Connected Street Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

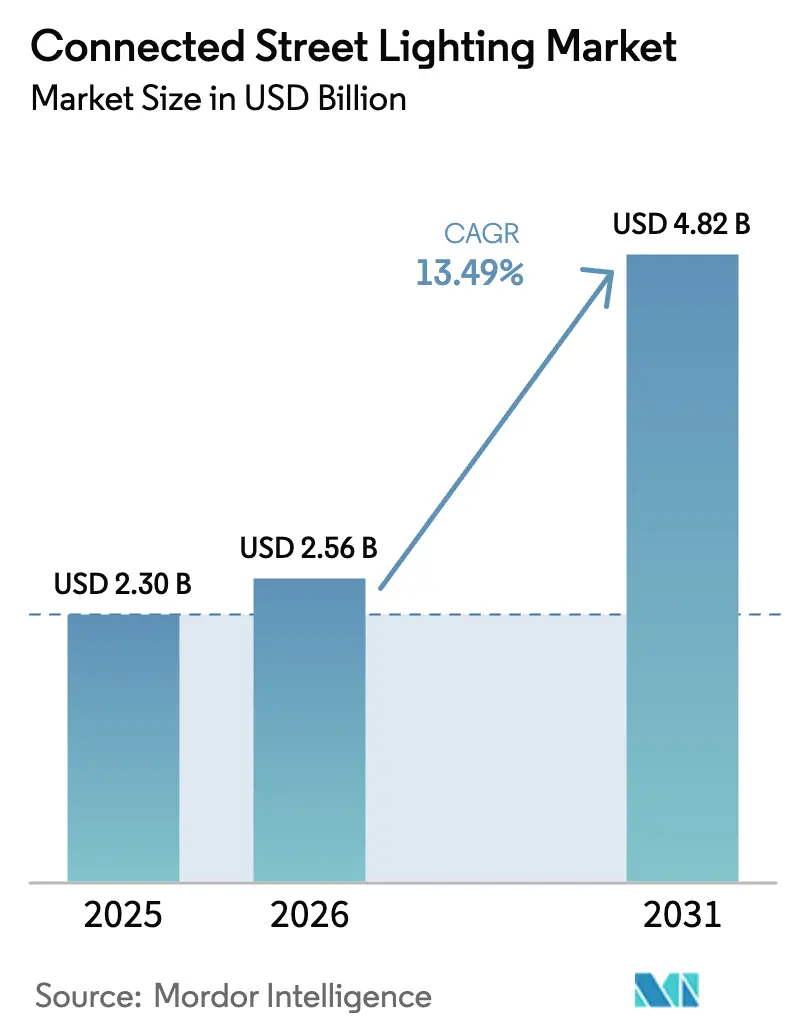

| Market Size (2026) | USD 2.56 Billion |

| Market Size (2031) | USD 4.82 Billion |

| Growth Rate (2026 - 2031) | 13.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Street Lighting Market Analysis by Mordor Intelligence

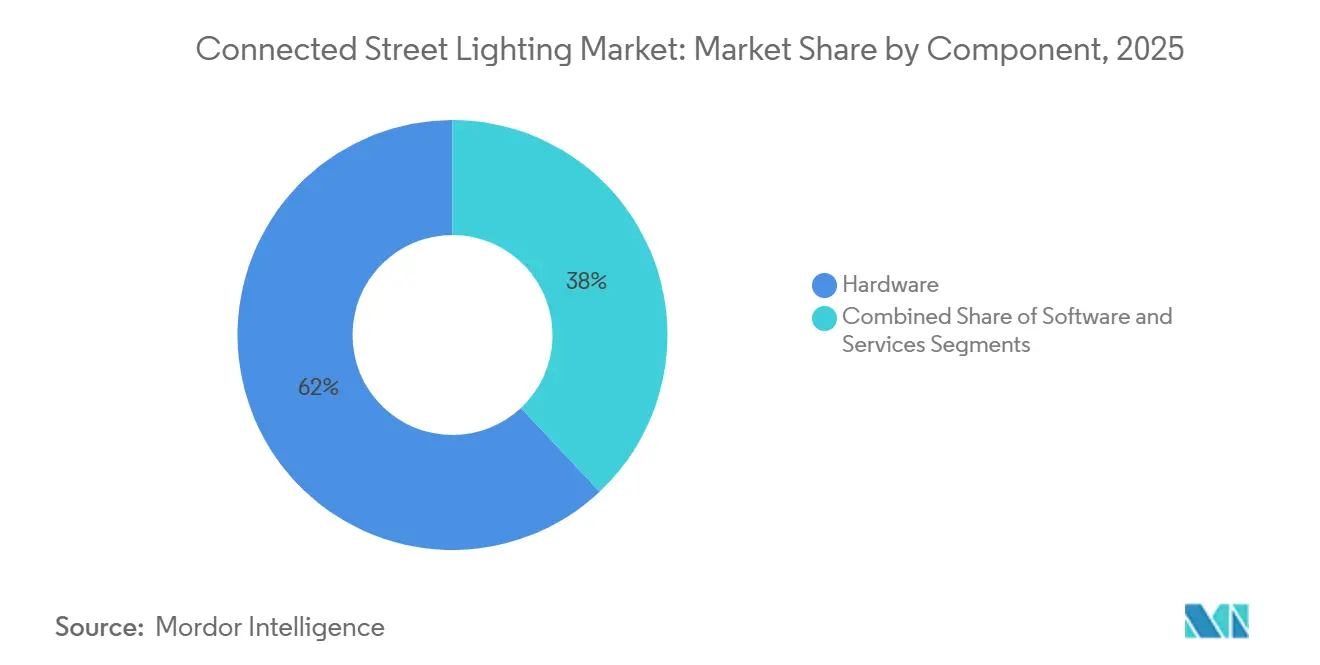

The connected street lighting market size is projected to reach USD 4.82 billion by 2031, reflecting a 13.49% CAGR over the forecast period, from USD 2.56 billion in 2026. Cities are prioritizing energy efficiency, cellular IoT maturity, and multiuse poles that can host 5G small cells, environmental sensors, and EV charging add-ons.[1]Signify, “Signify and Cornerstone to deploy city-wide multi-operator wireless network through street lighting,” signify.com Hardware commanded a 62% share in 2025, while software and services are expanding at 13.65% CAGR as buyers emphasize predictive maintenance and emissions reporting tied to revenue-grade metering. Proprietary RF held 55.5% of connectivity in 2025; however, cellular options such as NB-IoT and LTE-M are expected to grow at a 13.73% CAGR, as plug-and-play controllers reduce deployment friction. Cloud models accounted for 45% of deployments in 2025 and are scaling with open APIs that integrate lighting telemetry into traffic, air quality, and emergency dashboards.

Key Report Takeaways

- By component, hardware led with a 62% share in 2025, while software and services are projected to grow at a 13.65% CAGR to 2031.

- By connectivity, proprietary RF networking held a 55.5% share in 2025, and cellular is forecast to post a 13.73% CAGR through 2031.

- By application, traffic optimization accounted for 28% of deployments in 2025, while smart parking is expected to expand at a 13.89% CAGR through 2031.

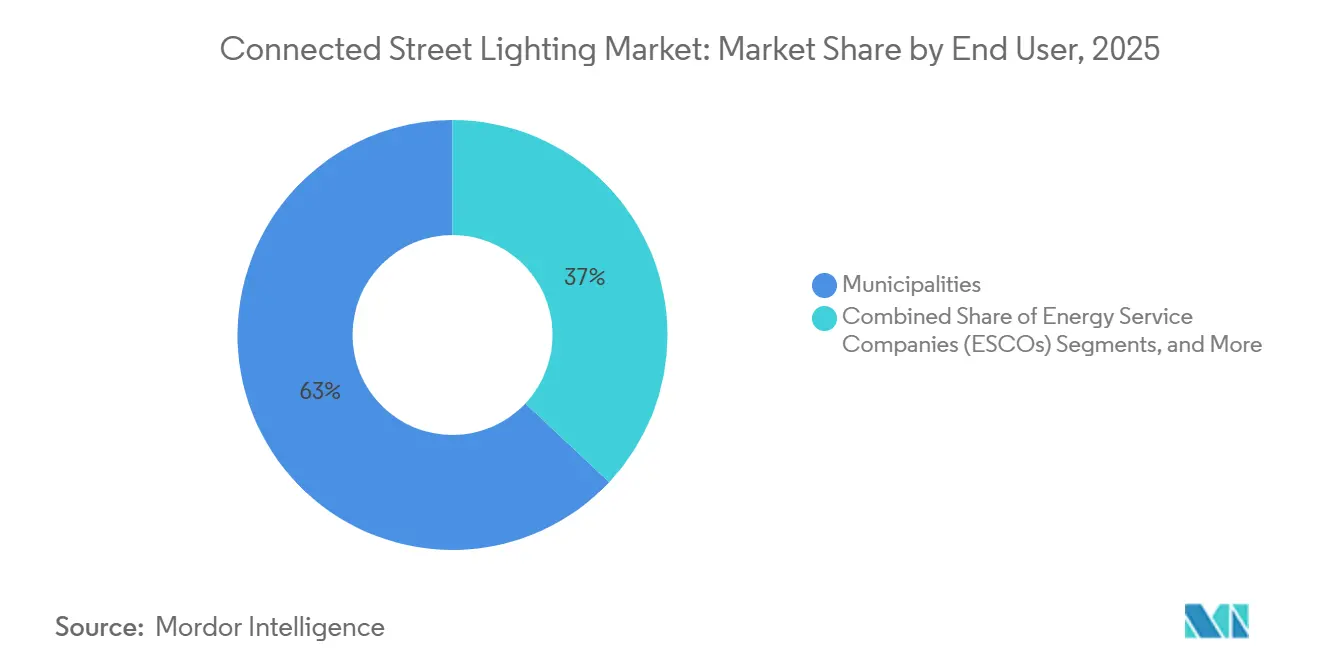

- By end user, municipalities accounted for 63% of adoption in 2025, while industrial parks and ESCOs are set to grow at a 14.04% CAGR.

- By geography, Europe held a 65% installed base lead in 2025, and Asia-Pacific is projected to be the fastest-growing region at a 14.12% CAGR.

- By deployment model, cloud held a 45% share in 2025 and is expected to rise at a 13.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Connected Street Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Electricity Prices and Energy Efficiency Mandates | +2.8% | Global, stronger in EU and North America | Medium term (2-4 years) |

| Acceleration of Smart City Programs and PPP Procurement | +3.1% | Asia-Pacific, Middle East, selected EU cities | Long term (≥ 4 years) |

| Rapid Shift to Cellular Controls for Plug-and-Play Deployments | +2.4% | North America, Asia-Pacific, early Middle East | Short term (≤ 2 years) |

| Interoperability via Zhaga-D4i, DALI-2, and TALQ | +1.9% | Europe, North America, global greenfield | Medium term (2-4 years) |

| Data-Driven Operations and Predictive Maintenance | +2.2% | North America, Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Lamp-Post-as-a-Platform for 5G and Sensing | +1.1% | Urban hubs in North America and Europe, APAC corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Prices and Energy Efficiency Mandates Compound Retrofit Economics

Networked LED streetlights with controls have delivered measurable energy and O&M cuts in large programs, which strengthens the business case for scale. Chicago’s 290,000 fixture rollout reduced annual electricity expenses by USD 8.7 million and generated USD 37 million in utility rebates over five years, while carbon reductions totaled 134,600 metric tons by September 2022. [2]Itron, “Sustainability Through Streetlights: Why Smart LED Streetlights are the Gold Standard for Measurable Carbon Reduction,” itron.com Revenue-grade metering in smart lighting platforms supports compliance and streamlined reporting, eliminating the need for costly substation instrumentation. Ontario’s 2025 grid-planning guidance emphasizes non-wires strategies during project screening, positioning adaptive lighting as a flexible demand-response tool for utilities and municipalities. Procurement teams increasingly link controller-capable luminaires to rebate eligibility and decarbonization tracking, reinforcing the role of connected lighting in municipal energy policy. These dynamics underpin durable demand in the smart street lighting management systems market as cities aim to protect budgets and meet climate targets.

Acceleration of Smart City Programs and PPP Procurement De-Risks Municipal Balance Sheets

Public-private partnerships enable cities to shift performance risk and transform energy savings into predictable payments over multi-year terms. Serbia’s Požega project under an energy service structure is cited as a practical template for smaller municipalities that lack upfront capital but need modernization and verifiable outcomes. India’s Smart Cities Mission directs sizable funding to corridor illumination, intelligent intersections, and connected poles, which sustains high-volume tenders and accelerates digital infrastructure in fast-growing urban clusters. These models also attract infrastructure funds that prefer long-duration, utility-like cash flows anchored in verified energy reductions. As multi-party agreements mature, performance guarantees, remote monitoring, and open-data clauses become standard, which reduces perceived vendor risk and advances bankability. This structural shift supports steady growth in the smart street lighting management systems market where fiscal constraints would otherwise stall upgrades.

Rapid Shift to Cellular Controls for Plug-and-Play Deployments Sidesteps Mesh Gateway Overhead

Deployments that rely on NB-IoT or LTE-M controllers can avoid large gateway fleets, which lowers installation time and simplifies maintenance. Washington, D.C. equipped 75,000 lights with cellular controllers, achieving lamp-level control and real-time monitoring while overcoming the gateway burden typical of private meshes. Standard device management protocols, such as LwM2M 2.0, enhance provisioning and lifecycle support, streamlining large-scale rollouts for utilities and city departments. [3]Open Mobile Alliance, “The Role of LwM2M 2.0 in Smart Cities,” openmobilealliance.org For city fleets numbering in the tens of thousands, plug-and-play configurations reduce truck rolls and working capital tied up in spares. Cellular models align with standard IT operations by leveraging carrier-grade security and SLAs, which support governance objectives in critical infrastructure. These advantages reinforce the adoption of smart street lighting management systems, where simplicity and speed favor cellular-first strategies.

Interoperability via Zhaga-D4i, DALI-2, and TALQ Improving Vendor Neutrality Unlocks Multi-Decade Asset Life

The DALI Alliance, TALQ Consortium, and Zhaga Consortium formalized a liaison to unify data streams, which reduces integration overhead for multi-vendor lighting fleets. Zhaga Book 18 Edition 4 extended socket-based control to heritage and decorative luminaires, opening a path for smart retrofits in districts with preservation mandates. TALQ-certified projects in Brussels and along major highways demonstrate that standardized interfaces allow utilities to mix controllers and luminaires while maintaining a single central management system. Common data models promote condition-based maintenance and scheduled interventions that reduce mean time to repair when integrated with back-office systems. These developments support lifetime extension and avoid full fixture swaps, strengthening economics in the smart street lighting management systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Costs, Complex Tendering and Financing | -1.8% | Latin America, Africa, smaller EU municipalities | Medium term (2-4 years) |

| Legacy Infrastructure Integration and Interoperability Gaps | -1.3% | North America, Europe, Asia | Medium term (2-4 years) |

| Cybersecurity, Data Governance, and Sovereignty Concerns | -0.9% | Global, acute in EU, North America, Middle East | Short term (≤ 2 years) |

| Standards Fragmentation and Spectrum Constraints | -0.6% | Dense metros in APAC, North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Costs, Complex Tendering and Financing Disproportionately Burden Smaller Municipalities

Network-ready luminaires and controller rollouts add capital intensity that is difficult for small cities to absorb within one budget cycle. Performance-based contracts and availability-payment PPPs move energy-savings risk to private operators, but they can extend procurement timelines due to verification and monitoring requirements. Municipalities evaluate Lighting-as-a-Service to eliminate upfront equipment costs and shift to predictable monthly fees backed by quantifiable O&M savings. Utility alignment around non-wires solutions makes adaptive lighting more attractive where network upgrades would otherwise be approved, although documentation needs and cross-department coordination can slow approvals. Even with long-term savings, smaller towns face elevated tendering overhead, which tempers near-term adoption in the smart street lighting management systems market.

Cybersecurity, Data Governance, and Sovereignty Concerns Elevate Compliance Overhead and Slow Vendor Selection

Manufacturers face lifecycle security obligations and data-access provisions that increase engineering and legal effort. The EU Data Act requires real-time access to device-generated data and ensures data portability without switching fees, changing how cities negotiate contracts and how vendors architect platforms. Many jurisdictions specify data residency or hybrid architectures that keep sensitive telemetry local while syncing anonymized aggregates to cloud analytics. Public-sector agencies acknowledge resource gaps in cybersecurity and consider targeted investments and labeling schemes to raise baseline protections for local governments. Vendor lock-in from legacy systems without modern encryption or over-the-air updates increases migration cost, which influences upgrade timing and supplier choice in the smart street lighting management systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Gains as Predictive Analytics Monetize Sensor Data

Hardware captured 62% of the smart street lighting management systems market in 2025, while software and services are growing at 13.65% CAGR as cities adopt central management systems that enable remote control, firmware updates, and carbon-accounting dashboards. City platforms such as Interact and similar SaaS offerings have shifted spending from upfront capital to per-endpoint fees, allowing integration with traffic signals, EV chargers, and public safety feeds through secure APIs. At scale, operators manage millions of telemetry messages per day, which supports digital-twin models of each luminaire and improves service planning and availability metrics across fleets. Software’s share expansion also reflects policy that favors revenue-grade metering and verifiable emissions reporting in city sustainability plans. As sockets standardize via ANSI C136.41 and Zhaga Book 18, hardware becomes more interchangeable, which pressures pricing and elevates the role of software differentiation in the smart street lighting management systems market.

Services remain substantial as turnkey PPP contracts bundle installation, commissioning, and multi-year performance obligations, though growth trails software as more value shifts to analytics and automation. Predictive maintenance drives measurable O&M savings, converting reactive truck rolls into scheduled interventions that consolidate tasks and reduce time to repair. These trends continue to draw spend toward SaaS and integration services as the smart street lighting management systems industry uses APIs and standardized data models to share insights across city departments. Over 2026 to 2031, software-led gains are reinforced by policy incentives tied to metering and carbon disclosure, which helps sustain premium pricing for analytics features. This mix strengthens recurring revenue and cushions vendors against hardware margin compression in the smart street lighting management systems market.

By Connectivity: Cellular Plug-and-Play Economics Challenge Proprietary RF Mesh Incumbency

Proprietary RF mesh, including Wi-SUN and IEEE 802.15.4g, held a 55.5% connectivity share in 2025, while cellular controls are forecast to grow at a 13.73% CAGR as cities value simpler rollouts and carrier-grade uptime. In Washington, D.C., 75,000 lamp-level cellular controllers reduced deployment complexity while enabling real-time monitoring, eliminating gateway installation and maintenance. Standard device-management frameworks like LwM2M improve reliability and lifecycle control for large distributed endpoint fleets. LoRaWAN remains favored where long-range, low-throughput links are sufficient, and spectrum management is practical, particularly in site-constrained corridors that need battery-friendly endpoints. Project owners weigh subscription fees against gateway overhead, with many choosing cellular when workforce constraints and timelines dominate decision criteria in the smart street lighting management systems market.

RF mesh retains a role in utilities that prefer privately managed networks with deterministic behavior and long operational experience. Niche use cases include power-line communication in conduits where wireless performance is impaired, and Wi-Fi or short-range variants for campus settings that do not require street-scale range. The mix of technologies persists across regions, but interoperability and certification reduce lock-in and allow mixed fleets to be managed via a single CMS. As standards mature, more cities adopt dual-socket controllers to preserve choice in vendor selection and lifecycle upgrades, which keeps procurement competitive in the smart street lighting management systems market. This balance ensures continuity for existing RF networks while enabling cellular-first scale-outs that deliver the best total cost of ownership.

By Application: Smart Parking and Environmental Sensing Monetize Installed Infrastructure

Traffic optimization accounted for 28% of 2025 deployments as cities applied pole-mounted cameras and sensors to improve signal timing and incident detection across busy corridors. Smart parking is the fastest-growing application at 13.89% CAGR by leveraging the same edge hardware to generate curbside analytics and operational insights that can offset controller costs. Energy analytics and asset management deliver core value through real-time kWh monitoring and fault localization that reduces truck rolls and shortens outage duration. Environmental monitoring and communications backhaul continue to expand, using lighting columns to host air quality, microclimate, and connectivity services through open interfaces. Adaptive lighting tied to presence sensing supports public safety and energy reduction, with guidance available to stage pilots before citywide expansion.

Multi-application designs optimize return on infrastructure by serving multiple departments from a common platform. Cities also tap analytics for resilience planning, improving visibility into outages, traffic patterns, and event-driven demand surges on roads and sidewalks. Software-defined features become key differentiators, and open APIs enable third-party application ecosystems to grow around the lighting backbone. As a result, application portfolios will continue to expand during 2026 to 2031, reinforcing adoption in the smart street lighting management systems market. The ability to monetize new services while meeting safety and compliance priorities solidifies the role of lighting as a neutral host for city data services.

By End User: Industrial Parks and ESCOs Scale Fastest as Lighting-as-a-Service Transfers Energy Risk

Municipalities dominate with 63% share in 2025, supported by replacement mandates, rebates, and energy-accountability targets that reward connected controls. Industrial parks and private campuses are the fastest-growing customers at 14.04% CAGR as operators integrate lighting with security and building systems for tenant experience and sustainability credentials. ESCO-led performance contracts are prevalent, offering guaranteed outcomes and service-level monitoring delivered through the central management platform. LaaS models offer zero-capex options that spread costs over multi-year terms and are anchored in verified energy and maintenance savings. Where utility regulations call for non-wires solutions, luminaire-level controls serve peak shaving and demand response to defer grid upgrades, which creates joint funding opportunities.

Public-private concessionaires bring program management discipline, integrating procurement, deployment, and performance dashboards into a single agreement to meet service targets. This shared-risk approach is valuable in cities with constrained borrowing capacity where long-term savings need to be securitized for investor comfort. Industrial parks value campus-scale connectivity and smart parking, which leverage the same lighting poles and network backbones, boosting adoption in the smart street lighting management systems market. As policies align around data access and portability, buyers demand contractual rights that preserve the flexibility to switch vendors without forfeiting historical data. These factors support diversified end-user growth during the forecast window.

By Deployment Model: Cloud Migration Accelerates as APIs Federate Siloed Systems

Cloud deployments held a 45% share in 2025 and are growing at a 13.67% CAGR as cities shift from on-premises CMS to SaaS platforms that guarantee uptime, enable remote updates, and expose standardized APIs. TALQ-compliant interfaces enable central platforms to aggregate data across lighting, traffic, and sensing, creating shared dashboards for multi-departmental operations. In regions with data-residency mandates, hybrid deployments keep sensitive telemetry local while pushing analytics to the cloud, which balances policy and operational flexibility. Vendors that demonstrate long-term commitment to open standards and data portability are favored in tenders that demand future-proofing. Interoperability reduces the total cost of ownership and accelerates the time to value in the smart street lighting management systems market.

On-premises systems persist where policy prohibits the cloud storage of critical infrastructure data, although device-level security and edge processing can often satisfy many requirements. As cities modernize, service-level guarantees and analytics features encourage contract structures that reward uptime and savings rather than perpetual licensing. Vendors demonstrate the value of cloud-first architectures through ecosystem partnerships that integrate cellular connectivity, small cells, and third-party applications into the lamppost. This momentum supports steady cloud penetration in the smart street lighting management systems market over the forecast horizon as standard APIs become the default. Procurement language increasingly codifies data access and switching rights, which fortifies buyer leverage and mitigates lock-in risk.

Geography Analysis

Europe held a 65% installed-base lead in 2025, reflecting a decade of coordinated retrofits and policy support that elevated connected controls as a compliance tool and operational backbone for utilities. This share underscores a significant portion of the smart street lighting management systems market, with buyers prioritizing TALQ certification to manage multi-vendor fleets over long asset lives. Projects in Brussels and on national highways demonstrate how standardized interfaces ensure CMS interoperability across controllers and luminaires, reducing integration complexity. Field results from European deployments show large and measurable energy savings and maintenance reductions as connected LED programs scale. Compliance with evolving cybersecurity and data access rules is shaping procurement, which favors platforms built on open standards.

Asia-Pacific is the fastest-growing region at a projected 14.12% CAGR as governments align investment for urban upgrades and corridor illumination across expanding megacities. India’s Smart Cities Mission channels significant funding to connected lighting, which stimulates city-scale procurement and multi-application use cases. Australia and New Zealand continue utility-led rollouts, with major cities planning second-generation LED replacements combined with smart controls to deepen savings and improve operations. Vendors adapt product designs to local requirements by balancing cellular and LPWAN coverage with dual-socket controllers to preserve vendor choice. This policy and technology mix strengthens adoption in the smart street lighting management systems market across both retrofit and greenfield deployments.

In North America, large municipal and utility programs focus on fault detection, truck-roll reduction, and analytics-driven maintenance while tapping P3 structures for megaprojects. Chicago’s multi-year program highlights energy and rebate outcomes alongside CO2 reductions, which reinforces the value proposition for other cities. Washington, D.C.’s citywide modernization uses cellular controls and expands digital services on top of the lighting backbone to improve equity and uptime. Off-grid solar systems are also part of the toolkit to deter copper theft and speed restoration in high-risk corridors. In the Middle East, street lighting upgrades anchor larger smart infrastructure programs, with new contracts specifying intelligent transportation features and AI-enabled asset management. Dubai’s multi-year district lighting plan demonstrates how standards-based LED and controls are applied at scale to deliver energy and reliability gains. These patterns together indicate a broadening base for the smart street lighting management systems market across varied funding models and policy environments.

Competitive Landscape

Competition centers on interoperability, lifecycle services, and the breadth of platform features that monetize the lighting backbone. Signify’s acquisition of Telensa expanded access to a large installed base and strengthened its connected lighting software stack and street-level device portfolio. Itron advances IPv6-based networks and SaaS, while multi-vendor certification through TALQ reduces customer lock-in concerns and supports mixed fleets over long asset lives. Flashnet emphasizes ANSI-Zhaga dual-socket controllers to serve North American and European retrofit needs. Many suppliers frame the pole as a service platform for connectivity, sensing, and future apps, which aligns with small-cell partnerships and neutral-host models. This competitive angle reinforces the smart street lighting management systems market as an anchor for city data services.

Companies differentiate with AI-driven maintenance, edge compute attachments, and data-sharing guarantees that support multi-application operations. Ubicquia’s recent platform updates add AI video accessories that run on existing infrastructure to provide curb analytics and adaptive lighting. Vendors position standard device models and management protocols to accelerate troubleshooting and reduce mean time to repair, which improves service-level performance. Partnerships between lighting firms and connectivity providers signal that neutral-host strategies will expand where poles can host small cells with minimal street clutter. Standards organizations continued to harmonize interfaces across controllers, luminaires, and CMS, which lowers integration risk and enables phased upgrades. This supports broader adoption in the smart street lighting management systems market as procurement criteria emphasize open architectures.

M&A and joint ventures are shaping regional footprints and local manufacturing strategies that serve policy goals and supply-chain resilience. Signify and Dixon Technologies formed a joint venture to expand LED and connected lighting manufacturing capacity in India, aligning with domestic production goals. Solar lighting specialists extend reach in theft-prone or power-scarce corridors by eliminating trenching and offering resilient alternatives that deploy quickly. City-led programs that center on measurable energy reductions and equity considerations further shape buying criteria, which favors platforms with verifiable savings and open interfaces. Collectively, these strategic moves help define competitive positions in the smart street lighting management systems market as it expands across varied urban and policy contexts.

Connected Street Lighting Industry Leaders

Signify N.V.

Itron, Inc.

Fonda Technology Co., Ltd.

Ubicquia, Inc.

Schréder S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Flashnet (Lucy Group) partnered with SESCO Lighting, combining the inteliLIGHT platform with SESCO’s U.S. market presence to accelerate smart street lighting adoption, with recent showcases including Washington, D.C.’s 75,000-fixture network.

- November 2025: Zhaga Consortium released Edition 4 of Book 18 to support heritage and decorative luminaires, following the Oct 2024 DALI-TALQ-Zhaga liaison agreement to unify data streams for smart street lighting.

- September 2025: Ashghal in Qatar awarded 13 contracts totaling QR 12 Billion (USD 3.3 Billion) to enhance sustainable infrastructure, including intelligent transportation systems that integrate AI-based digital platforms and smart monitoring for road assets.

- June 2025: Streetleaf completed Phase 1 of 110 solar-powered streetlights at Babcock Ranch, with additional phases planned as part of a resilience-first deployment model.

Global Connected Street Lighting Market Report Scope

Connected streetlights enable the operators to centrally manage the lighting infrastructure through a central management system via wired/wireless network architecture. Sensor suite generally helps the connected streetlight to save energy by detecting several environmental parameters.

The Connected Street Lighting Market is Segmented by Component (Hardware, Software, Services), Connectivity (RF Mesh – Wi-SUN and IEEE 802. 15. 4g, and More), Application (Smart Dimming and Policy-Based Scheduling, and More ), End User (Municipalities and Local Governments, Electric Utilities and Distribution System Operators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| RF Mesh (Wi-SUN, IEEE 802.15.4g) |

| Cellular (NB-IoT, LTE-M, 4G/5G) |

| LoRaWAN |

| Power-Line Communication (PLC) |

| Wi-Fi and IEEE 802.15.4 |

| Smart Dimming and Policy-Based Scheduling |

| Adaptive and Autonomous Lighting (Sensor-Driven) |

| Traffic and Safety Analytics Enablement |

| Energy Analytics and Asset Management |

| Environmental and Microclimate Monitoring |

| Public Wi-Fi and Communications Backhaul |

| Municipalities and Local Governments |

| Electric Utilities and Distribution System Operators |

| Energy Service Companies (ESCOs) |

| Public-Private Concessionaires (PPP Models) |

| Private Campuses and Industrial Parks |

| Cloud |

| On-Premises |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Kenya | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Connectivity | RF Mesh (Wi-SUN, IEEE 802.15.4g) | |

| Cellular (NB-IoT, LTE-M, 4G/5G) | ||

| LoRaWAN | ||

| Power-Line Communication (PLC) | ||

| Wi-Fi and IEEE 802.15.4 | ||

| By Application | Smart Dimming and Policy-Based Scheduling | |

| Adaptive and Autonomous Lighting (Sensor-Driven) | ||

| Traffic and Safety Analytics Enablement | ||

| Energy Analytics and Asset Management | ||

| Environmental and Microclimate Monitoring | ||

| Public Wi-Fi and Communications Backhaul | ||

| By End User | Municipalities and Local Governments | |

| Electric Utilities and Distribution System Operators | ||

| Energy Service Companies (ESCOs) | ||

| Public-Private Concessionaires (PPP Models) | ||

| Private Campuses and Industrial Parks | ||

| By Deployment Model | Cloud | |

| On-Premises | ||

| Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the smart street lighting management systems market?

The smart street lighting management systems market size is USD 2.56 Billion in 2026 and is projected to reach USD 4.82 Billion by 2031 at a 13.49% CAGR.

Which component category leads and which is growing fastest in this market?

Hardware leads with a 62% share in 2025, while software and services are growing fastest at a 13.65% CAGR as buyers prioritize analytics and remote operations.

Which connectivity approach is gaining momentum in smart street lighting?

Cellular options such as NB-IoT and LTE-M are expanding at a 13.73% CAGR due to plug-and-play deployment and reduced gateway overhead, challenging proprietary RF mesh incumbents.

Which applications are seeing the strongest uptake on smart lighting poles?

Traffic optimization led with 28% of deployments in 2025, while smart parking is the fastest-growing use case enabled by the same edge compute and sensors on poles.

Which regions are leading and which are expanding fastest?

Europe held a 65% installed-base lead in 2025, while Asia-Pacific is projected to be the fastest-growing region at a 14.12% CAGR over the forecast period.

What deployment model are cities preferring for management software?

Cloud models held a 45% share in 2025 and are gaining further traction due to open APIs, uptime guarantees, and easier integration with adjacent city systems.

Page last updated on: