Critical Limb Ischemia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

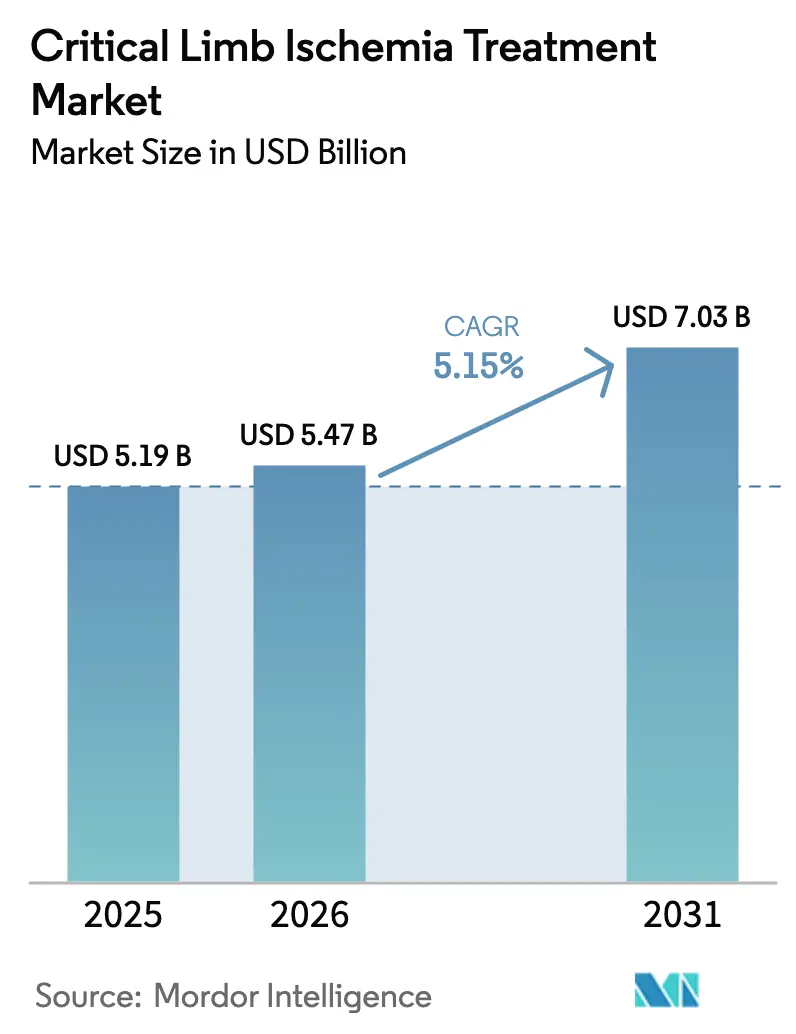

| Market Size (2026) | USD 5.47 Billion |

| Market Size (2031) | USD 7.03 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Critical Limb Ischemia Treatment Market Analysis by Mordor Intelligence

The Critical Limb Ischemia Treatment Market size was valued at USD 5.19 billion in 2025 and is estimated to grow from USD 5.47 billion in 2026 to reach USD 7.03 billion by 2031, at a CAGR of 5.15% during the forecast period (2026-2031).

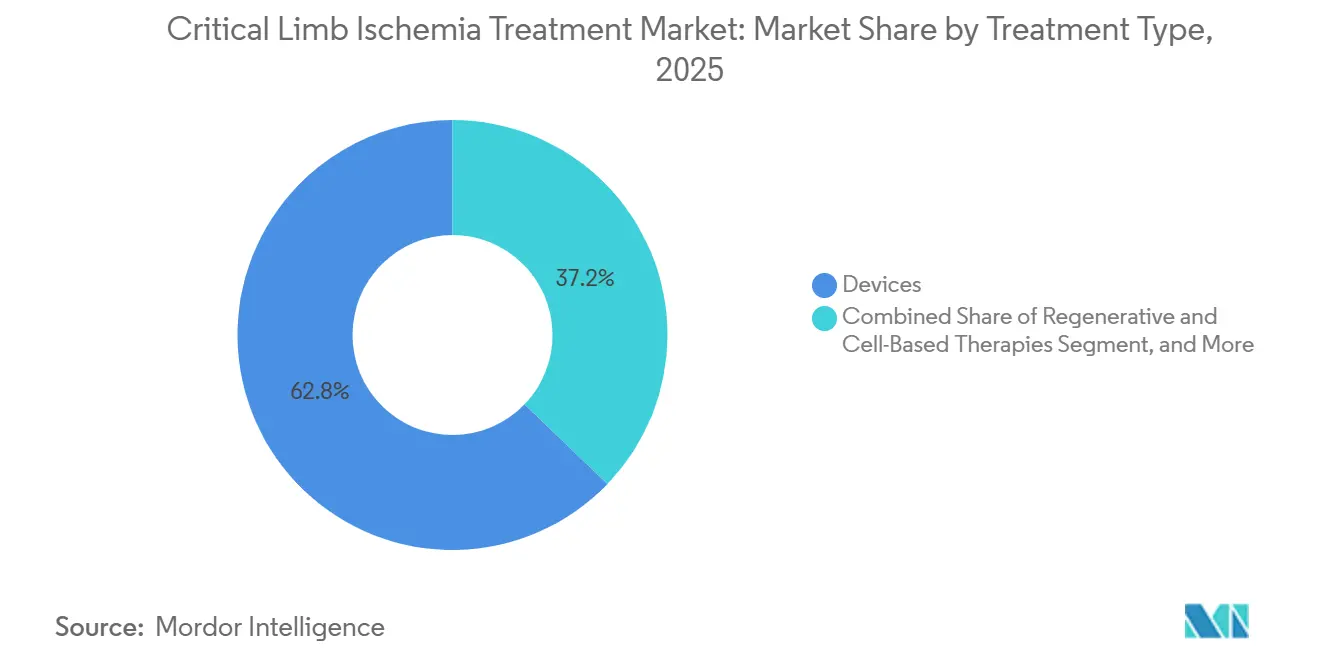

Device-based revascularization remains the cornerstone of therapy; however, its 62.81% revenue share in 2025 disguises a decisive pivot toward regenerative and cell-based options, which are expanding at more than double the overall pace. Hospitals, ambulatory surgical centers, and multispecialty vascular clinics are increasing access to these newer modalities as payers reward therapies that reduce re-intervention rates and prevent amputation. At the same time, emerging markets are unlocking latent demand through local approvals of cost-efficient drug-eluting balloons, offsetting slower growth in Europe where paclitaxel safety reviews have dampened enthusiasm for specific devices. Competitive intensity is intensifying as established device vendors defend their share against biologics start-ups, AI imaging specialists, and low-cost regional manufacturers.

Key Report Takeaways

- By treatment type, devices held 62.81% of the critical limb ischemia treatment market share in 2025, while regenerative and cell-based therapies are projected to advance at a 10.06% CAGR through 2031.

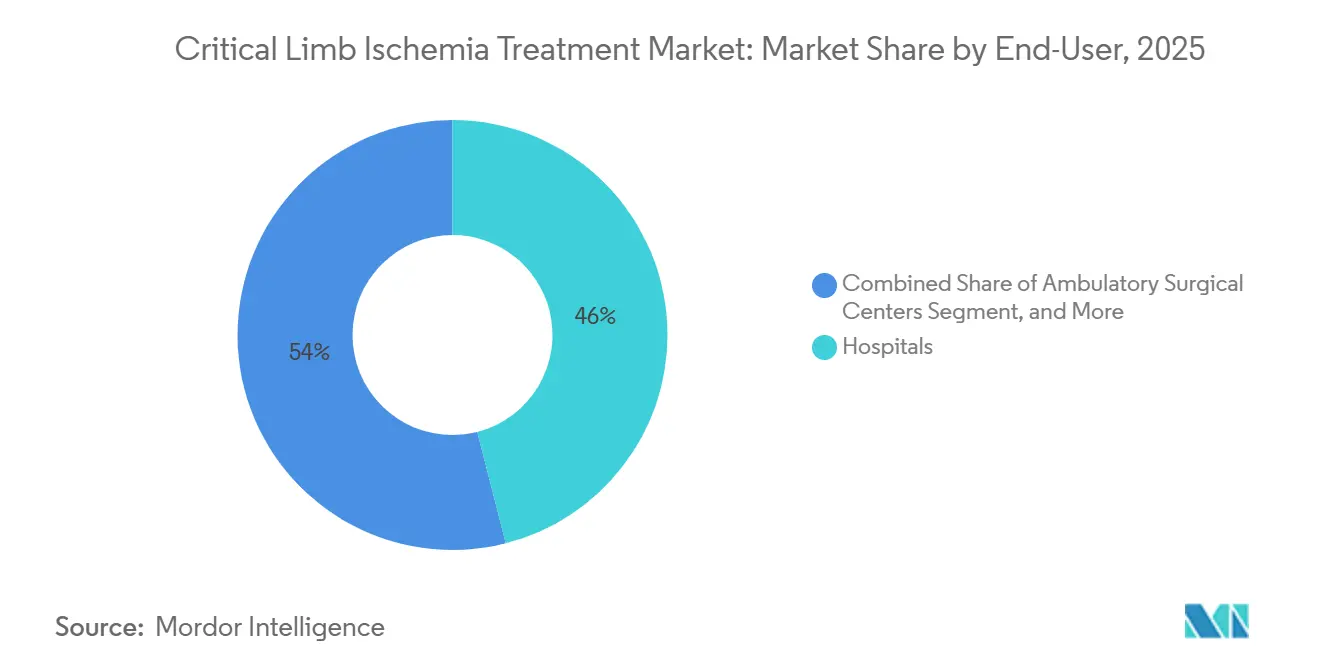

- By end-user, hospitals captured 46.03% share of the critical limb ischemia treatment market size in 2025, and ambulatory surgical centers are expanding at a 10.72% CAGR through 2031.

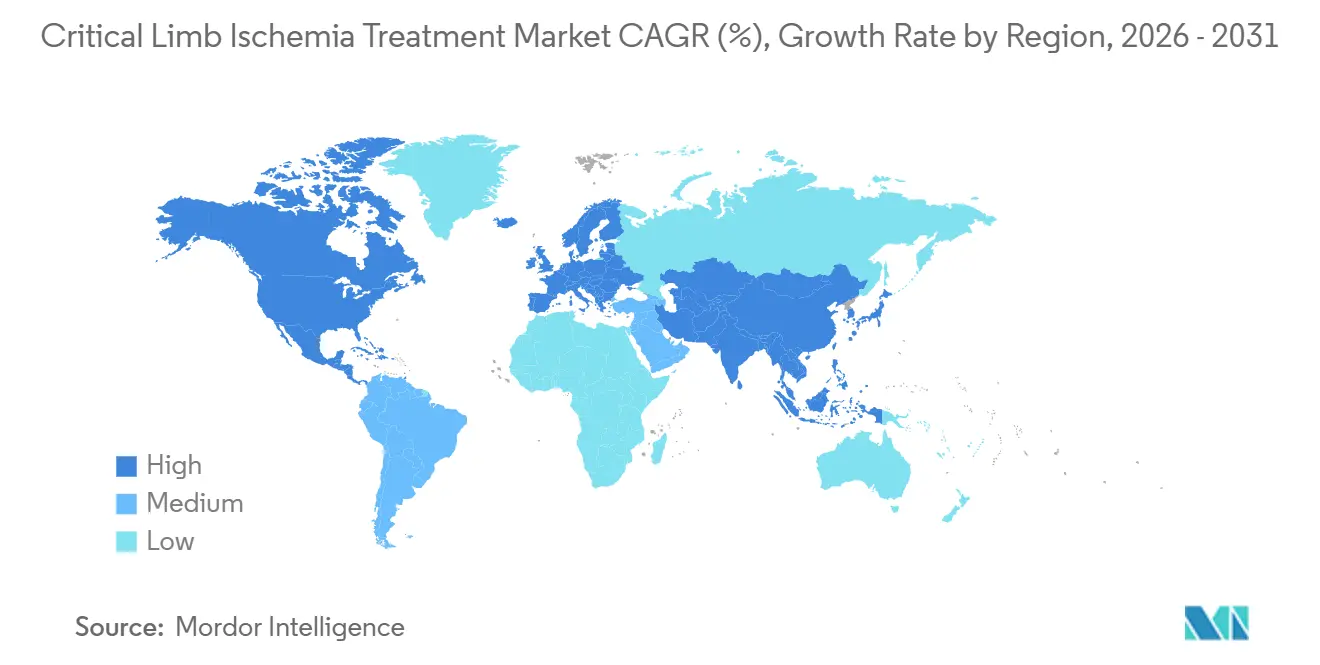

- By geography, North America commanded 44.32% revenue share in 2025; Asia-Pacific is forecast to post the fastest 11.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Critical Limb Ischemia Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes & PAD Prevalence | +1.2% | Global, with acute pressure in APAC (India, China) and Middle East | Medium term (2-4 years) |

| Growing Adoption of Minimally Invasive Revascularization Devices | +0.9% | North America & EU core, spillover to APAC urban centers | Short term (≤ 2 years) |

| Aging Population Intensifying CLI Incidence | +0.8% | Japan, Germany, Italy; emerging in South Korea, Singapore | Long term (≥ 4 years) |

| FDA Breakthrough Designations Speeding BTK Device & Cell-Therapy Launches | +1.1% | United States, with follow-on approvals in EU and Japan | Short term (≤ 2 years) |

| Expansion of Multispecialty Limb-Preservation Centers | +0.7% | United States (Medicare Advantage networks), select EU markets | Medium term (2-4 years) |

| AI-Enabled Perfusion Imaging Improving Patient Selection | +0.5% | United States, Germany, Japan; pilot programs in Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes and PAD Prevalence

The International Diabetes Federation estimated 537 million adults living with diabetes in 2024 and forecasts 643 million by 2030, with four-fifths of new cases clustered in developing regions.[1]International Diabetes Federation, “IDF Diabetes Atlas 2024,” idf.org Peripheral artery disease complicates 12%–15% of older diabetics, and the Centers for Disease Control and Prevention confirmed a 15-fold higher amputation risk for diabetic patients compared with non-diabetics. In India, undiagnosed PAD prevalence exceeds 25% among urban diabetics because primary care rarely performs ankle-brachial index testing, but new public screening mandates will soon expose this hidden cohort. China faces a similar surge, reporting 140 million diabetics in 2025, yet fewer than 30% receive statins, fueling progression to critical limb ischemia. These data point to a durable demand driver for revascularization devices, adjunct pharmacotherapy, and ultimately regenerative therapeutics.

Growing Adoption of Minimally Invasive Revascularization Devices

Percutaneous transluminal angioplasty and stenting represented 78% of all U.S. critical limb ischemia interventions in 2025, up from 62% five years earlier, due to shorter recovery times and lower hospital costs.[2]American College of Cardiology, “U.S. Revascularization Trends 2025,” acc.org Boston Scientific’s paclitaxel-free Ranger balloon achieved an 82% 12-month primary patency rate in below-the-knee lesions, capturing market share from legacy paclitaxel products. Medtronic’s IN.PACT Admiral balloon remains the leader in above-the-knee disease, with 2025 sales of USD 680 million; however, the company is diversifying into sirolimus coatings to navigate safety scrutiny. Segment diversification and rapid product cycles are therefore sustaining the device franchise even as novel biologics rise.

Aging Population Intensifying CLI Incidence

Japan projects that 35% of its citizens will be at least 65 years old in 2030, a demographic shift driving CLI rates to 400 per 100,000 person-years in this age bracket, which is triple the rate in younger cohorts.[3]Ministry of Health, Labour and Welfare Japan, “Population and Disease Statistics,” mhlw.go.jp Germany recorded an 18% jump in CLI hospitalizations between 2022 and 2025 despite stable diabetes prevalence, underscoring aging as an independent risk driver. South Korea’s national insurer reported average per-patient CLI expenditures of KRW 28 million (USD 21,000) in 2024, up 22% since 2022, because elderly patients often require multiple revascularizations. These data confirm that aging countries with generous coverage will continue to be premium markets for device and cell therapies.

FDA Breakthrough Designations Speeding BTK Device and Cell-Therapy Launches

LimFlow’s deep vein arterialization system secured FDA breakthrough device status in 2024 and full approval in 2025 after demonstrating 74% amputation-free survival at one year in no-option CLI. Pluristem’s PLX-PAD allogeneic cell therapy entered Phase III after a breakthrough designation in 2024 and aims for market entry by 2027. Cesca Therapeutics’ CartiCell autologous bone marrow platform also enjoys expedited review, shortening commercial timelines by up to two years. Breakthrough pathways thus reduce regulatory risk and send strong reimbursement signals to payers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Limited Reimbursement in Emerging Economies | -0.6% | India, Southeast Asia, sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Underdiagnosis and Late Presentation | -0.5% | Sub-Saharan Africa, rural India, Latin America | Medium term (2-4 years) |

| Paclitaxel Device Safety Controversy | -0.4% | EU core markets, United States (Medicare population) | Short term (≤ 2 years) |

| Shortage of Trained Vascular Specialists | -0.3% | United States, United Kingdom, Australia; acute in GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Limited Reimbursement in Emerging Economies

Drug-eluting balloons and stents cost USD 1,800–3,200 in India, but government schemes reimburse just USD 600, forcing patients to pay more than a year's median income out of pocket. Brazil offers coverage in public hospitals, yet waiting times average 180 days, prompting wealthier patients to seek private centers at BRL 45,000 (approximately USD 9,000) per case. Gulf Cooperation Council nations cover CLI fully for their citizens, but expatriate coverage caps at USD 5,000 per year, which is well below real-world costs. Tiered product portfolios and local manufacturing are emerging as mitigation strategies.

Underdiagnosis and Late Presentation

The World Health Organization reports that 60% of CLI cases in sub-Saharan Africa and 45% in rural India arrive at Rutherford 6, when tissue loss is irreversible. Less than 10% of primary care visits in low-resource regions include ankle-brachial index screening due to the scarcity of Doppler equipment. Argentina documented a 14-month median lag from symptom onset to specialist referral in 2024, explaining high amputation rates. Point-of-care Dopplers priced under USD 200 could close this gap, but require national adoption schemes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Regenerative Therapies Outpace Devices Despite Smaller Base

Devices accounted for 62.81% of 2025 revenue, anchored by drug-eluting stents, plain balloons, and atherectomy systems. Embolic protection devices accounted for just 3% of device revenue, as they are primarily reserved for high-risk distal work. Peripheral dilatation systems, such as Cardiovascular Systems’ Diamondback 360, grew 14% year-over-year, displacing plain angioplasty in calcified lesions. The growth of vascular and drug-eluting stents softened to a 3.2% CAGR amid headwinds from paclitaxel. Regenerative and cell-based therapies held an 8% share in 2025, but their 10.06% CAGR positions them to erode repeat device revenue, as successful biologic repair lowers re-intervention rates.

By End-User: Ambulatory Surgical Centers Capture Complex Procedures

Hospitals still accounted for 46.03% of the revenue in 2025; however, payer steering and bundled payments are shifting suitable cases to ambulatory environments that deliver similar outcomes at a lower cost. Ambulatory surgical centers executed 28% of U.S. CLI interventions in 2025 and are growing at a 10.72% CAGR, lifted by CMS coverage of below-the-knee angioplasty since 2024. Office-based labs, a subset of ASCs, accounted for 35% of Boston Scientific’s Ranger balloon sales in 2025, up from 18% in 2023, confirming a shift in channel economics. The specialty vascular and wound-care clinics segment is growing at a rapid pace, as integrated care models demonstrate a 40% reduction in major amputations.

Geography Analysis

North America dominated with a 44.32% share in 2025, due to U.S. Medicare’s generous reimbursement, which underpins device usage. However, scrutiny of paclitaxel and a mature installed base temper the acceleration. Canada reimburses CLI at CAD 8,500 (USD 6,300), which is 25% below U.S. rates, thereby restraining premium adoption. Mexico expanded its vascular capacity by 18% between 2023 and 2025; however, specialist scarcity continues to keep guideline adherence below 40%. U.S. limb-preservation protocols delivered via telehealth are opening adjacent Latin markets to American devices, further consolidating supplier advantage.

Germany halted broad paclitaxel reimbursement in 2024, resulting in a one-third reduction in national sales. Conversely, the United Kingdom issued positive guidance for LimFlow’s deep vein arterialization system in 2026, creating a GBP 45 million (USD 57 million) opportunity.

Asia-Pacific is the growth driver with an 11.53% CAGR. China’s approval of 14 home-grown drug-eluting devices between 2024 and 2025 reduced local prices by 60%, unlocking rural demand and expanding the critical limb ischemia treatment market size in the region. Japan grows 5.2% as reimbursement for cell therapies rose 18% in 2025. Australia’s TGA green-lit Cynata’s Cymerus therapy for compassionate use in 2025, reinforcing its role as a regenerative test bed.

Saudi Arabia has earmarked SAR 12 billion (approximately USD 3.2 billion) for 50 limb-preservation clinics by 2028. The UAE’s 2024 fast-track pathway shrank device approval times from 18 to 6 months, encouraging multinational launches. Sub-Saharan Africa remains underserved, with only 22% of patients in South Africa receiving revascularization due to cost and capacity constraints.

Competitive Landscape

The five most prominent companies, Medtronic, Boston Scientific, Abbott Laboratories, Cook Medical, and Terumo, controlled significant revenue in 2025, illustrating moderate concentration. Medtronic generated USD 1.2 billion from CLI balloons and stents in fiscal 2025, but growth slipped to 2.8% amid safety questions. Boston Scientific’s USD 145 million purchase of Bolt Medical in 2024 included the Motus thrombectomy system, which addresses 18% of CLI cases complicated by clot burden. Abbott leveraged the Supera stent’s 89% two-year patency to target below-the-knee disease traditionally owned by Cook Medical’s Zilver PTX. White-space arenas include AI perfusion imaging, where Philips and Siemens are early movers, point-of-care cell processing from Cesca, and deep vein arterialization led solely by LimFlow. Disruptors such as Rexgenero and Micro Medical Solutions are exploiting local cost advantages and novel biologic platforms, eroding incumbent share from below.

Critical Limb Ischemia Treatment Industry Leaders

LimFlow SA

Cardiovascular Systems, Inc

Eli Lilly and Company

Abbott Laboratories

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: MEDINET signed an option license to commercialize Stempeucel regenerative therapy for chronic limb-threatening ischemia in Japan, expanding bilateral cell-therapy collaboration.

- July 2025: AngioDynamics enrolled the first patient in the AMBITION BTK trial evaluating its Auryon atherectomy system plus balloon angioplasty in infrapopliteal disease.

- April 2025: Reflow Medical received FDA De Novo clearance for its Spur peripheral retrievable stent system targeting infrapopliteal lesions.

- March 2024: Elixir Medical achieved FDA breakthrough designation for its DynamX BTK adaptive implant designed for below-the-knee vessels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the critical limb ischemia (CLI) treatment market as worldwide revenue from devices, drugs, and surgical or hybrid procedures that restore or maintain limb blood flow once chronic arterial blockage threatens tissue survival.

Scope exclusion: diagnostic imaging platforms and therapies aimed only at earlier intermittent claudication are not evaluated.

Segmentation Overview

- By Treatment Type

- Devices

- Embolic Protection Devices

- Peripheral Dilatation Systems

- Balloon Dilators

- Vascular & Drug-Eluting Stents

- Drugs

- Antiplatelet Agents

- Antihypertensive Agents

- Lipid-Lowering Agents

- Antithrombotic Agents

- Regenerative & Cell-Based Therapies

- Devices

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Vascular & Wound-Care Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed vascular surgeons, interventional radiologists, procurement leads, and reimbursement advisers across North America, Europe, Asia-Pacific, Latin America, and the Middle East. Their insight on therapy-mix shifts, regional selling prices, and regulatory timing let us validate and refine desk findings.

Desk Research

We began by mapping age-stratified CLI incidence and PAD prevalence from the World Health Organization, the International Diabetes Federation, the CDC, and European vascular registries. To frame industry context, our team layered macro indicators, reimbursement schedules, and hospital discharge snapshots. Paid resources, D&B Hoovers for revenue splits, Dow Jones Factiva for news flow, Questel for patent trails, and Volza for shipment clues, rounded out secondary inputs. The titles named are illustrative; many other public and commercial datasets were reviewed.

Market-Sizing & Forecasting

We apply one top-down prevalence-to-treated-patient model per country and multiply resulting pools by regional average prices. Supplier roll-ups and sampled ASP multiplied by procedure checks add bottom-up guardrails before final alignment. Core drivers, diabetes prevalence, revascularization penetration, revision rates, reimbursement caps, and gene-therapy launch timing, feed a multivariate regression that projects values through 2030.

Data Validation & Update Cycle

Outputs clear variance screens against vascular registries and procurement trackers, move through multi-analyst and supervisory review, and refresh every year; interim updates follow recalls, landmark trials, or major reimbursement shifts.

Why Mordor's Critical Limb Ischemia Treatment Market Baseline Commands Confidence

Published estimates often diverge because some groups blend earlier PAD stages, freeze prices, or lean on dated epidemiology. By focusing only on late-stage CLI, refreshing inputs annually, and cross-checking two modeling paths, we deliver a balanced baseline buyers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.20 B (2025) | Mordor Intelligence | - |

| USD 4.90 B (2022) | Global Consultancy A | Older base year; omits gene and cell therapies. |

| USD 4.20 B (2023) | Industry Journal B | Hospital procedures only; excludes outpatient devices. |

| USD 5.55 B (2025) | Regional Consultancy C | Mixes broader PAD stages; one global ASP. |

These comparisons show that our narrow scope, transparent variables, and repeatable checks make Mordor's numbers the most dependable baseline for CLI strategy.

Key Questions Answered in the Report

How large is the critical limb ischemia treatment market in 2026?

The market generated USD 5.47 billion in 2026 and is projected to reach USD 7.03 billion by 2031, growing at a 5.15% CAGR.

Which treatment segment is expanding fastest?

Regenerative and cell-based therapies are advancing at a 10.06% CAGR, outpacing both devices and drugs.

Why are ambulatory surgical centers gaining share in CLI procedures?

CMS reimbursement and same-day discharge protocols make ASCs cost-effective, enabling them to perform 28% of U.S. interventions in 2025.

What is driving rapid growth in Asia-Pacific?

China’s approval of locally made drug-eluting devices and India’s expansion of Ayushman Bharat coverage are propelling an 11.53% regional CAGR.

Which companies lead the competitive landscape?

Medtronic, Boston Scientific, Abbott Laboratories, Cook Medical, and Terumo together generate significant revenue, but new entrants in biologics and imaging are challenging their dominance.

Page last updated on: