Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

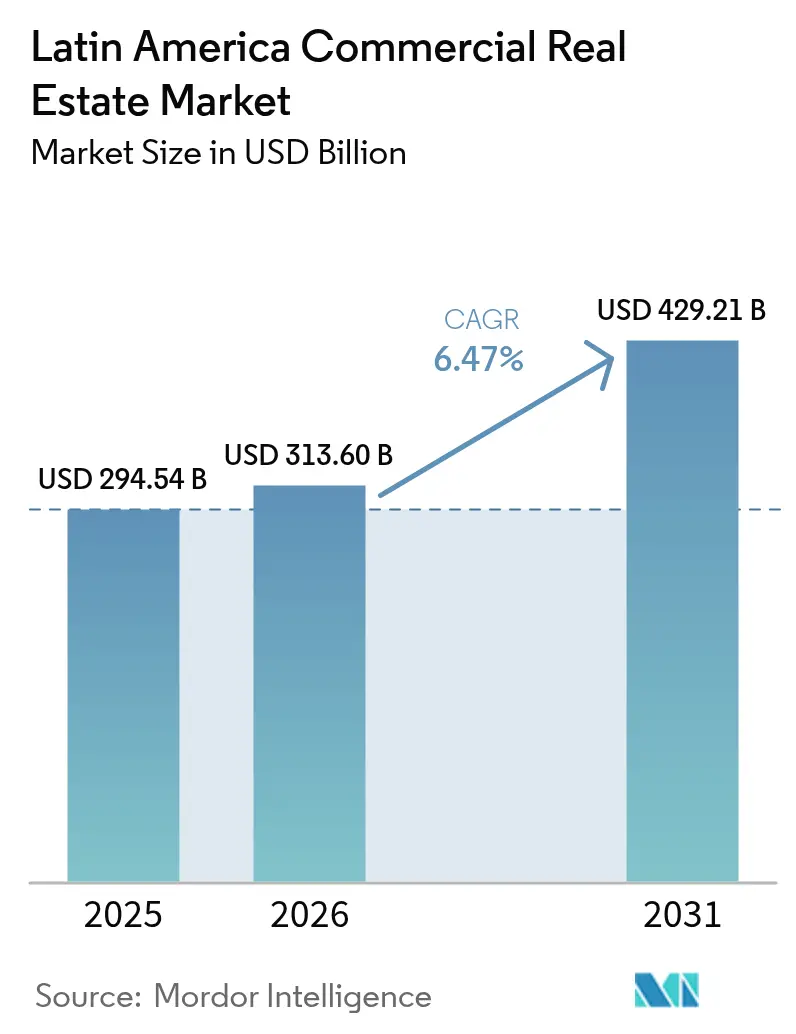

| Base Year Market Size (2025) | USD 294.54 Billion |

| Market Size (2026) | USD 313.6 Billion |

| Market Size (2031) | USD 429.21 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

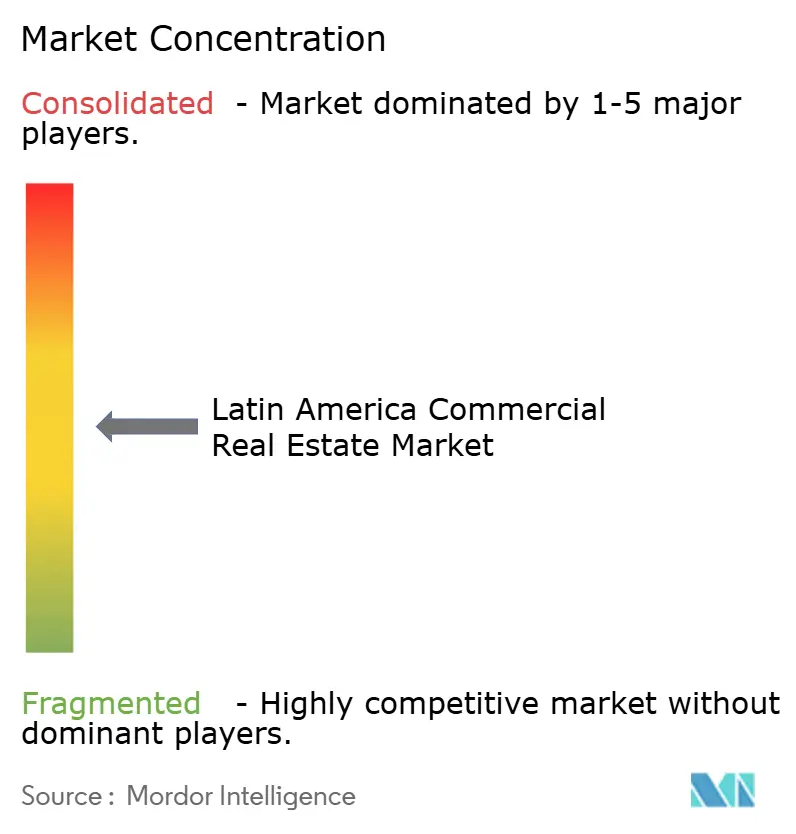

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Commercial Real Estate Market Analysis by Mordor Intelligence

The Latin America Commercial Real Estate Market size in 2026 is estimated at USD 313.6 billion, growing from 2025 value of USD 294.54 billion with 2031 projections showing USD 429.21 billion, growing at 6.47% CAGR over 2026-2031. Strong tenant appetite for Grade-A logistics parks, deepening digital commerce penetration, and steady institutional capital inflows have created a clear runway for expansion. Nearshoring has intensified demand along Mexico’s Bajío and northern border corridors, while Brazil’s intermodal hubs continue to attract modern distribution assets. Corporates appear more willing to lease than to buy, which keeps vacancy tight in prime submarkets and lifts effective rents despite construction-cost pressure. At the same time, mixed-use redevelopments in São Paulo, Mexico City, Bogotá, and Santiago are drawing lifestyle-driven foot traffic, helping landlords diversify income streams and hedge against single-asset downturns. Capital markets activity remains supportive as regional REITs, FIBRAs, and FIIs recycle assets to fund new pipelines and as global investors hunt for cash-flow visibility at yields well above advanced-economy benchmarks.

Key Report Takeaways

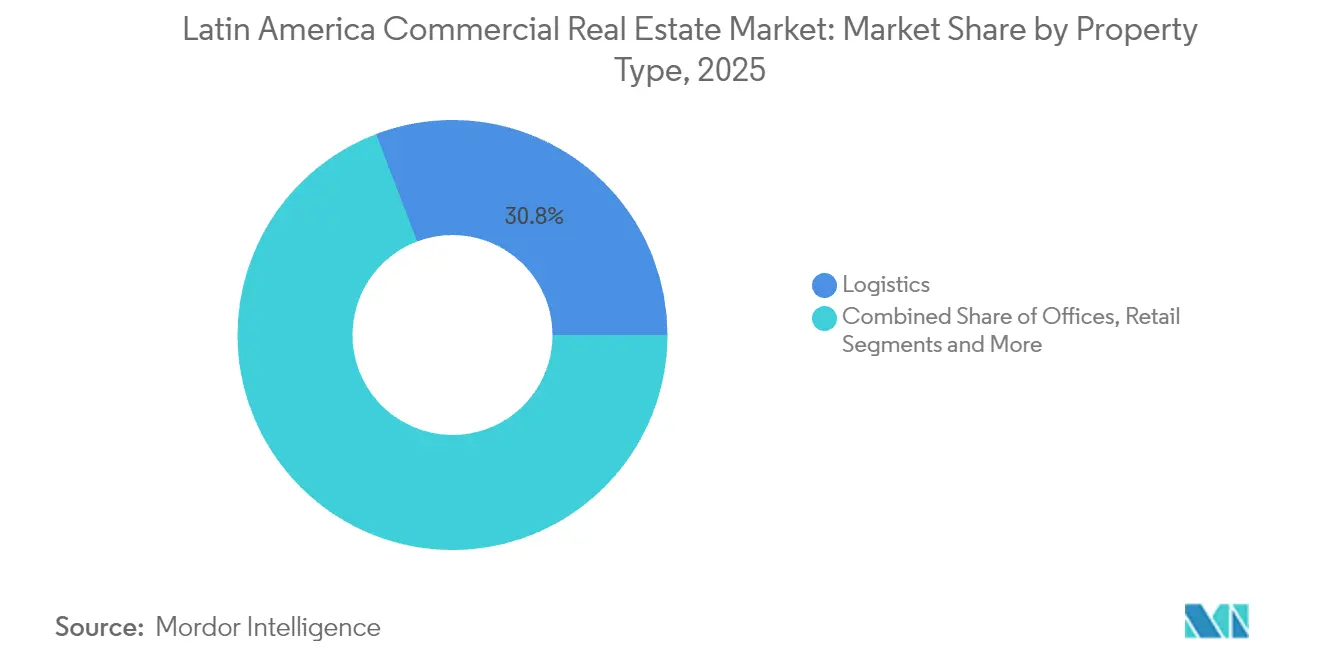

- By property type, logistics captured 30.78% revenue share in 2025; hospitality is forecast to expand at a 7.08% CAGR through 2031.

- By business model, the rental segment held 67.65% of the Latin America commercial real estate market share in 2025, while it is projected to compound at a 7.31% CAGR through 2031.

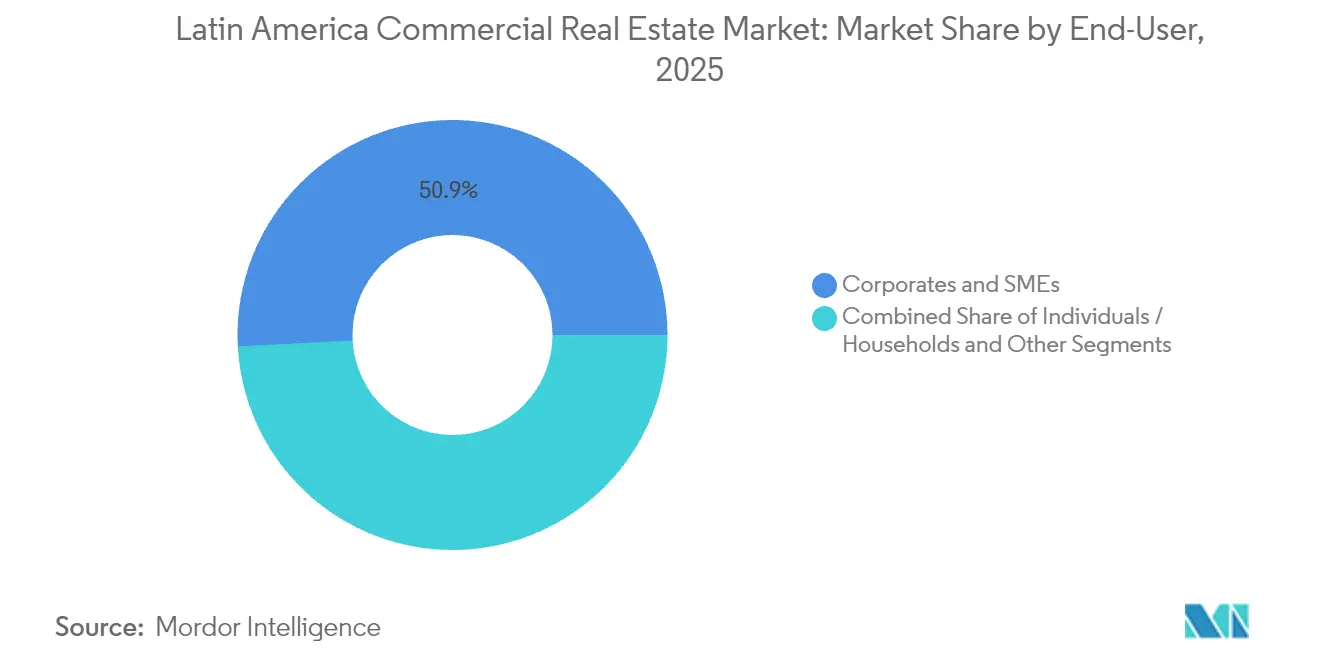

- By end-user, corporates and SMEs accounted for 50.85% of the Latin America commercial real estate market size in 2025 and are advancing at a 7.74% CAGR through 2031.

- By geography, Brazil led with 39.85% share of regional value in 2025, whereas Mexico is projected to expand at an 8.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring and “Mexico+” manufacturing wave boosting industrial parks and logistics demand | +1.8% | Mexico, Brazil, Colombia | Medium term (2-4 years) |

| E-commerce penetration rising, driving modern warehousing, last-mile hubs, and cold chain | +1.5% | Brazil, Mexico, Argentina, Chile | Short term (≤ 2 years) |

| Tourism rebound and experiential retail lifting hospitality and mixed-use projects | +0.9% | Colombia, Chile, Dominican Republic, Peru | Short term (≤ 2 years) |

| Infrastructure upgrades creating new development corridors | +1.2% | Brazil, Peru, Mexico | Long term (≥ 4 years) |

| Institutionalization via REITs, FIBRAs, and FIIs channeling global capital into Grade-A assets | +1.0% | Mexico City, São Paulo, Santiago, Bogotá | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nearshoring And “Mexico+” Manufacturing Wave Boosting Industrial Parks And Logistics Demand

Near-term leasing momentum is strongest where electronics, automotive, and appliance producers relocate capacity to sidestep tariff risk. Plants cluster along Mexico’s Bajío spine and the northern border, pushing vacancy for Class-A sheds below 3% in some submarkets. Vesta has added land in Guadalajara and Monterrey to ensure it can pre-lease buildings before slab pour, a tactic that anchors cash flow early in the development cycle. FIBRA Prologis financed its expansion through a 100 million-certificate issuance, confirming institutional conviction in USMCA-linked growth. Colombia’s free-trade zones are following a similar script, positioning Bogotá and Medellín as secondary embassies for light assembly. The overall effect is a structural shift that favors logistics as the largest and fastest-growing slice of the Latin America commercial real estate market.

E-Commerce Penetration Rising, Driving Modern Warehousing, Last-Mile Hubs, And Cold Chain

Online retail volumes did not retreat after the pandemic, pressing occupiers to secure urban cross-dock sites and temperature-controlled space. The USD 34.8 million purchase of a Vallejo facility by FIBRA Macquarie exemplifies the pricing premium for last-mile proximity in Mexico City, where embedded rent reversion exceeds 20% at lease rollover. Prologis disclosed USD 38 million in quarterly NOI from its “Other Americas” portfolio, evidence that click-to-doorstep supply chains rely on large-scale distribution nodes. Yet refrigerated stock remains sparse outside São Paulo, Mexico City, and Santiago, leaving perishables at risk and creating an investable gap for build-to-suit developers. The World Bank ranks Latin America below the OECD average on logistics efficiency, underlining the upside for sponsors who can integrate real-time tracking, energy-efficient systems, and accredited food-safety protocols[1]World Bank, “Logistics and Trade Facilitation in Latin America,” worldbank.org . Investor appetite for such assets remains robust given the stickiness of tenants once mission-critical cold chains come on-line.

Tourism Rebound And Experiential Retail Lifting Hospitality And Mixed-Use Projects

International arrivals climbed to 97% of 2019 levels in 2024, restoring hotel occupancy and boosting retail sales in leisure corridors. Parque Arauco reports that six flagship malls now generate over 60% of NOI, with tenant sales at Parque Arauco Kennedy topping USD 606 million on a trailing twelve-month basis. Developers are moving away from enclosed centers in favor of open-air complexes that blend entertainment, food, and local craft vendors, formats that encourage longer dwell time and higher spend per visit. Peru’s USD 16.8 billion infrastructure pipeline includes airport and highway upgrades that shorten travel to Cusco and Arequipa, further expanding the catchment for hospitality venues. Anchored by these dynamics, tourism-linked projects provide diversified revenue streams and counter-cyclical traits that enhance portfolio resilience.

Infrastructure Upgrades Creating New Development Corridors

Public–private spending on ports, metros, and highways is re-charting freight routes and elevating land values. Brazil alone has earmarked roughly USD 74 billion through 2029 for logistics connectors that reduce transit costs between hinterland farms and coastal export terminals. In Peru, Callao Port expansion and regional road concessions widen Lima’s retail and industrial reach, supporting new submarkets for speculative warehouse builds. Mexico City, Guadalajara, and Monterrey are extending metro lines that compress commute times and raise foot traffic to mixed-use precincts. Environmental standards now feature in bid documents, nudging sponsors toward LEED-compliant designs and renewable-energy sourcing, which in turn unlock cheaper green-bond funding. Large-scale landlords and infrastructure funds are best placed to capture these synergies and recycle capital across overlapping asset classes.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic volatility and FX risk complicating funding and underwriting | -1.3% | Argentina, Brazil, Mexico | Short term (≤ 2 years) |

| Regulatory, permitting, and land-title complexity varying widely by country and city | -0.8% | Argentina, Brazil, Peru | Medium term (2-4 years) |

| Construction inflation, high financing costs, and uneven power/logistics reliability squeezing feasibility | -0.9% | Mexico, Brazil, Colombia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Volatility And FX Risk Complicating Funding And Underwriting

Currency swings and policy shifts can erase underwriting buffers overnight. Argentina’s peso fell 11% before stabilizing at 1,195 per dollar following April 2025 liberalization, prompting sponsors to hedge or price deals in hard currency. Mexico’s rate cuts to 7.25% eased debt service but did not halt a Q3 construction dip triggered by U.S. tariff uncertainty. Brazil’s real has traded within a 15% band for 18 months, forcing foreign investors to weigh costly hedges against potential translation losses. Even Prologis notes that a 10% adverse FX move could trigger USD 152 million in derivative settlements, underlining exposure for the most sophisticated players. As a result, lenders demand wider spreads or additional equity, raising total project costs and thinning achievable leverage.

Regulatory, Permitting, And Land-Title Complexity Varying Widely By Country And City

Approval timelines range from 18 months in Chile to over 36 months in parts of Argentina, adding uncertainty to development pro-formas[2]Banco Central de Chile, “Monetary Policy Report December 2024,” bcentral.cl . In Peru, indigenous consultations can pause logistics projects for up to two years, a risk often underestimated by first-time entrants. Brazil’s municipal codes differ block by block, subjecting sponsors to overlapping heritage and environmental reviews that stretch design phases. Argentina’s RIGI scheme centralizes federal oversight for projects above USD 200 million, yet provincial veto powers remain, leaving title risks unresolved until late in the cycle. These hurdles discourage speculative pipelines and tilt investment toward brownfield or sale-leaseback structures where entitlement risk is lower.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Logistics Captures Nearshoring Premium

Logistics held 30.78% of the Latin America commercial real estate market share in 2025, cementing its status as the largest property segment. Occupancy for Class-A industrial space in Mexico’s border zones slipped below 3%, pushing effective rents to record highs. The category is forecast to post a 7.05% CAGR through 2031, comfortably ahead of office and retail growth rates.

Persistent reshoring by electronics and auto assemblers underpins forward leasing, encouraging landlords such as Vesta to amass 148 acres of ready-to-build land in Guadalajara and Monterrey. FIBRA Macquarie’s Vallejo acquisition, complete with 6.9% annual rent step-ups, shows how last-mile footprints in land-scarce capitals command pricing power. Prologis reports USD 38 million in quarterly NOI from “Other Americas,” validating the thesis that global supply chains require scalable, modern logistics networks. Offices remain vital for finance and tech clusters in São Paulo, Mexico City, Santiago, and Bogotá, though hybrid work compresses space per employee. Prime towers with LEED badges and wellness amenities enjoy firm demand, while Class-B assets see double-digit vacancy and flat rents. Retail is split between struggling secondary malls and outperforming open-air lifestyle centers, with Parque Arauco achieving 96.4% occupancy across a 1.18 million-square-meter regional portfolio. Hospitality assets benefit from the tourism rebound, and data centers attract fresh capital as cloud providers expand Latin American nodes, highlighted by Brookfield’s search for a partner in Ascenty.

By Business Model: Rental Dominance Reflects Balance-Sheet Flexibility

Rental structures controlled 67.65% of total transaction value in 2025, making them the dominant model in the Latin America commercial real estate market. This share is expected to rise at a 7.31% CAGR as corporates prioritize balance-sheet agility during volatile currency cycles. FIBRA Prologis’ 100 million-certificate offering highlights the liquidity available for landlords willing to retain ownership and distribute predictable cash.

Parque Arauco discloses that fixed minimum rents account for roughly 85% of its revenue, an arrangement that shields landlords from sales volatility while granting tenants stability. Although Brazil’s upcoming 5% tax on FII distributions could prompt portfolio reallocations, the net effect is likely a tilt toward institutional vehicles that can optimize withholding via double-tax treaties or offshore feeder funds. The sales segment, at 32.35% share, remains relevant for developers looking to recycle capital, but it will cede ground to rental models because investors favor long-duration income streams in inflation-indexed leases.

By End-User: Corporates And SMEs Lead Lease Absorption

Corporates and SMEs made up 50.85% of occupied space in 2025, the largest slice of the Latin America commercial real estate market and the cohort projected to grow fastest at a 7.74% CAGR through 2031. Blue-chip manufacturers and e-commerce operators are locking in 5- to 10-year leases with CPI or dollar indexation that protect landlord returns.

FIBRA Macquarie’s Vallejo deal features a triple-net structure with pass-throughs on insurance and maintenance, illustrating tenant willingness to absorb operating costs for strategic locations. End users such as experiential retail chains value flexible, modular footprints that can adapt to omnichannel fulfillment, boosting demand for mixed-use urban precincts. Individuals, households, and public bodies hold the balance of space; their growth is tied to multifamily conversions of obsolete office towers and the rollout of co-living units in transit-oriented zones.

Geography Analysis

Brazil commanded 39.85% of regional value in 2025, underpinned by São Paulo’s 10 million-square-meter office stock, Rio’s waterfront ‘Porto Maravilha’ regeneration, and the fast-expanding industrial belt serving consumer and export demand. Prologis’ “Other Americas” arm, which includes Brazil, generated USD 38 million in Q1 2025 NOI, showcasing the scale of institutional capital in Brazilian logistics. A forthcoming 5% tax on FII distributions has already nudged some retail investors toward direct deals, yet large sponsors remain committed given infrastructure outlays of USD 74 billion that promise smoother freight flows and stronger asset-level cash generation.

Mexico is set to post the quickest trajectory, with an 8.01% CAGR projected through 2031 as USMCA rules-of-origin provisions push electronics and auto production south. FIBRA Prologis controls 46.9 million square feet across six industrial hubs and is adding assets via its latest certificate issuance, indicating conviction in long-run tenant demand. Banco de México’s policy-rate cuts have trimmed funding costs, although near-term starts dipped due to tariff uncertainty; Vesta’s land banking in Guadalajara and Monterrey underscores developer confidence once policy clarity returns. Argentina, Chile, Colombia, and Peru form the next tier. The IMF-backed stabilization program in Argentina, coupled with the RIGI incentive scheme, attracted USD 19 billion in project submissions by mid-2024, reviving dormant logistics corridors. Chile logged 16% tourism growth in 2024, sustaining high occupancy at Parque Arauco’s 534,000-square-meter domestic portfolio. Colombia enjoyed a 37% jump in arrivals, sparking hotel and mixed-use builds in Bogotá and Medellín. Peru grew 3.1% in 2024 and maintains a USD 16.8 billion infrastructure pipeline that is opening land in Lima’s periphery to new retail and office schemes. Smaller Central American and Caribbean markets remain niche plays where tourism, free-trade-zone manufacturing, and agricultural logistics can deliver outsized returns but carry higher liquidity and political-risk premiums.

Competitive Landscape

Competition is moderate yet tightening as global REITs and regional platforms consolidate prime stock. Prologis, Brookfield, and FIBRA Uno leverage balance-sheet heft and co-investment structures to secure trophy logistics and mixed-use assets, often at cap-rate levels unavailable to smaller peers. Prologis earns both asset income and USD 21.2 million in quarterly management fees by syndicating stakes to institutional partners, a dual-revenue model that reduces concentration risk.

Regional champions such as Vesta, Parque Arauco, and BR Malls retain localized advantages: long-standing tenant ties, intimate knowledge of zoning nuance, and brand recognition that supports pre-leasing. Vesta’s 92.3% occupancy across 41.7 million square feet speaks to disciplined underwriting and minimal churn, even in soft quarters. Parque Arauco manages a USD 713 million pipeline across Chile, Peru, and Colombia, balancing exposure across economies and spreading development risk.

Innovation gaps persist. Cold-chain specialists, data-center operators like Ascenty, and PropTech platforms that automate leasing and maintenance can still carve space as incumbents focus on core business lines. Sustainability credentials are emerging as a competitive moat, with ISO 14001 compliance and LEED or EDGE certification now baseline requirements for multilateral lenders. Parque Arauco has set science-based emission-reduction targets across scopes 1, 2, and 3, highlighting how large landlords can differentiate on ESG performance.

Latin America Commercial Real Estate Industry Leaders

Brookfield Asset Management

Fibra Uno (FUNO)

Prologis

BR Malls Participações

Multiplan Empreendimentos

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: FIBRA Macquarie México acquired a 250,000 sq ft Vallejo logistics asset in Mexico City for USD 34.8 million, secured by a three-year triple-net lease with 6.9% annual escalations and 20% reversion potential at expiry.

- April 2025: Prologis reported Q1 2025 results, noting 276 properties and USD 38 million NOI in its “Other Americas” segment plus USD 4.55 billion of co-investment AUM.

- February 2024: FIBRA Prologis launched a 100 million-certificate global offering to fund accretive acquisitions across its 46.9 million-sq-ft Mexican platform.

- January 2024: Vesta posted USD 67.3 million in revenue on 92.3% occupancy, while land-banking 148 acres in supply-constrained corridors.

Latin America Commercial Real Estate Market Report Scope

Commercial real estate (CRE) is a property used solely for business or to provide a workspace rather than for residential purposes. Commercial real estate is often leased to tenants for the purpose of conducting income-generating activities.

The commercial real estate market in Latin America is segmented by type (office, retail, industrial, logistics, multi-family, and hospitality) and by country. The report offers market size and forecasts for the Latin American real estate market in value (USD billion) for all the above segments. The impact of the COVID-19 pandemic on the market will be covered in the report.

By Property Type

| Offices |

| Retail |

| Logistics |

| Others (Industrial, Hospitality, etc.) |

By Business Model

| Sales |

| Rental |

By End-user

| Individuals / Households |

| Corporates & SMEs |

| Others |

By Country

| Brazil |

| Argentina |

| Mexico |

| Chile |

| Colombia |

| Peru |

| Rest of Latin America |

| By Property Type | Offices |

| Retail | |

| Logistics | |

| Others (Industrial, Hospitality, etc.) | |

| By Business Model | Sales |

| Rental | |

| By End-user | Individuals / Households |

| Corporates & SMEs | |

| Others | |

| By Country | Brazil |

| Argentina | |

| Mexico | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of Latin America |

Key Questions Answered in the Report

What is the 2026 valuation of the Latin America commercial real estate market?

It stands at USD 313.6 billion and is expected to reach USD 429.21 billion by 2031 on a 6.47% CAGR trajectory.

Which property type is expanding the fastest?

Logistics facilities are forecast to grow at 7.05% CAGR as nearshoring and e-commerce compress vacancy in prime industrial corridors.

How much space do corporates and SMEs occupy?

They account for 50.85% of leased area and are projected to expand at 7.74% CAGR through 2031, outpacing other user groups.

Why are rental structures preferred?

Rental models provide balance-sheet flexibility, shield owners from capital-gains taxes, and suit institutional mandates for stable, inflation-linked cash flows.

Which geography shows the quickest growth outlook?

Mexico leads with an 8.01% CAGR through 2031, driven by USMCA-driven manufacturing relocation and strong institutional support for logistics assets.

What main risks could derail growth?

FX volatility, protracted permitting, and rising construction costs can compress returns and delay project timelines across several jurisdictions.

Page last updated on: