China Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.95 Billion |

| Market Size (2026) | USD 3.08 Billion |

| Market Size (2031) | USD 3.81 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

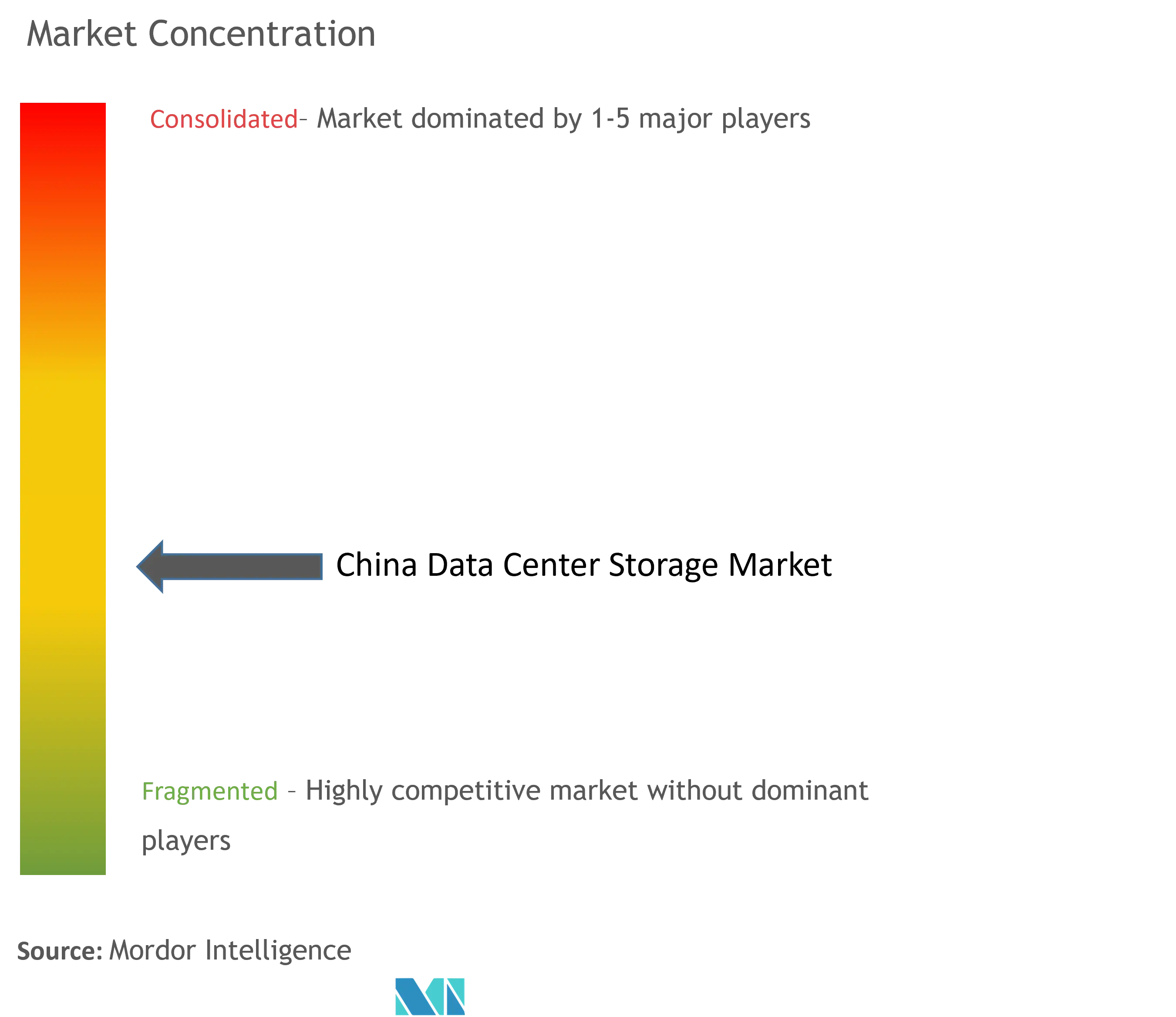

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Data Center Storage Market Analysis by Mordor Intelligence

The China data center storage market size is expected to grow from USD 2.95 billion in 2025 to USD 3.08 billion in 2026 and is forecast to reach USD 3.81 billion by 2031 at 4.38% CAGR over 2026-2031. Robust national programs—including the East-Data-West-Compute project—shift storage build-outs toward western provinces where renewable power costs sit 30% below coastal averages. Enterprises continue to favor colocation sites and high-performance arrays, yet adoption of object, tape, and software-defined platforms is accelerating alongside artificial-intelligence workloads. The China data center storage market is also shaped by power-efficiency rules in Tier-1 cities, tighter semiconductor export controls, and a growing preference for domestically designed NAND components. Vendors that can deliver high-IOPS flash, automated tiering, and intelligent data-management software are best placed to capture incremental growth as utilization gaps close and AI inference traffic rises.

Key Report Takeaways

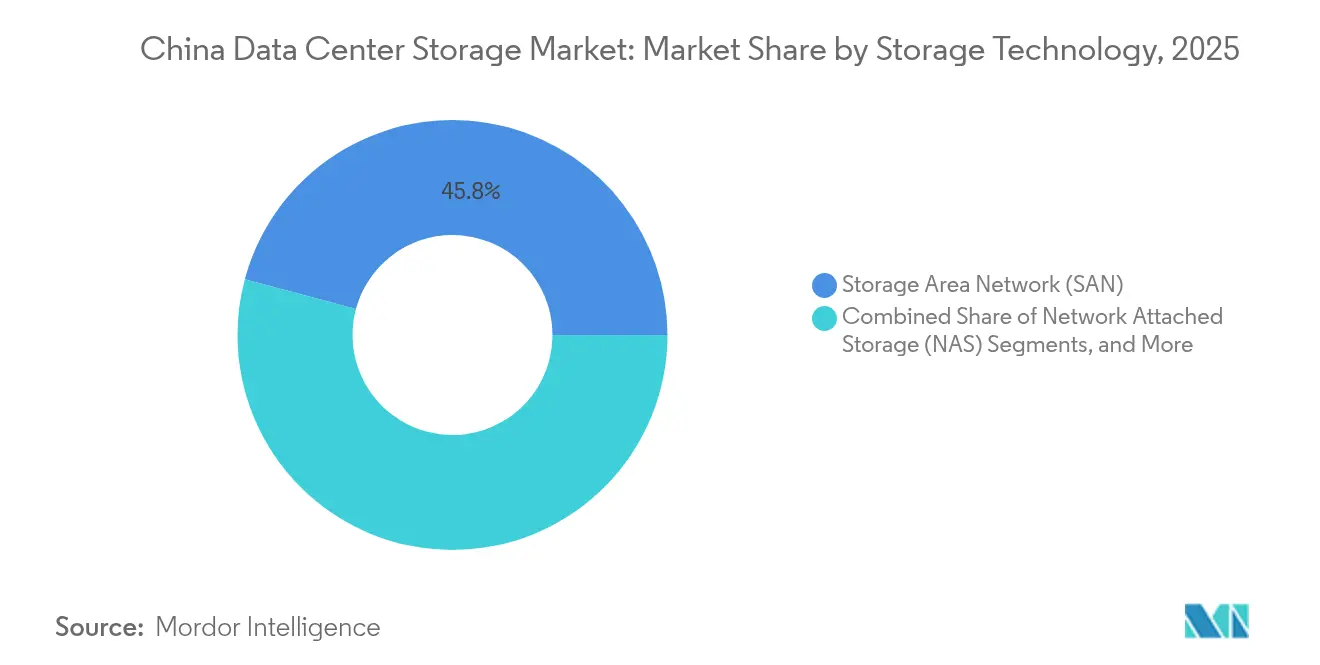

- By storage technology, Storage Area Networks led with 45.83% revenue share in 2025; object and tape solutions are projected to grow at a 6.05% CAGR through 2031 Yicai.

- By storage type, traditional HDD arrays accounted for 47.10% of the China data center storage market size in 2025, while all-flash arrays are advancing at a 7.55% CAGR.

- By data center type, colocation facilities held 66.60% of the China data center storage market share in 2025; hyperscaler deployments show the fastest CAGR at 8.22%.

- By end user, IT and telecommunications commanded 38.70% share of the China data center storage market size in 2025; healthcare and life sciences register the highest 9.05% CAGR.

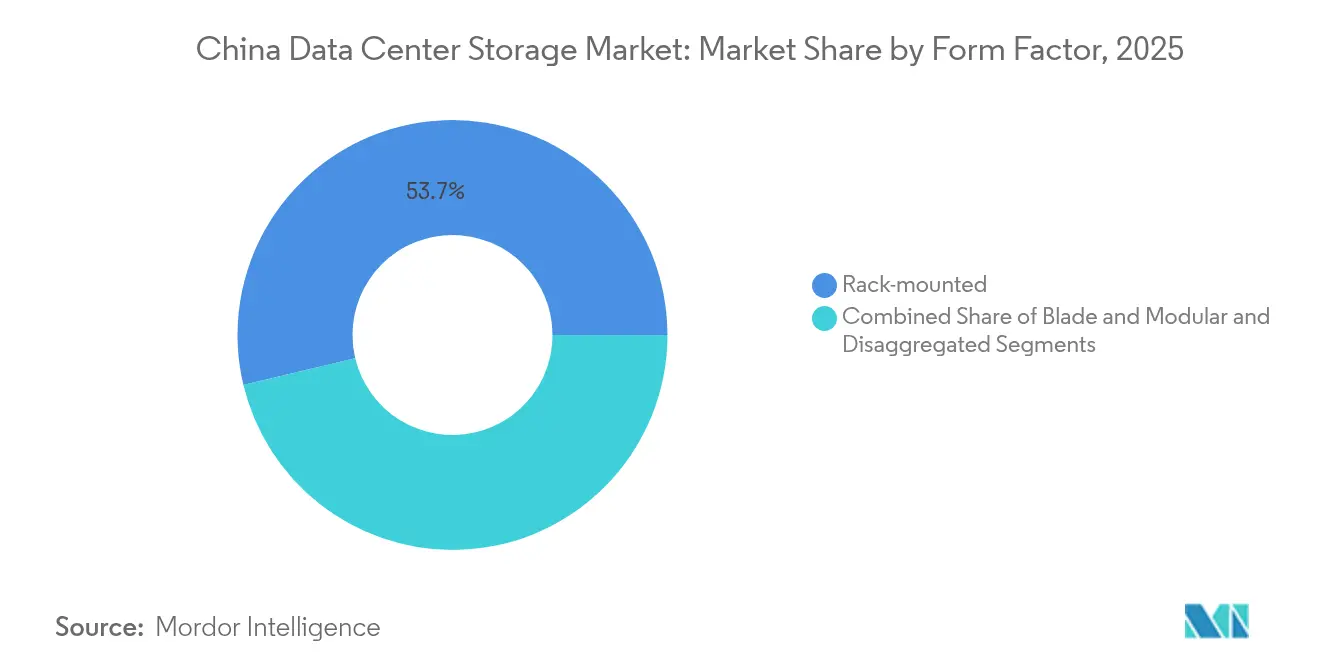

- By form factor, rack-mounted systems retained 53.74% share in 2025; composable storage is set to expand at 5.52% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first strategies of SOEs and internet giants | +1.2% | National, concentrated in Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| National "East-Data-West-Compute" hub rollout | +0.8% | Western regions: Guizhou, Inner Mongolia, Gansu, Ningxia | Long term (≥ 4 years) |

| AI/LLM workload surge demanding high-IOPS flash arrays | +1.5% | Tier-1 cities with spillover to designated AI zones | Short term (≤ 2 years) |

| Growing adoption of SDS & HCI in Tier-2 city colos | +0.7% | Secondary cities: Chengdu, Wuhan, Xi'an, Nanjing | Medium term (2-4 years) |

| 5G edge-cloud integration for low-latency services | +0.6% | Urban centers with manufacturing clusters | Medium term (2-4 years) |

| Semiconductor self-reliance push boosting domestic NAND supply | +0.4% | National, with production hubs in Yangtze River Delta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Strategies of SOEs and Internet Giants

State-owned enterprises and leading platforms such as Alibaba are raising capital-expenditure ceilings to meet digital-transformation mandates. Alibaba alone pledged USD 53 billion over three years for AI and cloud hardware, lifting near-term demand for multi-tier storage that supports analytics, training, and backup in a single stack. China Telecom’s healthcare subsidiary is rolling out provincial data pools that require scalable block and object capacity for imaging and genomic workloads. Unified public-and-private strategies increase orders for systems that combine NVMe performance with petabyte-scale object repositories, a sweet spot where the China data center storage market rewards vendors able to balance latency and cost. Procurement guidelines from SOEs also give preference to domestic controllers, offering local firms a route to higher bill-of-materials share.

National East-Data-West-Compute Hub Rollout

The East-Data-West-Compute program has committed almost USD 33 billion to build eight national hub nodes and 10 cluster zones, routing compute traffic away from grid-strained coastlines to renewable-rich inland sites.[1]State Council Information Office, “East-Data-West-Compute Project Overview,” scio.gov.cn Operators design western clusters for batch processing and archival workloads, spurring purchases of dense HDD cages and high-capacity object systems. Digital twins of grid assets feed real-time telemetry into these hubs, underscoring the need for intelligent tiering engines that migrate cold data to energy-efficient pools. Hardware selection now factors altitude, cooling requirements, and remote-management automation, which in turn elevates the China data center storage market’s appetite for AI-enabled orchestration software.

AI/LLM Workload Surge Demanding High-IOPS Flash Arrays

Large-language-model training drove national computing capacity 30% higher in 2023 and continues to lift IOPS budgets in Tier-1 cities. Huawei’s April 2025 launch of the OceanStor A-series AI lake underlines how vendors tailor parallel-file architectures, NVMe-over-Fabrics, and smart-NIC acceleration to sustain sub-100 µs read latencies.[2]Huawei Technologies, “OceanStor A-Series and AI Data Lake Launch,” huawei.com Model-inference traffic now exceeds training traffic at several hyperscale sites, pushing operators to deploy dual-personality arrays that juggle small-file random access with deep-archive throughput. The China data center storage market, therefore, skews toward all-flash systems enhanced by computational storage drives and data-reduction ASICs to optimize cost per inference query.

Semiconductor Self-Reliance Push Boosting Domestic NAND Supply

Beijing’s Made-in-China 2025 roadmap prizes indigenous flash processes; YMTC’s 294-layer 3D TLC and QLC breakthroughs reduce the import bill for SSDs.[3]YMTC, “294-Layer 3D NAND Mass Production Announcement,” ymtc.com Local fabs benefit from tax rebates and preferential power tariffs, easing cost barriers for all-flash deployments. Greater in-country wafer capacity stabilizes supply during geopolitical friction, letting integrators secure consistent drive allocations for long-term contracts. As controller and firmware capability rises, the China data center storage market rewards suppliers that co-optimize silicon and enclosure design for local regulatory and security mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-use efficiency caps in Tier-1 metros | -0.9% | Beijing, Shanghai, Guangzhou, Shenzhen | Short term (≤ 2 years) |

| Import restrictions on advanced controllers › supply risk | -0.6% | National, affecting high-end enterprise deployments | Medium term (2-4 years) |

| Under-utilization of newly built AI data centers | -0.4% | AI-designated zones and industrial parks | Short term (≤ 2 years) |

| Shortage of skilled data-storage architects outside coastal regions | -0.3% | Western and central provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Power-Use-Efficiency Caps in Tier-1 Metros

Beijing, Shanghai, and Guangzhou mandate PUE below 1.3 for new halls and impose retrofit timelines on legacy sites, restricting rack-level watt budgets and cooling density. Operators replace HDD JBODs with flash shelves, drawing 80% less power, yet initial capex remains a hurdle for smaller enterprises. Liquid-immersion pods and underwater modules off Hainan absorb up to 100 kW per rack while meeting urban planning codes. These constraints moderate near-term shipment volumes but shift the China data center storage market toward energy-efficient architectures with granular power-capping firmware.

Import Restrictions on Advanced Controllers › Supply Risk

The October 2024 expansion of U.S. export rules widens the entity list to cover advanced NAND controllers essential for 200-layer NVMe drives. Domestic OEMs scramble to dual-source silicon and redesign boards around locally licensed IP. Lead times for top-end PCIe 5.0 cards stretch beyond 30 weeks, forcing hyperscalers to over-provision older PCIe 4.0 fleets. While China funds joint ventures to accelerate controller tape-outs, short- and mid-term supply uncertainty drags on the China data center storage market’s high-performance segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: Enterprise SAN Holds Ground as Object Platforms Accelerate

SAN deployments accounted for 45.83% of 2025 revenue within the China data center storage market, reflecting entrenched demand for centralized block storage from state banks, telecom core networks, and ERP workloads. Established Fibre-Channel fabrics, high availability, and certified interoperability keep procurement cycles locked into SAN replacements even as software-defined options mature. Over the forecast window, most SAN refreshes include NVMe-FC upgrades and intelligent tiering to object repositories, helping CIOs manage surging AI training datasets without abandoning existing workflows.

At the same time, object and tape solutions post a 6.05% CAGR, the fastest among all technologies. AI model training consumes petabyte-scale image and text corpora, well suited to S3-compatible platforms backed by cost-optimized HDDs or next-generation optical media capable of 1.6 Pb per platter. Tape libraries also regain relevance because cold-archive regulations require offline copies for critical data. Vendors that offer seamless namespace sharing between SAN and object clusters gain an advantage as enterprises modernize at their own pace across the China data center storage market.

By Storage Type: Flash Displaces Spinning Media at the Performance Tier

HDD arrays still delivered 47.10% of 2025 revenue in the China data center storage market size, yet year-on-year trendlines favor solid-state drives. All-flash arrays expand at 7.55% CAGR to 2031 as AI inference, realtime analytics, and high-frequency trading reject mechanical latency. YMTC’s QLC endurance improvements narrow the price gap, encouraging banks and cloud providers to migrate relational databases to flash tiers during refresh cycles. Power-efficiency mandates further tilt procurement toward SSDs that draw one-fifth the watts per terabyte compared to 15 K RPM SAS drives.

Hybrid systems remain essential for mid-tier workloads needing cost-effective bulk capacity with a flash cache front end. Vendors mix QLC SSDs, PMR HDDs, and compression ASICs in a single chassis, providing a glide path for customers to transition gradually. As a result, shipments of pure HDD enclosures decline, yet cold-archive vaults continue purchasing multi-TB helium drives for write-once storage. The China data center storage market therefore evolves into a two-tier model—flash for active datasets and high-density HDD or tape for deep archives.

By Data Center Type: Colocation Retains Leadership While Hyperscalers Surge

Colocation operators held a 66.60% share in 2025, thanks to enterprises outsourcing power-intensive and compliance-driven workloads to professional facilities. Commit rates at the leading provider, GDS, stand near 93%, underscoring persistent demand for secure, carrier-neutral space. Retail colos differentiate through service catalogs that bundle backup-as-a-service and archiving, driving incremental purchases of mass-capacity storage arrays.

Hyperscale and cloud-service providers, however, post the fastest 8.22% CAGR as Alibaba, Tencent, Huawei Cloud, and ByteDance accelerate AI cluster deployments. Their three-year capex plans lock in forward buy-tiers for SSDs, pushing flash suppliers toward long-term supply commitments. Enterprise-owned on-premises halls shrink as firms face PUE ceilings and skill shortages. Edge micro data centers are located in factories and telecom central offices, but they represent a small sliver of the China data center storage market size, albeit one expected to scale rapidly once 5G private networks mature.

By End User: Healthcare Outpaces an IT-Telecom Core

IT and telecom customers delivered 38.70% of 2025 revenues in the China data center storage market; their steady refresh cycles and new-protocol adoption will continue, but growth rates flatten. Conversely, hospitals, genomics labs, and pharmaceutical research institutes are forecast to log 9.05% CAGR as 8K imaging, pathology digitization, and population-scale sequencing projects intensify storage density requirements. China Telecom’s Zhongdian Telecom Yikang subsidiary illustrates telco entry into healthcare clouds, rolling out PACS-friendly block storage racks and S3 tiers across provinces.

Manufacturing absorbs storage for smart-factory video analytics and digital twins, while BFSI focuses on encrypted flash arrays that meet strict data-sovereignty codes. Government clouds require domestic encryption algorithms and zero-trust access controls, thereby steering contracts toward local vendors. Each vertical thus drives distinct technical features, yet common across segments is heightened interest in integrated ransomware protection and immutable snapshots within the China data center storage market.

By Form Factor: Rack Systems Dominate as Composable Architectures Gain Mindshare

Rack-mounted chassis constituted 53.74% of shipments in 2025, reflecting standardized 19-inch cabinet layouts that simplify cable management and airflow modeling. Upgrades now embed E1.S and E3.S ruler drives, lifting per-rack capacity beyond the 1 PB mark. Composable storage grows 5.52% CAGR as cloud-native developers embrace NVMe-oF and PCIe switch fabrics that disaggregate compute and storage resources. Such systems increase utilization by pooling flash at pod level and assigning lanes dynamically.

Blade and modular designs carve out specialized niches—particularly in high-density AI training nodes that require front-loading of GPUs and rear-loading of NVMe bricks. Edge gateways deploy miniature enclosures with fanless cooling for harsh plant-floor environments but remain small in absolute numbers. For the China data center storage market, suppliers that package software-defined orchestration in familiar rack form factors help customers evolve incrementally without forklift upgrades.

By Interface: NVMe Rises as Legacy Protocols Persist in Mixed Fleets

SAS and SATA still represented 57.10% of the 2025 interfaces in the China data center storage market share, a testament to the installed base's inertia and the acceptable throughput for archival and nearline workloads. Nevertheless, NVMe demonstrates a 6.01% CAGR, propelled by PCIe 5.0-driven latency benefits. UNIS and other domestic manufacturers now ship SSDs reading up to 14.9 GB/s, broadening local ecosystem options. Fibre Channel remains entrenched in financial data centers that prioritize lossless transport, while iSCSI endures within mid-market appliance lines.

Operators deploy NVMe shelves for AI inference clusters, yet continue to order SAS disks for content vaults. NVMe-oF gateways let both zones coexist, allowing customers to delay full network upgrades. Over time, protocol abstraction within software-defined controllers will make interface differences invisible; however, for now, the China data center storage market must balance breakthrough speed with predictable costs.

Geography Analysis

Eastern seaboard provinces, Beijing, Shanghai, and Guangzhou, contributed roughly 44.60% of 2025 shipments in the China data center storage market as banks, regulators, and cloud titans demand ultra-low-latency access to core systems. However, PUE caps, land scarcity, and premium utility tariffs prompt an outward pivot toward secondary hubs such as Chengdu, Wuhan, and Xi’an. These cities offer dark-fiber routes to coastlines, while providing 20% lower real estate costs and supportive municipal incentives.

Western clusters in Guizhou, Inner Mongolia, Gansu, and Ningxia are accelerating the fastest under the East-Data-West-Compute blueprint, leveraging cool climates and abundant hydroelectric or wind power. Guizhou’s big-data corridor welcomes both state-backed and private operators, bundling tax breaks with renewable-energy quotas that cut operating expenses by a third. The China data center storage market size for western provinces, therefore, is expected to post double-digit growth, favoring bulk capacity arrays optimized for batch analytics and archival repositories.

Southern regions tie growth to export manufacturing and Hong Kong finance. Guangdong’s Pearl River Delta couples 5G private networks with edge compute nodes near industrial parks, generating sustained NVMe appliance demand. Northern provinces remain policy centers yet exhibit more measured expansion, focusing on system upgrades rather than greenfield sites. Cross-regional workload orchestration, supported by telecom dispatch centers, increases the value of distributed snapshots, WAN-optimized replication, and automated compliance tagging across the China data center storage market.

Competitive Landscape

Competition in the China data center storage market intensifies as domestic suppliers close technology gaps with multinational companies. Inspur captured 11.4% share in Q1 2024, posting 13.6% sales growth on the back of hyper-converged clusters for finance and healthcare customers. YMTC surpassed Samsung in domestic SSD unit sales during 2024’s Singles’ Day, indicating rising confidence in local flash brands. Huawei continues to pioneer magneto-electric drives promising 90% lower power draw and tape-class cost, aligning perfectly with energy-efficiency mandates.

International vendors retain corporate accounts through long-standing service and compatibility contracts; however, export-control risks prompt them to localize production and firmware. ZTE expands its portfolio into distributed object systems, targeting telecom and rail operators, while GDS and VNET invest in self-developed cloud storage software to deepen vertical integration. Start-ups focus on Kubernetes-native storage, erasure-coding parity engines, and zero-trust snapshot validation, vying for white-space segments such as edge federated learning.

Vendor strategies converge on tight coupling between hardware, data-protection software, and orchestration APIs. Partnerships with domestic silicon houses, AI accelerator firms, and renewable-energy providers create joint value propositions. Compliance with China-specific cryptographic regulations and support for confidential computing frameworks further distinguish bids. Against this backdrop, the China data center storage market rewards firms delivering turnkey AI pipelines, multi-protocol tiering, and proactive cybersecurity analytics.

China Data Center Storage Industry Leaders

Huawei Technologies Co., Ltd.

Alibaba Cloud Computing Co., Ltd.

Inspur Electronic Information Industry Co., Ltd.

Dell Technologies Inc.

Hewlett Packard Enterprise Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: YMTC began shipping 5th-generation 3D TLC NAND with 294 layers, achieving 20 Gb/mm² density and bolstering domestic flash competitiveness

- June 2023: Alibaba Group announced USD 53 billion investment in AI and cloud infrastructure over three years, marking the country’s largest private compute project

- March 2025: GDS Holdings reported Q4 2024 revenue of RMB 2.69 billion, up 9.1% YoY, and raised 2025 revenue guidance to up to RMB 11.59 billion

- April 2025: Huawei launched its AI Data Lake Solution, integrating OceanStor A-series high-performance flash with OceanStor Pacific object storage and OceanProtect backup

- June 2025: HiCloud signed an agreement to build China’s first offshore wind-powered underwater data center near Shanghai, pioneering sustainable storage models

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China data center storage market as the value of new on-premise or colocation storage systems, SAN, NAS, DAS, object, and tape arrays deployed inside purpose-built data centers that serve enterprise, hyperscale, edge, and government workloads. Software bundled with those arrays and the embedded operating environment are counted at transaction price.

Scope Exclusions: Public cloud storage services, consumer external drives, and DRAM modules are outside this scope.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with data center operators in Beijing, Chengdu, and Guangzhou, procurement heads at domestic cloud providers, and storage architects from multinational OEMs. These discussions tested value share splits, typical usable-to-raw capacity ratios, and emerging NVMe adoption intent, thereby filling gaps uncovered during desk analysis.

Desk Research

We began with authoritative Chinese sources such as the Ministry of Industry and Information Technology, CAICT capacity bulletins, and customs shipment tables that clarify unit inflows. To gauge installed rack density and refresh cycles, our analysts reviewed technical white papers from the Open Data Center Committee and quarterly disclosures from leading array manufacturers filed with the Shanghai and Shenzhen exchanges. Broader context came from PUE guidelines in the National Development and Reform Commission's "East-Data West-Compute" program, patent trends mined through Questel, and IT hardware sell-through signals captured in Dow Jones Factiva and D&B Hoovers. The sources cited are illustrative; additional open and paid references were consulted to cross-validate every data point.

Market-Sizing & Forecasting

A top-down reconstruction links annual server rack additions with average terabytes per rack, which are then priced by weighted average ASP to size 2024 hardware revenue. Selective bottom-up checks, channel inventory sweeps, and sampled vendor invoices adjust totals by plus or minus two percent. Key variables in the model include rack adds, flash-to-HDD mix, edge site rollouts, hyperscale CAPEX, energy caps, and RMB-USD exchange paths. Multivariate regression, validated by primary experts, projects each driver and feeds a five-year ARIMA overlay for scenario stress. Gaps in vendor roll-ups are bridged using form-factor market share proxies from Marklines-style shipment data.

Data Validation & Update Cycle

Outputs pass a three-step review: variance scans against historical series, peer review by a senior analyst, and an automated alert if quarterly array imports deviate beyond one standard deviation. The study refreshes annually, with interim updates issued when policy or supply shocks materially move the baseline.

Why Mordor's China Data Center Storage Baseline Commands Reliability

Published estimates often diverge because firms select different hardware mixes, price points, and refresh cadences. Our disciplined scope, anchored to physical array deployments rather than broad "data storage," keeps the base year modest and reproducible.

Key gap drivers stem from rivals folding in enterprise backup appliances shipped to offices, projecting aggressive flash pricing curves without channel checks, or updating models only every three years when RMB volatility can distort value.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.95 B (2025) | Mordor Intelligence | NA |

| USD 8.74 B (2024) | Global Consultancy A | Counts all enterprise storage hardware, relies on vendor revenue roll-ups, omits double-count adjustments |

| USD 15.94 B (2025) | Industry Research Firm B | Bundles cloud storage services and consumer drives, applies macro multipliers without shipment validation |

Taken together, the comparison shows that Mordor's numbers sit at the intersection of verifiable shipment flows, transparent assumptions, and a refresh cadence that keeps investors and planners grounded in today's realities.

Key Questions Answered in the Report

What is the current size of the China data center storage market?

The market is valued at USD 3.08 billion in 2026 and is projected to reach USD 3.81 billion by 2031, growing at a 4.38% CAGR.

Which storage technology leads in China today?

Storage Area Networks hold the top position with 45.83% market share in 2025, thanks to strong uptake in finance and telecom sectors.

How fast are all-flash arrays growing?

All-flash arrays are expanding at a 7.55% CAGR, the fastest among primary storage types, driven by AI inference and power-efficiency mandates.

Why are western provinces gaining storage investment?

The East-Data-West-Compute initiative channels workloads to inland regions offering cheaper renewable power and ample land, boosting storage demand there.

Which end-user vertical shows the highest growth?

Healthcare and life sciences lead with a 9.05% CAGR as hospitals adopt AI imaging and genomic sequencing platforms requiring substantial storage capacity.

How do power-use-efficiency regulations affect new builds?

Tier-1 cities cap PUE at 1.3, motivating operators to deploy flash arrays and advanced cooling to meet efficiency targets without compromising density.

Page last updated on: