China DC Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

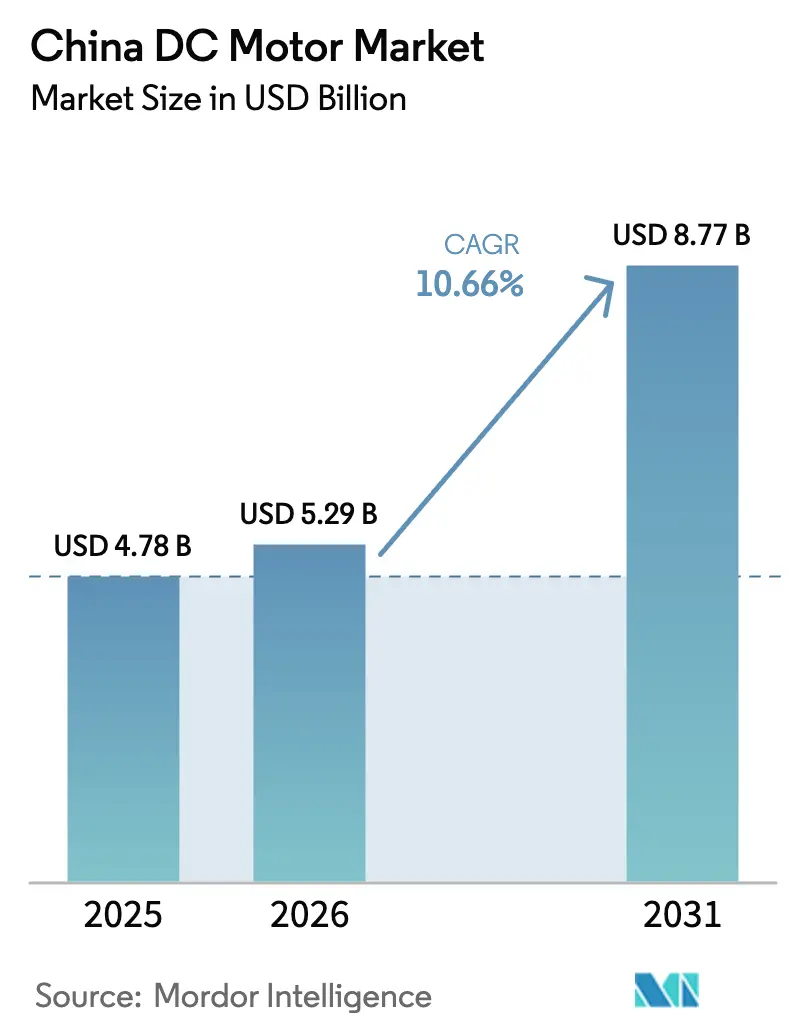

| Base Year Market Size (2025) | USD 4.78 Billion |

| Market Size (2026) | USD 5.29 Billion |

| Market Size (2031) | USD 8.77 Billion |

| Growth Rate (2026 - 2031) | 10.66% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China DC Motor Market Analysis by Mordor Intelligence

The China DC motor market size was valued at USD 4.78 billion in 2025 and estimated to grow from USD 5.29 billion in 2026 to reach USD 8.77 billion by 2031, at a CAGR of 10.66% during the forecast period (2026-2031). The current growth reflects how electrification, industrial automation, and infrastructure modernisation work together to lift demand across every voltage class and power rating. Scale-up in electric vehicle production, energy-efficiency mandates that now cover IE3-class motors, and rising investment in automated factories are reinforcing the need for compact, high-performance motion systems. Producers are responding with brushless and permanent-magnet designs that balance higher power density with lower maintenance requirements. Materials risk tied to rare-earth magnets remains the key cost headwind, yet domestic supply-chain policies soften much of the impact. Foreign and local suppliers alike are also integrating digital controls to improve reliability, reduce downtime, and satisfy emerging predictive-maintenance norms. Together, these forces keep the China DC motor market on a structurally higher growth path than most other national motor arenas.

Key Report Takeaways

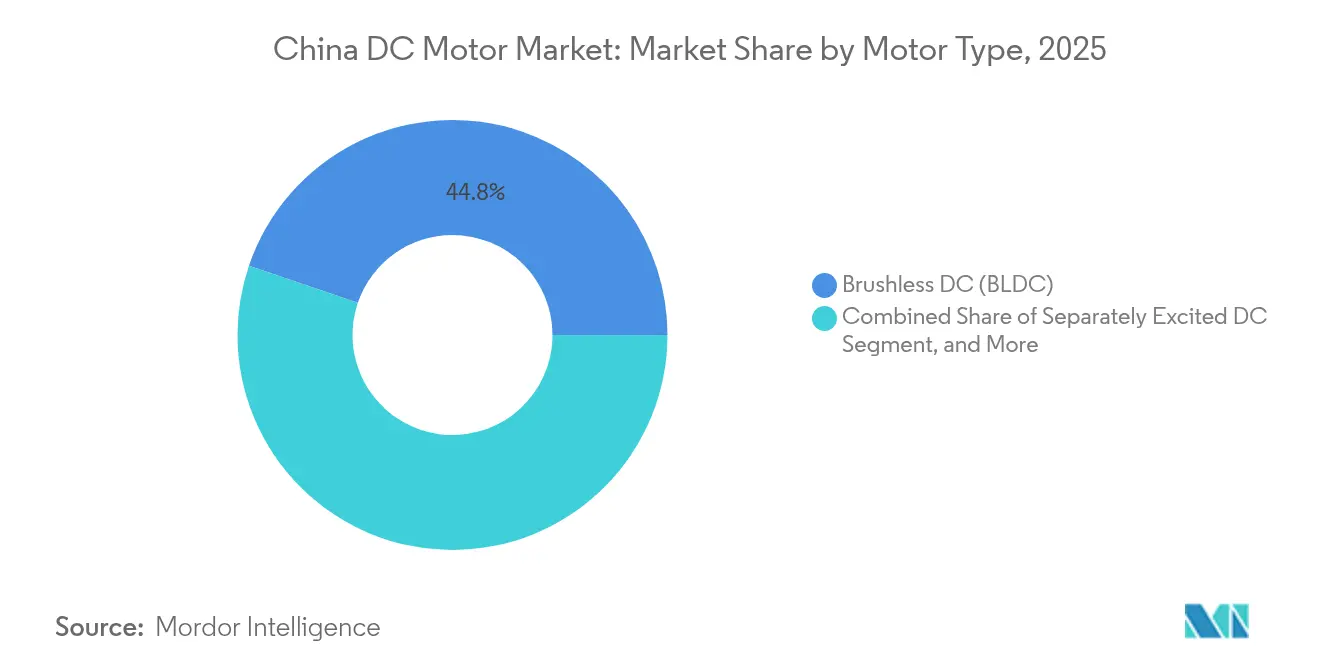

- By motor type, brushless designs led with 44.78% of China DC motor market share in 2025, while permanent-magnet models are set to post a 12.06% CAGR through 2031.

- By voltage class, low-voltage units (< 60 V) dominated with 50.62% share in 2025; medium-voltage motors (60-600 V) are projected to expand at a 12.98% CAGR to 2031.

- By power rating, sub-1 kW products accounted for 48.15% of the China DC motor market size in 2025; the 1-10 kW range is on track for a 12.21% CAGR.

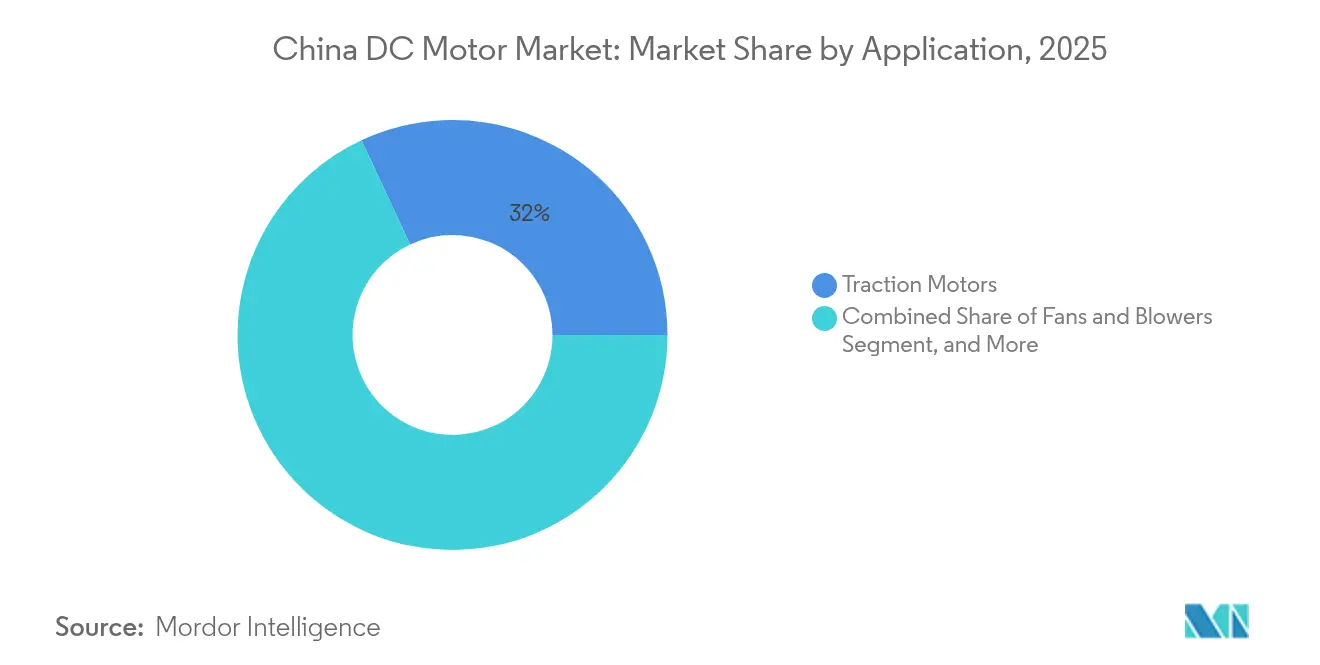

- By application, traction motors held 31.96% share of the China DC motor market size in 2025, whereas robotics and AGVs are advancing at a 15.02% CAGR through 2031.

- By end-user industry, industrial automation captured 16.84% of China DC motor market share in 2025; automotive and e-mobility will deliver the fastest 15.11% CAGR in the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China DC Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV production and adoption | +2.8% | National, with concentration in Guangdong, Jiangsu, Shanghai | Medium term (2-4 years) |

| Rapid industrial automation in manufacturing | +2.1% | National, with emphasis on Yangtze River Delta, Pearl River Delta | Long term (≥ 4 years) |

| Expansion of water and wastewater infrastructure | +1.4% | National, with focus on western provinces and urban centers | Long term (≥ 4 years) |

| Government energy-efficiency mandates (IE3+) | +1.8% | National implementation with industrial clusters prioritized | Medium term (2-4 years) |

| Subsidy-fuelled rise of delivery robots and AGVs | +1.2% | Urban centers, e-commerce hubs, manufacturing zones | Short term (≤ 2 years) |

| Growth of domestic smart-appliance robotics | +0.9% | National, with higher adoption in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in EV Production and Adoption

China’s electric-vehicle build hit 10 million units in 2024 and continues to climb, making traction motors the largest single application. Carmakers seek ≥4 kW/kg power density, driving premium demand for brushless and permanent-magnet designs. Higher-voltage (800 V) platforms shorten charging times, enhance drive cycles, and increase per-vehicle motor count. NIO’s 38.7% delivery growth in 2024 illustrates the production pull that now defines the China DC motor market.[1]South China Morning Post, “China Produces 10 Million EVs in 2024,” scmp.com

Rapid Industrial Automation in Manufacturing

Robot density reached 470 units per 10,000 employees in 2024, with a 500-unit target set for 2025. Automated lines require precision motors that combine fine speed control with energy savings, a niche served most efficiently by brushless DC models. Provincial automation plans in Jiangsu and Guangdong drive aggregated tender volumes that benefit local motor producers with fast-cycle customisation capabilities. Patents that embed digital signal processors directly on the drive board show how suppliers address torque ripple and downtime concerns.[2]Nankai University, “DSP-Based Control for Brushless DC Motors,” nankai.edu.cn

Expansion of Water and Wastewater Infrastructure

The 10 billion-yuan Gansu Yongchang Pumped Storage Power Station and similar megaprojects rely on DC motors for variable-speed pumping. Such projects cut coal usage and support clean-energy targets, so operators favour IE3-ready machines to control lifecycle electricity costs. International brands supply premium high-torque units, while domestic firms leverage nearby service depots to win aftermarket contracts. The China DC motor market therefore benefits each time an urban centre allocates capital to modernise water grids.[3]International Energy Network, “Gansu Yongchang Pumped Storage Station Project,” ien.com.cn

Government Energy-Efficiency Mandates (IE3+)

Mandatory labels applied from February 2025 force factories to replace legacy IE1 and IE2 units. Equipment-upgrade subsidies announced by the National Development and Reform Commission create a clear payback path, further stimulating demand for high-efficiency motors. Producers that integrate smart monitoring features show up with stronger order books because buyers want to verify savings in real time. This regulatory push locks in long-run demand, ensuring the China DC motor market stays on a double-digit growth path.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rare-earth magnet price volatility | -1.6% | National, with supply chain dependencies on domestic mining | Short term (≤ 2 years) |

| Substitution by high-efficiency AC drives | -1.2% | Industrial applications, manufacturing clusters | Medium term (2-4 years) |

| Stricter e-waste compliance costs | -0.8% | National, with emphasis on electronics manufacturing regions | Long term (≥ 4 years) |

| R&D talent shortage in magnetic materials | -0.5% | National, concentrated in advanced manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rare-Earth Magnet Price Volatility

Neodymium and praseodymium oxide prices more than doubled between 2020 and 2025, squeezing margins in permanent-magnet segments. April 2025 export controls gave domestic producers priority access, yet volatility requires hedging and alloy-mix optimisation. Some suppliers file patents that cut magnet volume per kilowatt, though adoption takes time. Price swings thus subtract near-term growth but reinforce localisation strategies inside the China DC motor industry.

Substitution by High-Efficiency AC Drives

Variable-frequency AC drives eliminate brush wear and now match DC precision in many conveyor, fan, and pump duties. Cost-conscious buyers in mature factories run total-cost comparisons that favour AC when torque transients are mild. DC retains an edge in high-torque starts, tight voltage windows, and mobile systems, yet share pressure persists. Suppliers mitigate the risk by bundling DC-AC hybrid portfolios and investing in after-sales ecosystems that lock in spare-parts revenues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Brushless Technology Drives Innovation

Brushless units captured 44.78% of China DC motor market share in 2025, and the segment holds clear momentum because it couples efficiency with low maintenance. Continuous-operation factories prefer these designs, as downtime carries steep costs. Manufacturers add sensor-less control algorithms that raise precision yet trim bill-of-material expenses. Permanent-magnet motors trail in share yet post a 12.06% CAGR by 2031 on superior power density demanded by EVs and robotics. Their adoption rate would be even higher absent magnet price swings. Series or compound-wound motors remain a choice for budget-sensitive buyers, while separately excited designs serve niche speed-regulation needs. The cumulative technology mix ensures the China DC motor market delivers balanced top-line growth and an attractive margin profile for innovators.

Brushless suppliers improve thermal paths, use resin-filled hollow rotors, and switch to arc-groove cores to cut copper loss. Patent data confirm a leap toward coreless discs optimised for heat dissipation. These incremental gains matter because energy-labelling rules now factor total system losses. Given rising customer focus on predictive maintenance, producers that package motors with cloud-linked condition-monitoring software gain stickier service revenue. Such moves illustrate why the China DC motor market rewards firms that unite materials science, electronics, and digital analytics.

By Voltage Class: Medium-Voltage Segment Accelerates

Low-voltage motors held 50.62% revenue in 2025 as they power home electronics and light appliances. Still, medium-voltage (60-600 V) machines grow faster at 12.98% as EV makers adopt 800 V architectures and plant engineers demand higher torque without extra weight. The China DC motor market size for this class is projected to expand from USD 2.22 billion in 2026 to nearly USD 4.07 billion by 2031. Hairpin-winding techniques raise slot-fill factors and therefore power density, making mid-voltage attractive even in tight chassis spaces. High-voltage motors above 600 V serve pumps and heavy industry, yet their growth stays steady rather than spectacular.

Domestic suppliers that master high-voltage insulation and partial-discharge control win premium automotive contracts. International groups leverage cross-border R&D platforms to push next-generation laminated-steel stacks that limit eddy-current loss. Each advance feeds customer appetite to shrink battery packs without sacrificing range. For process industries, mid-voltage ratings allow retrofits in speed-critical lines, reinforcing the China DC motor market’s move toward a higher-value mix.

By Power Rating: Mid-Range Motors Capture Growth

Sub-1 kW units dominate volume because consumer electronics and smart appliances move in the millions each quarter. Yet 1-10 kW models exhibit the quickest 12.21% CAGR. This range powers auxiliary EV systems, pick-and-place robots, and conveyor actuators across auto parts plants. It also fits new urban-infrastructure assets such as compact pumping stations. The China DC motor market size attributed to 1-10 kW units is set to cross USD 2.73 billion by 2031. High-power machines above 10 kW remain a high-value niche in energy storage and metallurgical lines.

Growth in the mid-range also benefits suppliers through higher average selling prices. Firms apply silicon-carbide inverters to lift overall system efficiency, thereby meeting IE3 class with margin to spare. Combined with rising R&D tax incentives, these trends encourage continual optimisation of winding factors and magnetic circuits. The payoff materialises not only in upfront sales but in multi-year service agreements that supply steady cashflows within the China DC motor market.

By Application: Robotics and AGVs Lead Innovation

Traction motors owned 31.96% share in 2025 and will stay the revenue anchor. Yet robotics and AGVs deliver a blistering 15.02% CAGR as labour costs climb and e-commerce platforms need lights-out fulfilment centres. Robot density targets of 500 units per 10,000 workers require high-precision, low-maintenance drives, making brushless DC the default choice. For pumps and compressors, water projects lift unit demand, especially in western provinces. Fans, blowers, and HVAC systems benefit from urban building codes that hinge on energy-performance ratings. Medical device applications, though still small, rise with healthcare digitalisation and an ageing population.

Service-robot makers want compact drives below 60 V to pass safety rules while still delivering strong torque. Suppliers respond with slot-less rotor constructions that reduce cogging. In AGVs, battery life acts as the ultimate buying criterion, making electrical efficiency a deciding factor. Such dynamism keeps the China DC motor market vibrant across multiple verticals, sheltering revenue streams from single-sector volatility.

By End-User Industry: Automotive Electrification Accelerates

Industrial automation carried the biggest 16.84% slice in 2025, yet automotive and e-mobility now set the pace with a 15.11% CAGR. One-in-three new light vehicles sold worldwide was electric or hybrid in 2024, and a growing share came from Chinese factories. Each EV hosts at least two main traction motors plus several auxiliaries, multiplying per-vehicle motor demand. Water, wastewater, HVAC, and refrigeration continue to order steady volumes, reflecting urbanisation. Metals, mining, and oil-and-gas users need ruggedised designs; food and beverage plants prize hygienic enclosures.

Tier-1 auto suppliers adopt vertical integration, bringing stator and rotor production in-house to secure supply. Industrial firms, by contrast, often outsource motor packages and focus on controls software. The divergent strategies still push volumes into the same China DC motor market, ensuring broad-based pull for high-efficiency units that comply with forthcoming IE4 guidelines.

Geography Analysis

Eastern provinces anchor production and consumption. Guangdong alone assembled 2.53 million NEVs in 2024, fostering dense supplier clusters around traction and accessory motors. Jiangsu’s manufacturing sector generated RMB 4.66 trillion (USD 640 billion) value-added, sustaining ongoing procurement of automation-grade brushless units. Zhejiang’s private-sector model spurs small and mid-size enterprises to order low-voltage motors in bulk. These coastal hubs therefore account for the lion’s share of China DC motor market demand.

Central China attracts relocations from coastlines to save costs and tap local stimulus. Emerging clusters in Hubei and Henan show double-digit motor demand growth as new factories scale. Western provinces such as Gansu absorb infrastructure spend, notably pumped-storage and long-distance water pipelines that specify large DC pumps. The Pearl River Delta’s export focus contrasts with the Yangtze River Delta’s integrated manufacturing, but both contribute high absorption rates for medium-voltage and mid-power designs.

Northern provinces keep an appetite for ruggedised, high-torque units suitable for steel mills, mining, and petrochemicals. Policymakers facilitate integration of green motors via provincial subsidy lists that slash payback periods. This regional mosaic cushions the China DC motor market against local cyclical swings, ensuring national growth persists even if one cluster slows investment.

Competitive Landscape

The market shows moderate concentration. Six leading suppliers control about 42% of revenue yet face active competition from dozens of specialists. Global companies such as Nidec, Siemens, and ABB defend premium sectors with deep R&D pipelines and global sourcing. Domestic brands Wolong Electric, Broad-Ocean Motor, and Johnson Electric convert local material access and fast engineering cycles into pricing and speed-to-market advantages. Patent filings reveal an industry pivot toward sensor-less control and resin-filled rotors that mitigate torque ripple and heat build-up.

Strategic differentiation occurs along three lines. Technology leaders integrate cloud analytics to sell outcome-based maintenance contracts. Cost leaders streamline assembly through flexible production cells, cutting changeover time to meet small-lot orders. Niche innovators target medical, humanoid-robot, and high-speed spindle opportunities that reward miniaturisation know-how. Rare-earth volatility and export controls give an edge to players with in-house magnet plants, improving cost visibility. As buyers seek fewer vendors able to guarantee long-term spares, supplier collaborations and small acquisitions are likely to rise inside the China DC motor industry.

China DC Motor Industry Leaders

-

Hansen Corporation

-

Addison Electric

-

CH Motion Co. Ltd

-

ABB Ltd.

-

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: China imposed export controls on seven rare-earth elements vital for NdFeB magnets. Strategy: channel domestic magnet output to local industries and raise switching costs for foreign DC motor competitors.

- March 2025: NIO disclosed 221,970 vehicle deliveries for 2024, a 38.7% uptick. Strategy: scale production to consolidate premium-EV positioning, thereby expanding demand for dual-motor AWD setups supplied by domestic and international motor makers.

- February 2025: BorgWarner signed four EV motor contracts with three Chinese OEMs covering 400 V hairpin designs for 200 kW hybrids and 150 kW BEVs. Strategy: lock in scalable platforms ahead of 2026 mass production, securing anchor volumes and local validation that may spur future 800 V awards.

- January 2025: The National Development and Reform Commission enforced mandatory energy-efficiency labels for motors, transformers, and pumps

China DC Motor Market Report Scope

DC motors, or direct current motors, are electrical machines that convert direct current electrical energy into mechanical energy. They operate based on the interaction of magnetic fields and conductors carrying the current to produce rotational motions. DC motors are known for their precise speed control, high starting torque, and efficiency, and they are ideal for applications requiring variable speed and load conditions. The study tracks the revenue accrued through the sale of DC motors by various players in China.

The Chinese direct current (DC) motor market is segmented by type (permanent magnet and self-excited and separately excited) and end-user industry (oil and gas, chemical and petrochemical, power generation, water and wastewater, metal and mining, food and beverage, and discrete industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Permanent-Magnet DC (PMDC) |

| Brushless DC (BLDC) |

| Series / Compound Wound (Brushed) |

| Separately Excited DC |

| < 60 V (Low) |

| 60–600 V (Medium) |

| > 600 V (High) |

| < 1 kW |

| 1 – 10 kW |

| > 10 kW |

| Traction Motors |

| Pumps and Compressors |

| Fans and Blowers |

| Robotics and AGVs |

| Home Appliances |

| Medical Devices |

| Automotive and E-Mobility |

| Industrial Automation |

| Water and Wastewater |

| HVAC and Refrigeration |

| Metals and Mining |

| Oil and Gas |

| Food and Beverage |

| Other End-user Industries |

| By Motor Type | Permanent-Magnet DC (PMDC) |

| Brushless DC (BLDC) | |

| Series / Compound Wound (Brushed) | |

| Separately Excited DC | |

| By Voltage Class | < 60 V (Low) |

| 60–600 V (Medium) | |

| > 600 V (High) | |

| By Power Rating | < 1 kW |

| 1 – 10 kW | |

| > 10 kW | |

| By Application | Traction Motors |

| Pumps and Compressors | |

| Fans and Blowers | |

| Robotics and AGVs | |

| Home Appliances | |

| Medical Devices | |

| By End-user Industry | Automotive and E-Mobility |

| Industrial Automation | |

| Water and Wastewater | |

| HVAC and Refrigeration | |

| Metals and Mining | |

| Oil and Gas | |

| Food and Beverage | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current size of the China DC motor market?

The market is valued at USD 5.29 billion in 2026 and is forecast to touch USD 8.77 billion by 2031.

Which motor type leads the China DC motor market?

Brushless DC motors lead with 44.78% share in 2025, thanks to high efficiency and low maintenance.

Why are medium-voltage motors growing faster than low-voltage units?

EV platforms shifting to 800 V systems and factory upgrades that need higher torque without added weight push demand for 60-600 V motors.

How will rare-earth export controls affect motor prices?

Export restrictions prioritise domestic supply, easing local price pressure but raising costs for foreign competitors reliant on Chinese magnets.

Which end-user industry shows the fastest growth?

Automotive and e-mobility is projected to post a 15.11% CAGR through 2031 as EV production scales.

What policy measures are driving motor replacements in factories?

Mandatory IE3 energy-efficiency labels effective from February 2025 and generous equipment-upgrade subsidies accelerate replacement of older motors.

Page last updated on: