Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

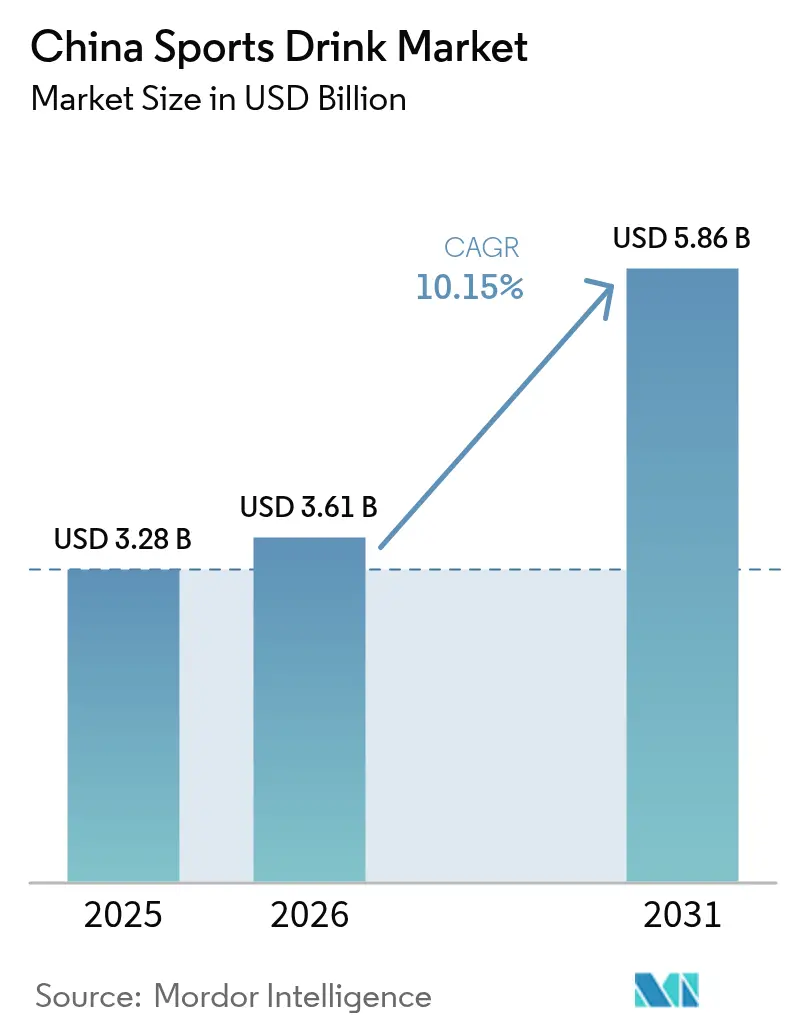

| Base Year Market Size (2025) | USD 3.28 Billion |

| Market Size (2026) | USD 3.61 Billion |

| Market Size (2031) | USD 5.86 Billion |

| Growth Rate (2026 - 2031) | 10.15% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Sports Drink Market Analysis by Mordor Intelligence

China's sports drink market size in 2026 is estimated at USD 3.61 billion, growing from 2025 value of USD 3.28 billion with 2031 projections showing USD 5.86 billion, growing at 10.15% CAGR over 2026-2031. This growth trajectory is fueled by policy-driven fitness initiatives, rapid urbanization, and a notable shift in consumer preferences from basic hydration to nutrient-rich, performance-oriented beverages. Currently, electrolyte-enhanced isotonic drinks lead the market, serving as everyday recovery solutions. Meanwhile, protein-fortified variants are gaining traction on mainstream shelves, touted as essential post-workout muscle builders. Packaging strategies are diverging: while low-cost PET caters to mass distribution, premium glass appeals to sustainability-conscious millennials. Additionally, manufacturing investments in inland provinces are slashing freight costs. In retail, supermarkets leverage scale and refrigeration, but specialty outlets are carving a niche, attracting premium consumers with expert insights on functional claims.

Key Report Takeaways

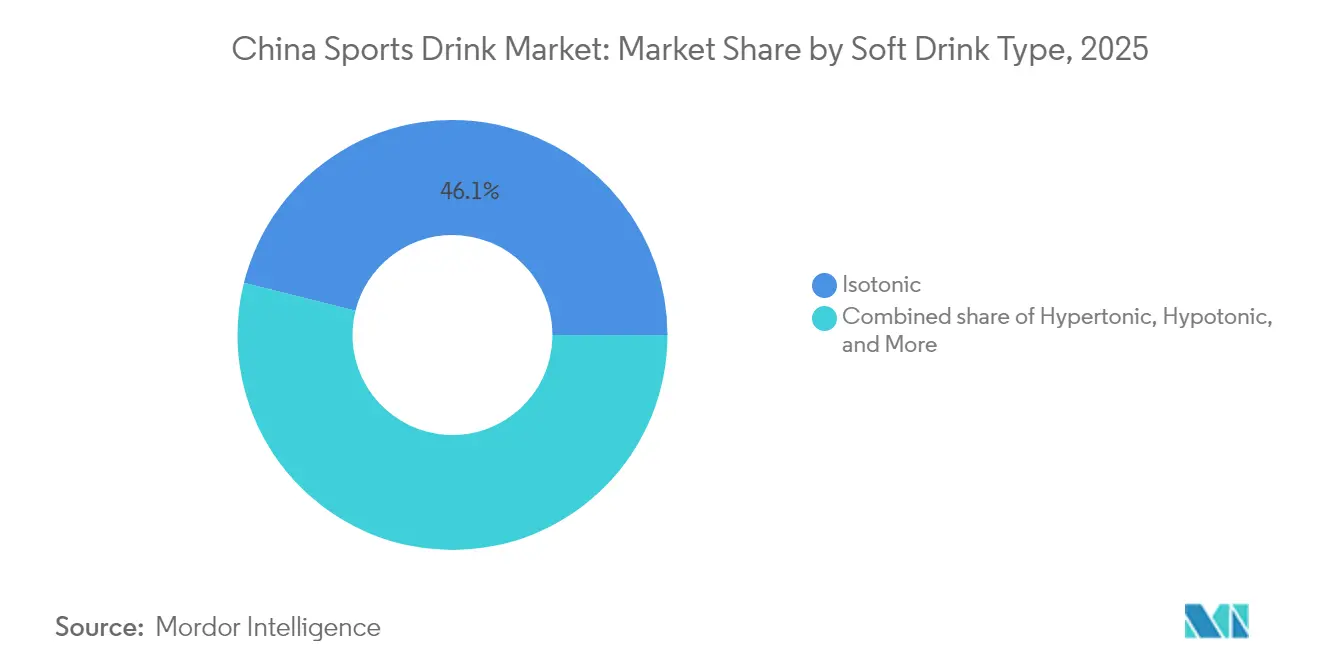

- By soft-drink type, isotonic drinks led with 46.10% revenue share in 2025, while protein-based variants are forecast to expand at a 10.74% CAGR to 2031.

- By packaging, PET bottles accounted for 54.58% of China sports drink market share in 2025, whereas glass bottles are projected to grow at an 11.05% CAGR through 2031.

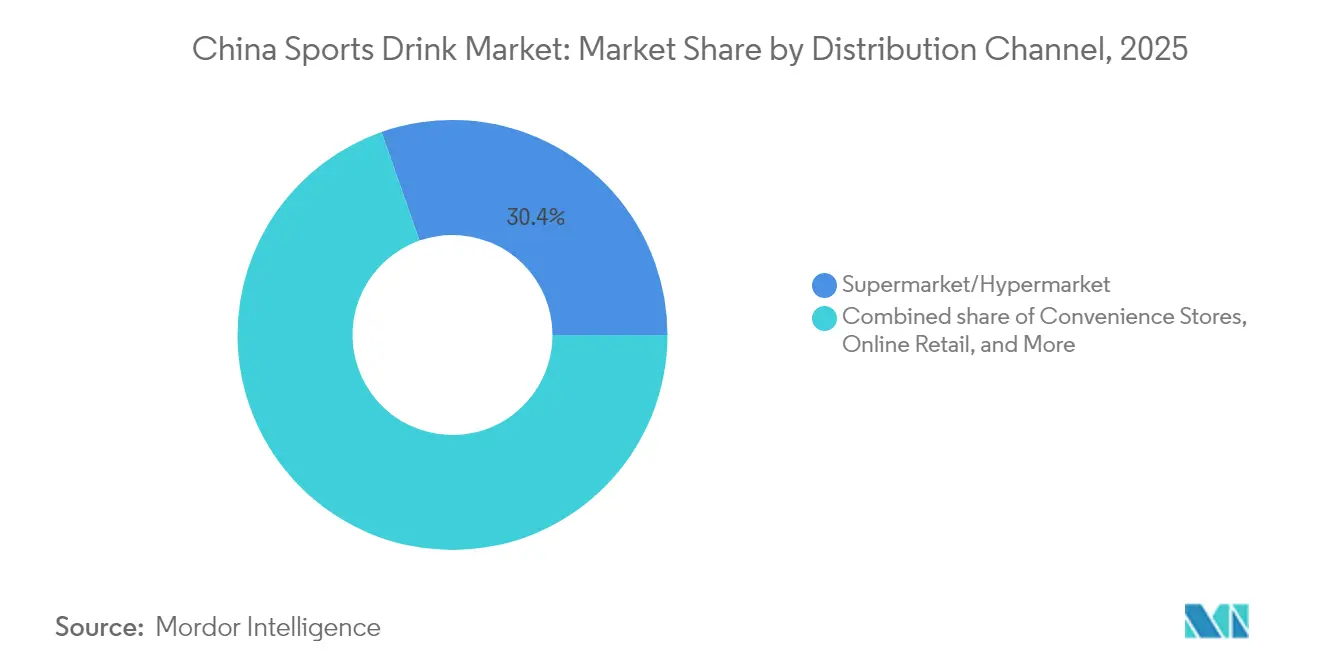

- By distribution channel, supermarkets and hypermarkets held 30.36% share of the China sports drink market size in 2025, and specialty stores are set to post a 10.42% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Sports Drink Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness among consumers | +2.8% | National, with higher intensity in Tier-1 and Tier-2 cities (Beijing, Shanghai, Guangzhou, Shenzhen) | Medium term (2-4 years) |

| Expansion of gym memberships and fitness centers | +2.1% | National, concentrated in urban centers; Pearl River Delta and Yangtze River Delta leading | Medium term (2-4 years) |

| Regional sports culture in southern China | +1.5% | Southern China (Guangdong, Guangxi, Fujian, Hainan) | Long term (≥ 4 years) |

| Product innovation with natural ingredients | +1.9% | National, with early adoption in Tier-1 cities and e-commerce channels | Short term (≤ 2 years) |

| Government sports promotion initiatives | +1.6% | National, with policy enforcement strongest in urban and school settings | Long term (≥ 4 years) |

| Demand for clean-label and functional benefits | +1.4% | National, driven by millennial and Gen Z consumers in urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness Among Consumers

Health-conscious consumption is reshaping demand patterns, with 45% of Chinese consumers engaged in regular physical exercise citing weight management as their primary motivation[1]State General Administration of Sports (China), "Share of population engaged in regular physical exercising in China from 2014 to 2025", sport.gov.cn. This shift in consumer behavior is driving the growing demand for functional beverages, which are increasingly seen as a key component of a healthy lifestyle. Many active individuals now consider specialized nutrition essential for achieving their fitness goals, with nearly one in four reporting an increase in their consumption of sports drinks. This trend extends beyond professional athletes to include casual exercisers and lifestyle-focused individuals, who are prioritizing health objectives such as better sleep, improved exercise routines, and healthier diets. To cater to this demand, brands are enhancing sports drink formulations by incorporating vitamins, minerals, and amino acids, effectively positioning these beverages as everyday wellness products rather than niche athletic supplements. Furthermore, the integration of sports and medical policy frameworks is reinforcing the role of functional hydration in preventive healthcare, driving its adoption across various age groups and solidifying its place in mainstream health and wellness trends.

Expansion of Gym Memberships and Fitness Centers

In 2023, China had 117,000 gyms serving 69.75 million members. However, the fitness sector is undergoing significant changes[2]Shanghai University of Sport, "Number of fitness clubs in China as of 2023, by leading region", eng.sus.edu.cn. Traditional annual memberships are being replaced by more flexible pay-per-use and monthly subscription models. These options make fitness more accessible, particularly for younger and cost-conscious consumers. This shift is also expanding the market for sports drinks, which are now being purchased not only by professional athletes but also by casual gym-goers. Many of these consumers buy beverages directly at gyms or from nearby convenience stores. Fitness centers are increasingly selling functional beverages on-site, creating a profitable retail channel that eliminates the need for traditional distribution networks. Sam's Club China, which operates 48 stores in 2024 and plans to expand to 65 by 2025, offers over 1,000 health and wellness products. Sports drinks are prominently displayed alongside supplements and protein powders, catering to health-conscious customers. Additionally, the growing popularity of digital fitness apps and outdoor activities, such as cycling, running, and winter sports, is driving demand for portable, single-serve beverage formats that suit active lifestyles. Brands are taking advantage of this trend by securing shelf space in gym vending machines and collaborating with fitness chains to create co-branded products. These strategies help capture impulse purchases at the moment of need, further boosting sales.

Product Innovation with Natural Ingredients

The growing consumer demand for transparency and clean labels is accelerating the shift toward natural ingredients in the functional beverage market. Danone's Mizone brand has replaced synthetic colors with natural options like beta-carotene, spirulina, gardenia blue, and purple sweet potato to align with the popular “0 sugar, 0 fat, 0 calories” trend dominating China's functional beverage industry. Similarly, Nongfu Spring is leveraging its natural mineral water sourcing to position its sports drinks as free from artificial additives, a claim that strongly appeals to health-conscious millennials seeking healthier options. Coconut water is gaining popularity as a natural source of electrolytes, while plant-based proteins such as pea and soy are increasingly being used in recovery drinks to cater to the majority of consumers who consider protein the most attractive health claim. The share of new functional beverage launches in China labeled as a "High Protein Source" has surged in 2024, reflecting the rapid pace of innovation and evolving consumer preferences in this market.

Government Sports Promotion Initiatives

State policies are driving the growth of the sports industry. The "Healthy China 2030" initiative encourages youth to engage in two hours of daily physical activity. By 2025, the government aims to increase the percentage of people participating in regular exercise to 38.5%, up from 37.2% in 2023. With the support of 4.8 million sports venues, efforts are underway to raise the per capita sports venue area from 2.89 square meters in 2023 to 3.0 square meters by 2025. The sports industry is also targeting a valuation of CNY 5 trillion by 2025, which is fueling demand for sports nutrition and hydration products. School fitness programs play a key role in introducing sports drinks to younger audiences, who are expected to become the primary consumers over the next decade. Additionally, the promotion of outdoor activities such as cycling, hiking, and winter sports is increasing the need for portable, single-serve products. Brands that align their marketing strategies with government wellness programs and support state-sponsored sporting events not only gain regulatory approval but also secure access to schools and institutions, which are often challenging to reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high sugar content | -1.8% | National, with heightened scrutiny in Tier-1 cities and among younger consumers | Short term (≤ 2 years) |

| Regulatory restrictions on ingredients | -1.3% | National, enforced by SAMR and provincial food safety authorities | Medium term (2-4 years) |

| Competition from traditional beverages | -0.9% | National, strongest in lower-tier cities and rural areas | Long term (≥ 4 years) |

| Supply chain and distribution challenges | -0.7% | Lower-tier cities, rural areas, and western provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over High Sugar Content

As awareness of diabetes and obesity grows, sugar content is becoming a major challenge for brands. Consumers are increasingly demanding low-sugar and sugar-free products. To address this, new nutrition labeling standards, GB 28050-2025, will take effect on March 16, 2027. These standards require brands to disclose sugar, sodium, and energy content and classify "low sugar" as ≤5 grams per 100 milliliters. Brands must reformulate their products to meet these requirements or risk losing shelf space in health-focused retail stores. The Nutri-Grade system, introduced in March 2024 and managed by the Shanghai Center for Disease Control, grades beverages from A to D based on their levels of added sugar, saturated fat, trans fat, and non-sugar sweeteners. For example, 70% of Chagee's tea products have achieved an A or B rating under this system. Younger consumers, who value functional benefits over taste, are increasingly viewing high-sugar sports drinks as unsuitable for their fitness goals. Brands that fail to adapt risk losing market share to competitors like Genki Forest, which has built its reputation on zero-calorie products.

Regulatory Restrictions on Ingredients

As the State Administration for Market Regulation (SAMR) tightens ingredient restrictions, food additive standards and nutrition labeling requirements are being updated. Effective February 8, 2025, GB 2760-2024 imposes combined sweetener limits. This move constrains the formulation flexibility of sugar-free products that typically rely on blends of aspartame, sucralose, and acesulfame potassium[3]United States Department of Agriculture, "China: Usage Standard for Food Additives Finalized", fas.usda.gov. Meanwhile, GB 7718-2025, set to take effect on March 16, 2027, mandates a quantitative ingredient declaration. This requirement compels brands to disclose the precise amounts of electrolytes, vitamins, and amino acids in their products. Such transparency could potentially highlight formulation gaps when compared to premium competitors. In 2024, the China Food Industry Association is set to develop standards for electrolyte beverages. These standards are expected to establish minimum thresholds for sodium, potassium, and magnesium content, elevating the criteria for products aspiring to be recognized as sports drinks. These regulatory changes seem to favor established brands, equipped with R&D resources, enabling them to reformulate and ensure compliance. In contrast, smaller players grapple with heightened testing and certification expenses. Brands that swiftly adapt to these evolving standards stand to benefit. For instance, Danone's Mizone, which preemptively reformulated with natural colors ahead of regulatory mandates, has secured a competitive edge in health-conscious retail channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Soft Drink Type: Isotonic Dominance Meets Protein Surge

In 2025, isotonic formulations captured a 46.10% share of the segment, primarily due to their appeal to active consumers and athletes seeking electrolyte replenishment. Dominating this segment, products like Nongfu Spring's Scream isotonic line and Danone's Mizone+ Electrolyte, boasting 455 milligrams of electrolytes, cater specifically to post-exercise hydration. The electrolyte beverage market has seen a surge, with rapid adoption extending beyond traditional sports to everyday wellness routines. Eastroc's Water Boost, introduced in 2023 and featuring ≥400 milligrams of electrolytes per liter, raked in CNY 1.211 billion (USD 167 million) in the first three quarters of 2024, underscoring the commercial success of its affordable electrolyte strategy. With consumers well-versed in the benefits of electrolytes and the drinks readily available in convenience stores and supermarkets, isotonic beverages have become the go-to choice for casual exercisers.

Forecasted to grow at a 10.74% CAGR from 2026 to 2031, protein-based sports drinks are gaining traction, fueled by a surge in consumer interest in post-exercise recovery and muscle-building nutrition. While dairy proteins like whey and casein are hailed as premium choices—81% of consumers express a preference for whey—plant-based options such as pea and soy protein are carving out a niche, especially among younger, eco-conscious consumers. Mengniu's M-Action line, which ventured into bone, joint, and anti-oxidation SKUs, witnessed a threefold sales surge in H1 FY24, highlighting the lucrative potential of multi-functional protein beverages. While hypertonic and hypotonic drinks cater to niche athletic needs, the broader market gravitates towards isotonic hydration and protein recovery.

By Packaging Type: PET Portability Versus Glass Premiumization

In 2025, PET bottles captured a dominant 54.58% share of the packaging market, thanks to their portability, cost-effectiveness, and seamless integration with high-speed production lines, facilitating mass-market distribution. In a testament to the capital-intensive nature of scaling PET production, Sidel, in 2024, provided C'estbon Beverage with a tailored Combi packaging line, boasting the EvoBlow XL blower, which can handle 12,000 bottles per hour for larger formats. PET's supremacy is further underscored by its alignment with on-the-go consumption trends. Formats like the single-serve 500-milliliter and 330-milliliter bottles dominate sales in convenience stores and vending machines. Brands such as Eastroc and Genki Forest harness PET's cost efficiency to engage in price competition, a strategy especially vital in lower-tier cities where consumers exhibit pronounced price sensitivity, limiting opportunities for premiumization.

From 2026 to 2031, glass bottles are projected to witness a robust growth rate of 11.05% CAGR, driven by urban millennials and Gen Z's increasing preference for premiumization and sustainability. Urban consumers associate glass packaging with superior quality and natural ingredients, a perception that resonates with the prevailing clean-label trend in Tier-1 city retail. Yili's pioneering packaging initiatives, like plant-based caps achieving a 33% carbon footprint reduction, laser-engraved bottles that forgo traditional labels, and labels made from PCR/PIR content boasting a 17.8% carbon reduction, underscore the strategic significance of sustainable packaging. These innovations not only align with evolving environmental regulations but also cater to heightened consumer expectations. With an ambitious target of 99.12% packaging recyclability in 2024, Yili also aims for a significant 17,000-ton cut in petroleum-based plastics, benchmarked against 2019 figures. Furthermore, glass bottles' premium pricing enhances profit margins for brands that emphasize natural sourcing and artisanal craftsmanship.

By Distribution Channel: Supermarket Scale Versus Specialty Focus

In 2025, supermarkets and hypermarkets accounted for 30.36% of the distribution share, using their large scale, refrigeration systems, and promotional strategies to increase sales. Sam's Club China, operating 48 stores as of 2024, offers more than 1,000 health and wellness products, including sports drinks placed alongside supplements and protein powders. Supermarkets attract high customer traffic, encourage impulse purchases, and provide multi-pack options that lower per-unit costs for budget-conscious consumers. Eastroc, with its 3.6 million active retail outlets, including supermarket chains, ensures extensive nationwide coverage and quick product rollouts. Similarly, Nongfu Spring leverages its strong distribution network to secure shelf space for its new sports drink products.

Specialty stores are expected to grow at a CAGR of 10.42% from 2026 to 2031, driven by increasing demand for expert advice, curated product selections, and premium offerings. As of 2024, China has over 1,100 specialty stores in the sports drink market, providing dedicated shelf space for functional beverages, protein powders, and supplements. Herbalife operates more than 3,000 service centers in China, offering personalized nutrition consultations that help boost sales of higher-margin products. Fitness centers are also emerging as key specialty retail channels, selling sports drinks directly to members, capturing impulse purchases, and bypassing traditional distribution methods.

Geography Analysis

In Eastern China, cities like Beijing, Shanghai, and the Yangtze River Delta are at the forefront of driving premiumization and innovation in the sports drink category. Urban consumers here are notably health-conscious, with many exercising weekly and favoring functional benefits over price. E-commerce dominates in these eastern provinces, with platforms like Tmall, JD.com, and Douyin leading the charge in sports nutrition sales. This digital landscape not only facilitates rapid SKU iterations but also paves the way for direct-to-consumer brand launches. In March 2024, the Shanghai Center for Disease Control introduced the Nutri-Grade system, underscoring the region's regulatory leadership and its influence on national compliance standards. Consumers in these markets are increasingly gravitating towards glass bottle formats and protein-based formulations, showing a readiness to pay a premium for natural ingredients and sustainable packaging.

Southern China, with Guangdong province and the Pearl River Delta (home to Guangzhou and Shenzhen), boasts a vibrant sports culture and a climate that drives heightened hydration needs. The region's affinity for basketball, highlighted by the Guangdong Southern Tigers CBA team, and traditions like dragon boat racing, fuel a consistent demand for isotonic and electrolyte beverages. Given the hot, humid subtropical climate, sports drinks have transitioned from being a niche athletic product to a daily wellness staple. Fitness engagement in Guangzhou and Shenzhen surpasses the national average of 37.2%, buoyed by rising disposable incomes and urbanization, leading to increased gym memberships and outdoor sports participation. In a strategic move, Red Bull's TCP Group is channeling a hefty USD 897 million into a Guangxi plant, set to debut in early 2025. This investment not only caters to the southern demand but also eyes exports to ASEAN markets, capitalizing on reduced logistics costs.

While western provinces and lower-tier cities showcase significant growth potential, challenges like supply chain fragmentation and cold chain logistics gaps hinder deeper rural penetration. PepsiCo's strategic USD 180 million investment in a plant in Xi'an, which began trial operations in September 2025, and Red Bull's impressive USD 1.38 billion facility in Sichuan, operational since December 2023 with a capacity of 1.44 billion cans annually, underscore the industry's push to localize production and cater to inland markets, all while slashing transportation costs. Yet, these markets' price sensitivity leans towards mass-market PET bottle formats, curbing premiumization opportunities and emphasizing affordability over functional claims. Distribution hurdles remain, especially with cold chain coverage dipping below 90% in certain western provinces, a stark contrast to the over 97% coverage in coastal areas. This discrepancy poses challenges for maintaining the shelf life and quality of refrigerated sports drinks.

Competitive Landscape

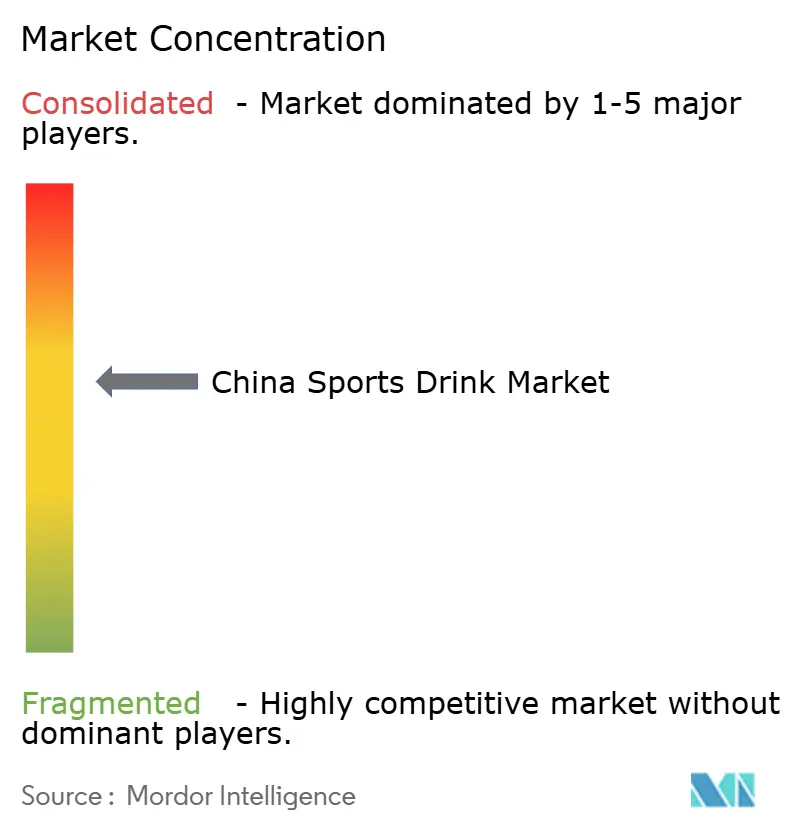

The China sports drink market is moderately consolidated, with a few key domestic and international brands dominating the competition through extensive distribution networks and consistent marketing efforts. These major players, including The Coca-Cola Company, Danone S.A., PepsiCo, Inc., Otsuka Pharmaceutical Co., Ltd., and Nongfu Spring Co., Ltd., have established partnerships with retail chains, gyms, and convenience stores. This allows them to maintain strong visibility in urban and semi-urban areas. Their large-scale operations enable continuous innovation, focusing on functional hydration, electrolyte blends, and low-sugar formulations to meet evolving consumer preferences.

At the same time, regional brands and emerging nutrition-focused companies are gaining attention by catering to niche groups like young athletes and fitness enthusiasts. However, smaller players face challenges such as high marketing expenses and strong brand loyalty among consumers, which slow their expansion efforts.

New disruptors like Genki Forest are leveraging social commerce and live-streaming platforms to bypass traditional retail channels and reach consumers directly. On the other hand, established brands are under pressure from herbal tea competitors, a category worth RMB 60 billion (USD 8.4 billion), led by Wong Lo Kat and JDB. These competitors offer functional health benefits at more affordable prices, creating stiff competition. Technology is playing an increasingly important role in the market. Brands are using tools like QR-code engagement (Eastroc's Water Boost added over 1 million unique QR scans in 2024) and e-commerce analytics to optimize their product offerings and adjust regional pricing strategies effectively.

China Sports Drink Industry Leaders

-

The Coca-Cola Company

-

Danone S.A.

-

PepsiCo, Inc.

-

Otsuka Pharmaceutical Co., Ltd.

-

Nongfu Spring Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: INNOCOCO, under lFBH Limited, officially launched its new sports drink, INNOCOCO electrolyte water. According to the brand, the new products are available in different pack sizes, including 350 ml, 500 ml, 1000 ml and more.

- May 2024: The China Beverage Industry Association (CBIA) approved and released the new group standard "Electrolyte Beverages" (T/CBIA 012-2024). This significant development aims to regulate the production and quality of electrolyte drinks, ensuring safety, consistency, and innovation within the industry.

- June 2023: Danone China has introduced Mizone Electrolyte +, a grapefruit-flavored electrolyte drink, to cater to the growing demand for functional beverages in China. This product is designed for active consumers or those seeking to supplement their electrolyte intake.

China Sports Drink Market Report Scope

China sports drink market is segmented by packaging into PET bottles and cans. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other channels. Other distribution channels include vending machines and pharmacies.

Soft Drink Type

| Electrolyte-Enhanced Water |

| Hypertonic |

| Hypotonic |

| Isotonic |

| Protein-based Sport Drinks |

Packaging Type

| Aseptic packages |

| Glass Bottles |

| Metal Can |

| PET Bottles |

| Others |

Distribution Channel

| Convenience Stores |

| Online Retail |

| Specialty Stores |

| Supermarket/Hypermarket |

| Others |

| Soft Drink Type | Electrolyte-Enhanced Water |

| Hypertonic | |

| Hypotonic | |

| Isotonic | |

| Protein-based Sport Drinks | |

| Packaging Type | Aseptic packages |

| Glass Bottles | |

| Metal Can | |

| PET Bottles | |

| Others | |

| Distribution Channel | Convenience Stores |

| Online Retail | |

| Specialty Stores | |

| Supermarket/Hypermarket | |

| Others |

Key Questions Answered in the Report

How large is the China sports drink market in 2026?

The China sports drink market size is USD 3.61 billion in 2026 and is forecast to reach USD 5.86 billion by 2031.

Which product segment currently leads sales?

Isotonic drinks hold 46.10% of 2025 revenue due to broad consumer familiarity with electrolyte benefits.

Which packaging format is growing fastest?

Glass bottles are projected to expand at an 11.05% CAGR through 2031, supported by premiumization and sustainability trends.

Which sales channel offers the highest growth opportunity?

Specialty sports-nutrition stores are expected to increase at a 10.42% CAGR, driven by demand for expert guidance and curated assortments.

Page last updated on: