Cloud Workflow Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

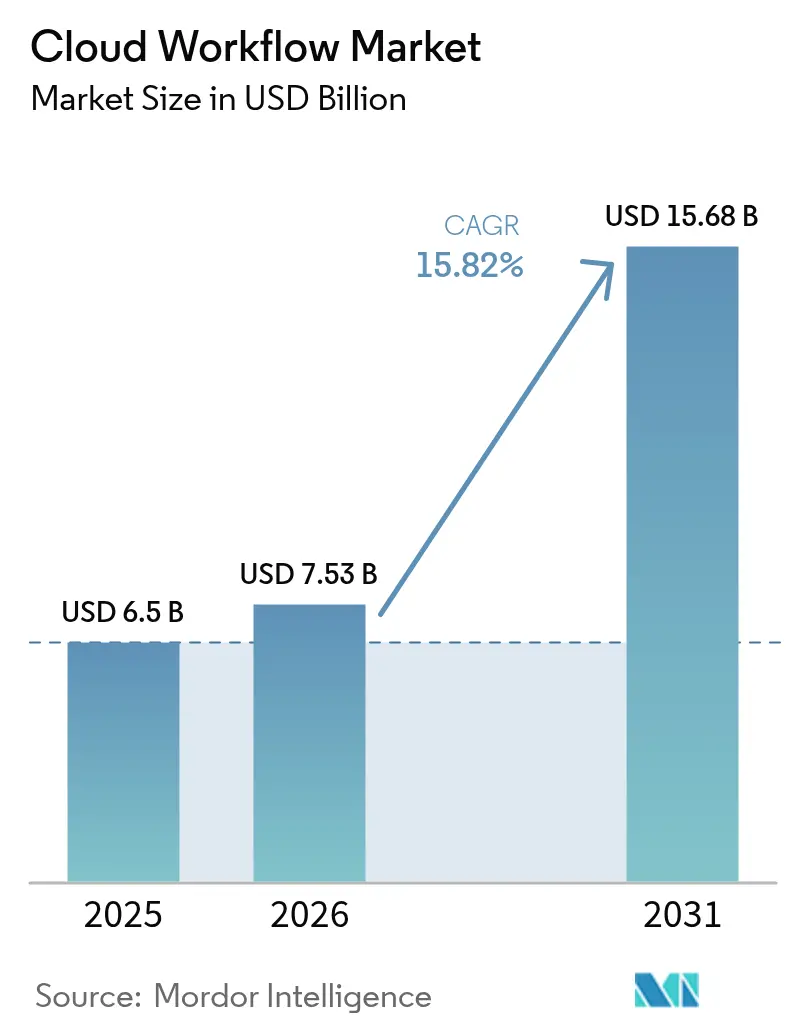

| Market Size (2026) | USD 7.53 Billion |

| Market Size (2031) | USD 15.68 Billion |

| Growth Rate (2026 - 2031) | 15.82% CAGR |

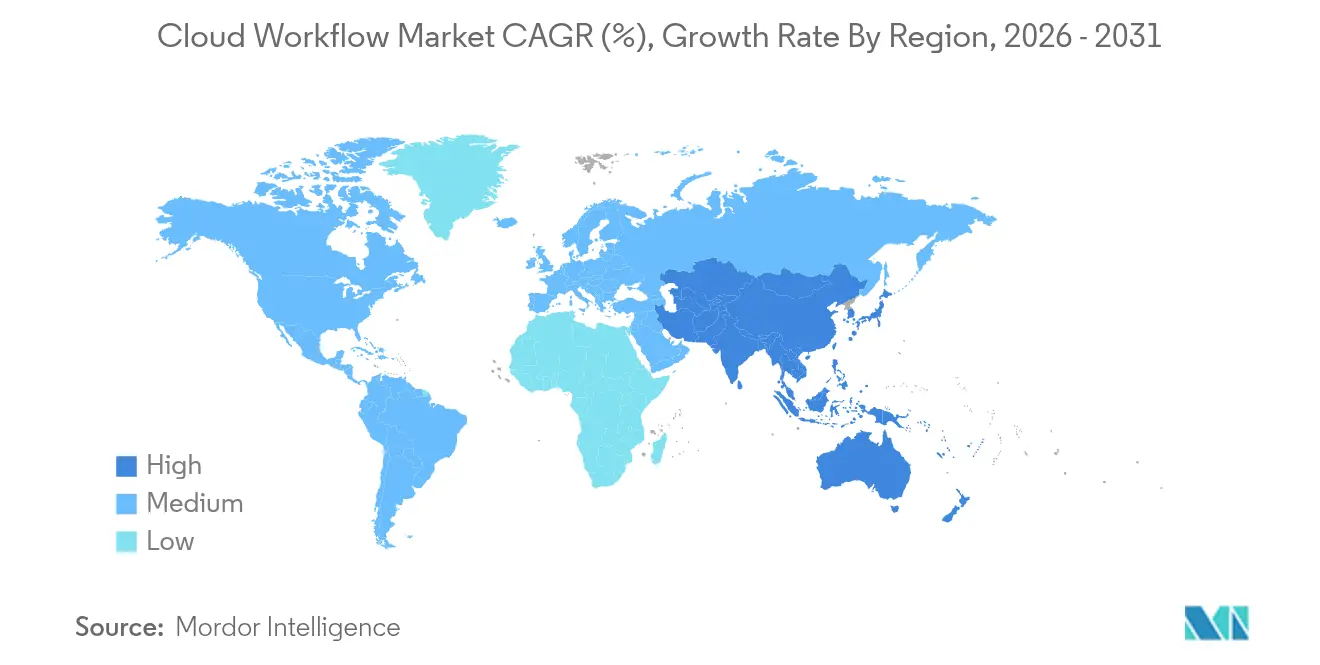

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Workflow Market Analysis by Mordor Intelligence

Cloud workflow market size in 2026 is estimated at USD 7.53 billion, growing from 2025 value of USD 6.50 billion with 2031 projections showing USD 15.68 billion, growing at 15.82% CAGR over 2026-2031. Strong demand stems from enterprises replacing legacy process tools with AI-enriched orchestration platforms that promise faster decision cycles, lower manual workload, and tighter regulatory alignment. Low-code design studios, now bundled into most leading suites, let non-technical users automate everyday tasks without compromising security controls. The spread of generative AI further raises platform utility, allowing conversational creation of flows and real-time anomaly detection. Vendors differentiate through industry-specific templates, sovereign-cloud alignment, and cross-platform interoperability to reduce vendor-lock risks. North America’s first-mover advantage keeps it the largest regional buyer, while Asia-Pacific’s public-sector digitization programs create the steepest growth curve.

Key Report Takeaways

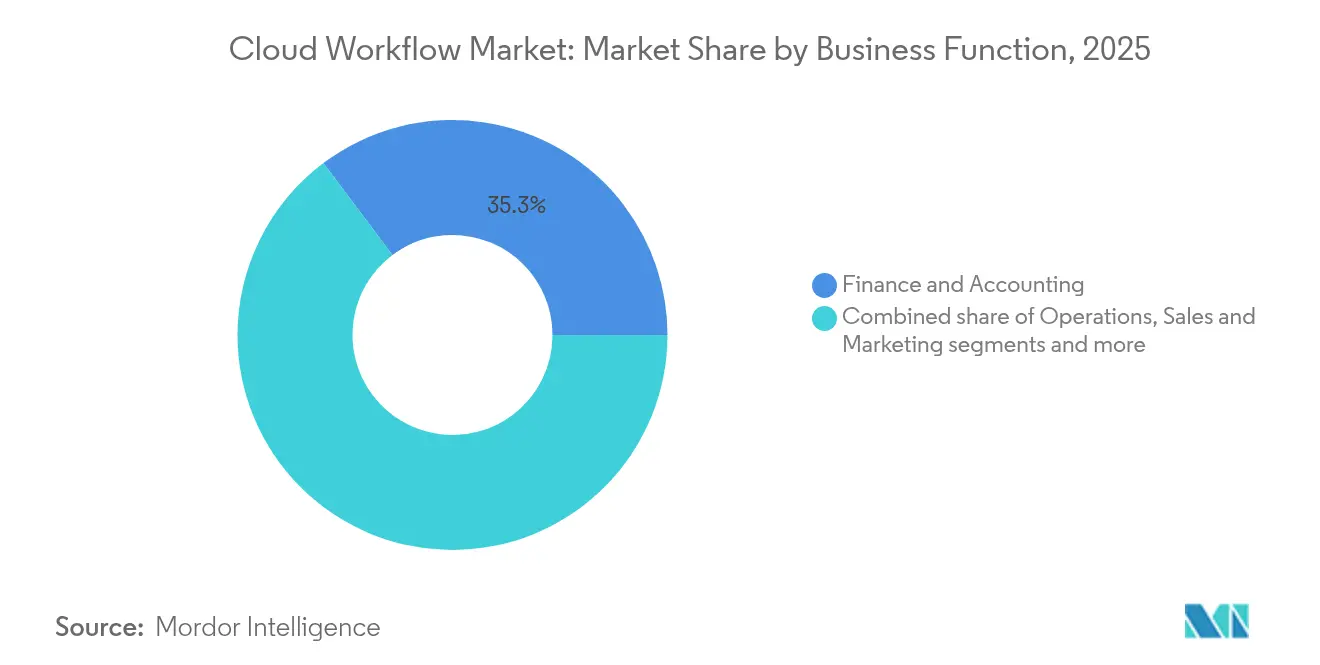

- By business function, Finance and Accounting led with 35.25% revenue share in 2025; Sales and Marketing is projected to expand at a 16.32% CAGR through 2031.

- By deployment model, Public Cloud held 66.10% of the cloud workflow market share in 2025, while Hybrid Cloud is forecast to grow at 17.02% CAGR to 2031.

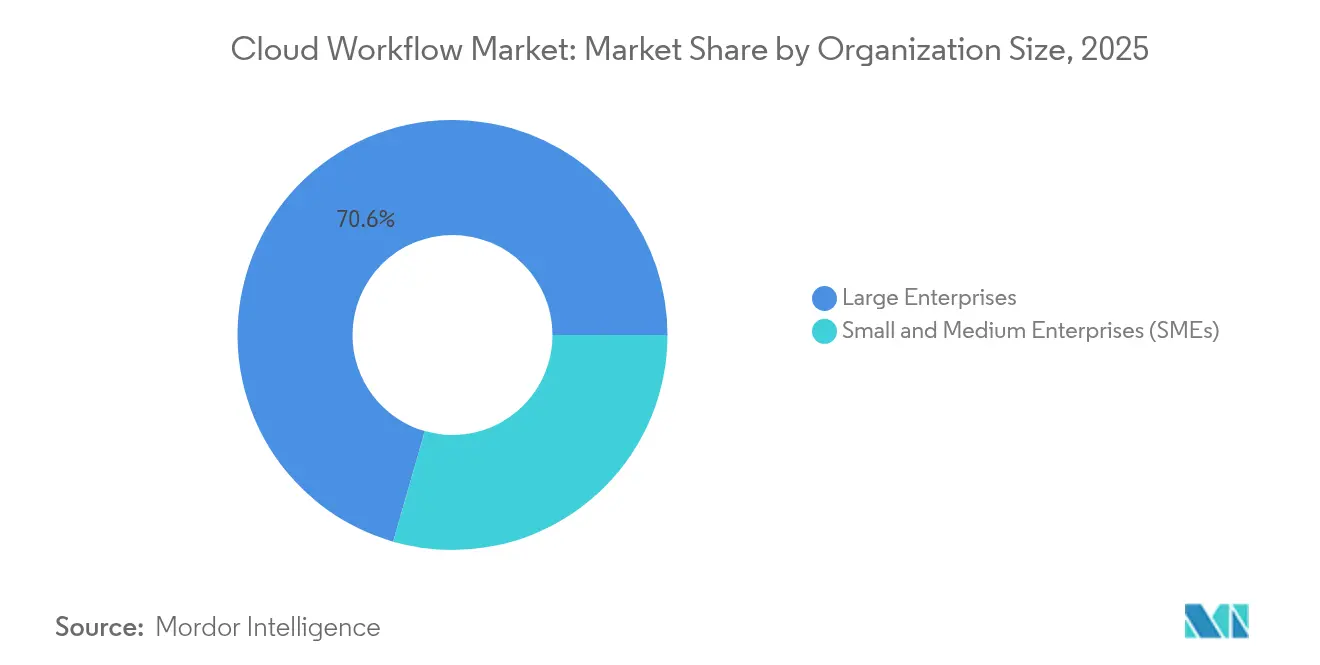

- By organization size, Large Enterprises accounted for 70.55% share of the cloud workflow market size in 2025 and Small and Medium Enterprises are advancing at an 17.45% CAGR through 2031.

- By end-user vertical, BFSI captured 31.75% of revenue in 2025, whereas Retail and E-Commerce is set to rise at a 15.92% CAGR to 2031.

- By geography, North America commanded 38.65% share of the cloud workflow market size in 2025 and Asia-Pacific is expected to post a 16.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Workflow Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid migration to public and hybrid cloud infrastructure | +2.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Rise of low-/no-code platforms among business users | +3.2% | Global, particularly strong in North America and APAC | Short term (≤ 2 years) |

| AI-driven automation elevating ROI and analytics insight | +4.1% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Operational-cost pressure pushing workflow outsourcing | +2.5% | Global, with emphasis on cost-sensitive emerging markets | Long term (≥ 4 years) |

| Expansion of industry-specific sovereign cloud templates | +1.9% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Edge-native orchestration for latency-critical IoT flows | +1.6% | Global, with manufacturing hubs in APAC and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Migration to Public and Hybrid Cloud Infrastructure

Enterprises view cloud migration as fundamental to modernizing workflows that rely on elastic compute and global reach. Multi-cloud patterns give risk-averse industries flexibility to segregate sensitive workloads while tapping public-cloud economics for burst capacity. A 2023 IBM study found that 92% of executives aim to digitize and apply AI to their workflows by 2025. Asia-Pacific banks, guided by updated supervisory notices, now deploy regulated workloads on cloud platforms once off-limits, accelerating regional uptake. As more systems operate in cloud environments, each new integration raises network effects that amplify platform value. Sovereign-cloud blueprints in Australia, Japan, and Singapore illustrate how policy can shape architecture choices without stalling adoption.

Rise of Low-/No-Code Platforms Among Business Users

Low-code design tools push automation to the business front line. KPMG reports that every surveyed enterprise has achieved measurable ROI from low-code deployments, with 34% already running the technology inside core ERP workflows. Generative AI now turns text prompts into live flows, shrinking build cycles from weeks to hours. Democratization boosts agility but complicates governance, as a wider creator base increases variation in security posture. Platform vendors answer with policy-driven guardrails and unified monitoring that keep compliance teams in control. Microsoft’s deep integration of ServiceNow’s Now Assist into Teams shows how conversational experiences expand the user pool without rewriting back-end logic.

AI-Driven Automation Elevating ROI and Analytics Insight

Machine-learning enhancement transforms rule-based automations into adaptive, self-optimizing workflows. UiPath’s use of advanced language models reduced healthcare prior-authorization times by 50%, underscoring tangible savings. AI heat-maps detect bottlenecks in near real time, recommending fixes that operations managers can deploy in a click. Appian’s Autoscale runs up to 6 million workflows per hour under FedRAMP controls, proving that compliance and velocity are not mutually exclusive[1]Appian, “Introducing Appian Autoscale,” appian.com. Competitive advantage arises from the data exhaust of every execution, letting firms spot trends invisible to manual review. Paid AI add-ons therefore command premium pricing yet often pay back within a fiscal quarter.

Operational-Cost Pressure Pushing Workflow Outsourcing

With margins tight, companies externalize non-core processes to partners that bundle technology, talent, and outcome guarantees. Digital components lift contract value far beyond classic labor-arbitrage deals, creating room for co-innovation on top of base cost savings. Vendors assume KPIs such as cycle-time reduction or error-rate caps, aligning incentives with client objectives. Nevertheless, success hinges on upfront process re-design and clear joint-accountability frameworks; otherwise, automation merely shifts inefficiency outside the building.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-security and privacy concerns | -2.1% | Global, with heightened impact in Europe due to GDPR | Short term (≤ 2 years) |

| Acute skill gaps in cloud-native workflow design | -1.8% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Vendor lock-in and poor multi-cloud interoperability | -1.4% | Global, with emphasis on enterprises with complex IT landscapes | Medium term (2-4 years) |

| Escalating egress-fee economics impacting TCO | -0.9% | Global, with reduced impact as major providers cut fees | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Security and Privacy Concerns

Organizations continue to weigh automation gains against exposure risks when data leaves internal boundaries. The Cloud Security Alliance warns that opaque data flows complicate residency compliance in jurisdictions such as the European Union[2]Cloud Security Alliance, “Data Residency in the Cloud Era,” cloudsecurityalliance.org. Healthcare providers in particular must prove chain-of-custody for protected health information across multi-cloud footprints. Fragmented statutes in Asia-Pacific add cost and delay, as each new project demands a fresh legal review. Providers respond with region-pinning, customer-managed encryption keys, and audit-ready logging, yet confidence builds slowly.

Acute Skill Gaps in Cloud-Native Workflow Design

A global talent shortfall drives up project costs and stretches timelines. Studies suggest that unfilled roles in cloud and automation may reach 85 million by 2030, eroding gains from faster software cycles. HashiCorp data shows 91% of practitioners report avoidable cloud spend due to sub-optimal configurations, much of it traceable to skill gaps. Upskilling efforts help but cannot close the gap overnight, leaving consultancies and managed-service providers to plug holes at premium rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Function: Finance and Accounting Hold Primacy

Finance owns the largest slice of the cloud workflow market with 35.25% share in 2025. Compliance calendars, multi-entity consolidation, and audit trails make automated workflows indispensable to CFO teams. As generative AI matures, real-time anomaly spotting and auto-narrative reporting further raise adoption appetite. Sales and Marketing, while smaller, posts the fastest growth at 16.32% CAGR as revenue teams orchestrate omnichannel journeys and AI-led lead scoring. These gains should lift the overall cloud workflow market size for front-office flows to USD-denominated, double-digit growth every year through 2031. Cross-function templates blend finance approval gates with sales quoting, reflecting a trend toward end-to-end order-to-cash automation.

The cloud workflow industry also sees Operations modernize supply-chain coordination, and HR leaders automate recruitment funnels. UiPath’s October 2024 pact with SAP shows how cross-stack connectors help companies blend ERP and non-ERP data without manual extract scripts. Legal and procurement remain underpenetrated yet ripe, as contract-lifecycle stress mounts with global supply volatility.

By Deployment Model: Hybrid Strategies Gain Momentum

Public cloud retains a 66.10% hold on the cloud workflow market in 2025. Yet hybrid architectures grow faster, clocking 17.02% CAGR as firms hedge sovereignty risks. Data-sensitive workloads anchor on-prem cores while elastic analytics run in the public layer. As egress fees drop, the cloud workflow market share of hybrid designs will rise steadily, giving platform vendors a fresh battleground over portability perks. The cloud workflow industry therefore prizes open APIs and policy-driven portability that let administrators shift workloads without re-authoring logic.

Private clouds remain for classified data or regulatory edge cases but attract less net-new spend. Google’s 2024 cut in cross-cloud transfer costs signals a broader shift toward fee relief, encouraging architecture choices based on performance rather than penalty avoidance.

By Organization Size: SME Acceleration Reshapes Demand

Large enterprises still command 70.55% of spending, yet SMEs produce the highest velocity at 17.45% CAGR. Simplified subscriptions, pre-built flows, and embedded best-practice guards lower entry friction, aligning with lean IT budgets. Appian’s SMB cohort delivered double-digit cloud-subscription growth in 2024, proving willingness to pay for outcome-oriented tooling. As SME volume expands, vendors must rebalance packaging, moving from seat-based to usage-tier models that reward efficiency gains.

The vast unmet base among mid-market firms should add millions of new users to the cloud workflow market by 2031. Open Marketplace plug-ins for payroll, invoicing, and local tax filings draw interest from owners who need compliance assurance without hiring specialists.

By End-User Vertical: BFSI Leads While Retail Gains Speed

BFSI continues to capture 31.75% of cloud workflow market size due to stringent risk and reporting mandates. Anti-money laundering flows, real-time fraud detection, and credit approvals anchor investment. Retail and E-Commerce, running at 15.92% CAGR, automates personalization, inventory updates, and returns processing. Healthcare gains momentum through HIPAA-compliant clinical flows such as UiPath’s medical-record summarizer, showing that specialized AI agents can unlock regulated sectors. Energy, telecom, and government round out adoption, each with unique compliance layers but similar need for traceability.

Horizontal platforms respond by shipping vertical starter kits that shorten time-to-value. ServiceNow’s telecom service-management pack and Appian’s life-science quality suite illustrate this move toward out-of-the-box compliance.

Geography Analysis

North America controls 38.65% of 2025 spend, buoyed by Fortune 500 cloud-first mandates, deep venture capital activity, and supportive regulators who grant cloud usage approvals to banks and federal agencies. Tight labor markets accelerate automation investments as firms offset talent shortages with digital labor. Europe remains compliance-centric; GDPR spurs demand for data-sovereign architectures and meticulous audit controls. Localized regions inside hyperscaler footprints enable resident processing, keeping continental adoption on a steady upward path despite policy complexity.

Asia-Pacific delivers the fastest climb at 16.68% CAGR. Government stimulus programs, such as Singapore’s Digital Economy Blueprint and India’s Production-Linked Incentive updates, push companies toward cloud modernization. The Asian Development Bank projects that cloud computing could lift regional GDP by up to 0.7% between 2024 and 2028. Sovereign-cloud deals in Korea and Japan illustrate a pragmatic answer to residency concerns without forgoing hyperscaler speed. ServiceNow’s 2025 investment in inMorphis signals vendor commitment to build local talent pools and maintain culturally-relevant support.

The Middle East and Africa, though a smaller base, reports double-digit expansion as energy and public-sector entities digitize citizen services. The launch of region-hosted data centers by leading clouds removes a prior adoption hurdle. South America progresses unevenly; Brazil advances on the back of central-bank open-finance mandates while smaller economies lag until telecom bandwidth improves. Cross-market collaboration schemes, such as New Zealand’s All-of-Government Common Process Model that shares workflow blueprints with agencies, demonstrate how policy leadership can compress rollout time.

Competitive Landscape

Incumbent enterprise-software giants, born in ERP and ITSM, now position workflow as the nervous system of digital operations. They face specialist automation vendors whose pure-play focus yields rapid product cycles. A third axis involves hyperscalers embedding workflow engines into platform offerings, bundling compute credits with automation licenses to drive stickiness.

ServiceNow’s USD 2.85 billion Moveworks buy in March 2025 broadens its generative-AI talent pool and shores up conversational interfaces. UiPath stakes its claim on deep AI integration partnerships, as seen in its Google Cloud alliance that targets healthcare. Appian differentiates through FedRAMP-ready scalability that appeals to defense and civilian agencies. Microsoft and IBM fold orchestration features into broader cloud suites, betting on account depth rather than standalone feature parity.

White-space hotspots include edge-native orchestration, pre-validated sovereign-cloud stacks, and AI agents that self-tune workflows. Vendors invest in marketplaces where partners publish vertical accelerators, cutting delivery time for regulated customers. Pricing models evolve toward consumption-based tiers honored across on-prem, cloud, and edge, easing fears of lock-in. The race now centers on who can ship governance frameworks that let citizen developers innovate safely, solving the skill-gap problem at scale.

Cloud Workflow Industry Leaders

IBM Corporation

SAP SE

Pegasystems Inc.

Microsoft Corporation

Appian Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ServiceNow closed its USD 2.85 billion Moveworks acquisition, adding AI assistant and enterprise search to its platform.

- February 2025: ServiceNow invested in inMorphis to deepen India and ASEAN reach while training 2,500 specialists in generative-AI workflows.

- January 2025: ServiceNow expanded its Google Cloud alliance, listing the platform on Google Cloud Marketplace with native BigQuery feeds for instant analytics.

- January 2025: ServiceNow and SoftwareOne entered a multi-year pact to blend workflow automation with license-optimization services, promising higher ROI on enterprise tech portfolios.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the cloud workflow market as all revenues earned from cloud-hosted platforms and closely allied support services that let business users design, execute, and monitor process flows across multiple enterprise systems. These figures cover subscription, usage-based, and perpetual license models for SMEs and large enterprises across all verticals.

(Scope exclusion) On-premise workflow software and fully custom, one-off scripts are not included.

Segmentation Overview

- By Business Function

- Operations

- Finance and Accounting

- HR and Talent Management

- Sales and Marketing

- Other Business Functions

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Vertical

- BFSI

- Telecommunications and IT

- Retail and E-Commerce

- Government

- Healthcare and Life Sciences

- Other End-User Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

To close gaps, we interviewed platform product managers, implementation partners, and IT heads in North America, Europe, and Asia-Pacific. Discussions explored average seat counts, churn, hybrid-cloud spillover, and typical price stair-steps, allowing us to cross-check desk estimates and refine adoption curves.

Desk Research

Our analysts first mapped the supply landscape through non-paywalled sources such as the US Bureau of Labor Statistics, Eurostat ICT surveys, OECD cloud adoption trackers, and trade-group white papers from the Cloud Native Computing Foundation and the Workflow Management Coalition. Public company 10-Ks, investor decks, and press releases helped size vendor revenues, while patent abstracts from Questel clarified emerging AI-driven orchestration techniques. Complementary insights were drawn from D&B Hoovers for vendor financial splits, Dow Jones Factiva for deal news, and customs shipment dashboards that reveal regional data-center hardware inflows, which proxy future workflow capacity. This list is illustrative; many further sources were consulted to validate totals and assumptions.

Market-Sizing & Forecasting

The core model begins with a top-down reconstruction of global enterprise software spend, isolating cloud workflow shares through adoption ratios gathered above. Results are then sense-checked with selective bottom-up roll-ups of leading vendors' public revenues and sampled average selling price-by-user calculations. Key variables include active SaaS seats, workflow penetration within digital transformation budgets, average annual price inflation, regional data-sovereignty premiums, and the ramp-up of AI-assisted design tools. Forecasts employ multivariate regression blended with ARIMA to capture cyclical IT spending and long-run digitization trends. Where bottom-up gaps appear, midpoint estimates from interview ranges are used before final triangulation.

Data Validation & Update Cycle

We run variance checks against external macro indicators, reroute anomalies for senior review, and refresh each dataset annually, triggering interim updates when material vendor disclosures or regulatory shifts occur. A final analyst pass ensures the client receives the most current view.

Why Mordor's Cloud Workflow Baseline Commands Reliability

Published market numbers often differ because firms choose distinct scopes, price assumptions, and refresh rhythms. Our framework starts with a clarified definition, folds in verified usage metrics, and applies an annually renewed model, which together anchor a balanced midpoint that decision-makers can trust.

Key gaps arise when other studies bundle on-prem tools, omit service revenues, apply unvetted linear growth, or ignore currency volatility, whereas Mordor adjusts for each factor and re-checks inputs through live interviews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.50 B (2025) | Mordor Intelligence | - |

| USD 4.34 B (2024) | Global Consultancy A | Excludes support services and hybrid deployments |

| USD 3.41 B (2023) | Trade Journal B | Mixes on-prem data and uses straight-line projection |

| USD 4.97 B (2023) | Regional Analyst C | Counts licenses only; no currency uniformity |

In sum, our disciplined source mix, transparent scope choices, and iterative checks produce a dependable baseline that sits between overly conservative and aggressively optimistic views, giving stakeholders a clear, reproducible foundation for strategy and planning.

Key Questions Answered in the Report

What is the current size of the cloud workflow market?

The cloud workflow market is valued at USD 7.53 billion in 2026, growing toward USD 15.68 billion by 2031 at a 15.82% CAGR.

Which business function holds the largest adoption share?

Finance and Accounting leads with 35.25% share owing to stringent compliance and audit needs.

Why are hybrid deployments gaining traction?

Hybrid models balance data-sovereignty, latency, and cost considerations while avoiding vendor lock-in, driving a 17.02% CAGR through 2031.

How are SMEs influencing the cloud workflow market?

Low-code platforms remove technical barriers, allowing SMEs to adopt automation quickly and fuel an 17.45% CAGR in their segment.

Which region is expanding fastest?

Asia-Pacific shows the highest growth at 16.68% CAGR, supported by sovereign-cloud policies and government-led digitization programs.

What role does AI play in modern workflows?

Generative AI adds predictive insights and conversational build tools, cutting cycle times and boosting ROI, as seen in UiPath’s 50% reduction in healthcare authorization processing.

Page last updated on: