Azodicarbonamide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

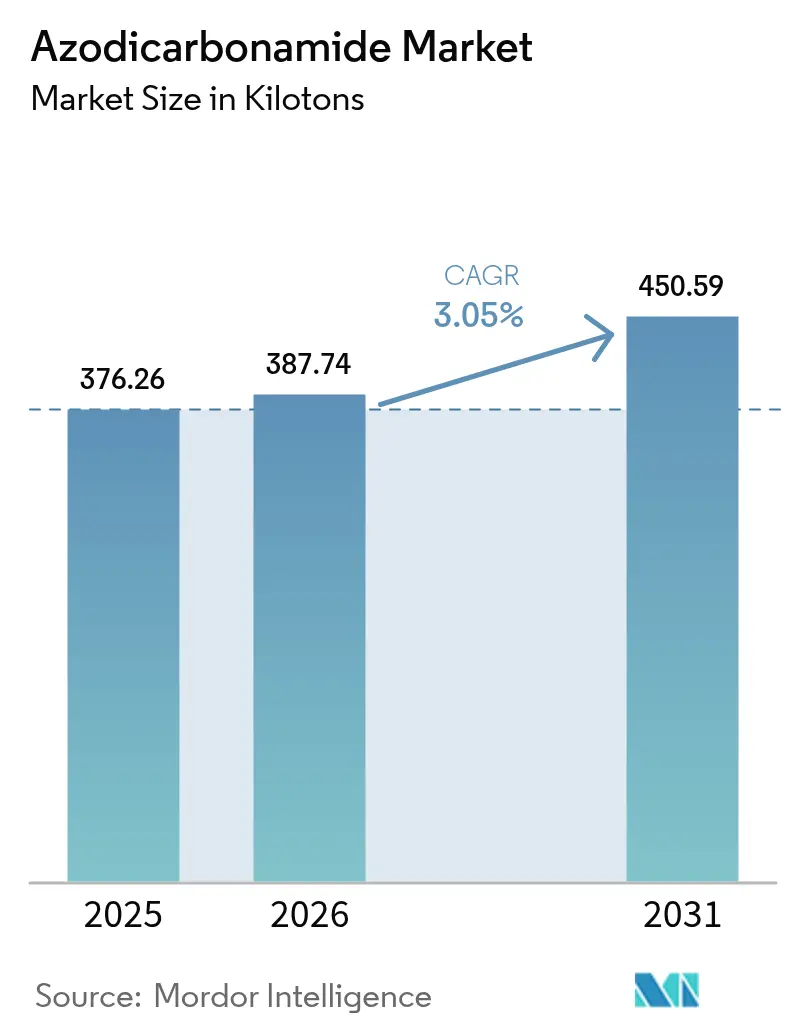

| Market Volume (2026) | 387.74 kilotons |

| Market Volume (2031) | 450.59 kilotons |

| Growth Rate (2026 - 2031) | 3.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Azodicarbonamide Market Analysis by Mordor Intelligence

The Azodicarbonamide Market size was valued at 376.26 kilotons in 2025 and estimated to grow from 387.74 kilotons in 2026 to reach 450.59 kilotons by 2031, at a CAGR of 3.05% during the forecast period (2026-2031). Continued uptake in industrial foam manufacturing keeps the azodicarbonamide market on a steady upward path, even as food-use bans accelerate in the United States and the European Union. Cost-effective gas-yield performance underpins the compound’s resilience: its 220–230 ml/g gas generation capacity produces lighter, stronger foams at lower formulation cost than alternatives, a decisive advantage for automotive, construction, and packaging processors. Manufacturers with vertically integrated hydrazine and urea feedstock lines mitigate input volatility, an edge that proved critical when global urea spot prices fell 10.99% year-over-year in April 2024. Regulatory divergence intensifies regional specialization: while California’s Food Safety Act eliminates bakery usage from January 2027, industrial customers in Asia, the Middle East, and Africa expand purchases for lightweight electric-vehicle (EV) insulation and vegan leather substrates, cushioning the global azodicarbonamide market against food-sector losses.

Key Report Takeaways

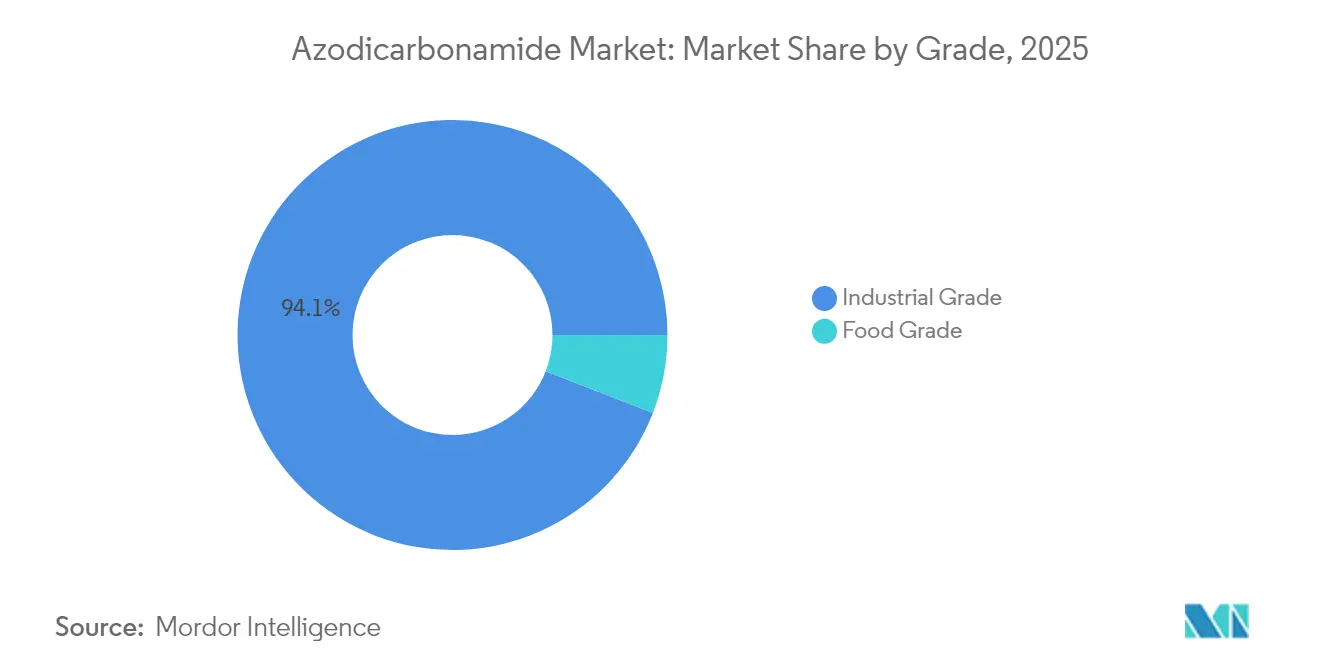

- By grade, Industrial Grade held 94.10% of the azodicarbonamide market share in 2025; the same grade is projected to advance at a 3.17% CAGR through 2031.

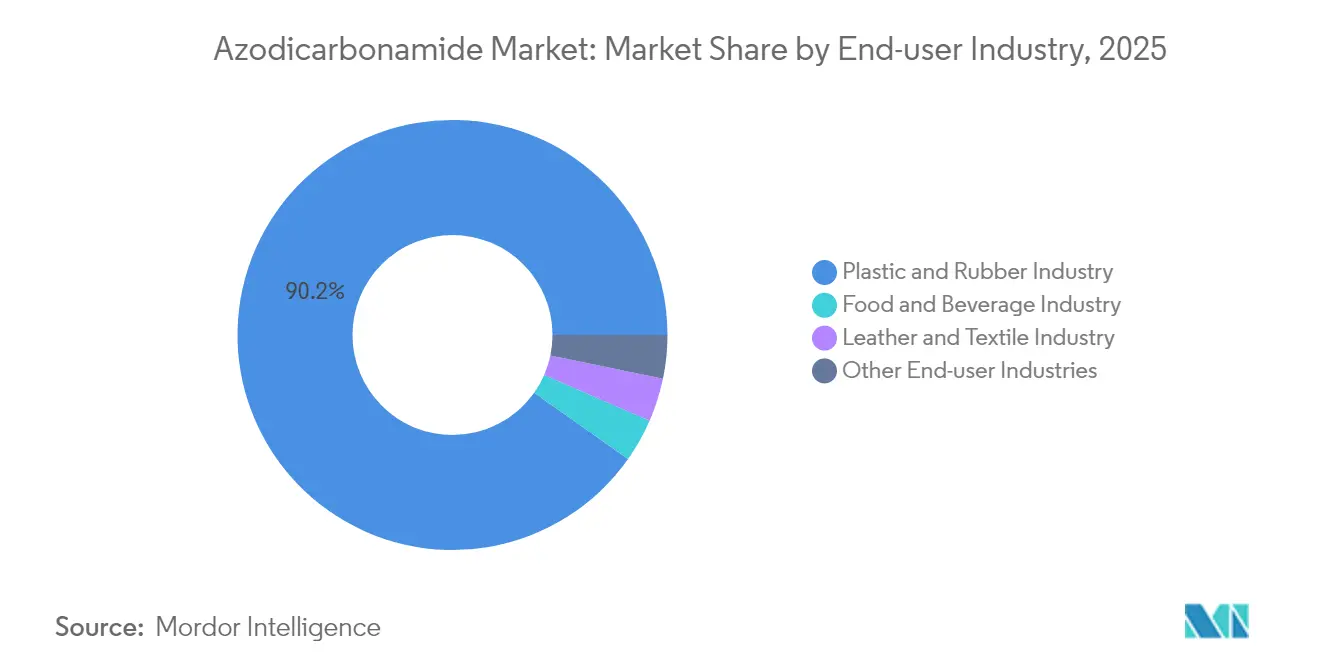

- By end-user industry, the Plastic and Rubber Industry captured 90.21% of the azodicarbonamide market size in 2025 and is forecast to post the fastest 3.21% CAGR during 2026-2031.

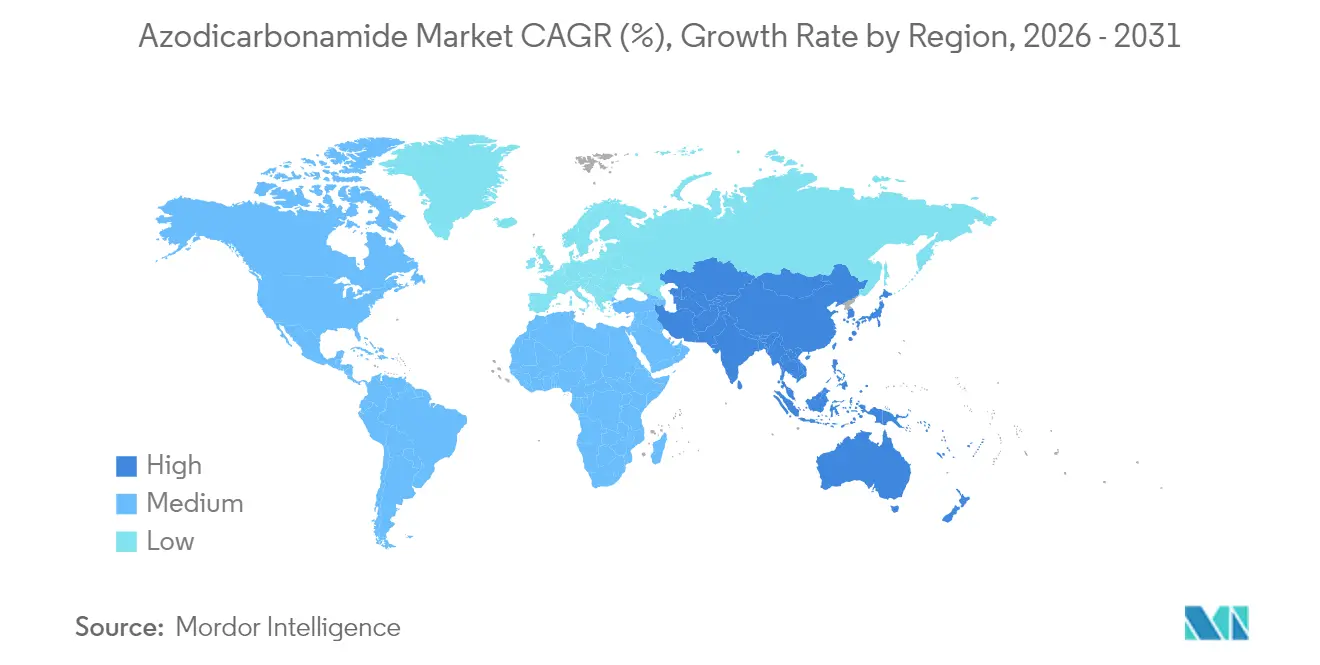

- By geography, Asia-Pacific commanded 73.08% of global volume in 2025, and is expected to log the quickest 3.41% CAGR through 2031 as EV-related foam demand accelerates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Azodicarbonamide Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in plastic and rubber foam manufacturing | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Rising bakery demand for dough-conditioning additives | +0.3% | Global, declining in EU and Australia | Short term (≤ 2 years) |

| Cost-effective, high-gas-yield blowing agent economics | +0.8% | Global | Long term (≥ 4 years) |

| Lightweight EV insulation and packaging applications | +0.6% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Vegan leatherette production for fashion industry | +0.2% | Global, concentrated in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Plastic and Rubber Foam Manufacturing

Industrialization across Asia sustains double-digit expansion in polymer-foam capacity, a trend that translates directly into higher azodicarbonamide market consumption because the blowing agent’s narrow 220–225 °C decomposition window allows precise density control essential for automotive crash-absorption pads and building-envelope insulation. Chinese chemical clusters increasingly supply value-added foams rather than commodity grades, capturing margins that insulate producers from purely price-based competition. As North American processors shift procurement toward lightweight parts for electric SUVs and trucks, cross-regional demand balances and reduces the sector’s exposure to any single geography. Equipment upgrades in Vietnam and Indonesia further broaden the azodicarbonamide market base by bringing small and mid-size converters into export-oriented supply chains. Finally, ongoing innovation in supercritical-fluid foaming complements, rather than replaces, chemical blowing methods, keeping azodicarbonamide indispensable for fine-cell structures that mechanical techniques cannot yet replicate.

Cost-Effective, High-Gas-Yield Blowing-Agent Economics

Azodicarbonamide liberates up to 230 ml/g of gas, more than twice that of typical endothermic agents, which lets processors achieve target foam densities with fewer additive kilograms and shorter extrusion cycles. Integrated producers in China and South Korea capitalize on hydrazine-to-azodicarbonamide synergies, shaving unit costs and buffering margins during feedstock swings. In Europe, where energy prices remain elevated, the compound’s lower activation temperature compared with exothermic alternatives reduces oven residence times and electricity consumption, an operational saving that resonates with manufacturers pursuing Scope 3 emission reductions. As urea prices stabilized in early 2025, converters locked in long-term supply agreements, reinforcing the azodicarbonamide market’s pricing floor and improving visibility for capacity-expansion decisions. The absence of specialized handling equipment requirements—unlike hydrofluorocarbon or hydrofluoro-olefin systems—adds a further cost edge that favors small and medium processors lacking extensive capital budgets.

Lightweight EV Insulation and Packaging Applications

Global EV sales surpassed 17 million units in 2024, spurring demand for flame-retardant, low-density foams that insulate battery packs while meeting stringent UL-94 V-0 standards. Azodicarbonamide-blown polyolefin foams demonstrate superior fire-smoke-toxicity profiles versus traditional polyurethane, aligning with automakers’ thermal-runaway mitigation strategies. Battery module engineers also value the compound’s uniform cell structure, which distributes mechanical stress during charge-discharge cycles, extending pack life. In packaging, e-commerce brands adopt azodicarbonamide-based polyethylene inserts that cushion fragile goods while trimming shipment weight, thereby cutting logistics emissions. The incremental uptake in Europe’s EV supply chain offsets the region’s near-total elimination of food-grade azodicarbonamide, maintaining a stable azodicarbonamide market baseline while opening higher-margin industrial niches.

Vegan Leatherette Production for Fashion Industry

Luxury and mass-market fashion labels accelerate commitments to cruelty-free products, scaling synthetic leather volumes that require consistent, closed-cell foams to replicate natural hide grain. Azodicarbonamide provides the micro-cellular matrix underpinning polyurethane-coated fabrics, and its compatibility with emerging bio-based PBS substrates positions the additive for long-term growth within sustainability-oriented portfolios. Asian contract manufacturers supply over 80% of global synthetic leather, reinforcing the continent’s centrality to the azodicarbonamide market. Premium apparel lines command price premiums that absorb recent raw-material fluctuations, ensuring stable demand despite regulatory uncertainty in unrelated food uses. Concurrent research and development targets odor reduction in finished goods, a milestone believed achievable by refining azodicarbonamide particle size distribution rather than switching to less efficient blowing agents.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food-use bans in EU and Australia | -0.8% | EU, Australia, expanding to North America | Short term (≤ 2 years) |

| Raw-material price volatility (urea, hydrazine) | -0.4% | Global | Medium term (2-4 years) |

| Clean-label enzyme-based dough improvers gaining share | -0.3% | Global, accelerated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Food-Use Bans in EU and Australia

The regulatory tide turned decisively in 2025 when China’s GB 2760-2024 standard deleted azodicarbonamide from the national food-additive list, following earlier prohibitions in the EU and Australia[1]Food Compliance International, “CFSA Implements Standard GB 2760-2024,” foodcomplianceinternational.com. California, New York, and Pennsylvania will enforce statewide bans from 2027, effectively erasing bakery demand across three of the largest U.S. consumer markets. Multinational chains pre-emptively reformulated inventories to avoid supply-chain complexity, removing 15-20% of pre-existing global food-grade volume. Smaller regional bakeries face higher costs when switching to enzyme systems, but liability considerations outweigh the economic benefits of continued azodicarbonamide use. The cumulative effect trims near-term growth in the azodicarbonamide market until industrial uptake in foam and textile applications fills the gap.

Clean-Label Enzyme-Based Dough Improvers Gaining Share

Novozymes’ Fungamyl and similar alpha-amylase blends facilitate softer crumb texture without chemical residues, matching consumer expectations for “kitchen cupboard” ingredients. While enzymatic solutions cost up to 30% more per kilo than azodicarbonamide, premium bakery segments accept the mark-up for transparent labels and regulatory certainty. European retailers increasingly blacklist additives carrying E-number 927a, accelerating enzyme penetration even in price-sensitive private-label categories. Concurrent marketing campaigns highlight clean-label credentials, amplifying demand pull and constricting the remaining food-grade azodicarbonamide market. Nonetheless, azodicarbonamide retains a niche in select pastry lines requiring instantaneous gas release not easily replicated by biological catalysts, ensuring a residual though declining revenue stream.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Industrial Applications Drive Market Evolution

Industrial Grade represented 94.10% of total volume in 2025, a dominance expected to widen as the segment grows at a 3.17% CAGR through 2031. Manufacturers value the grade’s low impurity profile, which minimizes scorch risk during PVC and EVA processing and supports end-use compliance in automotive interiors. Larger converters negotiate annual contracts directly with integrated Asian producers, locking in supply and reaping scale discounts that smaller buyers cannot match. Combined with capital investments in new continuous-foaming lines across Vietnam, Thailand, and India, the trend secures Industrial Grade’s primacy in the azodicarbonamide market.

Food Grade continues a structural decline amid sweeping bakery bans, yet survives in regions lacking prohibitions, notably parts of Southeast Asia and the Middle East. Multinational food groups standardize enzyme-only recipes worldwide to streamline quality-assurance protocols, relegating Food Grade to niche local bakeries and specialty confectionery formats. Even here, volumes fall as cost parity between enzymes and azodicarbonamide narrows, eroding the compound’s price advantage and further shrinking its share of the azodicarbonamide market size.

By End-User Industry: Plastic and Rubber Dominance Intensifies

The Plastic and Rubber Industry accounted for 90.21% of consumption in 2025 and is projected to register the fastest 3.21% CAGR during 2026-2031. Automotive, footwear, and flexible-packaging converters prize azodicarbonamide for its fine-cell morphology and thermal stability, features that alternative blowing agents struggle to replicate without raising formulation costs. Investment announcements from specialty-chemical leaders in Green Bay and Shanghai underscore faith in sustained polymer-foam momentum. As EV manufacturers swap metal for polyolefin and elastomeric foams, demand for high-performance blowing agents will scale proportionally, reinforcing the azodicarbonamide market’s industrial focus.

Food and Beverage usage shrinks in line with regulation, yet the Leather and Textile Industry maintains stable offtake for synthetic leather backings adopted by global athletic-footwear brands. In pharmaceuticals, azodicarbonamide’s controlled gas release enables porous tablet matrices for rapid drug dissolution, a niche but profitable channel that offsets partial losses elsewhere. Collectively, these diversified industrial applications shield overall azodicarbonamide market share from food-related attrition.

Geography Analysis

Asia-Pacific’s 73.08% grip on 2025 volume reflects the region’s unmatched combination of feedstock proximity, skilled labor, and vertically integrated processing hubs. Regional producers capitalize on efficient logistics corridors linking coastal chemical complexes to downstream converters in Guangdong, Zhejiang, and Tamil Nadu. Longer term, environmental-compliance upgrades in China aim to reposition national plants as global benchmarks for low-emission fine-chemicals manufacturing, preserving cost competitiveness while satisfying tightening ESG disclosure requirements.

North America’s share contracts after California’s Food Safety Act takes effect in 2027 but rebounds as EV, aerospace, and building-insulation projects ramp up. Canada’s push for zero-emission buildings spurs polyurethane-foam retrofits where azodicarbonamide delivers necessary R-values at reduced density, lowering material usage and installation weight. The azodicarbonamide market size for industrial customers thus offsets bakery exits, illustrating the additive’s ability to pivot across end-markets without fundamental chemistry changes.

Europe, an early mover on food bans, now focuses on technical-grade applications. German and French compounders develop bio-based EVA foams for sports-equipment brands relying on azodicarbonamide to achieve micro-cell structures. Stricter CO₂ pricing under the EU Emissions Trading System intensifies the search for energy-efficient reagents; azodicarbonamide’s moderate activation temperature provides a process advantage that sustains its presence in European factories.

South America and the Middle-East and Africa trail in absolute volume but post above-average industrial-sector CAGRs as infrastructure spending accelerates. Brazil’s petrochemical investments target domestic substitution of imported foams, while Saudi Arabia’s Vision 2030 diversification drives demand for thermal-insulation materials.

Value Chain Analysis

Azodicarbonamide (ADCA/ADC) production sits upstream of polymer-foam and specialty plastics compounding, with core inputs centered on urea and hydrazine hydrate routes, followed by oxidation steps. Process safety, waste handling, and permitting needs around hydrazine handling act as practical entry barriers and influence where capacity is located. Catalyst systems and process know-how, including continuous oxidation and impurity control approaches reflected in technical disclosures, help differentiate commodity output from tighter-spec industrial grades used in automotive, construction insulation, and footwear foams.

Downstream, industrial converters and compounders typically procure ADCA through distributors or direct annual contracts with integrated producers. This structure can buffer feedstock swings and help maintain consistent gas-yield performance needed for density control. Food-grade flows face tighter limits from regulatory divergence, and compliance work, including documentation, testing, and customer audits, becomes a gating function for access to specific end markets. In the United States, ADA remains permitted under 21 CFR 172.806, but shifting review activity increases the importance of traceability and specification management for suppliers serving food-adjacent channels.

Competitive Landscape

Competition remains moderately fragmented. Chinese producers leverage scale and backward integration into hydrazine to lead on cost, while Japanese firms prioritize ultra-high-purity grades for semiconductor-packaging foams. Korean and Taiwanese suppliers occupy a mid-price segment, balancing quality with competitive pricing. Regulatory adaptability becomes a key differentiator. Firms holding dual production lines, one food-grade, one industrial, rapidly pivot volume between segments as legislation evolves, maintaining utilization above 85%. Those lacking flexibility risk stranded assets, especially in Western jurisdictions phasing out food applications. Overall, operational agility paired with raw-material control defines winner profiles in the azodicarbonamide market.

Azodicarbonamide Industry Leaders

Ajanta Group

Jiangsu SOPO (Group) Co. Ltd

Jiangxi Selon Industrial Co. Ltd

Kumyang Co., Ltd.

Otsuka Chemical Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Industrial-grade demand creation remains concentrated in foam-intensive value chains where ADCA provides high gas yield (up to about 230 ml/g) and a controllable decomposition window for fine-cell structures. That performance underpins opportunities in higher-spec formulations, including low-odor or modified grades for automotive interiors, footwear, and packaging. The market also shows whitespace in supply reliability and qualification services, particularly as Western production retrenched under EU chemicals scrutiny, with ADCA having SVHC status. This has increased dependence on Asia-based suppliers that can meet tighter impurity limits and documentation requirements for global OEM and tier supply chains.

On the food side, activity in the United States continues to be shaped by active reassessment and patchwork restrictions rather than broad global harmonization. In May 2026, the FDA issued a Request for Information on azodicarbonamide use in food and food contact contexts, while ADA remains authorized as a direct food additive under 21 CFR 172.806 (with defined use limits). Together, these conditions create near-term opportunity for suppliers offering compliance-ready, segregated supply chains, as well as for downstream users accelerating reformulation and substitution planning. Industrial applications remain the primary commercialization pathway.

Recent Industry Developments

- May 2026: The US Food and Drug Administration published a Request for Information to gather data on azodicarbonamide (ADA) use and safety in food and food contact contexts. The action raised the compliance bar for suppliers serving food-adjacent channels and increased the value of traceable specifications and documentation while industrial-grade demand remains the core volume driver.

- February 2026: Kumyang Co., Ltd. started new production operations at its Lianyungang facility in China, linking the site with its existing Jinyang operations in Inner Mongolia. The move strengthens the company's ability to supply industrial-grade blowing agent demand with improved operational scale and logistics options for export-oriented customers.

- February 2025: China implemented GB 2760-2024, delisting azodicarbonamide from the permitted food-additive list. This regulatory shift accelerated domestic reallocation toward industrial-only applications and pushed food-use demand further toward reformulation alternatives.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers azodicarbonamide supplied for industrial and approved food-related uses, where demand is linked to polymer processing and other end-use manufacturing that consumes this chemical.

Scope exclusions: We exclude downstream finished goods value (for example, finished foam sheets, footwear, and baked products) and count only azodicarbonamide volumes.

Segmentation Overview

- By Grade

- Industrial Grade

- Food Grade

- By End-User Industry

- Plastic and Rubber Industry

- Food and Beverage Industry

- Leather and Textile Industry

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and build a practical demand map before any modeling started. We relied on public references such as chemical safety and regulatory documents from agencies like the US FDA and the European Commission, plus customs and trade statistics portals and national statistics offices for industrial output.

In parallel, we reviewed technical papers and standards discussions that describe typical use rates and substitution behavior in polymer foaming and processing. This background supports translating end-use activity into azodicarbonamide requirements. Company annual reports, investor decks, and credible industry press were also scanned to understand capacity additions, plant shutdowns, and regional supply shifts. Where needed, paid subscriptions supporting company financials and intelligence, shipment-level import export checks, and patent databases were used to confirm timelines and product positioning. The sources mentioned here are illustrative and not exhaustive, since additional references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were run with a mix of manufacturers, distributors, compounders, and end-use formulators to confirm how demand is formed and how it tracks polymer production. For a global market like this, we validated inputs across APAC, EMEA, and the Americas so regional regulation impacts and local supply constraints could be reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | APAC: 43% |

| Mid tier: 43% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 22% | Managers: 48% | Americas: 21% |

Market-Sizing & Forecasting

Market size was constructed mainly through a top-down logic that starts from regional polymer processing and foamed-plastics activity, then applies realistic penetration and use-rate assumptions for azodicarbonamide in those formulations. To keep the output grounded, we tested totals with selective bottom-up approximations, including sampled supplier volumes by region and application-level checks using typical dosage ranges.

Key inputs used in the model include regional production trends in plastics and rubber, the split between industrial grade and food grade consumption, observed shifts tied to regulatory restrictions in food applications, and trade flow signals that indicate import dependence versus local supply. We also tracked capacity and operating-rate changes for major production hubs, since supply tightness can change apparent consumption from one year to the next. Forecasts were built using scenario analysis, where drivers like industrial foam demand growth and the pace of food-use displacement were stress-tested with expert feedback. When bottom-up visibility was limited in smaller countries, gaps were handled by using regional proxies based on comparable end-use intensity and trade patterns, then applying interview-based correction factors.

Data Validation & Update Cycle

Outputs were checked through several steps so that one unusual input did not distort the final view. We compared modeled demand against independent signals like trade balances, capacity utilization direction, and expected grade mix by end use, then reworked outliers before internal sign-off.

If a variance could not be explained by a clear driver, analysts re-contacted sources and re-checked assumptions like use rates and regional shares. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, plant disruptions, or large capacity expansions. Before delivery, a final pass is completed to ensure the latest public data and field inputs are reflected.

Mordor Intelligence's Azodicarbonamide Market Sizing Compared With Other Published Estimates

Published market numbers for azodicarbonamide can differ because some authors size the market in revenue while others size it in physical volume, and because adjacent blowing agents or broader chemical additives sometimes get grouped together. Timing also matters, since currency conversion, unit price assumptions, and the year used for normalization can move a headline figure even when demand is stable.

In this study, the main gap driver is scope discipline, since only azodicarbonamide volumes are counted by grade and end-use. The forecast is anchored to polymer processing demand signals and trade checks, which is why the baseline is shown in kilo tons by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.00 B (2025) | |

| Global Consultancy A | USD 1.70 B (2025) | Uses a revenue build that likely assumes blended selling prices and may include broader chemical foaming agents or related polymer additives, which inflates the total versus a pure azodicarbonamide-only count. |

| Industry Publisher B | USD 0.38 B (2025) | Revenue estimate appears to be derived from high-level price assumptions without transparent grade mix and regional validation, so the implied volume-to-price conversion may not match observed trade and end-use intensity. |

The spread is mostly explained by whether the market is treated as a volume pool tied to polymer output, or as a revenue pool that depends heavily on assumed prices and what is included around the core chemical. By keeping assumptions traceable to grade mix, end-use pull, and cross-checkable trade signals, the final number stays repeatable even when pricing and regulation move year to year.

Key Questions Answered in the Report

How large will global demand for azodicarbonamide be by 2031?

Volume is projected to reach 450.59 kilo tons by 2031, up from 387.74 kilo tons in 2026.

Which region dominates consumption?

Asia-Pacific held 73.08% of 2025 volume thanks to integrated supply chains and strong industrial demand.

Why is usage in bakery products declining?

Food-safety regulations in the EU, China, and several U.S. states prohibit azodicarbonamide in dough, pushing bakeries toward enzyme alternatives.

What drives industrial-grade growth?

Automotive, construction, and packaging firms prefer azodicarbonamide for its high gas yield and consistent cell structure in lightweight foams.

How will EV adoption influence demand?

Battery insulation and structural foams for electric vehicles are expanding at more than 3% CAGR, creating new industrial demand streams.

Is the competitive landscape concentrated?

No. The top five suppliers control about 30% of global volume, keeping the market fragmented and price-competitive.

Page last updated on: