Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

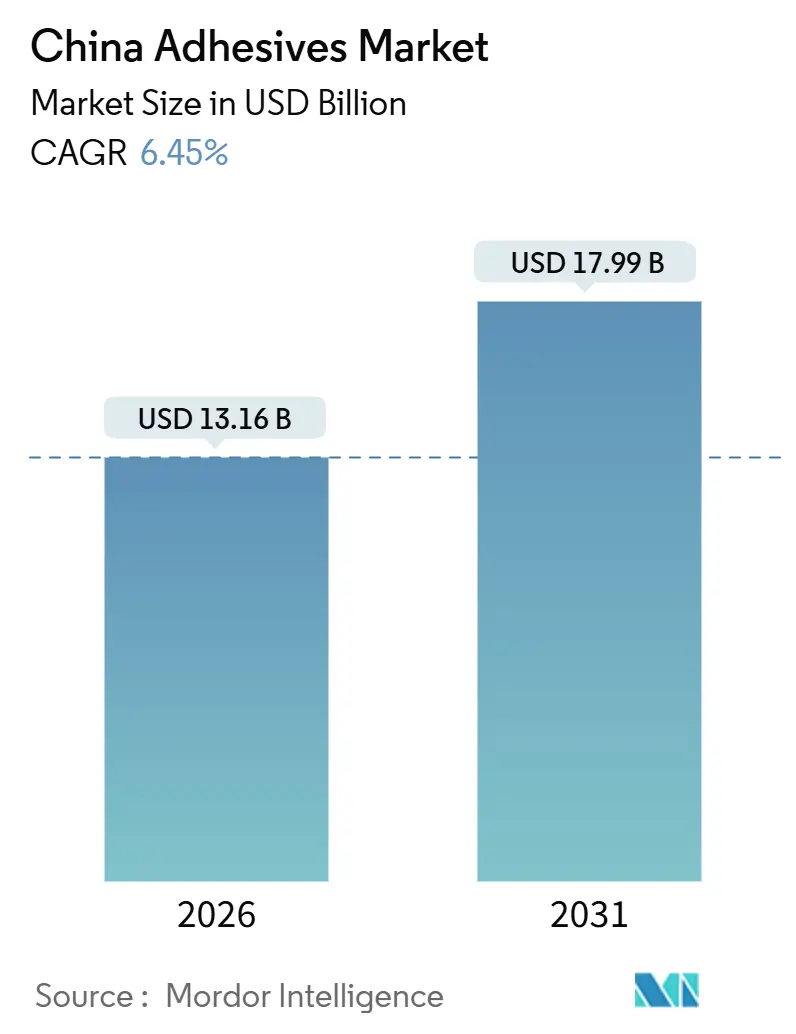

| Market Size (2026) | USD 13.16 Billion |

| Market Size (2031) | USD 17.99 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Adhesives Market Analysis by Mordor Intelligence

The China Adhesives Market size is estimated at USD 13.16 billion in 2026, and is expected to reach USD 17.99 billion by 2031, at a CAGR of 6.45% during the forecast period (2026-2031). Robust e-commerce logistics, surging electric-vehicle battery assembly, and sustained infrastructure modernization underpin this growth trajectory, each requiring specialized chemistries that outpace legacy solvent-borne systems. Acrylic formulations dominate label, construction, and packaging jobs, while water-borne platforms strengthen as GB 33372-2020 emission caps tighten, limiting solvents below 50 grams per liter. At the same time, reactive technologies gain momentum inside smart factories because their fast cures synchronize with robotic dispensing lines. Multinational producers add local capacity to secure volatile feedstock and to meet tighter VOC quotas, but local specialists leverage cluster proximity and competitive pricing to defend share.

Key Report Takeaways

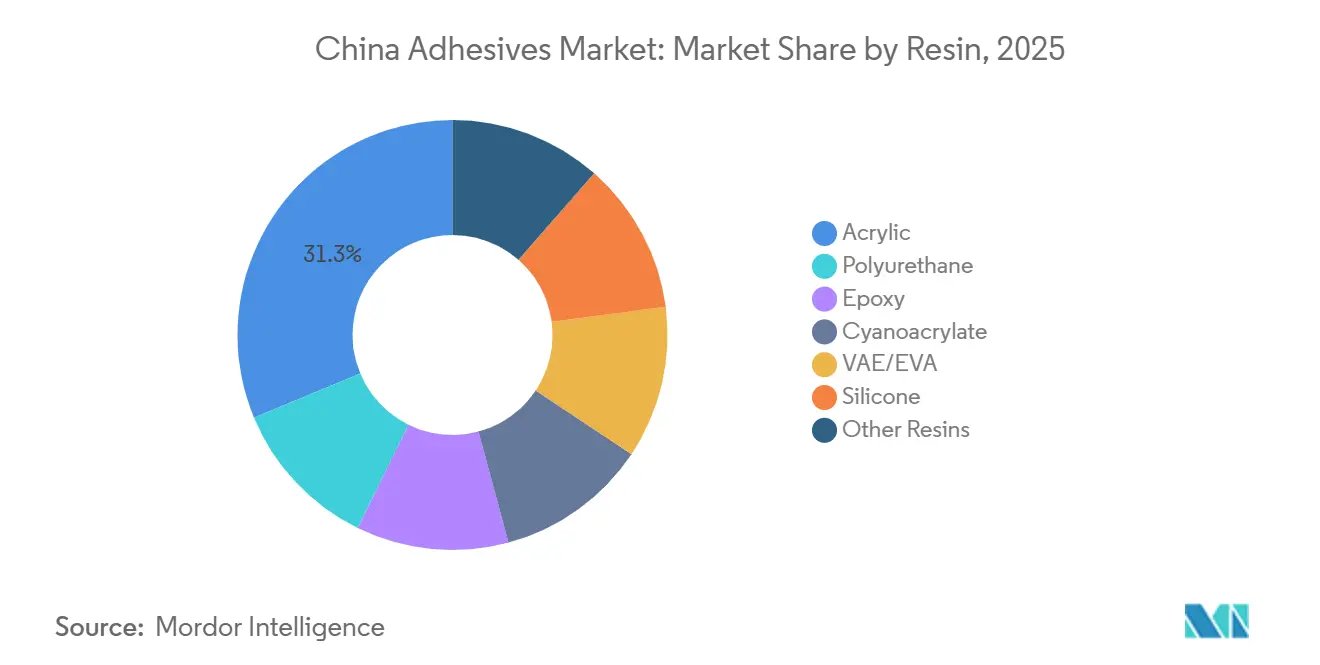

- By resin, acrylic captured 31.28% of China adhesives market share in 2025, while polyurethane is forecast to post the fastest 6.74% CAGR through 2031.

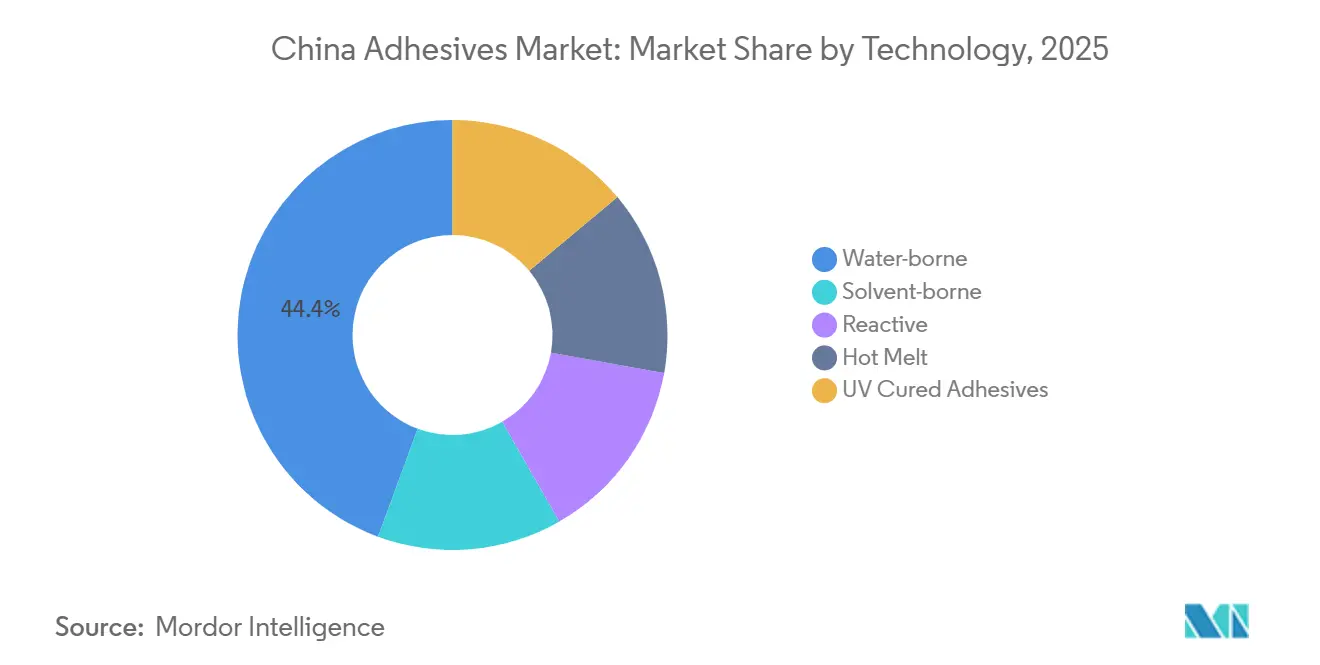

- By technology, water-borne held 44.36% of China adhesives market size in 2025, whereas reactive is set to expand at 6.81% CAGR to 2031.

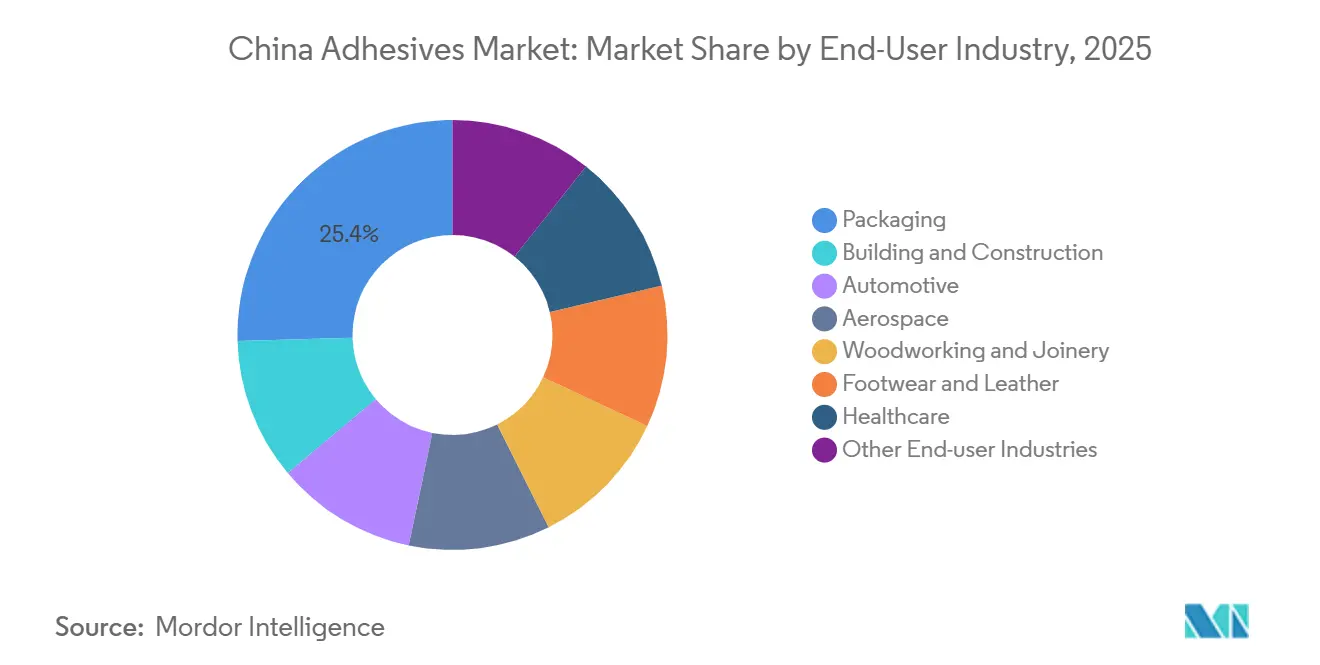

- By end-user industry, packaging led with 25.44% revenue share in 2025, although automotive is projected to advance at a 6.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce-Driven Packaging Boom | +1.2% | National, with concentration in Eastern logistics hubs (Shanghai, Hangzhou, Shenzhen) | Short term (≤ 2 years) |

| Electric-Vehicle Manufacturing Surge | +1.5% | National, with early gains in Guangdong, Jiangsu, Shanghai battery clusters | Medium term (2-4 years) |

| Infrastructure and Urbanization Push | +0.9% | Beijing-Tianjin-Hebei, Yangtze River Delta, Pearl River Delta, Western corridor cities | Long term (≥ 4 years) |

| Regulatory Pivot to Eco-Friendly Chemistries | +1.0% | National, stricter enforcement in Tier-1 cities (Beijing, Shanghai, Guangzhou) | Medium term (2-4 years) |

| Smart-Factory Demand for Automation-Ready Reactive Adhesives | +0.8% | Eastern manufacturing zones (Jiangsu, Zhejiang), Southern export hubs (Guangdong) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Driven Packaging Boom

China processed 122.5 billion parcels in 2025, a scale that cements packaging as the largest end-use share within the China adhesives market[1]China Postal Service, “Annual Express Parcel Statistics 2025,” chinapost.gov.cn . Label output rose to 9.98 billion m², and RFID inlay sales touched 39 billion units, creating heavy pull for acrylic-emulsion pressure-sensitives able to survive automated applicators and temperature swings. Water-based hot-melts gain preference because e-commerce firms impose bio-content mandates to satisfy corporate sustainability goals. The boom also invites volume rebates that squeeze converter margins, forcing suppliers to scale or differentiate. As a result, innovation centers shift toward low-temperature, fully recyclable formulations that keep pace with just-in-time logistics.

Electric-Vehicle Manufacturing Surge

New-energy-vehicle shipments closed 2024 at 12 million units, while CATL alone targeted 750 GWh of cell capacity by 2025, both of which inflate demand for thermally conductive, flame-retardant adhesives qualified to UL94 V0. Polyurethane systems thrive because they bond aluminum housings and match lithium-ion battery thermal profiles, pushing their CAGR to 6.74% through 2031. Domestic suppliers launched bio-based TPU grades that cut life-cycle carbon by roughly 20% without sacrificing peel strength. As European CBAM tariffs loom, automakers bring adhesive qualification cycles below 18 months, rewarding vendors with in-country pilot lines and full traceability.

Infrastructure and Urbanization Push

The State Council set a CNY 300 billion target for green building materials by 2026, channeling volume to low-VOC sealants and structural glazing compounds. Prefabrication policies require 30% of new builds to be factory-made, shifting bonding tasks from construction sites to panel plants. Water-borne acrylics cure at ambient temperatures, sidestepping flammability and OSHA-style hazards. Although real-estate investment slid 10% in 2024, public transit, high-speed rail, and renewable installations fill part of the gap. Suppliers with automated dosing and on-line QC gain an edge as panel makers lock multi-year sourcing deals.

Regulatory Pivot to Eco-Friendly Chemistries

GB 33372-2020 sliced allowable VOCs to 50 g/L for interior products, driving water-borne adhesives to 44.36% of the China adhesives market in 2025. Shanghai and Guangzhou impose even lower thresholds, accelerating solvent-free polyurethane adoption in footwear clusters that ship to Europe and North America. GB 18580 tightened formaldehyde ceilings in wood bonding, pushing urea-formaldehyde producers either to re-engineer or exit. Compliance spending, often 5-8% of revenue, favors multinational plants with large amortization bases. Local champions counter by scaling bio-feedstocks and courting provincial subsidies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock Price Volatility | -0.7% | National, with acute impact on coastal petrochemical clusters (Zhanjiang, Ningbo) | Short term (≤ 2 years) |

| Stringent VOC and HAP Compliance Costs | -0.5% | National, stricter enforcement in Tier-1 cities and export-oriented zones | Medium term (2-4 years) |

| Prefab-Construction Shift to Mechanical Fasteners | -0.3% | Beijing-Tianjin-Hebei, Yangtze River Delta, Pearl River Delta prefab zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

First-half 2025 data showed toluene di-isocyanate at CNY 12,131/ton, down 21.96%, while epoxy rose 7.56% to CNY 13,790/ton, creating cost divergence for polyurethane and epoxy formulators. New butyl-acrylate lines from Wanhua and BASF suppressed acrylic prices, but downstream real-estate demand lagged. Vertically integrated majors protected margins; smaller converters endured 15-20% swings, triggering quarterly price resets. Anti-dumping probes on epoxy exports further squeezed domestic availability, nudging some users toward acrylic or polyurethane substitutes where they meet specs.

Stringent VOC and HAP Compliance Costs

Meeting GB 33372-2020 limits forces mid-tier plants to invest 5-8% of annual revenue in scrubbers, monitoring kits, and reformulation trials. Onsite bans push panel factories to ventilate and install solvent-recovery, adding capex. In tall prefab projects, seismic codes favor bolted steel frames, cutting adhesive volume by 3-5% each year in some structural tasks[2]Ministry of Housing and Urban-Rural Development, “Prefab Building Code,” mohurd.gov.cn . Footwear exporters pivot to solvent-free systems to avoid green-tariff penalties, but SMEs face learning curves and payback delays, slowing broad adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Acrylic Dominance Anchors Packaging and Construction

Acrylics held 31.28% of China adhesives market share in 2025, reflecting balanced tack, UV resistance, and wide compatibility. Polyurethane’s 6.74% CAGR stems from EV battery bonding and solvent-free footwear lines that satisfy export audits. Local firms expand bio-based TPU and polyester polyols, trimming lifecycle emissions by roughly one-fifth. Epoxies serve aerospace and wind blades yet face feedstock cost pressure that accelerates use of acrylic-modified variants. Silicones rise in photovoltaic modules as China reached 1,200 GW of combined solar and wind capacity in 2024, six years early.

Demand clusters matter. Coastal converters benefit from butyl-acrylate and HDI plants in Zhanjiang and Yantai, shortening inbound logistics and stabilizing totals. Inland sites pay premiums and hedge with multi-resin portfolios. Regulatory headwinds push phenol-formaldehyde and styrene-butadiene niches to rethink formulations or exit. Whether acrylic sustains its lead through 2031 depends on how rapidly polyurethane addresses cost gaps and how fast silicone and cyanoacrylate penetrate high-value electronics and medical devices.

By Technology: Water-Borne Leadership Reflects Regulatory Momentum

Water-borne chemistries commanded 44.36% of China adhesives market size in 2025 thanks to VOC caps and easier plant permitting. Solvent-borne lines decline as footwear hubs adopt emission-free polyurethane systems to maintain export status. Reactive technologies, however, are the performance frontier, registering a 6.81% CAGR because their instant cure keeps pace with robot lines and battery plants. Hot-melts thrive in carton sealing and e-commerce handle wraps, yet face pressure from pressure-sensitive grades that support variable data labels.

Hybrid water-borne-reactive designs emerge from the EUR 60 million Henkel Inspiration Center opened in Shanghai in 2025, merging low-VOC with fast set for automotive interiors. UV-cured grades stay niche due to lamp capital costs but capture mini-electronics with zero heat load. Over the outlook horizon, technology mix will fragment: cost-sensitive high-volume tasks stay water-borne, whereas high-margin automation-ready segments adopt reactive or UV systems.

By End-User Industry: Packaging Scale Meets Automotive Momentum

Packaging absorbed 25.44% of total volume in 2025 as 122.5 billion parcels demanded labels, tapes, and recyclable seals. The China adhesives market size tied to packaging therefore remains resilient, though rebates pressure margins. Automotive bonding grows at 6.92% CAGR as battery packs require gap fillers above 2 W/m-K and flame-retardant structural lines. Construction trends hinge on green material quotas; while real-estate was soft in 2024, public infrastructure still channels steady demand.

Footwear lines in Guangdong and Fujian switched to solvent-free polyurethane, lifting raw material cost but meeting EU audit rules. Healthcare bonding accelerates with an aging population of 280 million citizens aged 60-plus, driving cyanoacrylate tissue glue and gentle-skin tapes. Aerospace gains volume via COMAC programs that localize epoxy film adhesives. Across end uses, segment winners will be those that align cure speed, sustainability, and cost with sector-specific assembly logic.

Geography Analysis

Eastern provinces—Jiangsu, Zhejiang, and Shanghai—anchor more than one-third of China adhesives market demand because they host automotive, electronics, and packaging clusters backed by BASF’s Caojing resin line and Henkel’s Shanghai Inspiration Center. Yangtze River Delta prefabrication targets intensify water-borne sealant consumption, while 700-plus digital presses fuel pressure-sensitive labels. Southern zones—Guangdong and Fujian—lead footwear and RFID inlays, leaning on local butyl-acrylate from BASF’s 400,000-ton Zhanjiang plant commissioned in 2025.

Western corridors—Chongqing, Chengdu, Xi’an—capture share through high-speed rail and renewable projects tied to the CNY 300 billion green-building directive. Nevertheless, procurement cycles run long and real-estate softness temper numbers. BTH region focuses on elevator retrofits and low-VOC glazing due to stricter municipal codes, supporting suppliers of construction sealants. Inland formulators lacking feedstock integration pay volatility premiums, driving clustering along coastal petrochemical parks.

Photovoltaic-module output in Jiangsu and Zhejiang leverages local silicone lines to meet 25-year outdoor durability. Multisite majors hedge logistics and provincial regulatory differences by operating plants in both south and east, but coordination complexity rises. Looking forward, regional policy incentives—especially around green credit and carbon trading—will shape the distribution of China adhesives market growth through 2031.

Competitive Landscape

The China adhesives market shows low concentration. Global majors - Henkel and Sika - collectively hold about 35-40% through technical service depth, broad portfolios, and vertically integrated feedstocks. Domestic leaders - Beijing Comens New Materials Co., Ltd. and Hubei Huitian - capture in commodity and cluster-served niches. BASF secured raw-material chain control by adding 400,000 tpa butyl-acrylate in Zhanjiang in 2025 and lifting Caojing dispersion capacity to 18,800 tpa. Wanhua doubled HDI to 40,000 tpa and unveiled bio-based TPU in 2024, positioning for EV and sustainable footwear lines.

Henkel opened its EUR 60 million Inspiration Center in 2025 to co-develop hybrid low-VOC chemistries with Chinese OEMs. Smaller firms such as Hubei Huitian recorded CNY 3.989 billion revenue in 2024 and launched 48 products focused on silicone solar sealants and polyurethane construction lines. Competitive focus now shifts to UV-cured electronics grades, medical tissue glues, and debond-on-demand systems for battery recycling. Patent races and localized supply chains will define pricing power as regulatory overhead grows.

China Adhesives Industry Leaders

H.B. Fuller Company

Henkel AG & Co. KGaA

Hubei Huitian New Materials Co. Ltd

Sika AG

Beijing Comens New Materials Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: BASF commenced commercial production at its 400,000 tpa butyl-acrylate unit in Zhanjiang. This development ensures a stable feedstock supply for acrylic emulsions, which are widely used in the adhesives market.

- May 2025: Shandong ADINO New Materials Co., Ltd. launched operations in Tancheng County, Linyi. The company, a joint venture between China’s Guangdong Zhenghe Adhesive Materials Co., Ltd. and Germany’s ADINO Group, signifies a new phase of Sino-German collaboration in high-performance hot melt adhesives.

China Adhesives Market Report Scope

Adhesives are substances, such as glues or cements, that bond materials through surface attachment. They hold materials together and resist separation through chemical or physical interactions. Adhesives provide advantages over mechanical fasteners, including better stress distribution and compatibility with various materials such as wood, metal, and plastic.

The China adhesives market is segmented by resin, technology, end-user industry, and geography. By resin, the market is segmented into acrylic, polyurethane, epoxy, cyanoacrylate, VAE/EVA, silicone, and other resins. By technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV cured adhesives. By end-user industry, the market is segmented into packaging, building and construction, automotive, aerospace, woodworking and joinery, footwear and leather, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin

| Acrylic |

| Polyurethane |

| Epoxy |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By End-User Industry

| Packaging |

| Building and Construction |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear and Leather |

| Healthcare |

| Other End-user Industries |

| By Resin | Acrylic |

| Polyurethane | |

| Epoxy | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By End-User Industry | Packaging |

| Building and Construction | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear and Leather | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms