Left Ventricular Assist Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

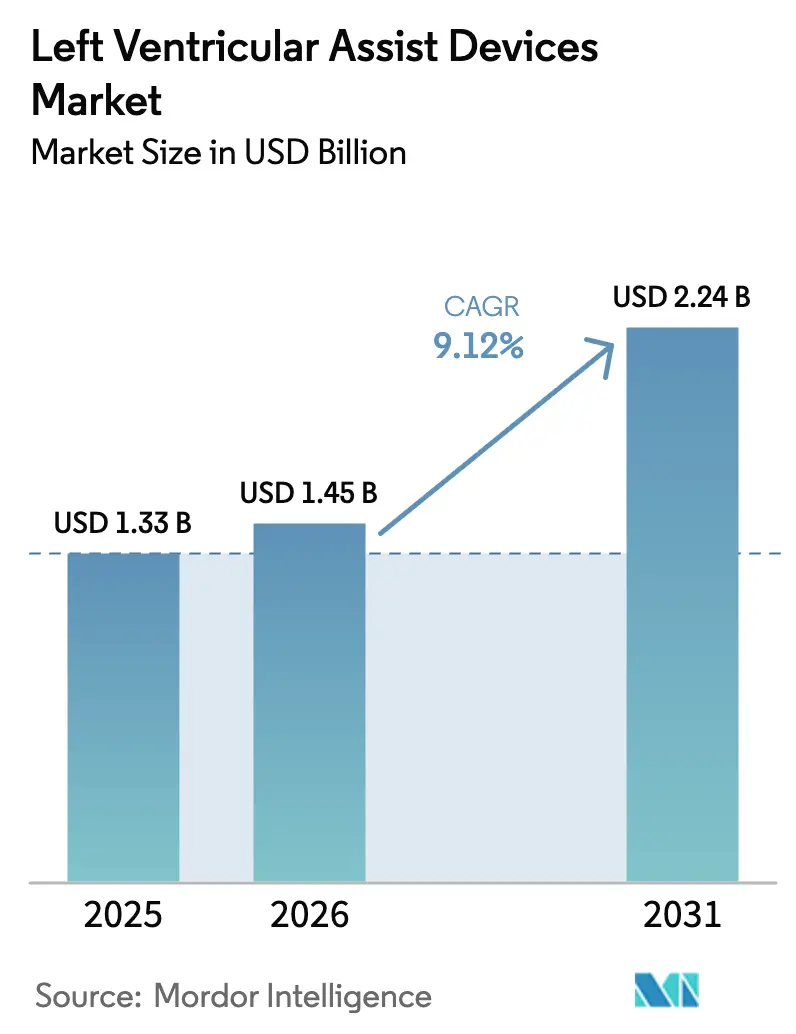

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

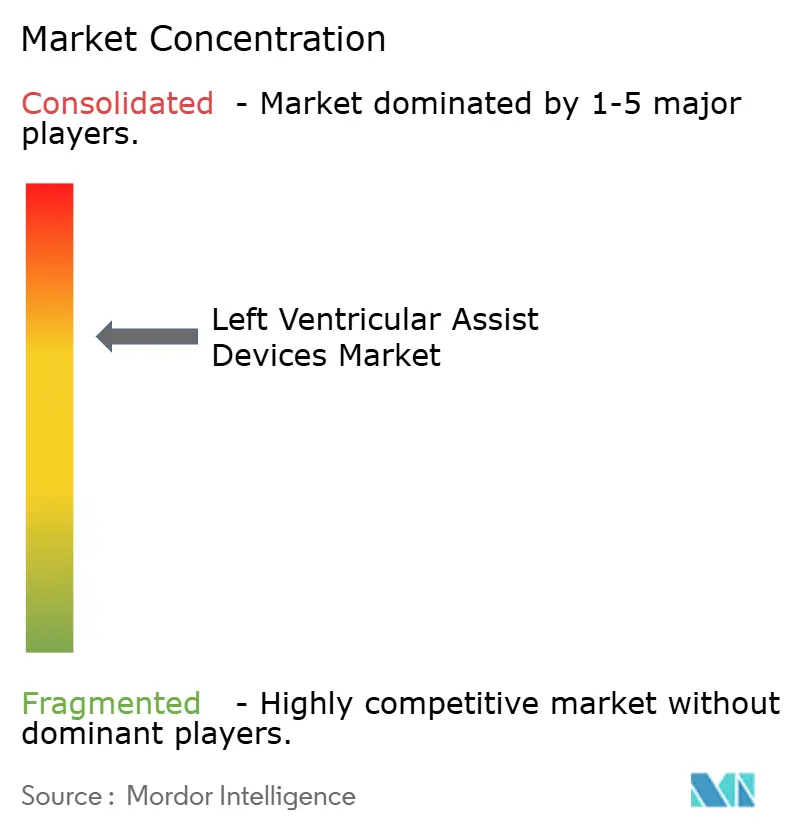

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Left Ventricular Assist Devices Market Analysis by Mordor Intelligence

The left ventricular assist device market size is expected to grow from USD 1.33 billion in 2025 to USD 1.45 billion in 2026 and is forecast to reach USD 2.24 billion by 2031 at 9.12% CAGR over 2026-2031. Rising donor heart shortages, sustained advances in magnetic-levitation pumping systems, and broader reimbursement for destination therapy collectively underpin this multi-year growth trajectory. Centrifugal flow technology now sets the clinical performance standard by lowering stroke and thrombosis risk, which expands physician confidence and device volumes.[1]Mandeep R. Mehra et al., “Fully magnetically centrifugal left ventricular assist device and long-term outcomes: the ELEVATE registry,” European Heart Journal, academic.oup.com Destination therapy already absorbs the bulk of implant activity as transplant waiting lists lengthen, while bridge-to-recovery protocols accelerate on the back of better myocardial-recovery selection tools. North America retains market leadership due to mature reimbursement systems and a dense network of high-volume LVAD centers, but Asia-Pacific registers the fastest regional CAGR thanks to indigenous Chinese programs and Japan’s national registry expansion. Competitive intensity remains moderate after Medtronic withdrew the HVAD, leaving Abbott’s HeartMate 3 as the benchmark product and giving space for fully implantable newcomers such as FineHeart and BiVACOR to gain visibility.

Key Report Takeaways

- By therapy, destination therapy held 59.10% of left ventricular assist device market share in 2025, whereas bridge-to-recovery is projected to rise at 12.18% CAGR through 2031.

- By pump technology, centrifugal flow captured 67.60% revenue share in 2025; axial flow is expected to trail but still expand at 7.98% CAGR to 2031.

- By implant type, continuous-flow implants accounted for 80.55% of the left ventricular assist device market size in 2025, versus a robust 10.05% CAGR outlook for the same category through 2031.

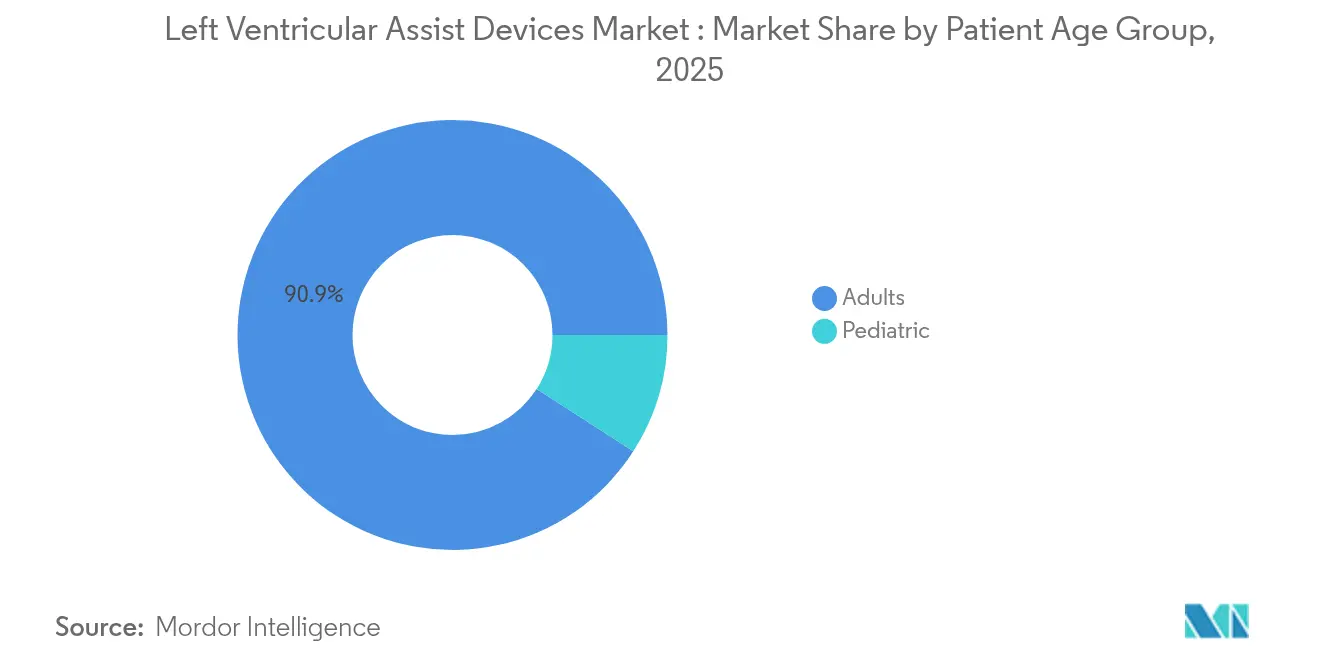

- By patient age, adults dominated with 90.90% share in 2025, while the pediatric segment posts a 11.92% CAGR to 2031.

- By region, North America commanded 41.95% of 2025 revenue, yet Asia-Pacific is forecast to outpace all geographies at 10.98% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Left Ventricular Assist Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organ-Donor Shortage Accelerating Adoption Of Durable LVADs | +2.1% | Global, with acute impact in North America & Europe | Long term (≥ 4 years) |

| Rapid Shift Toward Advanced LVADs | +1.8% | Global, led by North America & EU | Medium term (2-4 years) |

| Expanding Reimbursement Coverage For Destination Therapy | +1.4% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Miniaturization Enabling Minimally-Invasive Implantation | +1.2% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| AI-Driven Remote Monitoring Reducing Post-Discharge Costs | + 0.9% | North America & EU, pilot programs in APAC | Short term (≤ 2 years) |

| Government Initiatives and Emerging LVAD Programs | +0.7% | APAC core, with spillover to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Organ-donor shortage accelerating adoption of durable LVADs

Long transplant waiting lists keep pushing clinicians toward destination therapy as a permanent alternative to heart replacement. Five-year survival with HeartMate 3 now exceeds 63% in real-world registries, a level once attainable only with transplantation. Regulators have responded by classifying LVADs as definitive treatment and Medicare has extended coverage beyond bridge-to-transplant coding. Providers consequently build long-term support programs, invest in remote monitoring, and allocate ICU resources for chronic LVAD cohorts. The budget impact is meaningful because each patient carries multi-year follow-up costs, yet hospitals balance this against the expense of repeated decompensation admissions.

Rapid shift toward advanced LVADs

Third-generation centrifugal pumps employ full magnetic levitation that removes mechanical bearings and minimizes blood trauma. ARIES-HM3 data show aspirin-free regimens cut bleeding events by 40% without higher thrombosis risk, an outcome that broadens the eligible pool to patients with bleeding tendencies. Smaller pump footprints lend themselves to thoracotomy approaches instead of sternotomy and shorten ICU stays.[2]Journal of Thoracic and Cardiovascular Surgery, “Thoracotomy-based implant technique for HeartMate 3,” jtcvs.org With FineHeart and BiVACOR aiming for fully implantable designs, the performance baseline keeps moving upward.

Expanding reimbursement coverage for destination therapy

Cost-utility models peg the incremental cost per QALY at USD 102,587, below willingness-to-pay thresholds in the United States. CMS added destination therapy to CPT 33975, prompting commercial insurers to align policy language. In Europe, health technology agencies in Germany, the UK, and France have begun systematic budget impact assessments to incorporate LVAD programs into standard care. These actions increase procedure volumes at specialized cardiac centers that already own care pathways.

Miniaturization enabling minimally-invasive implantation

Thoracotomy implantation demonstrates 85% event-free survival at 6 months while reducing surgical trauma. Smaller pumps also unlock pediatric indications that were previously size-restricted. Coupling miniaturization with robotic assistance enhances placement precision and could ultimately shift selected implants to ambulatory surgery settings. Early adopters position less-invasive routes as differentiators to win referrals from moderate-volume hospitals.

Restraints Impact Analysis of Left Ventricular Assist Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device Explant Revision Costs Burden Hospital Budgets | -1.3% | Global, acute in cost-sensitive markets | Medium term (2-4 years) |

| Adverse Events Associated LVADs | -1.1% | Global, with regional variation in management | Long term (≥ 4 years) |

| Supply-Chain Constraints For Rare-Earth Magnetic Bearings | -0.8% | Global, concentrated in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Limited Pediatric-Size Pump Availability | -0.6% | Global, acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Device explant revision costs burden hospital budgets

Roughly one in four recipients requires a surgical revision within 2 years, and each episode can exceed USD 50,000 in direct hospital expense.[3]ESC Heart Failure, “Economic aspects of long-term LVAD treatment for chronic heart failure,” onlinelibrary.wiley.com Safety-net hospitals serving underinsured populations face unreimbursed charges that dampen program expansion. The unpredictability of revision caseloads complicates OR scheduling and inventory planning, prompting administrators to limit LVAD capacity or partner with higher-volume centers for complex cases.

Adverse events associated with LVADs

Despite hemocompatibility advances, stroke rates remain higher than in medically managed heart-failure cohorts and driveline infections still trigger long antibiotic courses or pump exchange. Physicians must weigh these risks against potential survival gains, especially for borderline candidates. The psychological weight of living with an external driveline adds another layer of reluctance for some patients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Left Ventricular Assist Devices Market Segment Analysis

By Pump Technology:

Centrifugal flow sustains clinical dominanceCentrifugal systems controlled 67.60% of 2025 revenue and are projected to post an 11.12% CAGR, reflecting clinicians’ preference for devices with near-physiologic flow and reduced shear stress. The left ventricular assist device market size for centrifugal technology is therefore expected to widen its gap over axial flow through 2031. HeartMate 3’s compelling stroke-reduction profile remains the primary adoption trigger.

Axial flow still fills niche needs when small pump footprints matter, although centrifugal designs are nearing similar volumes while offering superior hemocompatibility. Continuous improvement in magnetic levitation firmware and flow-estimation algorithms supports better autoregulation and long-term durability.

By Implant Type:

Continuous-flow implants near universal adoptionContinuous-flow implants secured 80.55% share in 2025 and are tracking a 10.05% CAGR as remaining pulsatile devices age out of practice. Hospitals gravitate toward systems with smaller driveline ports, lower acoustic signatures, and remote-programming capability. Left ventricular assist device market share for this category will likely exceed 84.80% by 2031 given the discontinuation of most pulsatile platforms.

Clinical workflows are optimized for continuous-flow post-operative management, limiting incentives to keep legacy pulsatile infrastructure. Innovations toward fully implantable drivers could push continuous-flow even closer to the physiologic ideal and diminish infection risk further.

By Therapy:

Destination therapy cements primary roleDestination therapy commanded 59.10% revenue in 2025 as transplant-ineligible patients increasingly gain coverage. The left ventricular assist device market size linked to destination therapy will expand in parallel with payer acceptance. Bridge-to-recovery shows the highest growth at 12.18% CAGR because better imaging and biomarker profiling now identify candidates likely to regain native function.

Hospitals with recovery programs benefit from shorter device support duration and lower lifetime cost profiles. Bridge-to-transplant volumes remain flat yet essential, safeguarding stability for candidates waiting on scarce donor hearts.

By Patient Age Group:

Pediatric volumes rise from small baseAdults still occupy 90.90% of procedures, but pediatric implant counts are climbing at 11.92% CAGR. The left ventricular assist device market size for children remains modest, yet the clinical demand is disproportionate to supply. Berlin Heart EXCOR continues to bridge infants to transplant, while adolescent usage of smaller continuous-flow pumps is gaining institutional review board clearance.

Growth drivers include national funding for congenital heart disease programs and cross-center data sharing that diffuses best practice. Device miniaturization and pump flow customization will remain critical to unlock broader pediatric eligibility.

By End User:

Specialty centers drive outcomes leadershipHospitals carried 62.65% of 2025 revenue because they own the installed OR base, yet specialty cardiac centers are expanding faster at 10.42% CAGR. Concentrated expertise translates into lower complication rates and stronger payer negotiations. The left ventricular assist device market size captured by these centers is set to rise as referral patterns tilt toward proven programs.

Ambulatory surgical centers could absorb follow-up driveline checks and speed ramp tests, freeing tertiary ICUs for complex revisions. Nevertheless, regulatory frameworks will drive a gradual transition to non-hospital settings to ensure patient safety.

Geography Analysis

North America Left Ventricular Assist Devices Market

North America represents the single largest geography with 41.95% revenue in 2025, anchored by Medicare reimbursement for destination therapy and high clinician familiarity. Registries such as INTERMACS inform evidence-based protocols that sustain favorable outcomes benchmarks. Market penetration still varies by state depending on transplant-center density, but remote monitoring could equalize access across rural catchments.

APAC Left Ventricular Assist Devices Market

Asia-Pacific records the fastest expansion at 10.98% CAGR through 2031, propelled by China’s push for domestic LVAD manufacturing and Japan’s structured J-MACS data collection. Chinese authorities classify LVADs as strategic domestic devices, shortening regulatory timelines and lowering costs. India’s private cardiology networks also import centrifugal pumps to address its growing advanced-heart-failure burden.

Europe Left Ventricular Assist Devices Market

Europe remains a mature but dynamic arena. Germany leads implant volumes due to early adoption and national reimbursement that favors high-volume centers. The UK and France maintain centralized service models to curb costs while standardizing care quality. Eastern Europe offers upswing potential once funding mechanisms for advanced heart failure broaden beyond transplant referral pathways.

Competitive Landscape

Abbott dominates current share with HeartMate 3, benefiting from maglev performance and the absence of Medtronic’s HVAD, recalled in 2021. Competitors now chase differentiation via fully implantable or total artificial heart configurations. FineHeart received French authority approval for first-in-human Flowmaker, while BiVACOR secured FDA breakthrough designation for its rotary total artificial heart.

Pediatric-focused suppliers, led by Berlin Heart, maintain niche leadership owing to specialized device design and regulatory exemptions for compassionate use. Device makers eye AI-enabled monitoring partnerships to embed data services that raise switching costs and extend revenue beyond hardware sales. Strategic alliances between pump developers and telehealth platforms are emerging to bundle remote diagnostics into procurement contracts.

From a supply chain standpoint, rare-earth magnet sourcing is a shared vulnerability. Manufacturers are hedging through dual-supplier policies or exploring ceramic bearing alternatives to insulate against geopolitical disruption. Intellectual-property moats center on magnetic levitation algorithms, driveline seal technology, and battery chemistry, shaping ongoing litigation and licensing agreements.

Left Ventricular Assist Devices Industry Leaders

Medtronic

Abbott

Jarvik Heart Inc.

Berlin Heart GmbH

Johnson and Johnson (Abiomed)

- *Disclaimer: Major Players sorted in no particular order

Left Ventricular Assist Devices Market Companies Covered in this Report

- Abbott Laboratories

- Medtronic

- Johnson and Johnson (Abiomed)

- Berlin Heart

- Jarvik Heart

- Terumo

- CorWave

- Evaheart

- Relitech Systems

- Leviticus Cardio

- Calon Cardio-Technology

- FineHeart

- CH Biomedical

- Windmill Cardiovascular

- VentriFlo

- Magenta Medical

Recent Industry Developments in Left Ventricular Assist Devices Market

- June 2025: FineHeart obtained national approval to launch the first-in-human study of its Flowmaker fully implantable LVAD

- October 2024: Abbott began a trial combining CardioMEMS remote sensors with HeartMate 3 to examine integrated heart-failure management benefits

Left Ventricular Assist Devices Market Report Scope and Research Methodology

Market Definition and Coverage

Mordor Intelligence defines the left ventricular assist devices (LVAD) market as the global sales revenue generated by durable or temporary mechanical pumps that support the left ventricle for bridge-to-transplant, destination therapy, bridge-to-recovery, or bridge-to-candidacy indications. Revenue is counted at the device level and covers implantable continuous-flow, extracorporeal pulsatile, controllers, driveline kits, and battery packs supplied by medical-device companies to hospitals and specialty cardiac centers.

Scope exclusion: peripheral pumps used solely for right-heart or total artificial heart support are excluded.

Segments Covered in This Report

- By Pump Technology

- Axial Flow

- Centrifugal Flow

- By Implant Type

- Implantable Continuous-Flow

- Extracorporeal Pulsatile

- By Therapy

- Bridge-to-Transplant (BTT)

- Destination Therapy (DT)

- Bridge-to-Recovery (BTR)

- Bridge-to-Candidacy (BTC)

- By Patient Age Group

- Adult (≥18 yrs)

- Pediatric (<18 yrs)

- By End User

- Hospitals

- Specialty Cardiac Centers

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews and targeted surveys with cardiothoracic surgeons, VAD program directors, perfusionists, and hospital supply managers across North America, Europe, and high-growth Asia-Pacific markets validated incidence assumptions, device average selling prices, and post-HVAD withdrawal brand shifts. These exchanges also clarified real-world penetration of fully implantable systems and regional reimbursement cut-offs.

Desk Research

Our analysts began with public health datasets such as the WHO Global Health Observatory, CDC heart failure prevalence files, Eurostat surgical procedure tables, and UN demographic outlooks, which helped map the eligible patient pool. We overlaid import-export codes from UN Comtrade and national customs portals to confirm shipment values and leading trade corridors. Regulatory registries, including the FDA PMA database and Eudamed, revealed annual LVAD approvals and adverse-event alerts that shape uptake curves. Company 10-Ks, select investor decks, and peer-reviewed journals in Circulation and the Journal of Heart & Lung Transplantation provided price trends and survival outcomes. Subscription sources like D&B Hoovers and Dow Jones Factiva furnished hard sales references. The sources listed are illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down construct starts with country-level end-stage heart-failure prevalence, transplant wait-list additions, and LVAD implantation ratios, which are then multiplied by weighted ASPs. Bottom-up checkpoints, supplier shipment roll-ups, sampled tender awards, and channel checks tighten variance to within five percent. Key variables include donor-heart availability, continuous-flow adoption rate, guideline expansions for destination therapy, exchange-rate moves, and device ASP erosion. Five-year projections rely on multivariate regression with heart-failure incidence, donor shortage delta, and reimbursement coverage breadth as predictors, followed by ARIMA smoothing to handle short time series. Gaps in low-visibility countries are bridged using regional proxy ratios anchored to verified implant volumes.

Data Validation & Update Cycle

Outputs undergo two-stage peer review, anomaly scans versus hospital implant logs and trade statistics, and recalibration if deviations exceed preset thresholds. Mordor refreshes the model annually and reopens interviews when material events, major recalls, pivotal trial readouts, and policy shifts occur.

How Mordor Intelligence's Left Ventricular Assist Devices Market Size Compares to Other Published Estimates

Published estimates frequently diverge because each firm defines vents, flow types, and therapy windows differently and applies its own refresh cadence.

Our disciplined variable selection and dual-pass validation keep the baseline balanced.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.33 B | Mordor Intelligence | - |

| USD 1.73 B | Global Consultancy A | Includes transcutaneous VAD consumables and pediatric RVAD sales in total |

| USD 2.70 B | Trade Journal B | Reports combined LVAD + RVAD market therefore inflates base |

| USD 1.49 B | Regional Consultancy C | Uses historic price list averages, overlooks recent ASP cuts after HVAD exit |

Taken together, the comparison shows that Mordor's clearly bounded definition, annual refresh, and cross-checked volumes yield a dependable reference point that executives can trace to transparent, reproducible steps.

Key Questions Answered in the Report

What is the projected size of the left ventricular assist device market by 2031?

The market is expected to reach USD 2.24 billion by 2031 given a 9.12% CAGR projection.

Why are centrifugal flow pumps preferred over axial designs?

Centrifugal pumps use magnetic levitation that cuts stroke and thrombosis rates, improving long-term survival compared with older axial systems.

How does destination therapy differ from bridge-to-transplant?

Destination therapy treats patients who are not eligible for transplant, while bridge-to-transplant maintains candidates until a donor heart becomes available.

Which region shows the fastest LVAD market growth?

Asia-Pacific posts the quickest CAGR at 10.98% because of Chinese domestic production and Japan’s expanding registry infrastructure.

What key technology trends could reshape the LVAD landscape?

Fully implantable devices, AI-enabled remote monitoring, and continued pump miniaturization are poised to improve outcomes and widen patient eligibility.

What are the main challenges limiting wider LVAD adoption?

High revision costs, adverse events such as stroke and infection, and supply constraints for rare-earth magnets collectively restrain faster uptake.

Page last updated on: