Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 54.72 Billion |

| Market Size (2026) | USD 55.49 Billion |

| Market Size (2031) | USD 62.14 Billion |

| Growth Rate (2026 - 2031) | 2.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Kitchen Appliances Market Analysis by Mordor Intelligence

The China Kitchen Appliances Market size is expected to grow from USD 54.72 billion in 2025 to USD 55.49 billion in 2026 and is forecast to reach USD 62.14 billion by 2031 at 2.29% CAGR over 2026-2031.

A steady shift from unit-led expansion to value upgrading shapes demand patterns, aided by energy-efficiency re-grading that tightens product thresholds, ecosystem bundling that locks in device usage, and livestream shopping that lowers acquisition costs. Within product categories, refrigerators and freezers remain the largest revenue pool while counter-top ovens gain ground as compact, installation-light formats for urban homes. Residential demand accounts for most purchases, yet commercial kitchens are building momentum as prepared-meal operators add capacity. Regional sales skew toward East China’s strong manufacturing and retail base, with North China growing faster on policy support and income gains in leading cities.

Key Report Takeaways

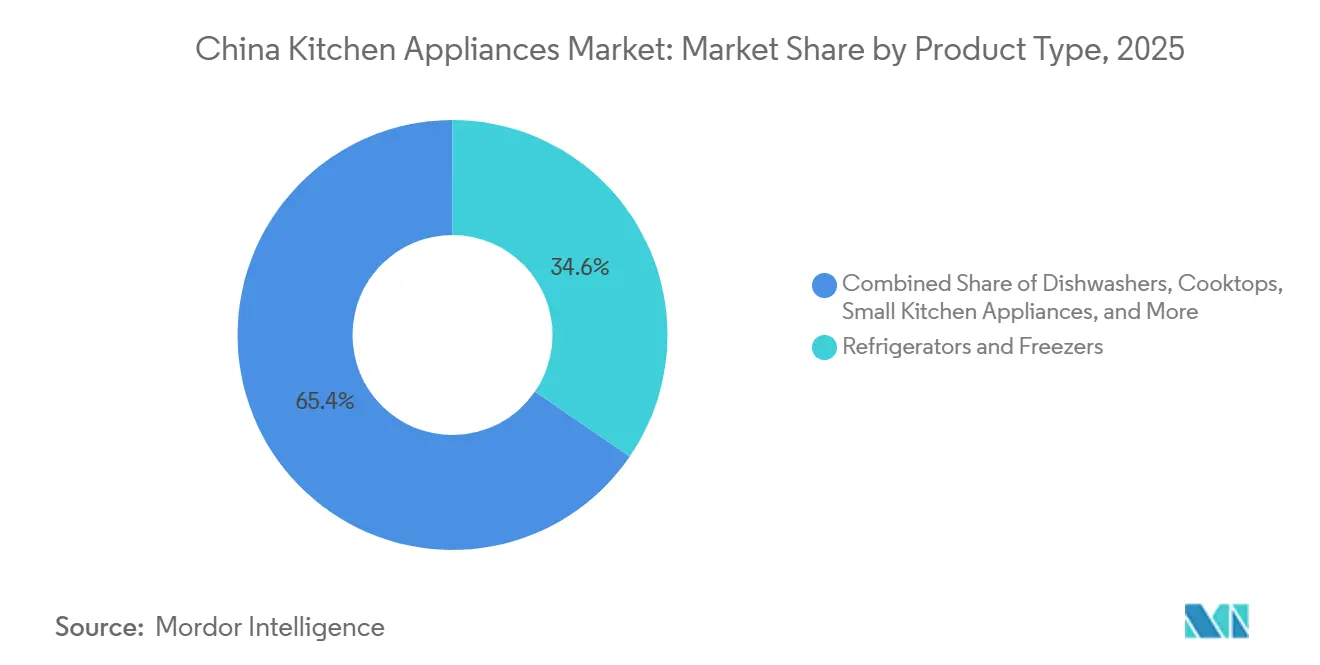

- By product type, refrigerators and freezers led with 34.56% of the China kitchen appliances market share in 2025; counter-top ovens are forecast to expand at a 3.62% CAGR through 2031.

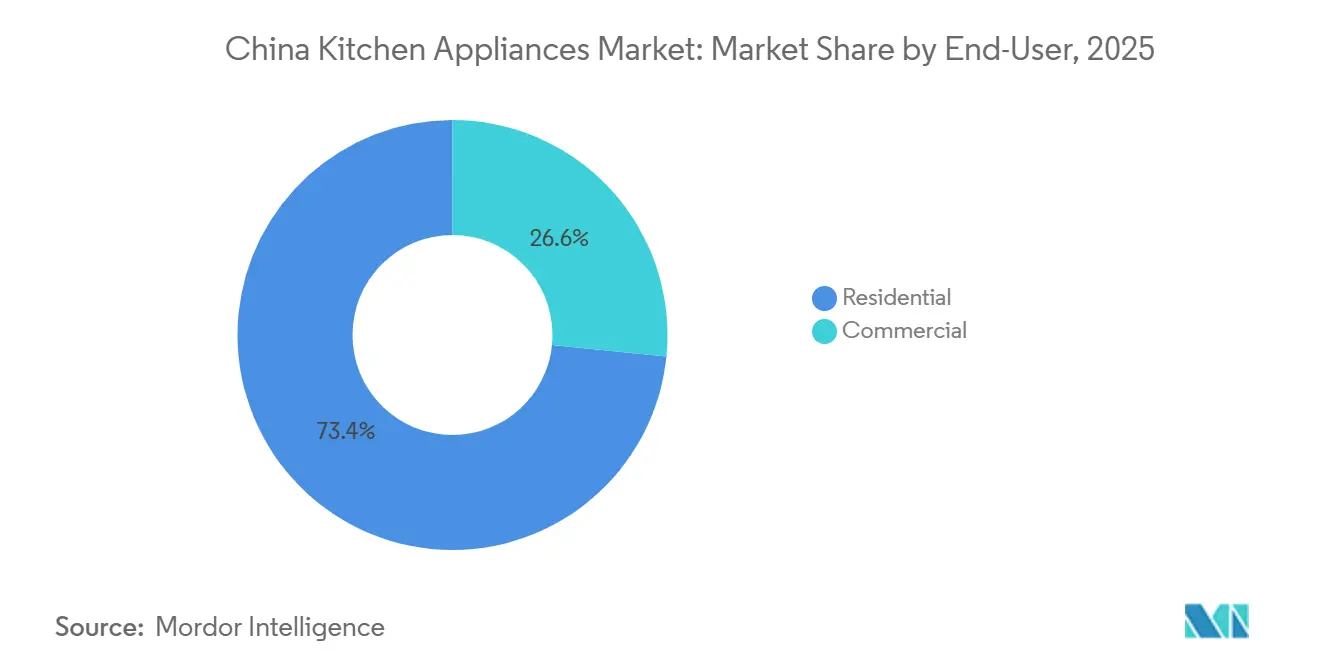

- By end user, residential held 73.41% of the China kitchen appliances market share in 2025, while commercial recorded the fastest projected growth at 3.35% through 2031.

- By distribution channel, B2C retail captured 71.83% of the China kitchen appliances market share in 2025, and the online sub-channel recorded the highest projected growth at 4.12% through 2031.

- By geography, East China accounted for 32.63% of the China kitchen appliances market share in 2025, and North China posted the highest projected growth at 3.14% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban middle-class expansion | +0.5% | National, strongest in Tier 2–3 cities | Medium term (2-4 years) |

| Post-COVID premiumization of home-cooking culture | +0.4% | National, early gains in East and South-Central China | Short term (≤ 2 years) |

| "Smart home" ecosystem bundling by Chinese OEMs | +0.6% | National, led by Shanghai, Guangdong, Beijing tech hubs | Long term (≥ 4 years) |

| E-commerce livestreaming as a low-CAC sales engine | +0.5% | National, spill-over to less penetrated prefectures | Short term (≤ 2 years) |

| Mandatory national energy-efficiency re-grading in 2026 | +0.3% | National, uniform standards and labeling compliance | Medium term (2-4 years) |

| Commercial kitchen upgrade wave from prepared-meal chains | +0.2% | South-Central and East China meal-delivery corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Middle-Class Expansion

China’s rapidly expanding urban middle class is a key driver of growth in the kitchen appliances market. In 2024, the per capita disposable income of urban residents reached CNY 54,188 (USD 7,432), rising year-on-year, giving city dwellers stronger purchasing power to spend on modern appliances[1]Source: National Bureau of Statistics of China, “Households’ Income and Consumption Expenditure in 2024,” stats.gov.cn. Moreover, in 2024, China’s nationwide per capita disposable income was CNY 41,314 (USD 5,660), up 5.3% year‑on‑year. The median income was CNY 34,707 (USD 4,754), indicating overall income growth across the population[2]Source: China Daily, “Expanding the middle‑income group,” 27 Feb 2023, epaper.chinadaily.com.cn. Higher incomes enable families to invest in products that are not only functional but also convenient, high-quality, and lifestyle-enhancing. The growth of smaller urban homes is increasing demand for space-saving and multi-functional appliances that fit modern living spaces. Consumers are also becoming more conscious of hygiene, energy efficiency, and smart features, which influences their purchasing choices. As urban lifestyles continue to evolve, households increasingly view kitchen appliances as essential tools for comfort and convenience rather than just chores. With rising disposable incomes and expanding middle-class populations, the market for premium and innovative kitchen appliances is expected to grow steadily over the coming years.

"Smart Home" Ecosystem Bundling by Chinese OEMs

OEMs integrate kitchen appliances into broader connected ecosystems that raise lifetime value and reduce churn. Households operating three or more linked devices show markedly higher engagement and repurchase behavior, which has encouraged vendors to pair range hoods with cooktops that automatically synchronize smoke extraction when high-temperature cooking is detected. Adoption rates for smart, connected versions are now mainstream across several categories, with connected range hoods, gas stoves, and dishwashers exceeding half of retail volumes in 2024. This approach builds scale advantages that are hard to replicate for brands without adjacent device portfolios or proprietary platforms. Consumers also benefit from scenario-based usage and simplified setup, which together support upgrades to higher-efficiency and quieter models.

E-Commerce Livestreaming as a Low-CAC Sales Engine

Livestreaming compresses awareness, evaluation, and purchase into short, interactive sessions that reduce customer acquisition costs compared with traditional retail. During the 2025 Singles Day shopping festival, China’s major e-commerce, instant retail, and community group-buying platforms achieved a total of CNY 1.695 trillion (USD 232.2 billion) in sales, up 14.2 % year-on-year, with e-commerce platforms alone generating CNY 1.619 trillion and instant retail sales surging 138.4 % to CNY 67 billion (USD 9.18 billion). Platforms such as Tmall, JD.com, and Douyin led the growth, underscoring the power of livestreaming and interactive commerce in driving high-volume sales[3]Source: Zheng Yiran, “E-commerce market embraces livestreaming,” China Daily, chinadaily.com.cn. This format helps reduce return rates by aligning expectations with live demonstrations, while enabling rapid price discovery for bundled kitchen suites. Subsidy programs promoting efficient appliances further improve price realization during major shopping festivals, keeping the China kitchen appliances market favorably positioned online despite slower foot traffic in legacy brick-and-mortar stores.

Mandatory National Energy-Efficiency Re-Grading 2026

A tighter national energy-efficiency framework and updated labeling have created a visible migration toward Grade 1 models in cooking and counter-top devices. Implementation rules and labeling updates have progressed, with requirements around energy grades and standardized disclosures shaping assortments on shelves and online. Policy instruments, including the 2026 trade-in program, allocate CNY 62.5 billion (USD 8.8 billion) for consumer upgrades and subsidize 15% of purchase prices up to CNY 1,500 per item, equal to USD 211.3, which shifts demand toward compliant models and accelerates replacement[4]Source: Shanghai Metal Market editors, “Notice on the Implementation of Large-Scale Equipment Renewal and Consumer Goods Trade-In Policy in 2026,” SMM, metal.com. The tightened standards lift barriers for smaller brands while reinforcing the scale advantages of incumbents that can amortize compliance costs across higher volumes. For consumers, clearer labels and verifiable data improve confidence at the point of selection and reduce the incidence of low-efficiency options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Property-market slowdown dampening new-home fit-outs | -0.9% | National, acute in overbuilt Tier 1–2 cities | Medium term (2-4 years) |

| Raw-material cost volatility (steel, compressors, chips) | -0.4% | National, affects coastal export hubs | Short term (≤ 2 years) |

| Import-tariff risks on critical components | -0.3% | National, sourcing from Japan, South Korea, the EU | Medium term (2-4 years) |

| Lengthening replacement cycles due to durable build quality | -0.2% | National, pronounced in saturated East China markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Property-Market Slowdown Dampening New-Home Fit-Outs

The new-housing slump reduces developer installations for built-in ranges, hoods, and integrated stoves, directly weighing on categories tied to turnkey handovers. Fine-decoration project volumes declined year over year in the first half of 2025, and new-home sales fell in value terms across key cities where mortgage approvals tightened. Brands more exposed to developer channels reported revenue and profit declines as institutional orders retrenched, while companies with stronger direct-to-consumer channels offset a portion of the contraction. To adapt, leading players partner with renovation firms to bundle full-suite kitchens for stock housing upgrades, which taps into older apartments with legacy appliances. This shift keeps the China kitchen appliances market anchored in replacement and renovation pathways even as new-home demand softens.

Raw-Material Cost Volatility

Fluctuations in steel, copper, aluminum, and semiconductors have compressed margins for brands with limited hedging and weaker bargaining leverage. Company disclosures attribute revenue and net profit pressure to rising input costs and higher spending to defend share in price-competitive categories. Larger incumbents mitigate volatility through vertical integration, long-term supply agreements, and design rationalization that consolidates functions and reduces bill-of-materials counts. Currency swings that raise imported component costs complicate planning even when export markets provide a partial buffer. These supply-side dynamics reinforce scale advantages within the China kitchen appliances market and reward operational resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Compact Formats Challenge Established Categories

Refrigerators and freezers accounted for 34.56% of 2025 revenue, while counter-top ovens are projected to grow at a 3.62% CAGR through 2031, underscoring the pivot to compact formats fit for smaller kitchens in large cities. Consumers are increasingly trading up to high-value built-in appliances, including quieter range hoods and larger dishwashers with sterilization features, supporting overall price growth. Dishwashers are evolving toward larger-capacity models that double as storage solutions, reflecting rising hygiene and convenience preferences. Range hoods and gas cooktops remain essential in daily cooking, with airflow efficiency and precise flame control guiding purchase decisions. Technology-driven improvements, such as smart dosing and hot-air circulation in dishwashers, are helping overcome historic adoption barriers by emphasizing cleanliness and ease of use.

Built-in microwave-steamer-oven combinations are becoming more attractive as advanced features like dual-chamber cooking enhance versatility. AI-powered ovens that allow separate cooking zones appeal to multi-generational households preparing diverse meals simultaneously. Gas cooktop innovations that optimize thermal efficiency and reduce energy use align with government energy policies and sustainability goals. In small appliance categories, premium materials and non-coating designs are supporting replacement demand as markets mature. Counter-top ovens that combine baking, reheating, and air-frying in compact designs are opening the category to renters and nano-apartment dwellers who lack space for built-in installations.

By End User: Commercial Segment Outpaces Residential Despite Smaller Base

Residential applications accounted for 73.41% of 2025 demand, reflecting mass household penetration in refrigeration and cooking essentials and rising adoption of dishwashers in urban core markets. The market benefits from premiumization and renovation-driven bundles that combine ventilation, cooktops, and steam-bake ovens, while new-home installation slowdowns have shifted focus toward upgrades in existing homes. Partnerships with renovation firms allow vendors to offer full-suite kitchen packages, making it easier for households to modernize their kitchens. Government subsidies promoting energy-efficient models further lower the cost barrier for consumers considering appliance replacements. Premium product lines continue to gain traction, with designs that address smoke control, noise reduction, and performance in open-plan kitchens.

Commercial demand grows from a smaller base at a projected 3.35% through 2031 as prepared-meal platforms and organized chains expand central kitchens and upgrade in-store cooking capacity. Operators prioritize reliable, high-throughput equipment that meets food safety and energy-efficiency standards, while manufacturers introduce compact commercial lines suitable for retrofitted spaces. Supermarkets and new retail formats are driving demand for specialized equipment that can handle long duty cycles and comply with electromagnetic standards. Vendors that offer modular platforms can serve both residential and commercial customers efficiently, reusing components without compromising performance. Tailored sales strategies, including scenario-based showrooms for households and project-focused direct sales for businesses, along with robust service networks, strengthen retention and create cross-selling opportunities across the market.

By Distribution Channel: Online Dominance Accelerates via Livestreaming

B2C retail held 71.83% of 2025 sales, led by the online sub-channel that is projected to expand at 4.12% annually through 2031. B2C retail continues to dominate the China kitchen appliances market, with online channels leading growth as interactive livestream commerce during major shopping festivals helps reduce uncertainty in high-involvement purchases. Small appliances have nearly full online penetration, while larger appliances are increasingly sold online as installation and delivery services improve. Government subsidies for energy-efficient models integrated into online promotions have boosted consumer adoption of premium-grade appliances. These trends reinforce an online-first orientation for the market, even as select premium products continue to sell in physical stores. Livestreaming and interactive demonstrations allow consumers to evaluate products virtually, supporting confidence and driving sales across categories.

Offline B2C channels, including exclusive brand outlets and multi-brand stores, remain important for experiential selling and same-day installation services. Leading brands are expanding networks in lower-tier cities to reach consumers who prefer in-person demonstrations or bundled installation options. Exclusive outlets enable scenario-based setups where linked cooking suites are configured and fine-tuned by trained staff, enhancing the in-store experience. For B2B customers, direct-from-manufacturer contracts with property projects and institutional buyers provide stable volumes despite longer sales cycles. Integrated online and offline workflows, including fast delivery and installation, create a seamless purchase experience that reduces returns, builds trust, and encourages repeat and cross-category purchases.

Geography Analysis

East China holds the largest regional contribution with 32.63% of 2025 sales in the China kitchen appliances market. East China remains the largest contributor to the China kitchen appliances market, anchored by manufacturing hubs near Hangzhou and Ningbo that streamline supply chains and reduce logistics costs. Coastal cities with higher per-capita incomes support strong adoption of premium refrigerators and built-in cooking suites. Smart-home integration is particularly advanced in these areas, enabling bundled purchases of connected devices across cooking, cleaning, and refrigeration categories. Coastal exports also help maintain factory utilization and achieve scale economies, allowing a broader domestic product assortment. This combination of income, infrastructure, and technology adoption positions East China as the primary engine of market growth.

South-Central China contributes significantly through both production and consumption, with Guangdong’s manufacturing ecosystem supporting national and export demand. Leading vendors reported revenue growth in the first half of 2025, driven by smart, green, and higher-end products across several cooking and cleaning lines. Emerging urban centers in Hunan and Hubei registered robust retail growth for household appliances on the back of infrastructure investment and urbanization. The region also concentrates central kitchens for prepared-meal networks, raising orders for commercial-grade cooking and cooling equipment. These developments provide a second growth engine for the China kitchen appliances market alongside residential replacement and renovation in coastal cities.

North China is the fastest-growing region at a projected 3.14% CAGR from 2026 to 2031 within the China kitchen appliances market. In North China, policy pilots for energy efficiency and smart-city standards accelerate the adoption of premium appliances, while rising incomes and expanding dual-income households support built-in solutions. Subsidy programs in the region further incentivize first-time buyers and modern appliance upgrades. Meanwhile, Northeast, Southwest, and Northwest provinces exhibit a mix of renovation-driven and rural/secondary city demand, supported by infrastructure spending, electrification, and logistics improvements. Hard-water conditions and other regional needs drive the adoption of specialized products, such as water purifiers, providing a multi-year runway as these markets converge toward coastal penetration levels.

Regulatory Landscape

China kitchen appliances are governed by national regulators and standard-setting bodies led by the State Administration for Market Regulation (SAMR) and the National Certification and Accreditation Administration (CNCA), with compliance structured around GB/GB-T safety standards, energy-efficiency grades, and the China Energy Label system. Key recent anchors include GB 21456-2024 (Household and Similar Kitchen Appliance Energy Efficiency Limit Values and Energy Efficiency Grades), published in August 2024 and implemented from September 1, 2025, and the updated Kitchen Appliance Energy Efficiency Labeling Implementation Rules that took effect November 1, 2025, with a transition window for products manufactured or imported before that date through November 1, 2027.

A new compliance wave peaks around August-September 2026. GB/T 4706.1-2024 and GB/T 4706.30-2024 safety standards were published July 24, 2024, with mandatory implementation from August 1, 2026. CNCA Announcement 2024 No. 29 sets the certification transition to the updated safety standards on the same date, tightening market access for non-aligned models. Additional mandatory national standards such as GB 44498-2024 (health technical specifications) and GB 44499-2024 (energy saving and environmental protection specifications) are scheduled for implementation on September 1, 2026. Smart appliance requirements also advance through standards such as GB/T 45354.1-2025 for voice interaction, implemented on September 1, 2025, reinforcing documentation, testing, and labeling obligations across connected kitchen categories.

Value Chain Analysis

The China kitchen appliances value chain runs from upstream raw materials and components (steel, plastics, compressors, semiconductors, PCBs, sensors, heating elements, and packaging) into ODM/OEM and brand-led manufacturing clusters, then to omnichannel distribution that blends B2C online platforms, exclusive brand outlets, multi-brand stores, and B2B project sales (including commercial kitchens and property-linked orders). Compliance-driven design and verification sit across the chain, with energy-efficiency grades (GB 21456-2024 effective September 1, 2025) and energy-label implementation rules (in effect from November 1, 2025) shaping bill-of-materials selection, lab testing, and labeling workflows before products reach retail shelves and major online storefronts.

Midstream, larger incumbents strengthen resilience through structured supplier partnerships and ecosystem sourcing, while smaller players rely more heavily on contract manufacturing and spot procurement. Evidence of deeper supplier alignment includes procurement and supply-chain collaboration activity such as Midea engaging upstream partners for long-term coordination (for example, supplier collaboration visits and materials ecosystem partnerships referenced in 2025). In electronics-heavy smart appliances, lead-time and PCB availability become binding constraints, and supply-chain coordination tools can compress response times, as shown by reported use of shared-order collaboration mechanisms in China to coordinate PCB and assembly schedules for large orders. Downstream, the shift toward online-led retail, livestream commerce, and bundled kitchen suites increases the importance of last-mile delivery, installation capacity, and after-sales service networks as differentiators, particularly for large appliances and built-in cooking and ventilation packages.

Competitive Landscape

The China kitchen appliances market remains moderately concentrated, led by a few national players alongside a range of specialist and premium brands. Leading incumbents invest heavily in research and development, focusing on AI-powered automation and connected features that enable predictive maintenance and real-time optimization. Multi-brand strategies allow top players to serve budget, mid-tier, and premium segments, maintaining growth across categories. Specialist brands continue to capture significant offline share in core segments such as range hoods by leveraging high-performance designs and embedded intelligence tailored to cooking habits. These strategies collectively support durability, connectivity, and pricing power, enabling incumbents to defend market share while expanding into adjacent categories using established service and distribution networks.

White-space opportunities remain in under-penetrated categories such as dishwashers, where larger-capacity and sterile-drying models are driving adoption among new households. Product innovations that combine intelligent dosing and high-temperature cleaning are shifting consumer perceptions from convenience to hygiene-focused utility. Connected controls for ventilation and heating simplify daily use while delivering consistent, restaurant-quality results in home kitchens. Premium brands emphasize airflow optimization, precise baking performance, and low-noise operation to meet the needs of modern open-plan layouts. These pillars underpin ongoing premiumization and concentrate growth among incumbents with the intellectual property, testing capabilities, and service infrastructure required to scale effectively.

Regulatory compliance and digital manufacturing further differentiate market leaders. Expanded environmental standards and energy-labeling requirements increase costs for non-compliant products, prompting smaller brands to adjust supply chains and materials. At the same time, a national digital-transformation roadmap is accelerating the adoption of intelligent R&D and supply chain practices, improving speed to market and product quality for larger vendors. Together, these operational and regulatory moats reinforce market concentration while sustaining new-product development. Over time, these advantages support competitiveness as the market matures and value shifts from hardware toward connected, service-oriented experiences.

China Kitchen Appliances Industry Leaders

Midea Group

Haier Smart Home

Robam Appliances

Fotile Kitchenware

Joyoung

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory tightening and re-grading create clear whitespace for differentiated, compliant product refreshes across cooking, ventilation, and cleaning categories. With GB 44499-2024 (energy saving and environmental protection specifications) scheduled for implementation on September 1, 2026, and updated safety standards (GB/T 4706.1-2024 and GB/T 4706.30-2024) becoming mandatory from August 1, 2026, brands that can industrialize testing, documentation, and rapid SKU transitions have room to trade consumers up into higher-grade models, quieter ventilation, and premium built-in suites. The 2025 China Energy Label implementation rules (effective November 1, 2025, with transition provisions through November 1, 2027 for earlier-produced and imported stock) also support assortment pruning and clearer performance signaling at the point of purchase.

Smart kitchen opportunities increasingly center on interoperability and standardized interaction, not only app-level features. MIITs drafting activity around mandatory smart home interconnection standards and the implementation of GB/T 46456.1-2025 (smart home architecture and general requirements) from February 1, 2026 moves the market toward cross-brand compatibility, which reduces friction for whole-home bundles that include kitchen appliances. At the same time, policy mechanics are shifting: removal of certain kitchen categories from the national 2026 trade-in subsidy program increases the value of local programs and retailer-led promotions, while keeping emphasis on green and smart qualification criteria where local governments continue to include kitchen appliances. For manufacturers and channels, this combination supports focused plays in compliant premiumization, interoperable smart suites, and commercial kitchen replacement cycles, where durability, energy performance, and service readiness influence procurement decisions.

Recent Industry Developments

- May 2026: Midea Electronics Indonesia opened its third Midea Kitchen Pro Shop in Gading Serpong, Tangerang, in partnership with PT Era Bangunan. The store-led expansion strengthens owned retail reach and supports higher-value kitchen suite selling through in-person demonstrations and installation coordination, a model that can be mirrored across other markets served by Chinese appliance OEMs.

- April 2026: Electrolux Group and Midea Group formed a long-term strategic partnership in North America focused on food preservation and kitchen appliance innovation. The collaboration links a China-based manufacturing and R&D scale player with a global brand portfolio, supporting faster platform development and broader channel access for kitchen categories.

- November 2025: China updated the China Energy Label implementation rules, modernizing technical frameworks and testing criteria for products such as microwave ovens under the energy labeling system. The change tightens documentation and compliance execution for brands and sellers, influencing 2026 assortment planning and label-transition management for existing inventory.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is sized as the value of kitchen appliances sold in China, covering equipment used for cooking, food preparation, ventilation, cleaning, and related kitchen functions across household and non-household buyers.

Scope exclusions: We exclude unrelated home appliances that are not primarily used in the kitchen, along with standalone spare parts and repair-only services where they are not bundled with a product sale.

Segmentation Overview

- By Product (Value)

- Large Kitchen Appliances

- Refrigerators & Freezers

- Dishwashers

- Range Hoods

- Cooktops

- Ovens

- Other Large Kitchen Appliances

- Small Kitchen Appliances

- Food Processors

- Juicers & Blenders

- Grills & Roasters

- Air Fryers

- Coffee Makers

- Electric Cookers

- Toasters

- Electric Kettles

- Counter-top Ovens

- Other Small Kitchen Appliances

- Large Kitchen Appliances

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C / Retail

- Multi-brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- B2B (Direct from Manufacturers)

- B2C / Retail

- By Geography

- East China (Shanghai, Jiangsu, Zhejiang)

- South-Central China (Guangdong, Hunan, Hubei, etc.)

- North China (Beijing, Tianjin, Hebei, Shanxi, Inner Mongolia)

- Rest of China (Northeast,Southwest,Northwest)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to anchor key demand and supply signals that can be checked over time. We referenced public statistics and standards sources such as the National Bureau of Statistics of China, China Customs trade data, the Standardization Administration of China for relevant appliance standards, and China Energy Label program information for efficiency grading patterns. To connect these signals to market value, we also reviewed sources such as listed-company annual reports, investor presentations, industry association websites, and coverage from business press.

In addition, paid subscriptions were used selectively to speed up company financial checks, track news and corporate actions, and screen patent activity around product upgrades (for example, smart functions and energy saving designs). These inputs mainly helped validate product scope boundaries and the timing of market shifts, rather than directly setting the final totals. The desk sources listed above are illustrative only, and other public and internal reference points were also used for collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is really being sold, at what price bands, and through which channels in China, especially where published numbers disagree on retail versus manufacturer pricing. We spoke with brand-side leaders, distributors and retailers (including online-led sellers), and category specialists who track core kitchen categories and replacement-driven demand in both large and smaller cities. These discussions were used to confirm assumption ranges, fill gaps where public data is not detailed enough, and pressure-test the final model totals before sign-off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | |

| Mid tier: 48% | Functional/Unit leaders: 41% | |

| Smaller Players: 21% | Managers: 46% |

Market-Sizing & Forecasting

The sizing logic starts with a top-down build where appliance demand in China is reconstructed using category-level demand pools and adoption, then converted into value using price bands that reflect mix shifts. We tracked variables such as urban household formation and renovation cycles, replacement timing for installed appliances, online versus offline channel mix, efficiency upgrades tied to energy label preferences, and category penetration changes for items like dishwashers and range hoods. Once these drivers were set, the totals were corroborated with selective bottom-up approximations, including sampled average selling price ranges times unit volume indicators, alongside supplier and channel checks to confirm direction and scale.

For forecasting, scenario analysis was used because the market is sensitive to consumer sentiment, housing-related cycles, and the speed of premiumization. In each scenario, we adjusted the same core variables, such as category penetration, pricing mix, and channel shifts, and then cross-checked that the implied growth did not conflict with replacement behavior and realistic price progression. Where bottom-up information was missing for smaller categories or fragmented channels, gaps were handled by applying conservative ranges from interviews and then rebalancing to match the top-down demand pool outcome.

Data Validation & Update Cycle

Validation was done in layers so that no single input could swing the outcome. Model outputs were compared against independent signals, such as trade movement for relevant appliance groupings, public financial disclosures that indicate category momentum, and observed shifts in online sales importance, and then outliers were investigated. When a variance could not be explained by scope or timing, assumptions were revisited and respondents were re-contacted to confirm whether a one-time event or a structural change was being captured.

Each report goes through multi-step analyst review before publication, followed by an annual refresh cycle. If material events happen between refreshes, such as policy changes that alter appliance upgrades or a sudden pricing shock, interim checks are performed so the numbers stay aligned to the current market reality. Before delivery, an analyst completes a final pass to ensure the latest available data has been incorporated.

Mordor Intelligence's China Kitchen Appliances Product Market Size Compared With Other Published Estimates

Published market sizes for China kitchen appliances can differ by a wide margin because the scope and pricing basis are not always treated the same way. Differences show up most often when one estimate uses retail sales value and another uses manufacturer-level value, or when product boundaries expand into broader home appliance baskets.

By tracking pricing basis and refreshing scope rules with category experts, Mordor Intelligence keeps the number tied to kitchen-only appliances sold in China and avoids counting adjacent home appliance revenues that sit outside the kitchen use case.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 54.72 B (2025) | |

| Global Consultancy A | USD 151.50 B (2023) | Uses a broader definition that explicitly spans major and small appliances with retail channel value, which can pull in wider home-appliance revenues and retail markups. |

| Industry Research House B | USD 42.80 B (2024) | Anchors on a narrower product basket and a different base year, and the pricing basis is not clearly stated, which can understate value when premium mix and channel markups rise. |

The spread in the table mostly comes down to what gets counted as a kitchen appliance and whether the value is measured closer to retail sales or closer to the product value before retail margins. Using consistent category boundaries, time alignment, and interview-checked price logic helps keep the estimate explainable and repeatable when assumptions are updated year to year.

Key Questions Answered in the Report

What is the current size of the China kitchen appliances market and how fast is it growing?

The China kitchen appliances market size is estimated at USD 55.49 billion in 2026 and is projected to reach USD 62.14 billion by 2031 at a 2.29% CAGR.

Which product category leads the China kitchen appliances market and which is growing fastest?

Refrigerators and freezers lead with 34.56% of 2025 revenue, while counter-top ovens are the fastest growing at a 3.62% CAGR through 2031.

How is demand split between residential and commercial buyers in China?

Residential applications accounted for 73.41% of 2025 demand, while the commercial segment is projected to expand at a 3.35% CAGR through 2031.

Which region has the largest share of the China kitchen appliances market?

East China holds 32.63% of 2025 sales, and North China is the fastest growing at a 3.14% projected CAGR from 2026 to 2031.

What strategies are leading brands using to compete in the China kitchen appliances market?

Leaders invest in AI, connected ecosystems, and energy-efficient designs, while expanding scenario-based retail and strengthening service networks to defend share and drive premiumization.

Page last updated on: