Colombia Fruits And Vegetables Market Analysis by Mordor Intelligence

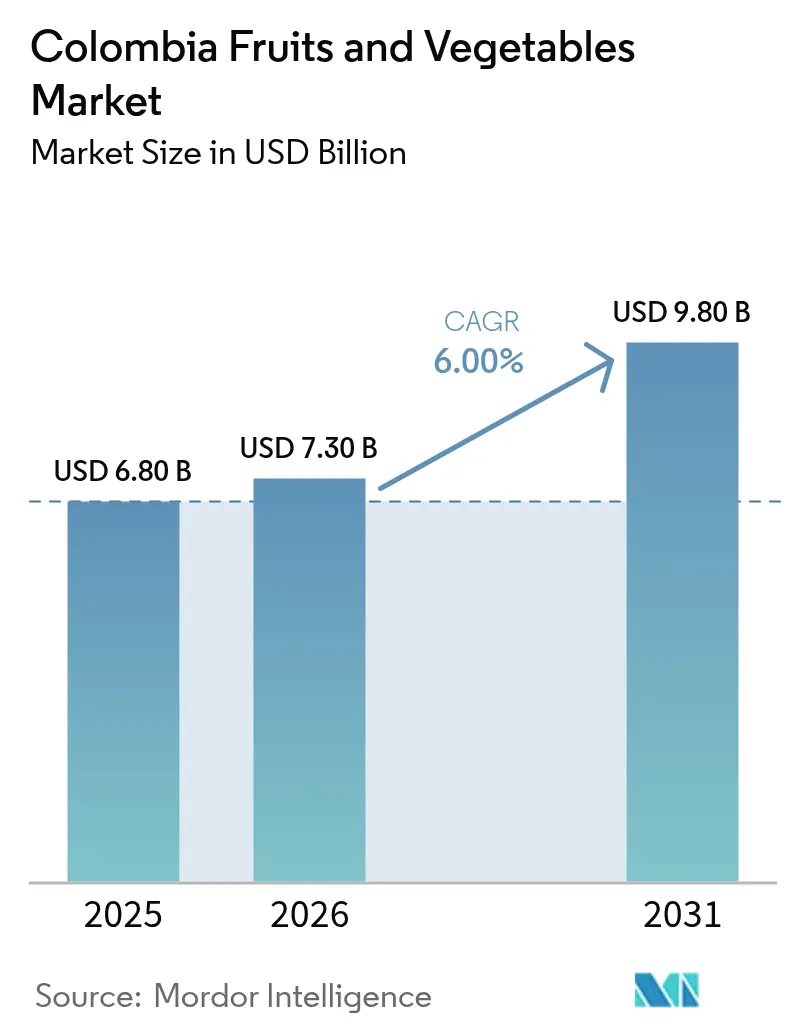

The Colombia fruits and vegetables market size is projected to be USD 6.8 billion in 2025, USD 7.3 billion in 2026, and reach USD 9.8 billion by 2031, growing at a CAGR of 6.0% from 2026 to 2031. Significant investments in cold-chain infrastructure, the rapid adoption of precision agriculture, and zero-duty access through the Pacific Alliance are driving export-oriented growth, particularly for Hass avocados and premium tropical fruits[1]Source: Departamento Administrativo Nacional de Estadística, “Boletín de Comercio Exterior,” dane.gov.co. The newly operational deep-water terminals will reduce fruit export routes, enhancing the competitiveness of Urabá growers against Peruvian and Mexican suppliers in Asian markets. Concurrently, increasing urban demand for traceable and pesticide-safe produce, driven by vegan and flexitarian trends, is boosting domestic consumption and expanding retailer margins, despite challenges such as El Niño-related droughts and fluctuations in tomato prices. The market remains moderately concentrated, providing opportunities for mid-tier exporters to gain market share by adopting blockchain traceability, climate-smart insurance, and sensor-driven fertigation technologies, which reduce water and fertilizer costs.

Key Report Takeaways

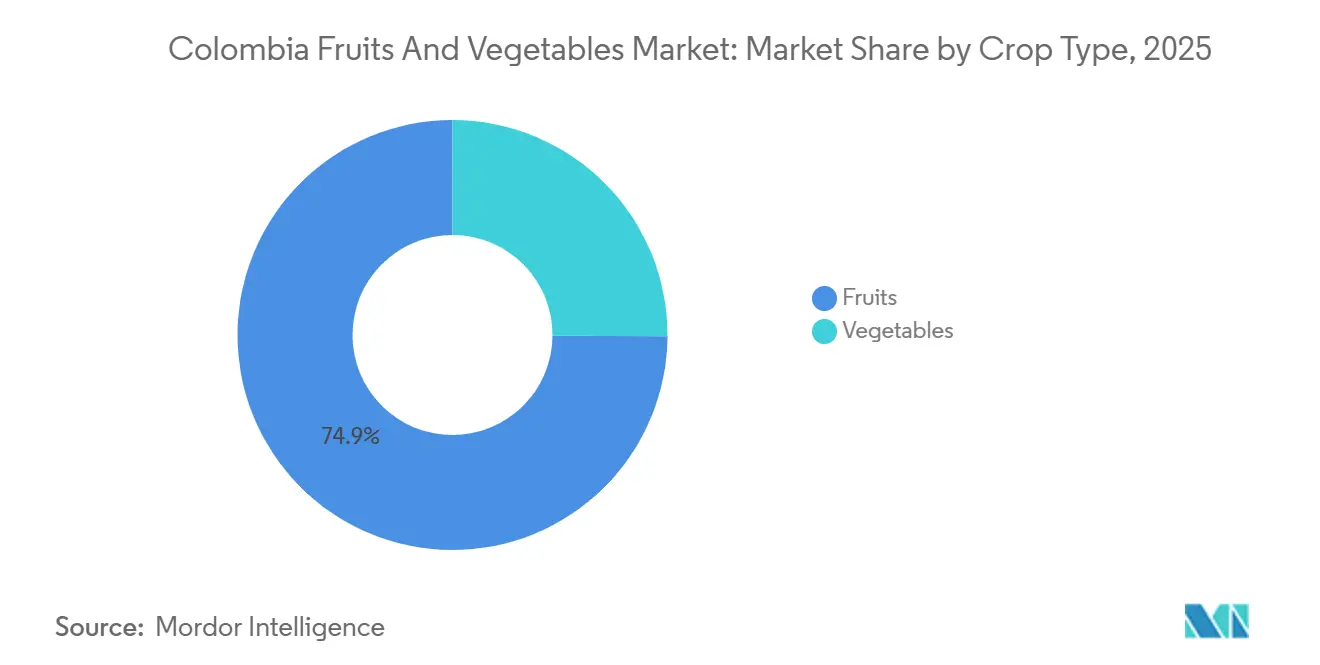

- By crop type, fruits led with 74.9% of the Colombia fruits and vegetables market share in 2025, with the vegetable segment set to grow at a 5.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of precision-agricultural tools | +0.90% | National, with early gains in Antioquia, Cundinamarca, Valle del Cauca | Medium term (2-4 years) |

| Expansion of cold-chain capacity across major fruit corridors | +1.20% | Urabá-Antioquia corridor, Caribbean lowlands, Valle del Cauca | Short term (≤ 2 years) |

| Rising vegan and flexitarian diets among urban Colombians | +0.70% | Bogotá, Medellín, Cali metropolitan areas | Medium term (2-4 years) |

| Preferential trade tariffs under the Pacific Alliance | +0.80% | National, with spillover to Mexico, Peru, Chile export channels | Long term (≥ 4 years) |

| Roll-out of climate-smart crop-insurance products | +0.60% | Andean highlands, drought-prone municipalities | Medium term (2-4 years) |

| Growing demand from specialty-ingredient processors | +0.50% | National, concentrated among top 20 exporters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Precision-Agricultural Tools

Colombian fruits stand out as high-quality ingredients in the food industry. For instance, fruit exports increased by 29% during the first months of 2024 compared to the same period in 2023. Sensor-driven fertigation and drone-based crop monitoring have reduced input costs in Colombian Hass avocado orchards. This cost efficiency is significant, as it supports the expansion of avocado cultivation in the country. Precision tools help reduce water waste and fertilizer runoff, enabling growers to meet sustainability benchmarks without compromising yield. The technology is expanding from large estates in Antioquia to mid-sized farms in Cundinamarca and Boyaca, where blueberry cultivation is also emerging as a high-altitude niche. However, adoption remains inconsistent, as smallholders often lack the upfront capital and digital skills needed to operate cloud-based dashboards, creating a productivity gap that benefits vertically integrated exporters.

Expansion Of Cold-Chain Capacity Across Major Fruit Corridors

Puerto Antioquia, a deep-water terminal with significant annual capacity, began operations in 2025. It reduces transit distances for Uraba's banana and avocado shipments to Asian markets. The port features extensive refrigerated storage, allowing growers to consolidate shipments and minimize spoilage rates. Reduced transit times extend the shelf life of perishable exports, providing a competitive edge against other regional producers in key markets. This infrastructure development also enhances domestic cold-chain logistics, meeting the demand for consistent quality and traceability from urban retailers in Bogota and Medellín. In April 2025, Emergent Cold LatAm plans to expand its cold storage capacity in Colombia to meet the growing demand for temperature-controlled logistics. The initial phase of the project will offer 7,000 pallet positions, with a total planned capacity of 18,000 pallet positions upon full completion. While cold-chain investments are concentrated in specific regions, highland vegetable corridors still rely on ambient-temperature trucking, limiting their ability to serve premium urban segments.

Rising Vegan and Flexitarian Diets Among Urban Colombians

A dietary study revealed that sustainable eating patterns require significant increases in vegetable and fruit consumption compared to current averages, according to a 2025 report from the European Journal of Nutrition. This indicates untapped domestic demand, as many urban residents are reducing meat consumption multiple days per week. This shift is driven by health awareness, environmental concerns, and the growing presence of plant-based restaurants in metropolitan areas. A study conducted in the Medellín metropolitan area during 2021-2022 revealed that 18.1% of surveyed vegetarians identify as vegan, with 60.8% of this group aged between 18 and 30 years. Urban consumers are willing to pay premiums for products with organic certification, local sourcing, and traceability. This creates opportunities for mid-tier growers to bypass traditional wholesale channels and supply directly to supermarket chains or farm-to-table cooperatives. The trend is particularly strong among millennials and Generation Z, who prioritize sustainability narratives over cost considerations.

Preferential Trade Tariffs Under the Pacific Alliance

Zero-duty access to Mexico and Peru under the Pacific Alliance framework, which came into full effect in 2025, has allowed Colombian avocado exporters to compete in markets previously dominated by Chilean and Mexican suppliers. The imposition of a tariff in 2025 redirected export volumes toward Pacific Alliance partners and Asian markets. This adjustment accelerated diversification efforts, with companies increasing mango and papaya shipments to Mexico's processing sector. Pacific Alliance rules of origin, which require regional content, have encouraged Colombian packers to source inputs locally instead of importing packaging materials from Asia. This policy has created a multiplier effect across the value chain, benefiting domestic suppliers of corrugated boxes, labels, and refrigerated containers. The long-term impact of these developments will depend on Colombia's ability to maintain phytosanitary compliance and avoid trade disputes over pesticide residues, which have historically disrupted shipments to Mexico.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility for bulk produce categories | -0.80% | National, concentrated in Andean vegetable zones | Short term (≤ 2 years) |

| Increasing frequency of El Niño-linked droughts | -1.10% | Andean highlands, Caribbean lowlands | Medium term (2-4 years) |

| Rural labor shortages in key highland zones | -0.60% | Cundinamarca, Boyacá, Nariño vegetable zones | Long term (≥ 4 years) |

| Traceability compliance costs for smallholders | -0.40% | National, concentrated among smallholder cooperatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility for Bulk Produce Categories

Spot tomato prices in Colombian wholesale markets experienced significant fluctuations due to erratic rainfall, pest outbreaks, and logistical challenges that disrupted deliveries to urban centers. This volatility has discouraged food processors and supermarket chains from entering into long-term contracts, forcing them to maintain higher inventory levels and pass increased costs to consumers. In response, growers have reduced tomato cultivation and shifted to crops with more stable demand, further exacerbating supply shortages and perpetuating the cycle of volatility. The absence of futures markets or price-stabilization mechanisms leaves farmers vulnerable to spot-market risks, particularly during harvest periods when prices may fall below production costs. Government interventions, such as minimum-price guarantees, have been sporadic and underfunded, limiting their impact. Additionally, the volatility has hindered investment in greenhouse infrastructure, which could stabilize year-round supply but requires multi-year payback periods that are incompatible with unpredictable revenue streams.

Increasing Frequency of El Niño-Linked Droughts

The El Niño episode caused significant agricultural losses. As of early 2024, El Niño resulted in over 500 municipalities being placed on alert for water shortages. In April 2024, the situation in the capital, Bogotá, became critical, leading to water rationing for approximately 10 million people as reservoir levels fell to 40-year lows. These events occur periodically, with projections indicating increased intensity and duration in the coming years. This threatens production stability in regions lacking irrigation infrastructure. Drought conditions also increase susceptibility to pests and diseases, leading to higher pesticide use and raising risks for export shipments. While the government's insurance program mitigates financial losses, it does not address lost yields or prevent soil degradation from repeated droughts. Long-term adaptation requires investments in water-harvesting systems, drought-tolerant crops, and agroforestry practices to improve soil moisture retention. However, these measures demand upfront capital and technical support, which remain challenging for smallholders to access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Export Channels Drive Premium Fruit Growth

Fruits held the dominant share of the Colombian fruits and vegetables market at 74.9% in 2025, led by bananas, mangoes, avocados, and pineapples, which enjoy sanitary clearances and zero-duty corridors into Asia and Pacific Alliance partners. Hass avocado acreage continues to expand in Antioquia and Tolima, while Puerto Antioquia’s cold-chain capacity extends shelf life on outbound fruit cargoes and preserves price premiums in China and South Korea. Export orientation shields growers from domestic price swings, and blockchain traceability now secures placement with European retailers focused on deforestation compliance. Together, these strengths keep the fruits segment the principal value contributor to the Colombia fruits and vegetables market size.

Vegetables make up the smaller but fastest-growing major segment, with a 5.9% CAGR, as Bogota, Medellín, and Cali consumers adopt plant-forward diets and supermarket chains roll out temperature-controlled distribution for leafy greens and highland staples. Precision-agriculture sensors and subsidized parametric drought insurance are helping onion, carrot, and chili growers curb input waste and secure bank financing, improving year-over-year yield stability despite El Niño shocks. Retailers reward QR-code provenance and GlobalGAP seals with shelf-space premiums, pushing mid-tier cooperatives to invest in traceability even as compliance costs squeeze margins. Rising urban demand and expanding cold-chain coverage therefore position vegetables to outpace fruit growth in contributing incremental value to the overall Colombia fruits and vegetables market size.

Geography Analysis

Antioquia accounted for a significant share of the projected 2026 consumption value, driven by Urabá’s banana plantations and Medellín’s strong distribution network. The launch of Puerto Antioquia in 2025 facilitated direct shipments to Asia, reducing logistics costs and improving product freshness. Valle del Cauca contributed notably, supported by agro-industrial clusters focused on processing pineapple, mango, and sugarcane. Cundinamarca provided a substantial share, supplying Bogota’s population from nearby highland agricultural fields.

The Caribbean lowlands, including Magdalena and La Guajira, are anticipated to grow steadily, driven by irrigated banana and pineapple projects. Newly constructed highways connecting farms to Cartagena have reduced freight times and enabled consistent year-round export flows. In contrast, Boyacá and Nariño face challenges such as drought risks and labor shortages, which hinder yield recovery. However, initiatives like parametric insurance and drip irrigation pilots aim to stabilize production in these regions.

Export dynamics significantly influence regional economies. The United States remains a key importer of fruits and vegetables, despite the imposition of new tariffs. The European Union values Colombia’s organic certifications but has increased compliance requirements under new regulations[2]Source: European Commission, “Reglamento sobre Deforestación,” ec.europa.eu. Meanwhile, China and South Korea, primarily sourcing from Antioquia orchards, experienced strong growth in demand, further strengthening the export segment of Colombia’s fruits and vegetables market.

Regulatory Landscape

Colombia's fruits and vegetables supply chain is primarily governed by the Instituto Colombiano Agropecuario (ICA) for plant health and export phytosanitary controls. ICA Resolution 824 of 2022 requires registration of fresh-vegetable production sites, packing facilities, and exporters, and it links export eligibility to sourcing from ICA-registered farms with verifiable traceability, alongside the use of ICA phytosanitary certification processes for shipments.

On the commercialization and food-system side, Ley 2378 of 2024 established the National Agricultural Marketing Policy framework covering production, logistics, and market organization. In March 2026, the Gobierno Nacional enacted Decree 0212 of 2026 to implement an urgent reactivation plan for agri-food systems and rural livelihoods following the declared emergency, reinforcing government-led programs that affect farm-to-market logistics, credit access, and operational continuity for horticultural producers and exporters.

Value Chain Analysis

The value chain begins with input supply (seeds, fertilizers, crop protection products) and on-farm production that spans smallholders and vertically integrated estates in export-oriented fruit corridors. Post-harvest activities include field aggregation, grading, packing, and phytosanitary compliance (ICA registrations and export certification), followed by refrigerated and ambient transport to ports and domestic consumption centers. Export logistics have been strengthened by new cold-chain and port infrastructure, including Puerto Antioquia, which started operations in 2025, and cold-storage expansion activity such as Emergent Cold LatAm's planned multi-phase buildout announced in April 2025.

Downstream, produce reaches wholesalers and traditional markets, as well as modern retail chains in Bogota, Medellin, and Cali that increasingly demand QR-code provenance and GlobalGAP-style assurance for premium shelf placement. Bottlenecks remain in secondary and tertiary roads and in uneven access to cold chain for highland vegetable corridors, which increases losses and limits penetration into high-value urban and export programs. Policy actions such as Ley 2378 of 2024 and the March 2026 Decree 0212 reactivation plan support a shift toward lower intermediation, improved logistics coordination, and stronger regional technical support across the chain.

Competitive Landscape

The top five firms accounted for a significant portion of the projected 2025 market value, indicating moderate concentration in the Colombia fruits and vegetables market. Uniban led the market, leveraging its banana estates and exclusive shipping slots. Banacol followed, supported by diversification into plantains and pineapples. Grupo Cartama focused on organic Hass avocado exports, while Greenyard Fresh Colombia and Daabon Group completed the top five.

Technology plays a significant role in shaping competitive advantages. Uniban and Banacol utilize QR codes to verify farm labor conditions, a feature that smaller cooperatives find challenging to implement due to compliance costs. Grupo Cartama and Camposol Colombia have introduced sensor-guided irrigation systems that reduce fertilizer waste, improving yield consistency and enhancing buyer confidence[3]Source: Cropviz Research Team, “Sensor Networks and Yield Consistency,” mdpi.com. Mid-tier exporters are increasingly pursuing mergers with cooperatives to secure supply volumes and distribute traceability investment costs, signaling a trend toward gradual market consolidation.

Emerging opportunities in the market include blueberries, baby carrots, and greenhouse tomatoes. While high capital expenditure deters smaller, fragmented growers, it aligns well with cash-rich incumbents seeking defensible niches. Innovations such as parametric insurance and digital agronomy services help mitigate risks, encouraging lenders to finance greenhouse projects. As profit margins narrow for bulk staples, specialty produce is poised to redefine market share dynamics within the Colombia fruits and vegetables market.

Market Opportunities and Future Outlook

Export diversification beyond core bananas and Hass avocados is creating a narrower set of gaps where new sanitary authorizations and buyer programs can be activated quickly through existing packing and cold-chain assets. A concrete case is the first exploratory commercial shipment of Tahitian limes to China initiated by Celifruit in July 2026 following new sanitary authorization, showing how market-access work can translate into incremental horticultural export lanes for Colombian suppliers that already meet phytosanitary and traceability requirements.

Technology-enabled productivity and compliance services also remain a key focus area, particularly for mid-tier growers and cooperatives trying to narrow the gap with vertically integrated exporters on traceability, water efficiency, and residue risk management. Public programs and partnerships support this shift, including the Government of Valle del Cauca citing 2,307 biofactories installed under its Plan Integral Fruticola to turn agricultural waste into liquid fertilizers, and the ICA and Analdex collaboration to structure productive-chain models for native Amazonian fruits (including acai and copoazu) under international sanitary and biocommerce standards. At the same time, national policy actions in 2026, including Decree 0212 and emergency risk-fund measures, increase the addressable market for climate-resilience tools such as parametric insurance, remote technical assistance, and sensor-driven fertigation that support both export programs and premium urban retail.

Recent Industry Developments

- July 2026: Celifruit initiated the first exploratory commercial shipment of Tahitian limes to China following new sanitary authorization. This signals a practical expansion path for Colombian exporters into higher-value citrus channels that depend on strict phytosanitary compliance and dependable cold-chain execution.

- April 2025: Emergent Cold LatAm announced plans to expand cold storage capacity in Colombia, with an initial phase of 7,000 pallet positions and a planned total of 18,000 pallet positions upon full completion. This investment supports temperature-controlled logistics for perishables and aligns with retailers' and exporters' needs for longer shelf life and lower spoilage.

- June 2024: Corpohass launched the unified country brand "Avocados from Colombia" in Antwerp, Belgium, as part of a push to position Colombian Hass avocados on quality and sustainability credentials in the European market. The brand launch supports coordinated promotion and can help align exporters and growers around shared standards and buyer requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market means the value of fruits and vegetables traded and consumed in Colombia across the supply chain, using consistent USD valuation for the study period, and supported by value and volume signals where available.

Scope exclusions: This sizing excludes non-produce categories like grains, meat, seafood, and packaged foods where fruit or vegetable is only a minor ingredient.

Segmentation Overview

- Crop Type

- Fruits

- Banana

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Mango

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Avocado

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Pineapple

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Papaya

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Banana

- Vegetables

- Tomato

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Onion

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Carrot

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Chilli

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Cabbage

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Tomato

- Fruits

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial fact base on Colombia produce supply, demand, and trade, and then to set guardrails for the model. We referenced public sources such as FAOSTAT for crop output and yield context, UN Comtrade for import and export flows, and national statistics releases and agriculture bulletins from DANE and the agriculture ministry for crop calendars and production signals.

To keep the market value logic consistent, we also reviewed price and inflation indicators from Banco de la Republica and sanitary guidance from ICA, along with customs and port updates that affect export throughput. General secondary materials like company filings, investor presentations, association websites, and reputable press were used to validate direction of change and timing of disruptions. In a few cases, paid subscriptions for company financials and shipment-level import and export checks were used to cross-verify the public data series. These desk sources are illustrative, and many other public references were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test the sizing assumptions that are hard to confirm from public sources, especially around channel mix, post-harvest losses, and price realization at different points in the chain. We spoke with a mix of growers, exporters, importers, wholesalers, and retail and foodservice stakeholders across Colombia, and we also checked logistics and cold-chain perspectives to reduce blind spots.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | |

| Mid tier: 48% | Functional/Unit leaders: 33% | |

| Smaller Players: 14% | Managers: 55% |

Market-Sizing & Forecasting

Our market model starts with a top-down reconstruction of Colombia fruits and vegetables demand using production, trade, and consumption signals, which are then converted into value using observable price series and interview-tested price pass-through. The totals are then corroborated through selective bottom-up approximations, such as sampled price per kilogram multiplied by estimated volumes for key channels, and cross-checks against supplier and exporter revenue patterns where disclosures exist.

Inputs that matter in this market include harvested area and yields for major crops, export volumes and destination mix, import volumes for items that supplement domestic supply, seasonality and weather-driven variability, and local price movement for frequently traded products (for example, tomatoes are a visible volatility marker). Forecasts were built using scenario analysis supported by multivariate regression on a small set of drivers, including inflation, income-linked consumption, trade momentum, and yield trends, and then adjusted after expert feedback on expected planting and logistics constraints. Where bottom-up checks had gaps, assumptions were kept conservative and were only scaled after they aligned with independent trade and production boundaries.

Data Validation & Update Cycle

Validation is done in layers so single-source noise does not drive the outcome. We compare outputs against independent signals such as import and export totals, major crop production direction, and reported price movement, and then we investigate variances that do not align with on-ground seasonality or known disruptions.

Before sign-off, the model and assumptions go through internal analyst reviews, and re-contact is triggered when responses diverge on a key variable like price realization or post-harvest loss. Reports are refreshed annually, and interim updates are added when material events occur, such as policy shifts, major weather impacts, or trade disruptions. Right before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Colombia Fruit Vegetable Market Size Measured Against Other Published Estimates

Published estimates for Colombia fruits and vegetables do not always line up because the underlying boundaries are not identical, even when the report titles look similar. The biggest differences usually come from what is counted in the value chain, which year is used as the base, and how prices are converted into USD when inflation is moving.

By tracking trade-linked volumes, checking crop-level production signals, and refreshing USD price assumptions with interview inputs, Mordor Intelligence keeps the market value tied to Colombia-only produce flows, rather than mixing in adjacent processed categories or using a single price point across channels.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.80 B (2025) | |

| Market Aggregator A | USD 6.41 B (2024) | Uses a different base year and tends to emphasize fresh produce dynamics, which can shift the value level when price inflation and exchange rates change between years. |

| Trade Platform B | USD 6.11 B (2023) | Earlier base year and a shorter horizon can anchor pricing and channel assumptions lower, especially if later export momentum and cold-chain effects are not fully reflected. |

The table shows that year choice and scope boundaries explain most of the spread. When production and trade checks are paired with practical price validation and consistent currency timing, the result is a market size that is easier to trace back to real Colombia demand and supply signals, and to repeat when new annual data is released.

Key Questions Answered in the Report

What is the projected value of the Colombia fruits and vegetables market by 2031?

The market is projected to grow at USD 9.8 billion, supported by a 6.0% CAGR from 2026 to 2031.

How does Puerto Antioquia improve export competitiveness?

The deep-water port cuts 300 kilometers off routes, adds 220,000 square meters of reefer space, and lowers spoilage, directly lifting margins.

What role does parametric insurance play for smallholders?

It pays out automatically during droughts, covering replanting costs and unlocking bank credit that stabilizes on-farm investment.

Why is cold-chain investment important?

Better refrigerated storage and transport preserve quality, reduce loss, and unlock premium export markets.

Page last updated on: