Scleral Lens Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

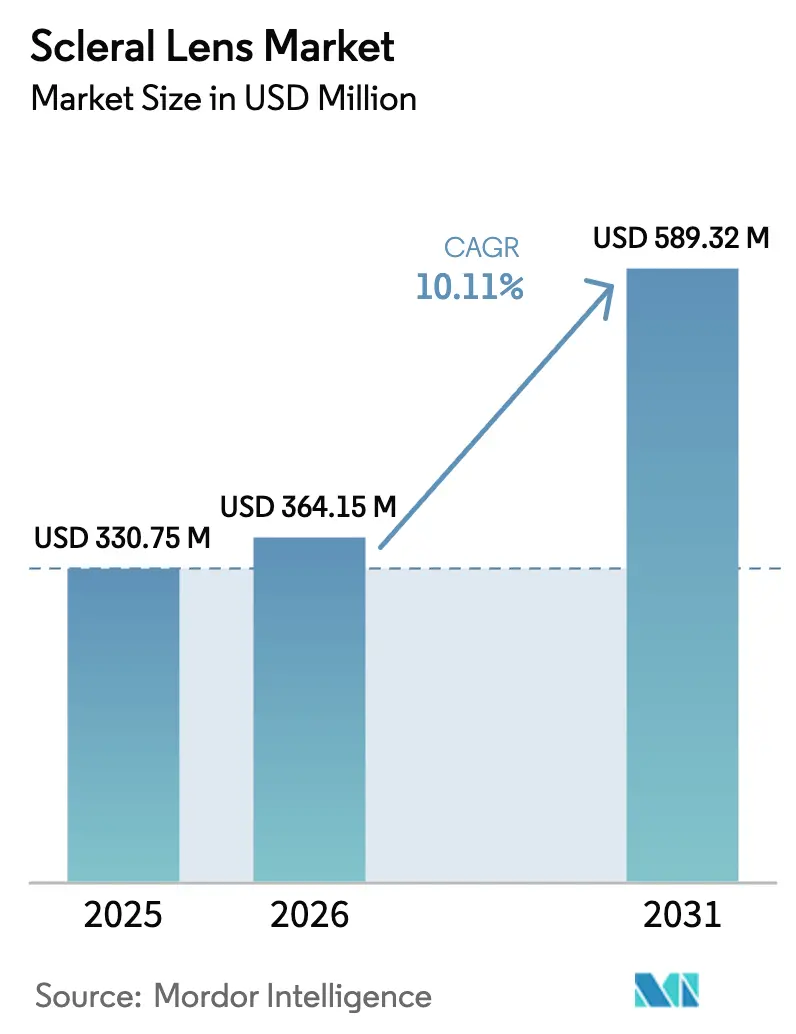

| Market Size (2026) | USD 364.15 Million |

| Market Size (2031) | USD 589.32 Million |

| Growth Rate (2026 - 2031) | 10.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scleral Lens Market Analysis by Mordor Intelligence

The Scleral Lens Market size was valued at USD 330.75 million in 2025 and estimated to grow from USD 364.15 million in 2026 to reach USD 589.32 million by 2031, at a CAGR of 10.11% during the forecast period (2026-2031). Increasing clinical acceptance of scleral lenses for complex corneal disorders, rapid material science innovation in high-oxygen-permeable polymers, and greater practitioner proficiency are fueling demand. Growing pediatric keratoconus detection, expanding drug-eluting lens pipelines, and the emergence of 3-D printing for bespoke devices further reinforce momentum. North American reimbursement policies and specialty fitters underpin current revenue leadership, while Asia-Pacific’s accelerating practitioner training drives the fastest uptake. Heightened investment in digital fitting platforms and supply-chain resilience for fluorosilicone acrylate compounds will likely influence competitive strategy across the scleral lens market.

Key Report Takeaways

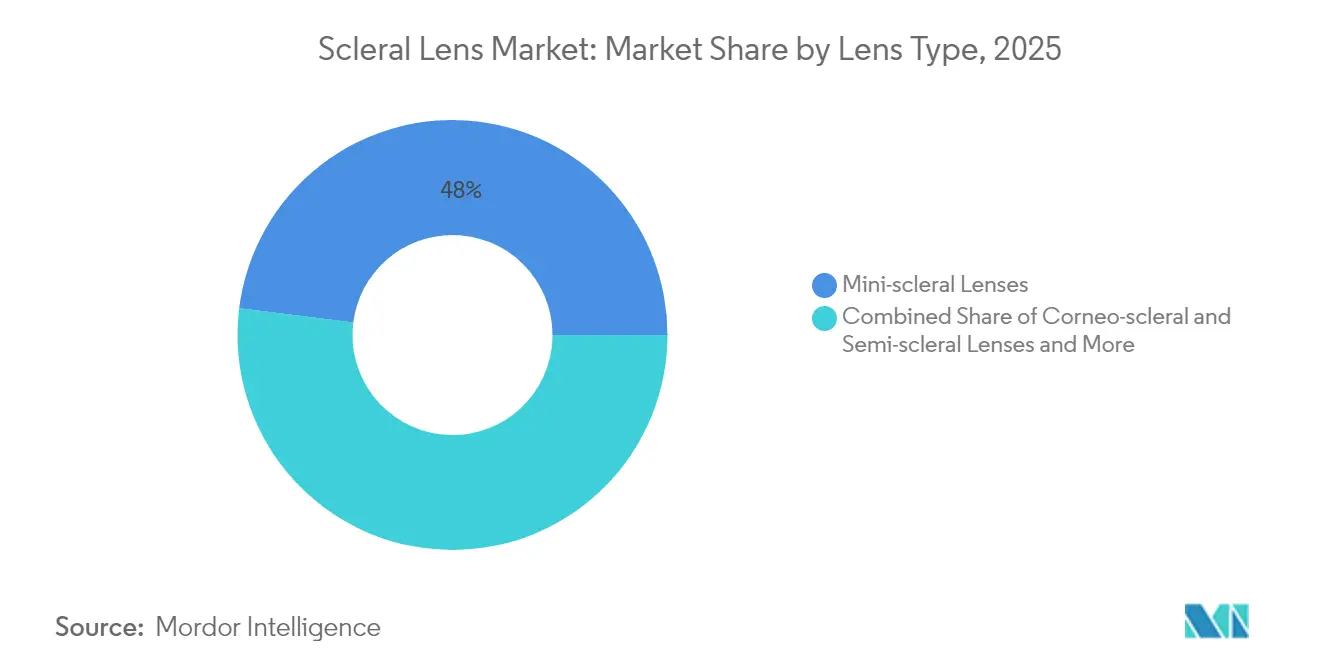

- By lens type, mini-scleral lenses held 48.02% of scleral lens market share in 2025, whereas full scleral lenses are forecast to grow at a 14.05% CAGR through 2031.

- By application, irregular cornea indications commanded 62.06% share of the scleral lens market size in 2025; ocular surface disease applications are advancing at a 16.39% CAGR to 2031.

- By end user, hospitals led with 37.68% revenue share in 2025, while eye clinics are poised for a 13.98% CAGR through 2031.

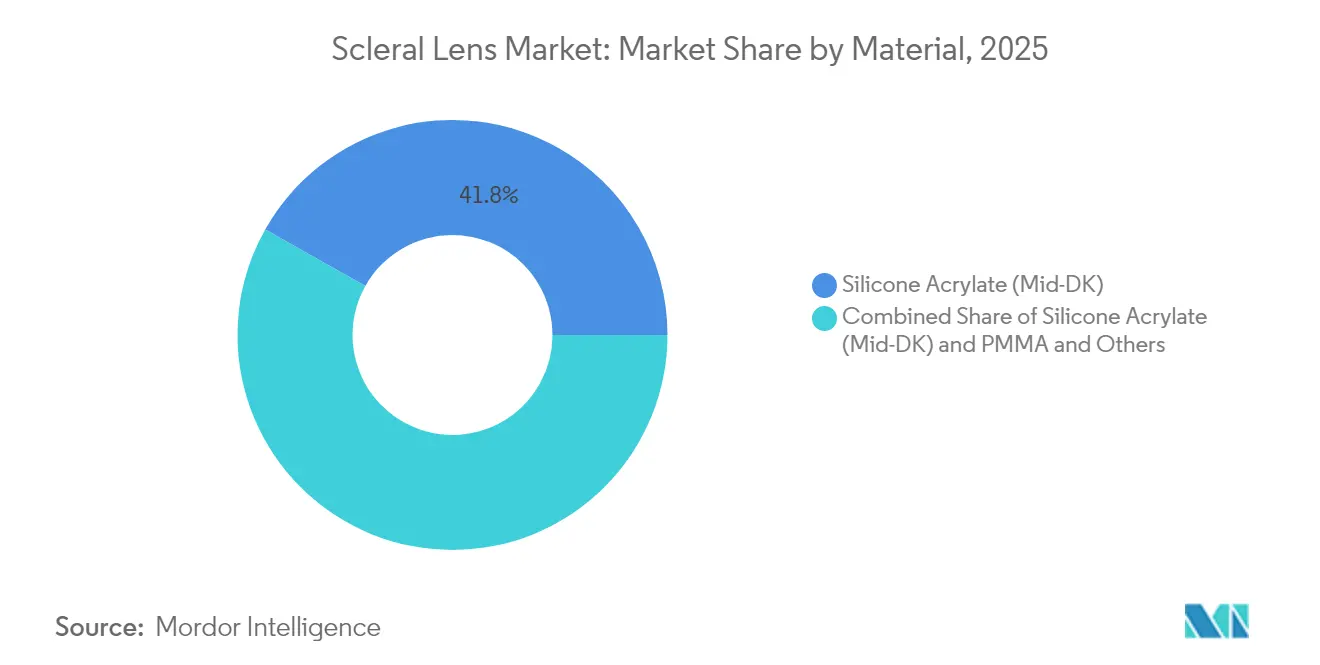

- By material, silicone acrylate captured 41.83% share of the scleral lens market in 2025; fluoro-silicone acrylate materials are projected to expand at 12.55% CAGR by 2031.

- By distribution channel, offline outlets accounted for 71.55% of the scleral lens market size in 2025; online channels exhibit a robust 15.92% CAGR forecast to 2031.

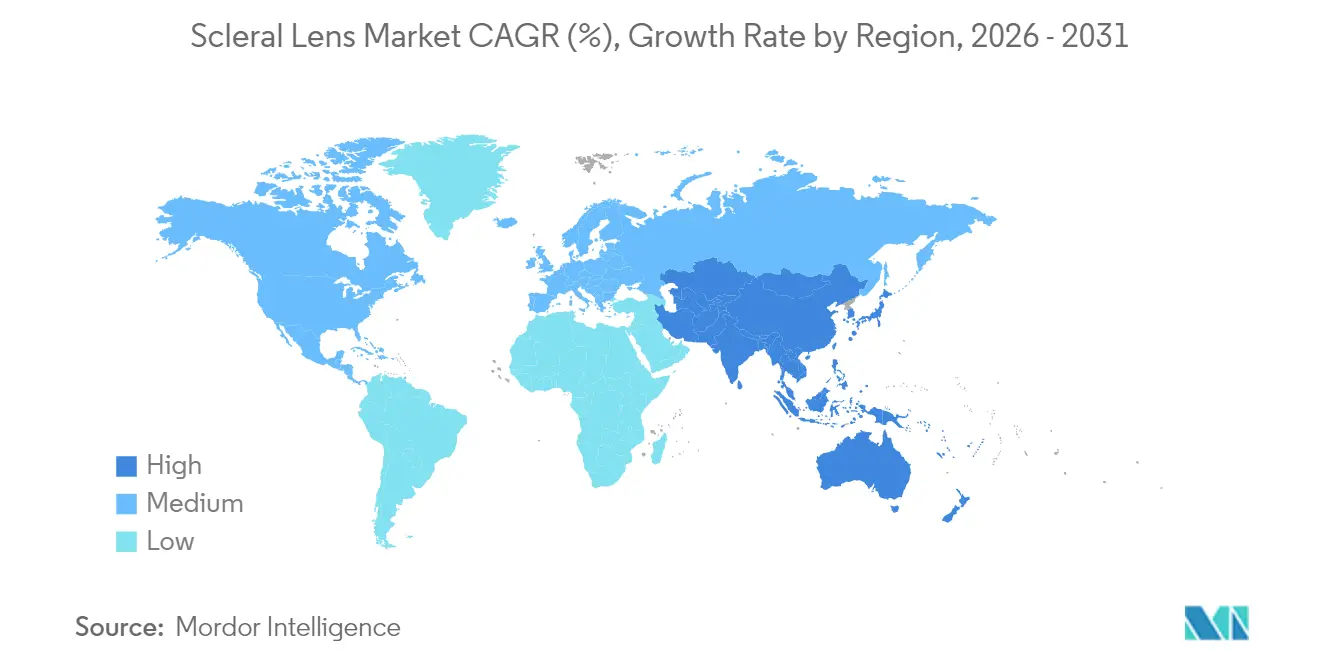

- By geography, North America secured 42.34% of global revenue in 2025, whereas Asia-Pacific is projected to post a 15.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Scleral Lens Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Keratoconus & Ectatic Disorders | +2.8% | Global, with highest impact in APAC and North America | Medium term (2-4 years) |

| Growing Number Of Post-Refractive-Surgery Complications | +1.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Increasing Global Adoption By Specialty Eye-Care Chains | +1.6% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Advancements In High-DK GP Materials | +1.4% | Global | Long term (≥ 4 years) |

| Emergence Of 3-D Printed Customised Scleral Lenses | +1.2% | North America & EU, early adoption | Long term (≥ 4 years) |

| Drug-Eluting Scleral Lenses In Late-Stage Pipelines | +0.8% | Global, regulatory-dependent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Keratoconus & Ectatic Disorders

Large-scale pediatric screening now reports a 1:334 keratoconus incidence, a rate far higher than historical adult-only estimates. Earlier diagnosis means more patients require lifelong visual rehabilitation, and long-term studies show that scleral lenses reduce corneal transplant risk by 81% compared with no lens use. National health systems increasingly endorse early lens fitting to delay or avert surgery, reinforcing steady demand across the scleral lens market. Improved tomography tools make detection routine in primary eye care, expanding patient pools. Correspondingly, specialty practitioners are integrating first-line scleral lens protocols to manage progression and enhance quality of life.

Advancements in High-DK GP Materials

Next-generation gas-permeable materials surpassing 200 Dk have alleviated hypoxia concerns that once limited daily wear durations. Valley Contax’s Acuity 200 polymer combines ultrahigh oxygen transmission with surface wettability that diminishes deposit formation, extending comfortable wear time[1]Valley Contax, “Acuity 200 – Welcome to the World of GP Materials,” valleycontax.com. Such materials permit thicker vaults for severe ectasias without compromising corneal physiology, broadening treatable cases within the scleral lens market. Research into hydrogel composites achieving super-lubricity further lowers friction-induced dropout risk. Computational material design accelerates iteration, speeding commercialization and helping manufactures differentiate premium portfolios.

Emergence of 3-D Printed Customised Scleral Lenses

Additive manufacturing now fabricates clinical-grade lenses with micron-level precision, tailoring sagittal depths to individual ocular profiles. Peer-reviewed work on 3-D-printed drug-releasing contact lenses underscores the technology’s viability for ocular devices[2]Piyush Garg et al., “3D-Printed Contact Lenses to Release Polyvinyl Alcohol,” MDPI Journals, mdpi.com. Automated printers reduce manual polishing steps, potentially cutting practitioner chair time and trimming per-lens costs. Custom lattice structures enable variable thickness zones that optimize oxygen diffusion while preserving rigidity. While scaling output remains challenging, investment in industrial printers suggests broader availability within the forecast window, opening new growth pockets for the global scleral lens market.

Drug-Eluting Scleral Lenses in Late-Stage Pipelines

Combining vision correction with sustained therapeutic delivery tackles entrenched adherence problems of topical drops, where less than 5% of drug reaches target tissues. Early clinical programs using cyclosporine-impregnated scleral lenses have reported stable 24-hour release profiles and symptomatic relief for severe dry eye. Regulatory pathways for combination device-drug products demand extensive safety data, but positive pilot results strengthen investor confidence. Commercial roll-out is expected first in niche ocular surface diseases, then progressively in glaucoma and post-surgical inflammation, expanding addressable revenue streams across the scleral lens market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability Of Alternative Techniques | -1.8% | Global, with highest impact in developed markets | Medium term (2-4 years) |

| High Chair-Time & Learning Curve For Practitioners | -1.5% | Global, particularly in emerging markets | Short term (≤ 2 years) |

| Limited Oxygen Delivery In Very Long-Term Wear | -1.2% | Global | Long term (≥ 4 years) |

| Supply-Chain Fragility In Fluorosilicone Acrylate Polymers | -0.9% | Global, with highest impact in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative Techniques

Advances in corneal cross-linking, intrastromal ring segments, and small-incision lenticule extraction offer non-contact-lens solutions for irregular corneas. Patients seeking minimally invasive correction may opt for these procedures despite higher cost, limiting conversion to the scleral lens market. Public and private insurers in several developed nations now reimburse ring implant surgery, narrowing the economic gap with specialty lenses. Device makers respond by highlighting reversible, adjustable benefits of scleral modalities, yet competition from surgical technologies persists over the medium term.

High Chair-Time & Learning Curve for Practitioners

Initial scleral lens fitting often requires 2-4 hours versus under one hour for soft lenses, straining busy primary care schedules. Surveys indicate many optometrists need six months of dedicated training to consistently achieve optimal vaults. Limited access to tomography and profilometry in smaller clinics further elevates barriers, especially in developing economies where capital budgets are restricted. Manufacturers increasingly bundle virtual certification courses and predictive fitting software to shorten onboarding, but retention of new skills still hinges on sustained case volume. These workflow challenges continue to temper adoption across the scleral lens market, particularly outside major urban centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lens Type: Mini-Scleral Dominance Drives Market

Mini-scleral designs captured 48.02% of global revenue in 2025, making them the cornerstone of the scleral lens market. Their 15–18 mm diameter provides reliable corneal vaulting with easier handling than larger formats, supporting widespread clinical use. The segment benefits from incremental design refinements such as toric haptics that boost first-fit success rates. Full scleral lenses, though currently niche, are projected to grow at a 14.05% CAGR as severe ocular surface disease cases rise. Increased availability of high-DK materials encourages broader full-scleral adoption, especially for postoperative and graft patients requiring maximal protection. Corneo-scleral hybrids sustain a modest share, serving mild ectasia and post-LASIK irregularities where central clearance demands are lower. Continuous R&D in edge alignment algorithms and surface coatings sustains product differentiation.

The scleral lens market size contribution from mini-scleral products will remain dominant through 2031 as manufacturing efficiencies keep prices stable. Companies bundle trial sets with digital fitting tools, reducing chair time and underpinning practitioner loyalty. Patient word-of-mouth and social media testimonials further lift awareness, reinforcing structural growth. Adoption of full scleral formats in tertiary centers acts as a feeder pipeline, with some wearers transitioning to mini designs once corneal surfaces stabilize. On balance, lens type diversity enhances market resilience, limiting revenue concentration risk.

By Application: Irregular Cornea Applications Lead Market

Irregular cornea indications accounted for 62.06% of the scleral lens market share in 2025. Keratoconus, pellucid marginal degeneration, and post-refractive ectasia dominate prescription volumes because alternative corrections offer limited visual quality for complex topographies. Longitudinal data confirm that early scleral lens use delays transplant surgery and supports stable visual acuity, encouraging payer acceptance. Ocular surface disease, while smaller today, is forecast to post a 16.39% CAGR as evidence grows for therapeutic hydration benefits in severe dry eye and graft-versus-host disease. This segment draws clinician attention in aging societies where autoimmune and iatrogenic dryness escalate.

The scleral lens market size linked to refractive error correction remains modest but strategically important. Ultra-precise wavefront-guided optics allow correction of high-order aberrations in post-LASIK or trauma cases unmet by spectacles. Emerging drug-eluting platforms could create new hybrid indications such as combined visual and anti-inflammatory therapy. Cross-functional clinical trials are expanding knowledge on cost-effectiveness, which may eventually bring broader insurer coverage and lift application diversity.

By End User: Hospital Dominance Shifts Toward Specialized Clinics

Hospitals represented 37.68% of 2025 revenue, reflecting the need for multidisciplinary teams to manage complex corneal pathology. Integrated surgical and fitting services cater to patients with grafts, advanced ectasia, or ocular surface compromise. However, independent eye clinics are registering a 13.98% CAGR, propelled by targeted training programs and investment in corneal tomography. These centers offer flexible scheduling and personalized follow-up, appealing to younger and working-age demographics. Tele-consultation links between community optometrists and tertiary specialists further democratize access, enlarging the scleral lens market.

Academic centers and research hospitals serve as innovation hubs, trialing adaptive optics and AI-driven fitting algorithms that eventually diffuse to private practice. Practitioner associations disseminate protocols, raising baseline competence across geographies. As clinics scale, manufacturers supply turnkey fitting suites, reinforcing symbiotic growth between device vendors and outpatient providers.

By Material: Silicone Acrylate Leads Despite High-DK Growth

Silicone acrylate maintained 41.83% global revenue share in 2025, underscoring its balance of oxygen permeability, rigidity, and cost efficiency. The segment’s adoption benefits from decades of clinician familiarity and stable supply chains. High-DK fluoro-silicone acrylate materials, however, are expanding at 12.55% CAGR as they enable extended wear schedules and accommodate thicker vaults without compromising corneal physiology. Breakthrough super-hydrophilic coatings reduce fogging and protein build-up, improving long-term comfort. PMMA’s footprint continues to recede but holds value in specialty cases demanding extreme dimensional stability.

Investment in R&D centers on polymer blends surpassing 200 Dk while preserving mechanical strength. Success in this arena could trigger accelerated migration toward premium materials, reshaping the scleral lens market size distribution by 2031. Producers are forging strategic alliances with raw-material suppliers to secure fluorosilicone acrylate inventories, mitigating recent supply-chain shocks.

By Distribution Channel: Offline Dominance Faces Digital Disruption

Offline channels in optometry and ophthalmology practices generated 71.55% of 2025 global sales, reflecting the highly customized nature of fittings. Nonetheless, online platforms are expected to climb at a 15.92% CAGR as tele-optometry gains regulatory acceptance. Digital refills, virtual check-ups, and subscription models enhance patient convenience, lifting compliance and retention rates in the scleral lens market. Hybrid delivery frameworks emerge, whereby initial fitting occurs in-clinic and subsequent lens reorders shift online. Several manufacturers now integrate QR-coded care guides and AI symptom trackers, driving seamless omni-channel experiences. While fully remote fittings remain limited by liability and data-accuracy constraints, incremental digitalization is likely to narrow the gap between clinical supervision and consumer expectations.

Geography Analysis

North America contributed 42.34% of global revenue in 2025 owing to mature specialty eye-care infrastructure, advanced insurance coverage, and continuous practitioner education. Canada’s single-payer model and Mexico’s private insurance expansion diversify regional growth drivers. Increased availability of high-DK materials supports longer wear schedules, broadening indication scope.

Asia-Pacific is the fastest-growing territory with a projected 15.02% CAGR, propelled by widespread adoption in urban hospitals and proliferating specialty chains. China and India together account for the largest prospective patient pools as pediatric screening initiatives uncover understudied keratoconus prevalence. Government-supported capacity-building programs train new fitters, elevating baseline service availability across the scleral lens market. Local manufacturing facilities in Malaysia and Singapore shorten supply lead times and insulate against currency volatility.

Europe maintains steady mid-single-digit expansion backed by established optometry programs and consistent CE-mark regulations. Germany and the United Kingdom dominate regional volumes through academic-industry collaborations that fast-track clinical innovation. Southern European markets witness rising demand as public health systems emphasize non-surgical management of ectasia. Post-Brexit regulatory realignments introduce mild friction in cross-border supply chains, yet manufacturers re-route inventory to maintain continuity. Overall, region-wide adherence to evidence-based reimbursement guidelines secures predictable adoption trajectories.

Competitive Landscape

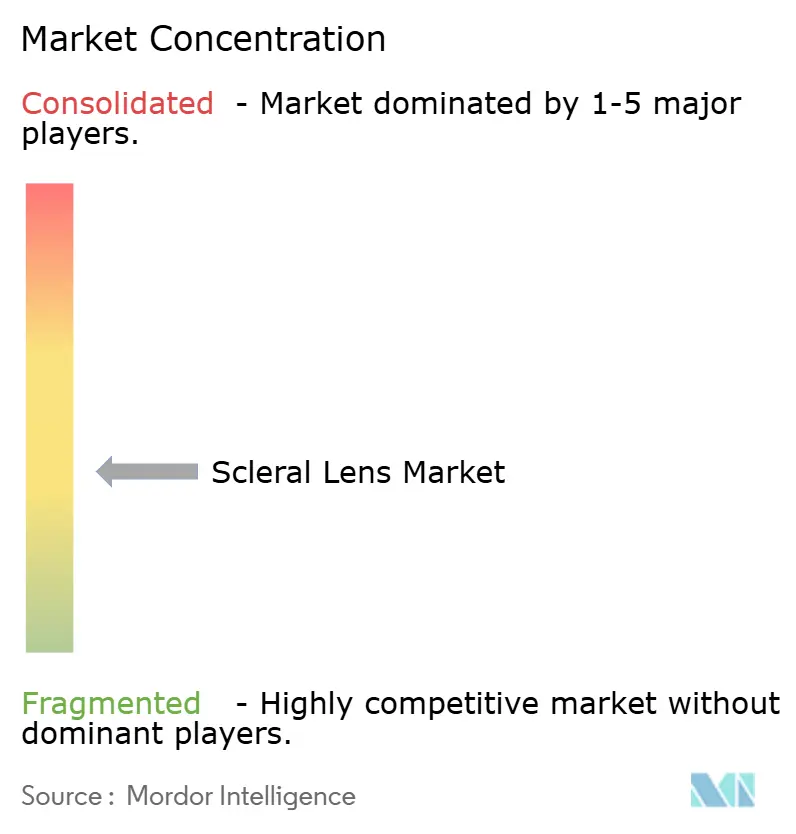

The scleral lens market is moderately fragmented. Established multiproduct groups—Bausch + Lomb, CooperVision, and Alcon—leverage economies of scale and international distribution, while pure-play specialists such as BostonSight, Visionary Optics, and Art Optical build loyalty through bespoke design platforms. Competitive differentiation centers on proprietary fitting software, ultrahigh-DK material access, and embedded practitioner training ecosystems.

Investment in artificial-intelligence-guided sagittal depth prediction reduces refit rates and elevates first-lens success, sharpening competitive edges. Alcon’s USD 356 million acquisition of LENSAR underscores a strategy to integrate diagnostics and refractive technology into a unified portfolio[3]Alcon, “Alcon Agrees to Acquire LENSAR, Inc.,” alcon.com. EssilorLuxottica’s 2024-2025 med-tech acquisitions of Heidelberg Engineering and Espansione Group signal similar vertical integration to capture data analytics and therapeutic device synergies.

Supply security for fluorosilicone acrylates becomes a battleground advantage; manufacturers with dual-source procurement hedge against volatility and protect production timelines. Start-ups focusing on 3-D printed or drug-eluting formats draw venture capital, positioning themselves as take-over targets once proof-of-concept trials conclude. Overall, tactical collaboration between raw-material chemists, software developers, and clinical educators shapes future competitive contours across the scleral lens market.

Scleral Lens Industry Leaders

Visionary Optics

ABB Optical Group

EssilorLuxottica

Bausch + Lomb

Art Optical Contact Lens

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bausch + Lomb introduced Zenlens CHROMA HOA wavefront-guided scleral lenses in the United States to correct higher-order aberrations.

- January 2025: EyePrint Prosthetics, Advanced Vision Technologies, and WAVE Contact Lens System merged operations to form WAVE Eye Care, specializing in fully customized scleral devices.

Global Scleral Lens Market Report Scope

Scleral contacts are large-diameter gas permeable contact lenses specially designed to vault over the entire corneal surface and rest on the sclera. These lenses functionally replace the irregular cornea with a perfectly smooth optical surface to correct vision problems caused by keratoconus and other corneal irregularities. The scleral lens market is segmented by Type (Corneo-Scleral Lenses and Semi-Scleral Lenses, Mini-Scleral Lenses, and Full Scleral Lenses), Application (Irregular Cornea, Ocular Surface Disease, Refractive Error, and Other Applications), End User (Hospitals, Eye Clinics, and Other End Users), and Geography (North America, Europe, Asia-Pacific and Rest of World). The report offers the value (in USD million) for the above segments.

| Corneo-scleral & Semi-scleral Lenses |

| Mini-scleral Lenses |

| Full Scleral Lenses |

| Irregular Cornea |

| Ocular Surface Disease |

| Refractive Error |

| Other Applications |

| Hospitals |

| Eye Clinics |

| Other End Users |

| Fluoro-silicone Acrylate (High-DK) |

| Silicone Acrylate (Mid-DK) |

| PMMA & Others |

| Offline (Optometry & Ophthalmology Clinics) |

| Online (E-commerce, Tele-optometry) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Lens Type | Corneo-scleral & Semi-scleral Lenses | |

| Mini-scleral Lenses | ||

| Full Scleral Lenses | ||

| By Application | Irregular Cornea | |

| Ocular Surface Disease | ||

| Refractive Error | ||

| Other Applications | ||

| By End User | Hospitals | |

| Eye Clinics | ||

| Other End Users | ||

| By Material | Fluoro-silicone Acrylate (High-DK) | |

| Silicone Acrylate (Mid-DK) | ||

| PMMA & Others | ||

| By Distribution Channel | Offline (Optometry & Ophthalmology Clinics) | |

| Online (E-commerce, Tele-optometry) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the scleral lens market?

The scleral lens market size was USD 364.15 million in 2026 and is forecast to reach USD 589.32 million by 2031.

Which region is growing fastest in the scleral lens market?

Asia-Pacific shows the highest growth with an expected 15.02% CAGR through 2031 due to rising keratoconus prevalence and rapid specialty-clinic expansion.

Why are mini-scleral lenses so popular?

Mini-scleral lenses balance handling ease and corneal vaulting effectiveness, capturing 48.02% of 2025 global revenue and suiting most irregular cornea cases.

What materials are driving future innovation?

High-DK fluoro-silicone acrylates exceeding 200 Dk and super-lubricious hydrogel coatings are advancing longer wear schedules while safeguarding corneal health.

How are digital tools changing scleral lens fittings?

AI-guided design software and tele-optometry platforms cut chair time, enhance first-fit accuracy, and pave the way for hybrid online-offline distribution models.

Page last updated on: