Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

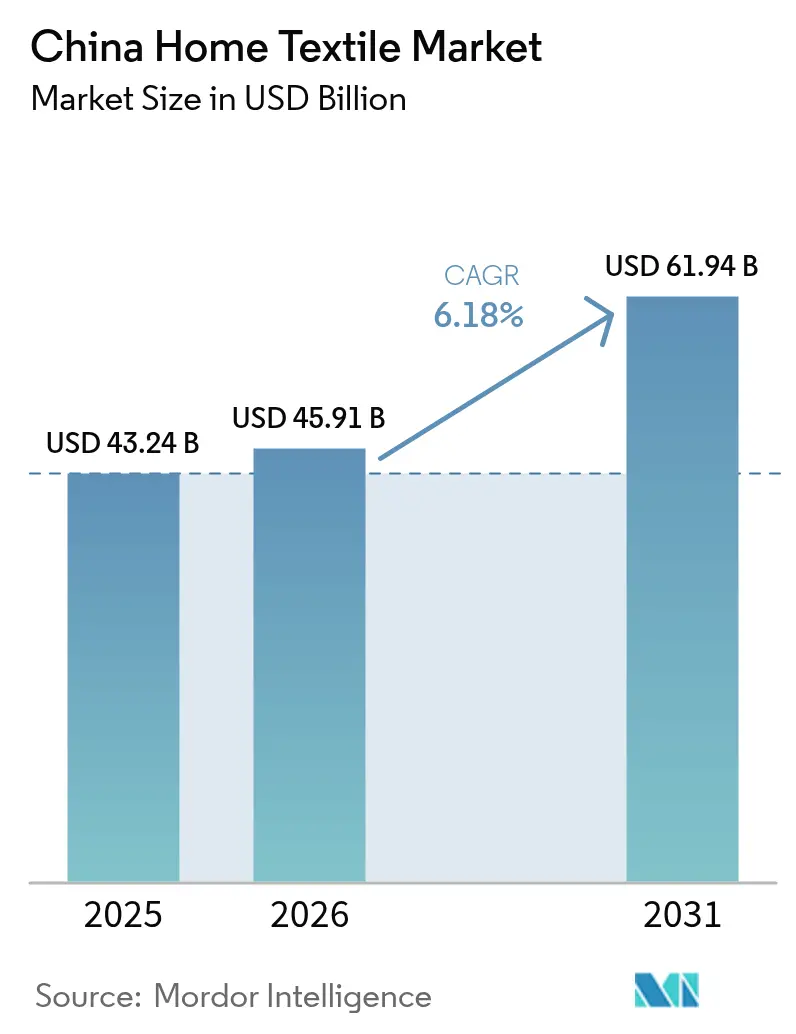

| Base Year Market Size (2025) | USD 43.24 Billion |

| Market Size (2026) | USD 45.91 Billion |

| Market Size (2031) | USD 61.94 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

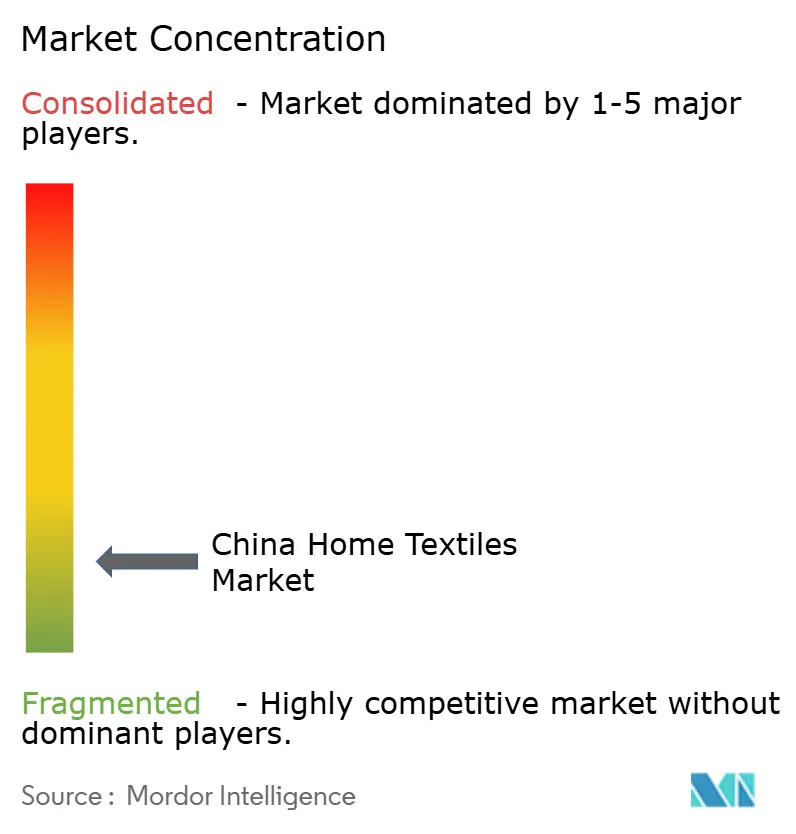

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Home Textile Market Analysis by Mordor Intelligence

The China Home Textile Market size was valued at USD 43.24 billion in 2025 and estimated to grow from USD 45.91 billion in 2026 to reach USD 61.94 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031).

Continued middle-class expansion, sustained urban migration, and rapid digital-commerce uptake collectively reinforce steady demand in the China home textile market, even as cotton-price volatility and international sourcing restrictions create cost uncertainties. Mobile-first shoppers now treat textiles as affordable lifestyle upgrades, pushing branded suppliers toward faster style refreshes and eco-labeled fabrics. Platform retailers use data analytics to shorten design-to-market cycles, while manufacturers invest in AI-assisted production to counter rising labor costs. Across distribution, offline stores retain tactile-product appeal, but their dominance erodes each year as live-streaming and same-day delivery turn smartphones into primary purchase engines. Lastly, corporate ESG targets, government carbon-neutrality mandates, and intensifying traceability rules elevate demand for natural and recycled fibers, accelerating the transition from conventional cotton to bamboo, hemp, and other niche naturals.

Key Report Takeaways

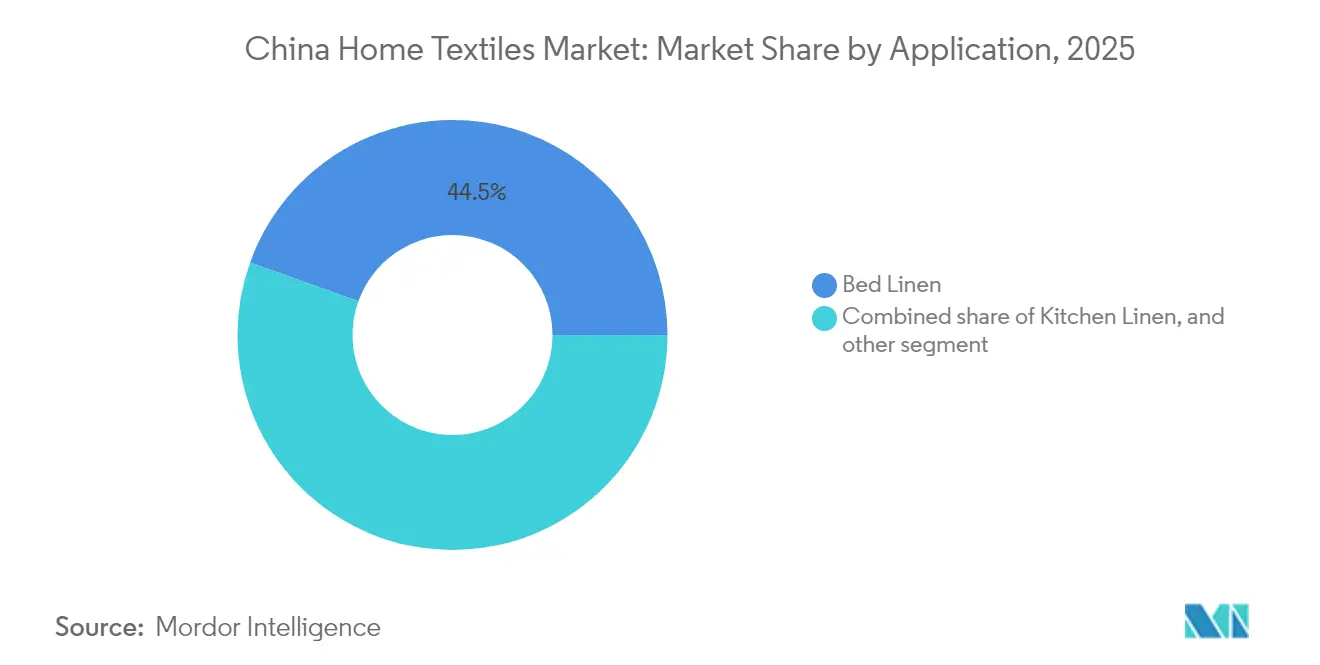

- By application, bed linen led with 44.52% of the China home textile market share in 2025; carpets and area rugs are forecast to grow at an 8.45% CAGR through 2031.

- By material, cotton held 48.93% of the China home textile market share in 2025, whereas bamboo and other niche naturals are projected to expand at an 10.84% CAGR to 2031.

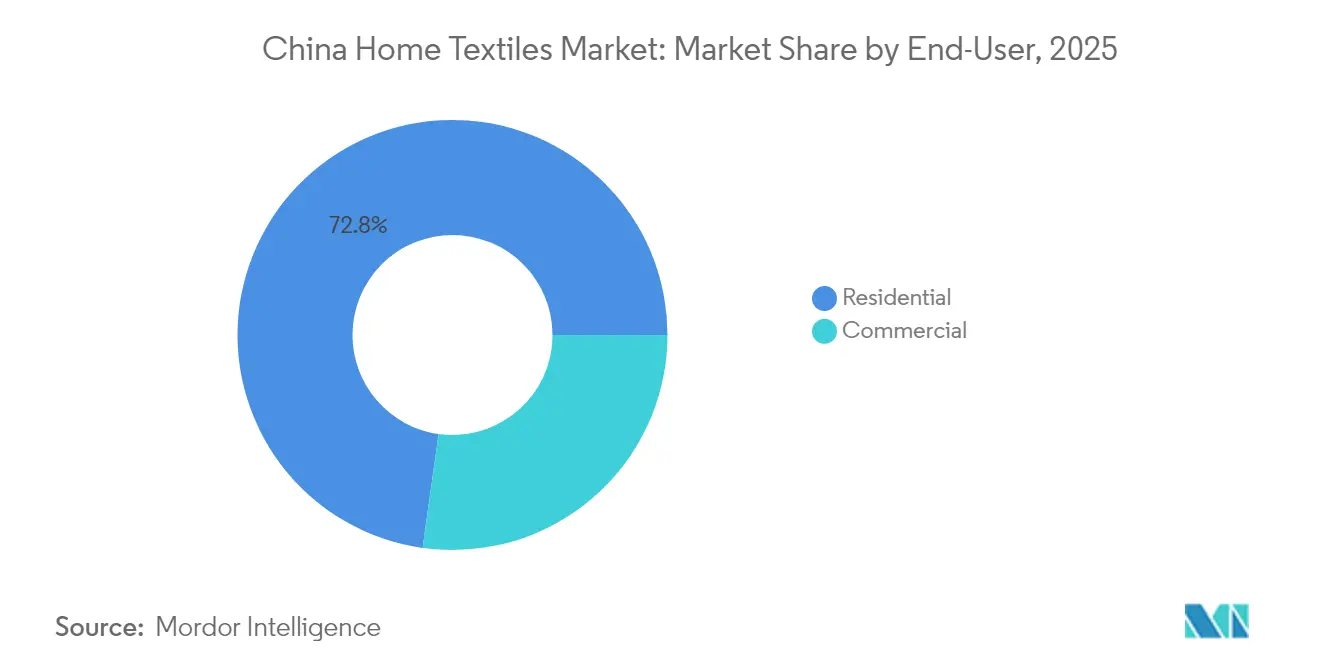

- By end-user, residential accounted for 72.78% of the China home textile market size in 2025, while the commercial/hospitality segment advances at an 8.05% CAGR to 2031.

- By distribution channel, offline retail retained 63.85% of the China home textile market size in 2025, but online platforms are expanding at a 14.72% CAGR.

- By geography, East China captured 35.05% of the China home textile market share in 2025, yet Southwest China is expected to post a 9.92% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & urbanization | +2.1% | Nationwide, the highest in tier-2/3 cities | Medium term (2-4 years) |

| Expansion of e-commerce & omnichannel retail | +1.8% | Nationwide, strongest in East & South-Central China | Short term (≤ 2 years) |

| Government push for sustainable fibers & green manufacturing | +1.2% | Policy-driven in Xinjiang and coastal provinces | Long term (≥ 4 years) |

| Digital design & AI-driven on-demand production | +0.9% | East China hubs with spill-over to Southwest | Medium term (2-4 years) |

| Domestic tourism-led hotel linen upgrade cycle | +0.7% | Tourism clusters in Beijing, Shanghai, Guangzhou | Short term (≤ 2 years) |

| Break-through functional textiles (e.g., Y-Warm nano-insulation) | +0.8% | Global demand, production centered in East China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes & Urbanization Drive Premium Segment Expansion

Urban household spending on furnishings has grown faster than national income, especially in tier-2 and tier-3 cities, where new apartments foster first-time purchases of coordinated textile sets. Younger buyers prioritize aesthetics and sleep quality, lifting demand for premium thread counts, organic cotton, and branded matching collections. This consumer shift elongates replacement cycles into seasonal refreshes, generating recurrent revenue streams for suppliers. Retailers respond by curating themed bedroom bundles and limited-edition color palettes. The ongoing influx of rural workers into urban areas sustains baseline volume growth, anchoring the Chinese home textile market at both value and mass-market price points.

E-Commerce Platform Revolution Reshapes Distribution Dynamics

Online channels already contribute more than one-third of sales, and live-streaming, augmented-reality “try-on” apps, and same-day fulfillment now blur the line between discovery and purchase. Marketplaces such as Tmall and JD.com leverage behavioral data to micro-target shoppers with personalized style feeds and dynamic discounting. Direct-to-consumer brands exploit this infrastructure to sidestep legacy wholesalers, allowing them to release micro-collections weekly. For suppliers, these data loops slash forecasting errors and inventory write-downs, improving working-capital efficiency while broadening geographic reach into lower-tier cities. As rural broadband coverage widens, incremental e-commerce penetration still offers at least a decade of upside.

Government Sustainability Mandates Accelerate Green Manufacturing Adoption

Beijing’s dual-carbon roadmap incentivizes mills to upgrade from coal to renewable electricity and to integrate water-recycling systems, cutting emissions and effluent. Subsidies for bamboo, hemp, and recycled fibers lower their cost disadvantage versus cotton, encouraging brands to launch eco-certified SKUs that command higher shelf prices. Textile exporters also face stricter compliance audits under EU environmental regulations and U.S. Customs traceability checks; blockchain tracking solutions have therefore become standard among leading mills. This regulatory environment underpins the double-digit CAGR forecast for bamboo and other niche naturals, positioning sustainability as both a compliance necessity and a marketing differentiator[1]Fred Gale, “Cotton and Products Update,” United States Department of Agriculture, usda.gov.

Digital Design & AI-Driven Production Enable Mass Customization

Cloud-based design studios now let consumers adjust patterns, colors, and dimensions on mobile screens, with AI automatically converting specifications into machine-readable production files. 3D knitting equipment, paired with predictive demand algorithms, drastically cuts fabric waste and shortens order-to-ship cycles to as little as 72 hours. For bedding, buyers select thread count, fabric blend, and embroidery, creating virtual exclusivity without high cost. Manufacturers deploy machine-vision quality control and automated packing lines, mitigating rising labor expenses while maintaining consistency. These efficiency gains strengthen local suppliers against imports and embed personalization as a mainstream value proposition [2]Advancing Textile Waste Recycling: Challenges and Opportunities,” Polymers, mdpi.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cotton prices & supply-chain shocks | –1.2% | Nationwide, acute in cotton-dependent clusters | Short term (≤ 2 years) |

| Forced-labor/Xinjiang-related sourcing restrictions | –0.9% | Export-oriented manufacturers nationwide | Long term (≥ 4 years) |

| Forced-labor/Xinjiang-related sourcing restrictions | –0.9% | Export-oriented manufacturers nationwide | Long term (≥ 4 years) |

| Tier-1 city market saturation & price wars | –0.6% | Beijing, Shanghai, Guangzhou, Shenzhen | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cotton Price Volatility Creates Input Cost Pressures

ICE cotton futures swung to four-year lows in early 2025 after tariff escalations, yet freight bottlenecks and quality disparities between Xinjiang stocks and imported yarn keep mill procurement unpredictable. Mills hedge with synthetic or blended yarns, but substitution raises re-engineering costs and can dilute brand positioning in premium cotton lines. Financial volatility forces smaller spinners to operate on razor-thin margins, curbing R&D budgets and delaying equipment upgrades. Government stock-release mechanisms provide some stability but cannot fully offset global price swings, making cost pass-through to consumers unavoidable in the near term.

Xinjiang Sourcing Restrictions Force Supply-Chain Restructuring

The Uyghur Forced Labor Prevention Act prompts retailers in the United States to demand end-to-end traceability, pushing Chinese exporters to adopt blockchain tracking, third-party audits, and segregated warehouses. Mills outside Xinjiang gain overseas orders but must absorb higher logistics costs to secure cotton from Pakistan, Brazil, or Australia. Compliance spending disproportionately burdens SMEs, spurring consolidation as larger groups acquire smaller peers to expand traceable capacity. Domestically, retailers reassure consumers through QR-code provenance labels, signaling a permanent shift toward transparent supply chains and increasing investment in traceability technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Dominance Amid Carpet Innovation

Bed linen accounted for 44.52% of the China home textile market size in 2025, buoyed by multiple-set ownership, seasonal refresh cycles, and increasing preference for organic cotton and higher thread counts. Upmarket brands bundle pillowcases, duvet covers, and fitted sheets to raise average selling prices and encourage coordinated bedroom aesthetics. Wellness marketing links sleep quality to breathable fabrics and accelerates premiumization within this category. Industry players also experiment with antimicrobial finishes and phase-change cooling fibers to differentiate beyond design and color.

Carpets and area rugs, though comprising a smaller revenue base, are projected to register an 8.45% CAGR through 2031—the fastest among all applications—as urban apartment dwellers adopt Western-style décor and demand sound-absorbing floor coverings. Platform-enabled “room-in-a-box” kits often include complementary rugs, driving cross-category pull-through. Innovations in stain-resistant yarns and modular tile configurations elevate ease of cleaning and simplify replacement, making rugs more attractive for families with young children or pets. Commercial builders add further momentum by specifying flame-retardant carpet tiles that qualify for green-building credits.

By Material: Cotton Leadership Challenged by Sustainable Alternatives

Cotton maintained 48.93% of China home textile market share in 2025 due to its established supply chain and consumer familiarity. However, sustainability-oriented shoppers now scrutinize water consumption and pesticide use in cotton farming, pushing brands to source organic certificates or blend in recycled cotton. Polyester and other synthetics secure footholds in performance-driven segments through moisture-wicking, wrinkle-free, and quick-dry attributes, particularly for hospitality linens that require frequent laundering. These blends also temper cost spikes during cotton-price surges.

In the China home textile market, bamboo and other niche naturals are expected to expand at an 10.84% CAGR to 2031, capitalizing on antibacterial properties, soft hand feel, and storytelling appeal around renewable agriculture. Government subsidies for bamboo pulp and lower-emission viscose processing reduce raw-material premiums, making eco-certified SKUs more price-competitive. Hemp, jute, and silk likewise benefit from policy incentives and premium positioning, though limited farming acreage keeps their volume share modest. Across materials, brands increasingly adopt digital traceability tags to reassure consumers about provenance and processing practices.

By End-User: Commercial Sector Drives Growth Innovation

Residential buyers generated 72.78% of 2025 revenue in the China home textile market, reflecting China’s vast household base and ongoing urban apartment completions. Tier-2 and tier-3 city homeowners allocate higher discretionary budgets to home décor, drawing inspiration from social-media influencers and livestream hosts who curate coordinated bedding and window-treatment schemes. In tier-1 cities, where replacement cycles dominate, retrofits favor premium smart-textile functions such as temperature regulation and dust-mite resistance.

The commercial/hospitality segment in the China home textile market is forecast to post an 8.05% CAGR on the back of resumed domestic tourism and a new wave of mid-scale hotel openings across transport hubs. Property owners upgrade to higher GSM towels and long-staple cotton sheets to differentiate guest experience, simultaneously specifying durable, chlorine-resistant fabrics to curb operating costs. Institutional demand from healthcare, education, and senior-living facilities further boosts volume, with procurement committees prioritizing antimicrobial and flame-retardant certifications. Smart linen closets equipped with RFID tags track usage and trigger automated re-ordering, underscoring the segment’s leadership in IoT integration.

By Distribution Channel: Digital Transformation Accelerates

Offline outlets—department stores, shopping-mall flagships, and franchised specialty shops—accounted for 63.85% of 2025 sales in the China home textile market, thanks to tactile evaluation preferences and immediate take-home convenience. Brands invest in experiential showrooms that feature bedroom vignettes and on-site monogramming to defend foot traffic. However, per-store productivity is plateauing in saturated tier-1 markets, encouraging retailers to pivot toward smaller pop-up kiosks and shop-in-shop partnerships.

Online channels, projected to climb at a 14.72% CAGR, deliver nationwide reach and enable algorithm-driven personalization. Livestream flash-sales compress decision cycles, while virtual-reality room planners help shoppers visualize pattern coordination at scale. Brands gather first-party data—from fabric-preference quizzes to predictive size recommendations—to refine product roadmaps and reduce returns. Cross-border e-commerce platforms further diversify assortments, allowing Chinese consumers to purchase Scandinavian minimalism or Japanese zen-style linens without overseas travel. The digital shift, therefore, functions as both a sales engine and a product-development laboratory for the China home textile market.

Geography Analysis

East China commanded 35.05% of 2025 revenue in the China home textile market, leveraging dense manufacturing clusters in Jiangsu, Zhejiang, and Shanghai that integrate spinning, dyeing, cut-and-sew, and port logistics within a 250 km radius. Proximity to Ningbo-Zhoushan and Shanghai ports accelerates export processing, while local consumer wealth sustains premium price points. Provincial governments subsidize robotics and water-recycling retrofits, keeping factories globally cost-competitive despite higher wages. Retail penetration is mature; flagship stores in Shanghai’s prime malls anchor brand visibility, but most incremental sales now stem from online orders shipped from regional fulfillment centers.

South-Central China—including Guangdong, Fujian, Hunan, and Hubei—benefits from a balanced mix of manufacturing know-how and rising local purchasing power. Pearl River Delta mills pivot from apparel to higher-margin home-textile runs, repurpose circular-knit machines for towel loops and jacquard sheeting. Guangzhou’s wholesale mega centers still funnel bulk orders to domestic mom-and-pop shops, yet digital adoption is brisk: merchants livestream product auctions via mobile apps. Provincial infrastructure upgrades, notably high-speed rail links, compress freight lead times to inland consumers, feeding omnichannel growth.

Southwest China is poised for the fastest expansion in the China home textile market, at a 9.92% CAGR through 2031, propelled by inland industrial-relocation incentives that reduce land lease costs up to 40% versus coastal peers. Chongqing and Chengdu attract greenfield mills equipped with automated looms and renewable-energy power purchase agreements. The region’s proximity to Xinjiang’s cotton output cuts raw-material transit time, though logistics bottlenecks across the Hengduan mountains necessitate ongoing road and rail investment. Local governments partner with vocational schools to upskill labor, mitigating talent shortages and enabling quality convergence with coastal production benchmarks.

Competitive Landscape

China’s home-textile arena exhibits moderate concentration: the top five players hold a cumulative revenue share in the China home textile industry, while a long tail of regional specialists and digital-native brands fills niche demands. Incumbents such as Luolai Lifestyle Technology and Fuanna Bedding respond to price-aggressive online entrants by deepening vertical integration—extending from upstream yarn spinning to downstream branded e-stores—capturing margin and real-time consumer data. Cross-border competitors, notably IKEA and Zara Home, expand localized sourcing to sidestep tariffs and shorten delivery schedules. IKEA alone activated 47 new supplier contracts in 2025, pushing its renewable-energy adoption above 90% within its Chinese value chain [3]Linqin Sun, “IKEA ‘planning now for the next 60 years’ in nation,” China Daily, chinadaily.com.cn.

Product innovation in the China home textile market focuses on functionality: nano-insulated Y-Warm quilts, anti-odor modal-cotton blends, and phase-change cooling pillows cater to wellness-centric shoppers. Early movers patent proprietary fiber treatments, erecting IP barriers that temper commoditization. Concurrently, investments in AI-linked planning tools trim design-to-shelf cycles from six months to six weeks, enabling rapid reaction to influencer-driven micro-trends. Blockchain traceability platforms, now mainstream among major exporters, serve dual roles—regulatory compliance and brand storytelling—by showcasing cotton provenance and emissions metrics to eco-conscious consumers.

M&A activity accelerates as leading groups pursue capacity scale and digital capabilities. Fuanna’s 2025 acquisition of Guangzhou Textile Manufacturing expanded its smart-textile line by 35% and embedded RFID stitching into high-turnover SKUs. Meanwhile, Sunvim Group’s new automated Chongqing facility integrates machine-vision defect detection and AI-driven scheduling, enabling 2.5 million annual units with 30% lower labor input. Smaller specialty labels, unable to match technology capex, increasingly partner with platform influencers or license designs to volume producers, ensuring continued category diversity yet reinforcing the scale advantages of top-tier enterprises.

China Home Textile Industry Leaders

Luolai Lifestyle Technology Co., Ltd.

Shenzhen Fuanna Bedding & Furnishing

Hunan Mengjie Home Textile

Violet Home Textile

Ningbo Veken Elite Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: IKEA China finalized a USD 150 million supply-chain expansion that added 47 renewable-energy-compliant suppliers across Jiangsu and Zhejiang. The move lowers the average sourcing cost by 12% and guarantees a greener input mix for its bedroom textile line, reinforcing the retailer’s premium yet affordable positioning in the Chinese home textile market.

- February 2025: Luolai Lifestyle Technology reported Q4 2024 revenue of RMB 2.1 billion (USD 292 million), a 18.6% jump driven by direct-to-consumer online flagship growth. Management cited premium bedding launches and a data-driven replenishment algorithm that cut stock-out days by 22%, demonstrating how omnichannel agility can lift margins in a competitive environment.

- January 2025: Fuanna Bedding acquired Guangzhou Textile Manufacturing for RMB 680 million (USD 94.7 million) and immediately retrofitted the plant with RFID sewing machines. The integration expands smart-textile capacity by 35% and positions Fuanna to meet rising commercial-hospitality demand for track-and-trace linens.

- December 2024: Beyond Home Textile invested RMB 45 million (USD 6.3 million) to roll out a blockchain-based supply-chain platform covering cotton bale to finished SKU. This system enables compliance with U.S. UFLPA audits and provides QR-code provenance labels for domestic shoppers seeking transparency.

China Home Textile Market Report Scope

A complete background analysis of the China home textile market, including an assessment of the economy, the contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and company profiles of the key players are covered in the report. China Home Textile Market is Segmented by Product into Bed Linen, Bath Linen, Kitchen Linen, Upholstery, and Floor Covering, and by Distribution Channel into Supermarkets & Hypermarkets, Speciality Stores, Online and Other Distribution Channels.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others (Carpets and Area Rugs) |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo etc.) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline |

| Online |

By Geography

| East China |

| South-Central China |

| North and Northeast China |

| Southwest China |

| Northwest China |

| By Application | Bed Linen |

| Bath Linen | |

| Kitchen Linen | |

| Upholstery | |

| Others (Carpets and Area Rugs) | |

| By Material | Cotton |

| Linen | |

| Synthetic Fibres | |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo etc.) | |

| By End-User | Residential |

| Commercial | |

| By Distribution Channel | Offline |

| Online | |

| By Geography | East China |

| South-Central China | |

| North and Northeast China | |

| Southwest China | |

| Northwest China |

Key Questions Answered in the Report

How large is the China home textile market in 2026?

The sector recorded USD 45.91 billion in revenue in 2026.

What is the projected CAGR for China’s home textile demand to 2031?

The market is forecast to grow at 6.18% annually through 2031 during the 2026-2031 forecast period.

Which application category grows the fastest through 2031?

Carpets and area rugs are expected to register an 8.45% CAGR.

Why are bamboo and other niche naturals gaining market share?

Sustainability mandates, subsidies, and antibacterial qualities fuel an 10.84% CAGR for these fibers.

Which sales channel is expanding most quickly?

Online platforms are rising at a 14.72% CAGR as livestreaming and same-day fulfillment attract shoppers.

How are Xinjiang sourcing restrictions affecting exporters?

Brands invest in blockchain traceability and alternative cotton sourcing to maintain overseas market access.

Page last updated on: