Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

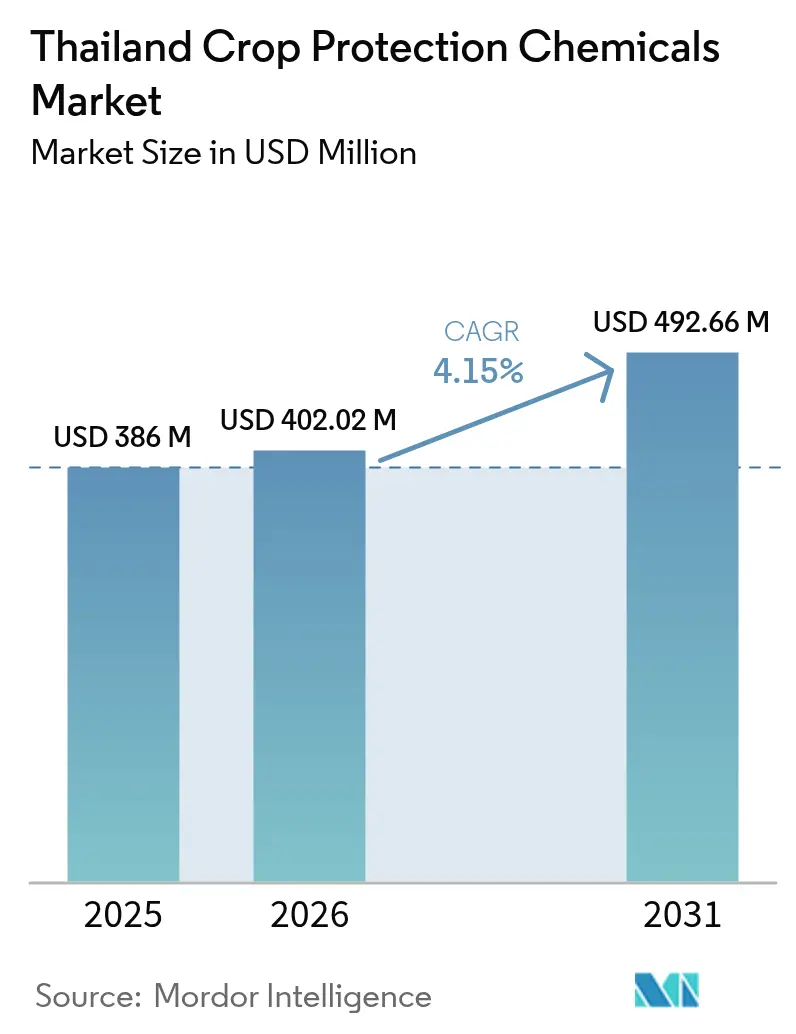

| Base Year Market Size (2025) | USD 386 Million |

| Market Size (2026) | USD 402.02 Million |

| Market Size (2031) | USD 492.66 Million |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Crop Protection Chemicals Market Analysis by Mordor Intelligence

The Thailand crop protection chemicals market size was valued at USD 386 million in 2025 and estimated to grow from USD 402.02 million in 2026 to reach USD 492.66 million by 2031, at a CAGR of 4.15% during the forecast period (2026-2031). Rising pest pressure in rice, accelerating bans on paraquat and chlorpyrifos, and the government’s precision-agriculture subsidies are reshaping input choices across the farming sector. Momentum is building for biological alternatives as exporters seek residue-free certification for durian, mango, and other premium fruit. Digital farm-input marketplaces and variable-rate sprayer programs are narrowing access gaps for smallholders while improving application accuracy. Meanwhile, the regulatory environment rewards companies able to deliver proven efficacy, strong stewardship, and data-driven product recommendations. Key market risks include seasonal labor migration patterns that disrupt optimal application timing, rising organic farming adoption in northern provinces that reduces chemical demand, and potential trade disruptions from pesticide residue concerns in key export markets like China.

Key Report Takeaways

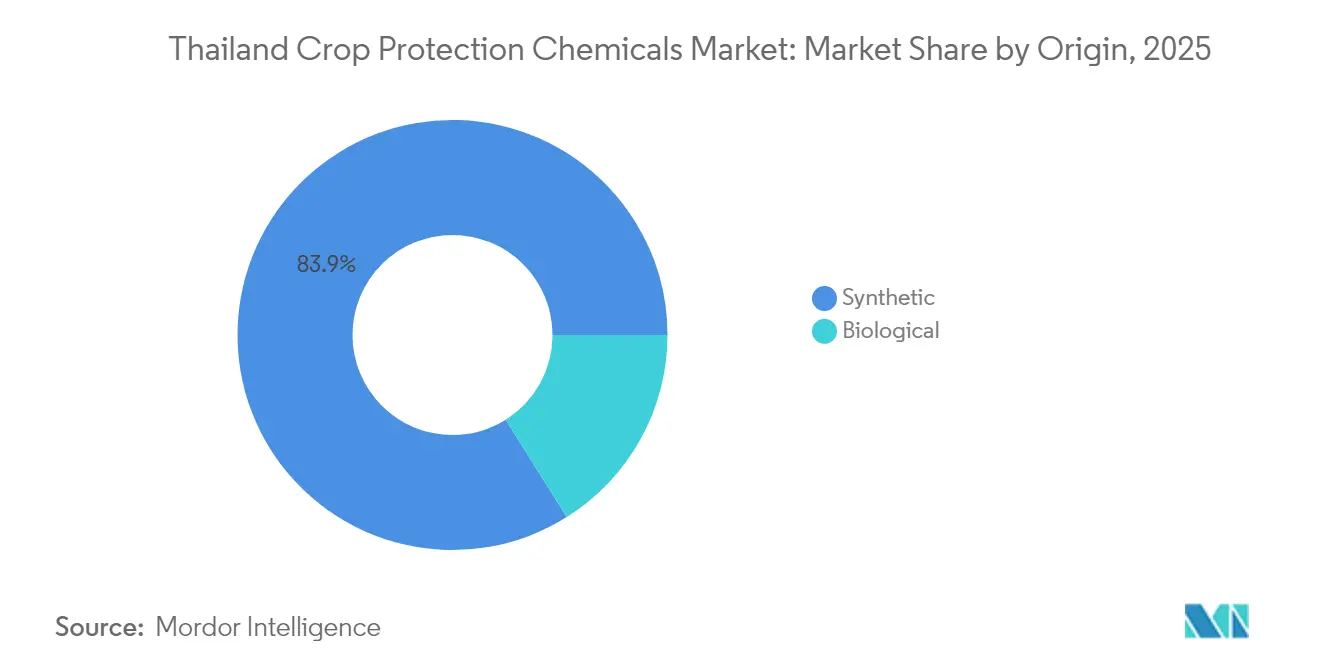

- By origin, synthetic led with 83.92% of the Thailand crop protection chemicals market share in 2025, while biologicals are advancing at a 9.49% CAGR through 2031.

- By product, herbicides led with 44.32% of the Thailand crop protection chemicals market share in 2025, while bio-pesticides are projected to advance at a 11.03% CAGR through 2031.

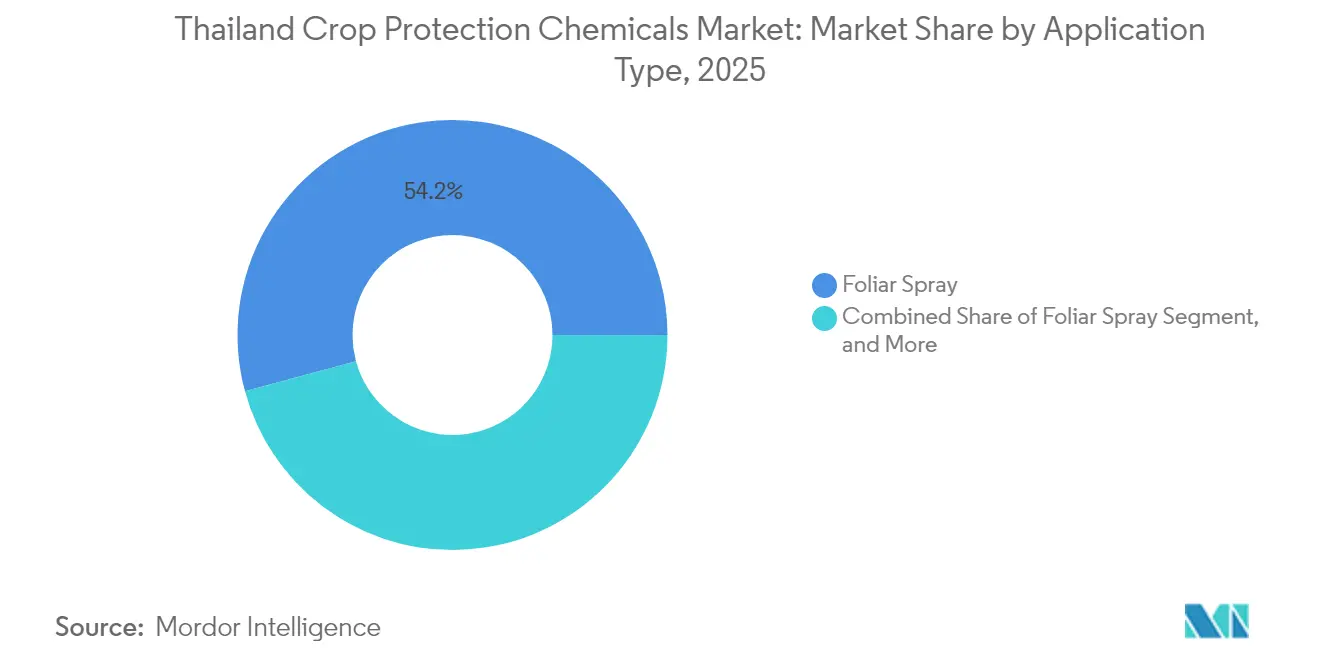

- By application method, foliar spray accounted for a 54.21% of the Thailand crop protection chemicals market size in 2025, and seed treatment is growing at a 9.07% CAGR through 2031.

- By crop, grains and cereals contributed 40.35% of the Thailand crop protection chemicals market share in 2025, whereas fruits and vegetables are expanding at an 8.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying rice blast outbreaks in the Central Plains | +0.8% | The Central Plains provinces, spillover to the northeastern rice areas | Medium term (2-4 years) |

| Government subsidies for precision-sprayer adoption | +0.6% | National, with early gains in the Chao Phraya River Basin | Short term (≤ 2 years) |

| Expansion of contract-farming fruit exports | +0.5% | Southern provinces (Chumphon, Chanthaburi), eastern regions | Long term (≥ 4 years) |

| Rapid growth of sugarcane ratoon herbicide programs | +0.4% | Northeastern Thailand, the central sugarcane belt | Medium term (2-4 years) |

| Surge in e-commerce ag-input platforms among smallholders | +0.3% | National, concentrated in digitally connected rural areas | Long term (≥ 4 years) |

| Biocontrol partnerships with royal research projects | +0.2% | Northern highlands, Royal Project areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying rice blast outbreaks in the Central Plains

Disease severity has reached 27.85% in untreated plots, compelling growers to increase fungicide spray frequency. Tricyclazole-based programs raise yields by up to 3.93 metric ton/ha, helping sustain profitability despite tighter margins[1]Source: Nattapatphon Kongcharoen, “Efficacy of Fungicides in Controlling Rice Blast,” nature.com. Wetter La Niña patterns forecast through 2025 bolster inoculum pressure across the core rice belt. Close monitoring and timely applications, therefore, underpin demand stability for high-efficacy fungicides within the Thailand crop protection chemicals market. Climate variability associated with La Niña conditions is anticipated to intensify disease pressure through 2025, with increased rainfall creating favorable conditions for pathogen proliferation across major rice-growing regions.

Government subsidies for precision-sprayer adoption

The Ministry of Agriculture covers up to 40% of the cost of Global Positioning System (GPS)-enabled boom sprayers, distributing starter kits to smallholders in 26 provinces along the Chao Phraya River Basin. These starter kits include advanced application equipment and personal protective gear. Demonstrations show a 98.23% reduction in operator exposure and a 15% savings in active ingredients. These incentives strengthen the adoption of modern delivery technologies that optimize chemical volumes and compliance with re-entry intervals. The initiative aligns with broader digitalization objectives that integrate precision agriculture with sustainable farming practices. Regulatory compliance requirements under the Department of Agriculture's safety protocols further incentivize the adoption of advanced application technologies that minimize environmental exposure risks.

Expansion of contract-farming fruit exports

Durian output is forecast to touch 1.68 million metric tons in 2025, a 30.72% rise over 2024, underpinning spray programs designed to meet China’s stringent residue limits[2]Source: The Nation, “Thailand’s Fruit Yields Up in 2025,” fftc.org.tw. Contract farming models provide farmers with technical support and guaranteed procurement, reducing market risks while ensuring compliance with international phytosanitary requirements. The Royal Project Foundation's success in highland fruit production, involving 3,000 families across 37 extension stations, demonstrates the scalability of contract farming approaches that integrate sustainable pest management practices. Export quality premiums create economic incentives for precision chemical application that balance pest control efficacy with residue minimization objectives.

Rapid growth of sugarcane ratoon herbicide programs

After paraquat restrictions, growers are trialing ametryn, s-metolachlor, and mechanical row weeding to curb perennial grasses. Field tests demonstrate 12% yield gains when ratoons receive two post-emergence herbicide passes versus single-pass traditional practice. Rising mechanization and the drive to end pre-harvest burning sustain herbicide demand in cane belts. Government initiatives to eliminate sugarcane burning practices have intensified reliance on chemical weed control methods as farmers transition from traditional field preparation techniques.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Hazardous Substance Act restrictions on paraquat and chlorpyrifos | -1.2% | National, with acute impacts in rice and sugarcane regions | Short term (≤ 2 years) |

| Rising organic rice acreage in northern provinces | -0.6% | Northern Thailand (Chiang Rai, Chiang Mai), expanding southward | Medium term (2-4 years) |

| Seasonal labor migration limiting timely pesticide application | -0.4% | Rural agricultural areas, concentrated in northeastern provinces | Medium term (2-4 years) |

| Consumer backlash against chemical residues in durian exports | -0.3% | Southern fruit-growing provinces, export-oriented operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Hazardous Substance Act restrictions on paraquat and chlorpyrifos

On-farm inventories worth THB 10 billion (USD 307.7 million) were written off after the 2020 ban. Alternative chemistries command premium pricing while often delivering inferior efficacy against target pests, creating economic pressure on farmers who face yield penalties without access to previously relied-upon active ingredients. The ban's enforcement has been complicated by black market distribution channels that continue to supply prohibited substances, undermining regulatory objectives while creating unfair competitive advantages for non-compliant operatorsSubstitute chemistries carry premium pricing and sometimes lower efficacy, pressuring margins within the Thailand crop protection chemicals market.

Rising organic rice acreage in northern provinces

Certified area in Chiang Rai and Chiang Mai reached 135,410 ha in 2024, equating to 0.2% of national farmland but signaling wider consumer shifts. Organic growers eliminate synthetic pesticides, directly trimming addressable demand. Organic certification requirements prohibit synthetic pesticide use, directly reducing market demand in converted areas while potentially influencing neighboring conventional operations through peer effects. The Chiang Rai Green Network's advocacy for food safety and environmental protection has gained political support that could accelerate organic conversion rates beyond current projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Origin: Biological Solutions Accelerate Despite Synthetic Dominance

Synthetic formulations controlled 83.92% of the Thailand crop protection chemicals market share in 2025, underscoring farmer reliance on proven active ingredients that deliver consistent results under high pest pressure. Biologicals, though starting from a small base, are advancing at a 9.49% CAGR through 2031, making them the fastest-growing slice of the Thailand crop protection chemicals market as exporters demand residue-compliant solutions for durian, mango, and longan. Cost remains a pivotal advantage for synthetics because large-scale manufacturing spreads fixed costs and keeps per-liter prices attractive to smallholders. The embedded dealer network that offers seasonal credit further locks many farmers into legacy products that require no new application training.

Regulatory shifts are changing the calculus. Department of Agriculture extension services now distribute Bacillus thuringiensis and Trichoderma powders at subsidized rates, signaling state backing for eco-friendly modes of action. Multinationals have responded by striking technology alliances. As stewardship programs emphasize integrated pest management, growers are likely to blend lower-dose synthetics with targeted biologicals, gradually reshaping the chemical mix without eroding the efficacy safeguards that intensive Thai agriculture still requires.

By Product: Bio-pesticides Gain Momentum under Regulatory Pressure

Herbicides held 44.32% of the Thailand crop protection chemicals market share in 2025, reflecting the weed-control needs of rice and cane systems. In contrast, bio-pesticides are growing at an 11.03% CAGR, bolstered by government support for Bacillus thuringiensis and pheromone-based products. Multinationals and local start-ups alike ramp up R&D spending to capture this opportunity. The Thailand crop protection chemicals market size allocated to insecticides remains resilient as armyworm incursions persist, while fungicides expand modestly on escalating rice blast prevalence.

Molluscicides and nematicides remain niche but benefit from intensifying root-knot nematode outbreaks documented in central paddies. Adoption barriers for biologicals' short shelf life, higher per-hectare cost are easing as field trials verify yield parity with synthetics. Syngenta’s pheromone partnership targets nationwide commercial roll-out by 2026. Portfolio diversification protects growers from compliance risks and supports integrated pest-management strategies across the Thailand crop protection chemicals market.

By Application Method: Seed Treatment Rises with Precision Agriculture

Foliar sprays represented 54.21% of 2025 demand due to entrenched farmer practice and accessible knapsack sprayers. Seed treatment, however, is posting 9.07% CAGR as coated rice and maize seed becomes a cost-effective delivery route for systemic actives that reduce operator exposure. Soil treatment and chemigation occupy niche roles in protected cultivation, while fumigation addresses post-harvest insect management.

Government subsidies for GPS-guided booms and variable-rate tech optimize droplet deposition, cutting wastage by up to 15% per hectare. These gains enhance stewardship credentials and align with residue-compliance mandates, cementing modern delivery methods in the Thailand crop protection chemicals market. Chemigation systems benefit from irrigation infrastructure expansion but face adoption barriers related to equipment costs and technical complexity. Fumigation applications remain limited to specific pest scenarios and controlled environment agriculture.

By Crop: Fruit and Vegetable Segment Outpaces Traditional Staples

Grains and cereals commanded 40.35% of the Thailand crop protection chemicals market size in 2025, due to rice’s dominance. Yet fruits and vegetables are accelerating at an 8.42% CAGR through 2031, propelled by expanding durian, mango, and longan orchards geared to Chinese demand. Export premiums incentivize residue-compliant spray programs and push biological adoption. Meanwhile, sugarcane and cassava use stable herbicide volumes, while pulses, oilseeds, and ornamental crops remain small but rising as diversification initiatives gather pace.

Fruit acreage growth clusters in Chanthaburi and Chumphon, where contract schemes guarantee farmers technical advice and purchase. Precision nutrient and pest programs help command higher grades, reinforcing demand diversity within the Thailand crop protection chemicals market. Pulses and oilseeds occupy smaller market shares but benefit from government diversification initiatives that promote crop rotation and soil health improvement. Ornamental and turf applications remain niche markets with specialized product requirements and premium pricing structures.

Geography Analysis

The Central Plains dominate demand due to intensive double-cropped rice. Here, fungicide applications rise as blast and bacterial leaf blight intensify under wetter cycles. Northeastern provinces, home to mechanized cane estates, consume high herbicide volumes, especially post-ratoon. Adoption of paraquat substitutes is fastest here as regulatory enforcement tightens.

The Northern highlands demonstrate sustainable agricultural practices through Royal Project farms that incorporate biological products into high-value vegetable production. While synthetic pesticide use decreases in this region, premium bio-pesticides show increased adoption. The Southern fruit-growing regions generate demand for specialty crop protection chemicals due to export requirements. In 2024, product rejections led to increased adoption of low-residue pesticides and enhanced monitoring services, establishing quality-focused application practices in Thailand's crop protection chemicals market.

Proximity to Bangkok and Laem Chabang ports facilitates the rapid distribution of imported active ingredients. Coastal areas face unique challenges from pest pressure and environmental conditions that require adapted chemical solutions, while proximity to major ports facilitates access to imported active ingredients and export market feedback. Government initiatives supporting contract farming arrangements in southern provinces create structured demand for crop protection chemicals that balance efficacy with residue minimization objectives, reflecting the region's integration with global value chains that demand consistent quality standards.

Competitive Landscape

Multinationals Bayer AG, BASF SE, Syngenta Group, Corteva Inc., and FMC Corporation command leadership through broad portfolios and deep stewardship resources. Some other suppliers, such as UPL Ltd. and Sumitomo, compete through cost competitiveness and localized mixtures. Biological specialists partner with established distributors to scale market entry, while sprayer manufacturers embed advisory software to capture downstream value. The Department of Agriculture's oversight of product registration and quality standards ensures market access for compliant players while creating competitive moats for established participants with regulatory expertise and government relationships.

Strategic moves center on biological acquisitions, precision application alliances, and residue testing services. Syngenta’s 2024 pheromone tie-up illustrates focus on disruptive modes of action. BASF SE’s announcement of six new actives slated for Asia by 2028 underscores its ongoing commitment to chemistry innovation. Local formulators utilize e-commerce portals to connect directly with smallholders, thereby bypassing traditional retail channels.

Emerging disruptors include biological control specialists and digital agriculture platforms that bypass traditional distribution channels through direct farmer engagement and technical service integration. Technology adoption patterns favor companies that combine chemical expertise with digital delivery systems, exemplified by precision sprayer subsidy programs that create competitive advantages for equipment-integrated solution providers. Regulatory compliance under the Hazardous Substances Act creates barriers to entry while rewarding companies with robust product stewardship capabilities and alternative chemistry portfolios.

Thailand Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

Corteva Inc.

UPL Ltd.

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thailand’s Office of Agricultural Economics projected durian volume to hit 1.68 million metric tons, prompting exporters to tighten pest-management protocols.

- September 2024: Syngenta Biologicals partnered with Provivi on pheromone solutions targeting rice stem borer and fall armyworm, with commercialization planned in 2026.

- August 2024: Bayer AG and UPL Ltd. expanded biological pipelines, unveiling more than 20 product launches aligned with regenerative farming goals.

Thailand Crop Protection Chemicals Market Report Scope

Crop protection chemicals are a class of agrochemicals used to prevent the destruction of crops by insect pests, diseases, weeds, and other pests. The Thai crop protection chemicals market is segmented by product (herbicides, insecticides, fungicides, molluscicide, and nematicide), crop (commercial crops, fruits and vegetables, grains and cereals, pulses and oil seeds, and turf and ornamental crops), and application (chemigation, foliar, fumigation, seed treatment, and soil treatment). The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Chemical Type

| Synthetic |

| Biological |

By Product

| Herbicides |

| Insecticides |

| Fungicides |

| Molluscicides |

| Nematicides |

| Bio-pesticides |

By Application Method

| Foliar Spray |

| Seed Treatment |

| Soil Treatment |

| Chemigation |

| Fumigation |

By Crop

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oil seeds |

| Ornamental and Turf |

| By Chemical Type | Synthetic |

| Biological | |

| By Product | Herbicides |

| Insecticides | |

| Fungicides | |

| Molluscicides | |

| Nematicides | |

| Bio-pesticides | |

| By Application Method | Foliar Spray |

| Seed Treatment | |

| Soil Treatment | |

| Chemigation | |

| Fumigation | |

| By Crop | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oil seeds | |

| Ornamental and Turf |

Key Questions Answered in the Report

What is the value of the Thailand crop protection chemicals market in 2026?

The Thailand crop protection chemicals market size stands at USD 402.02 million in 2026.

Which segment is expanding fastest by product type?

Bio-pesticides are growing at an 11.03% CAGR through 2031, outpacing other product categories.

How did the paraquat and chlorpyrifos ban affect growers?

The ban removed cost-effective broad-spectrum options, forcing a switch to pricier alternatives and prompting inventory write-offs worth THB 10 billion (USD 307.7 million).

Why is seed treatment gaining traction?

Precision-agriculture programs and safety regulations favor seed coatings that reduce operator exposure while ensuring systemic protection.

Which crop drives future demand growth?

Fruits and vegetables, led by durian expansion, are anticipated to post the highest CAGR at 8.42% to 2031, lifting demand for residue-compliant solutions.

Page last updated on: