China Inorganic Iodide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.12 Billion |

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 5.25 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Inorganic Iodide Market Analysis by Mordor Intelligence

The China Inorganic Iodide Market size is projected to expand from USD 4.12 billion in 2025 and USD 4.29 billion in 2026 to USD 5.25 billion by 2031, registering a CAGR of 4.13% between 2026 and 2031. Expansion is paced by pharmaceutical demand for potassium iodide, the migration of display-panel incentives that support optical-grade iodides, and government restocking of nuclear-preparedness tablets. Upstream control of 20% of global API output and about 80% of key starting materials keeps domestic converters well placed to absorb feedstock volatility while maintaining capacity utilization at chemical parks along the Bohai Rim and the Yangtze River Delta. Structural headwinds stem from Chile-centric iodine sourcing, LCD-to-OLED substitution, and tighter environmental standards that pressure smaller plants to relocate or shut down. Inventory cycles rather than feedstock swings currently drive domestic spot prices, underscoring the importance of working-capital discipline and long-term supply contracts.

Key Report Takeaways

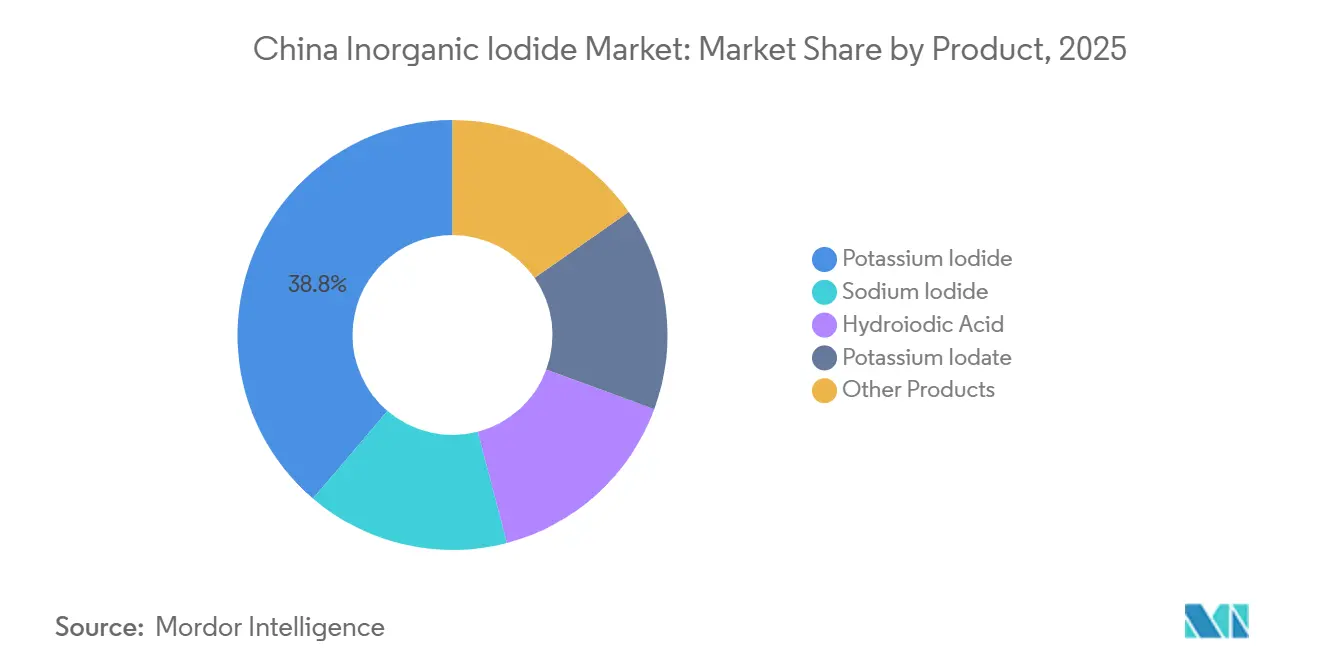

- By product, potassium iodide led with 38.76% of China Inorganic Iodide market share in 2025. Hydroiodic acid is forecast to post the fastest 5.18% CAGR during the forecast period (2026-2031) within the China Inorganic Iodide market size.

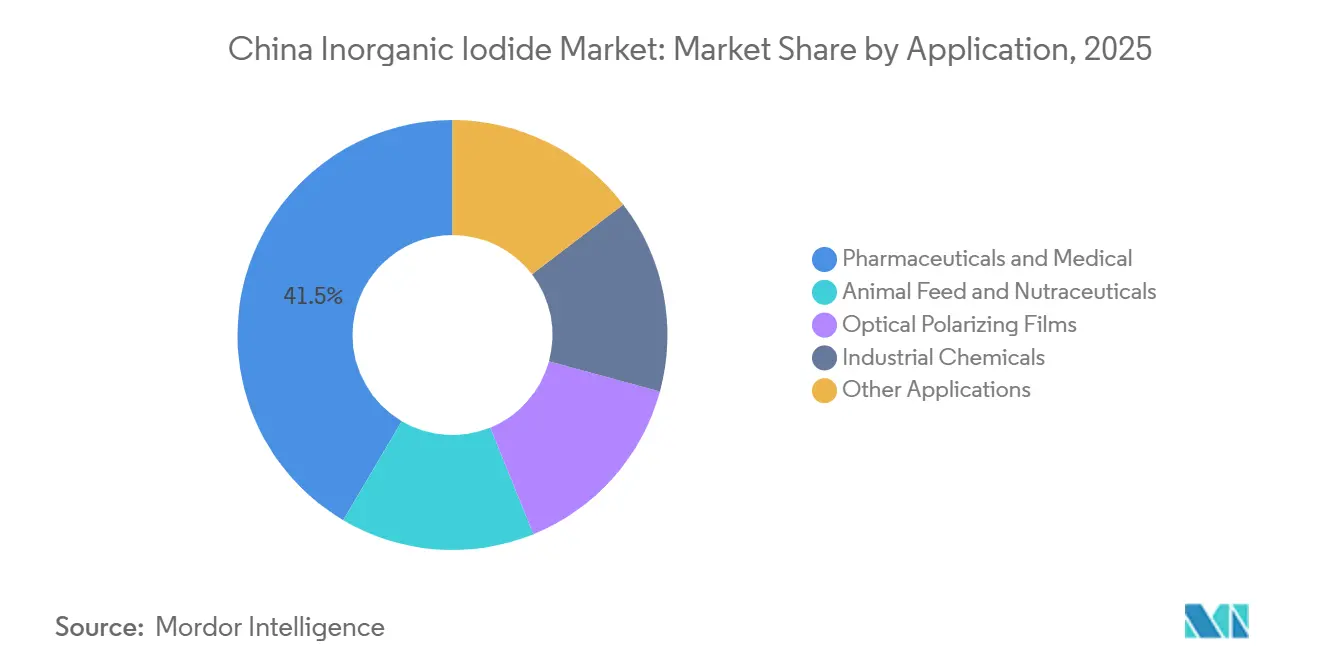

- By application, pharmaceuticals and medical captured 41.52% of revenue in 2025, while optical polarizing films are advancing at a 5.36% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Inorganic Iodide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging API output fueling iodide demand in China’s pharma clusters | +1.2% | Bohai Rim, Yangtze River Delta | Medium term (2-4 years) |

| Expansion of industrial feed mills boosting iodide-fortified premixes | +0.5% | National livestock belts | Long term (≥ 4 years) |

| Re-stocking of KI tablets for nuclear preparedness | +0.7% | Coastal provinces, near nuclear facilities | Short term (≤ 2 years) |

| Rising adoption of KI heat stabilizers in nylon and engineering plastics | +0.6% | East and South China chemical parks | Medium term (2-4 years) |

| Government incentives for LCD fabs sustaining polarizer demand | +1.1% | Bohai Rim, Yangtze Delta panel hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging API Output Fueling Iodide Demand in China’s Pharma Clusters

Converters anchored in Shandong and Jiangsu chemical parks benefit from integrated utilities and regulatory moats created by China’s 18% share of European Pharmacopoeia certificates, ensuring that potassium iodide and hydroiodic acid track API growth rather than GDP. The removal of tax rebates on certain fermentation feedstocks in 2024 raised costs, yet margin resilience persists because contrast media and thyroid drugs absorb price swings. High-purity iodides therefore enjoy demand insulation when commodity grades soften.

Expansion of Industrial Feed Mills Boosting Iodide-Fortified Feed Premixes

Animal nutrition accounts for roughly 7% of global iodine use and gains ground as salt-reduction campaigns lower dietary iodine intake[1]The Journal of Nutrition, “China Dietary Iodine Intake Revision 2024,” nutrition.org. Consolidating feed mills in Shandong and Henan are shifting from crude additives to pharmaceutical-grade potassium iodide, backed by Ministry of Agriculture residue limits that favor ISO 9001-certified suppliers. Because premix contracts turn over slowly, volume growth materializes over multiple seasons, yet intensified livestock farming locks in a durable vibration for the China Inorganic Iodide market.

Re-stocking of KI Tablets for Nuclear-Emergency Preparedness

WHO’s July 2025 dosing update sharpened focus on pre-distribution of tablets to households, schools, and evacuation sites[2] WHO, “Potassium Iodide Guidelines July 2025,” who.int. China’s 55 operating reactors sit mainly along the coast, where civil-defense bureaus replace expiring tablets on three- to five-year cycles. Episodic bids can tighten supplies, so producers with GMP tableting capacity and scored formulations win tender preference, supporting specialty demand inside the China Inorganic Iodide industry.

Rising Adoption of KI Heat Stabilizers in China’s Nylon and Engineering Plastics

Potassium iodide improves thermal stability in PA6 and PA66, and China’s engineering-plastics sector rides EV component penetration and tighter flammability codes. As more chemical output migrates into designated parks, access to centralized wastewater treatment and cheaper salt-based caustic soda enhances cost competitiveness. Automotive and electronics supply chains require two-year qualification runs, implying medium-term momentum for the China Inorganic Iodide market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-related side-effects triggering tighter use caps | -0.4% | Jiangsu, Zhejiang governance zones | Medium term (2-4 years) |

| Volatile imported iodine prices squeezing margins | -0.6% | Coastal converters, Shanghai, Qingdao | Short term (≤ 2 years) |

| LCD-to-OLED migration eroding display-sector demand | -0.8% | Bohai Rim, Yangtze Delta fabs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-Related Side-Effects Triggering Tighter Use-Level Caps

WHO’s updated contraindications highlight thyroid risks among the elderly, prompting Chinese regulators to examine consumer-goods iodine content and possibly list certain iodides as priority-control substances. Jiangsu’s draft pollutant plan outlines audits and potential phase-outs, raising compliance costs for smaller converters. Firms holding comprehensive toxicology files and ISO 9001 certification are positioned to retain access, while non-compliant plants risk exit, shaving a fraction from the China Inorganic Iodide market CAGR.

Volatile Imported Iodine Prices Squeezing Producer Margins

China relies on Chile for 83.2% of elemental iodine, yet domestic spot prices fell 0.86% quarter-over-quarter in Q4 2025 as inventory overhang outpaced feedstock inflation. Freight spikes linked to Red Sea disruptions doubled container rates, compressing working capital. Converters without long-term supply agreements or recycling loops suffer margin squeeze, trimming near-term momentum in the China Inorganic Iodide market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Pharmaceutical-Grade Potassium Iodide Anchors Share, Hydroiodic Acid Captures Specialty Growth

Potassium iodide held 38.76% China Inorganic Iodide market share in 2025, capturing demand from thyroid treatments, feed fortification, and civil-defense tablets. Hydroiodic acid is projected to rise at a 5.18% CAGR through 2031 on the back of acetic-acid carbonylation catalysts and graphene reduction, pushing its slice of the China inorganic iodide market size upward. Sodium iodide, potassium iodate, lithium iodide, and silver iodide together fill niche segments such as scintillator crystals and cloud-seeding agents. The decisive factor is purity: ultra-high-grade lots command 3-5 times commodity pricing, shielding earnings when bulk prices weaken.

Second-generation catalytic reduction and electrodialysis purification lower environmental overhead and match Jiangsu pollutant-governance demands, allowing compliant converters to raise output without breaching discharge limits. Because these technologies cut sulfur waste and heavy-metal residues, they also improve ESG profiles sought by multinational pharma buyers, reinforcing the stickiness of imports from the China Inorganic Iodide market.

By Application: Pharmaceuticals Dominate, Optical Films Post Steepest Trajectory

Pharmaceuticals and medical uses represented 41.52% of 2025 revenue and continue to set the floor for the China Inorganic Iodide market. Optical polarizing films should climb at a 5.36% CAGR to 2031 as LCD fabs keep running under subsidy umbrellas, despite OLED inroads. Animal feed and nutraceuticals grow steadily thanks to salt-reduction efforts that shift the iodine-adequacy burden toward fortified rations. Engineering plastics and biocides rely on performance plastics in EVs and hygiene products, adding incremental tonnage. Niche fields such as cloud seeding, radiographic scintillators, and analytical reagents remain fragmented but lucrative for specialty suppliers able to meet micro-batch customization. Integration with API producers ensures that pharmaceutical demand, rather than GDP volatility, remains the core engine for the China Inorganic Iodide industry.

Geography Analysis

Shandong leads production with coastal chemical parks in Weifang and Shouguang, housing expansions like Boyuan’s 4,000-ton line. Jiangsu hosts API clusters in Taizhou and Lianyungang, plus stricter environmental oversight, squeezing low-spec plants yet favoring ISO 9001 operators. Guangdong services display and electronics chains anchored in the Pearl River Delta, pulling in optical-grade iodides for panel fabrication. Inland Qinghai and Inner Mongolia provide lower-cost feedstock from salt-lake brines and coal-based caustic soda but lack dense customer bases, limiting them to bulk grades. Regional clustering means that shutdowns or logistics snags in a province ripple fast across the China inorganic iodide market. Consolidation inside chemical parks simplifies effluent control, but it also raises the capital bar for entrants, reinforcing the dominance of existing certified players.

Competitive Landscape

The China Inorganic Iodide market is moderately consolidated. Recycling and domestic brine recovery are white-space horizons; success could cushion the China inorganic iodide market against Chile supply shocks. Emerging clean-tech disruptors like IOFina’s produced-water extraction method promise carbon-lean iodine, a future competitive lever once China strengthens ESG procurement standards.

China Inorganic Iodide Industry Leaders

Zibo Wankang Pharmaceutical & Chemical Co., Ltd.

Shandong Boyuan Pharmaceutical Co., Ltd.

Jiangxi ShengDian Technology Co., Ltd.

Hebei Lingding Biotechnology Co., Ltd.

NIPPOH CHEMICALS CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: In a bid to bolster thyroid protection during nuclear or radiological emergencies, the World Health Organization rolled out revised guidelines on potassium iodide usage. These guidelines detail age-specific dosing, highlight contraindications, and stress the importance of pre-distributing potassium iodide to households, schools, hospitals, and evacuation centers.

- October 2024: China's Ministry of Commerce (MOFCOM) announced plans to extend anti-dumping tariffs on hydriodic acid from the United States and Japan for five years. A review found that removing the tariffs could damage the domestic industry.

China Inorganic Iodide Market Report Scope

Iodine forms iodide compounds with almost all elements except for the inert elements. The most important class of iodine compounds is commercially available inorganic iodides. Hydriodic acid, sodium iodide, potassium iodide, and potassium iodate are the inorganic iodides discussed in this report.

The Chinese Inorganic Iodide market is segmented by product and application. By product, the market is segmented into potassium iodide, sodium iodide, potassium iodate, hydroiodic acid, and other products. By application, the market is segmented into animal feed and nutraceuticals, pharmaceuticals and medical, optical polarizing films, industrial chemicals, and other applications. For all the above segments, market sizing and forecasts have been provided on the basis of value (USD).

| Potassium Iodide |

| Sodium Iodide |

| Hydroiodic Acid |

| Potassium Iodate |

| Other Products |

| Animal Feed and Nutraceuticals |

| Pharmaceuticals and Medical |

| Optical Polarizing Films |

| Industrial Chemicals |

| Other Applications |

| By Product | Potassium Iodide |

| Sodium Iodide | |

| Hydroiodic Acid | |

| Potassium Iodate | |

| Other Products | |

| By Application | Animal Feed and Nutraceuticals |

| Pharmaceuticals and Medical | |

| Optical Polarizing Films | |

| Industrial Chemicals | |

| Other Applications |

Key Questions Answered in the Report

What drives potassium-iodide demand in China after 2026?

Growth in API output, nuclear-preparedness restocking, and feed-premix fortification keep uptake rising at about 4% a year.

How will LCD-to-OLED migration affect iodide sales?

Bulk polarizer demand falls, but specialty iodides for OLED materials partly offset the drop, keeping overall volume stable through 2031.

Which provinces dominate production?

Shandong and Jiangsu host the largest certified plants inside designated chemical parks, benefiting from port access and downstream clusters.

What risks threaten converter margins?

Dependence on Chilean iodine, freight volatility, and tighter environmental caps in Jiangsu and Zhejiang can compress spreads quickly.

Are domestic iodine-recovery projects scaling?

Seaweed and brine initiatives exist but remain sub-scale; most feedstock still arrives via imports from Chile.

What is the current market size of China Inorganic Iodide Market?

The China Inorganic Iodide Market size is projected to expand from USD 4.12 billion in 2025 and USD 4.29 billion in 2026 to USD 5.25 billion by 2031, registering a CAGR of 4.13% between 2026 and 2031.

Page last updated on: