Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.69 Billion |

| Market Size (2026) | USD 12.26 Billion |

| Market Size (2031) | USD 15.54 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC And MENA Valves Market Analysis by Mordor Intelligence

The GCC and MENA valves market size was valued at USD 11.69 billion in 2025 and estimated to grow from USD 12.26 billion in 2026 to reach USD 15.54 billion by 2031, at a CAGR of 4.86% during the forecast period (2026-2031). This momentum reflects parallel efforts to decarbonize hydrocarbon assets and scale up desalination capacity. Steady upstream gas development, multi-billion-dollar refinery upgrades, and record desalination contracting collectively underpin capital spending on control, isolation, and safety-critical valves. Suppliers able to furnish API 624 and API 641 fugitive-emissions compliance at short lead times win specifications, while smart-positioner retrofits deepen aftermarket revenue. Regulatory harmonization across the Gulf Standards Organisation, rising local-content rules, and digital-twin adoption further shape purchasing preferences across the GCC and MENA valves market.

Key Report Takeaways

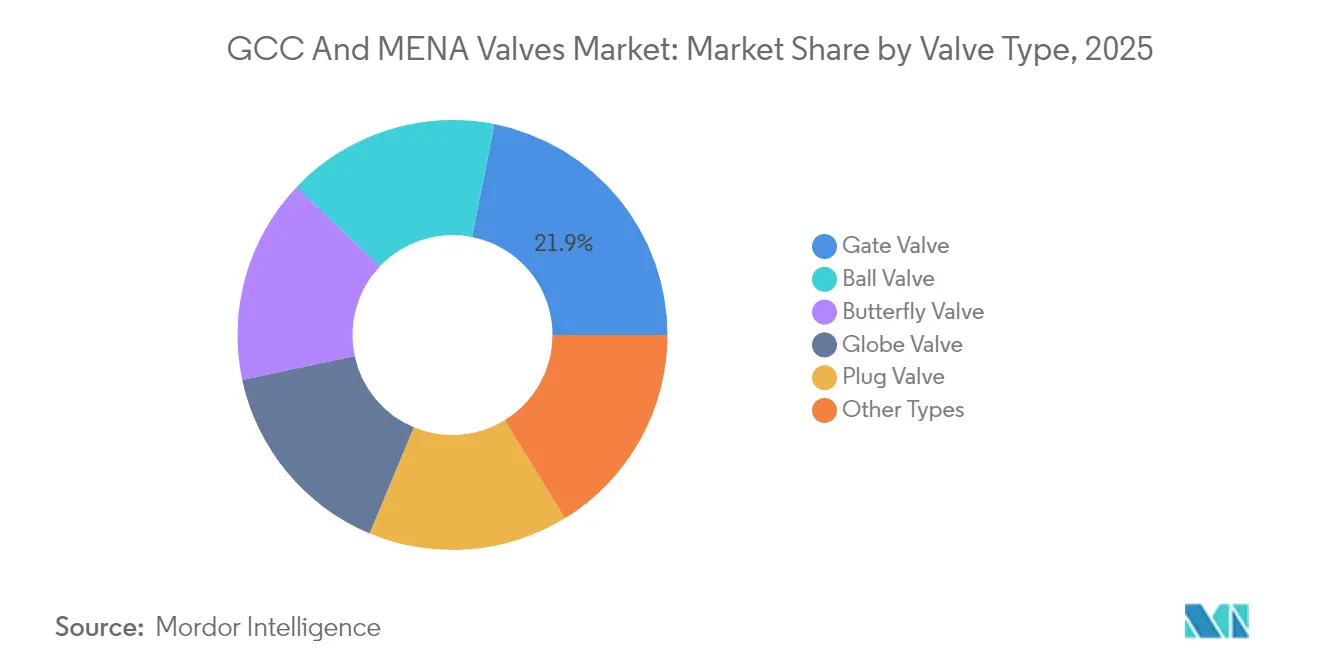

- By valve type, gate valves held 21.88% of the GCC and MENA valves market share in 2025, whereas ball valves are forecast to expand at a 4.98% CAGR to 2031.

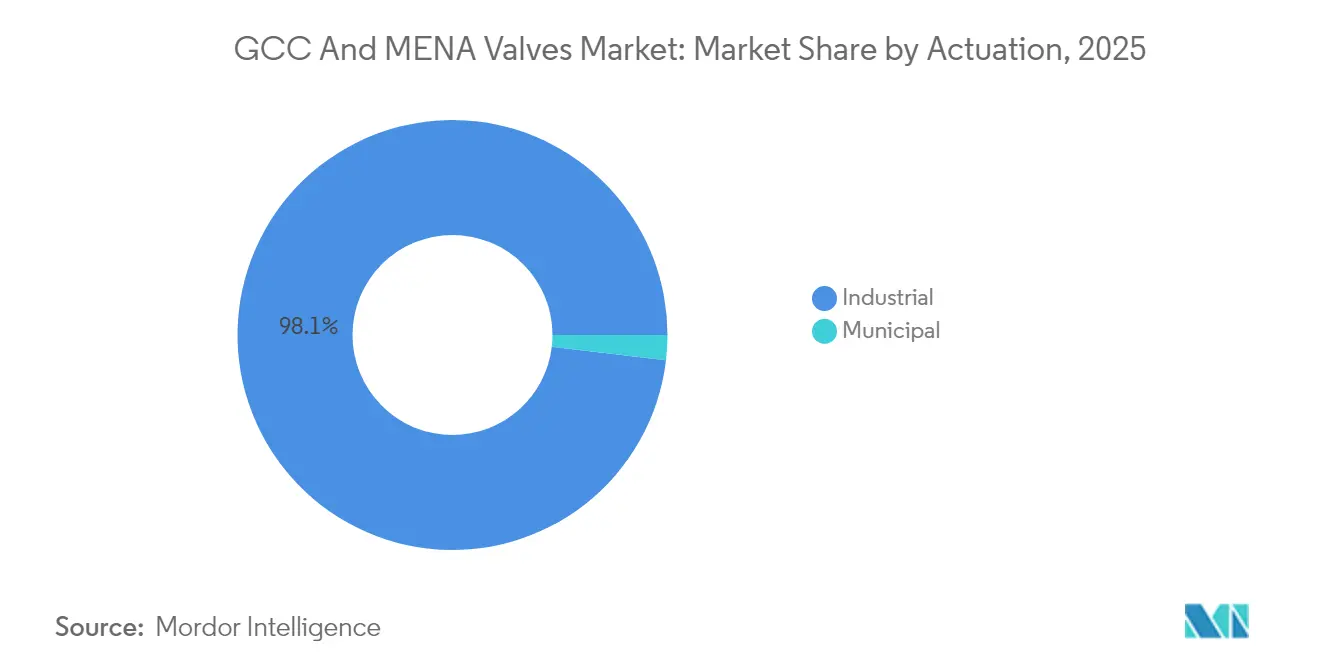

- By actuation, the industrial segment accounted for 98.12% of the GCC and MENA valves market size in 2025 and is expected to sustain a 4.84% annual growth rate through 2031.

- By geography, Saudi Arabia accounted for 37.24% of the 2025 revenue and is projected to advance at a 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC And MENA Valves Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing power-gen CAPEX in GCC countries | +1.2% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Mega-scale refinery upgrades across MENA region | +1.5% | Egypt, Algeria, Saudi Arabia, UAE | Long term (≥4 years) |

| Rapid desalination plant build-out | +0.9% | Saudi Arabia, UAE, Qatar, Algeria | Short term (≤2 years) |

| Mandatory leak-detection regulations (API 624/641) | +0.8% | GCC core (Saudi Arabia, UAE, Qatar) | Medium term (2-4 years) |

| Digital twins and remote valve-monitoring programs | +0.8% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Power-Gen CAPEX in GCC Countries

New combined-cycle gas turbines and solar-hybrid installations will add more than 20 GW of dispatchable and renewable capacity by 2028. Each megawatt requires steam-isolation gate valves, boiler blowdown ball valves, and feedwater control globes, driving immediate demand across the GCC and MENA valves market[1]Power Technology, “Qatar Facility E Water and Power Project Details,” power-technology.com. Qatar’s Facility E integrates 2,415 MW of generation with 110 million imperial gallons per day of desalination, consolidating thousands of valves into a single EPC package. Higher steam temperatures push specifications toward Class 900 and Class 1500 ASME ratings, which in turn elevate ticket prices and prolong forge-to-delivery cycles. OEMs able to pre-machine forgings and stock duplex trims mitigate schedule risk and win frame agreements. Over the medium term, hydrogen-ready turbines will introduce new metallurgical requirements that favor suppliers with in-house materials laboratories and additive manufacturing capacity.

Mega-Scale Refinery Upgrades Across the MENA Region

Egypt, Algeria, and Saudi Arabia collectively announced more than USD 20 billion in refinery CAPEX during 2024, embedding five- to seven-year procurement cycles for thousands of control, isolation, and pressure-relief valves. Egypt’s Assiut coker and isomerization units alone require several hundred specialty valves rated for high-temperature naphtha and catalyst slurry. Algeria’s Hassi Messaoud retrofit demands corrosion-resistant trims and tight shutoff to process heavier crudes. Saudi Aramco’s Ras Tanura expansion locks in long-term frame agreements for API 600 gate valves, API 608 ball valves, and smart positioners. Tier-1 suppliers leverage installed-base data to justify predictive-maintenance contracts, boosting aftermarket revenue in the GCC and MENA valves market. Long-duration megaprojects also create insulation from oil-price volatility, keeping order books visible well into 2029.

Rapid Desalination Plant Build-Out

Gulf governments view desalination as a national-security imperative. Saudi Arabia alone is targeting a significant increase in its desalination capacity, with plans for the private sector to reach a capacity of 8.1 million m³/d by 2032. The total capacity, including public projects, is projected to be approximately 8.8 million m³/d by 2028 and 9.6 million m³/d by 2030. This underpins the demand for large-diameter butterfly valves in seawater intake and the demand for high-pressure ball valves in brine discharge. Abu Dhabi’s 818,000 m³/d Hassyan plant established a new benchmark for electric actuators with low-emission seals, reinforcing a technology pivot already evident in the GCC and MENA valves market. Hybrid solar-powered RO schemes favor all-electric actuation to eliminate compressed-air infrastructure, lowering total lifecycle costs. Regional content policies direct commodity-grade butterfly casings to local foundries, while retaining high-spec trims for European or North American OEMs, striking a balance between cost and performance.

Mandatory Leak-Detection Regulations and Digital Twins

The Gulf Standards Organisation’s adoption of API 624 and API 641 caps fugitive emissions at 100 ppm, effectively obsoleting legacy packed-stem designs in refineries and gas plants[2]OnePetro, “API 641 Valve Compliance Roadmap,” onepetro.org. Saudi Aramco’s sitewide digital-twin program models valve performance under transient operations, enabling predictive maintenance that extends mean time between overhauls by up to 30%. OEMs offering smart positioners with embedded vibration sensors win retrofit orders, while regional assemblers lacking test labs exit the premium tier. ISO 15848 certification has become a de facto tender prerequisite in the UAE and Qatar, narrowing pre-qualified vendor lists and elevating margins across the GCC and MENA valves market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged subsidy cuts curbing municipal budgets | -0.5% | Kuwait, Egypt, Algeria | Short term (≤2 years) |

| Skills gap in advanced actuation maintenance | -0.6% | GCC countries | Medium term (2-4 years) |

| Geopolitical sanctions limiting Iran-linked trade | -0.6% | Iran, Iraq; regional spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Subsidy Cuts Curbing Municipal Budgets

Kuwait’s water production costs average USD 2.50 per cubic meter, while residential tariffs remain below USD 0.20, absorbing 92% of utility revenue and forcing the Treasury to cover annual deficits exceeding USD 8.8 billion. Similar distortions in Egypt and Algeria have deferred pipeline rehabilitation, resulting in shrinking valve orders from municipal buyers. Budget freezes lengthen tender cycles beyond 18 months, leaving the GCC and MENA valves market heavily skewed toward industrial projects. Utilities that postpone automation spend more on unplanned repairs, thereby widening the performance gap compared to digitally mature oil and gas operators. Political resistance to rate reform suggests a lingering drag on municipal valve contracting through 2027.

Skills Gap in Advanced Actuation and Geopolitical Sanctions

Fieldbus-enabled electric and pneumatic actuators now dominate large-project specifications, yet regional maintenance crews frequently rely on expatriate technicians for commissioning. High turnover during turnarounds constrains throughput when hundreds of valves require calibration. Concurrently, UK and EU sanctions imposed in 2024 prohibit the export of bellows-sealed and nickel-alloy valves to Iranian nuclear and petrochemical entities, fragmenting supply chains. Multinationals that serve dual markets in the GCC and Iran incur incremental compliance costs by segregating inventories and implementing end-use audits. Sanctions spillover into Iraq complicates World Bank-financed projects, while an exodus of skilled labor to higher-pay GCC roles amplifies the talent gap. These dynamics shave 0.6 percentage points off the projected CAGR of the GCC and MENA valves market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Legacy Gate Valves Yield Share to Severe-Service Ball Designs

Gate valves still generated 21.88% of 2025 revenue within the GCC and MENA valves market, cemented by decades of service on crude and gas trunklines where full-bore flow and minimal pressure drop are critical. Saudi Aramco’s Master Gas System and ADNOC’s onshore grids specify Class 900 slab-gate and Class 1500 expanding-gate designs in duplex stainless steel to combat sour environments. Yet the market’s fastest expansion belongs to ball valves, forecast at a 4.98% CAGR as operators retrofit subsea tiebacks and high-pressure gas-gathering systems. Flowserve’s USD 290 million acquisition of MOGAS in 2024 underscores a strategic pivot toward metal-seated severe-service ball valves that can withstand pressures of up to 15,000 psi and temperatures of up to 400 °C without seat damage. Triple-offset butterfly valves retain an economic edge in large-diameter desalination headers, while globe valves anchor refinery throttling duties despite higher pressure drops. Plug valves secure niche slurry applications. API 624 and API 641 mandates accelerate the shift from packed-stem gate valves toward bellows-sealed or diaphragm-sealed alternatives, subtly compressing gate-valve share by 2031 and diversifying revenue across the GCC and MENA valves market.

Growth in ball-valve orders also stems from LNG megaprojects pursuing low-leakage cryogenic isolation where bubble-tight shutoff minimizes methane slip. Metal-seated designs with spring-energized Inconel lip seals outperform elastomeric seats in extreme temperatures. Meanwhile, butterfly-valve manufacturers are innovating in composite-disc materials to reduce weight in 4-meter-diameter seawater shutoff units, unlocking savings in actuator sizing. Globe-valve suppliers differentiate on low-noise trims for hydrogen reformers, a critical feature as regional refineries curb flare emissions. Underlying all product lines is a premium on certified fugitive-emissions performance and traceable metallurgy, forging durable barriers to entry and underpinning price discipline in the GCC and MENA valves market.

By Actuation: Industrial Automation Sustains Dominance

Industrial operators captured 98.12% of the 2025 demand, and the segment is expected to sustain a 4.84% growth rate as upstream gas, refining, petrochemicals, and power generation absorb the bulk of capital expenditures. ADNOC’s USD 45 billion Ruwais LNG complex alone requires thousands of fail-safe pneumatic ESDs and modulating electric control valves, underscoring the scale advantage of industrial buyers. Process-industry users embed valves within sophisticated distributed-control systems, mandating smart positioners with HART, Foundation Fieldbus, or emerging Ethernet-APL protocols. Saudi Aramco’s digital-twin program demands real-time performance data, pushing the GCC and MENA valves market toward sensors that report stem friction, seat leakage, and cycle counts.

Municipal utilities remain capital-constrained, deferring automation and prolonging the service life of manual gate valves despite rising non-revenue water (NRW) losses. In desalination, however, electric actuation is gaining share as reverse-osmosis plants harness photovoltaic power, enabling solar-ready microgrids that sideline compressed-air infrastructure. Hybrid power-water schemes such as Qatar’s Facility E blur conventional segment boundaries yet remain classified as industrial due to their project size and financing structures. Over the forecast horizon, the industrial category’s share of the GCC and MENA valves market is unlikely to dip meaningfully below 97%, regardless of gradual reform in municipal tariffs.

Geography Analysis

Saudi Arabia accounted for a 37.24% share of the GCC and MENA valves market in 2025 and is on track for a market-leading 6.72% CAGR through 2031. The Jafurah unconventional-gas program targets 2 bcf/d of sales gas, catalyzing demand for 15,000 psi sour-service wellhead isolation and choke valves. Concurrently, the USD 7.7 billion Fadhili expansion and NEOM’s 8 million m³/d desalination backbone layer incremental orders for large-diameter butterfly valves, Class 1500 ball valves, and low-fugitive-emission packings. The Kingdom’s adoption of API 624 and API 641 governs both greenfield specifications and brownfield retrofits, ensuring steady aftermarket revenue across the GCC and MENA valves market.

The UAE’s valve spend is anchored by ADNOC’s Ruwais LNG megaproject and the 818,000 m³/d Hassyan RO plant. Both specify ISO 15848-certified electric actuators aligned with Abu Dhabi’s net-zero road map, nudging local fabricators into joint ventures with European OEMs. Qatar’s North Field expansion adds 49 million tonnes per annum (mtpa) of liquefaction capacity, emphasizing the use of cryogenic ball valves in Invar and Monel, which elevates the average selling price profile. Egypt’s USD 12 billion refinery modernization program is funneling orders to duplex-steel globe and gate valves, although payment-risk premiums persist. Algeria’s Hassi Messaoud revamp introduces corrosion-resistant trim requirements, yet local-content mandates complicate fast-track procurement. Iran occupies a special case: UK and EU sanctions prohibit high-spec valve exports, forcing Iranian operators to rely on Chinese and Russian suppliers at higher lifecycle costs. Iraq faces spillover risk as Iranian-origin components slip into cross-border trade, exposing EPCs to compliance violations. Smaller GCC states and North African markets collectively add niche volume through district-cooling networks and cross-border pipelines, but fiscal pressures constrain growth.

Competitive Landscape

The GCC and MENA valves market remains moderately consolidated, with major players such as Schlumberger leveraging multi-decade frame agreements with end-user giants in the region, including Saudi Aramco, ADNOC, and QatarEnergy. Installed-base familiarity and pre-qualification on sour-gas and cryogenic specifications create switching costs that insulate leading vendors. Flowserve’s USD 290 million acquisition of MOGAS signals a pivot toward metal-seated severe-service ball valves, addressing performance gaps in superheated steam, slurry, and high-pressure gas duties.

Below the top tier, niche specialists capture market share by offering API 624/641 compliance at 16-week lead times, compared to 24 weeks for incumbents —a crucial advantage during refinery turnarounds. Local assemblers in Algeria and Egypt meet content mandates but lack funding for research and development of severe-service trims. The aftermarket opportunity is expanding as refineries retrofit legacy valves to meet 100 ppm fugitive emissions limits; OEM upgrade kits command premiums that smaller fabricators cannot match. Overall, the supply landscape favors large players but leaves space for agile entrants adept at certification and rapid delivery, sustaining dynamic competition in the GCC and MENA valves market.

GCC And MENA Valves Industry Leaders

Flowserve Corporation

Emerson Electric Co.

AVK Gulf And Watecom International Water Network LLC

Baker Hughes, a GE Company

IMI Critical Engineering

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: IMI Critical Engineering has launched API 624-certified bellows-sealed globe valves, targeting GCC refinery retrofits.

- October 2024: Schlumberger has completed its USD 2.4 billion acquisition of Aker Solutions’ subsea business, integrating deepwater valve technology and enhancing its positioning in the Red Sea and East Med.

- August 2024: Flowserve finalized the USD 290 million acquisition of MOGAS Industries, bolstering metal-seated severe-service ball-valve capabilities for high-temperature steam and sour-gas duties.

GCC And MENA Valves Market Report Scope

By Valve Type

| Butterfly Valve |

| Ball Valve |

| Globe Valve |

| Gate Valve |

| Plug Valve |

| Other Types |

By Actuation

| Industrial |

| Municipal |

By Country

| Saudi Arabia |

| UAE |

| Qatar |

| Algeria |

| Egypt |

| Iran |

| Iraq |

| Rest of Middle East and North Africa |

| By Valve Type | Butterfly Valve |

| Ball Valve | |

| Globe Valve | |

| Gate Valve | |

| Plug Valve | |

| Other Types | |

| By Actuation | Industrial |

| Municipal | |

| By Country | Saudi Arabia |

| UAE | |

| Qatar | |

| Algeria | |

| Egypt | |

| Iran | |

| Iraq | |

| Rest of Middle East and North Africa |

Key Questions Answered in the Report

How large is the GCC and MENA valves market in 2026?

The GCC and MENA valves market size is estimated at USD 12.26 billion in 2026 and is forecast to reach USD 15.54 billion by 2031.

Which country will grow fastest in valve spending to 2031?

Saudi Arabia is projected to expand at a 6.72% CAGR, outpacing all other regional markets.

Which valve type will post the highest growth rate?

Ball valves are expected to register a 4.98% CAGR, driven by subsea tiebacks and high-pressure gas-gathering retrofits.

What drives the surge in valve demand for desalination projects?

Rapid build-out of reverse-osmosis capacity, especially in Saudi Arabia and the UAE, is boosting large-diameter butterfly and high-pressure ball-valve orders.

How are fugitive-emissions rules affecting procurement?

Adoption of API 624 and API 641 standards forces refiners to retrofit thousands of valves, favoring suppliers with certified low-leakage designs.

Which companies hold entrenched positions in the region?

Emerson, Flowserve, and Baker Hughes lead via long-term agreements with national oil companies, while niche severe-service specialists gain share through rapid compliance and delivery.

Page last updated on: