CRISPR Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

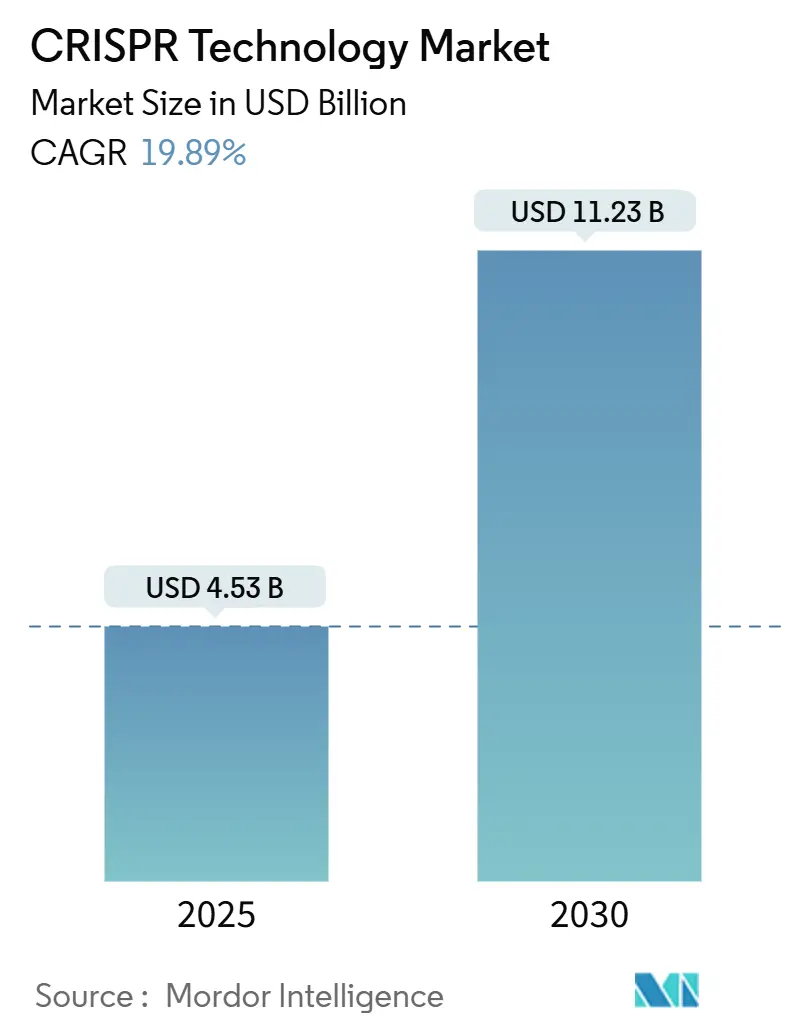

| Market Size (2025) | USD 4.53 Billion |

| Market Size (2030) | USD 11.23 Billion |

| Growth Rate (2025 - 2030) | 19.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CRISPR Technology Market Analysis by Mordor Intelligence

The CRISPR Technology Market size is estimated at USD 4.53 billion in 2025, and is expected to reach USD 11.23 billion by 2030, at a CAGR of 19.89% during the forecast period (2025-2030).

Rapid growth follows the December 2023 FDA clearance of CASGEVY, the first CRISPR therapy for β-thalassemia and sickle-cell disease. Capital inflows continue as prime-editing trials report positive human data and falling reagent costs widen the user base. Consolidation around delivery know-how is visible through investments such as Regeneron’s stake in Mammoth Biosciences, while public bioeconomy initiatives in the United States, United Kingdom, China, and Australia support downstream manufacturing. The CRISPR technology market benefits from clearer regulatory guidance and a growing pipeline that now spans hematology, oncology, neurological, and agricultural use cases.

Key Report Takeaways

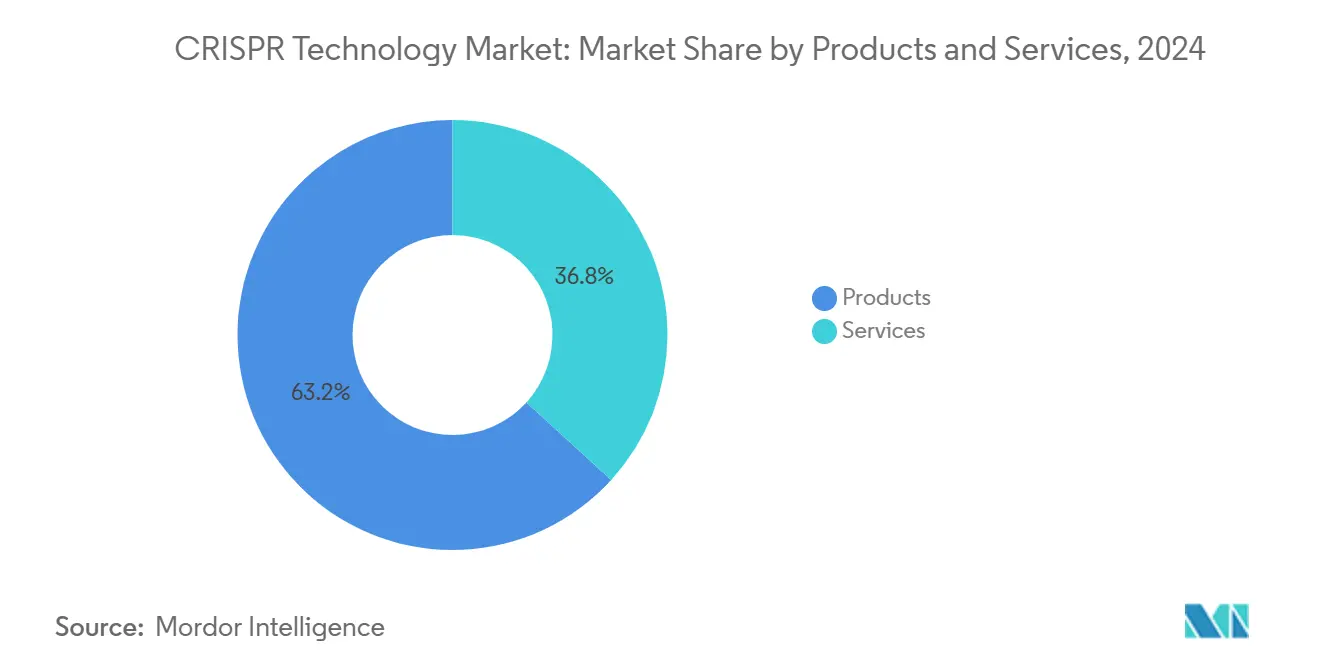

- By product & Services , Product category, led with 63.23% revenue share in 2024 and is forecast to register the fastest 22.03% CAGR through 2030.

- By technology, CRISPR/Cas9 commanded 71.54% share in 2024; Prime Editing is projected to grow at a 21.45% CAGR over the same period.

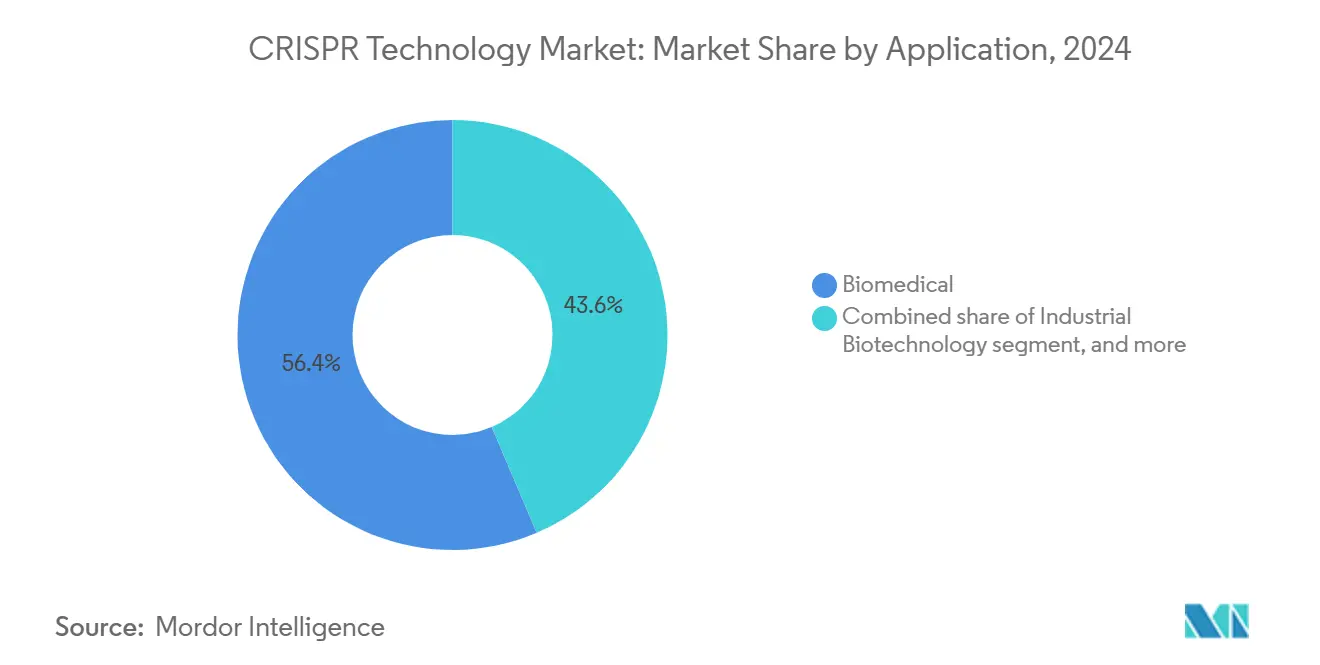

- By application, Biomedical applications held 56.43% of the CRISPR technology market size in 2024 and Environmental & Synthetic Biology is set to expand at a 22.31% CAGR through 2030.

- By end user, Pharmaceutical & Biotechnology Companies represented 50.32% share in 2024, whereas Contract Research Organizations are anticipated to record the highest 22.56% CAGR to 2030.

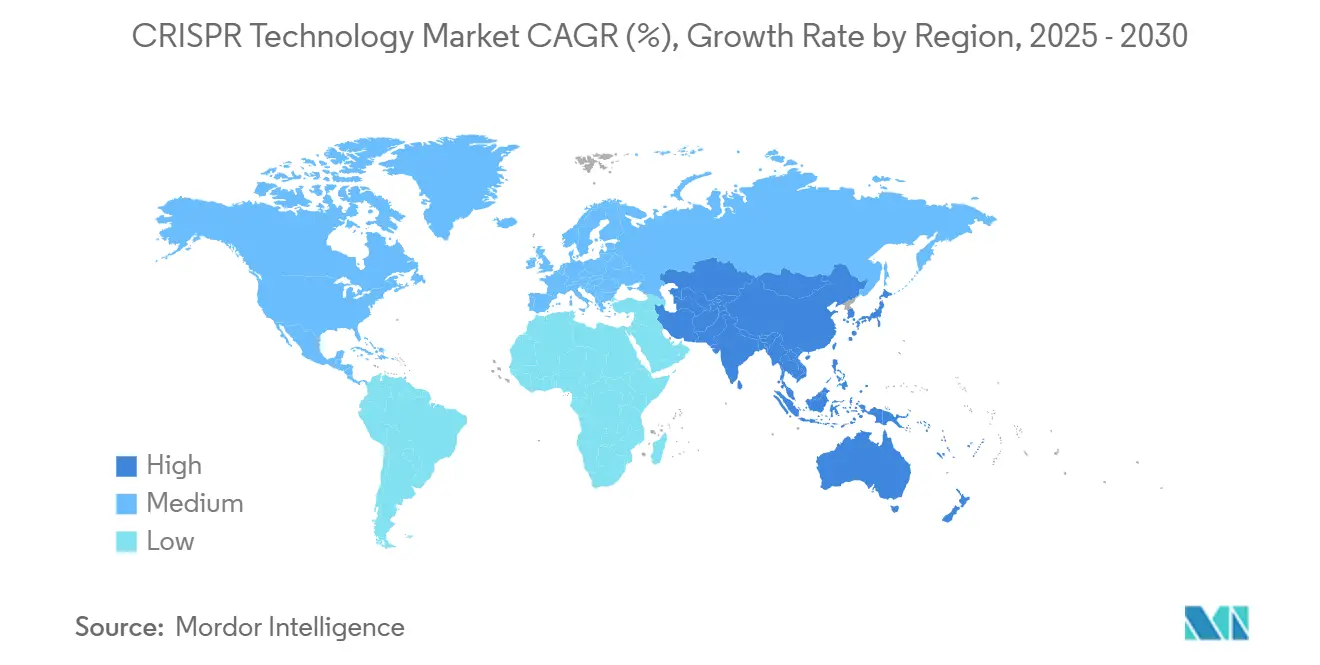

- By geography, North America captured 42.56% of 2024 revenue; Asia-Pacific is expected to post the fastest 20.34% CAGR between 2025 and 2030.

Global CRISPR Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding clinical pipeline for genetic disorders | +4.2% | Global, with early gains in North America & European Union | Medium term (2-4 years) |

| Surge in agri-biotech gene-edited crop approvals | +3.8% | Global, spill-over to Asia-Pacific & Latin America | Long term (≥ 4 years) |

| Falling genome-editing costs and tool democratization | +3.5% | Global | Short term (≤ 2 years) |

| Strategic pharma–biotech alliances for in-vivo CRISPR therapies | +2.9% | Core markets in North America & European Union | Medium term (2-4 years) |

| AI-enabled functional-genomics discovery acceleration | +2.7% | Technology hubs in North America, EU & Asia-Pacific | Medium term (2-4 years) |

| Government bioeconomy programs supporting synthetic-biology scale-up | +2.4% | National programs in United Kingdom, Australia & United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Clinical Pipeline for Genetic Disorders

More than 40 CRISPR-based medicines are in active trials worldwide. CASGEVY generated USD 200 million in first-year sales, validating premium pricing models for severe blood disorders. Prime-editing achieved functional immune restoration in chronic granulomatous disease without serious safety issues during its 2025 first-in-human study.[1]Kathrin Schmitt, “Prime Editing Enters the Clinic,” nature.com The FDA’s January 2024 guidance clarified biodistribution and off-target study expectations, shortening regulatory uncertainty. Early lung-cell work corrected 60% of cystic-fibrosis mutations, expanding respiratory prospects. Several programs targeting oncology and ophthalmology now enroll patients, backed by alliances that pair editing expertise with capital-rich pharma partners.

Strategic Pharma–Biotech Alliances for In-Vivo CRISPR Therapies

Regeneron’s USD 95 million upfront payment to Mammoth Biosciences exemplifies capital-sharing to solve delivery bottlenecks. Sanofi’s collaboration with Scribe Therapeutics carries USD 1.2 billion in milestones for compact Cas enzymes suited to neurological targets. CRISPR Therapeutics and Capsida joined forces to deploy AAV vectors against ALS. Danaher funds the Innovative Genomics Institute’s Beacon for CRISPR Cures to industrialize manufacturing pipelines. These alliances combine delivery, regulatory, and GMP capabilities, accelerating clinical timelines across the CRISPR technology market.

AI-Enabled Functional-Genomics Discovery Acceleration

AWS and ElevateBio integrated generative AI into cell-engineering workflows, promising faster target validation and design iterations. Academic centers leverage reinforcement learning to predict repair outcomes, reducing off-target screening costs. Software vendors now sell subscription analytics that support continuous guide-RNA optimization, adding recurring revenue to the CRISPR technology market. Faster target triage shrinks preclinical timelines, directing more projects toward IND readiness. AI-assisted platforms foster rapid innovation without proportionally increasing headcount, improving R&D economics.

Government Bioeconomy Programs Supporting Synthetic-Biology Scale-Up

The United Kingdom earmarked GBP 100 million for engineering-biology commercialization, including CRISPR fermentation hubs. The US Defense Advanced Research Projects Agency funds field-deployable biomanufacturing units that require robust CRISPR toolkits. Australia’s national roadmap foresees AUD 30 billion in synthetic-biology value by 2040 and channels grants to enzyme-engineering ventures. Such programs cultivate skilled labor and shared infrastructure, lifting the long-run ceiling of the CRISPR technology market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny and evolving compliance frameworks | -2.8% | Global, with variability across EU & Asia-Pacific | Medium term (2-4 years) |

| Complex intellectual-property landscape and litigation risks | -2.3% | United States & European Union patent jurisdictions | Medium term (2-4 years) |

| Limited delivery modalities for in-vivo editing | -2.1% | North America & EU for first-wave therapeutic programs | Short term (≤ 2 years) |

| Unresolved ethical concerns around germline editing | -1.9% | Global, with regional policy differences | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Scrutiny and Evolving Compliance Frameworks

The FDA now requires genome-wide off-target profiling plus long-term monitoring for human trials, extending timelines and budgets. The EMA mandates parallel but non-identical datasets, forcing developers to craft region-specific filings. US environmental tools must satisfy EPA, USDA, and FDA, complicating field-trial approvals for engineered microbes. Large companies build in-house compliance teams, whereas start-ups outsource to specialist CROs, raising operating costs across the CRISPR technology market. Until inter-agency harmonization progresses, smaller firms face higher capital hurdles to reach clinical or commercial scale.

Unresolved Ethical Concerns Around Germline Editing

Global consensus discourages heritable DNA edits, limiting funding for reproductive applications. Public attitudes differ by region, affecting uptake for food and environmental products. Gene-drive proposals targeting invasive species trigger suspensions in some jurisdictions, elevating reputational risk for sponsors. Companies invest in transparency campaigns and ethics boards, yet uncertainty persists, dampening investment in certain verticals of the CRISPR technology market. Policy clarity will likely remain fragmented through the decade, maintaining a moderate drag on overall growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Services: Product Anchor Revenue and Growth

In 2024, products generated 63.23% of total revenue, boasting a growth rate of 22.03%. Within the product category, Kits & Reagents emerged as the dominant revenue source, encompassing vital consumables such as guide RNAs, nucleases, and delivery mixes integral to experiments. This segment ensures consistent sales, stabilizing research funding cycles. Design Tools/Software is the fastest-growing segment, witnessing a 21.34% CAGR, driven by AI-assisted platforms streamlining experimental planning. Enzymes see steady demand, with annual launches of improved fidelity variants. Meanwhile, custom guide-RNA catalogs are expanding to cater to precision therapy demands. CRISPR libraries facilitate pooled screens in drug discovery, and specialized delivery reagents tackle tissue-specific challenges.

In the Services domain, Cell-line engineering emerged as the leading revenue generator, underscoring its importance in pharmaceutical pipelines that depend on tailored models for target validation. The technical intricacies involved command premium fees and extended contracts. CRISPR screening services are witnessing a robust CAGR, driven by the demands of functional-genomics programs that utilize high-throughput loss-of-function and gain-of-function assays. Every application hinges on gRNA design and synthesis, while the generation of animal models plays a crucial role in disease research, especially in areas where cell lines may not suffice.

By Technology: Cas9 Dominates but Precision Platforms Surge

CRISPR/Cas9 delivered 71.54% share in 2024 thanks to broad validation, simple design rules, and abundant off-the-shelf kits. Yet safety concerns around double-strand breaks push demand toward prime editing, base editing, and compact Cas12/13 systems. Prime editing posts a 21.45% CAGR, driven by 2025 clinical data that showed durable correction without translocations. Base editors target point-mutation diseases unsuitable for full re-writes. Cas13 unlocks transcript-level interventions with lower immunogenicity. Innovation pivots toward delivery-ready compact nucleases like Scribe’s X-editing family that fit AAV capsids, lowering dose requirements. Tool suppliers bundle high-fidelity variants with lipid nanoparticles to improve in-vivo performance. The CRISPR technology market share enjoyed by Cas9 is forecast to slip yet remain above 55% by 2030 given entrenched research usage, while combined precision platforms could exceed 30%, reflecting rapid clinical adoption.

By Application: Biomedical Underpins Revenue while Environment Gathers Pace

Biomedical uses generated 56.43% of 2024 revenue because therapies command premium pricing and require large reagent volumes. Oncology, hematology, and rare diseases dominate trial pipelines, with several programs in Phase III. Environmental & Synthetic Biology shows 22.31% CAGR as climate mandates fuel demand for carbon-negative microbes and biodegradable-plastic production strains. Agricultural applications gain momentum on regulatory clarity for non-transgenic crops in the European Union and expanding acreage in China, India, and Brazil. Industrial biotechnology uses CRISPR to fine-tune enzyme pathways for bio-based chemicals, cutting fossil inputs. The CRISPR technology industry navigates different capital cycles: healthcare benefits from venture and pharma funding, whereas environmental plays rely on government grants and corporate sustainability budgets. By 2030, biomedical may still represent about half of total sales, but environmental and industrial verticals together can close the gap as scale economies emerge.

By End User: Pharma Leads, CROs Scale Fast

Pharmaceutical & Biotechnology Companies held 50.32% share in 2024, reflecting internal pipeline investments and partnership payments. Yet these firms increasingly outsource specialized steps to Contract Research Organizations, which record a 22.56% CAGR through 2030. CRO expansion aligns with cost-control and speed-to-clinic pressures, driving multi-year master-service agreements. Academic institutes remain pivotal in discovery but lag in downstream manufacturing spending. Other end users—seed companies, environmental groups, bio-materials start-ups—collectively form a growing long-tail segment. The CRISPR technology market size generated by CRO engagements is on track to double by 2030. Competition amplifies as large CDMOs enter the space, bundling viral-vector manufacturing and cell-processing suites with gene-editing services.

Geography Analysis

North America held 42.56% of 2024 revenue, driven by mature venture funding, favorable reimbursement, and clear FDA guidance that de-risks clinical investment. Boston, San Francisco, and San Diego anchor ecosystems where CRISPR Therapeutics, Editas Medicine, and Beam Therapeutics run multi-indication pipelines. The 2025 National Biotechnology Initiative Act expands tax credits for GMP capacity, strengthening domestic supply chains and cementing regional dominance.[2]House of Representatives, “National Biotechnology Initiative Act of 2025,” congress.govAsia-Pacific is the fastest-growing region at 20.34% CAGR to 2030, led by China’s multi-billion-dollar synthetic-biology parks and relaxed rules for gene-edited crops.[3]CSIRO, “Synthetic Biology Roadmap,” csiro.auAustralia’s roadmap foresees AUD 30 billion value by 2040 and funds industrial enzymes, while Singapore subsidizes GMP suites to lure global clinical-trial production. India’s contract-research sector leverages cost advantages and skilled labor to capture discovery outsourcing, broadening regional participation in the CRISPR technology market.

Europe remains influential through deep regulatory expertise and generous public grants. The United Kingdom’s GBP 100 million Engineering Biology fund finances fermentation hubs, and the EU-backed SYNBEE accelerator spans 25 nations, nurturing start-ups in food and environmental editing. EMA guidelines standardize genome-editing submissions, providing predictability despite stringent data demands. Central-eastern EU members court agricultural trials on climate-resilient wheat and maize, reflecting a pan-continental spread of CRISPR technology market applications.

Competitive Landscape

The tools segment is moderately concentrated as Thermo Fisher Scientific, Merck KGaA, and Danaher control global reagent supply and distribution. Their advantage lies in GMP manufacturing scale, validated quality systems, and multi-channel sales footprints.

Therapeutics remain less concentrated; CRISPR Therapeutics, Intellia, Editas, and Beam each hold single-digit revenue shares, none exceeding 15% of overall pipeline investment. Intellectual-property disputes between UC Berkeley and Broad Institute continue, but larger companies mitigate risk by licensing both estates, creating a barrier for smaller entrants.

Strategic partnerships shape competition. Regeneron–Mammoth, Sanofi–Scribe, and Danaher–IGI exemplify pharma preference for compact nucleases and manufacturing leverage. Delivery innovation remains the main white space; startups engineer lipid nanoparticles and viral vectors tuned to tissue tropism, and incumbents respond through acquisitions. AI-powered design suites like CRISPR-GPT and OpenCRISPR-1 democratize access, prompting tool giants to integrate software subscriptions into reagent bundles. Over 2025-2030, winners will combine broad patent coverage, digital design ecosystems, scalable GMP production, and proven clinical safety to consolidate shares in the CRISPR technology market.

CRISPR Technology Industry Leaders

Merck KGaA

GenScript

Danaher

Revvity

ThermoFisher Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Prime Medicine announced up to 72% gene correction in Alpha-1 Antitrypsin Deficiency mice and plans an IND/CTA by mid-2026.

- May 2025: Aldevron and Integrated DNA Technologies delivered the first personalized mRNA CRISPR therapy for an infant with urea-cycle disorder within six months.

- May 2025: Corteva invested USD 25 million in Pairwise to accelerate climate-resilient crops via the Fulcrum platform

Global CRISPR Technology Market Report Scope

As per the scope of the report, CRISPR technology is a tool for editing genomes. It enables researchers to alter DNA sequences and further modify gene function easily. It has several potential applications, including treating and preventing disease spread, correcting genetic defects, and improving crops.

The CRISPR technology market is segmented by product, application, end user, and geography. The product segment is further segmented into enzymes, kits, and reagents, guide RNA, and other products. The application segment is further divided into biomedical, agricultural, industrial, and other applications. The end user segment is further bifurcated into pharmaceutical companies and biotechnology companies, academics and government research institutes, and other end users (CROs, etc.). By geography, the market is further segmented into North America, Europe, Asia-Pacific, Middle East And Africa, and South America. The report offers the value (in USD) for the segments mentioned above.

| By Product | Enzymes |

| Kits & Reagents | |

| Guide RNA | |

| CRISPR Libraries | |

| Design Tools / Software | |

| Other Products | |

| By Service | gRNA Design & Synthesis |

| Cell Line Engineering | |

| Animal Model Generation | |

| CRISPR Screening Services | |

| Other Services |

| CRISPR/Cas9 |

| CRISPR/Cas12 |

| CRISPR/Cas13 |

| Base Editing |

| Prime Editing |

| Other Technologies |

| Biomedical |

| Agricultural |

| Industrial Biotechnology |

| Environmental & Synthetic Biology |

| Other Applications |

| Pharmaceutical & Biotechnology Companies |

| Academic & Government Research Institutes |

| Contract Research Organizations |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product & Services | By Product | Enzymes |

| Kits & Reagents | ||

| Guide RNA | ||

| CRISPR Libraries | ||

| Design Tools / Software | ||

| Other Products | ||

| By Service | gRNA Design & Synthesis | |

| Cell Line Engineering | ||

| Animal Model Generation | ||

| CRISPR Screening Services | ||

| Other Services | ||

| By Technology | CRISPR/Cas9 | |

| CRISPR/Cas12 | ||

| CRISPR/Cas13 | ||

| Base Editing | ||

| Prime Editing | ||

| Other Technologies | ||

| By Application | Biomedical | |

| Agricultural | ||

| Industrial Biotechnology | ||

| Environmental & Synthetic Biology | ||

| Other Applications | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Government Research Institutes | ||

| Contract Research Organizations | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What was the CRISPR technology market size in 2025?

It stood at USD 4.53 billion, reflecting the first full year of commercial therapy sales.

How fast is the CRISPR technology market expected to grow to 2030?

The forecast indicates a 19.89% CAGR, pushing revenue to about USD 11.23 billion.

What region will expand quickest through 2030?

Asia-Pacific is projected to grow at a 20.34% CAGR because of strong public funding and manufacturing investment.

Why are Contract Research Organizations gaining importance?

Pharma companies outsource complex editing tasks to CROs to control costs and speed up development, driving a 22.56% CAGR in CRO demand.

Page last updated on: