Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

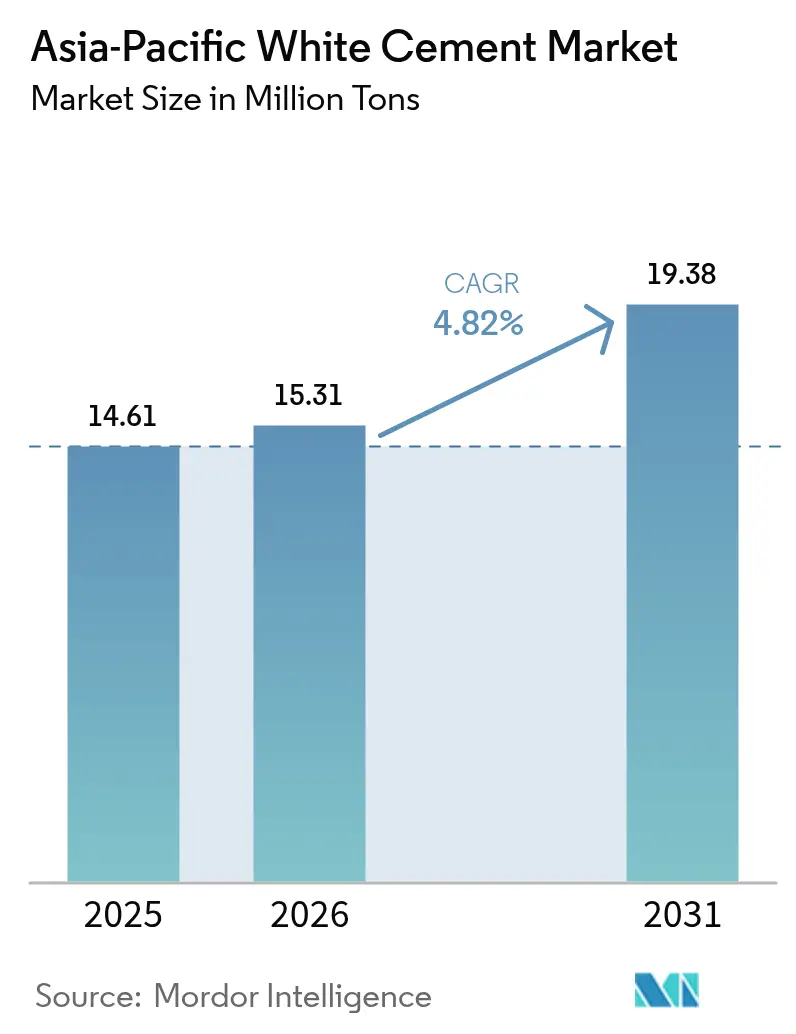

| Base Year Market Size (2025) | 14.61 Million tons |

| Market Volume (2026) | 15.31 Million tons |

| Market Volume (2031) | 19.38 Million tons |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

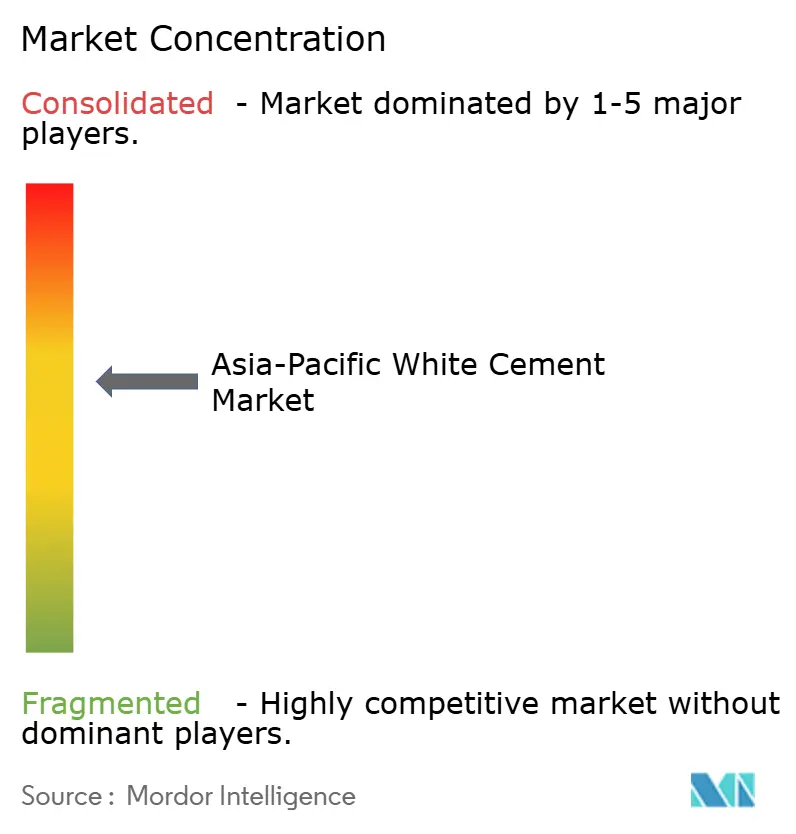

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific White Cement Market Analysis by Mordor Intelligence

The Asia-Pacific White Cement Market size is projected to be 14.61 million tons in 2025, 15.31 million tons in 2026, and reach 19.38 million tons by 2031, growing at a CAGR of 4.82% from 2026 to 2031. As delayed megacity projects commence, demand is increasing. This growth is further driven by the scaling of precast and 3-D-printed components, along with building-code revisions that mandate cool-roof requirements in key urban centers. While China continues to dominate in volume, Vietnam is rapidly establishing itself as the fastest-growing export hub. Simultaneously, India is expanding its capacity to cater to premium architectural segments. In response to tightening carbon policies, there has been a marked shift toward low-carbon formulations. This shift is compelling established producers to not only certify their products but also integrate waste-heat recovery and acquire low-carbon clinker assets, all in an effort to protect their margins. Despite an underutilization of gray-cement capacity, supply elasticity remains constrained. This is primarily due to the scarcity of new white-clinker permits, which keeps overall utilization rates elevated.

Key Report Takeaways

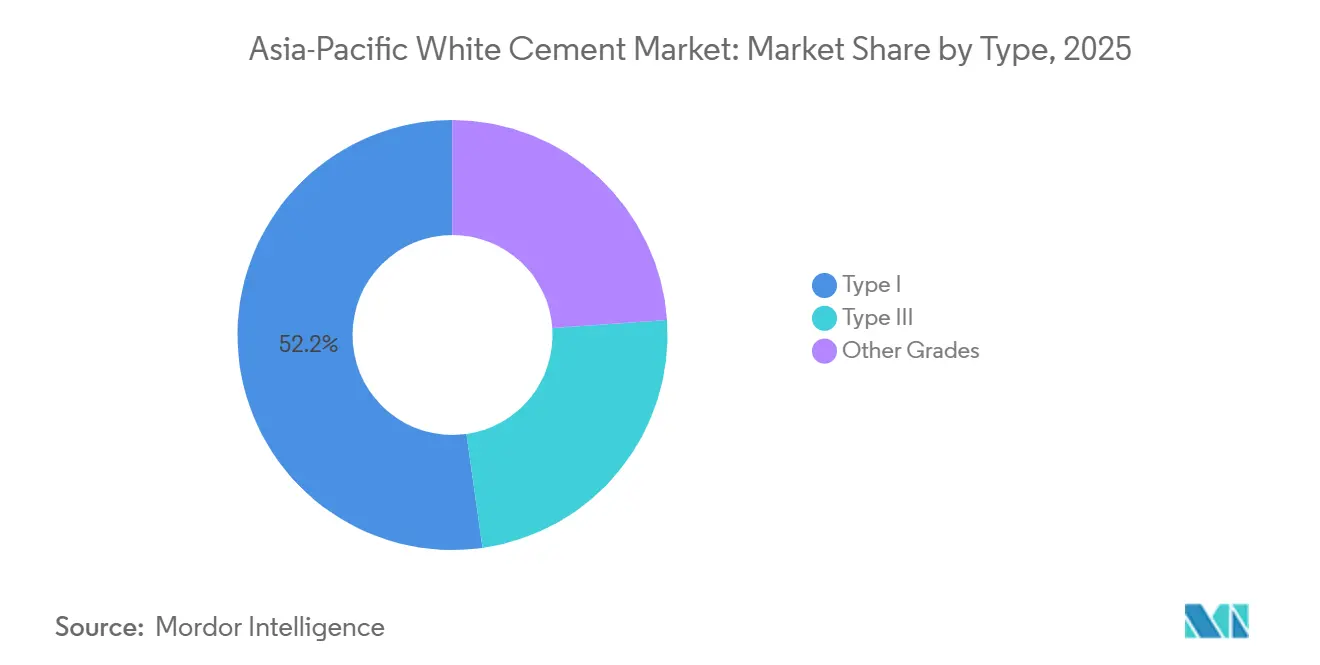

- By type, Type I held 52.22% of the Asia-Pacific white cement market share in 2025 and is advancing at a 5.12% CAGR to 2031.

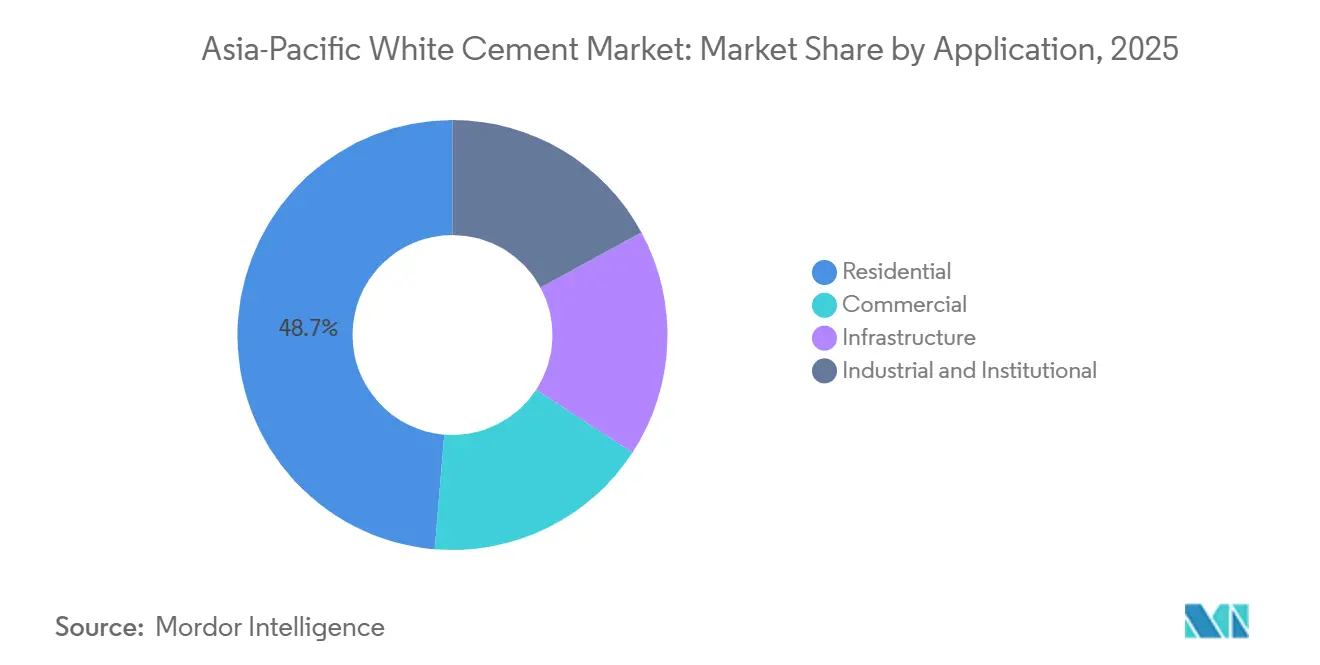

- By application, residential projects accounted for 48.69% share in 2025, while commercial projects are projected to expand at a 5.23% CAGR through 2031, the fastest among all end uses.

- By geography, Vietnam is forecast to post the highest 6.89% CAGR over 2026-2031, while China retained 75.12% of the Asia-Pacific white cement market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific White Cement Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction rebound across Asia-Pacific megacities | +0.50% | China, India, Indonesia, with spillover to Thailand and Malaysia | Medium term (2-4 years) |

| Scaling-up of precast, 3D-printed components | +0.50% | China, Japan, Australia, early adoption in Singapore and South Korea | Long term (≥ 4 years) |

| Aesthetic premium in luxury and heritage projects | +0.40% | India, China, Thailand, concentrated in tier-1 cities and UNESCO sites | Short term (≤ 2 years) |

| Cool-roof mandates for heat-island mitigation | +0.40% | India (Telangana, Gujarat), China (Shanghai, Guangzhou), Japan | Medium term (2-4 years) |

| Green-stimulus funding for low-carbon façades | +0.40% | China, South Korea, Japan, with pilot programs in Vietnam and Malaysia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Rebound Across Asia-Pacific Megacities

As metro-rail stations, airport terminals, and mixed-use complexes, previously delayed by the pandemic, transition to the construction phase, the demand for white cement is surging. In Hong Kong and Nusantara, Indonesia's new capital, capital works spending mandates white-cement façades to adhere to solar-heat-gain regulations. Meanwhile, in Vietnam, credit-backed public projects are bolstering order books, providing a buffer against softness in the residential sector.

Scaling-Up of Precast, 3-D-Printed Components

Major public and private projects have begun to use glass-fiber-reinforced or ultra-high-performance concrete panels molded off-site with Type I formulations, cutting labor and ensuring a uniform color across complex geometries. Japan’s pilot low-carbon clinker feedstock is feeding into these precast lines and positioning suppliers for net-zero building tenders.

Cool-Roof Mandates for Heat-Island Mitigation

Telangana’s 2024 building code and Shanghai’s 2025 green building standard set a minimum solar-reflectance threshold that white-cement roofs meet without added coatings[1]Telangana Government, “Energy Conservation Building Code 2024,” telangana.gov.in . Field monitoring in Ahmedabad recorded lower peak indoor temperatures, reducing cooling loads significantly.

Green-Stimulus Funding for Low-Carbon Façades

China allocates funds in its green-stimulus package for façade retrofits, while South Korea provides tax credits that cover costs for certified low-carbon materials. In Vietnam, producers with carbon footprints below 600 kg CO₂ per tonne are able to secure a preferred-supplier status in public tenders.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution by TiO₂-based pigments | -0.30% | China, India, with pilot adoption in Southeast Asia | Medium term (2-4 years) |

| Carbon-border-adjustment levies on exports | -0.30% | India, China, Vietnam, affecting EU and UK export routes | Short term (≤ 2 years) |

| Limited regional clinker capacity build-out | -0.30% | China, Vietnam, Thailand, with spillover to Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution by TiO₂-Based Pigments

Gray cement, now enhanced with Nano-TiO₂, achieves a high SRI rating at a lower cost. This development poses a challenge to the uptake of white cement, especially in price-sensitive applications, such as flooring and non-structural elements. However, weathering tests continue to favor Type I cement for its durability, safeguarding its core structural demand.

Limited Regional Clinker Capacity Build-Out

White-clinker lines require a low-iron feedstock and precise kiln control. China froze new permits in 2025, and Vietnam’s new capacity is limited to an SCG Low-Carbon Line. This has kept supply tight, even as gray-cement kilns remain idle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Type I Retains Leadership Through Structural Versatility

Type I captured 52.22% of the Asia-Pacific white cement market share in 2025 and is projected to expand at a 5.12% CAGR during the forecast period of 2026-2031, underpinning the largest slice of the Asia-Pacific white cement market size growth. With a 28-day strength suitable for load-bearing precast applications without the need for admixtures, it ensures the color uniformity essential for high-rise façades. Birla White, after securing metro-rail cladding contracts in Delhi and Mumbai, experienced notable sales growth. Type III, which was once the preferred choice for rapid repairs, is now losing traction. Ready-mix suppliers are shifting towards Type I with added accelerators, streamlining their inventory. Meanwhile, photocatalytic and self-cleaning grades, which constitute a growing portion of the volume, are on a positive growth trajectory. This surge is attributed to tunnel and noise-barrier tenders, aligned with Japan’s resilience guidelines.

Type I's demand is further bolstered by seismic-zone specifications in China. These specifications advocate for ultra-thin UHPC panels, which not only reduce dead loads but also uphold the integrity of façades. Developers tend to adhere to Type I, even when hybrid pigment options emerge, primarily because transitioning to another grade necessitates re-approval of structural drawings. While short-cycle residential flooring, where color precision is less critical, serves as the primary market for TiO₂-pigment substitutes, this segment represents only a small portion of the region's white cement consumption.

By Application: Commercial Projects Drive Next Leg of Growth

Commercial construction is projected to record the fastest 5.23% CAGR during the forecast period of 2026-2031, overtaking residential volume by the end of the decade as luxury retail, hospitality, and heritage-restoration pipelines expand. In Thailand, several five-star resorts are under construction, with developers selecting white-cement finishes to mitigate tropical humidity and reduce algae staining. Meanwhile, in India, heritage sites, led by the Taj Mahal restoration, have experienced significant material consumption, with a specific focus on color-matched mortars.

Residential construction accounted for 48.69% of the 2025 volume but faces near-term challenges due to credit tightening in Vietnam and Indonesia. Infrastructure projects, including metro stations and airport terminals, continue to grow steadily. This growth is driven by government contracts that prioritize low-maintenance cladding meeting increasingly stringent reflectance standards. Demand from industrial and institutional sectors, such as pharmaceutical and food-processing facilities, has shown consistent growth. This segment remains resilient, as hygiene regulations mandate non-porous, chemically resistant surfaces, regardless of fluctuations in the real estate market.

Geography Analysis

China controlled 75.12% of the Asia-Pacific white cement market size in 2025 and remains the largest demand center. Demand was primarily concentrated in coastal provinces, where new green-building codes incentivized façades with a Solar Reflectance Index (SRI) of 78 or higher. Proximity to low-iron limestone allowed Guangdong, Fujian, and Shandong to supply a significant portion of the nation's capacity. However, a national cap on clinker output curtailed further expansions, leading to sustained high utilization rates. A stimulus package supported retrofits that are set to add additional volume through 2027.

Vietnam is the growth outlier at a 6.89% CAGR during the forecast period of 2026-2031, as SCG’s 8,000 TPD low-carbon line turns the country into an export hub for Australia and the Americas. SCG's establishment of a low-carbon line is positioning Vietnam as an export hub for both Australia and the Americas. Draft regulations mandating a limit of 600 kilograms of CO₂ per ton for products in public projects are likely to benefit SCG and other certified plants. While the utilization of gray-cement kilns declined in 2025, white-clinker lines operated at full capacity, indicating a bottleneck that keeps prices elevated.

In 2025, a consortium of India, Japan, South Korea, Thailand, Indonesia, Malaysia, Australia, and other Asia-Pacific nations contributed to the remaining market volume. UltraTech is on track to double Birla White's capacity by 2027. Meanwhile, JK Cement has allocated significant investments for additional capacity. In Telangana, a cool-roof mandate is integrating white cement into compliance for commercial structures over 500 square meters. Japan’s Sumitomo Osaka Cement is piloting CO₂-recycling artificial limestone, and Australia is adopting non-combustible white-cement panels for BAL-40 bushfire zones[2]Australian Building Codes Board, “National Construction Code BAL-40,” abcb.gov.au .

Competitive Landscape

The Asia-Pacific white cement market is moderately consolidated. In 2025, UltraTech took a significant step by acquiring a majority stake in India Cements, boosting its capacity and initiating efficiency upgrades. SCG, after being the pioneer in securing the TIS 2594-2567 certification, achieved strong market penetration for its Low Carbon Cement Gen3 in Thailand. In a notable move in 2024, CEMEX exited the Philippines, channeling its capital towards regions boasting a higher demand for white cement. Meanwhile, in 2026, Sumitomo Osaka Cement made a comeback in the Philippines, acquiring a stake in Philcement, eyeing the nation's infrastructure opportunities.

Strategic focuses are evident: low-carbon innovations, vertical integration, and targeted mergers and acquisitions. In 2025, Hume Cement sold its concrete division to YTL, redirecting its focus towards the more lucrative white-cement segment. Technology partnerships are on the rise: Aalborg White showcased its unmatched expertise by delivering thousands of GFRC panels for Zaha Hadid’s Changsha project. Cementir’s D-Carb, with its innovative calcined-clay substitution, achieved a significant reduction in CO₂ emissions, strategically positioning the company ahead of impending carbon pricing trends.

Asia-Pacific White Cement Industry Leaders

Cementir Holding NV

CIMSA

J.K. Cement Ltd

UltraTech Cement Ltd

SCG International Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Adani Group (Ambuja Cement) initiated talks to acquire Heidelberg’s India unit for USD 1.2 billion, aiming to integrate 10.2 million tons of capacity.

- October 2024: Adani Group appointed Jefferies and Axis Capital to explore merging Ambuja and ACC, creating an entity valued above INR 2 trillion.

Asia-Pacific White Cement Market Report Scope

White cement is a high-quality Portland cement, free from iron and manganese, specifically designed for decorative and structural applications that require a pure white color. Common uses include mosaics, terrazzo flooring, and tile grouting. It offers high durability, water resistance, quick setting, and effective blending with pigments.

The white cement market is segmented by type, application, and geography. By type, the market is segmented into type I, type III, and other grades. By application, the market is segmented into commercial, residential, infrastructure, and industrial and institutional. The report also covers the market size and forecasts for white cement in 9 countries across major Asia-Pacific regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

By Type

| Type I |

| Type III |

| Other Grades |

By Application

| Commercial |

| Residential |

| Infrastructure |

| Industrial and Institutional |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Thailand |

| Indonesia |

| Malaysia |

| Vietnam |

| Australia |

| Rest of Asia-Pacific |

| By Type | Type I |

| Type III | |

| Other Grades | |

| By Application | Commercial |

| Residential | |

| Infrastructure | |

| Industrial and Institutional | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Malaysia | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large will Asia-Pacific white cement demand be by 2031?

The Asia-Pacific white cement market size stands at 15.31 million tons in 2026, and it is projected to reach 19.38 million tons by 2031 at a 4.82% CAGR.

Which country is the fastest-growing white-cement exporter?

Vietnam, forecast to post a 6.89% CAGR through 2031 on the back of SCG’s new low-carbon clinker line.

What is driving commercial uptake of white cement?

Luxury retail and hospitality projects plus heritage restorations favor its color stability and durability, supporting a 5.23% CAGR in commercial uses.

How are cool-roof mandates influencing demand?

Building-code revisions in Telangana and Shanghai set minimum solar-reflectance thresholds that white-cement roofs meet, pulling the material into compliance spending.

What is the main competitive strategy among leading producers?

Companies are investing in low-carbon formulations and vertical integration while pursuing selective M&A to secure clinker assets and defend margins under emerging carbon pricing.

Page last updated on: