by volatility, especially when hurricanes disrupt refinery operations.

Europe grapples with soaring energy costs and escalating carbon responsibilities, particularly under the EU-ETS and CBAM frameworks. In a strategic move for 2024, BASF is streamlining operations at its Ludwigshafen site, cutting back on non-core intermediates to reallocate resources towards integrated assets. This shift underscores the mounting pressures on its traditional phenol lines. In 2024, Western European benzene–naphtha spreads tightened, prompting a surge in cumene imports from the Middle East. While many in the region face challenges, INEOS’s advanced Marl plant stands out. Its innovative zeolite platform, combined with its proximity to the Gladbeck phenol units, helps mitigate the impact of elevated regional power costs.

The Middle East is solidifying its position as a competitive export hub in the cumene industry. Saudi Aramco is making a significant bet, investing heavily in a comprehensive liquids-to-chemicals strategy. Their ambitious roadmap envisions the integration of crackers, aromatics, and alkylation complexes, with a target of converting large volumes of crude daily by 2030. QatarEnergy's Ras Laffan initiative is set to produce on-purpose propylene for cumene. With mechanical completion anticipated in 2026, the project eyes exports primarily to Europe and South Asia. In South America, production levels are modest. Both Brazil and Argentina are channeling efforts towards meeting their domestic phenolic resin needs. Meanwhile, Sub-Saharan Africa finds itself reliant on imports for nearly all its phenol demands.

Competitive Landscape

The cumene market is consolidated. ExxonMobil has positioned itself as a technology licensor; its Badger unit’s MCM-22 framework sits in over half the global installed base, generating royalties without capital intensity. Middle-Eastern exporters are gaining traction as low-carbon footprints attract European customers seeking to hedge CBAM liabilities. Technology leadership is decisive: zeolite users record lower disposal costs and lower CO₂ per ton, providing a defensible cost edge that likely accelerates SPA and aluminum chloride plant retirements through 2031. Mitsui and Mitsubishi Chemical have launched a joint study to secure phenol supply chains after announcing the Ichihara closure. Among innovators, start-ups are piloting bio-based benzene derived from lignocellulosic biomass and catalytic routes to recover phenol from end-of-life polycarbonate, although commercial scale is several years away.

Cumene Industry Leaders

Versalis S.p.A.

Braskem

Cepsa

Chang Chun Group

CITGO Petroleum Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: IndianOil Corp. Ltd. (IOCL) selected Lummus/Versalis cumene technology for a 440 KTA unit in Paradip, India. This unit is part of IOCL's petrochemical and polymers expansion at its Paradip complex. The move is expected to boost the cumene market by increasing production capacity.

- January 2024: Ineos has opened Europe’s largest cumene plant in Marl, Germany, with a capacity of 750,000 metric tons per year. Cumene is used to make phenol, which is key for bisphenol A and phenolic resins. The plant’s new heat system cuts its carbon footprint by up to 50%. It connects via pipeline to Ineos’s phenol and acetone sites in Gladbeck, Evonik’s Chempark in Marl, and BP’s refinery in Gelsenkirchen. This development strengthens Ineos’s position in the cumene market by enhancing efficiency and sustainability.

Global Cumene Market Report Scope

Cumene (chemical name: isopropylbenzene) is an aliphatic-substituted aromatic hydrocarbon present in all crude oil and refined fuels. It is a colorless, flammable liquid with a boiling point of 152°C. Cumene is produced either from the distillation of coal tar and petroleum fractions or by the acid-catalyzed alkylation reaction of benzene with propene.

The cumene market is segmented by catalyst type, application, and geography. By catalyst type, the market is segmented into aluminum chloride catalyst, solid phosphoric acid (SPA) catalyst, zeolite catalyst, and other catalyst types. By application, the market is segmented into phenol, acetone, and other applications. The report also covers the market size and forecast for the cumene market in 16 countries across major regions. For each segment, the market sizing and forecast have been done based on volume (Tons).

| Aluminum Chloride Catalyst |

| Solid Phosphoric Acid (SPA) Catalyst |

| Zeolite Catalyst |

| Other Catalyst Types |

| Phenol |

| Acetone |

| Other Applications (Paints, Enamels, Aviation Fuels, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Catalyst Type | Aluminum Chloride Catalyst | |

| Solid Phosphoric Acid (SPA) Catalyst | ||

| Zeolite Catalyst | ||

| Other Catalyst Types | ||

| By Application | Phenol | |

| Acetone | ||

| Other Applications (Paints, Enamels, Aviation Fuels, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the 2026 cumene market size?

The cumene market size is 19.94 million tons in 2026.

How fast is global demand for cumene expected to grow?

Volume demand is forecast to expand at a 4.88% CAGR between 2026 and 2031, reaching 25.30 million tons.

Which region dominates cumene consumption?

Asia-Pacific holds 61.26% of global demand, despite overcapacity in China that contrasts with shortages in India and Southeast Asia.

What are the main risks facing cumene producers?

Margin volatility from crude-linked benzene and propylene prices and rising compliance costs under tougher emission rules are the key challenges.

Page last updated on: