Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

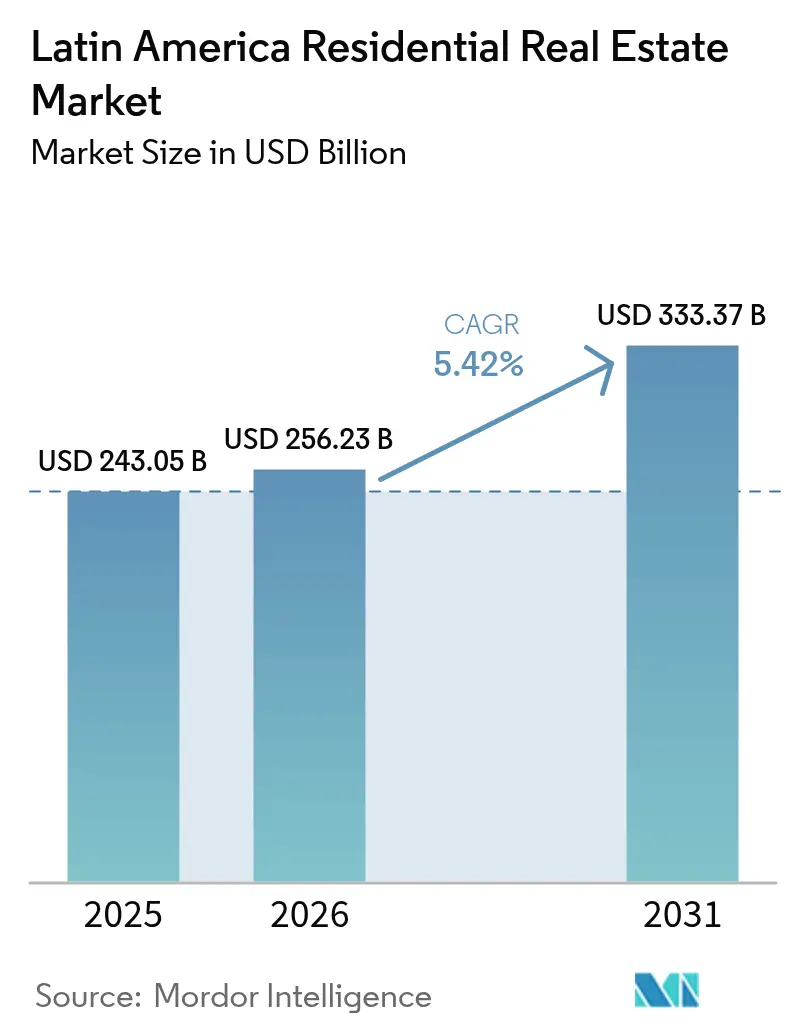

| Base Year Market Size (2025) | USD 243.05 Billion |

| Market Size (2026) | USD 256.23 Billion |

| Market Size (2031) | USD 333.37 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Residential Real Estate Market Analysis by Mordor Intelligence

The Latin America Residential Real Estate Market size was valued at USD 243.05 billion in 2025 and estimated to grow from USD 256.23 billion in 2026 to reach USD 333.37 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031). Robust household formation outpacing population growth, a regional housing deficit above 45 million units, and declining policy rates are the structural pillars behind this uptrend. Public‐sector subsidies, rising middle‐class incomes, and the steady professionalization of property management platforms continue to draw international capital, even as construction cost inflation of 3–4% presses margins. Investors find the Latin America residential real estate market particularly attractive because rental yields averaging 9–15% exceed comparable North American returns. The adoption of PropTech has lowered acquisition costs and reduced documentation bottlenecks, encouraging faster absorption of new stock across Brazil, Mexico, and Colombia.

Key Report Takeaways

- By country, Brazil led with 40.85% revenue share in 2025, while Colombia is projected to grow at a 6.92% CAGR through 2031.

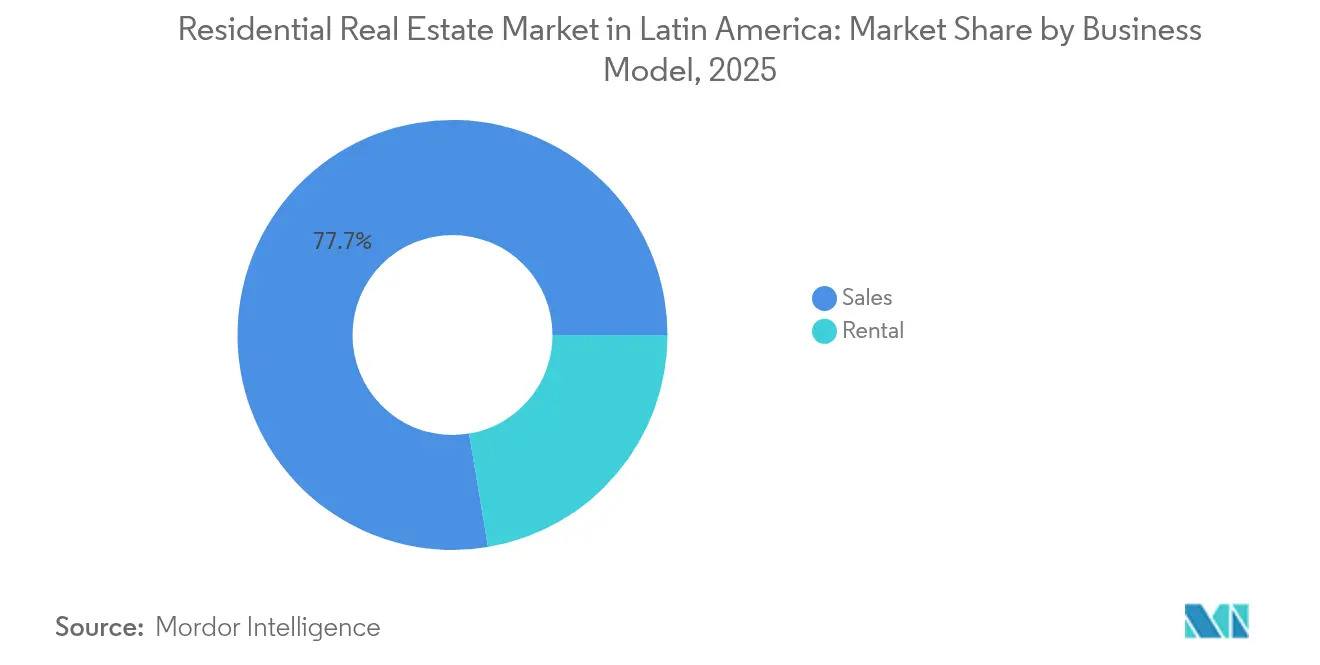

- By business model, the sales channel captured 77.65% of the Latin America residential real estate market share in 2025; the rental segment is expected to expand at a 6.02% CAGR to 2031.

- By property type, apartments and condominiums controlled 63.55% of 2025 revenue; villas and landed houses are forecast to post the fastest 6.15% CAGR over the same horizon.

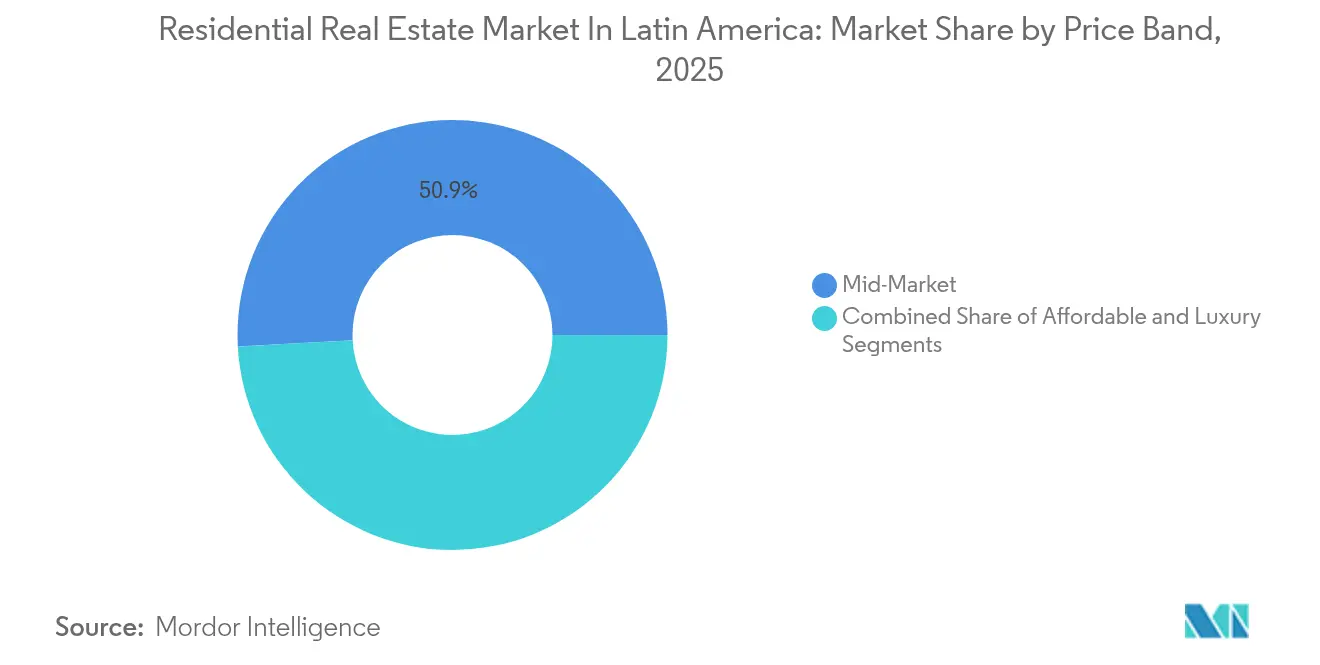

- By price band, the mid-market accounted for 50.85% of 2025 spending; the affordable tier is anticipated to climb at a 6.65% CAGR through 2031.

- By mode of sale, primary transactions represented 62.95% of revenue in 2025, whereas the secondary market shows a 6.37% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regional housing deficit exceeding 45 million units driving structural demand | +1.8% | Global, with highest impact in Brazil, Mexico, Colombia | Long term (≥ 4 years) |

| Government-led social housing programs expanding affordable housing supply | +1.2% | Brazil, Mexico, Colombia core, spill-over to Argentina, Chile | Medium term (2-4 years) |

| Expanding middle-class and rising incomes fueling mid- and premium housing demand | +0.9% | Brazil & Mexico primarily, emerging in Colombia, Chile | Medium term (2-4 years) |

| Improved housing finance access through mortgage and credit expansion | +0.7% | Brazil, Mexico, Colombia with regulatory influence from central banks | Short term (≤ 2 years) |

| Rising demand for gated and vertical housing driven by urban density and safety | +0.6% | Major metropolitan areas: São Paulo, Mexico City, Bogotá, Buenos Aires | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regional Housing Deficit Above 45 Million Units Driving Structural Demand

In Latin America, over 59 million residents live in substandard conditions, highlighting a persistent supply gap in the region's residential real estate market. To bridge its housing deficit, Mexico needs to produce over 800,000 new homes annually, a feat that demands construction spending equivalent to 1% of the nation's GDP. Meanwhile, Colombia requires an extra 400,000 units each year just to address its qualitative housing deficits. Such disparities in supply and demand have bolstered price stability, even amidst broader economic downturns. In tier-1 cities, acute land shortages have led developers to favor vertical projects, opting for reduced footprints but commanding premium prices. Furthermore, as household formation rates surpass population growth, it's evident that demographic trends, rather than cyclical GDP fluctuations, will dictate long-term housing demand.

Government Social-Housing Programs Expanding Affordable Supply

Access to affordable housing remains a critical challenge for many families across Latin America. Governments in the region are implementing innovative programs to address this pressing issue. Brazil's revamped Minha Casa, Minha Vida (MCMV) program now extends its reach to households earning up to USD 2,400 monthly. This adjustment has funneled 83% of MRV's sales in the first quarter of 2025 into subsidized categories. In Colombia, the Mi Casa Ya initiative permits families to secure grants two years ahead of unit delivery. This not only mitigates risks associated with construction financing but also speeds up the pre-sales process. Meanwhile, Mexico's INFONAVIT reform, set to roll out in February 2025, introduces a groundbreaking rent-to-own model. This innovation separates subsidy eligibility from the immediate need for homeownership. Together, these initiatives aim to deliver 2 million affordable units by 2026, unveiling a potential construction market worth an impressive USD 100 billion. Beyond housing, these measures promise benefits like enhanced credit access, a surge in mortgage securitization, and a broader embrace of industrialized building systems[1]Ministry of Housing, “Mi Casa Ya Subsidy Program,” minvivienda.gov.co.

Expanding Middle-Class and Rising Incomes Fuel Mid- and Premium Demand

The Latin American residential real estate market is undergoing a significant transformation, driven by evolving economic and demographic trends. In 2024 and 2025, real wages in Brazil and Mexico have outpaced inflation, enhancing the discretionary budgets of both first-time buyers and those seeking upgrades. In January 2025, Cyrela, in collaboration with the Canada Pension Plan Investment Board, allocated USD 340 million to develop luxury towers in São Paulo. These towers are designed to meet the needs of professionals aged 30–45, who are forming family units later in life and now prioritize superior amenities. Colombia reflects a similar trajectory: Camacol forecasts 63,000 new mid-market closings in Bogotá and Cundinamarca for 2025, representing a 14% year-on-year increase, supported by declining mortgage rates of 11–12%. As a result, the Latin American residential real estate market is diverging into two distinct segments: a robust subsidized production sector and a resilient premium tier, both appearing well-insulated from short-term market volatility.

Improved Housing Finance Access Through Mortgage and Credit Expansion

Access to housing finance is undergoing a significant transformation in Latin America, driven by innovative policies and financial reforms aimed at empowering borrowers and expanding market opportunities. Since July 2025, Brazil's newly introduced Legal Framework for Guarantees allows a single property to secure multiple loans through specialized guarantee managers. This innovation not only reduces collateral risk but also extends loan maturities. With the Brazilian Savings and Loan System boasting USD 280 billion in deployable resources, it stands poised to finance double the origination volume of 2024. In Mexico, mortgage affordability received a boost as INFONAVIT set payroll deductions at a maximum of 20% of wages, ensuring rent payments remain capped at 30%. This adjustment enhances borrowers' residual income. A region-wide trend of rate cuts, highlighted by Colombia's reduction from double-digit policy highs, has broadened the pool of potential borrowers. Collectively, these developments are not only enlarging the funding landscape for Latin America's residential real estate market but also speeding up the closing process for both primary and secondary transactions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High construction costs driven by inflation and supply chain volatility | -0.8% | Global, with highest impact in Mexico, Brazil, Argentina | Short term (≤ 2 years) |

| Land scarcity and rising land prices in tier-1 metropolitan areas | -0.6% | São Paulo, Mexico City, Bogotá, Buenos Aires metropolitan areas | Long term (≥ 4 years) |

| Economic instability and currency fluctuations reducing buyer confidence | -0.4% | Argentina primarily, secondary impact in Brazil, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Construction Costs Driven by Inflation and Supply Chain Volatility

The construction industry in Latin America is grappling with significant challenges as inflation and supply chain disruptions continue to impact operations. In 2024, material prices in Mexico surged by 4%, outpacing Colombia's 3% and Peru's 2% increases. This widening gap is tightening profit margins, especially on low-income projects. Backlogs from the Covid era still haunt the industry, particularly for glass, HVAC units, and finishing goods. As a result, developers face two choices: extend their build schedules or shell out extra for immediate purchases. Meanwhile, in Brazil, even as the civil-construction index sees a more moderate annual rise of 3.3%, contractors grapple with a shortage of skilled electricians and plumbers. This scarcity drives labor bids beyond budgeted amounts. The pinch is felt most acutely in affordable housing projects, where fixed sales prices clash with fluctuating material costs. In a bid to adapt, some builders are turning to off-site prefabrication of wall panels, managing to cut cycle times by 15% and providing a buffer against inflationary pressures.

Land Scarcity and Rising Land Prices in Tier-1 Metropolitan Areas

Land scarcity and rising prices in tier-1 metropolitan areas have become critical challenges for developers, reshaping strategies and decision-making processes. Strategic advantage now hinges on competition for prime plots. In Q2 2025, Cyrela invested USD 96 million in land acquisitions, a figure double its recent quarterly average, underscoring the tightening supply. While São Paulo's municipal plan encourages mixed-use transformations of vacant downtown buildings, uncertain expropriation timelines continue to delay progress and increase holding costs. To address price surges, developers like EZTEC are forming joint ventures with landowners, exchanging revenue shares for immediate cash. In Argentina, currency volatility has prompted some builders to import prefabricated homes from China, achieving a 90% reduction in construction costs, which highlights the extraordinary measures taken in response to severe scarcity. Long-term solutions, such as transit-oriented densification to maximize floor-area ratios, remain complex due to the intricate approval processes involved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Sales Still Commands, but Rental Accelerates

The sales channel held 77.65% of 2025 revenue, validating the homeownership culture that defines the Latin America residential real estate market. Rental, however, is predicted to log a 6.02% CAGR to 2031, propelled by delayed household formation, gig-economy mobility, and pension-fund appetite for stable cash flows. Mexico City’s August 2024 civil-code reform caps rent hikes at the inflation rate and mandates a digital registry within 30 days, heightening transparency and expanding the tenant pool. In Brazil, Cyrela and CPP Investments plan seven multifamily towers by 2027, demonstrating that institutional equity recognizes the rental gap. Savings yields near multi-year lows further redirect domestic investors into income properties, reinforcing rental’s momentum in the Latin America residential real estate market.

Better risk metrics also strengthen the rental thesis. Default data provided by Brazilian credit bureaus shows a 150 basis-point improvement in on-time payment after landlords adopted automated verification tools. Meanwhile, rent-to-own pilots under Mexico’s INFONAVIT broaden reach to lower-income households without burdening fiscal accounts. If pilot yields remain above 10%, analysts expect secondary-market securitizations to emerge by 2027, embedding liquidity into what was traditionally an opaque asset class. These trends converge to make the Latin America residential real estate market more diversified across tenure options, supporting both developers and long-term asset managers.

By Property Type: Apartments Dominate as Vertical Living Gains Popularity

Apartments and condominiums accounted for 63.55% of the 2025 value, confirming the preeminence of vertical solutions in congested metros. Villas and landed houses are projected to grow at a 6.15% CAGR, but infill condo projects still receive the lion’s share of capital allocations. EZTEC’s USD 43.6 million Moved Osasco Residence launch added 357 units across two towers in Greater São Paulo, targeting tech-sector employees and reinforcing the apartment narrative. Prefabricated façades reduce cycle time, enabling faster unit turnover and enhancing internal rates of return.

Urban land scarcity aligns with safety concerns, pushing demand toward gated high-rise communities that integrate coworking spaces, concierge services, and ESG certifications. Brazil’s Ecoparque Bairros Integrados blueprint illustrates next-generation master-planning: twin-use zoning, 50% green space, and net-zero infrastructure. In Colombia, verticalization is also driven by mortgage assessment ratios favoring smaller ticket sizes, which make apartment loans easier to originate and securitize. Consequently, the Latin America residential real estate market sees apartments remain the anchor segment, even as peripheral suburbs witness bungalow revival supported by road and rail expansions.

By Price Band: Mid-Market Retains Majority, but Affordable Leads Growth

The mid-market captured 50.85% of 2025 spend, underlining its importance as the volume backbone of the Latin America residential real estate market. Affordable housing, however, is slated for a 6.65% CAGR to 2031, outpacing all other price bands. Brazil’s revised MCMV lifted the price ceiling to USD 70,000, a move that trimmed new-launch counts by 3% yet spurred a 10% jump in sales because more families qualify. Subsidies now cover 85% of the unit price in the lowest bracket, de-risking developer pipelines.

Cury Construtora’s 2024 launch of 11,000 apartments valued at USD 620 million underscores that scale remains achievable in the affordable niche. In Colombia, pre-assignment subsidies guarantee demand before a project breaks ground, mitigating speculative oversupply. For mid-market players, competitive differentiation shifts to amenities: fiber-optic connectivity, daycare centers, and rooftop gardens. As rising incomes funnel buyers into larger footprints, the Latin America residential real estate market preserves its mid-tier volume base while using public policy to accelerate the lowest tier.

By Mode of Sale: Primary Supply Dominates but Secondary Market Fluidity Improves

Primary (new-build) deals represented 62.95% of 2025 transactions, buttressed by large-scale public programs and greenfield opportunities. The secondary channel is forecast to expand at a 6.37% CAGR, buoyed by digitized listings and improved valuation analytics. São Paulo recorded 76,000 unit sales against 73,200 launches in 2023, signaling inventory absorption and a budding resale pipeline. PropTech marketplaces fill the historical void left by the absence of MLS systems, reducing time-on-market by an average of 22 days.

Financial innovation follows. Brazil’s guarantee law permits collateral recycling, so homeowners can refinance and extract equity without extinguishing first liens, increasing mobility between primary and secondary segments. Mexico’s anti-money-laundering rules, effective August 2025, extend verification to secondary transfers, thereby lowering reputational risk for cross-border investors [lexology.com]. As trust builds, the Latin America residential real estate market becomes more liquid, encouraging portfolio rotation and professional brokerage services.

Geography Analysis

In 2025, Brazil maintained a significant 40.85% share of the Latin American residential real estate market, supported by the extensive Minha Casa, Minha Vida program and strong institutional co-investment. Last year, São Paulo alone achieved an impressive USD 8.8 billion in combined launch and sales volumes. Additionally, the newly implemented Legal Framework for Guarantees has unlocked USD 280 billion in mortgage liquidity. The growth of PropTech, increasing from 500 startups in 2018 to over 1,200 in 2024, is helping to simplify transactions. This development aligns well with construction-tech innovations, which have successfully reduced cycle times by 15%.

Mexico benefits from favorable demographic trends and industrial near-shoring, although it faces challenges with input-cost inflation exceeding 4%. In August 2024, rental reforms were introduced to stabilize tenant relationships by linking annual adjustments to headline inflation. Moreover, the February 2025 INFONAVIT reform introduced rent-to-own formats that are particularly appealing to the subprime segment. While stricter anti-money-laundering compliance has increased due diligence costs, it has also enhanced investor confidence. This improvement has allowed the Latin American residential real estate market to direct a larger portion of remittances into housing stock.

Colombia emerges as the region's growth leader, with a projected 6.92% CAGR through 2031. As mortgage rates gradually decline toward 11%, and with Mi Casa Ya subsidies covering up to USD 8,000 of the ticket price, Camacol forecasts the sale of 63,000 units in Bogotá and Cundinamarca by 2025. Despite facing temporary regulatory scrutiny-such as the investigation of Constructora Bolívar for alleged consumer-rights violations-the overall policy environment remains supportive of housing. Chile and Argentina present contrasting dynamics: Chile's Law 21,718 has reduced permit approval times to 30 days, while Argentina's volatile peso complicates cost planning, even as IRSA reports remarkable triple-digit revenue growth. Together, these factors create a diverse regional landscape where, despite increasing divergence in national cycles, the Latin American residential real estate market continues to experience overall growth.

Competitive Landscape

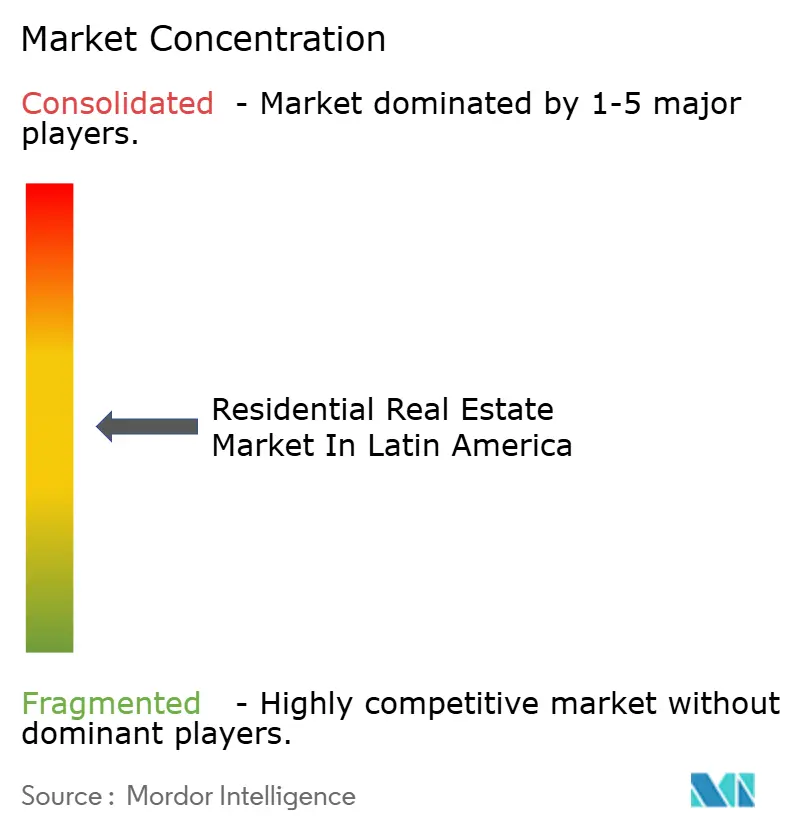

The Latin American residential real estate market features moderate concentration, while Mexico and Colombia present a more fragmented market, with no single developer holding more than a 6% share. Prominent companies such as MRV, Cyrela, and Gafisa leverage their scale by securing bulk material contracts and implementing proprietary digital sales funnels, which reduce brokerage fees by up to 70%. Their emphasis on government-backed projects ensures stable cash flows and facilitates faster turnover of their land banks. Meanwhile, mid-sized firms focus on suburban corridors that larger competitors often underserve. These firms build on local relationships and benefit from quicker municipal approvals.

Strategic partnerships are a cornerstone of the Latin American residential real estate market. For instance, Cyrela has partnered with CPP Investments in a USD 340 million venture aimed at developing luxury and multifamily rental towers, which are expected to be completed by 2027. EZTEC adopts a collaborative approach by entering revenue-sharing agreements with landholders instead of outright land purchases, thereby protecting its margins from land inflation. In Mexico, private equity firms Blackstone and Pátria demonstrated their confidence in scalable platforms by acquiring a 70% stake in Alphaville in August 2024, signaling strong global interest in the region.

The integration of technology has become indispensable. As of 2024, Brazil is home to over 1,200 PropTech firms, with regional marketplaces utilizing AI-driven credit scoring and blockchain documentation to streamline transaction times. Developers are increasingly incorporating solar micro-grids and smart-home infrastructure to enhance the appeal of their mid-market offerings. Collectively, these advancements contribute to a moderately concentrated Latin American residential real estate market while creating opportunities for specialized players in segments such as rentals, senior living, and co-living[3]Helmi Group, “PropTech Mapping in Brazil,” helmi.fi.

Latin America Residential Real Estate Industry Leaders

MRV Engenharia e Participações S.A.

Cyrela Brazil Realty S.A.

Gafisa S.A.

Tenda S.A.

Direcional Engenharia S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: BRZ completed a business combination with Fica, forming a new publicly listed developer focused on Brazil’s multifamily space.

- August 2025: EZTEC launched Moved Osasco Residence, a USD 43.6 million project in Greater São Paulo featuring 357 units across two towers.

- March 2025: Cyrela announced its first commercial tower, highlighting a strategy to diversify revenue streams.

- January 2025: Cyrela and CPP Investments formed a USD 340 million joint venture to finance luxury residential towers in São Paulo.

Latin America Residential Real Estate Market Report Scope

Homes or apartments are residential properties. These may include single-family homes, townhouses, or studios. Most residential property owners who own residential property but do not live there will rent it to others to make money from the property.

The report provides a comprehensive background analysis of the market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. The report on the Latin American residential real estate market is segmented by type (apartments and condominiums and landed houses and villas) and geography (Mexico, Brazil, Colombia, and the Rest of Latin America).

The report offers the market sizes and forecasts for the Latin American residential real estate market in value (USD) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

How large is the Latin America residential real estate market in 2026?

It reached USD 256.23 billion in 2026 and is projected to climb to USD 333.37 billion by 2031.

Which country leads regional sales?

Brazil held 40.85% of 2025 revenue, making it the region’s largest market.

What segment is expanding fastest?

The rental channel, aided by policy reform and institutional capital, shows a 6.02% CAGR outlook to 2031.

How big is the affordable-housing opportunity?

Government programs across Brazil, Mexico, and Colombia aim to fund about 2 million units by 2026, representing roughly USD 100 billion in construction value.

What is driving foreign investor interest?

Net rental yields of 9-15% and new guarantee laws that lower financing risk are attracting cross-border capital inflows.

What are the key risks?

Construction-cost inflation, urban land scarcity, and currency volatility remain the principal headwinds affecting returns.

Page last updated on: