India Industrial Valves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

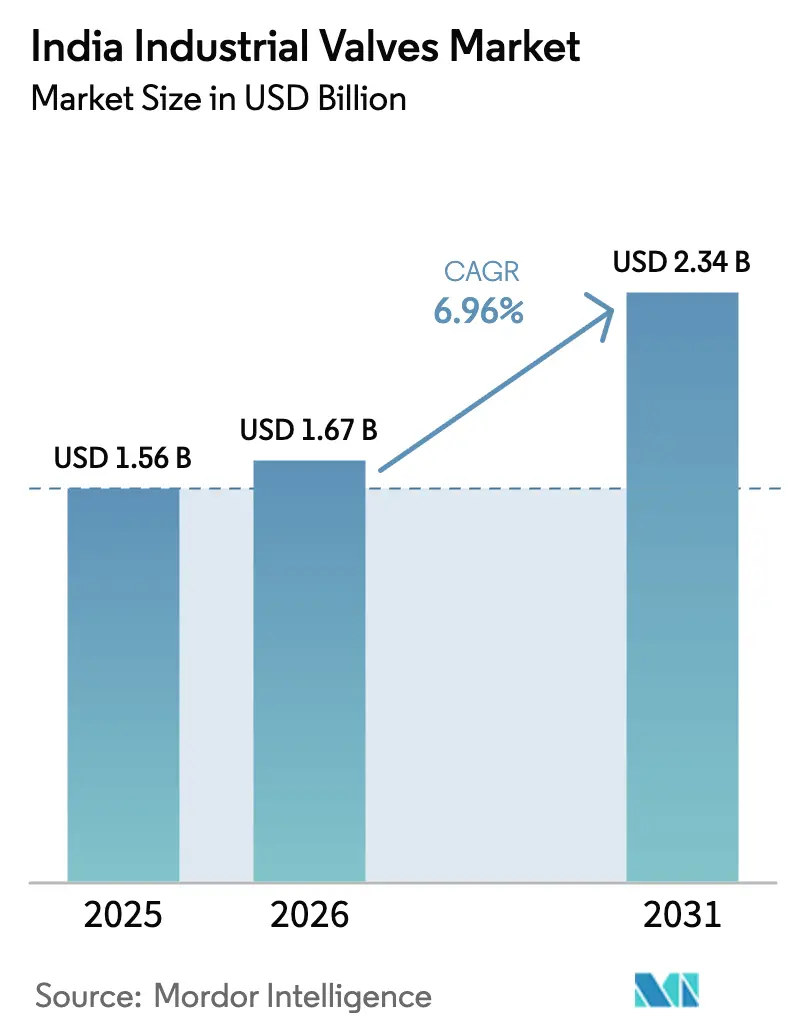

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.67 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 6.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Industrial Valves Market Analysis by Mordor Intelligence

The India Industrial Valves Market size is expected to grow from USD 1.56 billion in 2025 to USD 1.67 billion in 2026 and is forecast to reach USD 2.34 billion by 2031 at 6.96% CAGR over 2026-2031. Rising capital outlays in water supply networks, hydrocarbon pipelines, and renewable power plants keep the demand curve steep. Contract awards tied to national missions such as Jal Jeevan push public utilities to order corrosion-resistant gate, globe, and butterfly valves, while refineries, city-gas distributors, and petrochemical complexes widen the call for high-pressure ball valves. Automation programs across chemical clusters in Gujarat and Maharashtra accelerate the uptake of smart, IIoT-ready control valves, raising the average selling price. At the same time, raw-material cost swings and import competition from China compress margins, making scale and integrated machining critical to profitability. Suppliers that offer rapid-turnaround service and Bureau of Indian Standards (BIS) compliance gain an edge in winning multi-state contracts.

Key Report Takeaways

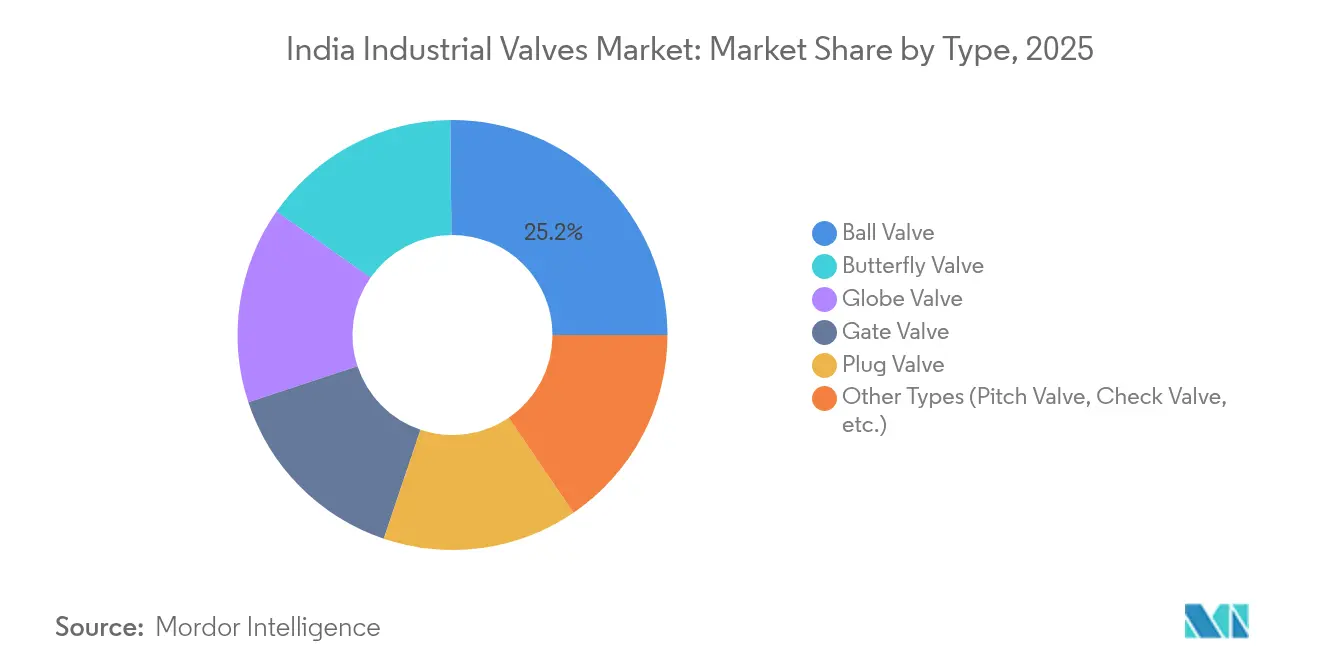

- By type, ball valves led with a 25.17% share of the India industrial valves market in 2025, while butterfly valves are projected to expand at a 7.05% CAGR through 2031.

- By product, quarter-turn valves held 39.80% share of the India industrial valves market size in 2025, and other products, including control valves and actuators, are expected to rise at a 7.25% CAGR to 2031.

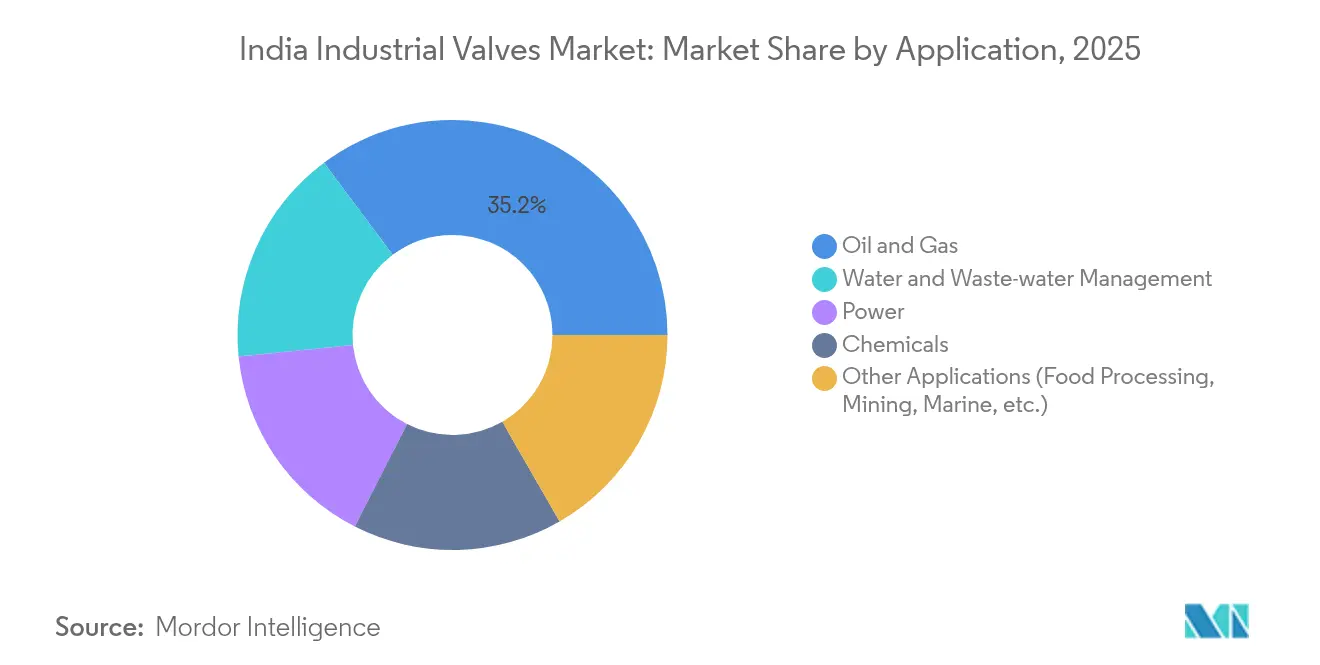

- By application, oil and gas accounted for 35.20% of the India industrial valves market size in 2025; water and wastewater management is forecast to grow at a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Industrial Valves Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government investment in water and waste-water networks | +1.8% | National, with concentration in rural areas and tier-2 cities | Medium term (2-4 years) |

| Expansion of oil and gas pipeline and CGD projects | +1.2% | National, with focus on western and northern regions | Long term (≥ 4 years) |

| Ongoing power-generation capacity additions | +0.9% | National, with emphasis on renewable energy corridors | Medium term (2-4 years) |

| Rising chemical and process-industry investments | +0.8% | Gujarat, Maharashtra, Andhra Pradesh clusters | Long term (≥ 4 years) |

| Adoption of IIoT-enabled smart valves | +0.6% | Industrial hubs in western and southern India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Investment in Water and Waste-water Networks

Jal Jeevan Mission and AMRUT 2.0 continue to fund household tap connections, sewage treatment plants, and water-recycling facilities. The USD 50 billion allocation through 2024 created rolling tenders for gate, globe, and butterfly valves across treatment trains, distribution mains, and sludge lines. States now extend procurement schedules to 2028 to meet both rural service and urban reuse targets. Projects specify stainless-steel trims, epoxy coatings, and actuator-ready flanges, boosting the ticket size per valve. Suppliers that secure BIS certification and deploy regional service teams win repeat orders, as municipalities insist on local support for preventive maintenance[1]Ministry of Jal Shakti, “Jal Jeevan Mission,” jaljeevanmission.gov.in.

Expansion of Oil and Gas Pipeline and CGD Projects

City-gas distribution licenses covering 280 districts demand pressure-regulation stations, metering skids, and safety shut-off assemblies. Each skid integrates fire-safe ball valves, double-block-and-bleed designs, and remotely actuated isolation units. Concurrent product and crude pipelines linking refineries to consumption clusters call for ANSI Class 600 and above ball and check valves. The government’s vision of blending bio-fuels into existing networks adds dual-service specifications, favoring manufacturers with metallurgy and sealing know-how for mixed-media flows[2]Petroleum and Natural Gas Regulatory Board, “City Gas Distribution,” pngrb.gov.in.

Ongoing Power-Generation Capacity Additions

Thermal units ordered under super-critical and ultra-super-critical programs require globe and gate valves that tolerate 600 °C steam and 300 bar pressure. Renewable additions headed for 500 GW by 2030 spur demand for butterfly and ball valves in solar-thermal storage circuits, wind-turbine hydraulic brakes, and pumped-hydro reservoirs. Grid modernization projects need automated control valves in substations and battery farms, anchoring steady offtake from utilities.

Rising Chemical and Process-Industry Investments

The USD 142 billion downstream program through 2035 concentrates large-scale crackers, specialty intermediate units, and polymer plants inside Petroleum, Chemicals and Petrochemicals Investment Regions. High-purity lines use PTFE-lined or alloy-20 valves, while aromatic chains specify low-leakage control valves for VOC abatement. Cluster development lets buyers negotiate volume deals, prompting suppliers to stock standard sizes in regional warehouses for rapid call-offs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost and maintenance burden | -1.5% | National, affecting smaller industrial users | Short term (≤ 2 years) |

| Raw-material price volatility (steel/alloys) | -1.0% | National, with higher impact on domestic manufacturers | Medium term (2-4 years) |

| Competition from low-cost imports (mainly China) | -1.0% | National, particularly affecting standard valve segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Maintenance Burden

Smart valves raise purchase prices by 15-30% compared with manual versions, and long-cycle spares enlarge inventory budgets. Small water boards and MSME plants often postpone upgrades until grant funding arrives. Some municipalities specify lower-grade trims to cut capex, but this boosts lifecycle costs when corrosion sets in. Training gaps further deter adoption of sophisticated positioners, locking many buyers into basic on-off models.

Raw-Material Price Volatility (Steel/Alloys)

Carbon-steel and stainless-steel coils form up to 70% of the valve bill of materials. Benchmark prices swung more than 20% between 2023 and 2024, reflecting iron-ore shortages and coking-coal premiums. Domestic producers carry lean inventory; a sudden spike forces them to re-quote or accept margin erosion on fixed-price contracts. Long-term framework agreements with EPC contractors become difficult to price without escalation clauses, slowing the closure of large deals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type – Ball Valves Lead Multi-Application Demand

Ball valves secured a 25.17% India industrial valves market share in 2025 on account of tight shut-off, minimal pressure drop, and ease of automation. Oil terminals, CGD stations, and chemical reactors favor forged and trunnion-mounted designs that operate at up to 600 bar. The India industrial valves market size for butterfly valves is forecast to widen rapidly, supported by large-diameter intake pipelines in desalination and sewage treatment plants advancing at a 7.05% CAGR. Globe valves keep relevance in throttling duties across power-station steam circuits where precise flow is vital. Gate valves remain the default isolators in fire-water mains, while plug valves serve niche hydrocarbon vapor-recovery lines. Check valves, though smaller in ticket value, post steady volumes thanks to mandatory non-return requirements in water transfer schemes.

Mid-tier EPC firms increasingly bundle valve supply under master service agreements to shorten tender cycles. Makers that pre-qualify under multiple valve categories receive higher frame-contract volumes. Workshops equipped for cryogenic testing and fugitive-emission certification are seeing rising inquiries from LNG logistics players. Standards compliance to API 6D, ISO 15848-1, and BIS IS 14846 influences wins across refineries, water boards, and fertilizer units.

By Product – Quarter-Turn Dominance Reflects Operational Preferences

Quarter-turn devices, covering ball, butterfly, and plug variants, held 39.80% share of the India industrial valves market in 2025. Plant operators value their 90-degree stroke, clear visual indication, and compatibility with both pneumatic and electric actuators, which eases remote control. Multi-turn valves, largely gate and globe, continue to dominate high-temperature, high-pressure lines but lose share where quick isolation is critical. The India industrial valves market size for other products, chiefly control valves and actuators, is tracking a 7.25% CAGR due to process optimization programs in the petrochemical and pharmaceutical sectors.

Leading actuator suppliers roll out modular platforms that accept digital positioners and wireless sensors by design. Integration with distributed control systems lowers commissioning time. Vendors now ship pre-wired skid-mounted packages, reducing site labor. Cast-iron housings see a gradual phase-out in favor of ductile-iron or carbon-steel bodies that fit higher pressure classes without significant cost jumps.

By Application – Oil and Gas Leadership Amid Water-Sector Acceleration

Oil and gas held a 35.20% share of the India industrial valves market size in 2025, anchored by refinery expansions, strategic petroleum reserves, and the widening CGD footprint. Specifications stress fire-safe designs, secondary seat-insert materials like PTFE-graphite, and antistatic stems. Meanwhile, water and wastewater management revenues are growing at a 7.08% CAGR, backed by mission-mode funding for surface water treatment, desalination, and reuse plants. The application mix keeps shifting toward automated knife-gate valves in sludge lines and double-eccentric butterfly designs for potable grids.

Chemical plants retain a high value-per-ton ratio, particularly within specialty intermediate blocks that demand corrosion-resistant alloys such as duplex stainless steel. Power-sector procurement splits between super-critical thermal stations and renewable support infrastructure like solar-thermal storage and pumped-hydro facilities. Miscellaneous segments—food processing, mining, and marine—contribute incremental orders, with mining valves benefiting from coal block auctions and marine valves from port-side tank farm growth.

Geography Analysis

Western and northern states lead India's industrial valves market demand owing to petrochemical clusters, oil logistics corridors, and dense urban populations. Gujarat’s PCPIR belt and Maharashtra’s refinery and chemical complexes attract high-volume, high-specification orders that favor suppliers carrying API and BIS certifications. Rajasthan, Haryana, and Uttar Pradesh add volumes through CGD rollouts and thermal-plant overhauls.

Southern India showcases the fastest uptake of automation and smart valve platforms. Tamil Nadu and Karnataka, home to strong wind and solar supply chains, specify actuator-ready butterfly valves for cooling loops and brake hydraulics. IT parks and electronics factories in these states stipulate low-leakage isolation valves for ultra-pure water systems, creating a niche for high-purity designs. Kerala and Andhra Pradesh ports adopt stainless-steel marine-grade valves to handle saline environments.

Eastern regions, notably Odisha, Jharkhand, and Chhattisgarh, register rising offtake tied to mining and steel capacity hikes. Coal washeries, slurry pipelines, and pellet plants deploy abrasion-resistant knife-gate valves and pinch valves. Northeast pipeline projects connecting gas fields to fertilizer units pull in cryogenic ball valves suited for LNG transport. Across most rural districts, Jal Jeevan civil works continue to favor cost-effective, manually operated gate valves, yet pilot projects now trial smart metering systems that would lift actuator demand in the future.

Competitive Landscape

The India industrial valves market exhibits moderate fragmentation. International majors such as Flowserve, Emerson, and Baker Hughes retain share in high-specification segments through global references and technology portfolios. Domestic leaders, including L&T Valves and Kirloskar Brothers, leverage local manufacturing, extensive dealer networks, and familiarity with public-tender procedures. Niche players focus on specialty alloys, cryogenic designs, or mini-valves for instrumentation panels, filling gaps that larger firms overlook. Supply-chain resilience gains attention after raw-material price shocks. Integrated foundries allied with valve plants mitigate lead-time risk and improve traceability. Firms sourcing from in-house steel shops control metallurgical consistency, easing BIS audits. For export-oriented orders, Indian producers pursue CE-PED and API monograms to tap Gulf and African projects.

India Industrial Valves Industry Leaders

AVK Valves India Pvt Ltd

Emerson Electric Co.

Flowserve Corporation

KIRLOSKAR BROTHERS LIMITED (INDIA)

L&T Valves Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hydreco Hydraulics inaugurated a new valve manufacturing facility in Bangalore to expand localized supply for mobile and industrial equipment.

- September 2025: Danfoss India introduced the STL industrial refrigeration valve series, designed for energy-efficient cold-chain operations.

India Industrial Valves Market Report Scope

Industrial valves are mechanical devices that control the flow and pressure of liquids, gases, and slurries within a system. They are also known as regulators and are used in various applications. Valves vary significantly in size, design, function, and operation.

The Indian industrial valves market is segmented by type, product, application, and geography. By type, the market is segmented into butterfly valve, ball valve, globe valve, gate valve, plug valve, and other types (pitch valve, check valve, etc.). By product, the market is segmented into quarter-turn valves, multi-turn valves, and other products (control valves, valve actuators, etc.). By application, the market is segmented into power, water and wastewater management, chemicals, oil and gas, and other applications (food processing, mining, marine, etc.).

For each segment, the market sizing and forecasts are provided in terms of value (USD).

| Butterfly Valve |

| Ball Valve |

| Globe Valve |

| Gate Valve |

| Plug Valve |

| Other Types (Pitch Valve, Check Valve, etc.) |

| Quarter-turn Valve |

| Multi-turn Valve |

| Other Products (Control Valves, Valve Actuators, etc.) |

| Power |

| Water and Waste-water Management |

| Chemicals |

| Oil and Gas |

| Other Applications (Food Processing, Mining, Marine, etc.) |

| By Type | Butterfly Valve |

| Ball Valve | |

| Globe Valve | |

| Gate Valve | |

| Plug Valve | |

| Other Types (Pitch Valve, Check Valve, etc.) | |

| By Product | Quarter-turn Valve |

| Multi-turn Valve | |

| Other Products (Control Valves, Valve Actuators, etc.) | |

| By Application | Power |

| Water and Waste-water Management | |

| Chemicals | |

| Oil and Gas | |

| Other Applications (Food Processing, Mining, Marine, etc.) |

Key Questions Answered in the Report

What is the projected value of the India industrial valves market by 2031?

The market is forecast to reach USD 2.34 billion by 2031, reflecting a 6.96% CAGR.

Which valve type currently holds the largest share in India?

Ball valves lead with 25.17% share in 2025 due to widespread use in oil, gas, and water applications.

Which end-use sector is expected to grow fastest for valve demand?

Water and waste-water management is set to advance at a 7.08% CAGR as Jal Jeevan and AMRUT 2.0 projects scale up.

What drives the adoption of smart valves in Indian plants?

Digitalization initiatives in chemical, oil, and power facilities favor IIoT-enabled valves that support predictive maintenance and remote control.

How do raw-material price swings affect valve manufacturers?

Steel and alloy cost volatility squeezes margins on fixed-price contracts, prompting suppliers to seek escalation clauses and integrated supply chains.

Page last updated on: