CRISPR And CRISPR-associated (Cas) Genes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

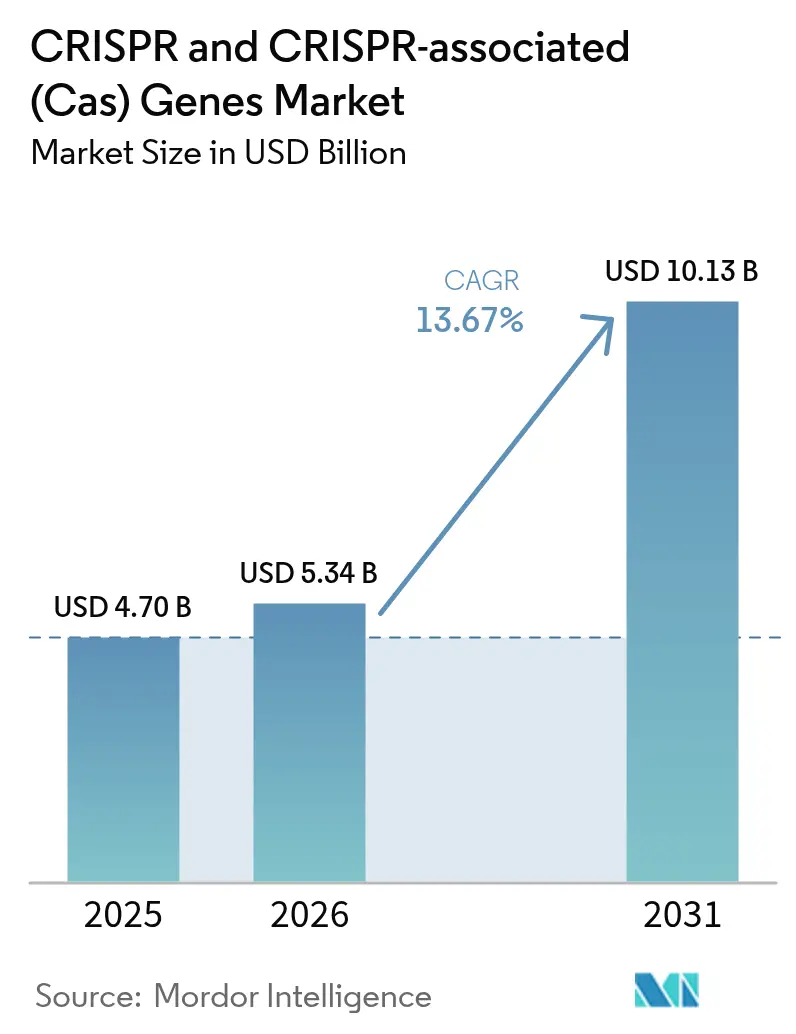

| Market Size (2026) | USD 5.34 Billion |

| Market Size (2031) | USD 10.13 Billion |

| Growth Rate (2026 - 2031) | 13.67% CAGR |

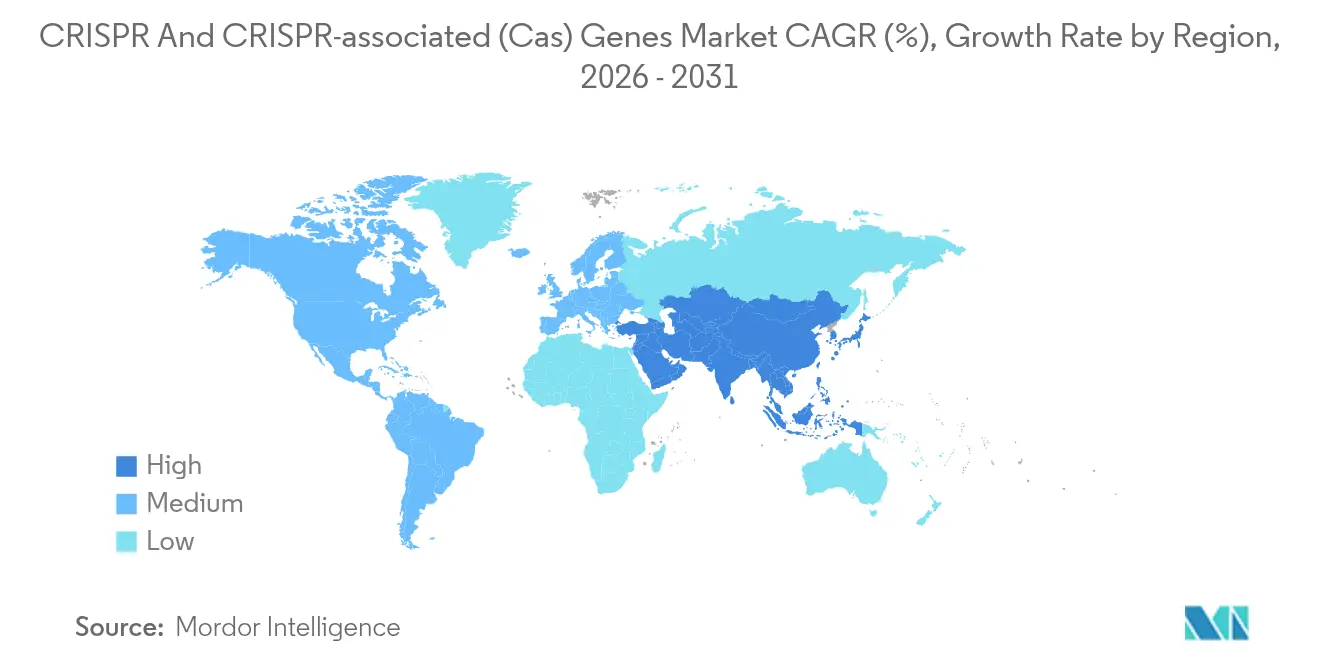

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

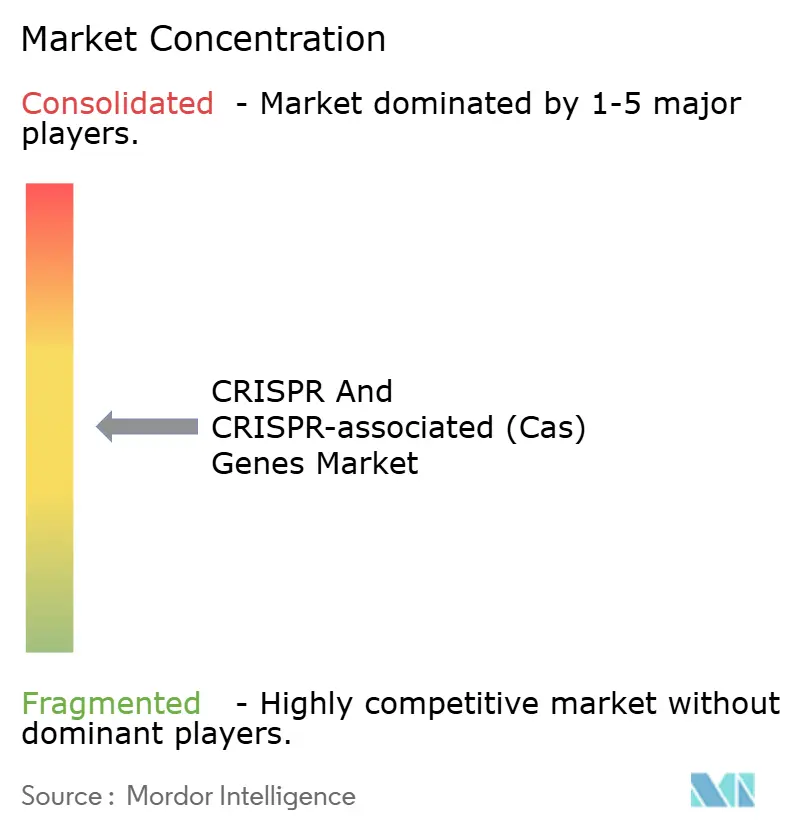

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CRISPR And CRISPR-associated (Cas) Genes Market Analysis by Mordor Intelligence

CRISPR and CRISPR-associated (CAS) genes market size in 2026 is estimated at USD 5.34 billion, growing from 2025 value of USD 4.70 billion with 2031 projections showing USD 10.13 billion, growing at 13.67% CAGR over 2026-2031. The growth arc signals that gene editing has shifted from a specialized research tool toward a validated therapeutic and agricultural platform. Adoption has accelerated since the landmark late-2023 approval of Casgevy for sickle cell disease and beta thalassemia, which created a regulatory precedent and de-risked the clinical pathway for follow-on programs. Investment flows remain strong, supported by 14 FDA review designations granted to CRISPR therapies in 2023, an unusually high figure for a single modality. Agricultural use cases are scaling as the United States and select Asia-Pacific regulators exempt gene-edited crops that mimic conventional breeding, removing significant time and cost barriers. Technology refinement continues, with prime and base editing addressing off-target risks and AI-driven guide design cutting candidate selection cycles from months to weeks.

Key Report Takeaways

- By component, products led with 78.45% revenue share in 2025 while services are advancing at a 14.12% CAGR through 2031.

- By application, biomedical uses commanded 81.40% share of the CRISPR and CRISPR-associated (CAS) genes market size in 2025; agriculture is projected to expand at a 15.18% CAGR to 2031.

- By technology, CRISPR-Cas9 held 61.85% of CRISPR and CRISPR-associated (CAS) genes market share in 2025, whereas prime editing is forecast to grow at 15.76% CAGR.

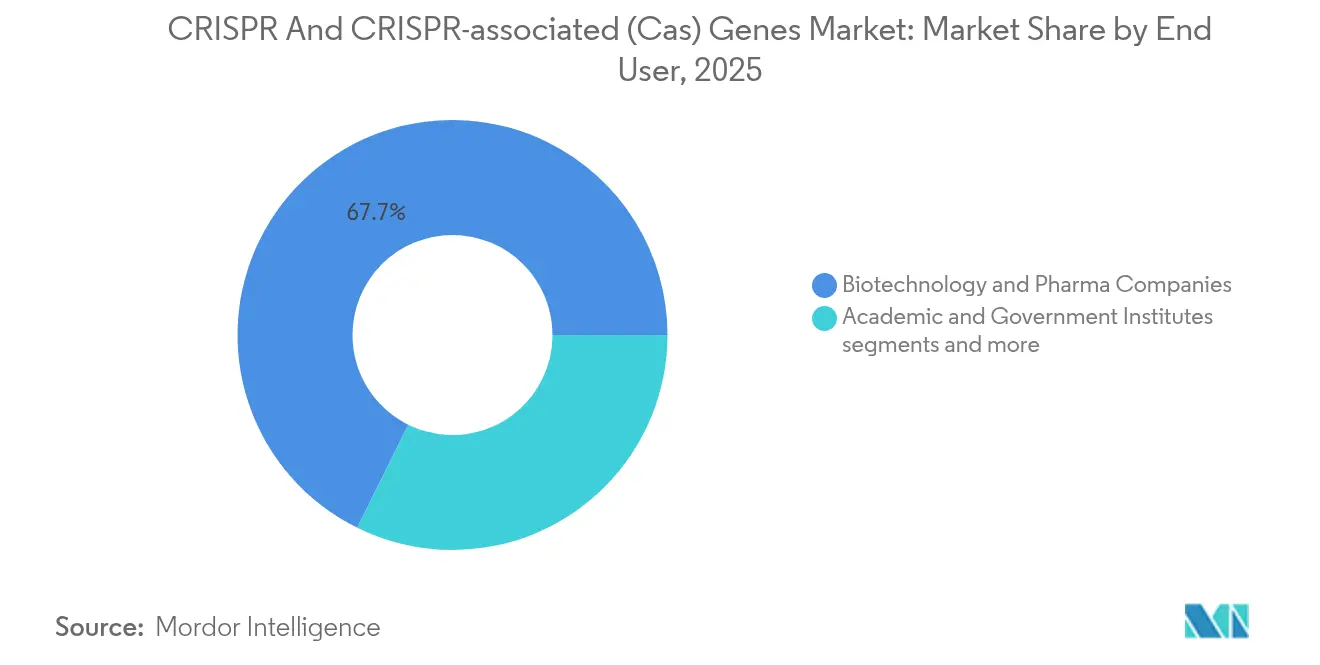

- By end user, biotechnology and pharmaceutical firms captured 67.70% share in 2025; contract research and manufacturing organizations (CRO/CMO) record the fastest CAGR at 14.74%.

- By geography, North America accounted for 47.10% revenue in 2025 and Asia-Pacific is pacing at a 15.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global CRISPR And CRISPR-associated (Cas) Genes Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA approvals of CRISPR-based therapies | +3.2% | Global, with North America leading | Medium term (2-4 years) |

| Advances in delivery technologies (viral & non-viral) | +2.8% | Global, concentrated in US and EU | Long term (≥ 4 years) |

| Rising R&D funding & strategic partnerships | +2.1% | Global, with APAC acceleration | Short term (≤ 2 years) |

| Mitochondrial in-vivo CRISPR opens rare-disease pipeline | +1.9% | North America & EU | Long term (≥ 4 years) |

| AI-driven sgRNA design accelerates time-to-lead | +1.7% | Global, tech hubs leading | Medium term (2-4 years) |

| Regulatory easing for gene-edited crops | +1.6% | North America, selective APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FDA Approvals of CRISPR-Based Therapies

The December 2023 approval of Casgevy established a safety and efficacy template that is now guiding at least eight additional late-stage programs worldwide. Prime Medicine soon received clearance for PM359, the first prime-editing therapy to reach human trials, signaling that regulators view next-generation platforms as incremental improvements rather than risks [1]Source: Prime Medicine, “PM359 IND Clearance,” primemedicine.com . Intellia Therapeutics advanced two candidates to Phase 3 simultaneously, underscoring the confidence provided by prior approvals. Pricing pressure remains, as the USD 2 million per-dose list price of Casgevy has intensified the hunt for delivery and manufacturing efficiencies.

Advances in Delivery Technologies (Viral and Non-Viral)

Tissue-specific capsid engineering has produced vectors like Sangamo’s STAC-BBB, which delivers 700-fold more transgene across the blood-brain barrier than AAV9 and opens lucrative neurology indications. Lipid nanoparticles, refined during COVID-19 vaccine production, now package CRISPR cargos for in-vivo cardiovascular applications at CRISPR Therapeutics. A USD 95 million strategic investment by Regeneron into Mammoth Biosciences targets ultracompact nucleases that fit within viral payload limits while cutting immunogenicity risks. Hybrid systems that marry targeted viral vectors with scalable synthetic carriers are under evaluation to widen organ reach and ease manufacturing bottlenecks.

Rising R&D Funding and Strategic Partnerships

Vertex expanded its collaboration with CRISPR Therapeutics through a USD 175 million upfront and milestones up to USD 1 billion to pursue Duchenne and myotonic dystrophy programs. Genentech placed USD 50 million upfront with Sangamo, potentially rising to USD 1.9 billion, for neurological disease assets deploying proprietary AAV capsids. Collaboration formats now emphasize co-development to share regulatory and manufacturing infrastructure, demonstrated by the CRISPR Therapeutics–Nkarta alliance for edited NK-cell therapies. Cash-constrained biotechs benefit from these structures while pharmaceutical backers gain optionality in precision-medicine pipelines.

AI-Driven sgRNA Design Accelerates Time-to-Lead

Machine-learning models such as PAMmla can predict on- and off-target outcomes across thousands of potential guide RNAs, cutting the design cycle to weeks and lowering lab reagent consumption significantly. The approach is moving into commercial pipelines; Agilent embeds AI optimisation in its sgRNA kit workflow that feeds directly into clinical-grade manufacturing, shortening the pre-clinical timeline. Agricultural developers employ similar analytics to stack climate-resilient traits while navigating evolving regulatory matrices in the United States, China, and Brazil. In therapeutics, end-to-end AI platforms are now integrating guide design with delivery carrier optimisation, a convergence that promises bespoke treatments on accelerated schedules.

Restraint Impact Analysis*

| Restarint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Off-target safety & ethical concerns | -2.4% | Global, with EU most restrictive | Long term (≥ 4 years) |

| High CMC & manufacturing cost structure | -1.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Supply-chain concentration in Cas nucleases | -1.2% | Global, with US dependency concerns | Short term (≤ 2 years) |

| Public backlash over gene-drive ecology risk | -0.9% | North America & EU, agricultural focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Off-Target Safety and Ethical Concerns

Regulators require multi-layer detection assays for unintended edits because permanent changes cannot be reversed in vivo, extending pre-clinical development and adding cost. Studies citing myocardial infarction and stroke signals in early immuno-oncology trials have heightened vigilance, with European agencies adopting especially conservative positions for central-nervous-system targets. Ethical debate also surrounds gene-drive proposals for pest control, spilling over into human-health applications and clouding public perception in some regions. Base and prime editing aim to mitigate risk by avoiding double-strand breaks, but multi-year safety datasets will be needed before regulators relax current guardrails

High CMC and Manufacturing Cost Structure

Autologous cell treatments require personalised processing in Grade C cleanrooms, a major driver of the >USD 2 million per-patient sticker price for the first CRISPR therapy. Over 75% of Cas nuclease supply comes from facilities outside the United States, leaving developers vulnerable to freight delays and quality variability. CDMOs are installing modular suites to meet demand, yet capacity remains limited; top providers are booked 12-18 months ahead for large-scale viral vector runs. Allogeneic “off-the-shelf” approaches may lower costs, but they require extra edits to evade immune rejection, adding complexity and regulatory scrutiny that partly offsets manufacturing efficiencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component - Products Drive Current Revenue

Products controlled 78.45% of total revenue in 2025, reflecting sustained demand for guide RNA kits, Cas enzymes, and transfection reagents used across discovery and translational workflows. Thermo Fisher and Merck KGaA offer catalogue reagents that scale with research throughput, underpinning a predictable revenue base that buffers volatility in therapeutic milestones. Services are pacing at a 14.12% CAGR as biotech clients outsource assay development, cell-line engineering, and GMP viral-vector production to specialist CROs. Charles River Laboratories positions itself as an end-to-end partner from discovery to Phase I manufacturing, mirroring a broader shift in the CRISPR and CRISPR-associated (CAS) genes market toward integrated external capabilities.

Growing therapeutic pipelines multiply demand for process development, quality control, and regulatory documentation, lifting service penetration every year of the forecast. Suppliers are bundling reagents, delivery vectors, and analytics software into platform packages to secure switching costs and capture a larger slice of downstream value.

By Application - Biomedical Dominance Faces Agricultural Disruption

Biomedical programs generated 81.40% of 2025 revenue, sustained by high-value therapies, companion diagnostics, and drug discovery screens that command premium pricing and long-term partnerships. The implicit risk profile is balanced by strong venture capital support and expanding orphan-disease incentives. Agriculture, growing at 15.18% CAGR, benefits from streamlined regulation in the United States where gene-edited plants that could be derived through conventional breeding skip protracted environmental assessments, slashing the time to market and expanding farmer.

China’s 2025 guidance encouraging biotech cultivation of wheat, corn, and soy is set to unlock additional volume and reinforce the Asia-Pacific growth story. Synthetic biology use cases such as bio-production of specialty chemicals represent a nascent yet promising niche, though current revenue remains modest. Cross-fertilisation of knowledge between therapeutic and agricultural segments accelerates platform evolution, particularly around delivery vectors and computational design, deepening the overall CRISPR industry ecosystem.

By Technology - Prime Editing Challenges Cas9 Supremacy

CRISPR-Cas9 retained 61.85% share in 2025, anchored by extensive validation data and established manufacturing know-how that simplifies regulatory interactions. The CRISPR and CRISPR-associated (CAS) genes market now prizes precision; prime editing is achieving a 15.76% CAGR because it edits without double-strand breaks, alleviating safety hurdles that plague nuclease-based systems. Base editing occupies a middle ground, combining improved specificity with simpler reagent composition, and is moving into late-stage trials such as Beam's BEAM-302 for alpha-1 antitrypsin deficiency. Novel Type I-D CRISPR systems from Japanese research groups illustrate ongoing diversification, with long guide RNAs that broaden accessible genomic regions and reduce off-target cuts.

Developers choose technologies based on tissue target, therapeutic index, and intellectual-property landscape rather than familiarity, so each platform must demonstrate unique value to secure share. The CRISPR and CRISPR-associated (CAS) genes market size attributable to prime editing therapies could expand significantly after PM359 human proof-of-concept, which would validate the platform for dozens of monogenic diseases.

By End User - CROs Capture Outsourcing Wave

Biotechnology and pharmaceutical companies generated 67.70% of 2025 revenue by advancing proprietary therapeutic candidates through in-house research, yet capacity constraints in manufacturing and analytics fuel outsourcing momentum. CROs and CDMOs are scaling faster than any other group at 14.74% CAGR as they absorb specialised tasks such as GMP vector production, in-vivo model generation, and regulatory dossier preparation. Academic institutes hold a steady share as foundational discovery engines but are also spinning out start-ups that later partner with industry for development resources.

The trend mirrors post-pandemic supply-chain recalibration in which companies reserve scarce internal talent for strategic decision-making while entrusting operational execution to partners with purpose-built capacity. Integrated service providers that can bundle design, build, test, and manufacture into a single workflow gain competitive advantage and deepen client lock-in, reinforcing consolidation within the service tier of the CRISPR and CRISPR-associated (CAS) genes market.

By Delivery Method - Non-Viral Innovation Accelerates

AAV vectors dominate current approvals because decades of safety data reassure regulators and investors, yet their 4.7-kb payload ceiling constrains complex edits like prime or multiplex base editing. Lipid nanoparticles sidestep size limits and immunogenicity but have historically struggled with tissue specificity; recent chemistry iterations now enable myocardium and central nervous system targeting, broadening the commercial scope. Electroporation and nanoparticle carriers show promise for ex-vivo cell work, facilitating high edit rates with minimal cell toxicity.

Hybrid constructs that combine capsid targeting with synthetic-carrier scalability are being aggressively funded by large pharmaceutical companies such as Regeneron because they offer a path toward repeat dosing and broader tissue reach. Delivery modality will remain a key deciding factor for clinical success, meaning suppliers with robust vector IP can capture outsized value in the CRISPR and CRISPR-associated (CAS) genes market.

Geography Analysis

North America retained leadership with 47.10% revenue in 2025 thanks to FDA clarity, deep venture capital pools, and concentration of specialised talent in Boston and the San Francisco Bay Area. The region further benefits from USDA rules that treat certain gene-edited crops like conventionally bred varieties, supporting diversified revenue streams beyond therapeutics. Cost pressure and manufacturing bottlenecks create incentives for firms to establish production sites in lower-cost jurisdictions, slightly tempering growth yet maintaining strategic centrality through 2030.

Asia-Pacific posts the fastest CAGR at 15.89%, led by China’s strong state financing, a large talent base, and more than 700 active CRISPR clinical trials that now outnumber those in the United States. Policy initiatives like Japan’s Smart Cell Project aim to commercialise gene-engineered cellular factories for pharma and industrial applications, reinforcing a region-wide pivot to high-value biomanufacturing. India wrestles with restrictive licensing regimes that limit farmers’ adoption of CRISPR crops, underscoring the importance of intellectual-property frameworks in shaping local trajectories.

Europe holds significant scientific prowess but lags in commercialisation because gene-edited organisms fall under the same stringent rules as traditional GMOs, stretching approval timelines and raising compliance costs. Consequently many European firms conduct clinical trials in North America or Asia while maintaining R&D bases at home.

Latin America, the Middle East, and Africa remain emergent; regulatory frameworks are still evolving and healthcare spending is lower, yet early adoption in Brazil’s agritech sector suggests future opportunity once global supply chains mature and local policy aligns with scientific progress.

Competitive Landscape

The CRISPR and CRISPR-associated (CAS) genes market is moderately fragmented; the top five pure-play developers together hold well under a quarter of total revenue, while tool suppliers and service platforms capture diverse niches. CRISPR Therapeutics, Editas Medicine, Intellia Therapeutics, and Beam Therapeutics each focus on differentiated technology stacks—ranging from allogeneic CAR-T cells to base and prime editing—and augment pipelines through large-pharma partnerships. Tool providers such as Thermo Fisher and Merck KGaA capitalise on early-stage demand but observe rising competition from start-ups offering integrated reagent-plus-software suites. Delivery specialists Mammoth Biosciences and Scribe Therapeutics occupy a critical chokepoint by supplying ultracompact Cas variants adaptable to diverse vectors.

Strategic moves in 2024-2025 show partnerships surpassing outright acquisitions in frequency as both sides prefer risk-sharing. Regeneron’s USD 370 million-per-target collaboration with Mammoth seeks to combine compact nucleases with proprietary lipid nanoparticles, exemplifying how delivery IP attracts investment. Vertex’s expanded alliance with CRISPR Therapeutics broadens focus from hematology into neuromuscular diseases, indicating that platform breadth is a coveted asset. Intellectual-property disputes linger in agriculture; broad patents held by academic consortia oblige emerging-market firms to license or partner to secure freedom to operate, as seen in India’s protracted negotiations on seed-trait licensing.

Looking ahead, competitive advantage will accrue to companies that can simultaneously master delivery, reduce manufacturing cost, and demonstrate long-term safety. Those outcomes require capital intensity and multidisciplinary expertise, implying that collaboration will remain the default pathway to scale within the CRISPR and CRISPR-associated (CAS) genes market.

CRISPR And CRISPR-associated (Cas) Genes Industry Leaders

OriGene Technologies, Inc.

Thermo Fisher Scientific

Takara Bio Inc

Addgene

PerkinElmer Inc. (Horizon Discovery Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CRISPR Therapeutics reported Phase 1 data for CTX310 showing triglyceride reductions up to 82% and held USD 1.86 billion in cash

- May 2025: Sangamo Therapeutics priced a USD 23 million equity offering to fund neurology-focused AAV capsid programs

- April 2025: Beam Therapeutics released new BEAM-302 data showing 91% corrected protein in alpha-1 antitrypsin deficiency patients

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the CRISPR and CRISPR-associated genes market as all commercial products and fee-based services that employ CRISPR nuclease systems (Cas9, Cas12, Cas13, base and prime editors) for genome editing, screening, diagnostics, or cell-line engineering across human health, agriculture, and industrial biology. According to Mordor Intelligence, the business is valued at USD 4.70 billion in 2025 and is tracked through five core components: reagents and kits, enzymes, guide-RNA tools, libraries, and contract services.

Scope Exclusion: We do not count revenues from non-CRISPR genome editors such as TALEN or zinc-finger nuclease platforms.

Segmentation Overview

- By Component

- Products

- Services

- By Application

- Biomedical

- Agriculture

- Industrial & Synthetic Biology

- By End User

- Biotechnology & Pharmaceutical Cos.

- Academic & Government Institutes

- Contract Research / Manufacturing Orgs.

- By Technology Type

- CRISPR-Cas9

- Base Editing

- Prime Editing

- CRISPR-Cas12/13 & Others

- By Delivery Method

- Viral Vectors

- Non-viral (LNPs, Electroporation, Nanocarriers)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview bench scientists, CRISPR tool suppliers, CDMO executives, clinical investigators, and ag-biotech regulators across North America, Europe, and Asia-Pacific. The conversations validate input prices, kit consumption rates, editing success ratios, and expected therapeutic uptake, closing gaps left by desk research.

Desk Research

We start with publicly available data from tier-1 authorities such as the US NIH RePORTER grant database, FDA biologics approval logs, WHO International Clinical Trials Registry, USDA and EFSA crop approval files, OECD patent statistics, and IMF price series, which give foundational volume, adoption, and price cues. Additional context is gathered from peer-reviewed journals, trade association white papers (e.g., BIO, EuropaBio), and company 10-K filings, then enriched through paid resources like D&B Hoovers for firm-level revenue splits and Dow Jones Factiva for global deal flow.

Production trade flows for key reagents are further triangulated through Volza shipment data and Questel patent landscaping, helping us verify whether reported capacity expansions translate into export growth.

This list is illustrative; many other statistical portals, investor decks, and regulatory notices are reviewed before numbers are locked.

Market-Sizing & Forecasting

We apply a top-down model that rebuilds global demand from research funding outlays, clinical pipeline counts, agricultural trait approvals, and diagnostic kit shipments, which are then pressure-tested with selective bottom-up checks such as average selling price multiplied by estimated reagent volumes for frequently ordered sgRNA kits. Key drivers in the model include NIH and Horizon Europe grant pools, the number of CRISPR IND filings, crop genome-edited acreage, and kit ASP trends. Forecasts run through multivariate regression and ARIMA smoothing, with scenario buffers for regulatory shifts and off-target safety data.

Data Validation & Update Cycle

Outputs move through two rounds of analyst review where anomalies are flagged against external benchmarks; material variances trigger re-contacts. Models refresh each year, and interim updates follow major approvals or funding inflections before the report is shipped.

Why Mordor's CRISPR & CRISPR-associated Genes Baseline Underpins Sound Strategic Decisions

Published estimates often diverge; firms vary in what they count, the currencies they use, and how frequently they refresh, which leaves executives unsure which figure to trust.

Main gap drivers include broader product baskets in some studies, limited primary verification of ASP drift, reliance on static currency rates, and refresh cycles that skip recent therapy approvals. Our team's annual cadence and mixed-method validation tighten those levers, so decision-makers start from a steadier midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.70 B (2025) | Mordor Intelligence | - |

| USD 5.36 B (2025) | Global Consultancy A | Wider inclusion of sequencing consumables; minimal primary interviews; update every two years |

| USD 3.21 B (2025) | Trade Journal B | Focus on core reagents only; top-down revenue splits; conservative clinical adoption assumptions |

Differences aside, the comparison shows that our disciplined scope choices, yearly refresh, and cross-check routines deliver a balanced, transparent baseline that investors and planners can reproduce with clear variables and repeatable steps.

Key Questions Answered in the Report

What is the expected value of the CRISPR and CRISPR-associated (CAS) genes market in 2031?

The CRISPR and CRISPR-associated (CAS) genes market is projected to reach USD 10.13 billion by 2031, growing at a 13.67% CAGR.

Which segment is growing fastest within the CRISPR and CRISPR-associated (CAS) genes market?

Agricultural applications hold the highest growth rate, expanding at a 15.18% CAGR through 2031 due to streamlined crop regulations.

Why is prime editing attracting investor attention?

Prime editing delivers precise gene corrections without double-strand breaks, addressing off-target safety concerns and achieving the fastest 15.76% CAGR in the technology segmentation.

How significant is Asia-Pacific to future CRISPR and CRISPR-associated (CAS) genes market expansion?

Asia-Pacific records a 15.89% CAGR and benefits from strong governmental backing in China and innovation programs in Japan, making it the quickest-growing regional market.

What are the main barriers to widespread CRISPR therapeutic use?

Off-target safety concerns and high manufacturing costs constitute the primary restraints, reducing the projected CAGR by 2.4% and 1.8%, respectively.

Page last updated on: