Consent Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.07 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 17.05% CAGR |

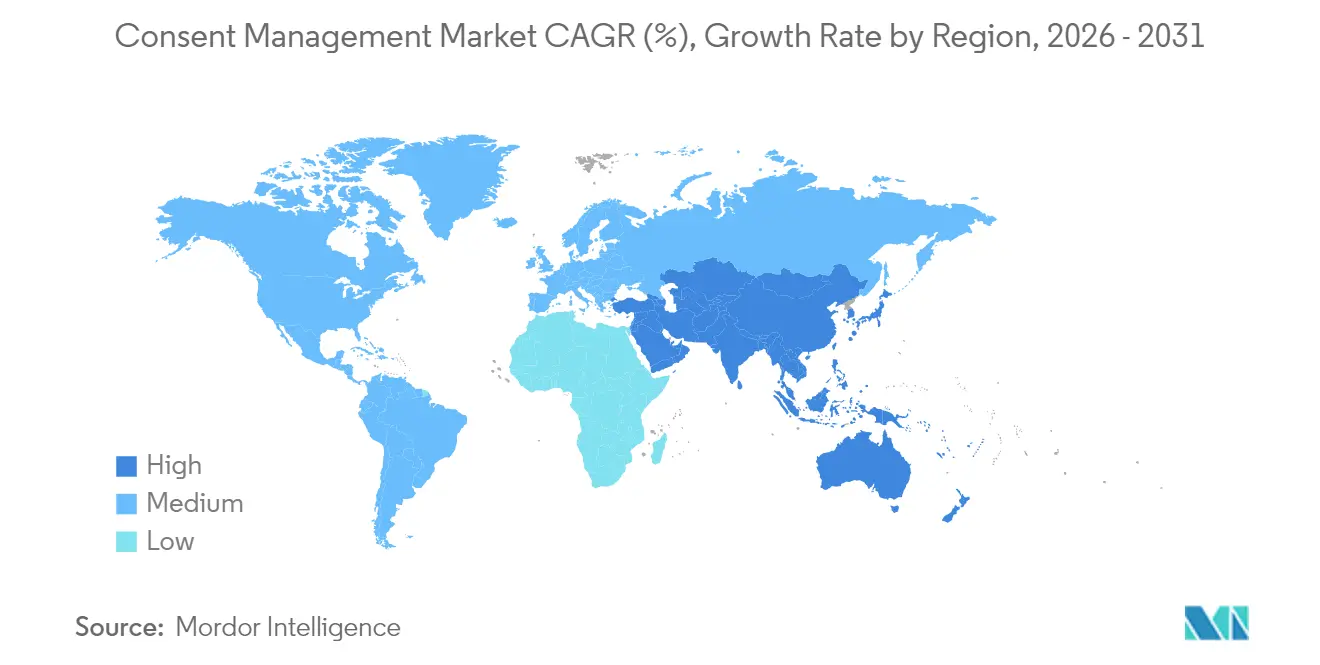

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

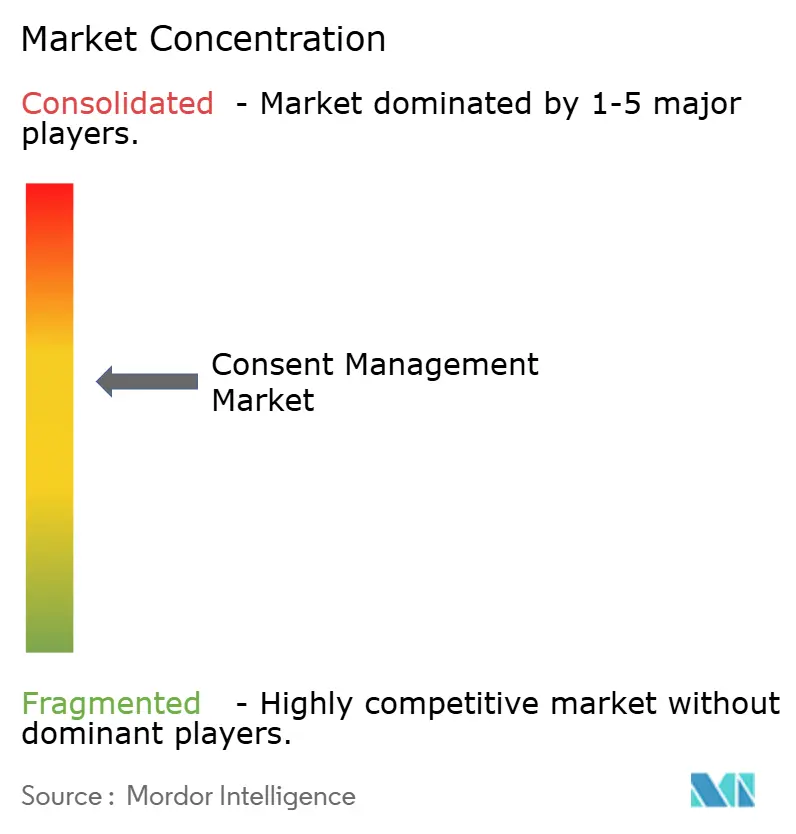

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consent Management Market Analysis by Mordor Intelligence

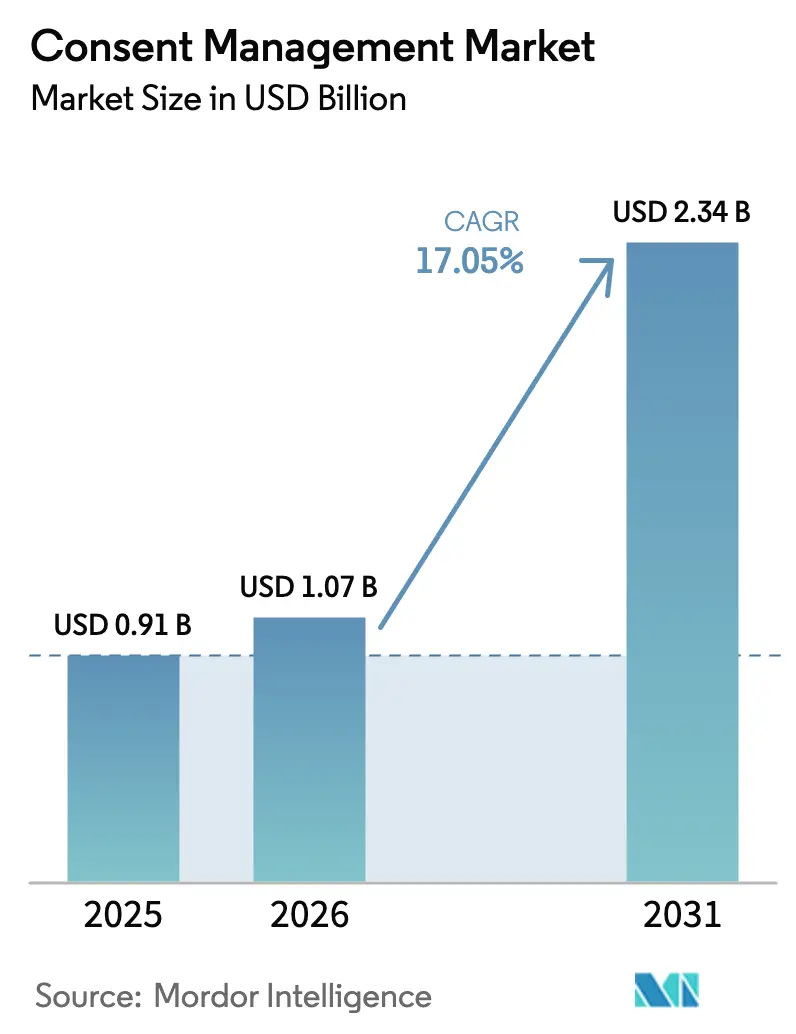

The consent management market size was valued at USD 0.91 billion in 2025 and estimated to grow from USD 1.07 billion in 2026 to reach USD 2.34 billion by 2031, at a CAGR of 17.05% during the forecast period (2026-2031). Strong global privacy mandates, an industry-wide move toward first-party data strategies, and rising executive recognition of consent as a driver of customer trust all underpin this expansion. Heightened enforcement activity in North America, swift regulatory rollouts in Asia Pacific, and rapid innovation in cloud-based consent orchestration are steering vendor investments toward platform breadth, AI-driven automation, and seamless identity integration. Competitive differentiation increasingly hinges on the ability to embed granular permissions across web, mobile, and IoT touchpoints, while also providing real-time analytics that translate consent signals into actionable marketing intelligence. Consolidation persists as large technology firms enter the field, prompting incumbent vendors to broaden their feature sets, extend partner ecosystems, and pursue vertical-specific solutions.

Key Report Takeaways

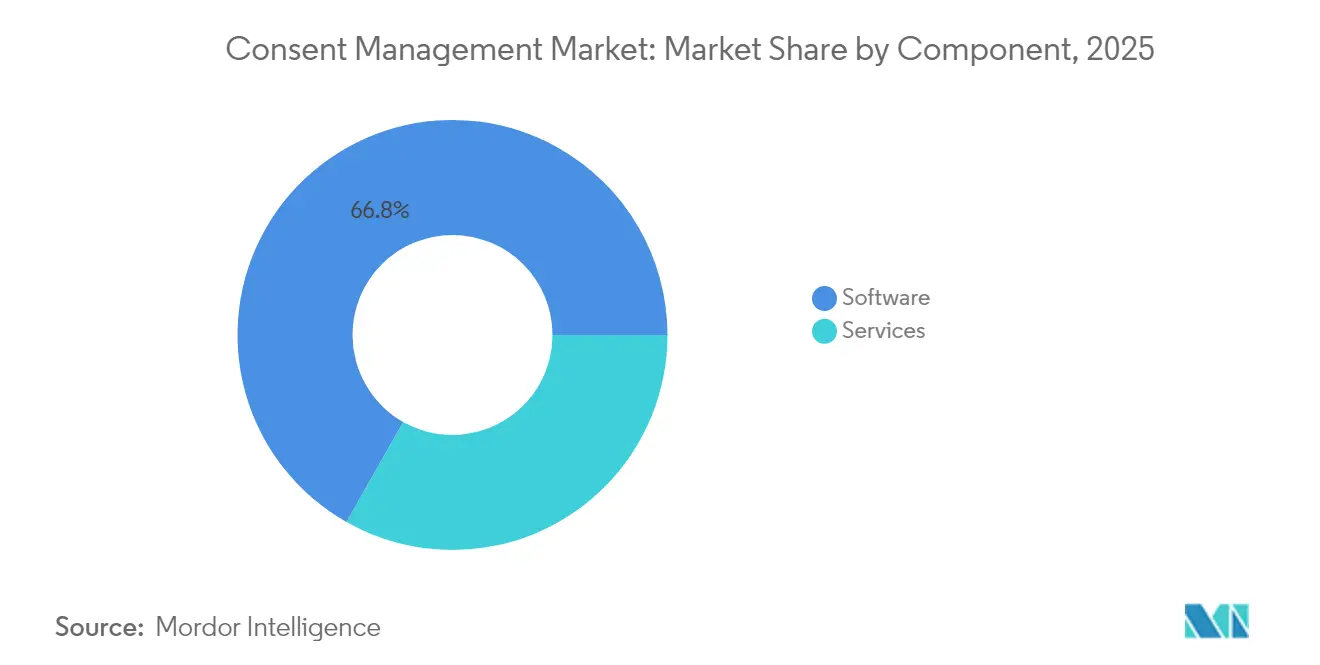

- By component, software accounted for 66.80% of the consent management market share in 2025, while services are forecast to expand at a 17.1% CAGR through 2031.

- By deployment model, cloud solutions captured 64.10% of the consent management market size in 2025 and are expected to grow at an 18.0% CAGR between 2026 and 2031.

- By touchpoint, web applications led with 55.40% revenue share in 2025; mobile apps are projected to advance at a 18.6% CAGR to 2031.

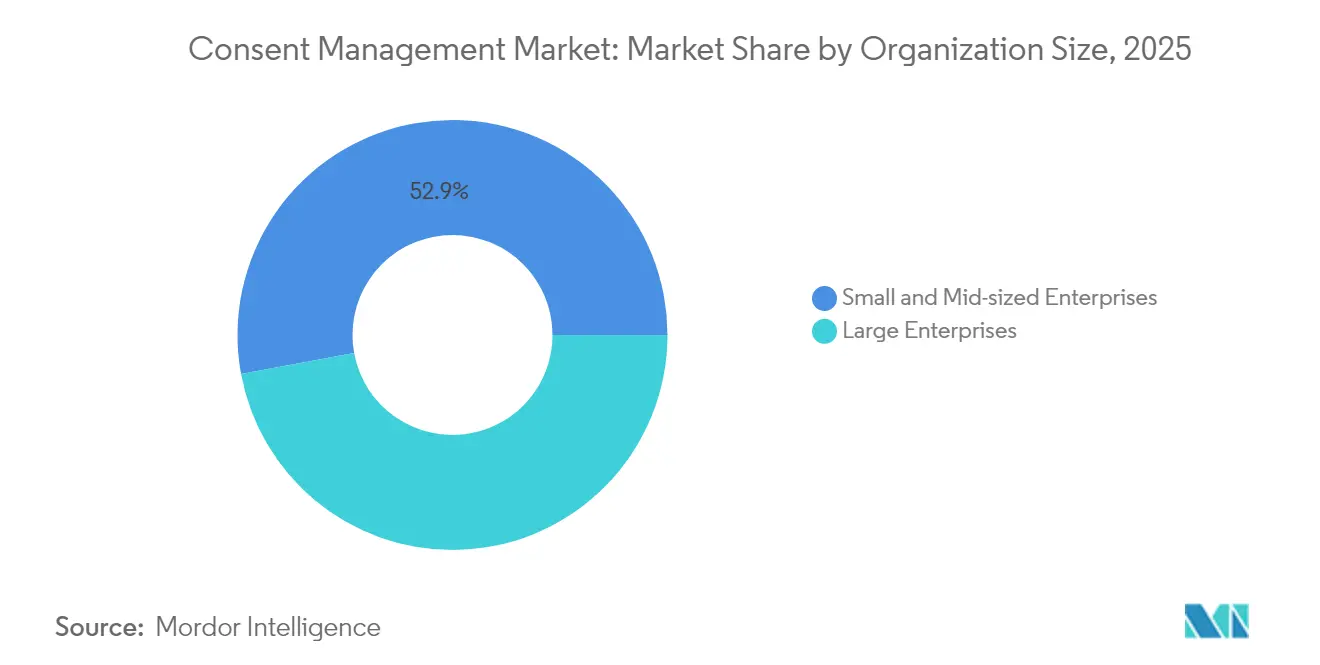

- By organization size, large enterprises held 47.10% of the consent management market share in 2025, while SMBs are poised for the fastest growth at an 18.2% CAGR through 2031.

- By end-user industry, retail and e-commerce controlled 24.80% of the consent management market size in 2025; healthcare is set to grow at a 18.7% CAGR to 2031.

- By geography, North America commanded 36.20% revenue in 2025, whereas Asia Pacific is on track for a 17.4% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Consent Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global and sector-specific privacy rules | +4.2% | North America and EU, expanding global | Long term (≥ 4 years) |

| First-party data strategies after cookie deprecation | +3.8% | North America and Asia-Pacific | Medium term (2-4 years) |

| Data-trust user experience as a differentiator | +2.9% | North America and EU, rising in Asia-Pacific | Medium term (2-4 years) |

| Embedded consent in IoT-edge devices | +2.1% | APAC core, spillover to North America | Long term (≥ 4 years) |

| Automated privacy-as-code pipelines | +1.8% | North America and EU | Short term (≤ 2 years) |

| Consent tokens for Web3 ecosystems | +1.5% | Early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent global and sector-specific privacy rules drive market expansion

Intensified enforcement arrived in 2025 as eight additional US state privacy statutes, India’s Digital Personal Data Protection Act, and new Department of Justice national-security rules forced enterprises to refresh consent tooling and governance processes. State laws such as Maryland’s ban on sensitive data sales and New Jersey’s heightened protections for minors require hyper-granular permissioning that legacy cookie pop-ups cannot deliver. Financial institutions face parallel pressures from rising GDPR penalties, India’s biometric safeguards, and Australia’s stricter open-banking mandates. Penalties levied in 2024, often reaching multimillion-dollar sums, have reframed consent platforms as core infrastructure rather than discretionary add-ons, triggering budget reallocations and board-level oversight.

First-party data strategies reshape consent architecture

Google’s decision to retain third-party cookies, while releasing an integrated CMP setup in August 2024, elevated the consent management market by shifting the enterprise focus from cookie compliance to holistic data governance. Research shows that 78% of B2C brands now prioritize direct data collection, creating demand for orchestration engines that honor user preferences across web, app, and server environments. Microsoft’s requirement that advertisers pass consent signals by May 5, 2025, accelerated the adoption of consent mode and real-time preference APIs.[1]Microsoft, “Advertising Consent Mode FAQ,” learn.microsoft.comServer-side tagging, championed by firms such as Didomi, is gaining traction as a privacy-preserving alternative that maintains campaign performance without sacrificing compliance.

Data-trust user experience emerges as a competitive differentiator

European regulators now scrutinize interface design as closely as legal language. Germany’s 2025 Consent Management Ordinance obliges businesses to shorten notices, remove dark patterns, and present genuine choices, spurring UX-first rebuilds of consent workflows. Brands are embedding behavioral analytics to A/B test banner copy, sequencing, and iconography, quantifying how each iteration affects opt-in rates. “Consent or pay” models remain under intense review by the European Data Protection Board, encouraging vendors to create preference centers that provide frictionless subscription alternatives. Academic work from UC Berkeley underscores how privacy engineering now blends design thinking with code, elevating consent from a compliance hurdle to a lever for lifetime value.

Embedded consent inside IoT-edge devices stimulates technical innovation

Wearables, vehicles, and home sensors collect expanding volumes of sensitive data, yet often lack conventional user interfaces. Device makers are integrating voice prompts, QR opt-in flows, and blockchain-based consent tokens to synchronize permissions across constrained networks. [2]Ministry of Electronics and Information Technology, “IoT SAFE Protocol Overview,” meity.gov.inAutomotive OEMs now must track individual passenger choices, enable jurisdiction-aware cross-border transfers, and retain audit trails that regulators can verify on inspection. The emerging IoT SAFE protocol further demands secure device authentication, prompting consent platforms to offer lightweight agents capable of offline operation with batched synchronization on reconnection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Constantly shifting multi-jurisdictional requirements | -2.1% | Global, particularly affecting multinational operations | Medium term (2-4 years) |

| Low executive budgets in SMBs for privacy tooling | -1.8% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Consumer "consent fatigue" reducing opt-in rates | -1.4% | Global, with acute impact in EU and mature markets | Medium term (2-4 years) |

| Absence of universal consent interoperability standards | -1.2% | Global, affecting cross-platform implementations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Constantly shifting multi-jurisdictional requirements create implementation barriers

Organizations operating across 19 US states, the EU, China, and India must juggle conflicting opt-in, opt-out, and data-localization rules, inflating configuration overhead and legal consulting spend. India’s concept of licensed “consent managers” adds a new actor to data flows, while China’s cross-border security assessments require consent records that satisfy domestic cybersecurity auditors' data guidance. Absent global standards, enterprise privacy teams maintain parallel rule sets, consuming as much as 40% of total program budgets and prolonging deployment cycles.

SMB budget constraints limit market penetration

Sophisticated CMPs often require professional services and custom integrations beyond the reach of smaller firms. Many SMBs still rely on low-cost cookie pop-ups that fail to satisfy regional rules, exposing them to fines and advertising restrictions. Google’s certified CMP requirement for Ad Manager properties operating in Europe forces even micro-brands to upgrade their consent stack. Yet, upfront costs and limited technical staff remain deterrents.[3]Google, “Google CMP Partner Program,” support.google.comVendors addressing this gap through simplified, flat-fee SaaS offerings and guided setups may unlock a sizeable untapped segment, but adoption lags nonetheless, suppressing the aggregate growth curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: software dominance faces services acceleration

Software platforms generated 66.80% revenue in 2025, reflecting enduring demand for automated banner rendering, preference vaults, and compliance dashboards that scale across digital estates. Services, covering implementation, integration, and managed compliance, are expanding at 17.1% annually as organizations outsource regulatory interpretation and ongoing monitoring. This momentum underscores how policy complexity outpaces point-and-click configuration, elevating demand for multidisciplinary teams that combine legal, UX, and DevSecOps skill sets.

Services providers are embedding automated scanning, script categorization, and edge consent monitoring into packaged offerings, shortening project timelines and lowering total cost of ownership. Enterprises can thus delegate continuous rule-set updates, ensuring banners adapt as legislatures revise statutes. Over the forecast window, hybrid models bundling licensed software with value-added services will become prevalent, especially for mid-market buyers lacking in-house privacy engineers.

By Deployment Model: cloud supremacy accelerates

Cloud delivery captured 64.10% revenue in 2025, expected to register a CAGR of 18.0% over the forecast period. As brands pursued always-on rule updates, global edge nodes for latency-free banner calls, and elastic compute for consent signal processing. The consent management market size for cloud solutions will expand fastest, supported by automatic feature releases that eliminate upgrade projects. On-premises deployments persist in healthcare and financial services, where data residency and internal audit obligations dictate local storage, yet even these sectors gravitate toward hybrid architectures that route analytics and non-identifying data to secure-cloud environments.

Edge computing introduces additional nuance. Connected cars, smart factories, and remote medical devices demand low-latency consent checks that cannot always rely on central servers. Cloud vendors respond with lightweight agents that cache policy logic locally while synchronizing state when connectivity resumes, marrying sovereignty requirements with global orchestration.

By Touchpoint: mobile apps challenge web dominance

Web properties retained 55.40% share in 2025, but mobile apps are advancing at 18.6% CAGR as in-app commerce and content streaming surge. The consent management market share for mobile will expand rapidly because smaller screens require novel UX patterns such as stacked dialogs and gesture-based opt-ins. Push toward native SDKs that harmonize consent across iOS, Android, and cross-platform frameworks simplifies developer adoption and promotes consistent preference handling.

APIs enabling consent portability across chatbots, voice assistants, and AR overlays gain relevance as omnichannel journeys scale. Token-based credentials allow a user’s choice to roam between devices, minimizing fatigue and reinforcing trust. These APIs also support server-side data collection, ensuring marketing tags fire only when permitted preferences exist.

By Organization Size: SMBs drive growth despite enterprise dominance

Large enterprises accounted for 47.10% of 2025 revenue, supported by complex international footprints and budgets able to absorb platform and consulting costs. However, SMB adoption races ahead at an 18.2% clip as regulatory obligations broaden and advertising platforms cut off non-compliant sites. Vendors are launching tiered licenses, wizard-based deployments, and templated notices to lower barriers.

Success in the consent management market ultimately hinges on meeting SMB expectations for quick time-to-value. Offerings that bundle basic tag scanning, granular analytics, and auto-translated notices into a single dashboard reduce implementation friction. Over 2026-2031, SMBs will account for a larger portion of net-new subscriptions, though revenue per customer will remain lower than enterprise accounts.

By End-User Industry: healthcare leads growth amid retail dominance

Retail and e-commerce accounted for 24.80% of 2025 turnover, as omnichannel personalization, loyalty programs, and high traffic volumes necessitated robust consent orchestration. Meanwhile, healthcare accelerates at the fastest rate, with a 18.7% CAGR, spurred by national security restrictions on the transfer of protected health information and stricter HIPAA enforcement. The consent management market size for healthcare is expected to more than double by 2031, driven by telemedicine, medical device data streams, and patient portals that handle sensitive biometric data.

Financial services, media, telecommunications, and public sector entities likewise deepen investment as identity verification, interest-based advertising, and smart-city initiatives require transparent data permissions. Education adds incremental demand as ed-tech providers adopt parental consent workflows for minors, rounding out a diverse industry adoption profile.

Geography Analysis

North America generated the largest portion of 2025 revenue at 36.20%, buoyed by the California Privacy Rights Act, rising state-level statutes, and corporate focus on first-party data governance. Federal agencies further tightened oversight in April 2025, restricting foreign access to sensitive US personal data and compelling health providers and cloud processors to upgrade consent verification. Canada’s PIPEDA amendments and Mexico’s emerging framework compound regional complexity, driving enterprises to platforms that can auto-calibrate notices by state and country.

Asia-Pacific is the fastest-growing region, rising at 17.4% CAGR through 2031 as India’s Digital Personal Data Protection Act formalizes “consent managers” and China enforces cross-border transfer security assessments. Japan, South Korea, and Australia maintain stable adoption under mature regimes, while Indonesia, Vietnam, and the Philippines enter enforcement phases that will unlock fresh demand. User fatigue within populous markets fuels innovation in visually streamlined notice design and alternative lawful bases.

Europe remains a mature yet evolving arena. The GDPR continues to anchor compliance, but Germany’s Consent Management Ordinance and the EU AI Act add fresh layers that require interface refinements and algorithmic transparency. Pan-EU debate around “consent or pay” models spurs the development of preference centers that offer equitable free alternatives. The United Kingdom’s evolving post-Brexit rules create divergent opt-out mechanics, forcing vendors to maintain configurable templates for EU and UK visitors.

Competitive Landscape

Market concentration is moderate, with the top quintet controlling roughly half of global revenue. Competitive tension intensified in 2024 when Google rolled out an integrated CMP setup and Microsoft mandated consent mode for EEA ad campaigns, pushing incumbents to invest in AI-assisted banner optimization, cross-device ID stitching, and zero-touch mobile SDKs.

Strategic consolidation reshapes the field. EQS Group’s December 2024 purchase of OneTrust’s ethics division illustrates vendor moves toward end-to-end governance that spans whistle-blowing, incident response, and consent orchestration. Partnerships such as ForgeRock and OneTrust bring identity federation and consent management into unified journeys, easing authentication-to-authorization handoffs. Disruptors, including Transcend and Privado, differentiate through code-centric privacy tooling and continuous monitoring; 90% of Transcend customers report tighter compliance post-migration, while Privado’s 2024 study found 75% of websites still violate consent rules, signaling substantial whitespace for innovation.

Emerging niches include IoT consent orchestration, Web3 credential issuance, and privacy-embedded DevSecOps pipelines. Vendors that deliver measurable business value, lower campaign drop-off, higher opt-in rates, and reduced legal spend will outpace purely compliance-driven offerings as buyers increasingly view consent as a growth enabler rather than a cost center.

Consent Management Industry Leaders

OneTrust

TrustArc

Usercentrics (incl. Cookiebot)

Crownpeak

Quantcast

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Microsoft Advertising confirmed mandatory consent signals by May 5, 2025, for EEA, UK, and Switzerland campaigns, formalizing Consent Mode requirements.

- January 2025: The US Department of Justice issued rules effective Apr 8, 2025, limiting foreign access to sensitive personal data, adding new consent controls for healthcare entities.

- December 2024: EQS Group acquired OneTrust’s ethics and compliance unit, expanding its presence in the United States.

- November 2024: Privado’s “State of Website Privacy Report 2024” showed 75% of US and EU sites remain non-compliant with consent requirements.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, our study counts the global consent management market as the yearly revenue generated by purpose-built software and the professional or managed services that capture, store, update, and audit user permissions across websites, mobile apps, connected devices, and API hooks while automating compliance with GDPR, CCPA, LGPD, DPDP, and comparable laws.

Scope exclusion: simple one-step cookie banners that neither keep granular preferences nor issue verifiable audit logs are left outside this scope.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Model

- Cloud

- On-premises

- By TouchPoint

- Web App

- Mobile App

- API/SDK

- By Organisation Size

- Large Enterprises

- Small and Mid-sized Enterprises

- By End-User Industry

- IT and Telecom

- Government and Public Sector

- Healthcare and Life Sciences

- Retail and E-commerce

- BFSI

- Media and Entertainment

- Others (Travel, Education)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with product leads, privacy counsels, mar-tech integrators, and data-protection officers in North America, Europe, Asia-Pacific, and Latin America; their insights refined adoption curves, average selling prices, and imminent rule changes.

Desk Research

Our analysts first mapped the legal terrain through open portals of the European Data Protection Board, US FTC, India's DPDP dashboard, and Australia's OAIC, which spell out mandatory consent elements. Trade bodies such as IAB Europe and IAB Tech Lab explained technical frameworks, while macro indicators from the World Bank, Eurostat, ITU, and national commerce ministries sized internet reach, online spending, and SME counts that steer adoption. Company filings, IPO papers, tender notices, and earnings calls framed vendor revenue ranges, and selective pulls from D&B Hoovers and Dow Jones Factiva cross-checked those figures. The sources cited are illustrative; many other public and subscription assets informed our desk work.

Market-Sizing & Forecasting

Sizing started with a top-down build, multiplying global internet users by daily site visits and by the share of domains under active privacy law to create a consent-event pool that we converted to spend using interview-verified CMP cost-per-mil rates. Targeted bottom-up supplier roll-ups validated totals, and gaps above five percent triggered recalibration. A multivariate regression blending fresh statutes, IAB-compliant CMP roll-outs, subscription ASP shifts, cloud traffic volumes, and digital-ad budgets drives the 2025-2030 outlook.

Data Validation & Update Cycle

Outputs pass two analyst reviews, logic tests, and variance scans against public disclosures. Reports refresh each year, with interim updates when landmark fines, rulings, or platform shifts materially alter demand.

Why Mordor's Consent Management Baseline Commands Credibility

Published estimates often differ because firms choose distinct scopes, currencies, and refresh cadences. Our disciplined, yearly-updated model offers a transparent midpoint that planners can trace.

Key gap drivers elsewhere include omission of service revenue, optimistic micro-SMB penetration, static 2020 forex, and restricted geography coverage.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 910 million (2025) | Mordor Intelligence | - |

| USD 765 million (2025) | Global Consultancy A | Services excluded, fixed 2020 USD |

| USD 903 million (2025) | Regional Consultancy B | Counts North America and Europe only |

| USD 2 271 million (2030) | Industry Association C | Headlines future value, aggressive micro-SMB rollout |

These contrasts show how our balanced scope, dual-path modeling, and timely refresh give decision-makers a dependable, repeatable baseline.

Key Questions Answered in the Report

What is the current size of the consent management market?

The consent management market is valued at USD 1.07 billion in 2026 and is forecast to reach USD 2.34 billion by 2031.

Which region leads in revenue?

North America leads with 36.20% revenue share in 2025, driven by state-level privacy laws and strong enterprise adoption.

Which segment is growing the fastest?

Healthcare shows the fastest growth at a 18.7% CAGR for 2026-2031 due to stricter rules on protected health information transfers.

Why are services expanding quickly?

Regulatory complexity and a shortage of in-house privacy expertise push firms toward implementation consulting and managed compliance services, driving a 17.1% CAGR for services.

How does cloud deployment benefit consent management?

Cloud platforms provide real-time regulatory updates, elastic scalability, and global edge delivery, supporting the highest forecast CAGR of 18.0% among deployment models.

Page last updated on: