Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

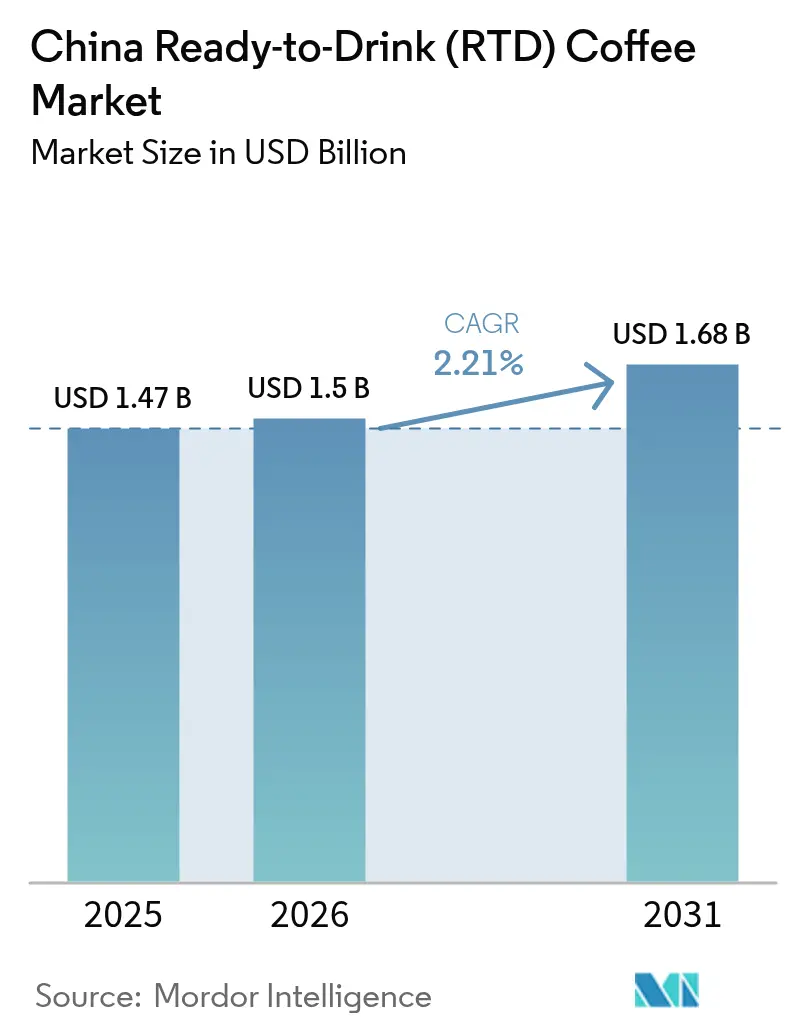

| Base Year Market Size (2025) | USD 1.47 Billion |

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 1.68 Billion |

| Growth Rate (2026 - 2031) | 2.21% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Ready-to-Drink (RTD) Coffee Market Analysis by Mordor Intelligence

The China ready-to-drink (RTD) coffee market size is expected to grow from USD 1.47 billion in 2025 to USD 1.5 billion in 2026 and is forecast to reach USD 1.68 billion by 2031 at 2.21% CAGR over 2026-2031. The market expansion is driven by increasing urban disposable incomes and the widespread adoption of digital payment platforms like WeChat and Alipay, which simplify purchase transactions. Consumer preferences are shifting from international premium brands to affordable local alternatives, indicating evolving value-conscious purchasing behavior. This transition to domestic brands highlights a market transformation as Chinese consumers choose cost-effective, locally-adapted coffee products that align with regional tastes and cultural preferences. The market benefits from the established café culture in major cities like Shanghai and Beijing, where coffee has become part of daily consumption patterns. Generation Z's preference for cold brew varieties has created new market opportunities. Additionally, technology-driven store expansions have improved operational efficiency through automated ordering and inventory management systems, reducing franchisee investment recovery periods. However, the market faces challenges including increased production costs due to rising Vietnamese arabica coffee prices, growing consumer and regulatory concerns about beverage sugar content and health effects, and competition with established tea brands for retail shelf space in traditional and modern outlets.

Key Report Takeaways

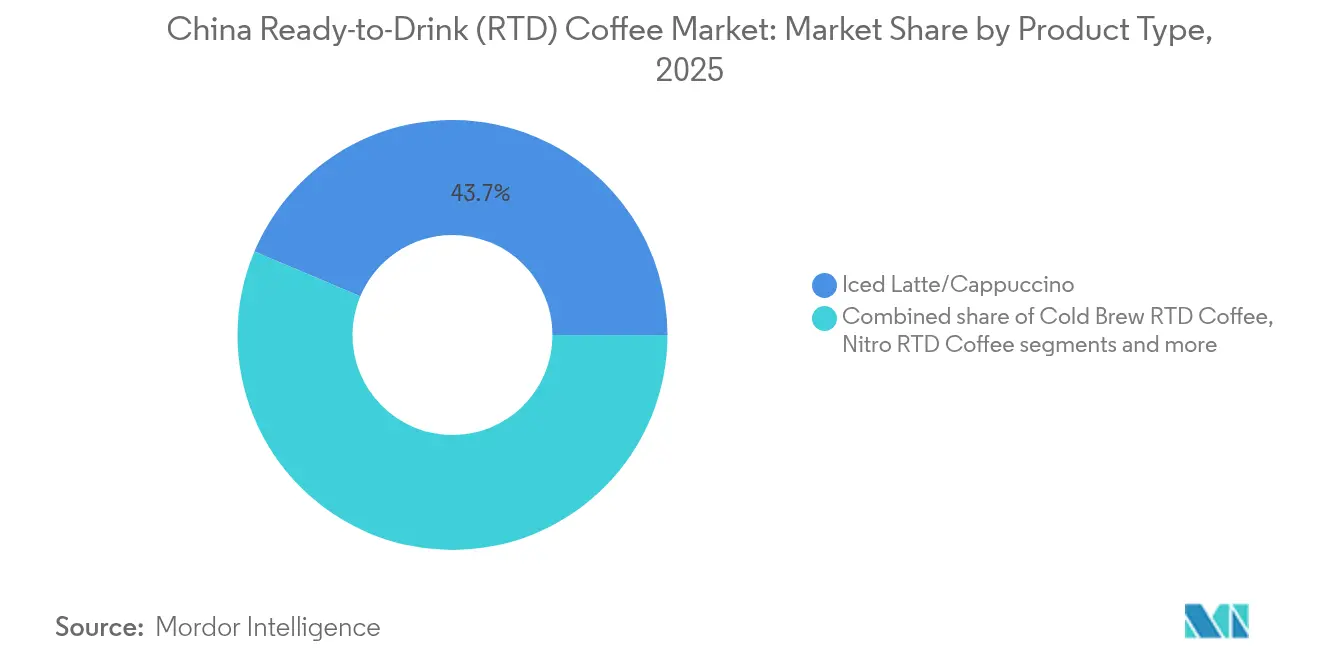

- By product type, iced latte/cappuccino held 43.65% of China RTD coffee market size in 2025; cold brew is expanding at a 4.26% CAGR.

- By ingredient, dairy-based commanded 71.40% share of China RTD coffee market size in 2025; plant-based milk usage is climbing at a 6.45% CAGR.

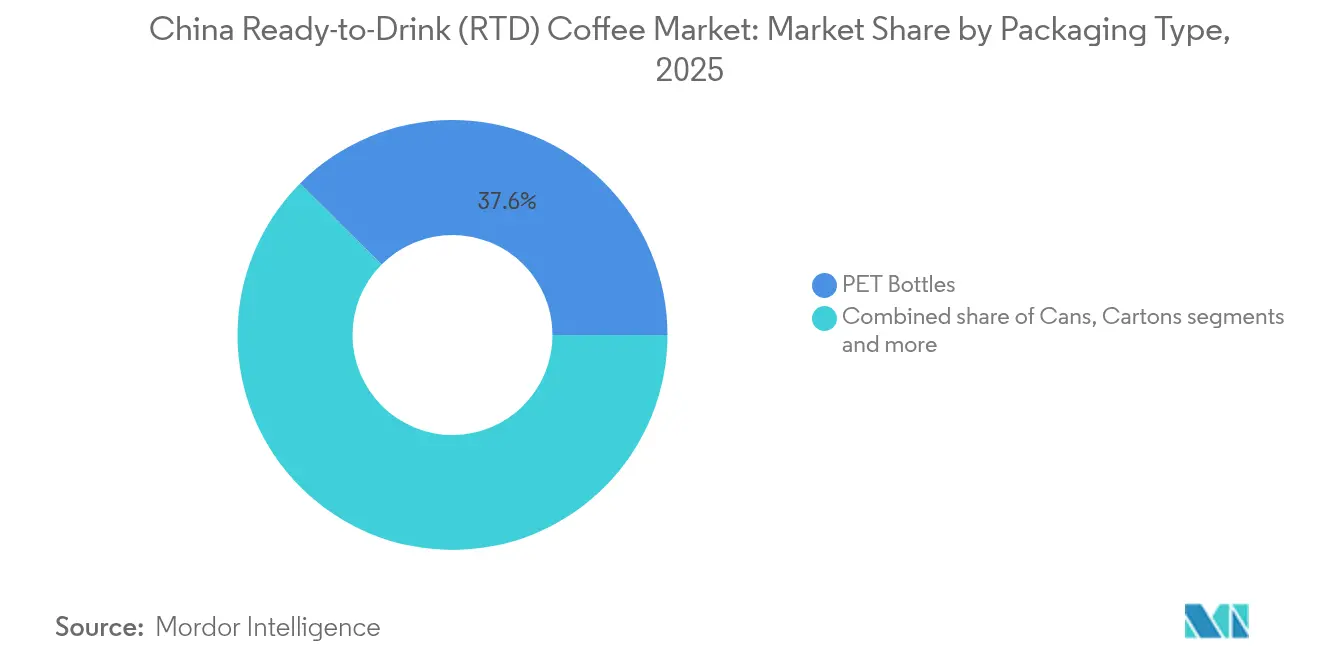

- By packaging, PET bottles captured 37.55% of the China RTD coffee market in 2025, while cartons are advancing at a 4.18% CAGR.

- By price positioning, the mass segment controlled 79.20% of China RTD coffee market share in 2025, whereas premium lines are growing at a 5.95% CAGR.

- By distribution channel, convenience and grocery stores delivered 36.70% of 2025 sales, yet online retail is scaling at a 6.15% CAGR.

- By flavor profile, plain/classic captured 60.40% of the China RTD coffee market in 2025, while flavored are advancing at a 6.34% CAGR.

- By region, East China led with 42.70% of China RTD coffee market share in 2025; Central and Western China is projected to pace the market at a 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Ready-to-Drink (RTD) Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience and on-the-go consumption on the rise | +0.8% | East China and South China, spill-over to Central regions | Short term (≤ 2 years) |

| Health trends spotting in rtd coffee beverages | +0.6% | Global, with early gains in Beijing, Shanghai, Guangzhou | Medium term (2-4 years) |

| Augmented expenditure on advertising and promotional activities | +0.4% | National, concentrated in Tier 1 and 2 cities | Short term (≤ 2 years) |

| Product innovation experiences notable surge | +0.5% | East China core, expansion to North and Central regions | Medium term (2-4 years) |

| Expansion of retail channels | +0.3% | National, accelerated in lower-tier cities | Long term (≥ 4 years) |

| Influence of western coffee culture and young professionals | +0.2% | East China and North China, limited rural penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience and on-the-go consumption on the rise

The adoption of RTD coffee in China is driven by evolving urban mobility patterns and increasingly demanding work schedules, as professionals in major cities seek efficient and convenient energy solutions in their fast-paced lifestyles [1]CoBank Knowledge Exchange, “China’s Coffee Consumption Jumps as Urban Workers Embrace On-the-Go Formats,” cobank.com. Luckin Coffee's mobile application enables customers to pick up orders or receive delivery within 30 minutes in major cities, streamlining the beverage purchasing process and addressing the time constraints of urban consumers. This convenience is particularly important in megacities like Shanghai and Beijing, where daily commute times often exceed 90 minutes and work schedules extend into late hours. Professionals frequently purchase chilled coffee drinks at metro stations during their commutes or store multiple bottles in office refrigerators throughout the day, establishing RTD coffee as a practical energy source for sustained productivity in high-pressure work environments. This fundamental shift in consumption behavior differs significantly from traditional tea drinking habits, which typically involve careful preparation, specific brewing temperatures, and communal sharing.

Health trends spotting in RTD coffee beverages

The market shows increasing demand for functional coffee products, including blood-orange coffee, tart-cherry coffee, and protein-enriched beverages, which cater to health-conscious consumers seeking nutritional benefits in their daily coffee consumption. These innovative formulations combine traditional coffee attributes with enhanced functional properties, addressing specific wellness needs. According to the ASEAN Food and Beverage Alliance, more than 80% of Asian consumers in 2024 are willing to purchase reformulated products that maintain taste while reducing sugar, salt, and fat content [2]ASEAN Food and Beverage Alliance Secretariat, “Reformulation Acceptance Survey 2024,” aseanfba.org.This health-conscious trend encompasses both modified ingredients and the incorporation of protein fortification and plant-based milk alternatives, reflecting a broader shift toward healthier beverage options in the coffee industry. The integration of functional ingredients and alternative formulations demonstrates the market's adaptation to evolving consumer preferences for wellness-oriented coffee products, with manufacturers focusing on developing products that deliver both taste satisfaction and health benefits.

Augmented expenditure on advertising and promotional activities

The coffee market's competitive landscape has driven increased marketing expenditure as companies vie for consumer attention across multiple channels, including television, digital platforms, and retail environments. Digital marketing strategies have evolved significantly to focus on comprehensive product launches and dedicated marketing budgets, incorporating data analytics and consumer behavior insights. Co-branding initiatives serve as additional growth channels to expand market reach and create unique value propositions for consumers. Companies have widely adopted celebrity endorsements and strategic social media presence across influential platforms like Weibo and Xiaohongshu to connect with younger, digitally-savvy consumers who prioritize authentic brand experiences. Nestlé's Nescafé ready-to-drink (RTD) coffee in China demonstrates this multi-channel approach through its strategic partnership with Yu Shuxin (Esther Yu) as brand ambassador, featuring her in television commercials and digital campaigns for their new silky flavor variant. This heightened promotional activity indicates a maturing market where brand distinction requires comprehensive marketing strategies beyond product quality and price competitiveness, including targeted digital campaigns, influencer partnerships, integrated marketing communications, and continuous consumer engagement across all platforms.

Product innovation experiences notable surge

RTD coffee product development is expanding as companies focus on unique flavors and functional benefits for differentiation. In April 2024, Nestlé introduced six new products, including Orange C Americano and China's first coffee fruit tea, addressing consumer demand for diverse taste experiences.The company's strategic product launches demonstrate its commitment to capturing market share through innovative flavor combinations and novel beverage formats. Cold Brew RTD Coffee continues to grow due to younger consumers preferring its smoother, less acidic profile, with many brands incorporating premium ingredients and specialized brewing techniques. Companies are also innovating in packaging design to improve sustainability and extend product shelf life, implementing recyclable materials and advanced preservation technologies. This emphasis on new product development reflects the understanding that innovation drives repeat purchases in a market with limited consumer loyalty, as companies strive to maintain competitive advantage through continuous product enhancement and market responsiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High amount of HFSS sugar limiting iced coffee growth | -0.3% | National, stricter enforcement in Tier 1 cities | Medium term (2-4 years) |

| Coffee bean cost volatility | -0.4% | National, Global supply chain impact, affecting all regions | Short term (≤ 2 years) |

| RTD coffee faces stiff competition for shelf space from emerging alternatives | -0.2% | National, intensified in convenience store channels | Long term (≥ 4 years) |

| Caffeine concerns curbing RTD coffee | -0.1% | Urban areas with health-conscious demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High amount of HFSS sugar limiting iced coffee growth

Regulatory oversight of high fat, salt, and sugar (HFSS) content in beverages significantly impacts RTD coffee formulations and marketing approaches. The 2024 pre-packaged labeling requirements mandate comprehensive ingredient disclosure and detailed origin information, which may substantially influence consumer purchasing decisions regarding high-sugar RTD coffee products. Major beverage manufacturers, including Coca-Cola and PepsiCo, are actively reformulating their product portfolios with reduced sugar content to align with increasing consumer demand for healthier alternatives. The stringent regulatory environment accelerates research and development in natural sweeteners and functional ingredients, focusing on alternatives like stevia, monk fruit, and other plant-based sweeteners. However, the extensive product reformulation processes, ingredient substitution costs, and research investments in alternative sweetening solutions may temporarily impact profit margins across the RTD coffee segment. Additionally, manufacturers must navigate complex regulatory compliance requirements while maintaining product taste profiles that meet consumer expectations, further adding to operational complexities and development timelines.

Coffee bean cost volatility

Coffee supply chain disruptions globally are creating significant pricing pressures that affect RTD coffee profitability and market accessibility across regions. Vietnamese coffee prices reached unprecedented 50-year highs of VND 131,000 (USD 5.1) per kilogram in February 2025, due to severe climate change impacts including drought conditions and irregular rainfall patterns, combined with persistent supply chain disruptions in transportation and labor availability [3]Vietnam Plus, "Coffee prices hit record highs, heightening speculation risks", vietnamplus.vn. These mounting cost pressures particularly affect premium RTD coffee segments that depend on high-quality arabica beans from specific growing regions, forcing brands to either reduce their profit margins substantially or increase consumer prices in various markets. Companies are implementing comprehensive supply chain diversification strategies, including sourcing from multiple origins and establishing forward contracting agreements with multiple suppliers, to maintain competitive pricing amid increasing market volatility and uncertainty in the global coffee trade. The impact extends beyond immediate pricing concerns, affecting production schedules, inventory management, and long-term sustainability initiatives within the RTD coffee industry. Manufacturers are also investing in advanced forecasting tools and strengthening relationships with local farming communities to ensure stable supply chains and mitigate future disruption risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Iced Latte Leads While Cold Brew Accelerates

Iced latte and cappuccino products hold a 43.65% market share in 2025, driven by consumer preferences for milk-based beverages across supermarkets, convenience stores, and specialty coffee shops. Consumer preferences are moving from traditional dairy-based sweetened beverages to fruit-infused varieties, reflecting trends toward complex flavor profiles and health-conscious consumption. The adoption of micro-foam technology in ready-to-drink coffee products at convenience stores shows product differentiation efforts, as manufacturers invest in packaging and processing techniques to create café-quality beverages. These innovations increase competition in the premium ready-to-drink coffee segment, supporting product development and market growth.

Cold brew coffee grows at a CAGR of 4.26%, attracting urban consumers through its smooth flavor profile, lower acidity, and premium quality positioning. This segment resonates with millennials and Gen Z consumers seeking new coffee experiences. Nitro coffee, despite its small market presence, generates sales through vending channels and specialty coffee shops, with major chains expanding their offerings. The protein-enriched coffee segment targets fitness enthusiasts through digital platforms, with manufacturers developing specialized formulations for post-workout recovery and collaborating with fitness influencers.

By Flavor Profile: Milk Flavor Dominates While Flavored Segments Surge

In 2025, milk-based flavor profiles dominate the market with a 60.40% share, underscoring the strong inclination of Chinese consumers towards creamy coffee experiences. These experiences seamlessly meld the nation's traditional tea culture with the burgeoning Western coffee trend. The widespread adoption of milk-based coffee reflects the success of brands in educating the market and positioning milk coffee as a familiar and approachable entry point for tea drinkers transitioning to coffee consumption. By leveraging the comfort and familiarity associated with milk, brands have effectively bridged the gap between traditional and modern beverage preferences. This preference for milk not only highlights a shift in coffee consumption but also resonates with broader Asian beverage trends, where dairy additions are seen as both comforting and nutritionally beneficial.

Flavored segments are on a growth trajectory, accelerating at a 6.34% CAGR through 2031. This surge is largely attributed to innovative product launches that resonate with local tastes and seasonal nuances. For instance, Kudi Coffee has rolled out culturally-relevant offerings like the Ejiao Latte, melding traditional Chinese ingredients with contemporary coffee styles. Meanwhile, Luckin Coffee's partnership with Moutai birthed alcohol-infused coffee variants, which were met with overwhelming enthusiasm, selling over 5.4 million cups on their debut day. Such flavor innovations underscore a pivotal realization among brands: in a landscape where price competition is fierce, distinct taste differentiation is key to driving both trial and repeat purchases. While plain and classic profiles still hold sway among purists, their market share is waning as flavor experimentation takes center stage in consumer preferences.

By Ingredient Base: Dairy Leads While Plant-Based Accelerates

In 2025, dairy dominated production, accounting for 71.40% of the total output. This dominance is supported by well-established supply chains and a consumer base that is increasingly aware of the health benefits of calcium. The strong presence of dairy reflects traditional consumer preferences, which have been shaped over decades, and the efficiency of established manufacturing processes. Dairy's role in various food and beverage applications further solidifies its position as a staple ingredient in the market. The continued reliance on dairy ingredients highlights the industry's ability to adapt to evolving consumer demands while maintaining its foundational strengths.

Plant-based milk alternatives have transitioned from niche products to mainstream options, achieving a notable 6.45% CAGR. Oat milk leads this segment, favored for its neutral taste and lower environmental impact, particularly in terms of reduced carbon emissions and water usage. Soy milk remains popular among protein-conscious consumers, while almond milk appeals to health-focused demographics seeking nutritious options. Manufacturers are also leveraging coconut cream to introduce tropical flavors in seasonal offerings, especially summer beverages. This diversification within the plant-based segment reflects the growing consumer demand for sustainable and innovative alternatives to traditional dairy products.

By Price Positioning: Mass Market Dominance With Premium Growth

Mass price positioning holds 79.20% market share in 2025, demonstrating Chinese consumers' value-consciousness and brands' focus on accessible pricing over premium positioning. This market control results from effective price competition by domestic brands such as Cotti Coffee, which provide quality coffee at lower prices than international competitors. The mass market strategy facilitates rapid market penetration and consumer adoption, particularly crucial in a market where coffee consumption remains in development compared to traditional tea drinking habits.

The premium segment exhibits a 5.95% CAGR through 2031, indicating increased consumer sophistication and readiness to invest in higher-priced offerings. This growth corresponds with rising incomes among urban professionals and increased appreciation for specialty coffee experiences. While Starbucks maintains its premium positioning despite competitive pressures, the market shows clear segmentation. Value-seeking consumers drive volume growth, while quality-focused demographics support margin expansion. Companies now implement portfolio strategies that address both segments through distinct product lines and market positions.

By Packaging Type: PET Bottles Dominate Convenience-Driven Market

In 2025, PET bottles captured a dominant 37.55% share of China's RTD coffee market, thanks to their portability and resealability. These features resonate with urban commuters, especially during subway rides and at work. PET bottles are lightweight, shatterproof, and convenient for on-the-go consumption, making them a preferred choice for consumers with busy lifestyles. Additionally, their resealable nature allows for portion control and multiple consumption occasions, enhancing their practicality. Manufacturers are also leveraging PET bottles for innovative designs and branding opportunities, further boosting their appeal. While glass bottles, positioned as premium offerings, struggle with a modest market share despite their enhanced product presentation. Cans, though adept at keeping beverages cold, fall short on resealability, curtailing their use for multiple drinking occasions.

Carton packaging is on a steady ascent, projected to grow at a CAGR 4.18% through 2031. This growth is bolstered by environmental concerns and Tetra Pak's technology, which not only extends shelf life to six months but also trims distribution costs via efficient storage and transport. The market is also witnessing the rise of innovative formats like pouches and distinct container shapes, such as ergonomic designs and single-serve options, underscoring the industry's response to evolving consumer tastes. Retailers' pledge to cut plastic waste by 30% by 2025 further cements carton packaging's status as the go-to choice for eco-conscious consumers. In a bid to enhance carton appeal, manufacturers are embedding QR codes, unlocking avenues for customer loyalty programs, point-based rewards, digital coupons, and immersive brand interactions, seamlessly weaving digital engagement into everyday consumer life.

By Distribution Channel: Convenience Stores Lead While Online Accelerates

Convenience and grocery stores hold a 36.70% market share in 2025, benefiting from China's extensive retail network and consumer preference for readily available products during daily activities. This channel's dominance reflects how RTD coffee has become integrated into regular shopping habits, with consumers purchasing coffee alongside other daily items. The success of convenience stores stems from their locations near offices, transport hubs, and residential areas, effectively capturing both impulse purchases and regular consumption.

Online retail stores exhibit the highest growth rate at 6.15% CAGR through 2031, supported by China's robust e-commerce infrastructure and increasing consumer adoption of digital beverage purchases. This growth aligns with broader retail digitization and allows brands to reach consumers in lower-tier cities where physical coffee retail presence is limited. Supermarkets and hypermarkets maintain substantial market share through volume purchases and promotions, while the Others category, including vending machines and forecourt retailers, provides round-the-clock access. The evolution of distribution channels highlights the importance of omnichannel strategies, as consumer segments show varying preferences based on accessibility, pricing, and product selection.

Geography Analysis

In 2025, East China commands a 42.70% market share, driven by Shanghai's strong financial sector and Beijing's concentration of multinational corporations, which boost coffee consumption among urban professionals. The region's well-established café culture and higher consumer spending power foster the development of premium coffee products, making it a hub for innovation in the RTD coffee market. Additionally, the presence of affluent consumers and a growing preference for convenience-oriented beverages further support market growth. However, as major cities approach market saturation, growth is beginning to moderate, with companies focusing on retaining market share through product differentiation and targeted marketing strategies. Despite these challenges, East China remains a critical region for premiumization and sustained revenue generation in the RTD coffee segment.

Central and Western China is experiencing the fastest growth, with a 5.12% CAGR projected through 2031. This growth stems from domestic brands successfully penetrating underserved markets with affordable, locally adapted coffee products that cater to regional tastes and preferences. Franchises in the region are expanding rapidly, leveraging lower rental costs and operational efficiencies to maintain profitability despite lower purchase values. The increasing urbanization and rising disposable incomes in these areas are also contributing to the growing demand for RTD coffee. Furthermore, the region's untapped potential and the ability of brands to establish a strong foothold in these emerging markets make it a focal point for long-term market expansion and investment opportunities.

Other regions, including Northern and South China, exhibit unique market dynamics that contribute to the overall diversity of the RTD coffee market. Northern China benefits from Russian and Korean tourist demand for stronger coffee varieties, which align with their taste preferences, while extended winters drive consistent consumption of shelf-stable canned lattes, ensuring year-round demand. In South China, the tropical climate supports year-round cold beverage consumption, with international food and beverage expertise further enhancing product offerings and consumer experiences. The region's openness to global trends and its established distribution networks make it a key area for introducing innovative RTD coffee products. These regional variations highlight the need for companies to adapt their pricing, flavors, and packaging to cater to the diverse preferences and consumption patterns across China's RTD coffee market, ensuring sustained growth and competitiveness.

Competitive Landscape

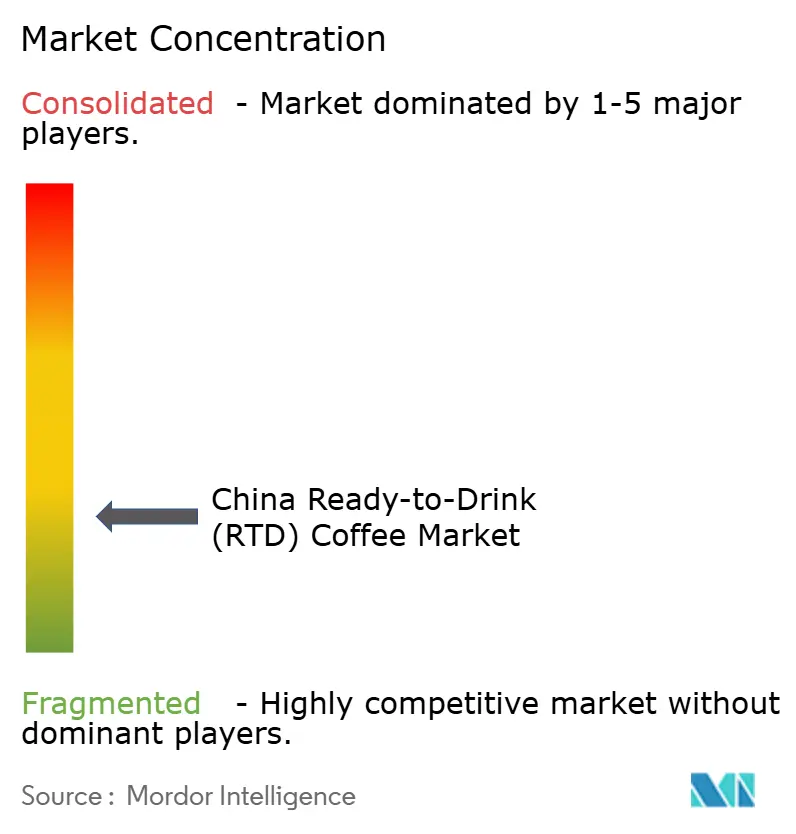

The China ready-to-drink (RTD) coffee market exhibits fragmentation. Domestic brands have captured substantial market share from international companies by implementing aggressive pricing strategies and developing products tailored to Chinese consumer preferences, particularly in tier-2 and tier-3 cities. Major global companies operating in the market include Nestle SA, Suntory Holdings Ltd, Restaurant Brands International Inc. (Tim Hortons), and Uni-President Enterprises Corp, among others.

Companies in the market implement advanced technology for supply chain optimization, customer data analysis, and automated production systems, with increasing investments in artificial intelligence and machine learning capabilities. These technological implementations reduce operational labor costs while maintaining consistent product quality across retail networks. Major companies like Nestlé have reduced their product innovation cycles from years to months to address market demands.

The market presents opportunities through protein-enhanced coffee beverages for health-conscious consumers, sugar-free cold brew variants in 250 ml cartons, and rural vending machines utilizing grain silos as automated retail points. The competitive environment remains intense as venture capital and private equity investors fund differentiated products and business models. Market growth is driven by increasing urbanization, rising disposable incomes, growing consumer preference for convenient ready-to-drink beverages, and expanding annual RTD coffee consumption in urban areas.

China Ready-to-Drink (RTD) Coffee Industry Leaders

-

Nestle S.A

-

Restaurant Brands International Inc. (Tim Hortons)

-

The Coca-Cola Company

-

Suntory Holdings Ltd (Boss Coffee)

-

Uni-President Enterprises Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Starbucks launched a new ready-to-drink (RTD) coffee and tea blend in China, with bottle design and visual identity developed by creative agency Marks. The product combines premium coffee and tea ingredients, marking the company's entry into the emerging RTD coffee-tea beverage category.

- April 2024: Nestlé Coffee introduced six new products, enhancing its consumer experience offerings. The company developed these products to address four key consumer preferences: sustained refreshment, immersive experience, flavor combinations, and health-conscious choices.

- June 2023: Tims China launched a ready-to-drink (RTD) coffee range in collaboration with Oatly. The co-branded oat milk latte products are available through both companies' e-commerce platforms and select third-party retailers.

China Ready-to-Drink (RTD) Coffee Market Report Scope

Ready-to-drink coffee is a cold drink that comes pre-made in a can or a bottle and is a quick takeaway option for lunches. China's ready-to-drink (RTD) coffee market is segmented by packaging type and distribution channel. Based on the packaging type, the market is segmented into bottles, cans, and other packaging types. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, foodservice channels, online retail stores, and other distribution channels. The report offers market size and forecasts in value (USD million) for the above segments.

By Product Type

| Cold Brew RTD Coffee |

| Iced Latte/Cappuccino |

| Nitro RTD Coffee |

| Functional/Protein-Enhanced RTD Coffee |

By Flavor Profile

| Plain/Classic |

| Flavored |

By Ingredient Base

| Dairy-Based |

| Plant-Based Milk |

By Price Positioning

| Mass |

| Premium |

By Packaging Type

| Bottles | Glass Bottles |

| PET Bottles | |

| Cans | |

| Cartons | |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience and Grocery Stores |

| Online Retail Stores |

| Others (Vending Machine, Forecourt Stores, etc) |

By Region

| East China |

| South China |

| North and Northeast China |

| Central and Western China |

| By Product Type | Cold Brew RTD Coffee | |

| Iced Latte/Cappuccino | ||

| Nitro RTD Coffee | ||

| Functional/Protein-Enhanced RTD Coffee | ||

| By Flavor Profile | Plain/Classic | |

| Flavored | ||

| By Ingredient Base | Dairy-Based | |

| Plant-Based Milk | ||

| By Price Positioning | Mass | |

| Premium | ||

| By Packaging Type | Bottles | Glass Bottles |

| PET Bottles | ||

| Cans | ||

| Cartons | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience and Grocery Stores | ||

| Online Retail Stores | ||

| Others (Vending Machine, Forecourt Stores, etc) | ||

| By Region | East China | |

| South China | ||

| North and Northeast China | ||

| Central and Western China | ||

Key Questions Answered in the Report

What is the current size of the China RTD coffee market?

It is valued at USD 1.5 billion in 2026 and is forecast to grow to USD 1.68 billion by 2031 at a 2.21% CAGR.

Which region leads RTD coffee sales in China?

East China leads with 42.70% market share, mainly driven by Shanghai and Beijing.

Which product segment is expanding fastest?

Cold brew RTD coffee is the fastest-growing, registering a 4.26% CAGR through 2031.

What packaging format shows the highest growth?

Cartons, thanks to sustainability appeal, are growing at a 4.18% CAGR, even though PET bottles still dominate overall sales.

Page last updated on: