Induced Pluripotent Stem Cells Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 4.14 Billion |

| Growth Rate (2026 - 2031) | 9.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Induced Pluripotent Stem Cells Market Analysis by Mordor Intelligence

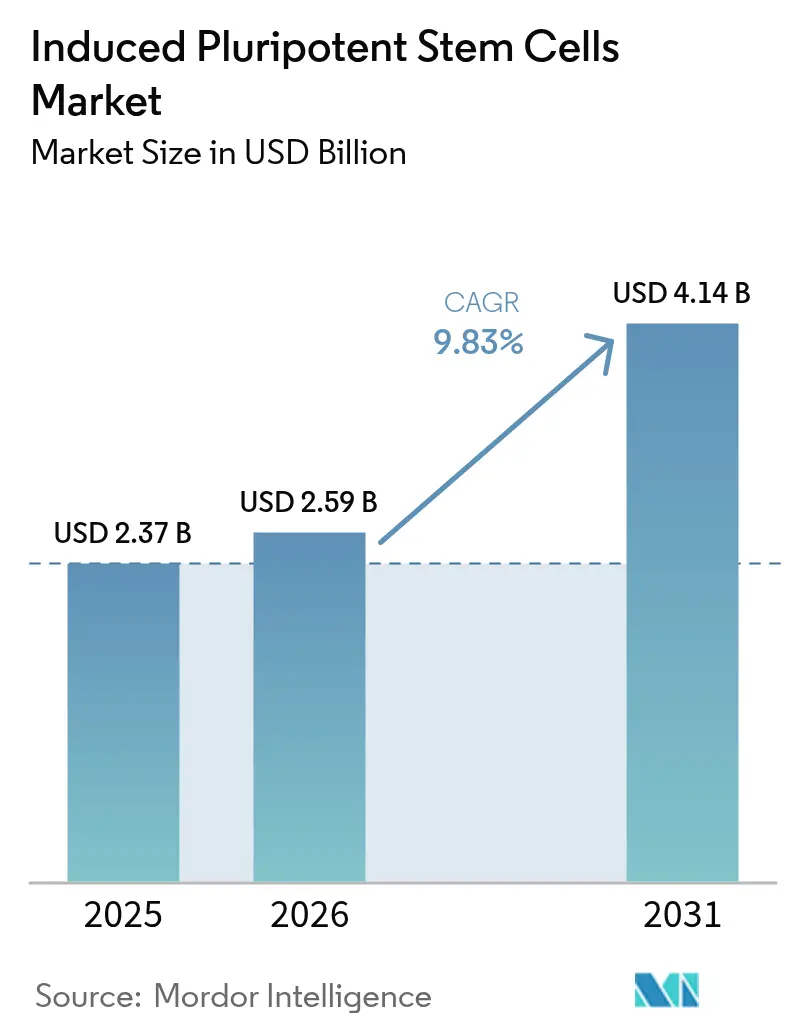

The Induced Pluripotent Stem Cells Market size is projected to expand from USD 2.37 billion in 2025 and USD 2.59 billion in 2026 to USD 4.14 billion by 2031, registering a CAGR of 9.83% between 2026 to 2031.

Consistent adoption of iPSC-enabled cardiotoxicity screens, robust Phase II-ready cell-therapy pipelines, and concerted public funding across the United States, Japan, and the European Union are driving double-digit growth in the induced pluripotent stem cells market. Pharmaceutical and biotechnology companies already command 58.46% of 2025 revenue as they pivot toward patient-specific toxicity models that lower late-stage attrition by as much as 30 percentage points. Rapid automation with closed-system bioreactors is compressing per-batch costs from USD 50,000 to USD 15,000 and widening access for mid-sized sponsors. Meanwhile, regulatory fast tracks in Japan and China shorten commercial timelines for iPSC-derived therapies, encouraging cross-border licensing deals that reinforce momentum in the induced pluripotent stem cells market.

Key Report Takeaways

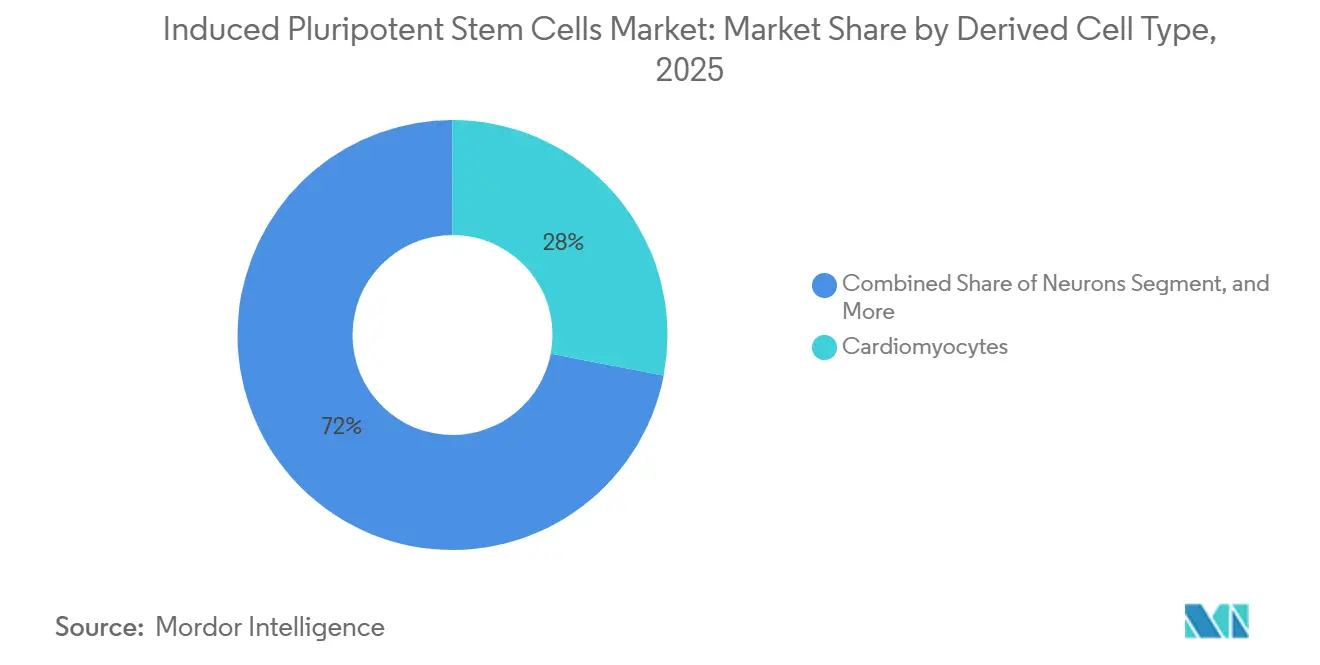

- By derived cell type, cardiomyocytes led with 28.02% revenue share in 2025, while neurons are projected to register a 10.06% CAGR through 2031.

- By application, drug discovery and development accounted for 39.67% of 2025 revenue; regenerative medicine is forecast to grow at an 11.63% CAGR through 2031.

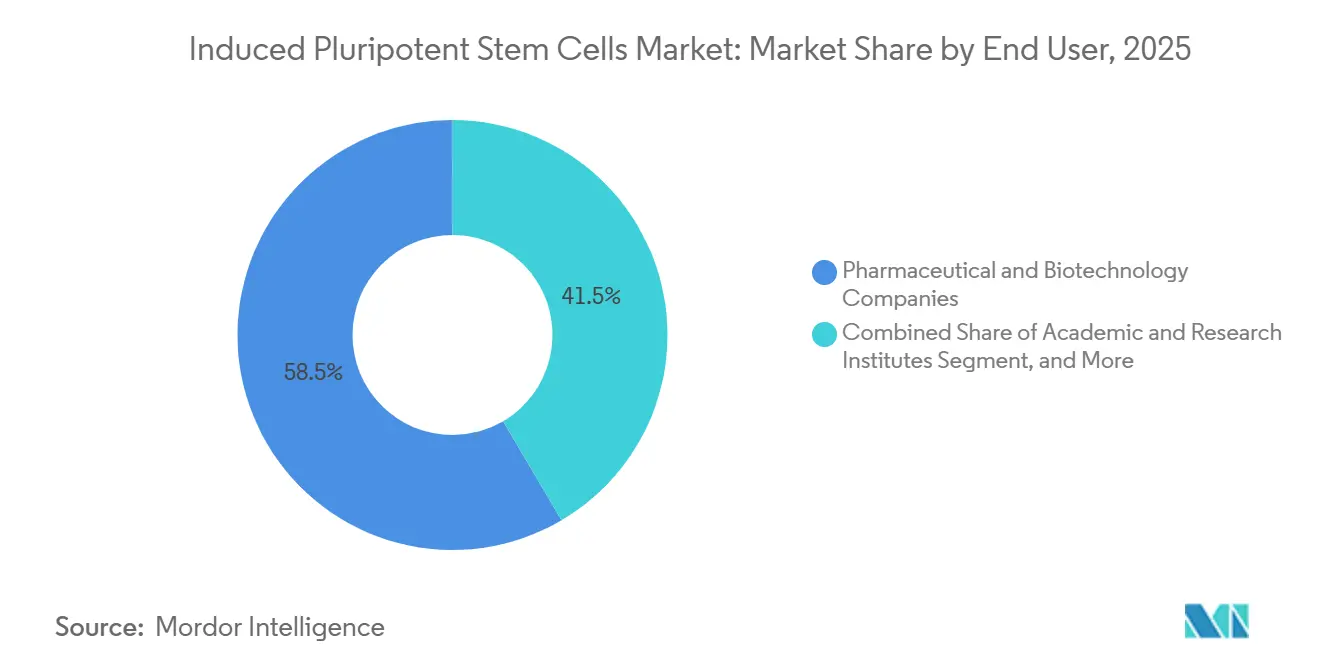

- By end user, pharmaceutical and biotechnology companies held 58.46% of the induced pluripotent stem cells market share in 2025, whereas academic and research institutes are expanding at a 12.18% CAGR over 2026-2031.

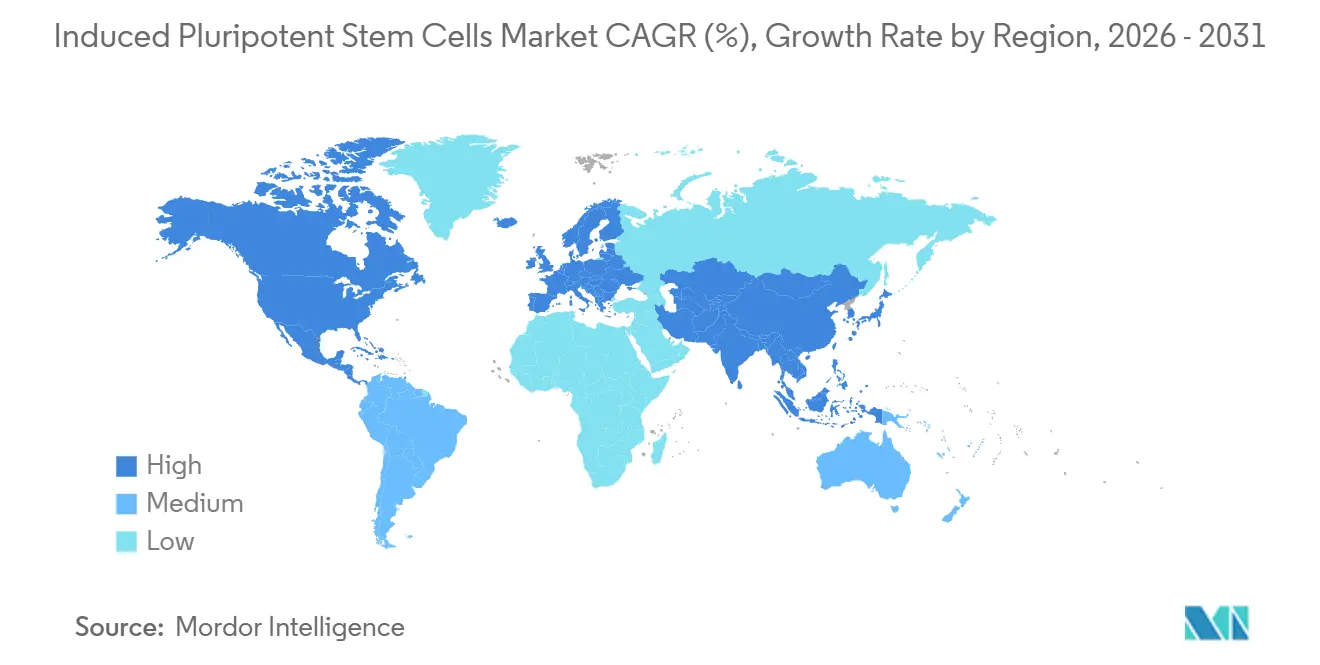

- By geography, North America dominated with a 38.91% share in 2025, yet Asia-Pacific is pacing the field with an 11.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Induced Pluripotent Stem Cells Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in iPSC-enabled drug discovery and toxicity testing demand | +2.1% | North America, Europe | Medium term (2-4 years) |

| Expanding clinical pipeline of iPSC-derived cell therapies | +1.8% | Japan, North America, Europe | Long term (≥ 4 years) |

| Robust public and private funding across U.S., EU, and Japan | +1.5% | North America, Europe, Japan | Short term (≤ 2 years) |

| Advances in non-integrating reprogramming and CRISPR editing | +1.3% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Adoption of closed-system automated GMP bioreactors | +1.2% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Emerging industrial uses (cultured meat, iPSC-platelets) | +0.9% | Israel, Japan, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in iPSC-Enabled Drug Discovery and Toxicity Testing Demand

Pharmaceutical sponsors are switching from animal models to iPSC-derived cardiomyocytes and hepatocytes that flag human-specific toxicities, cutting Phase II failure rates by up to 35 percentage points.[1]U.S. Food and Drug Administration, “Cellular and Gene Therapy Products,” fda.gov FUJIFILM Cellular Dynamics showed that iCell hepatocytes detected hidden liver liabilities in eight compounds that had cleared rodent screens, leading FDA reviewers to accept iPSC data in investigational new drug files in 2024. Takeda integrated these assays into 40% of its early pipeline by 2025, trimming preclinical timelines by six months and saving roughly USD 30 million per asset. Contract research organizations such as Charles River and Eurofins now charge USD 4,500 per compound for full iPSC toxicity panels, less than half the 2023 rate, broadening adoption among small biotechs. Growing regulatory acceptance under the U.S. 21st Century Cures Act and the EU’s 3Rs principles further institutionalizes the practice.

Expanding Clinical Pipeline of iPSC-Derived Cell Therapies

Seventeen iPSC-based therapeutics were in Phase I or II worldwide by mid-2025, led by BlueRock Therapeutics’ bemdaneprocel for Parkinson’s disease, which delivered a 40% improvement on the Unified Parkinson’s Disease Rating Scale at twelve months. Heartseed’s HS-001 cardiac patch posted a 15% rise in left ventricular ejection fraction without serious adverse events, advancing toward Japan’s conditional approval pathway that can cut three years from a typical launch schedule.[2]Heartseed, “HS-001 Interim Results,” heartseed.jp Fate Therapeutics’ FT596 off-the-shelf CAR-NK cells achieved 60% complete responses in B-cell lymphoma, outperforming autologous CAR-T benchmarks by 15 points. Century Therapeutics secured FDA clearance for CNTY-101 gamma-delta T cells for solid tumors, expanding the addressable oncology base. Collectively, these milestones sustain investor confidence in the induced pluripotent stem cells market.

Robust Public and Private Funding Across U.S., EU, and Japan

The U.S. National Institutes of Health raised its iPSC allocation to USD 450 million for fiscal 2025, targeting Alzheimer’s and diabetes programs. California’s CIRM added USD 310 million that same year, backing twelve clinical studies spanning spinal cord injury to retinal degeneration. Europe’s Horizon Europe committed EUR 280 million (USD 305 million) to multicenter consortia led by Fraunhofer and Institut Pasteur.[3]European Medicines Agency, “3Rs Initiative,” ema.europa.eu Japan’s budget rose to JPY 85 billion (USD 580 million) in 2025 to expand the national HLA-matched iPSC bank now covering 90% of the population. Venture investors added USD 1.8 billion during 2024-2025, underscoring durable capital flows into the induced pluripotent stem cells market.

Advances in Non-Integrating Reprogramming and CRISPR Editing

Sendai virus, episomal vectors, and synthetic mRNA now deliver reprogramming efficiencies above 80% while slashing insertional mutagenesis risks to below 5%. Thermo Fisher’s CytoTune 2.0 kit halves turnaround time to fourteen days and is used by 60% of academic labs worldwide. In 2024, Axol Bioscience supplied 50 isogenic iPSC lines carrying defined pathogenic variants to Vertex and CRISPR Therapeutics for precision target validation. Prime editing studies in 2025 corrected Duchenne muscular dystrophy mutations with 95% on-target accuracy and no detectable off-targets. Takara Bio’s GeneArt service now delivers custom knockouts in 4 weeks at USD 8,000 per line, a 2/3 cost reduction versus 2023.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and process complexity for large-scale GMP production | -1.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Fragmented global regulatory and standardization requirements | -1.2% | Global, with divergence between FDA, EMA, PMDA | Long term (≥ 4 years) |

| Genetic instability and tumorigenicity safety concerns | -1.0% | Global, with stringent oversight in North America and Europe | Medium term (2-4 years) |

| Concentrated patent ownership driving royalty pressure | -0.7% | Global, particularly affecting small biotechs and academic spin-outs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost and Process Complexity for Large-Scale GMP Production

ISO 13485 facilities, 30-day differentiation runs, and whole-genome release testing push batch costs to as high as USD 150,000, pricing many academic spin-outs out of the market. Media costs often exceed USD 2,000 per liter, and yield variability can reach 50%, hampering the reliable cost of goods. CDMOs charge up to USD 5 million for Phase I clinical material, a hurdle for seed-stage ventures. Cryopreservation losses of 30% force manufacturers to oversize production runs, inflating inventory overhead. Although automation cuts labor by 80%, setting up a 500-liter GMP suite still requires more than USD 10 million in capital, delaying scale-out in the induced pluripotent stem cells market.

Fragmented Global Regulatory and Standardization Requirements

FDA demands whole-genome sequencing, 12-month biodistribution, and tumorigenicity assays, extending development timelines by up to two years and adding USD 10 million in extra studies. EMA rules vary by member state; Germany mandates functional testing across three animal models, whereas France accepts in vitro surrogates, complicating multicountry trial logistics. Japan’s conditional pathway allows earlier launch but restricts prescribing to designated hospitals and requires decade-long surveillance, limiting first-wave volumes. China’s NMPA insists on domestic manufacture, forcing foreign sponsors to duplicate GMP capacity at up to USD 50 million per site. Consensus on potency assays is at least three years away despite ISSCR and ISO efforts, prolonging uncertainty within the induced pluripotent stem cells market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Derived Cell Type: Cardiomyocytes Sustain Leadership While Neurons Gain Momentum

Cardiomyocytes accounted for 28.02% of the induced pluripotent stem cells market share in 2025, supported by pharmaceutical use in cardiotoxicity screening and by regenerative medicine trials such as Heartseed’s HS-001 patch. Parallel progress in ventricular-patch trials could open therapeutic revenue streams as early as 2027.

Neurons remain the fastest-growing sub-segment at a forecast 10.06% CAGR. Pharmaceutical interest in Parkinson’s and ALS models, combined with academic consortia scaling patient-derived lines, underpins sustained demand. BlueRock’s Phase II data and Axol’s 50-line isogenic panel validate commercial potential beyond research reagents. Growing neurodegenerative disease burden reinforces the long-run contribution of neurons to the induced pluripotent stem cells market.

By Application: Drug Discovery Dominates as Regenerative Medicine Accelerates

Drug discovery and development commanded 39.67% revenue in 2025, driven by broad adoption of iPSC toxicity panels across large pharma portfolios. The induced pluripotent stem cells market size for drug discovery is projected to reach USD 1.8 billion by 2031. Falling assay prices and regulatory alignment keep barriers low for emerging biotechs.

Regenerative medicine logs the highest growth at an 11.63% CAGR to 2031, catalyzed by multiple Phase II cell therapies and Japan’s early commercialization pathway. Heartseed’s cardiac patch and Fate’s CAR-NK will be first movers, but mesenchymal products and iPSC-platelets are close behind. The rising tide extends to tissue-engineering constructs, which broaden clinical categories and enlarge the induced pluripotent stem cells market.

By End User: Pharma Retains Primacy While Academia Scales

Pharmaceutical and biotechnology companies accounted for 58.46% of 2025 revenue, purchasing bulk iPSC-derived cells for both screening and clinical applications. However, academic and research institutes are posting the fastest growth, with a 12.18% CAGR, as universities deploy automated bioreactors that trim per-batch costs by 70%. This democratization diversifies demand sources and stabilizes long-term unit volumes within the induced pluripotent stem cells market.

The contract research organizations segment's growth is driven by bundling iPSC assays with legacy in-vivo services, giving small sponsors a turnkey path to regulatory-grade data. Hospitals in Japan form an emerging purchaser class under PMDA’s conditional rules, illustrating how policy design can reshape downstream demand.

Geography Analysis

North America contributed 38.91% of 2025 turnover, reflecting FDA clarity, NIH and CIRM grant programs, and a dense venture-capital ecosystem. Canada’s STEMCELL Technologies supplies culture media to 70% of academic users worldwide, reinforcing the region’s critical input position. Mexico’s new Lonza facility signals movement of contract manufacturing into cost-advantaged locales.

Asia-Pacific is projected to grow at 11.67% CAGR through 2031, the fastest among all regions. Japan’s conditional approval pathway shortens launch timelines by up to five years, drawing global companies to partner or relocate trials. China’s USD 1.2 billion provincial funds and WuXi bioreactor build-out create the largest single new manufacturing corridor for the induced pluripotent stem cells market. India, South Korea, and Australia collectively add momentum through coordinated government grants and translational trials.

Germany, France, and the United Kingdom dominate clinical trial counts, while harmonized MHRA guidance in 2024 streamlined cross-border submissions. Israel and Brazil spearhead Middle East & Africa and South America adoption respectively, lifting those combined regions to an 8% contribution and illustrating global diffusion of the induced pluripotent stem cells market.

Competitive Landscape

Vertical integration enables FUJIFILM to deliver 10 billion cardiomyocytes per quarter, while Thermo Fisher and Lonza lock institutions into long-term reagent-plus-automation contracts. Patent royalties on foundational reprogramming IP, largely owned by Kyoto University and CIRM, impose 8-12% revenue tolls on downstream product developers, reinforcing incumbent advantage.

Fate Therapeutics and Century Therapeutics illustrate emerging competition in immune-cell therapies that bypass the cost and time hurdles of autologous CAR-Ts. Hitachi’s AI-optimized bioreactor is a technological challenger that could erode Lonza’s dominance in Asia. Cellino Biotech’s laser-enabled single-cell cloning targets genetic drift issues that constrain scalability, signalling ongoing innovation pressure in the induced pluripotent stem cells industry.

Cultured-meat entrants, platelet suppliers, and industrial platelets diversify the buyer set, attracting non-pharma capital and lowering reliance on therapeutic applications alone. This widening user base underpins durable volume expansion even as clinical timelines fluctuate, securing the long-run relevance of the induced pluripotent stem cells market.

Induced Pluripotent Stem Cells Industry Leaders

Axol Bioscience Ltd.

Evotec SE

FUJIFILM Cellular Dynamics, Inc.

Ncardia BV

Cynata Therapeutics Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Pluristyx and Teknova launched the PluriFreeze cryopreservation system to improve iPSC storage and shipping efficiency.

- June 2024: FUJIFILM presented expanded iPSC technology offerings at the BIO International Convention, highlighting scale-up readiness.

- May 2024: Cambridge Bioscience partnered with Axol Bioscience to distribute specialized iPSC-derived cell products across the UK and Ireland.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the induced pluripotent stem cells (iPSC) market as the value generated from products, services, and enabling technologies that reprogram adult somatic cells to a pluripotent state and subsequently differentiate them into lineage-specific cells for research, screening, and therapeutic use. According to Mordor Intelligence, figures include revenues from cell lines, culture media, reprogramming kits, downstream analytical tools, and fee-based manufacturing services purchased by laboratories, biopharma firms, and academic centers worldwide.

Scope exclusion: Embryonic, adult, and hematopoietic stem cell products that do not pass through an iPSC reprogramming step are excluded.

Segmentation Overview

- By Derived Cell Type

- Cardiomyocytes

- Neurons

- Hepatocytes

- Fibroblasts

- Keratinocytes

- Other Cell Types

- By Application

- Drug Discovery and Development

- Disease Modeling

- Toxicity Testing

- Regenerative Medicine

- Cell Therapy

- Tissue Engineering

- Other Applications

- By End User

- Academic and Research Institutes

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations

- Hospitals and Specialty Clinics

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview GMP cell-manufacturing directors, academic PIs, supply-chain managers, and regulatory advisors across North America, Europe, and Asia-Pacific. These conversations test price points for clinical-grade batches, typical success rates in reprogramming, and adoption intentions so that we refine desk findings and close data gaps before final triangulation.

Desk Research

We begin with a structured sweep of open datasets such as US NIH RePORTER grant logs, FDA RMAT designations, European Medicines Agency ATMP registers, OECD R&D spending tables, and clinical-trial postings that track iPSC pipelines. Statistical yearbooks from the World Health Organization, customs trade codes for pluripotent stem cell reagents, and publications in PubMed and Nature Biotechnology complement the view. Commercial signals are drawn from company 10-Ks, investor decks, and D&B Hoovers subscriber feeds (for revenue splits), while Dow Jones Factiva screens business news for investment rounds and acquisitions. This source list is illustrative, not exhaustive, as many additional references guide data checks.

Market-Sizing & Forecasting

A top-down construct links national biomedical R&D outlays and translational grant pools to estimated iPSC demand pools, followed by adjustment through sampled average selling price times volume data from supplier interviews. Bottom-up cross-checks include roll-ups of publicly reported reagent sales, contract manufacturing capacity utilization, and select hospital procurement audits. Key model drivers are: 1) average reprogramming efficiency, 2) clinical trial enrollments using iPSC-derived cells, 3) grant inflow to disease-modeling projects, 4) GMP facility start-ups, and 5) price erosion curves for high-volume cardiomyocyte and neuron lots. Forecasts employ multivariate regression linked to these drivers, complemented by ARIMA smoothing for short-term fluctuations. Assumption gaps in bottom-up samples are bridged with regional import data and validated expert ranges.

Data Validation & Update Cycle

Outputs pass variance scans against independent metrics, and anomalies trigger analyst re-checks. Senior reviewers sign off only after multi-step peer review. We refresh every twelve months, yet interim updates activate when material events, such as major approvals, supply shocks, or currency swings, shift fundamentals; a final validation pass is completed just before release.

Why Mordor's Induced Pluripotent Stem Cells Baseline Earns Early Trust

Published estimates differ because firms pick unique scopes, base years, and uptake curves. Some count only reagent sales, whereas others mix in organoid platforms or broader stem-cell therapy revenues.

Key gap drivers include varying inclusion of Asia-Pacific service contracts, divergent price-decline assumptions for cardiomyocyte lots, and refresh cadences that may lag fast pipeline progress. Mordor's disciplined annual refresh and dual-approach model mitigates these variances, yielding the dependable baseline clients need.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.36 B (2025) | Mordor Intelligence | - |

| USD 1.84 B (2024) | Global Consultancy A | Excludes Asia service revenues; relies mainly on company revenue roll-ups |

| USD 1.93 B (2024) | Industry Publication B | Treats organoid platforms as separate sub-market, trimming core iPSC value |

| USD 1.60 B (2025) | Regional Consultancy C | Conservative adoption rates and limited hospital R&D capture |

The comparison shows that differing scopes and aging assumptions drive most gaps, while our regularly updated, variable-anchored framework delivers a transparent, reproducible starting point for strategy and investment planning.

Key Questions Answered in the Report

How fast is the induced pluripotent stem cells market expected to grow through 2031?

The market is projected to advance at a 9.83% CAGR between 2026 and 2031, climbing from USD 2.59 billion in 2026 to USD 4.14 billion by 2031.

Which region will record the highest growth?

Asia-Pacific is forecast to post an 11.67% CAGR through 2031 because of Japan’s accelerated regulatory path and China’s USD 1.2 billion provincial funding.

What segment currently dominates revenue?

Drug discovery and development holds 39.67% of 2025 revenue as pharmaceutical firms rely on iPSC assays to de-risk compounds early.

Which derived cell type is growing the fastest?

Neurons are projected to expand at a 10.06% CAGR as Parkinson’s and ALS programs scale.

What is the main cost barrier cited by developers?

GMP production remains capital-intensive; media and release testing push batch costs up to USD 150,000, hindering small sponsors.

Page last updated on: