Cryocooler Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

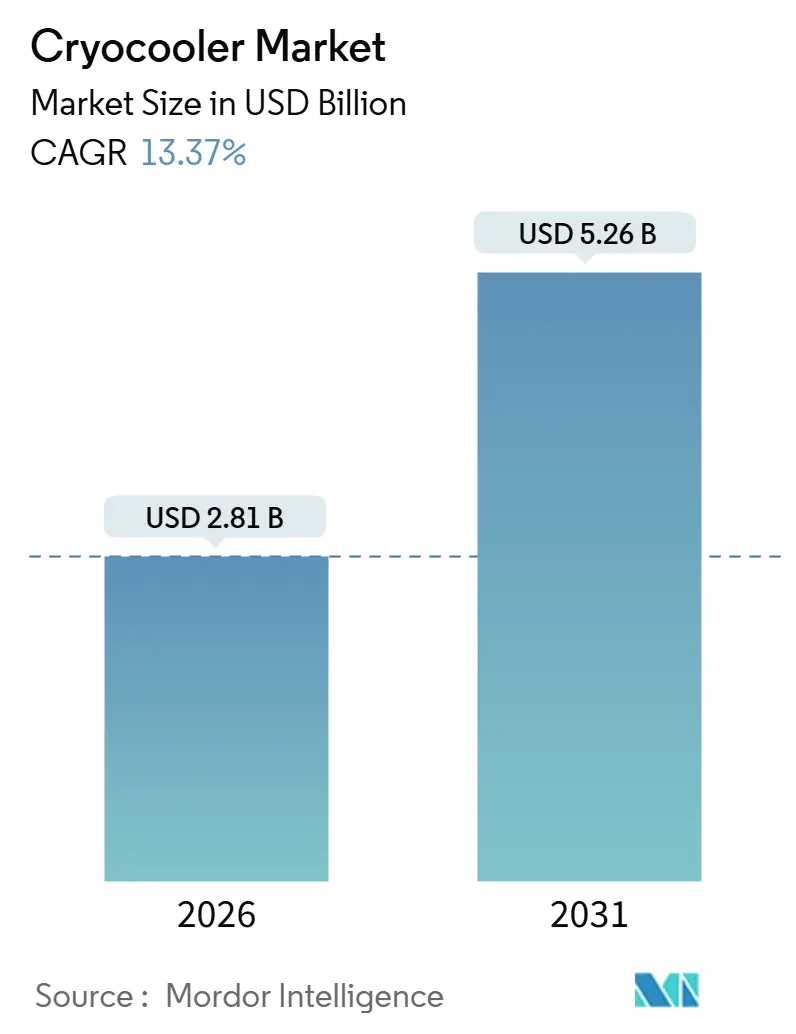

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 5.26 Billion |

| Growth Rate (2026 - 2031) | 13.37% CAGR |

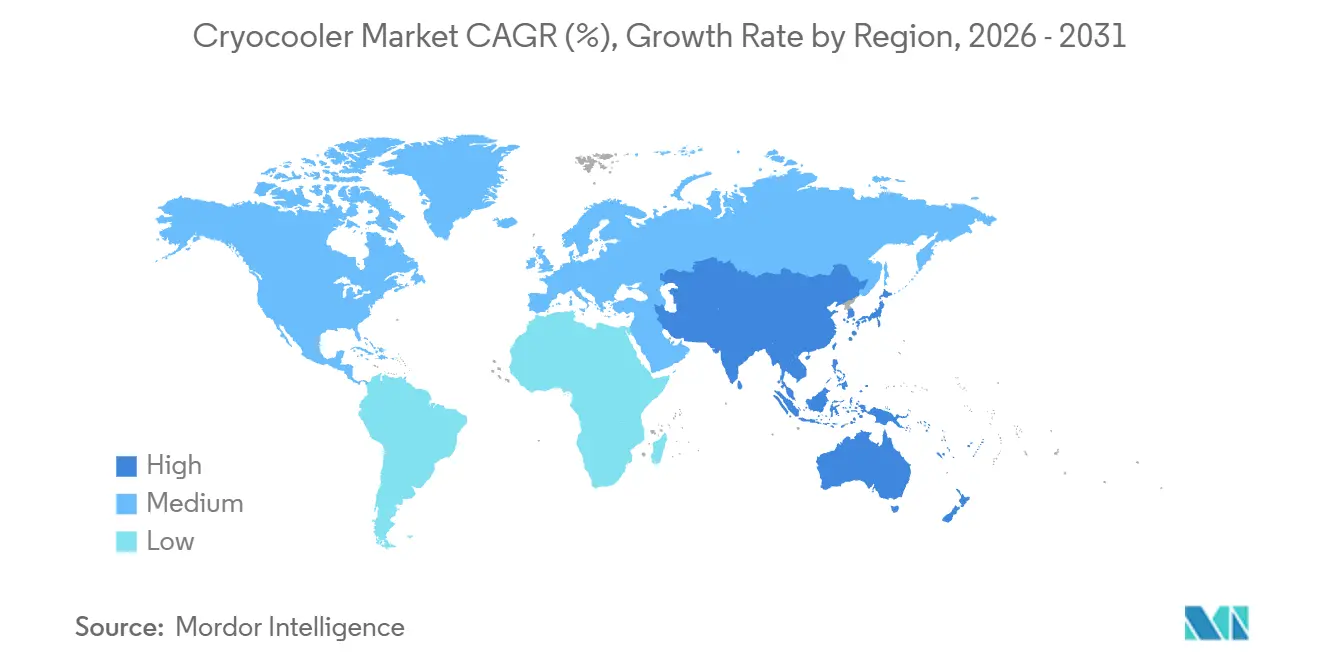

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cryocooler Market Analysis by Mordor Intelligence

The cryocooler market size stands at USD 2.81 billion in 2026 and is projected to reach USD 5.26 billion by 2031, posting a 13.37% CAGR over the period. Growth is fueled by quantum-computing scale-up that requires sub-4 kelvin pre-coolers, the rapid launch cadence of small-satellite constellations, and defense offset mandates that localize production in India and the United Arab Emirates. Stirling architectures remain the volume workhorse, yet pulse-tube designs are accelerating because vibration-free operation extends the life of precision instruments. Healthcare continues to dominate installed base revenue owing to cryogen-free MRI expansion, but quantum technology is advancing faster as laboratories transition to pilot-scale fabrication lines. Regionally, North America benefits from liquefied-natural-gas peak-shaving and Department of Defense quantum-sensor programs, while Asia Pacific builds tier-2 city MRI suites and sovereign quantum-computing centers. Across operating cycles, closed-loop systems lead deployments, yet open-loop Joule-Thomson expanders are penetrating portable military uses where helium logistics are manageable.

Key Report Takeaways

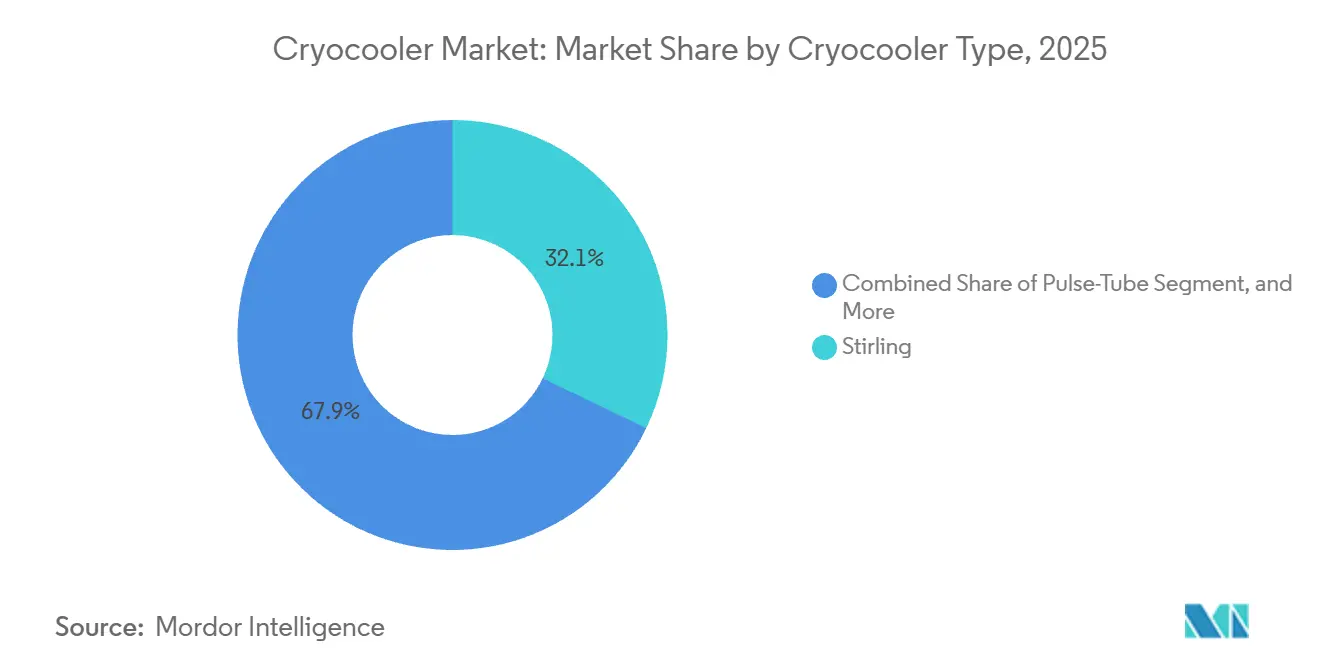

- By cryocooler type, Stirling units held 32.13% of cryocooler market share in 2025, whereas pulse-tube solutions are forecast to expand at a 14.87% CAGR to 2031.

- By temperature range, the 77 kelvin – 200 kelvin band captured 41.76% of cryocooler market size in 2025; the 1 kelvin – 20 kelvin segment is projected to rise at a 15.27% CAGR through 2031.

- By operating cycle, closed-loop designs commanded 68.49% of installations in 2025, while open-loop expanders are set to grow at 16.19% annually to 2031.

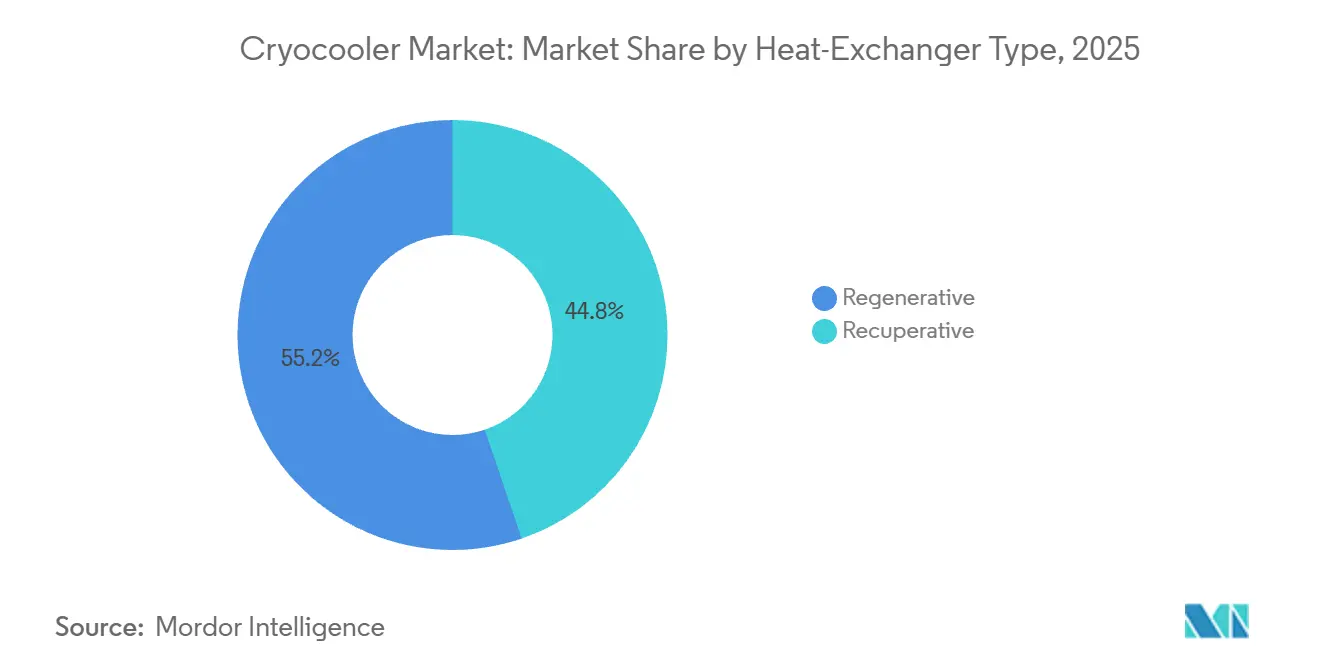

- By heat-exchanger type, regenerative cores led with 55.22% share in 2025; recuperative variants are expected to post a 15.19% CAGR during the forecast.

- By end-user vertical, healthcare retained 27.38% share in 2025, yet quantum technology applications are slated for a 14.19% CAGR to 2031.

- By geography, North America accounted for 34.51% of revenue in 2025, whereas Asia Pacific is anticipated to climb at 14.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cryocooler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for compact cryogenic cooling for IR sensors in soldier-borne devices | +2.1% | Global, with concentration in North America, Europe, India, and UAE | Medium term (2-4 years) |

| Rapid expansion of small-satellite constellations requiring long-life space cryocoolers | +2.4% | Global, led by North America, Europe, and Asia Pacific | Long term (≥ 4 years) |

| Growing MRI system installations in emerging economies tier-2 cities | +2.3% | Asia Pacific core, with spillover to Middle East and Africa | Medium term (2-4 years) |

| LNG peak-shaving projects in North America and China driving large-capacity GM systems | +1.8% | North America and China, with secondary impact in Europe | Short term (≤ 2 years) |

| Quantum-tech scale-up needs sub-4 K dilution pre-coolers | +2.5% | North America and Europe, with emerging activity in Asia Pacific | Long term (≥ 4 years) |

| Defense offset programs fostering domestic cryocooler production in India and UAE | +1.6% | India and UAE, with regional spillover to Middle East and South Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Compact Cryogenic Cooling for IR Sensors in Soldier-Borne Devices

Miniaturized Stirling coolers under 500 grams power helmet-mounted thermal imagers that run eight-hour patrols on one battery set, removing the need for mid-mission battery swaps.[1]Defence Research and Development Organisation, “MoU with Indian Army for Stirling Cryocooler Indigenization,” drdo.gov.in India’s March 2025 memorandum with the Army targets production of 10,000 local 0.5 watt units by 2028, capping unit cost at USD 3,000. Ricor rotary cryocoolers log mean time between failures above 25,000 hours, lifting confidence in harsh-environment reliability. Offset mandates in the United Arab Emirates compel prime contractors to transfer manufacturing know-how, slashing regional lead times to six months. Growing preference for field-replaceable modules is segmenting supply between high-performance special-forces variants and cost-optimized infantry devices.

Rapid Expansion of Small-Satellite Constellations Requiring Long-Life Space Cryocoolers

Operators specify 15-year orbital life and sub-10 watt power draw to safeguard satellite battery margins. Northrop Grumman’s heritage exceeds 300 orbital years, creating an incumbency hurdle for entrants lacking long-duration flight data. Sunpower free-piston Stirling units accumulate 525,000 hours over 230 launches, but the migration to pulse-tube models is quickening because vibration-free operation preserves star-tracker accuracy. ESA’s Copernicus and China’s Gaofen programs favor pulse-tube efficiency near 70 kelvin for infrared payloads. Bluefors introduced the PT205 in March 2025, addressing the sub-10 kelvin requirement of quantum-sensing satellites.

Growing MRI System Installations in Emerging-Economy Tier-2 Cities

Cryogen-free superconducting magnets integrate pulse-tube coolers that maintain 4.2 kelvin, eliminating helium contracts that can exceed USD 50,000 per year. Siemens Healthineers’ Shenzhen line, opened January 2025, produces DryCool magnets for regional tier-2 hospitals. India’s Ayushman Bharat program allocated USD 1.2 billion in 2025 for diagnostic equipment in cities of 0.5 million – 1 million population, underpinning 300 MRI installations by 2028. GE HealthCare’s BlueSeal magnet reduces helium inventory from 1,500 liters to 0.7 liter, although the embedded cooler adds USD 80,000 to capital cost. Service intervals compress from quarterly to annual, freeing hospital technicians for other imaging systems.

Quantum-Tech Scale-Up Needs Sub-4 K Dilution Pre-Coolers

Commercial quantum fabs require hundreds of dilution refrigerators per site; each employs a pulse-tube stage that reaches 3 kelvin before helium-3/helium-4 mixing. Bluefors’ July 2025 millikelvin Cryo-CMOS platform houses control electronics at 4 kelvin, enabling qubit counts above 1,000 per chip. A March 2025 Bluefors-Cryomech integration doubled cooling power at 3 kelvin, cutting dilution-refrigerator footprints by 25%. Honeywell’s Department of Defense awards under CRUISE and QUEST fund ruggedized mobile dilution systems, moving technology out of stationary labs. As qubit density doubles annually, total helium-3 inventory per fab rises, intensifying demand for higher-throughput cryocoolers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heat-lift limitations below 10 W in sub-5 kg platforms | -1.4% | Global, with acute impact on unmanned aerial vehicle and soldier-borne applications | Medium term (2-4 years) |

| Helium-3 supply bottleneck for sub-1 K applications | -1.7% | Global, with concentration in North America and Europe quantum research | Long term (≥ 4 years) |

| Vibro-acoustic noise non-compliance for airborne EO payloads | -1.2% | North America, Europe, and Asia Pacific defense markets | Short term (≤ 2 years) |

| Capex premium of pulse-tube over GM for greater than 100 W heat-lift | -1.3% | Global industrial and energy applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heat-Lift Limitations Below 10 W in Sub-5 kg Platforms

Miniaturized coolers seldom exceed 8 watts at 77 kelvin when total mass must stay under 5 kilograms. Free-piston Stirling variants reach specific cooling power near 1.6 W/kg but require costly beryllium regenerators for further gains, lifting unit prices above USD 15,000. Rotary Stirling models cut vibration yet sacrifice 20% heat-lift versus linear peers. Pulse-tube approaches remove moving cold ends but entail heavier compressors, breaching mass ceilings. Some soldier systems switch to thermoelectric modules below 5 W heat-lift, leaving cryocoolers to focus on higher-performance military and space payloads.

Helium-3 Supply Bottleneck for Sub-1 K Applications

Global helium-3 output is roughly 8,000 liters per year, with the U.S. Department of Energy accounting for about 60% via tritium decay.[2]U.S. Department of Energy, “Helium-3 Production and Supply Management,” energy.gov Each dilution refrigerator requires 10-50 liters, capping worldwide shipments at under 200 systems annually. Spot prices exceeded USD 2,000 per liter in 2025, reflecting demand for neutron detectors and quantum computers. Closed-cycle units limit annual gas loss to 1%, but initial inventory adds USD 40,000 – 100,000 per system, straining academic budgets. Alternative adiabatic-demagnetization coolers reach sub-kelvin temperatures intermittently, unsuitable for continuous quantum-processor duty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cryocooler Type: Pulse-Tube Gains on Vibration-Free Edge

Stirling machines captured 32.13% cryocooler market share in 2025 on the strength of efficient 77 kelvin operation for soldier sensors and small satellites. Pulse-tube revenue is expected to outpace at a 14.87% CAGR, helped by vibration-free operation that lengthens the life of airborne electro-optical payloads and MRI magnets. Gifford-McMahon systems retain relevance for LNG and industrial gas tasks where heat-lift above 100 watts overrides vibration concerns. Joule-Thomson and Brayton-cycle units stay niche, serving portable or aerospace platforms with unique openness or reverse-flow requirements.

Innovation momentum reinforces the pulse-tube trajectory. Bluefors folded Cryomech regenerator know-how into its portfolio in March 2025, doubling cooling power at 3 kelvin and enabling single-vendor quantum stacks. Northrop Grumman’s Stirling catalog still sets reliability benchmarks with 300 orbital years logged by January 2025. MRI vendors reduce maintenance by shifting from Stirling to pulse-tube, moving service visits from quarterly to yearly. Ricor rotary Stirling platforms offer low vibration but concede heat-lift margin, pushing selection toward application-specific trade-offs.

By Temperature Range: Sub-20 K Segment Surges on Quantum Demand

The 77 kelvin – 200 kelvin band contributed 41.76% of cryocooler market size in 2025, underpinning MRI, industrial gas liquefaction, and HTS applications. However, 1 kelvin – 20 kelvin revenue should rise fastest at 15.27% CAGR as quantum processors and space IR detectors require sub-10 kelvin environments. Operating regimes between 20 kelvin and 77 kelvin favor LNG and hydrogen liquefaction, domains dominated by Gifford-McMahon and Brayton cycles.

Technology rollouts reflect this mix. Bluefors’ PT205 targets vibration-sensitive satellites that run superconducting detectors below 10 kelvin. Siemens’ DryCool magnet, in volume production since January 2025, keeps MRI bore temperatures at 4.2 kelvin without liquid helium, trimming lifetime operating costs by 30%. Honeywell’s defense navigation contracts expand ruggedized sub-kelvin cooling beyond labs into mobile platforms. Gifford-McMahon units remain unchallenged for 20 kelvin liquefaction, where cost per watt stays decisive.

By Operating Cycle: Open-Loop Expands in Tactical Applications

Closed-loop machines represented 68.49% of 2025 shipments, eliminating expendable cryogen and simplifying maintenance for stationary MRI, LNG, and research installations. Open-loop Joule-Thomson expanders are pegged for 16.19% annual growth through 2031 as soldier kits and drone payloads accept cryogen top-ups to slash system mass.[3]Defence Research and Development Organisation, “MoU with Indian Army for Stirling Cryocooler Indigenization,” drdo.gov.in Dismounted infantry devices consume under 1 liter of liquid nitrogen on an eight-hour mission, trading lower acquisition cost for consumable expense.

Reliability leadership favors closed-loop. Ricor rotary designs surpass 25,000 hour mean time between failures in field tests. Still, Thales and Northrop Grumman established UAE joint ventures to assemble open-loop expanders for regional UAV production, leveraging duty-free zones and proximity to Gulf customers. Capital premiums of 60% for closed-loop pulse-tube below 10 watts remain a barrier in weight-constrained roles, yet special-forces units often justify the spend for extended mission life.

By Heat-Exchanger Type: Recuperative Gains in Compact Platforms

Regenerative cores held 55.22% share in 2025 across Stirling, Gifford-McMahon, and pulse-tube systems where efficiency outweighs mass. Recuperative designs are forecast for 15.19% CAGR on Brayton and Joule-Thomson platforms that prioritize compact geometry over peak thermodynamic performance. Miniaturized Stirling coolers cut weight by 15% when swapping to recuperative matrices, although efficiency drops 10-15%, confining adoption to UAVs and soldier sensors.

Hybrid approaches blend both types. Bluefors’ millikelvin Cryo-CMOS stack marries regenerative pulse-tube stages with recuperative Joule-Thomson circuits to hit sub-1 kelvin targets. Linde’s European LNG peaks shave via Brayton recuperative loops teamed with regenerative Gifford-McMahon baseload units to balance capex and flexibility. Meanwhile, regenerative pulse-tube improvements, such as Cryomech-derived regenerator materials, have deferred widespread recuperative migration for many stationary users.

By End-User Vertical: Quantum Technology Disrupts Healthcare Dominance

Healthcare delivered 27.38% of 2025 revenue as tier-2 city hospitals installed cryogen-free MRI suites. Quantum technology, though smaller today, is tracking a 14.19% CAGR as fabs scale from lab pilots to hundreds of dilution refrigerators per site. Space payloads grow at roughly 13.5% annually on the back of earth-observation and missile-warning constellations, while military demand advances at 13.8% amid soldier-borne and airborne programs.

Vendor moves mirror vertical priorities. Siemens’ DryCool line lowers hospital running costs and sidesteps helium logistics in emerging markets. Bluefors and Qblox collaborate on low-dissipation control electronics, crucial as qubit density doubles every year. Honeywell’s DoD awards pivot quantum sensors from research to production, favoring vendors with security accreditation. Indian and UAE offset policies transfer Stirling assembly know-how locally, expanding regional defense ecosystems.

Geography Analysis

North America generated 34.51% of 2025 revenue, supported by LNG peak-shaving plants in the northeastern United States, Department of Defense quantum-sensor procurement, and commercial small-satellite launches. Chart Industries commissioned hydrogen liquefaction systems operating at 20 kelvin, tapping the burgeoning U.S. hydrogen economy. Honeywell’s July 2025 navigation awards accelerate ruggedized mobile dilution refrigerators, extending use cases beyond stationary labs. Northrop Grumman’s legacy of 300 orbital years reinforces the region’s technological moat. Despite demand, helium-3 allocation under Department of Energy custodianship limits North American dilution-refrigerator deliveries to under 120 units yearly, constraining quantum-computing scale-up.

Asia Pacific is set for a 14.16% CAGR to 2031 as China, India, and Japan invest in cryogen-free MRI suites, sovereign quantum initiatives, and satellite constellations. Siemens’ Shenzhen plant, opened January 2025, produces DryCool magnets that cut annual helium spend by USD 50,000 per MRI. India’s USD 1.2 billion Ayushman Bharat diagnostic allocation underwrites 300 MRI rooms by 2028. DRDO’s offset-driven Stirling program targets 70% local content, fostering a South Asian supply base. China’s LNG peak-shaving capacity added 8 million cubic meters in 2025, feeding demand for large Gifford-McMahon units.

Europe posts about 12.8% annual growth, anchored by ESA’s Copernicus satellites, defense modernization, and industrial gas projects. Linde teams regenerative Gifford-McMahon baseload coolers with recuperative Brayton peaks, optimizing European LNG infrastructure. Thales pursues UAE joint production to tap Gulf defense budgets. The Middle East itself is expanding roughly 13.5% on defense offsets, while South America and Africa remain under 10% of world revenue, hampered by limited MRI penetration yet buoyed by Brazil’s public-health outlays and South Africa’s astronomy programs.

Regulatory Landscape

Environmental and trade controls increasingly influence cryocooler design, sourcing, and cross-border delivery for quantum, space, and defense end uses. In the European Union, Commission Implementing Regulation (EU) 2024/3120 (December 2024) and Regulation (EU) 2026/286 (February 2026) set time-bound exemptions for specific ultra-low-temperature and semiconductor-manufacturing cooling uses involving F-gases, reflecting the tension between high-performance cryogenic duty and refrigerant phase-down requirements.

On trade compliance, export controls are tightening around ultra-low-temperature capability associated with quantum and advanced sensing. In the United States, BIS expanded controls (September 2024) to cover certain cryogenic cooling systems and specific pulse-tube configurations under ECCN 3A904, while EU exporters operate under the Union dual-use framework (Regulation (EU) 2021/821). Separately, the U.S. EPA finalized changes under the AIM Act Technology Transitions program (May 2026), with an effective date of July 27, 2026, raising compliance stakes for refrigeration and chiller systems used in industrial processes where cryogenic and sub-ambient cooling architectures intersect.

Value Chain Analysis

The cryocooler value chain starts with specialized upstream inputs, including high-purity gases (including helium for charging and test), precision bearings and compressors, regenerator materials, sensors, and high-integrity metals and brazed assemblies. Midstream manufacturing is concentrated among a small group of specialized OEMs and component suppliers (for example, SHI Cryogenics Group and Lihan Cryogenics), with production typically following an engineer-to-order model that combines thermal and vibration simulation, precision machining, contamination control, and multi-point qualification testing for space, defense, and medical reliability requirements.

Downstream, routes to market vary by application criticality. Defense, space, and quantum-research buyers often procure directly from OEMs or through system integrators (payload houses, dilution refrigerator vendors, and magnet OEMs), while more standardized configurations can move through technical distributors and service networks. Key bottlenecks include ultra-low-vibration integration for sensitive payloads and the helium-3 constraint for sub-kelvin dilution systems, even when cryocoolers handle the 3-4 K precooling stage. This shifts procurement emphasis toward lifecycle services, helium management, and modular field-replaceable architectures.

Competitive Landscape

Market concentration is moderate; the five largest firms capture nearly 55% of revenue, but the offset rules in India and the UAE propel new regional entrants. Sumitomo Heavy Industries, Northrop Grumman, and Bluefors dominate space and quantum applications on the strength of multi-decade heritage and in-orbit records.

Bluefors’ March 2025 merger of Cryomech pulse-tube technology doubled 3 kelvin cooling power, enabling one-stop quantum stacks that lower integration risk for hyperscale data-center buyers. Thales, Ricor, and Honeywell exploit rotary or linear Stirling know-how to win soldier-borne and airborne payloads where low vibration commands premium pricing.

White space exists in sub-5-kilogram systems that require over 8 watts of heat lift at 77 kelvin. Niche vendors such as Absolut System and CryoSpectra pursue cryogenic grinding and electronics cooling, segments that account for less than 5% of revenue but are growing at 15%. Distributed manufacturing trims lead times but raises early-phase costs by 15%, opening room for integrators skilled at localizing without eroding quality. Government procurement, exemplified by Honeywell’s CRUISE and QUEST programs - moves prototypes into production, favoring incumbents with security clearances and flight heritage.

Cryocooler Industry Leaders

Sumitomo Heavy Industries Ltd.

Northrop Grumman Corporation

Cryomech Inc. (Bluefors Oy)

Thales Group

Sunpower Inc. (AMETEK)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is emerging where quantum scale-up meets cryogenic infrastructure needs. Buyers are moving beyond single-lab refrigerators toward multi-system layouts that emphasize compressor packaging, facility integration, and helium management. Actions by cryocooler ecosystem players support this shift, including Bluefors introducing a rack-mountable, air-cooled compressor option for the Cryomech PT205 pulse-tube platform (March 2026) and launching a helium recovery solution aimed at single NMR systems (April 2026), both aligned with operational practicality in lab and pilot production environments.

Space and government science programs also continue to drive demand for higher-capacity, multi-stage cryogenic architectures at 4 K and below. This creates openings for suppliers that can meet flight-heritage reliability targets and integrate with detector and instrument chains. NASA activity provides current evidence of this direction, including activation of the upgraded Cold Atom Lab on the ISS (June 2026) and ongoing publication of 4 K cryocooling architectures for future missions (2026 literature). In parallel, export controls for ultra-low-temperature systems and refrigerant rules for industrial cooling push OEMs toward compliance-ready configurations, documentation, and region-specific supply chains, which supports continued demand for qualified, auditable designs across defense, semiconductor-adjacent, and scientific end uses.

Recent Industry Developments

- April 2026: Bluefors launched the Cryomech HeRL01-RM Helium Reliquefier for direct helium recovery from single NMR systems. The product targets end users seeking to reduce helium consumption and operating disruption, strengthening Bluefors presence around cryogen management adjacent to cryocooler deployments.

- July 2025: Honeywell Aerospace won US Department of Defense production contracts for quantum-sensor navigation under the CRUISE and QUEST programs. The move translates quantum sensing from prototypes into procurement-led production demand, supporting ruggedized cryogenic subsystem supply for defense platforms.

- March 2024: Bluefors and Qblox signed an MoU to co-develop low-dissipation control architectures for high-density quantum processors. The collaboration links electronics heat-load reduction to cryocooler and dilution refrigerator sizing, influencing system-level requirements for sub-4 K precooling in quantum stacks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cryocooler market covers revenue from mechanical cryogenic refrigeration systems that actively generate very low temperatures (typically below about 120 K) to cool sensitive payloads and components across industrial and scientific uses.

Scope exclusions: We exclude passive cryogenic storage equipment, cryogenic liquids, and large-scale liquefaction turbomachinery that are not sold as cryocooler systems.

Segmentation Overview

- By Cryocooler Type

- Stirling

- Gifford-McMahon

- Pulse-Tube

- Joule-Thomson

- Brayton

- By Temperature Range

- 1 K - 20 K

- 20 K - 77 K

- 77 K - 200 K

- Greater Than 200 K

- By Operating Cycle

- Closed-Loop

- Open-Loop

- By Heat-Exchanger Type

- Regenerative

- Recuperative

- By End-User Vertical

- Space

- Healthcare

- Military and Defense

- Commercial and Industrial

- Energy and Power

- Transportation

- Research and Academic

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by pinning down demand signals visible in public data, then mapping them to where cryocoolers are actually used. We referenced sources such as NASA and ESA mission and instrument publications, the US Department of Defense budget documents where cooling hardware is discussed at a program level, US International Trade Commission trade statistics, and peer-reviewed journals that report cooling performance and adoption in lab and field settings.

Alongside official sources, we used company annual reports, investor presentations, and reputable press coverage to understand product positioning and order activity. For data points that are hard to capture from public documents alone, we also used paid subscriptions that compile company financials and track patents, which helped us sanity-check supplier exposure and technology direction. These sources are illustrative and not exhaustive, and many other references were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating where shipments are occurring and how pricing moves by cooling approach and end-use environment. We spoke with a mix of manufacturers, component suppliers, integrators, and informed users across major regions, so assumptions on adoption timing, replacement cycles, and program-driven buying could be corrected before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 17% | APAC: 44% |

| Mid tier: 49% | Functional/Unit leaders: 33% | EMEA: 36% |

| Smaller Players: 18% | Managers: 50% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where visible demand pools were reconstructed from application activity, then converted into value using realistic attach rates and price bands. For cryocoolers, the model leaned on indicators such as satellite and space payload build activity, deployment of superconducting magnets in medical and research settings, procurement cycles in defense sensing, and lab scale-ups tied to quantum and cryogenic test infrastructure.

The totals were then corroborated with selective bottom-up approximations. We sampled supplier revenue exposure, checked typical unit pricing against cooling capacity and operating cycle, and used channel feedback to adjust for integration-heavy deliveries. When a supplier did not disclose a clean cryocooler split, revenue was allocated using product mix cues, patent focus, and interview-based shipment ranges, and then re-checked against the demand-side indicators.

For forecasting, we primarily used scenario analysis supported by trend smoothing on the key drivers, since adoption can swing with mission schedules and program awards. Growth assumptions were stress-tested using variables like build rates, replacement intervals, manufacturing lead times, and expected ASP movement from scale and design simplification, then refined based on expert consensus from the fieldwork.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the market number stays tied to real-world signals rather than a single data stream. We compared results against independent indicators such as publicly visible program pipelines, trade movements where relevant, and technology adoption patterns seen in journals, then investigated variances that did not match the story from interviews.

Before sign-off, the model and assumptions go through a step-by-step analyst review, with re-contact triggers when a large gap shows up in pricing, volumes, or timing. The report is refreshed annually, and interim updates are made when material events shift demand visibility, such as major mission changes, procurement pauses, or sudden capacity additions. Right before delivery, a fresh pass is completed so clients receive the most up-to-date view.

Mordor Intelligence's Cryocooler Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for cryocoolers, even when the same end uses are being discussed. The main reasons are usually the year chosen as the baseline, what gets counted as a cryocooler versus adjacent cryogenic equipment, and how pricing is handled when systems are sold as integrated sub-assemblies.

By tracking application-level demand markers and refreshing scope boundaries, Mordor Intelligence keeps the cryocooler total limited to active mechanical cooling systems below roughly 120 K, instead of mixing in passive cryogenic storage or large liquefaction machinery. Differences also come from whether a study anchors on defense and space program timing versus a smoother industrial growth curve, and whether it applies a single average selling price globally or adjusts ASP by operating cycle and integration depth.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.81 B (2026) | |

| Regional Consultancy A | USD 2.80 B (2024) | Uses an earlier base year and can understate step-changes tied to space and defense procurement cycles, and it is not clear how integrated cooling modules are valued versus full systems. |

| Industry Publisher B | USD 3.00 B (2024) | Likely applies broader product mapping across cryogenic equipment categories, and the pricing logic appears to rely on a single value band rather than cycle-specific ASP and integration-level adjustments. |

Taken together, the spread is largely explained by timing and boundary choices, followed by how ASP is progressed across technology types. Our approach stays repeatable because the market build is tied to observable demand triggers, with cross-checks that prevent adjacent cryogenic hardware from inflating the total.

Key Questions Answered in the Report

How fast is the cryocooler market expected to grow through 2031?

It is forecast to expand at a 13.37% CAGR, moving from USD 2.81 billion in 2026 to USD 5.26 billion by 2031.

Which cryocooler type is gaining ground most quickly?

Pulse-tube machines are projected to grow at 14.87% CAGR because vibration-free operation benefits MRI magnets and quantum processors.

Why is helium-3 availability a concern for quantum-computing projects?

Global supply is only about 8,000 liters per year, limiting annual dilution-refrigerator builds to fewer than 200 systems and adding USD 40,000-100,000 per unit upfront.

Which region will see the fastest revenue growth for cryocoolers?

Asia Pacific is set to post a 14.16% CAGR to 2031 as China and India add cryogen-free MRI suites and fund sovereign quantum programs.

What share did healthcare hold in 2025?

Healthcare accounted for 27.38% of revenue, driven by expansion of helium-free MRI systems in tier-2 city hospitals.

How are defense offsets reshaping the supplier landscape?

Policies in India and the UAE force foreign primes to transfer Stirling technology locally, shortening lead times but raising early-phase costs by roughly 15%.

Page last updated on: