Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

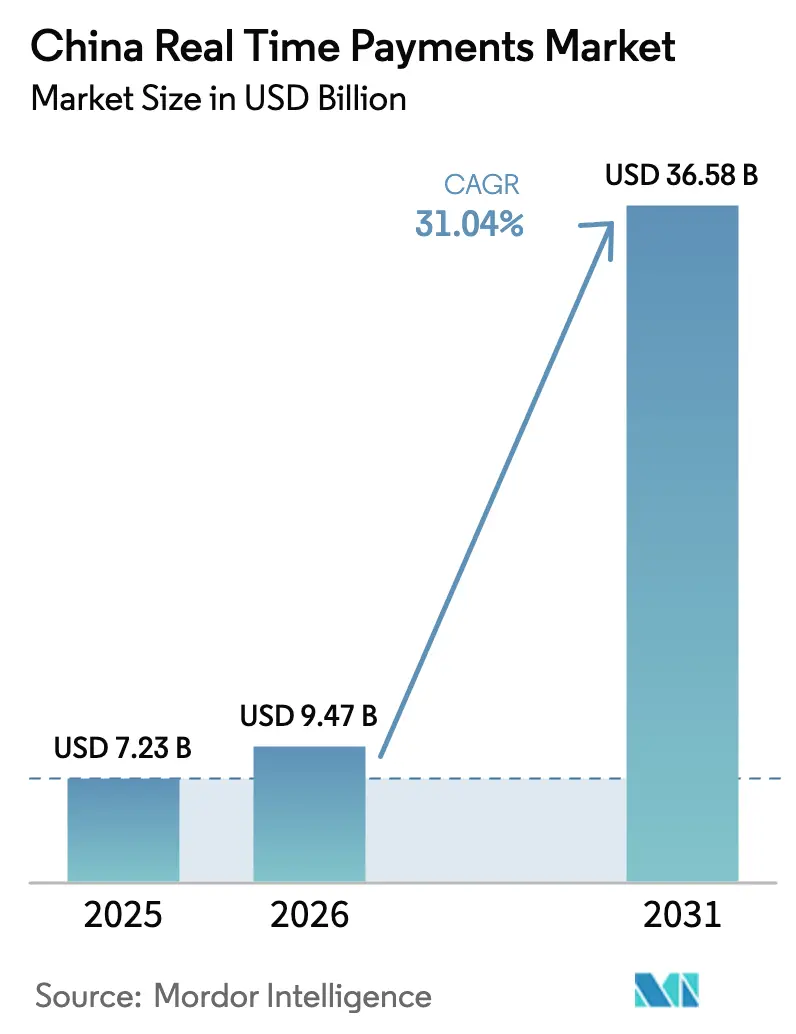

| Base Year Market Size (2025) | USD 7.23 Billion |

| Market Size (2026) | USD 9.47 Billion |

| Market Size (2031) | USD 36.58 Billion |

| Growth Rate (2026 - 2031) | 31.04% CAGR |

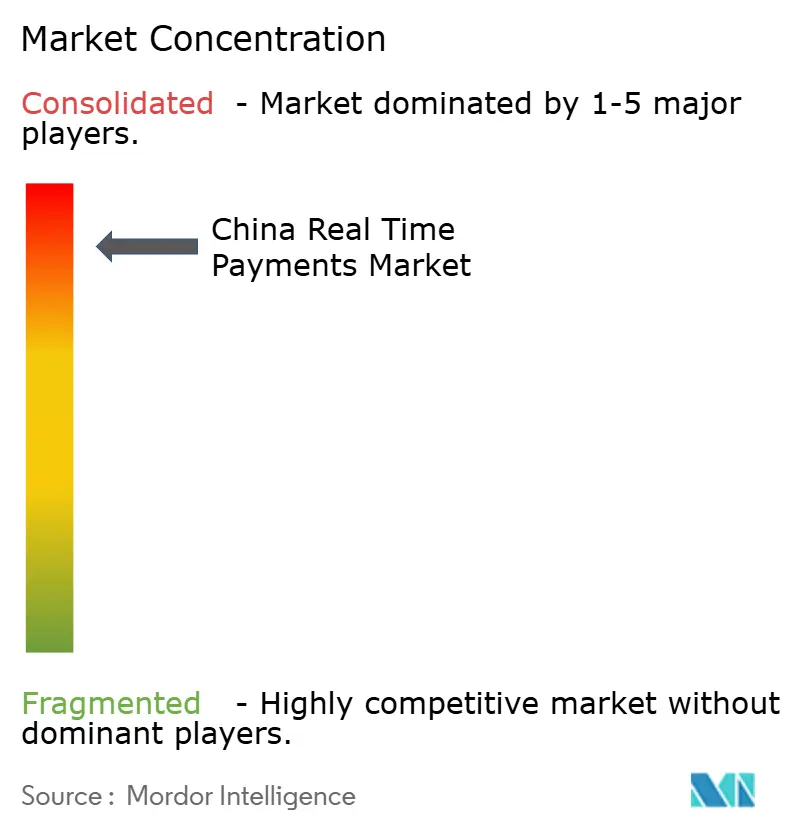

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Real Time Payments Market Analysis by Mordor Intelligence

The China Real Time Payments market size was valued at USD 7.23 billion in 2025 and estimated to grow from USD 9.47 billion in 2026 to reach USD 36.58 billion by 2031, at a CAGR of 31.04% during the forecast period (2026-2031). Growth is propelled by compulsory corporate connectivity to the NetsUnion clearing platform, roll-out of embedded “Alipay-Lite” mini-program payments, and the rapid scaling of cross-border e-CNY pilots that processed more than USD 1.2 trillion in 2024.[1]Proshare News, “Digital Yuan Cross-Border Volume Surges,” proshareng.com Competitive differentiation is shifting toward technology depth as Alipay and WeChat Pay accelerate NFC, AI fraud-monitoring, and ISO 20022 compliance investments to retain share while regulatory focus tightens on data localization and consumer protection. Market makers also face higher processing costs as sub-millisecond latency becomes a service level expectation for Tier-1 merchants, yet the QR-code interoperability mandate is lowering barriers for SMEs in lower-tier cities. Collectively, these forces create a market environment where scalable infrastructure, compliance agility, and value-added service orchestration outweigh pure transaction volume in determining long-term positioning.

Key Report Takeaways

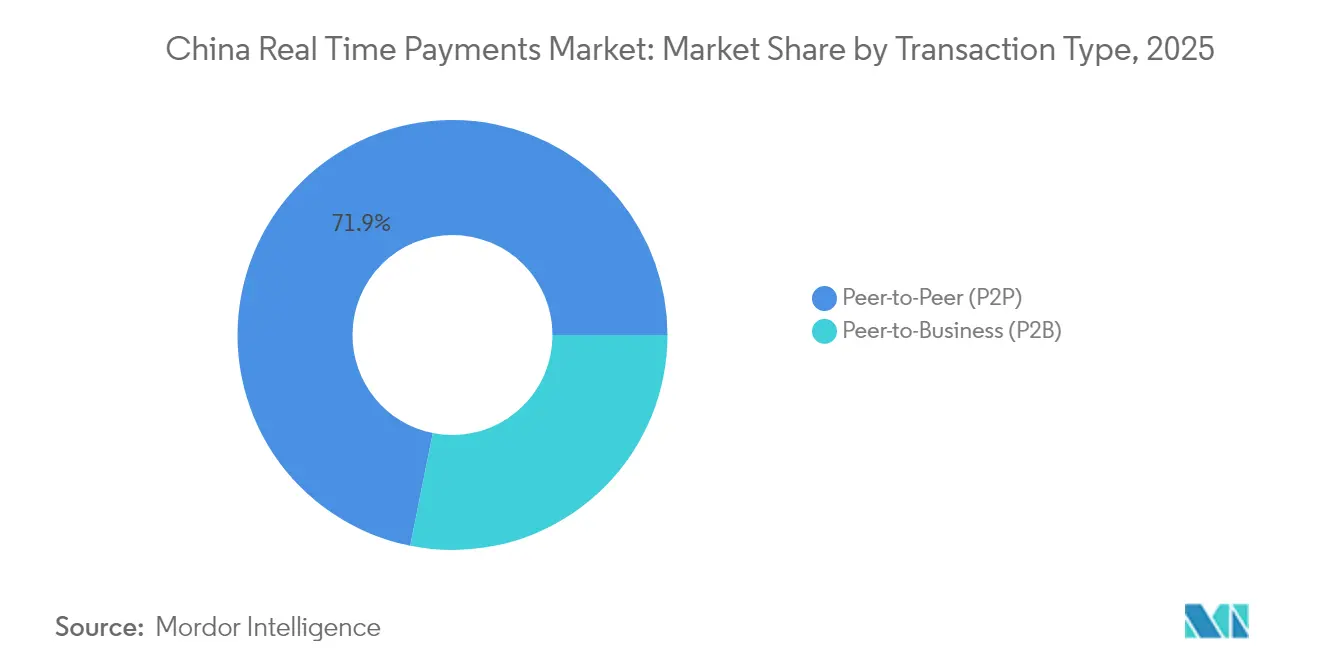

- By transaction type, P2P payments led with 71.85% China Real Time Payments market share in 2025 while P2B payments are projected to advance at a 33.68% CAGR through 2031.

- By component, Platform/Solution offerings accounted for 63.92% of the China Real Time Payments market size in 2025, whereas Services are expanding at a 32.8% CAGR.

- By deployment mode, Cloud solutions dominated with 77.96% share in 2025; On-Premise deployments are rising at a 33.4% CAGR.

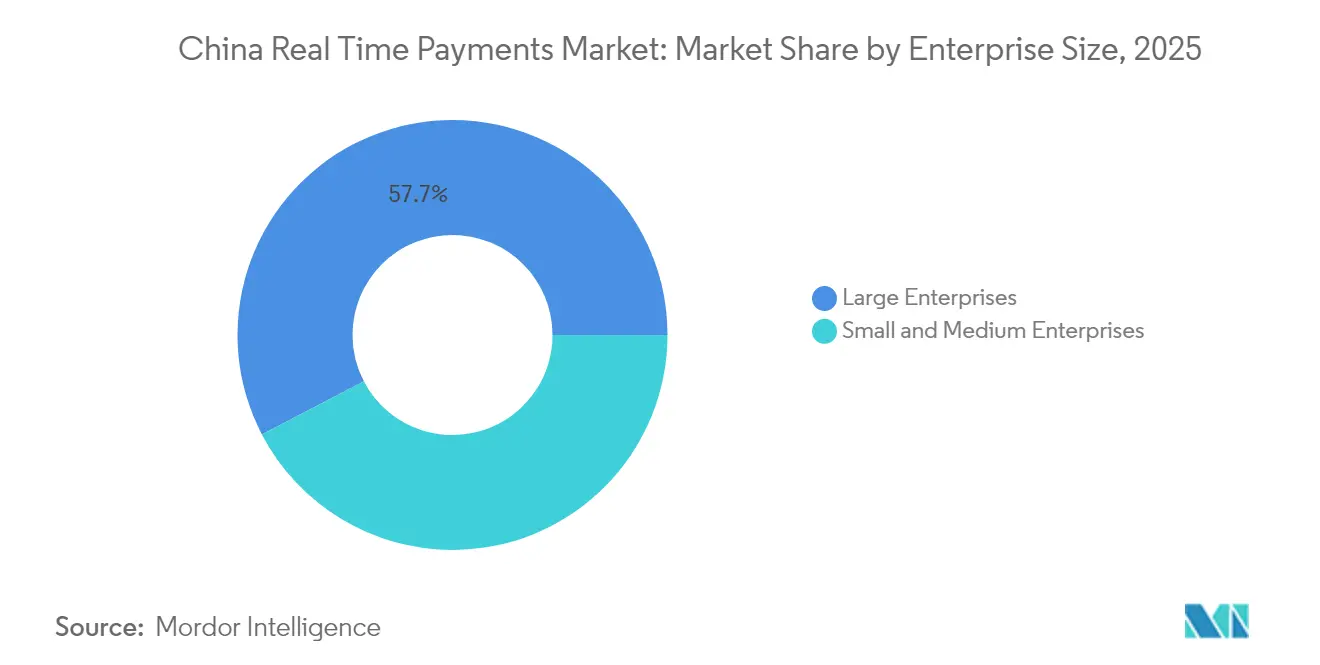

- By enterprise size, Large Enterprises held 57.65% revenue share in 2025, but SMEs are pacing the market with a 34.25% CAGR.

- By end-user industry, Retail & E-commerce commanded 40.08% of the China Real Time Payments market size in 2025, while Government & Public Sector is growing fastest at a 33.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Mobile Wallet Adoption Fuelled by "Alipay-Lite" Mini-Programs | +8.2% | National, with concentration in Tier-1 and Tier-2 cities | Short term (≤ 2 years) |

| Mandatory Corporate Connectivity to PBoC NetsUnion Platform | +6.5% | National, affecting all corporate entities | Medium term (2-4 years) |

| QR-Code Interoperability Mandate Accelerating SME Uptake in Lower-Tier Cities | +4.8% | Lower-tier cities and rural areas | Medium term (2-4 years) |

| Accelerated Cross-Border e-CNY Pilots for Belt & Road Digital Trade | +5.1% | Cross-border corridors, ASEAN and Middle East focus | Long term (≥ 4 years) |

| "Zero-Fee" Domestic Retail Transfers Policy Drives the Market | +3.7% | National, benefiting retail consumers | Short term (≤ 2 years) |

| High-Frequency Social Commerce Driving In-Chat Micro-Payments | +4.2% | Urban centers with high social media penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive Mobile Wallet Adoption Fuelled by “Alipay-Lite” Mini-Programs

The seamless insertion of payment buttons inside social feeds is reshaping conversion funnels as Alipay’s “Tap Once” feature surpassed 100 million users within 11 months of its June 2024 launch.[2]Retail Technology Innovation Hub, “Alipay Tap Once Hits 100M Users,” retailtechinnovationhub.com Eliminating app-switch friction triples membership registrations for offline chains such as FamilyMart, proving that embedded payments amplify loyalty acquisition while enriching shopper data lakes. Alipay’s USD 1.4 billion (RMB 10 billion) capital commitment to extend the ecosystem across 400 cities and 5,000 brands signals that the competitive axis is shifting from fee-discount campaigns to experiential stickiness and omnichannel data leverage.

Mandatory Corporate Connectivity to PBoC NetsUnion Platform

Full migration of non-bank payment institutions to the central clearing hub in 2024 standardized APIs and removed bilateral bank integrations, raising regulatory visibility and improving anti-money-laundering analytics. Corporates gain instant settlement capability, but service providers absorb a new layer of clearing fees, prompting them to bundle compliance dashboards and liquidity-management add-ons to defend margins. The NetsUnion architecture therefore incentivizes platform players to differentiate on value-added treasury functions rather than price.

QR-Code Interoperability Mandate Accelerating SME Uptake in Lower-Tier Cities

A single QR standard launched in December 2024 lets merchants accept UnionPay, WeChat Pay, and Alipay through one code.[3]UnionPay International, “UnionPay, WeChat Pay, Alipay Launch Unified QR,” unionpayintl.com Hardware consolidation lowers onboarding cost structures, making real-time acceptance viable for corner stores and wet-market vendors that previously viewed digital wallets as expensive or complex. By 2025, bilateral QR linkages between China and Japan have further expanded addressable merchant pools and tourist payment convenience, offering service providers new transaction corridors without redevelopment overhead.

Accelerated Cross-Border e-CNY Pilots for Belt & Road Digital Trade

The mBridge multilateral CBDC sandbox tied China to 16 partner nations and cut settlement lags from three days to seconds, validating instant trade finance clearing at scale. Over USD 22 million flowed through 164 test transactions by late 2024, reinforcing the feasibility of distributed ledger settlements that bypass correspondent banks. The Greater Bay Area rollout lets Hong Kong residents top-up e-CNY via Faster Payment System rails, giving regulators a live laboratory for cross-jurisdiction wallet operability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented ISO 20022 Implementation Among City Commercial Banks | -3.2% | Regional banks and city commercial banks | Medium term (2-4 years) |

| Real-Time Fraud-as-a-Service Rings Targeting QR Rail | -2.8% | National, with higher impact in urban centers | Short term (≤ 2 years) |

| Rising CPU & Network Costs for Sub-Millisecond Settlement SLAs | -1.9% | Data centers and payment processing hubs | Medium term (2-4 years) |

| Saturation in Tier-1 Urban User Base Hinders the Market | -1.5% | Tier-1 cities (Beijing, Shanghai, Guangzhou, Shenzhen) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented ISO 20022 Implementation Among City Commercial Banks

Large schemes such as CNAPS2 and CIPS already run on ISO 20022, yet 120-plus city commercial banks still juggle dual formats, creating message truncation and reconciliation lags. Budget constraints delay upgrades, forcing payment providers to maintain format converters that inflate operating cost structures. The July 2025 global compliance deadline intensifies pressure and could temporarily cap rural transaction growth until smaller banks finish rewiring core systems.

Real-Time Fraud-as-a-Service Rings Targeting QR Rail

Criminal networks now sell modular scripts that automate QR spoofing, account cycling, and AML evasion. Courts have jailed offenders for laundering RMB 200,000 using digital-yuan wallets, demonstrating the challenge of enforcing “controllable anonymity” safeguards. The People’s Bank of China imposed tighter transaction caps, yet providers must now invest in AI behavior analytics, pushing cost-to-income ratios higher for second-tier platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: P2B Payments Drive Enterprise Digitization

P2P transfers commanded 71.85% of the China Real Time Payments market in 2025, underlining entrenched peer payment habits that arose from social media wallet penetration. The dominance stems from features such as instant split bills and red-packet gifting that lock consumers into daily app usage. P2B flows, while smaller, are charting a 33.68% CAGR that is reshaping corporate treasury norms as businesses prioritize instantaneous cash application and automated invoice reconciliation. JD.com’s cross-border stablecoin program targets a 90% reduction in settlement cost and 10-second clearing, reinforcing that real-time liquidity optimization is now integral to trade competitiveness.

The trajectory shows enterprises recalibrating accounts-payable cycles toward continuous settlement, shrinking working capital buffers, and lowering counterparty risk. Supply-chain marketplaces and B2B fintechs bundle credit scoring with instant disbursement, broadening monetization beyond payment fees. The shift elevates P2B relevance within the China Real Time Payments market, signaling a future where merchant centricity overtakes consumer P2P in driving transaction value.

By Component: Services Segment Accelerates Through Compliance Investments

Platform/Solution stacks accounted for 63.92% of 2025 revenue as banks and PSPs implemented core switching engines, open APIs, and ledger services. As the foundation matures, the Services segment is expanding at 32.8% CAGR, with demand clustering around ISO 20022 migration, e-CNY integration, and AI fraud orchestration. Consulting houses and specialist integrators capture value by bridging legacy core banking platforms to cloud-native processors and by deploying rule-based compliance layers that satisfy NetsUnion reporting formats.

Ant International’s embedded finance suite doubled loans under administration in 2024, proof that service-led monetization outperforms one-time license revenue. Over time, professional services margins are expected to stabilize as standardized toolkits replace bespoke coding, yet the strategic need for regulatory choreography ensures durable growth for advisory portfolios within the wider China Real Time Payments industry.

By Deployment Mode: On-Premise Solutions Gain Traction for Data Sovereignty

Cloud architecture claimed 77.96% of the China Real Time Payments market in 2025, reflecting cost-efficiency and elastic scaling favored by fintech entrants. Nonetheless, On-Premise installations are recording a faster 33.4% CAGR as data-sovereignty statutes oblige state lenders and public agencies to localize sensitive payloads. The December 2024 Data Security Management Measures for Banking and Insurance underline governmental insistence on full control over citizen payment metadata.

Providers thus pursue hybrid topologies that anchor transaction ledgers within domestic data centers while distributing analytics microservices on public clouds, enabling regulatory compliance without sacrificing innovation speed. For the China Real Time Payments market, such architectures balance geopolitical mandates with platform economics, keeping barrier-to-entry high for foreign competitors.

By Enterprise Size: SMEs Embrace Digital Payment Transformation

Large Enterprises produced 57.65% of 2025 transaction value by virtue of high throughput and complex reconciliation needs. Yet SMEs represent the most dynamic adoption vector, expanding at a 34.25% CAGR as QR-code interoperability simplifies onboarding and zero-fee policies strip cost anxieties. Government programs that subsidize POS digitization in county-level cities further democratize access.

Studies published in 2024 link digital inclusive finance intensity to SME innovation capacity, showing heightened R&D investment and product launches when payment friction is removed. The implication for the China Real Time Payments market is a wider merchant base that generates long-tail volumes and pushes providers to offer modular service kits, such as instant invoice factoring, tailored for micro-entrepreneurs.

By End-User Industry: Government Sector Leads Digital Transformation

Retail & E-commerce retained a 40.08% slice of the China Real Time Payments market in 2025, leveraging embedded wallets to drive daily checkout convenience. However, Government & Public Sector transactions are accelerating at 33.85% CAGR as city authorities deploy smart-healthcare portals, digital welfare disbursement, and real-time utility billing. Alipay’s hospital checkout module reduced patient queuing times by 60%, illustrating how instant payments improve citizen service quality.

Utilities and telecom operators incorporate instant top-ups within smart-meter initiatives, while BFSI institutions continue steady migration to 24 × 7 retail clearing to stay on par with fintech challengers. For the China Real Time Payments market, growth diversity across verticals cushions revenue against saturation in consumer retail channels.

Geography Analysis

China’s Tier-1 cities—Beijing, Shanghai, Guangzhou, and Shenzhen—represented the bulk of 2024 transaction value due to mature digital ecosystems, multi-cloud data centers, and affluent consumer bases. Beijing’s smart-transit wallets exemplify municipal leadership in embedding payments within public infrastructure, while Shanghai’s extensive digital-yuan sandbox supports large-scale scenario testing through 2027. Market saturation in these metros prompts payment providers to deploy localized marketing, value-added tax tools, and loyalty bundles to deepen wallet stickiness.

Tier-2 and Tier-3 cities now deliver the highest growth rates as policymakers channel infrastructure subsidies and fintech innovation grants to narrow the urban–rural digital divide. The QR-code interoperability policy reduces merchant onboarding cycles from weeks to days, propelling adoption among food courts, mom-and-pop stores, and county hospitals. Telecom carriers such as China Unicom operationalize CUBE-Net 3.0 to guarantee low-latency coverage, enabling real-time processing in settings previously constrained by bandwidth.

Cross-border corridors add a third geographic dimension. The Greater Bay Area acts as a living lab, with Hong Kong residents now able to top-up e-CNY via FPS, demonstrating bilateral wallet harmonization. Project mBridge broadens outreach to ASEAN and Gulf Cooperation Council fronts, opening new settlement venues for exporters and lowering currency conversion drag. Consequently, international integration is set to amplify the transactional gravity of the China Real Time Payments market beyond domestic borders.

Competitive Landscape

Alipay and WeChat Pay jointly handle over 90% of mobile payment volume, giving the China Real Time Payments market a highly concentrated apex. Competitive tactics hinge on ecosystem breadth rather than fee discounting: Alipay+ links 90 million merchants in 66 economies to 1.6 billion users, whereas WeChat inserts social-commerce micro-stores inside its super-app, converting engagement into payments. Both incumbents invest in AI neural nets that flag anomalous activity within 50 milliseconds, a capability now critical as fraud rings weaponize automation.

Regulatory shifts enable selective disruption. UnionPay’s December 2024 move to let international cards scan Alipay or WeChat QR codes extends universal acceptance and builds a defensive moat against pure-play fintech wallets. Foreign schemes such as Visa and Mastercard leverage transit ticketing to gain local acceptance footholds, reflecting a partnership-led entry game as standalone wallet launches face licensing hurdles. Domestic challengers focus on vertical slices; Lakala targets SME offline payments with turnkey POS plus working-capital credit, and China UMS services state-owned utility billing.

The nascent CBDC channel represents both risk and opportunity. If e-CNY wallets eventually bypass third-party acquirers, incumbent PSPs could see interchange compression. Conversely, they can monetize B2B API gateways that connect corporate ERPs to the central currency ledger. Strategic success will thus depend on shaping value-added overlays—such as invoice tokenization and programmable escrow—on top of the base rails while cultivating compliance trust capital.

China Real Time Payments Industry Leaders

Paypal Holdings Inc.

ACI Worldwide Inc.

Ant Group Co., Ltd. (Alipay)

Tencent Holdings Ltd. (WeChat Pay)

JD.com, Inc. (JD Pay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: JD.com announced applications for stablecoin licenses in Hong Kong, Singapore, and Luxembourg, targeting 90% cost reduction and 10-second settlement times for cross-border payments, positioning the company to compete directly with traditional banking infrastructure for international trade finance applications.

- May 2025: Ant Group's international division reported USD 3 billion in revenue for 2024 ahead of planned spinoff, with cross-border transaction volumes tripling and total loans under management doubling, demonstrating the scalability of AI-powered embedded finance services in emerging markets.

- May 2025: Hong Kong Monetary Authority expanded e-CNY pilot program to all city residents, enabling digital yuan wallet creation using local mobile numbers and FPS top-ups, creating the first global linkage between a faster payment system and central bank digital currency.

- December 2024: UnionPay International enabled cross-platform QR payments with WeChat Pay and Alipay for international cards, allowing foreign visitors to access China's payment ecosystem through unified QR codes without service fees during promotional periods.

China Real Time Payments Market Report Scope

Real-time payments, or RTPs, process transactions in real-time or at least in the least possible time frame. RTPs initiate, clear, and settle payments within a few seconds, ideally up 247 and 365 days. Further, RTPs are 'open-loop,' meaning they are connected directly to a personal account and do not rely on prepaid balances.

The China real time payments market is segmented by payment type (P2P, P2B). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Transaction Type

| Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) |

By Component

| Platform / Solution |

| Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-User Industry

| Retail and E-Commerce |

| BFSI |

| Utilities and Telecom |

| Healthcare |

| Government and Public Sector |

| Other End-user Industries |

| By Transaction Type | Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) | |

| By Component | Platform / Solution |

| Services | |

| By Deployment Mode | Cloud |

| On-Premise | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Utilities and Telecom | |

| Healthcare | |

| Government and Public Sector | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the China Real Time Payments market?

The China Real Time Payments market size is estimated at USD 9.47 billion in 2026 and is projected to rise to USD 36.58 billion by 2031.

Which transaction type is expanding fastest?

P2B payments are forecast to grow at a 33.68% CAGR through 2031 as enterprises prioritize instant settlement for supply-chain and marketplace activities.

Why are services growing faster than platforms?

Compliance consulting, ISO 20022 migration support, and AI-based fraud detection drive a 32.8% CAGR for services because institutions need ongoing expertise beyond core processing engines.

How does QR-code interoperability benefit SMEs?

A single QR standard lowers device and integration costs, enabling small merchants in lower-tier cities to accept multiple wallets with one code and boosting digital payment adoption.

What role does the e-CNY play in cross-border payments?

The e-CNY, tested through mBridge pilots, enables near-instant settlement with trading partners across Belt & Road corridors, reducing reliance on correspondent banks and SWIFT rails.

Who are the main competitors and how concentrated is the market?

Alipay and WeChat Pay process over 90% of mobile transactions, yielding a high market concentration score of 9 and shaping a landscape where newcomers focus on niche or compliance-driven opportunities.

Page last updated on: