Clinical Trial Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

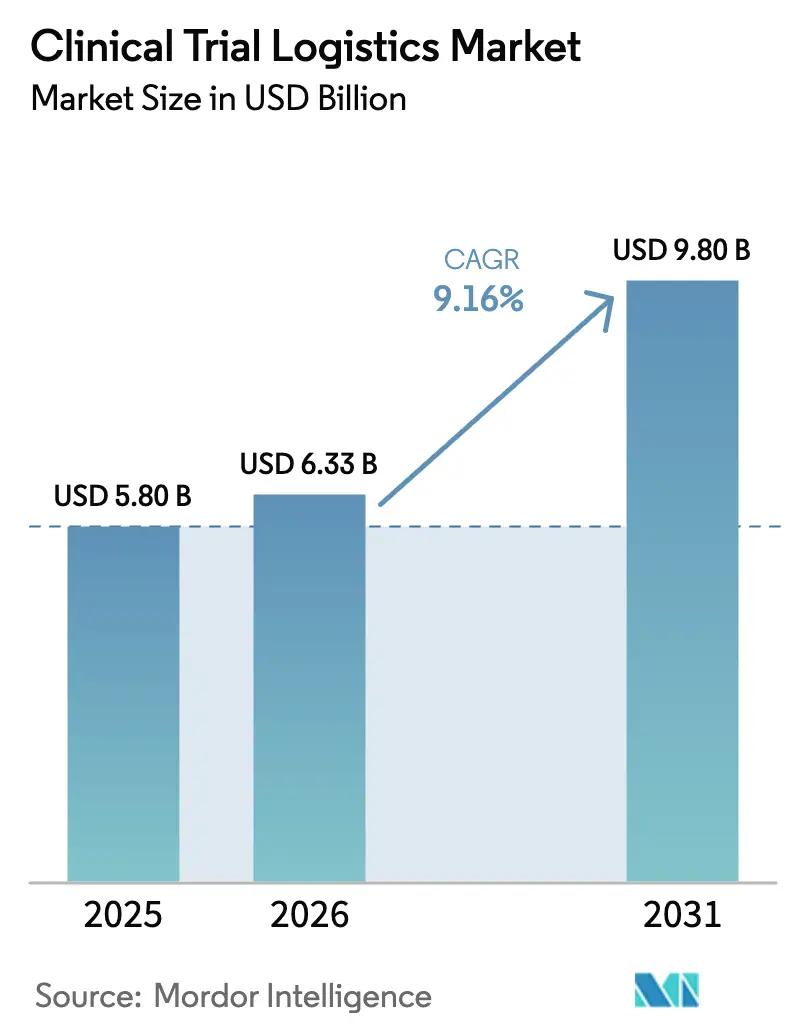

| Market Size (2026) | USD 6.33 Billion |

| Market Size (2031) | USD 9.8 Billion |

| Growth Rate (2026 - 2031) | 9.16% CAGR |

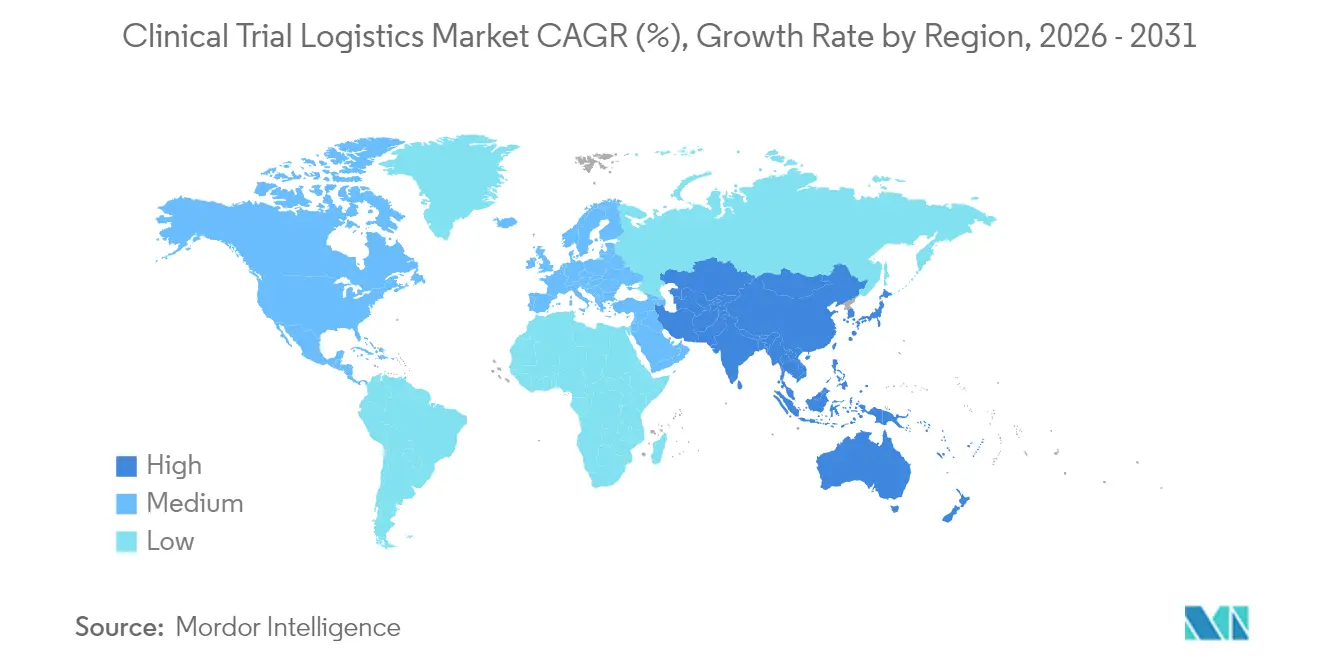

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Logistics Market Analysis by Mordor Intelligence

Clinical Trial Logistics Market size in 2026 is estimated at USD 6.33 billion, growing from 2025 value of USD 5.80 billion with 2031 projections showing USD 9.80 billion, growing at 9.16% CAGR over 2026-2031. Robust growth stems from decentralized trial adoption, rising ultra-cold chain shipments for cell and gene therapies, and global regulatory harmonization encourages multi-regional studies. Direct-to-patient delivery networks are reshaping distribution models and boosting value-added services, while predictive analytics limit wastage caused by volatile patient recruitment. Capital-intensive investments in temperature-controlled hubs and IoT tracking strengthen service reliability, and outsourcing momentum among biopharma sponsors fuels demand for integrated, end-to-end solutions.

Key Report Takeaways

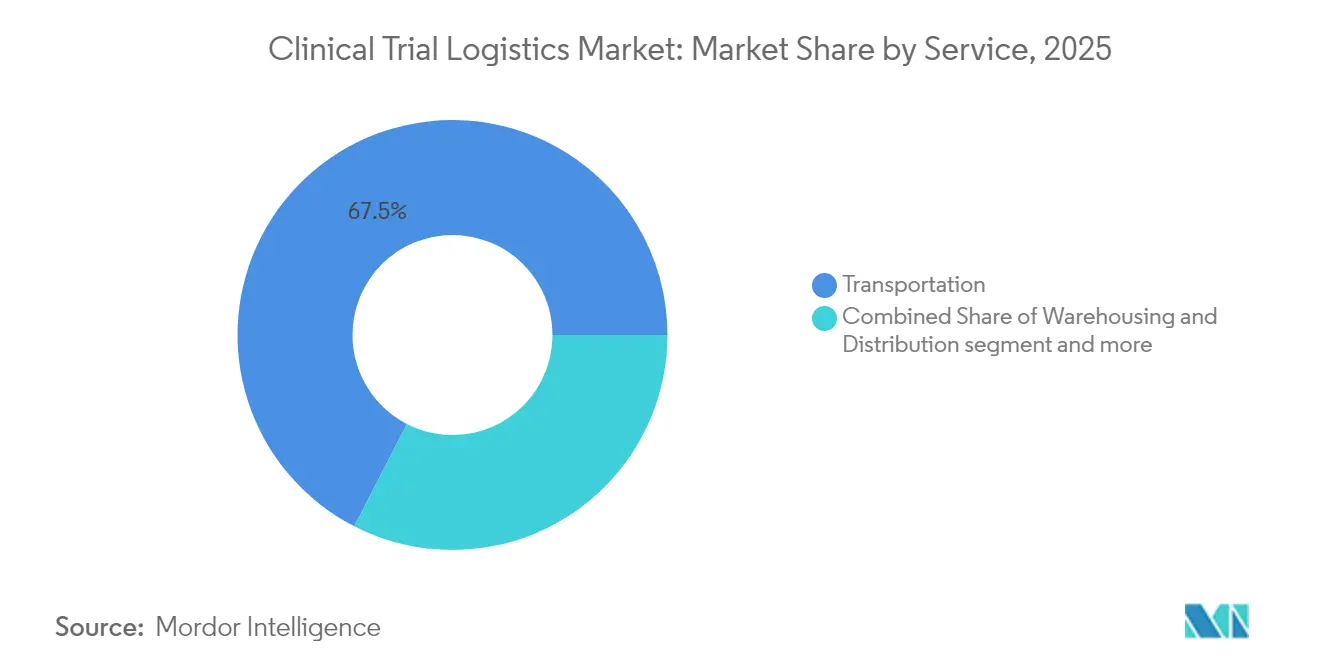

- By service, transportation held 67.45% of the clinical trial logistics market share in 2025. The clinical trial logistics market for value-added services is set to expand at a 10.35% CAGR between 2026-2031.

- By clinical phase, Phase III accounted for 45.12% of the clinical trial logistics market revenue share in 2025. The clinical trial logistics market for Phase I is projected to grow at 10.12% CAGR between 2026-2031.

- By therapeutic area, oncology led with 35.74% of the clinical trial logistics market size in 2025. The clinical trial logistics market for rare and orphan diseases will rise to 11.65% CAGR between 2026-2031.

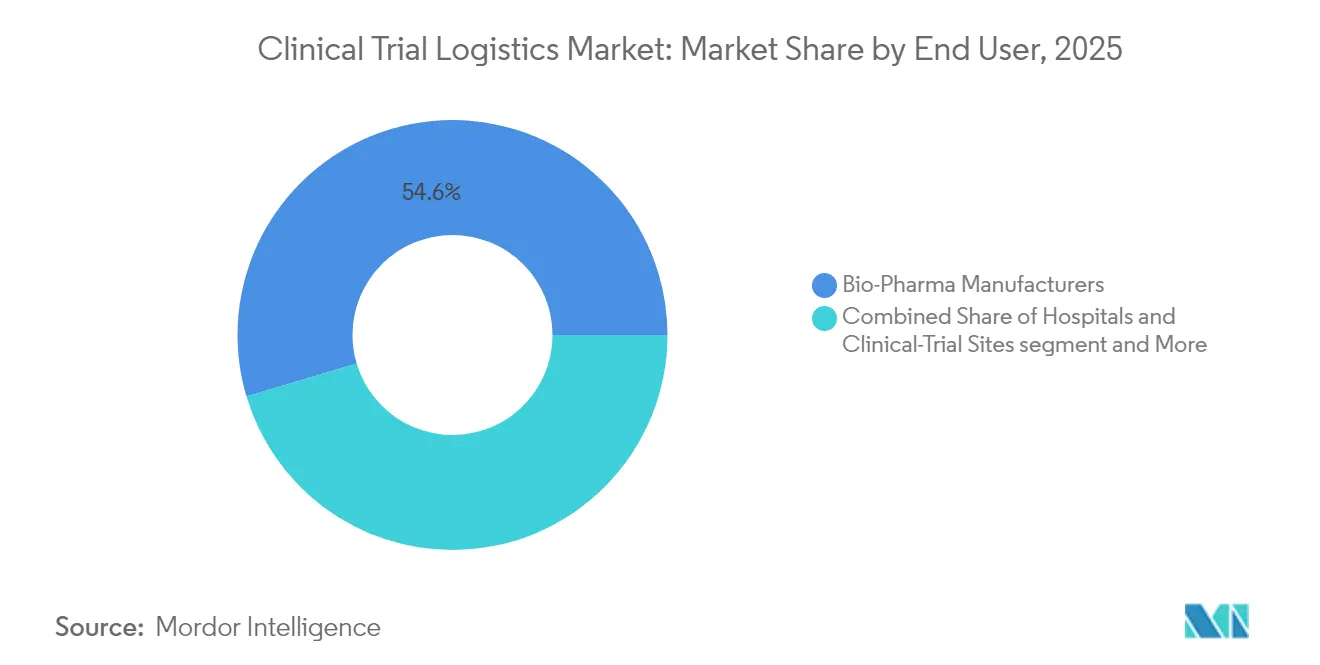

- By end-user, bio-pharma manufacturers represented 54.62% of the clinical trial logistics market share in 2025. The clinical trial logistics market for the CRO/CMO segment records the fastest 10.98% CAGR between 2026-2031.

- By temperature range, cold-chain services commanded 64.91% of the clinical trial logistics market size in 2025. The clinical trial logistics market for cold chain is advancing at an 11.42% CAGR between 2026-2031.

- By geography, North America led with 38.25% revenue share in 2025, while Asia-Pacific is projected to grow at an 10.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Clinical Trial Logistics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| An ageing population elevates multi-dose demand | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Decentralized/DtP adoption boosts outsourcing | +2.1% | North America, Asia-Pacific | Medium term (2-4 years) |

| The cell & gene therapy pipeline requires an ultra-cold chain | +1.8% | North America, Europe, and expanding Asia-Pacific | Medium term (2-4 years) |

| ICH GCP R3 harmonization enables multi-regional trials | +1.3% | Europe, Asia-Pacific | Short term (≤ 2 years) |

| Adaptive & platform trials lift mid-study change orders | +1.6% | North America, Europe, and emerging Asia-Pacific | Medium term (2-4 years) |

| Patient-centric retention drives home-healthcare logistics | +1.4% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Population Elevates Multi-Dose Trial Demand

Population ageing raises chronic disease prevalence, lengthening dosing schedules and amplifying inventory complexity. Japan, where 29% of citizens are ≥65 years, has scaled digital tools to support older trial participants. Logistics providers gain opportunities to introduce senior-friendly packaging and predictive stock-replenishment systems that avert disruptions during prolonged studies.

Decentralized/DtP Trial Adoption Accelerating Service Outsourcing

Full-scale decentralized programs—such as DCT Japan’s partnerships across seven disease areas—shift supply chains from site-centered depots to patient households. Service providers must orchestrate last-mile delivery, returns, and data capture under divergent local rules, reinforcing the outsourcing trend. Specialized clinical trial insurance products now cover home-delivery liabilities, heightening compliance requirements.

Cell & Gene Therapy Pipeline Requiring Ultra-Cold-Chain Capabilities

Storage between –20 °C and –150 °C is now routine for autologous therapies, prompting heavy investment in cryogenic freezers, validated packaging, and real-time telemetry. Packaging shortages have triggered long-term supplier contracts and consolidation among firms that can amortize capex across multiple sponsors.

ICH GCP R3 Harmonization Enabling Multi-Regional Trials

The EU’s uptake of ICH E6(R3) standards intensifies data-integrity demands and spurs adoption of digital quality-management systems. Consistent rules make cross-border studies easier for sponsors yet force logistics companies to prove compliance through granular tracking and frequent audits.

Restraints Impact Analysis of Clinical Trial Logistics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile recruitment forecasts cause waste | -1.4% | Competitive therapeutic areas worldwide | Short term (≤ 2 years) |

| Cross-border customs delays for specimens | -0.9% | Europe-United States and China-United States corridors | Medium term (2-4 years) |

| Shortage of temperature-controlled packaging | -1.1% | Supply chains concentrated in Asia | Medium term (2-4 years) |

| High liability insurance for DtP deliveries | -0.8% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Patient Recruitment Forecasts Causing Supply Overages & Waste

Over half of global trials miss enrolment goals, compelling sponsors to over-allocate inventory. Machine-learning models now predict accrual-failure risk with AUC 0.744, enabling leaner production while safeguarding continuity. Yet smaller biotech’s still struggle to fund advanced analytics, keeping wastage high.

Cross-Border Customs Delays for Biological Specimens

US CBP’s stricter documentation for biologics and multi-agency clearance lengthen transit windows. Trade tensions expose Chinese CDMOs to sudden delays, driving buffer-stock strategies and regional hub warehousing[1]U.S. Customs and Border Protection, “Biological Materials Import Guidance,” cbp.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Clinical Trial Logistics Market Segment Analysis

By Service:

Transportation Dominance Drives Infrastructure InvestmentTransportation services generated 67.45% of 2025 revenue, underscoring the criticality of time-definite delivery within the clinical trial logistics market. DHL’s EUR 2 billion allocation for new GDP-certified hubs and expanded cold chain lanes typifies the high capital barriers DHL faces. Value-added offerings enjoy a 10.35% CAGR as sponsors bundle kitting, relabeling, and Qualified Person release to a single provider. Within transportation, road services dominate regional moves, whereas premium-priced airfreight protects time- and temperature-sensitive payloads. Integration across modes supports seamless chain-of-custody, central to sponsor audits and ICH GCP R3 compliance.

Ongoing modal diversification strengthens resilience: chartered freighters for bulk vaccine moves, dedicated courier networks for cryogenic packages, and in-country bike couriers for same-day patient replenishment. Providers with multi-modal orchestration platforms retain an edge as the clinical trial logistics market transitions toward data-driven routing and predictive ETAs.

By Clinical Phase:

Early-Stage Acceleration Reshapes Resource AllocationPhase III studies continue to absorb the largest budget share, reflecting their expansive cohorts and rigorous endpoint monitoring. Yet a 10.12% CAGR in Phase I activity signals heightened early-stage screening, particularly in precision oncology. Japan’s fast-track waiver of domestic Phase I for imported assets expedites first-in-human starts, redistributing logistics spend upstream. Adaptive protocols compress timelines, demanding nimble supply chains that can upscale from micro-dosing to multi-arm expansion without service disruption.

Inventory digital twins enable real-time demand recalculation as dose-escalation cohorts progress, trimming waste. Sponsors increasingly stipulate service-level agreements that tie provider fees to enrolment adherence, incentivizing analytics investment. The clinical trial logistics market size for Phase I consignments is forecast to climb steadily as cell-therapy dose-finding studies proliferate.

By Therapeutic Area:

Precision Medicine Drives Specialized RequirementsOncology’s 35.74% share mirrors its pipeline dominance and the complexity of biomarker-guided regimens. Rare-disease programs, up 11.65% CAGR, demand bespoke pickups from geographically dispersed centers of excellence and bespoke kitting for minute cohorts. Logistics partners must handle companion-diagnostic kits alongside investigational products under unified tracking.

Combination therapy trials escalate packaging variety and require harmonized shelf-life management. IoT-enabled shippers paired with blockchain audit trails protect chain-of-identity for autologous products, supporting regulator scrutiny. The clinical trial logistics market share for rare-disease consignments remains small but commands premium pricing due to service intricacy.

By End-User:

Outsourcing Momentum Accelerates Service DemandBio-pharma sponsors produced 54.62% of 2025 revenue, yet CRO/CMO demand is accelerating at 10.98% CAGR as outsourcing deepens. Audax Private Equity’s purchase of Avantor Clinical Services indicates private-capital confidence in scalable third-party models. Sponsors offload regulatory complexity and temperature-controlled capex, while CROs seek differentiated, tech-enabled partners.

Site networks consolidate procurement, giving logistics firms opportunities to negotiate umbrella contracts that standardize processes across hundreds of hospitals. End-to-end control of planning, distribution, reverse logistics, and data capture is becoming table stakes in the clinical trial logistics industry.

By Temperature Range:

Cold Chain Innovation Drives Premium GrowthCold-chain consignments commanded 64.91% of 2025 revenue, and ultra-cold segments record the fastest 11.42% CAGR. Controlant’s Saga Card, which transmits real-time temperature and geolocation data, exemplifies innovation that expands visibility. Providers face shortages of qualified phase-change materials, prompting vertical integration into packaging manufacture.

Regulators increasingly inspect excursion records, raising quality-management requirements. The clinical trial logistics market size for ultra-cold moves is poised to grow by 2031, underpinning premium-margin growth as cell-therapy volumes scale.

Geography Analysis

North America and APAC Clinical Trial Logistics Market

North America claimed 38.25% of 2025 revenue, buoyed by dense sponsor headquarters, established depot networks, and mature regulatory frameworks. The region continues to invest in decentralized models and advanced analytics, although labor shortages elevate operating costs. Asia-Pacific leads expansion at an 10.77% CAGR as China surpasses the United States in new-trial count. Regulatory streamlining—such as China’s proposed 30-day IND review window—draws multinationals seeking accelerated recruitment.

EMEA and South America Clinical Trial Logistics Market

Japan’s drug-lag reforms and Australia’s HREC fast-track pathways further boost regional demand. India’s CDSCO digital portal eases import permitting, spurring depot investments. The clinical trial logistics market size for Asia-Pacific cold-chain consignments is projected to double between 2026 and 2031. Europe benefits from EMA oversight and ICH GCP R3 alignment, supporting cross-border consolidation of Phase I units and pan-EU adaptive trials. South America’s share remains modest but DHL’s Brazil-to-United States medical express lane shortens lead times to 24 hours, elevating the continent’s attractiveness for vaccine studies. The Middle East and Africa see nascent growth tied to oncology trials in Gulf Cooperation Council states, although customs and power-supply reliability still impede large-scale cold-chain adoption.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

Competitive intensity is moderate, with global integrators (DHL, UPS, FedEx) leveraging broad networks and specialized providers (World Courier, Marken) offering niche regulatory expertise. UPS’s acquisition of Frigo-Trans and BPL strengthens European cryogenic capacity. Investment priorities include IoT sensor fleets, blockchain traceability, and machine-learning demand forecasting.

White-space opportunities lie in ultra-cold infrastructure for autologous cell therapies, integrated direct-to-patient orchestration, and cloud platforms that marry RTSM with transport management. Start-ups delivering robotic micro-fulfilment or drone delivery pilot projects face scale-up hurdles, yet their technologies are ripe for partnership or acquisition.

Customer stickiness hinges on audit performance, on-time metrics, and digital transparency. Providers that can guarantee continuous temperature integrity from manufacturer to patient, supported by automated compliance documentation, command pricing premiums within the clinical trial logistics market.

Clinical Trial Logistics Industry Leaders

Alamc Group

Parexel International Corporation

DHL

Marken (UPS Healthcare)

Thermo Fisher Scientific – Fisher Clinical Services

- *Disclaimer: Major Players sorted in no particular order

Clinical Trial Logistics Market Companies Covered in this Report

- Almac Group

- Thermo Fisher Scientific - Fisher Clinical Services

- Marken (UPS Healthcare)

- DHL Supply Chain & Healthcare

- Parexel International Corporation

- Catalent Inc.

- PCI Pharma Services

- World Courier (Cencora)

- FedEx Clinical Transport Solutions

- Kuehne + Nagel PharmaChain

- Biocair

- Movianto (Walden Group)

- Sharp Clinical Services

- UDG Healthcare plc (Ashfield Clinical)

- Capsugel (Lonza)

- Klifo A/S

- Bilcare Limited

- Eurofins Scientific

- PRA Health Sciences (ICON plc)

- WuXi Clinical Supply Services

- Arvato Supply Chain Solutions

- DPDgroup Healthcare

- Yusen Logistics Pharma

- BioStorage Technologies*

Recent Industry Developments in Clinical Trial Logistics Market

- June 2025: DHL Group committed EUR 2 billion (USD 2.29 billion) by 2030 to expand GDP-certified Pharma Hubs and cold-chain lanes worldwide.

- May 2025: Bionical Emas and Pharma Resources formed an exclusive global supply partnership covering multi-therapeutic trials.

- May 2025: Perceptive eClinical introduced ClinPhone Pro, a next-gen RTSM platform with rolling forecast algorithms.

- April 2025: DHL Express launched a next-day Brazil-to-United States medical express service for time-critical trial materials.

Clinical Trial Logistics Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the clinical trial logistics market as every outsourced activity that moves investigational medicinal products, comparators, medical devices, ancillary supplies, and biological samples between manufacturers, depots, trial sites, and patients under Good Distribution Practice. According to Mordor Intelligence, the market is valued at USD 5.80 billion in 2025 and is forecast to reach USD 9.04 billion by 2030.

Scope Exclusion: Routine courier services that fail to comply with GxP and sponsor-managed in-house supply chains are not counted.

Segments Covered in This Report

- By Service

- Transportation

- Road

- Air

- Others

- Warehousing & Distribution

- Value-Added Services (Labelling, Kitting, QP Release)

- Transportation

- By Clinical Phase

- Phase I

- Phase II

- Phase III

- Phase IV / Post-Marketing

- By Therapeutic Area

- Oncology

- Cardiovascular Diseases

- Rare / Orphan Diseases

- Immunology & Inflammation

- Endocrine & Metabolic Disorders

- Neurology & Psychiatry

- Others

- By End-user

- Bio-Pharma Manufacturers

- CROs (Contract Research Organizations) & CMOs (Contract Manufacturing Organizations)

- Hospitals & Clinical-Trial Sites

- Other End Users

- By Temperature Range

- Cold Chain

- Ambient (15-25 °C)

- Refrigerated (2–8 °C)

- Frozen (0 °C to -20 °C)

- Ultra-Cold / Cryogenic (-20 °C to -150 °C)

- Non Cold Chain

- Cold Chain

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We enriched desk findings by interviewing supply-chain directors at biopharma sponsors, project managers in leading CROs, depot operators across North America, Europe, and Asia-Pacific, and regulators overseeing GMP audits. Their firsthand estimates of shipment frequency, lane mix, and spoilage rates filled gaps and sharpened our assumptions.

Desk Research

Mordor analysts assembled a fact base from tier-1 public sources such as ClinicalTrials.gov, the EU Clinical Trials Register, WHO-ICTRP, U.S. FDA and EMA inspection records, and International Air Transport Association capacity reports. Macro indicators on R&D outlays and cross-border trade were added from World Bank datasets and International Society for Pharmaceutical Engineering white papers. Financial signals and competitor intelligence came through paid access to D&B Hoovers and Dow Jones Factiva, while comparator pricing was sampled from customs filings and depot tenders. The sources noted are illustrative; many other public and paid references informed data collection, validation, and narrative shaping.

Market-Sizing & Forecasting

A blended top-down model reconstructs global spend by linking active-trial counts per phase to average logistics cost per patient, then weighting for cold-chain penetration, decentralized trial share, and cross-border shipment intensity. Bottom-up validations, sampled depot throughput, carrier revenue splits, and median ASP × volume checks anchor totals before alignment. Forecasts employ multivariate regression on trial starts, protocol amendments, R&D intensity, fuel indices, and biologic pipeline share; coefficients are corroborated with primary experts and scenario tested for direct-to-patient uptake.

Data Validation & Update Cycle

Model outputs undergo automated variance scans, peer review, and senior sign-off. We benchmark against fresh regulatory notices or major funding events, refresh annually, and issue interim updates whenever deviations exceed preset thresholds.

How Mordor Intelligence's Clinical Trial Logistics Market Size Compares to Other Published Estimates

Published estimates often diverge because firms select different service mixes, patient-count multipliers, and refresh cadences. Our disciplined scope selection plus transparent variable mapping tempers that volatility for decision makers.

Key gap drivers include whether comparators and ancillary kits are bundled, treatment of sponsor-run depots, and the month chosen for currency conversion; some publishers upscale historic ASPs without freight-rate resets, whereas Mordor updates these inputs each year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.80 B (2025) | Mordor Intelligence | |

| USD 3.98 B (2024) | Global Consultancy A | Excludes packaging & labeling and uses historic freight index without biologic premium |

| USD 4.29 B (2024) | Trade Journal B | Counts only logistics & distribution, omits manufacturing and comparator sourcing services |

| USD 14.88 B (2024) | Industry Analyst C | Broadly folds overall clinical trial operations and supply-chain management software into spend base |

The comparison shows that Mordor's moderate, fully itemized baseline, refreshed every twelve months, offers a balanced midpoint grounded in auditable trial counts and cost drivers, giving stakeholders a dependable foundation for strategic planning.

Key Questions Answered in the Report

What is the projected size of the clinical trial logistics market by 2031?

The market is expected to reach USD 9.80 billion by 2031, reflecting a 9.16% CAGR over 2026-2031.

Why is cold-chain logistics growing faster than ambient services?

Biologics, cell therapies, and gene therapies require stringent temperature control, driving cold-chain revenue, which held 64.91% share in 2025 and is expanding at an 11.42% CAGR.

Which region will witness the strongest growth in clinical trial logistics?

Asia-Pacific leads with an 10.77% CAGR as China surpasses the United States in annual trial starts and regional regulators streamline approvals.

How are decentralized trials altering logistics requirements?

Direct-to-patient delivery networks demand last-mile coordination, home-delivery liability coverage, and real-time monitoring platforms that traditional depot models do not provide.

What role do CROs and CMOs play in market expansion?

CROs/CMOs are the fastest-growing end-user segment at 10.98% CAGR because sponsors outsource specialized logistics, regulatory compliance, and technology capabilities.

What technologies are providers adopting to stay competitive?

IoT sensors, blockchain traceability, AI-based demand forecasting, and integrated RTSM-TMS platforms enhance visibility, compliance, and operational efficiency across global supply chains.

Page last updated on: