Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

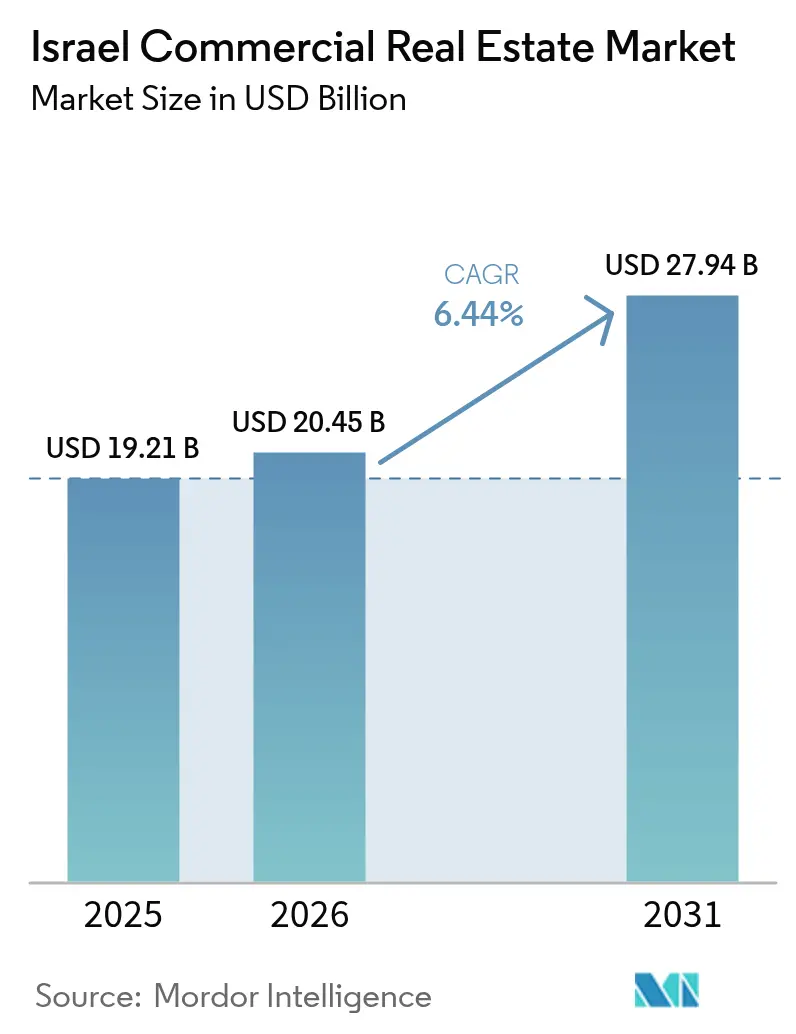

| Base Year Market Size (2025) | USD 19.21 Billion |

| Market Size (2026) | USD 20.45 Billion |

| Market Size (2031) | USD 27.94 Billion |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Commercial Real Estate Market Analysis by Mordor Intelligence

Israel commercial real estate market size in 2026 is estimated at USD 20.45 billion, growing from 2025 value of USD 19.21 billion with 2031 projections showing USD 27.94 billion, growing at 6.44% CAGR over 2026-2031. This expansion reflects Israel’s status as a global technology hub, its pivotal position between three continents, and the steady flow of domestic institutional capital seeking inflation-linked income. E-commerce–driven demand for Grade-A logistics parks, accelerated transit-oriented development along Tel Aviv’s new rail corridors, and edge data-center build-outs all lift occupier requirements. At the same time, geopolitical volatility and rising construction costs keep risk premiums elevated, prompting investors to emphasize asset quality, resilient locations, and diversified tenant bases[1]Amir Yaron, “Annual Financial Stability Report 2024,” Bank of Israel, bankisrael.gov.il. Established developers are responding with smart-building retrofits, energy-efficiency upgrades, and strategic joint ventures that reduce funding costs while widening market access.

Key Report Takeaways

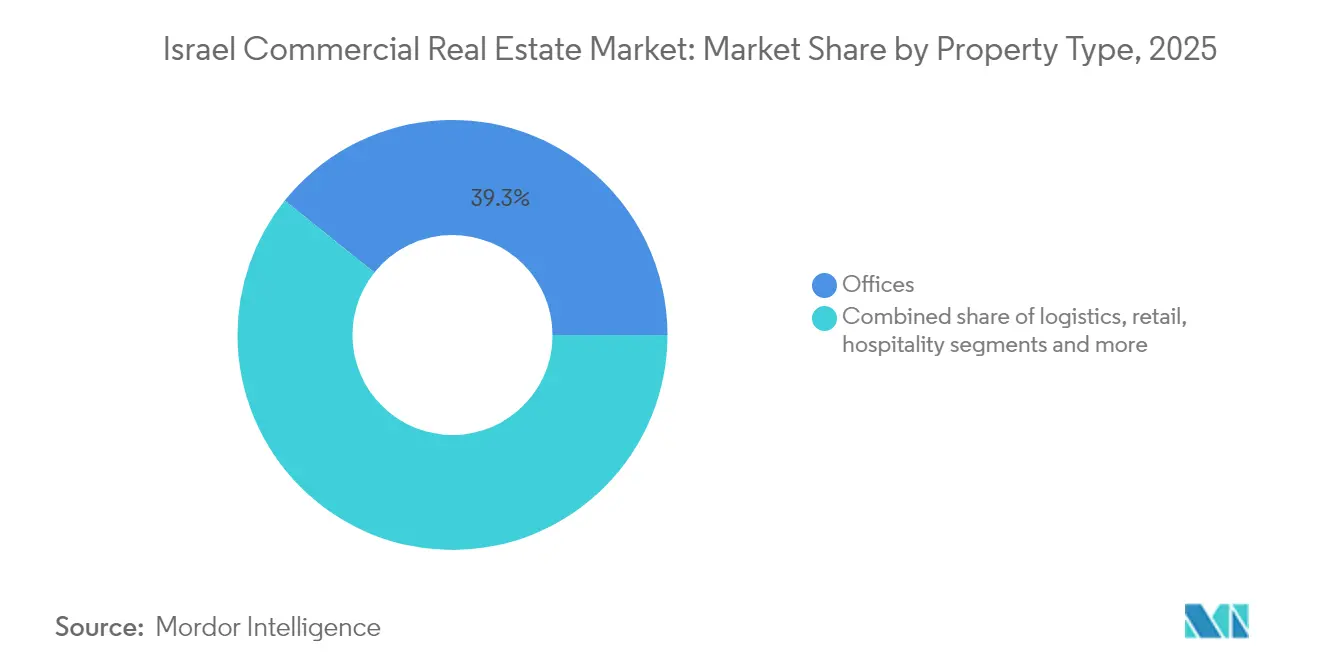

- By property type, offices held the largest 39.25% Israel commercial real estate market share in 2025, whereas logistics and industrial space is forecast to expand at a 7.33% CAGR through 2031.

- By business model, sales transactions accounted for 73.20% of the Israel commercial real estate market size in 2025, while rental and leasing activities record the fastest 7.12% CAGR for 2026-2031.

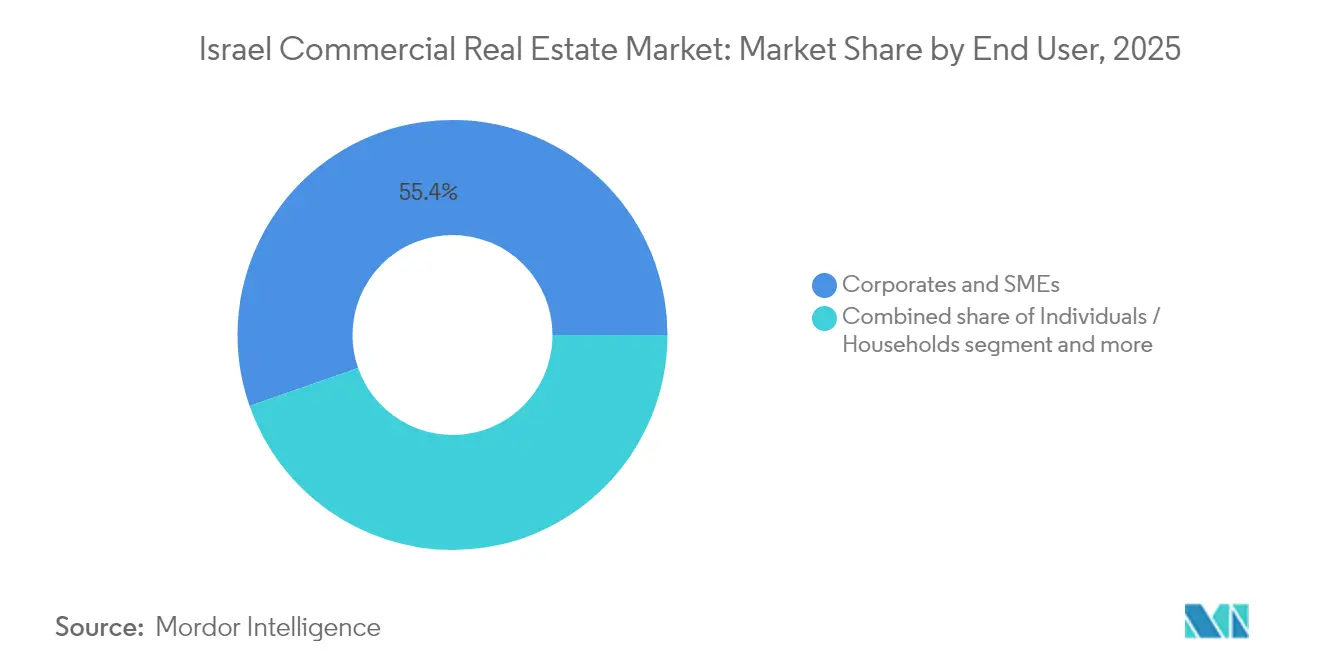

- By end-user, corporates and SMEs commanded 55.35% of activity in 2025; this segment is projected to grow at 6.36% over the forecast period.

- By region, Tel Aviv District led with 44.35% revenue share in 2025, whereas the Central District posts the highest 6.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Israel Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in global tech-tenant expansion | +1.2% | Tel Aviv & Central Districts | Medium term (2-4 years) |

| Grade-A logistics & cold-chain demand | +0.9% | National; Central & Southern | Short term (≤ 2 years) |

| Pension-fund rotation into REITs | +0.8% | National | Medium term (2-4 years) |

| Tel Aviv light-rail corridor uplift | +0.7% | Tel Aviv & Central corridors | Long term (≥ 4 years) |

| EU supply-chain diversion via Haifa | +0.6% | Northern District | Medium term (2-4 years) |

| Edge data-center campus growth | +0.5% | Tel Aviv & Central Districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Global Tech-Tenant Expansion Concentrating in Tel Aviv and Herzliya

Global technology firms continue to scale R&D and regional headquarters in Tel Aviv’s central business district and Herzliya Pituach. Demand centers on Grade-A towers offering resilient telecommunications backbones, redundant power, and adaptable floorplates. The clustering compresses vacancy, sustains premium rents, and stimulates adjacent mixed-use redevelopment. Government reforms in banking, capital markets, and real estate streamline approvals and encourage long-term corporate leasing commitments. Developers able to integrate high-density power, robust cybersecurity systems, and collaborative amenities find an edge in winning anchor tenants.

Accelerated Demand for Grade-A Logistics and Cold-Chain Parks Driven by E-Commerce

Online retail penetration fuels nationwide requirements for high-bay warehouses, automated fulfillment nodes, and temperature-controlled storage near population hubs. Facilities must support robotics, high throughput, and multi-tenant distribution. Israel’s central geography supports regional flows, yet operational bottlenecks at Haifa Port expose supply-chain vulnerabilities, prompting investors to build redundant capacity around Ashdod and inland hubs. Cold-chain parks command rental premiums given the need for precise climate controls for food and pharmaceutical inventory.

Tel Aviv Light-Rail and Metro Corridors Re-rating Adjacent Commercial Land Values

New transit lines reshape urban mobility, adding stations that expand catchment areas and lift footfall. Commercial parcels within walking distance enjoy uplift in appraisal values, while redevelopment pressure rises on under-utilized lots. Retail and office landlords capitalize on higher densities, and mixed-use schemes gain traction as planners encourage live-work-play clusters. Investors price long lead-time projects on expectations of sustained ridership and growing preference for public transport.

Pension-Fund Rotation into Israeli REITs Seeking Inflation-Linked Cashflows

Local pension managers increase allocations to REITs to hedge consumer-price rises. The influx deepens market liquidity and lowers funding spreads for seasoned issuers. In turn, REITs recycle capital into redevelopment of aging stock and acquisition of logistics platforms. Transparent governance and quarterly disclosure satisfy institutional due-diligence requirements, reinforcing a virtuous cycle of capital formation[2]Eyal Cohen, “Israel’s Real Estate Investment Trust Law—2025 Update,” Ministry of Finance, mof.gov.il.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Record-high construction & land costs | -1.1% | National; Tel Aviv acute | Short term (≤ 2 years) |

| Persistent hybrid-work adoption | -0.8% | Tel Aviv & Central CBDs | Short term (≤ 2 years) |

| Geopolitical risk-premium on financing | -0.7% | National; border regions | Medium term (2-4 years) |

| Rising water-stress & climate capex | -0.4% | Coastal Districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Hybrid-Work Adoption Softening CBD Office Net Absorption

Hybrid work policies reduce desk density and prolong decision cycles. Prime towers maintain occupancy by offering wellness amenities, flexible fit-outs, and digital access control, yet secondary stock faces longer vacancy and rent concessions. Landlords pivot to smaller floorplates, spec suites, and shared amenity floors to preserve appeal. Co-working operators aggregate swing demand from enterprise clients balancing remote and in-office patterns.

Record-High Construction and Land Costs Compressing Development Margins

Concrete, steel, and labor costs rose 15-20% year-over-year in 2024, while land auctions in Tel Aviv’s core set record benchmarks. Developers either seek joint ventures, pre-let commitments, or vertical mixed-use density to justify pro-forma returns. Value engineering, modular components, and green-building incentives each shave capex but cannot fully offset pricing pressures, delaying speculative starts[3]Lior Horowitz, “Israel Builders Association 2025 Outlook,” Israel Builders Association, iba.org.il.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Offices Hold the Largest Share While Logistics Accelerates

Offices controlled a commanding 39.25% Israel commercial real estate market share in 2025, anchored by technology and financial services tenants clustered in Tel Aviv’s CBDs. Prime towers achieve rent premiums through Class-A amenities, ESG certifications, and plug-and-play digital infrastructure. Despite hybrid work, net absorption remains positive for buildings offering flexible layouts and wellness features. Developers convert outdated stock into boutique mixed-use or life-science labs to capture emerging demand pockets. Meanwhile, the logistics sub-segment posts a forecast 7.33% CAGR, driven by e-commerce growth and near-shoring strategies. Institutional capital flows into build-to-core warehouse parks featuring high-clear heights and automation-ready slabs. Forward funding deals reduce leasing risk and accelerate project timelines.

The Israel commercial real estate market size tied to logistics benefits from port diversification and highway upgrades that shorten last-mile delivery. Cold-chain facilities gain traction with pharmaceutical importers and grocery platforms seeking compliance with stringent temperature standards. Speculative supply remains measured, sustaining healthy occupancy and encouraging rental growth. By comparison, retail faces structural change as omnichannel strategies reshape store footprints. Hospitality rebounds with the return of business travel and regional tourism, yet owners prioritize adaptive re-use potential to hedge demand swings.

By Business Model: Sales Still Dominate Yet Leasing Gains Momentum

Sales transactions represented 73.20% of overall activity in 2025, reflecting local preference for asset ownership and ready mortgage availability. High-net-worth investors and family offices acquire income-generating buildings to preserve capital and hedge inflation. Nonetheless, leasing shows a robust 7.12% CAGR outlook as corporates optimize balance sheets and international entrants favor operational flexibility. Landlords craft lease terms incorporating index-linked escalations, shared maintenance, and early termination options. Sale-leaseback structures unlock capital for occupiers while ensuring long-term tenancy for owners.

Recurring rental revenues stabilize cash flow for REITs, supporting dividend visibility that attracts pension funds. The Israel commercial real estate market size attributable to leasing widens as developers deliver purpose-built campuses tailored for single or multi-tenant occupancy. Prop-tech platforms digitize contract management, automate invoicing, and enable data-driven asset optimization, improving both tenant experience and owner margins.

By End-User: Corporates and SMEs Drive Demand Momentum

Corporates and SMEs contributed 55.35% of market activity in 2025, supported by a vibrant start-up ecosystem and steady multinational expansion. Venture capital inflows finance workspace take-up, while global firms base R&D centers in proximity to Israel’s talent pools. Flexible-workspace providers aggregate smaller tenant demand into master leases, easing entry for new businesses. The segment is projected to expand at 6.36% through 2031, sustaining steady absorption across offices, light-industrial, and mixed-use portfolios.

Household and individual users remain important in street-level retail, food-and-beverage outlets, and small warehouses. Government and institutional tenants lend stability through long leases in Jerusalem and district capitals. The Israel commercial real estate market size is linked to government users, supporting infrastructure investment, particularly for public administration and healthcare facilities. Developers balance speculative and pre-let strategies to serve varying procurement timelines and compliance requirements.

Geography Analysis

Tel Aviv District’s 44.35% share underscores its unchallenged status as the country’s financial and technology nucleus. Prime office towers with LEED or WELL certifications achieve above-average occupancy as technology giants and fintech start-ups expand R&D headcount. The district’s proximity to Ben Gurion Airport improves executive mobility, while the new light-rail network widens commuter catchments and lifts retail footfall around station nodes.

Southern District growth of 6.63% CAGR reflects concerted government efforts to diversify economic activity away from the crowded center. Industrial parks near Be’er Sheva attract semiconductor subcontractors, renewable-energy integrators, and defense-tech producers. Logistics developers acquire large tracts along Highway 6 to build multi-client distribution campuses serving both domestic and export flows through Ashdod Port. Lower land costs enable higher plot ratios, while municipal tax incentives bolster project feasibility.

Central District suburbs such as Petah Tikva and Ramat Gan provide cost-effective alternatives for space-intensive occupiers. Corporates relocating non-client-facing functions benefit from competitive rents yet remain within 20 minutes of Tel Aviv’s CBD by rail. The district hosts the largest concentration of edge data-center projects, taking advantage of robust power grids and fiber connectivity.

Jerusalem’s commercial demand remains steady, led by government ministries, diplomatic missions, and academic institutions. Life-science incubators linked to hospitals and universities spur demand for specialized lab-enabled office space. Heritage preservation rules constrain new supply, maintaining occupier loyalty to existing high-quality assets.

Northern coastal nodes around Haifa witness incremental absorption tied to port privatization and rail upgrades. Near-shore warehousing and cross-dock facilities reduce congestion and enable 24-hour operations. Investors integrate renewable energy micro-grids to mitigate grid instability and meet corporate sustainability goals.

Competitive Landscape

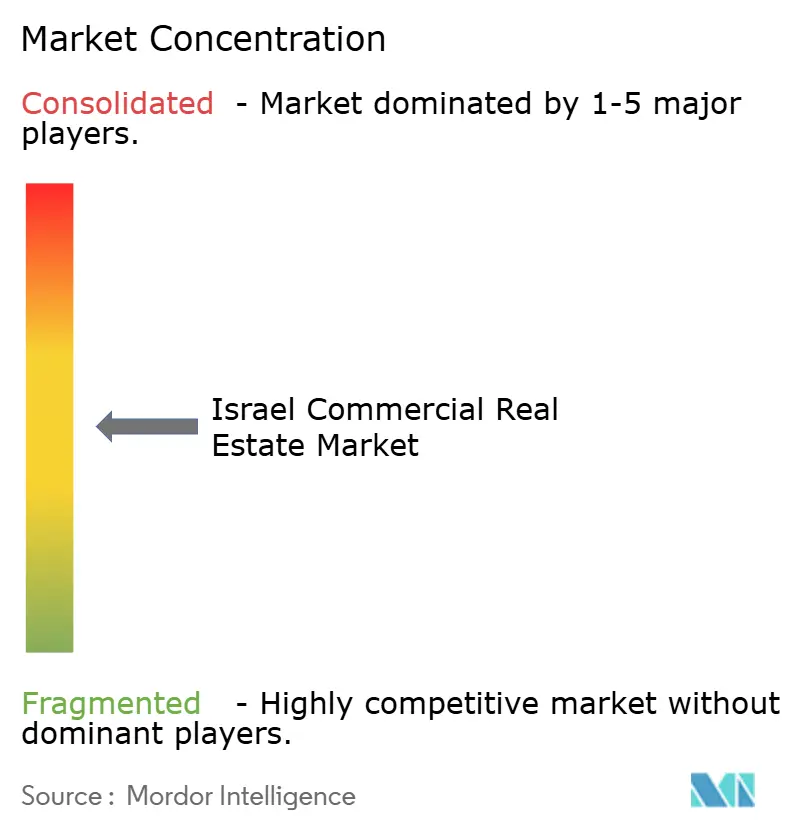

The Israel commercial real estate market exhibits moderate concentration, with established domestic developers such as Azrieli Group, Melisron, and Gazit Globe leveraging deep landbanks and regulatory familiarity to secure prime sites. These firms pursue diversification across office, retail, logistics, and data-center verticals to smooth income cycles. Capital-raising via domestic REIT structures lowers funding costs, while strategic disposals unlock capital for new developments.

International entrants partner with local players to navigate zoning processes and security regulations. Global service providers CBRE, JLL, Cushman & Wakefield, and Colliers advise on cross-border capital deployment, portfolio management, and ESG compliance. Joint ventures blend foreign capital with on-the-ground execution expertise, mitigating geopolitical and currency risk.

Technology integration differentiates leading landlords. Smart-building platforms monitor energy consumption, predictive maintenance, and indoor-air quality, improving tenant satisfaction and lowering operating expenses. Flexible-workspace operators lease contiguous floors in prime towers, offering enterprises turnkey swing space. Developers pilot modular construction to cut build times and carbon footprints.

Israel Commercial Real Estate Industry Leaders

Arko Holdings Ltd

Ashtrom Group Ltd

Gazit-Globe Ltd

Azrieli Group Ltd

Melisron Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: World Bank assessment values reconstruction needs for Gaza and West Bank at USD 53 billion, implying regional supply-chain disruptions that may affect Israeli commercial logistics flows.

- January 2025: Eli Cohen assumes office as Minister of Energy and Infrastructure, signaling potential revisions to building codes and grid expansion that influence future asset valuations.

- December 2024: Security threats to Haifa Port raise the prospect of cargo diversion, spurring investment in alternative logistics hubs.

- October 2024: Regional conflict escalation drives oil price spikes and increases the cost of capital for real estate investors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Israel's commercial real estate (CRE) market as the yearly transaction value plus rental income generated by office towers, shopping centers, logistics and industrial parks, and mixed-use assets that earn most revenue from commercial tenants across the eight statistical districts. The base year is 2024, and according to Mordor Intelligence, the market will reach USD 19.21 billion in 2025.

Scope exclusion: pure residential projects and raw-land speculation are out of scope.

Segmentation Overview

- By Property Type

- Offices

- Retail

- Logistics / Industrial

- Others (Mixed-Use, Data-Centres)

- By Business Model

- Sales

- Rental

- By End-User

- Individuals / Households

- Corporates & SMEs

- Others

- By Region

- Tel-Aviv District

- Central District

- Jerusalem District

- Rest of Israel

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed brokers, asset managers, pension-fund buyers, and SME occupiers in Tel Aviv, Jerusalem, Haifa, and Beersheba, and we fielded surveys that confirmed vacancy, achievable rents, and discount-rate assumptions relied upon in the model.

Desk Research

We extracted supply, demand, and pricing baselines from the Bank of Israel macro tables, Central Bureau of Statistics construction starts, and deed-registry logs. We then overlaid quarterly vacancy and rent surveys released by the Israel Real Estate Appraisers Council. Paid feeds from D&B Hoovers and Dow Jones Factiva helped map developer pipelines and investment flows.

To gauge cost trends, we reviewed Ministry of Transport project updates, customs import tallies for steel and cement, and Tel Aviv Stock Exchange filings. Trade publications such as the Israel Builders Association newsletter rounded out qualitative context. These references are illustrative; many other open and subscription sources informed the dataset.

Market-Sizing & Forecasting

We begin with a top-down build that aggregates recorded sales and rental turnover by district before validating totals through a bottom-up roll-up of sampled Grade-A assets' gross leasable area times average rents. Key model drivers include construction-start pipeline, prime rent trajectory, vacancy ratio, construction-cost index, and foreign direct investment. A multivariate regression, stress-tested under conservative and optimistic scenarios, extends the view to 2030. Where off-market trades are missing, we bridge gaps using analog districts adjusted for land-price differentials.

Data Validation & Update Cycle

Outputs pass variance scans against Bank of Israel dashboards, auditor-certified REIT disclosures, and broker indices. Senior reviewers sign off, and models refresh annually with interim updates for material events, so clients always receive the latest view.

Why Mordor's Israel Commercial Real Estate Baseline Commands Confidence

Published estimates diverge because publishers mix asset classes, apply book-value versus transaction-value lenses, and refresh data at different cadences.

By locking scope to income-earning assets and recalculating every year, Mordor delivers a consistent baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.21 B (2025) | Mordor Intelligence | |

| USD 24.3 B (2023) | Global Consultancy A | Includes hospitality and values standing stock; limited field checks |

| USD 18 B (2025) | Trade Journal B | Focuses on Tel Aviv core; applies conservative rent compression |

Takeaway: Once scope, refresh cadence, and variable choice are standardized, Mordor's disciplined blend of verified transactions and forward-looking indicators offers decision-makers a balanced, transparent baseline they can trust.

Key Questions Answered in the Report

What is the current value of the Israel commercial real estate market?

The market is valued at USD 20.45 billion in 2026 and is forecast to reach USD 27.94 billion by 2031.

Which property type leads the market?

Offices hold the largest 39.25% Israel commercial real estate market share, anchored by technology and financial services tenants in Tel Aviv.

Where is the fastest growth occurring regionally?

The Central District shows the highest growth with a 6.86% CAGR forecast for 2026-2031, driven by logistics and industrial expansion.

Why are logistics assets attracting increased investor interest?

E-commerce growth, port diversification, and cold-chain demand are driving a 7.33% CAGR in logistics and industrial real estate.

How are developers mitigating rising construction costs?

They employ joint ventures, modular construction, value-engineering, and mixed-use density to protect margins amid record land and material prices.

What role do REITs play in the market?

Domestic pension-fund allocation into REITs provides liquid, inflation-linked capital that supports new development and asset acquisitions.

Page last updated on: