Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

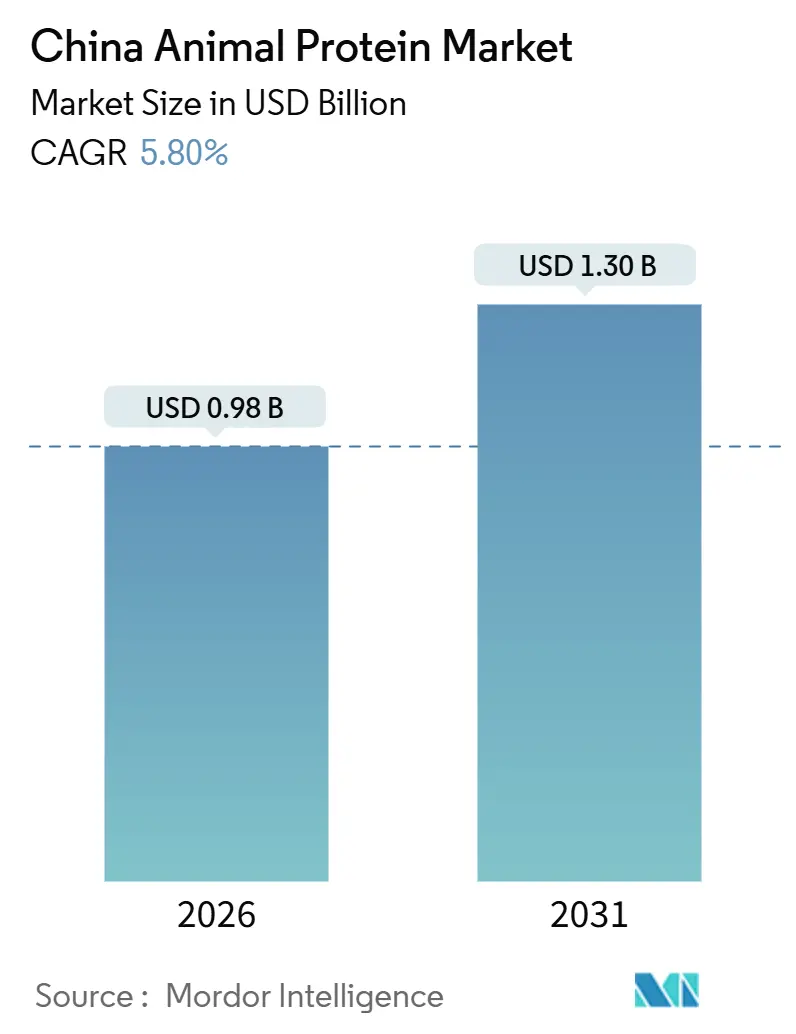

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.30 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Animal Protein Market Analysis by Mordor Intelligence

The China animal protein market size is valued at USD 0.98 billion in 2026 and is forecast to reach USD 1.30 billion by 2031, reflecting a 5.80% CAGR during 2026–2031. Beijing's push for domestic protein self-sufficiency, coupled with significant funding for dairy and livestock digitalization and a surge in precision fermentation output, drives the steady climb. The focus on whey protein as the volume anchor highlights its established role in the market, while insect protein experiences the fastest growth due to its sustainability and nutritional benefits. Urban centers, on the other hand, offer premium pricing for organic-certified ingredients, reflecting growing consumer preference for healthier and environmentally friendly options. Demand broadens across both consumer and B2B channels, fueled by livestreaming commerce, which enhances product visibility, functional food reformulations that cater to evolving dietary needs, and clinical nutrition prescriptions that address specific health concerns. As multinationals localize specialty production to meet stricter facility audits and domestic processors enhance quality systems to tap into export opportunities, competitive intensity escalates, creating a dynamic and rapidly evolving market landscape.

Key Report Takeaways

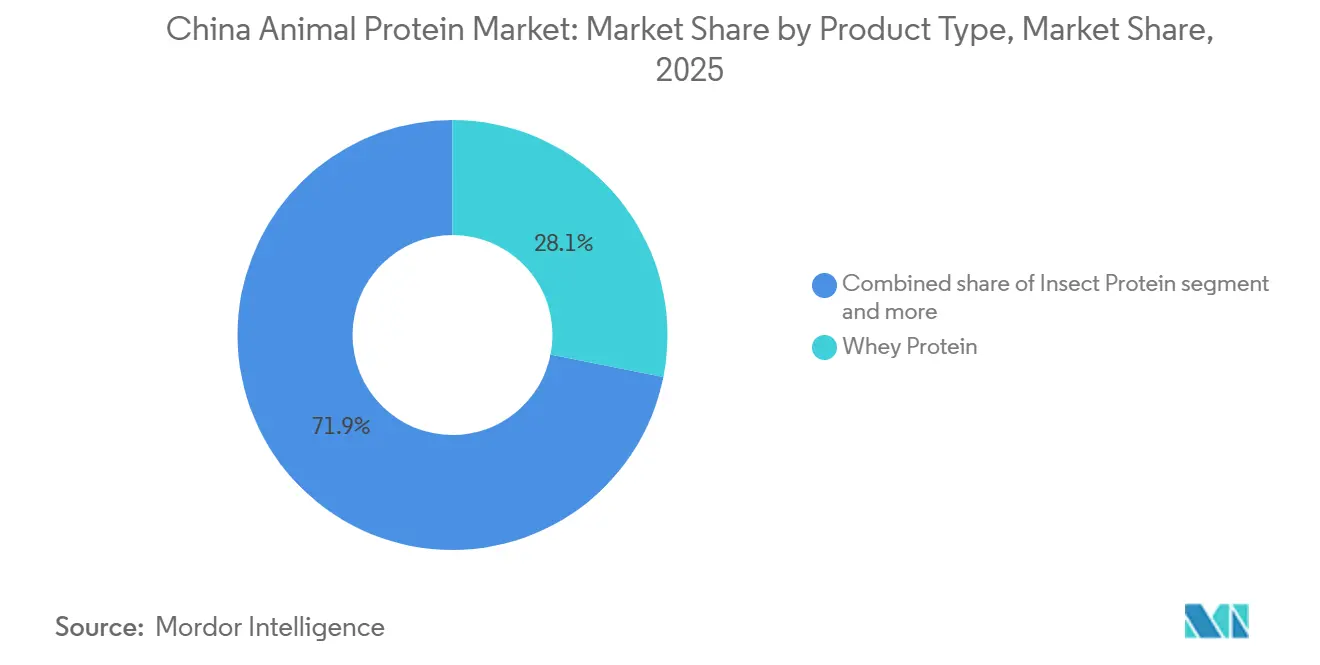

- By protein type, whey commanded 28.12% of China's animal protein market share in 2025, while insect protein is projected to advance at a 7.13% CAGR to 2031.

- By category, the conventional segment led with 68.13% revenue share in 2025; the organic segment is tracking an 8.41% CAGR through 2031.

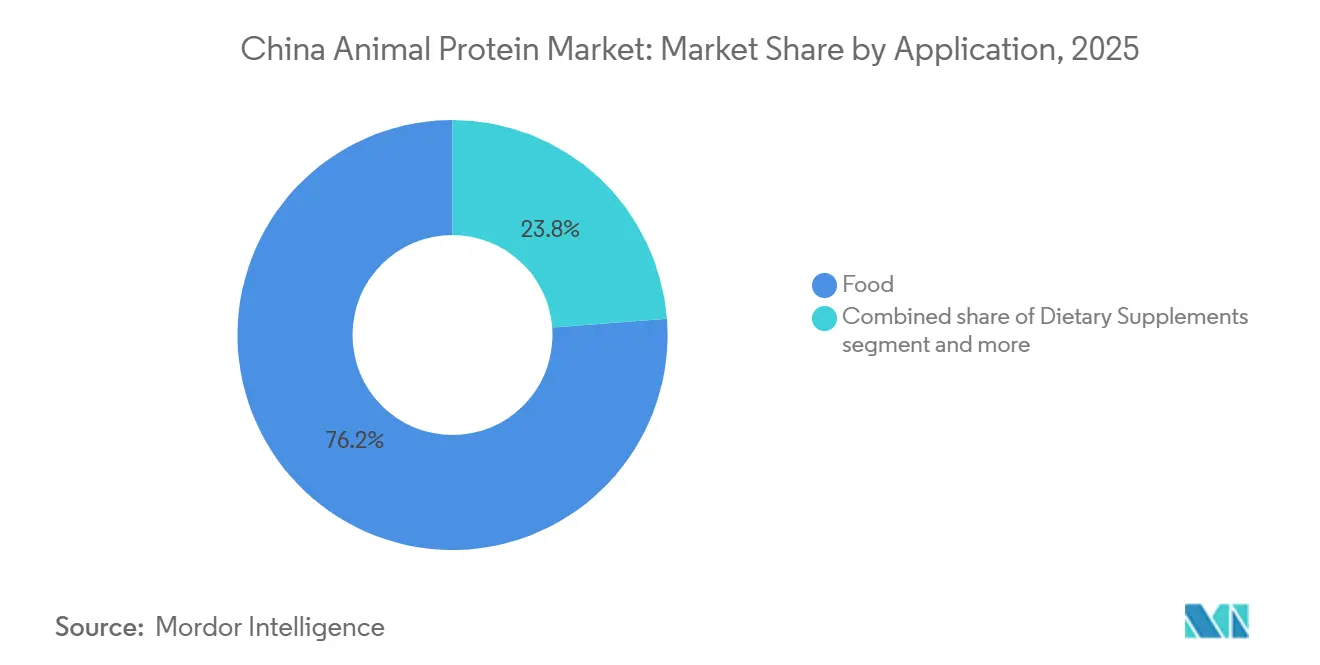

- By application, food held 76.21% share of the China animal protein market size in 2025, whereas sport and performance nutrition is expected to expand at a 7.52% CAGR during the same period.

- By geography, Inner Mongolia, Heilongjiang, and Hebei produced 62% of national raw milk output in 2025, underpinning the largest regional share; Tier-1 coastal provinces are forecast to post the quickest growth at a 6.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Animal Protein Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in high-protein demand among aging and fitness-focused consumers | +1.2% | Tier-1 and Tier-2 cities | Medium term (2–4 years) |

| Government-backed modernization of dairy and livestock supply chains | +1.0% | Dairy belts in Inner Mongolia, Heilongjiang, Hebei | Long term (≥4 years) |

| Expansion of functional food and beverage and clinical nutrition applications | +0.9% | Coastal provinces | Medium term (2–4 years) |

| E-commerce and livestreaming channels widening ingredient access | +0.7% | National | Short term (≤2 years) |

| AI-enabled precision-fermentation capacity scale-up | +0.6% | Shanghai, Shenzhen, Tianjin | Long term (≥4 years) |

| Carbon-credit incentives for low-methane proteins | +0.4% | Pilot provinces in West China | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Surge in high-protein demand among aging and fitness-focused consumers

In 2024, China's population aged 60 and above reached 310.31 million[1]Source: China's National Bureau of Statistics, “STATISTICAL COMMUNIQUÉ OF THE PEOPLE'S REPUBLIC OF CHINA ON THE 2024,” stats.gov.cn. This demographic shift highlights the growing focus on health and wellness among the elderly population. Gym memberships surged by 19% year-on-year, totaling 73 million, reflecting an increased interest in fitness and active lifestyles. Influencers, through livestreams, are not just promoting powders but also bundling them with diet consultations, effectively drawing in both the elderly and athletes into a unified purchasing strategy. These livestreams serve as a powerful marketing tool, creating a sense of community and trust among consumers. Brands are now pivoting, reformulating products to include joint-support collagen peptides and slow-release casein, specifically catering to overnight recovery demands. This shift in consumption patterns is amplifying the China animal protein market, as consumers increasingly spend more on premium formats, driven by a desire for better health outcomes and enhanced product functionality.

Government-backed modernization of dairy and livestock supply chains

China's CNY 50 billion National Smart Agriculture Action Plan is channeling funds into IoT herd monitoring, automated milking, and blockchain traceability, primarily in its major dairy provinces[2]Source: United States Department of Agriculture, “National Smart Agriculture Action Plan Published,” apps.fas.usda.gov. These initiatives aim to modernize dairy farming practices, improve operational efficiency, and enhance product quality. Fonterra’s Wuhan applications center is accelerating hydrolysate prototypes in collaboration with local infant-formula partners, reducing formulation cycles to just 12 months. This collaboration enables faster product development and strengthens partnerships within the infant formula segment. Meanwhile, dairy giants Mengniu and Yili have invested CNY 8.2 billion in filtration upgrades, enhancing the purity of domestic milk-protein concentrates and bridging the cost gap with imports. These upgrades are expected to improve the competitiveness of domestic products in both local and international markets. A decree set for 2025 will require real-time milk-quality data from all farms with over 500 cows, intensifying compliance scrutiny and ensuring higher quality standards across the industry. These infrastructural advancements and regulatory measures are bolstering the availability of high-grade inputs, propelling the growth of China's animal protein market.

Expansion of functional food and beverage and clinical nutrition applications

In 2025, SAMR approved 112 new SKUs of protein-fortified infant formulas, significantly boosting the adoption of lactoferrin and alpha-lactalbumin due to their nutritional benefits for infant health. Arla Foods Ingredients teamed up with Zhongbai Xingye, incorporating whey concentrates into ready-to-eat meals, a segment that experienced a 28% surge in volume, driven by increasing consumer demand for convenient and protein-rich food options. Bakeries are replacing emulsifiers with egg white protein, reaping 15-20% in cost savings while enhancing dough elasticity, which improves the overall quality and texture of baked goods. Following the 2025 Clinical Nutrition Guidelines, which recommended supplementation for seniors in hospitals to address malnutrition and support recovery, hydrolyzed collagen and casein hydrolysates made their way into medical nutrition. As applications broaden across various industries, the addressable market for animal proteins in China continues to expand, presenting significant growth opportunities.

E-commerce and livestreaming channels widening ingredient access

In 2025, Alibaba reported a 41% surge in B2B transactions for animal-protein ingredients, easing procurement hurdles for smaller manufacturers by providing streamlined access to suppliers and reducing costs. Douyin's livestreams raked in CNY 12.3 billion from supplement sales, bolstered by real-time quality tests that fostered consumer trust and highlighted product transparency. Customized collagen blends from Guangdong's VTR Bio-Tech, marketed directly to consumers through online platforms, showcased the scalability of niche brands by effectively targeting specific consumer needs. JD Logistics expanded its cold-chain services to cover 95% of county-level markets, significantly reducing spoilage rates for whey isolates and ensuring product freshness. Meanwhile, digital distribution channels have expedited market entry for newcomers, intensifying competition in China's animal protein sector by lowering barriers and enabling faster product launches.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility in raw milk & feed commodities | -0.8% | Dairy belts in Inner Mongolia, Heilongjiang, Hebei | Short term (≤2 years) |

| Intensifying competition from plant & cultivated proteins | -0.6% | Tier-1 cities and coastal innovation zones | Medium term (2–4 years) |

| Facility-registration & tariff barriers on imported inputs | -0.5% | National | Medium term (2–4 years) |

| Quality-assurance talent gaps at emerging domestic producers | -0.3% | Tier-2 and Tier-3 clusters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Price volatility in raw milk and feed commodities

In 2024-2025, Inner Mongolia's milk prices fluctuated between CNY 3.80 and CNY 4.50 per kg[3]Source: China Index, “2024 Inner Mongolia Modern Dairy Industry Index Operation Report,” china-index.io. This volatility was driven by a surge in feed corn prices, which reached CNY 2,900 per ton in Q3 2025, significantly tightening the margins for processors. Additionally, logistics delays in soybean meal distribution caused domestic prices to rise to CNY 4,200 per ton, further intensifying cost pressures across the supply chain. In response to these financial strains, New Hope Liuhe divested CNY 1.2 billion in non-core assets to strengthen its liquidity position and maintain operational stability. At the same time, vertical integration efforts gained momentum, with Mengniu increasing its self-supplied milk intake to 35% by the end of 2025, aiming to mitigate external supply risks and improve cost efficiency. However, persistent commodity price fluctuations continue to erode profitability and hinder expansion efforts within China's animal protein sector, creating a challenging environment for market players.

Intensifying competition from plant and cultivated proteins

CellX and Joe's Future Food secured USD 180 million for their cultivated-meat pilots, aiming to achieve commercialization by 2028. This funding underscores the increasing investor interest in alternative protein solutions as the industry transitions toward sustainable food production. In 2025, plant proteins accounted for a significant portion of the sports-nutrition volume, up from two years earlier, driven by their allergen-free appeal and increasing consumer preference for plant-based options. Kerry Group, in their Q4 2024 earnings report, observed a notable shift in consumer demand toward plant-forward ready-to-drink (RTD) beverages, reflecting the broader trend of plant-based innovation in the beverage market. The State Administration for Market Regulation (SAMR) reduced precision-ferment protein approval cycles to 12 months in 2025, significantly easing market entry for companies in this space. As alternative proteins continue to gain traction, they are increasingly limiting the growth potential of animal-based products in China's animal protein market, signaling a transformative shift in consumer preferences and market dynamics.

Segment Analysis

By Protein Type: Whey Dominance Meets Insect Protein Disruption

In 2025, whey protein dominated China's animal protein market, securing a 28.12% share. Its robust standing is attributed to cost efficiency, bolstered by plentiful cheese-whey streams and a surging demand in sports nutrition. Glanbia's upgrade of its Suzhou facility, boosting isolate purity to 92%, solidified its lead in the premium whey sector. Whey protein's versatility in applications, ranging from muscle recovery products to meal replacements, has further reinforced its market dominance. Meanwhile, casein, collagen, gelatin, and egg protein cater to niche markets like bakery, medical, and beauty. Notably, ventures such as Darling-Tessenderlo are amplifying the supply of pharmaceutical-grade gelatin, which is increasingly used in advanced drug delivery systems and cosmetic formulations. This expanding supply base has not only curbed price volatility but also spurred innovation in downstream applications, enabling manufacturers to explore new product formulations and target diverse consumer needs.

Insect protein is set to be the fastest-growing segment, eyeing a 7.13% CAGR through 2031. Its ascent is fueled by regulatory nods for black soldier fly meal in aquaculture and poultry, marking it as a sustainable, high-value choice. Pilot initiatives showcasing cricket-protein bars highlight the potential of hybrids to boost amino-acid profiles, sidestepping regulatory challenges. Additionally, insect protein's low environmental footprint, including reduced land and water usage compared to traditional protein sources, has garnered significant attention from both producers and policymakers. As China diversifies its protein sources, insect protein is transitioning from experimental phases to commercial viability, driven by a keen interest in functional, eco-friendly feed. This momentum hints at its transformative potential in the protein sourcing landscape and bolstered supply resilience throughout the value chain, paving the way for broader adoption in both human and animal nutrition markets.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Conventional Scale Versus Organic Premium

In 2025, conventional formats captured a dominant 68.13% share of China's animal protein market revenue. This dominance is largely attributed to mass-market bakeries and feed mills, which favor these formats for their cost efficiency and reliable supply. Companies like Bluestar Adisseo bolstered their leadership position by investing in additional capacities, enhancing both scale and price competitiveness. Furthermore, with rising export demand for antibiotic-free products, producers have modernized their herd-health systems, all while keeping conventional output volumes steady. The extensive reach of this segment provides a robust revenue base, even as the market shifts towards premium offerings. Conventional formats remain a cornerstone of the market due to their ability to cater to large-scale demand while ensuring affordability, making them indispensable for both domestic and export-oriented supply chains.

Organic proteins are on a rapid ascent, with projections indicating an 8.41% CAGR through 2031. This growth is bolstered by blockchain-driven traceability, accelerated certification cycles slashing approval times to 18 months, and a surge in consumer trust regarding ethical sourcing. Organic whey is now fetching a 30–40% price premium. Yili's recent launch of an organic infant formula underscores the nation's production capabilities. Urban consumers are allocating nearly 18% of their grocery spending to organic items, highlighting a pronounced shift towards premiumization. To navigate this landscape, producers are adopting dual strategies: nurturing organic pastures while capitalizing on conventional lines, striking a balance between value and volume. The increasing focus on organic proteins reflects a broader consumer trend toward health-conscious and environmentally sustainable choices, further driving innovation and investment in this segment.

By Application: Food Anchors Growth, Sports Nutrition Accelerates

In 2025, food applications dominated China's animal protein market, claiming 76.21% of its total value. Leading the charge, manufacturers in bakery, beverage, and ready-meal sectors harnessed whey concentrates to enhance shelf life and egg whites to bolster dough strength, all while minimizing emulsifier usage. These applications have gained traction due to their ability to meet consumer demand for convenience and quality, particularly in urban areas where processed and ready-to-eat foods are increasingly popular. In the realm of high-protein beverages, ready-to-drink (RTD) shakes, featuring a blend of hydrolyzed collagen and whey isolates, made significant inroads, championing muscle and joint health. These beverages cater to health-conscious consumers seeking functional benefits in their daily diets. Dietary supplements, with ingredients like casein hydrolysates and lactoferrin, resonate with the 2025 Clinical Nutrition Guidelines, emphasizing sarcopenia prevention. This steady growth across food and supplement channels underscores their foundational role in market consumption, driven by evolving consumer preferences for health and wellness.

Sports and performance nutrition is poised to be the fastest-growing segment, with a projected CAGR of 7.52% through 2031. The burgeoning fitness culture among Gen Z, coupled with the rise of boutique gyms, has catalyzed an influencer-driven embrace of high-protein and recovery-centric products. These products are increasingly tailored to meet the specific needs of fitness enthusiasts, offering targeted benefits such as muscle recovery and enhanced performance. Young, urban consumers, drawn to the benefits of an active lifestyle, are increasingly gravitating towards innovative drinks enriched with collagen and whey. Additionally, the surge in personal-care ingestibles, particularly collagen powders promoted on beauty-from-within platforms, has amplified their cross-category allure. These ingestibles not only appeal to fitness-conscious individuals but also to those seeking holistic health and beauty solutions. Collectively, these dynamics position sports nutrition as a central force in shaping the future trajectory of China's animal protein market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, Inner Mongolia, Heilongjiang, and Hebei accounted for 62% of China's raw milk supply, solidifying their role as the backbone of the nation's animal protein market. These regions benefit from favorable climatic conditions and extensive pasturelands, which support large-scale dairy farming. Meanwhile, coastal provinces like Jiangsu, Zhejiang, and Guangdong have become hubs for high-value processing, boasting research and development labs that innovate dairy proteins into functional foods such as protein-enriched beverages and meal replacements. Reflecting their higher per-capita incomes and a robust fitness culture, Tier-1 cities represented 38% of spending on organic and sports nutrition. In contrast, Tier-2 and Tier-3 urban clusters dominated with 54% consumption of conventional proteins in staple foods, driven by affordability and dietary preferences.

Sichuan, Gansu, and Qinghai, located in western provinces, are pioneering carbon-credit schemes that subsidize low-methane feed additives, marking them as frontrunners in sustainable production. These initiatives aim to reduce greenhouse gas emissions while maintaining livestock productivity, aligning with China's broader environmental goals. JD Logistics has expanded its cold chain to cover 95% of county-level markets in the Yangtze River Delta, facilitating same-day delivery of temperature-sensitive whey isolates and minimizing stock-outs for smaller manufacturers. This expansion enhances supply chain reliability and supports the growing demand for high-quality animal protein products. In biotech corridors across Shanghai, Shenzhen, and Tianjin, precision-fermentation startups are integrating yeast-protein into plant-hybrid formulations, reducing reliance on traditional dairy sources and addressing supply chain vulnerabilities.

Hebei and Shandong have positioned themselves as export powerhouses for collagen and gelatin, bolstered by Darling-Tessenderlo's CNY 2.1 billion investment in a joint plant targeting pharmaceutical-grade production. This facility leverages advanced processing technologies to meet the stringent quality standards required for pharmaceutical applications. This regional specialization harmonizes raw-material availability, technological advancements, and logistical efficiency, fostering a unified yet diverse landscape in China's animal protein market.

Competitive Landscape

In a market marked by moderate consolidation, the top five players command a significant share. Multinational giants like Fonterra, Glanbia, Arla, FrieslandCampina, and Kerry find themselves in fierce competition with domestic powerhouses such as Mengniu, Yili, Bluestar Adisseo, and New Hope Liuhe. While some players adopt scale-driven cost leadership, others pursue innovation-led premium strategies. Bluestar Adisseo, riding the wave of rising methionine demand, reported a 17% revenue uptick in H1 2025, reaching CNY 8.51 billion. Furthermore, its ambitious 150,000-ton expansion in Quanzhou solidifies its dominance in the amino-acid sector, enabling it to meet growing domestic and international demand while reinforcing its market leadership.

Arla Foods, banking on its organic credentials, has inked a distribution deal with Zhongbai Xingye, aiming to command price premiums in the ready-meal segment. This partnership allows Arla to tap into a growing consumer base that values organic and sustainable food options, further strengthening its foothold in the Chinese market. Meanwhile, Fonterra's Wuhan facility is making strides in the infant-formula arena, slashing prototype cycles and securing co-development partnerships. By accelerating product development timelines, Fonterra enhances its ability to meet evolving consumer needs and maintain a competitive edge. Demonstrating the nimbleness of domestic biotech, Angel Yeast's 11,000-ton yeast-protein venture achieved certification within a quarter, proudly boasting non-GMO validation. This rapid certification underscores the agility of domestic firms in responding to market demands and regulatory requirements.

As import challenges loom, localization emerges as a strategic buffer. To sidestep SAMR audits and meet the on-shore traceability demands of pharmaceutical contracts, Darling Ingredients and Tessenderlo Group have localized gelatin hydrolysis in Hebei. This move not only ensures compliance with stringent regulations but also positions these companies to capture a larger share of the pharmaceutical-grade gelatin market. On a different front, smaller players like Guangdong VTR Bio-Tech are harnessing the power of e-commerce, directly marketing bespoke collagen blends to consumers. Their strategy has paid off, with a notable 22% growth in 2025, all achieved without significant investments in traditional retail spaces. By leveraging digital platforms, Guangdong VTR Bio-Tech has effectively reached a broader audience while minimizing operational costs. This blend of scale, niche specialization, and innovative channels is amplifying the competitive intensity in China's animal protein landscape.

China Animal Protein Industry Leaders

Arla Foods AmbA

Darling Ingredients Inc.

Fonterra Co-operative Group Limited

Glanbia PLC

Kerry Group PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Darling Ingredients and Tessenderlo Group have established a 50-50 joint venture in Hebei, focusing on collagen peptides and pharmaceutical-grade gelatin. The venture utilizes local rendering inputs to meet stringent facility audit standards.

- September 2025: Bluestar Adisseo has committed CNY 2.1 billion to boost the Quanzhou facility's powder-methionine capacity by 150,000 tons by 2027. This investment aims to strengthen the company's position in the methionine market, catering to the growing demand in the aquafeed industry. Additionally, the company has secured aquafeed contracts to ensure a steady supply chain and market presence.

- June 2025: In Suzhou, Glanbia Nutritionals boosted its whey-isolate capacity by 8,000 tons, achieving a 92% purity level tailored for its sports-nutrition clientele. This expansion aims to meet the growing demand for high-quality protein ingredients in the sports nutrition market, ensuring a consistent supply and enhanced product offerings for its clients.

- April 2024: Fonterra inaugurated a USD 15 million applications center in Wuhan, featuring pilot spray-drying towers. These towers are specifically designed to expedite formulation cycles, enabling the company to enhance its product development processes and bring innovations to market more efficiently.

China Animal Protein Market Report Scope

Casein and Caseinates, Collagen, Egg Protein, Gelatin, Insect Protein, Milk Protein, Whey Protein are covered as segments by Protein Type. Animal Feed, Food and Beverages, Personal Care and Cosmetics, Supplements are covered as segments by End User.

Protein Type

| Casein and Caseinates |

| Collagen |

| Egg Protein |

| Gelatin |

| Insect Protein |

| Milk Protein |

| Whey Protein |

| Other Animal Protein |

By Category

| Conventional |

| Organic |

By Application

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternatives | |

| RTE/RTC Foods | |

| Snacks | |

| Personal Care and Cosmetics | |

| Dietary Supplements | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

| Protein Type | Casein and Caseinates | |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Protein | ||

| By Category | Conventional | |

| Organic | ||

| By Application | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| RTE/RTC Foods | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Dietary Supplements | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF