Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

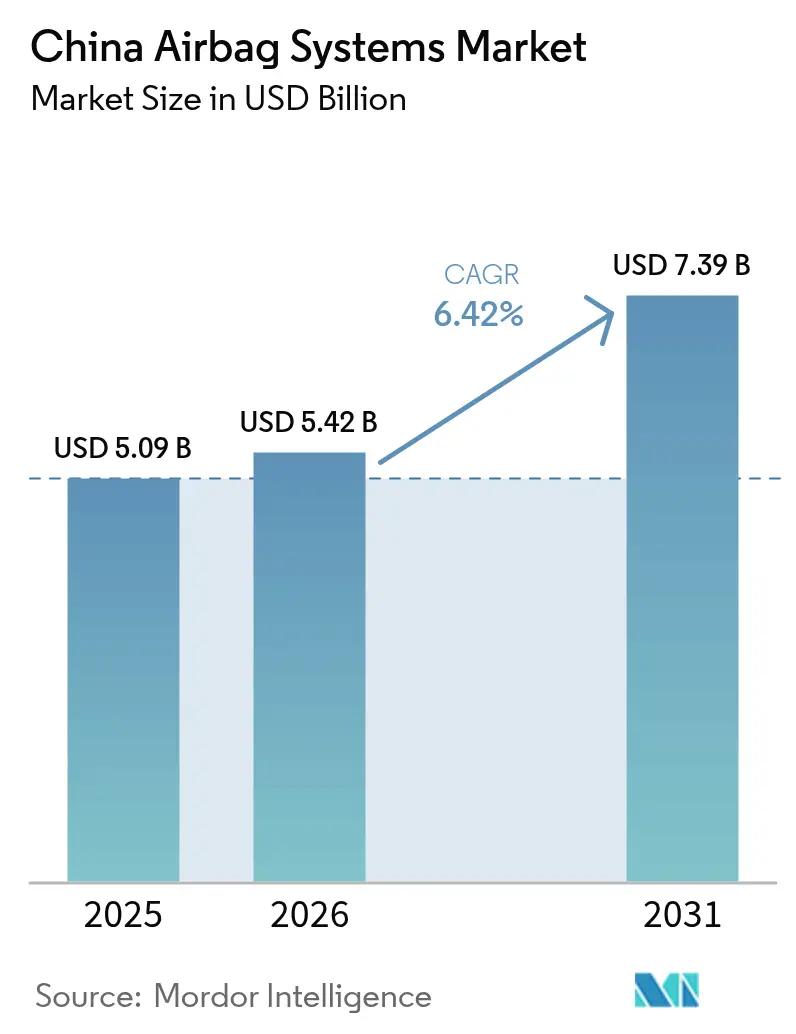

| Base Year Market Size (2025) | USD 5.09 Billion |

| Market Size (2026) | USD 5.42 Billion |

| Market Size (2031) | USD 7.39 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Airbag Systems Market Analysis by Mordor Intelligence

China Airbag Systems Market size in 2026 is estimated at USD 5.42 billion, growing from 2025 value of USD 5.09 billion with 2031 projections showing USD 7.39 billion, growing at 6.42% CAGR over 2026-2031. Mandatory GB 15083 and GB 14166 standards, rising passenger-vehicle output, and the premiumization of electric SUVs combined to sustain double-digit annual unit demand increases. Domestic suppliers are accelerating plant localization to avoid import tariffs and shipping delays, while global brands are expanding R&D outposts in Shanghai and Wuhan to keep pace with AI-enabled occupant sensing. Supply security for inflator propellants and semiconductor-grade MEMS crash sensors remains a strategic priority, pushing suppliers toward vertical integration or multi-sourcing pacts. In parallel, center airbags move from optional to standard equipment as OEMs chase the highest C-NCAP safety ratings, lifting per-vehicle content value by up to one-third.

Key Report Takeaways

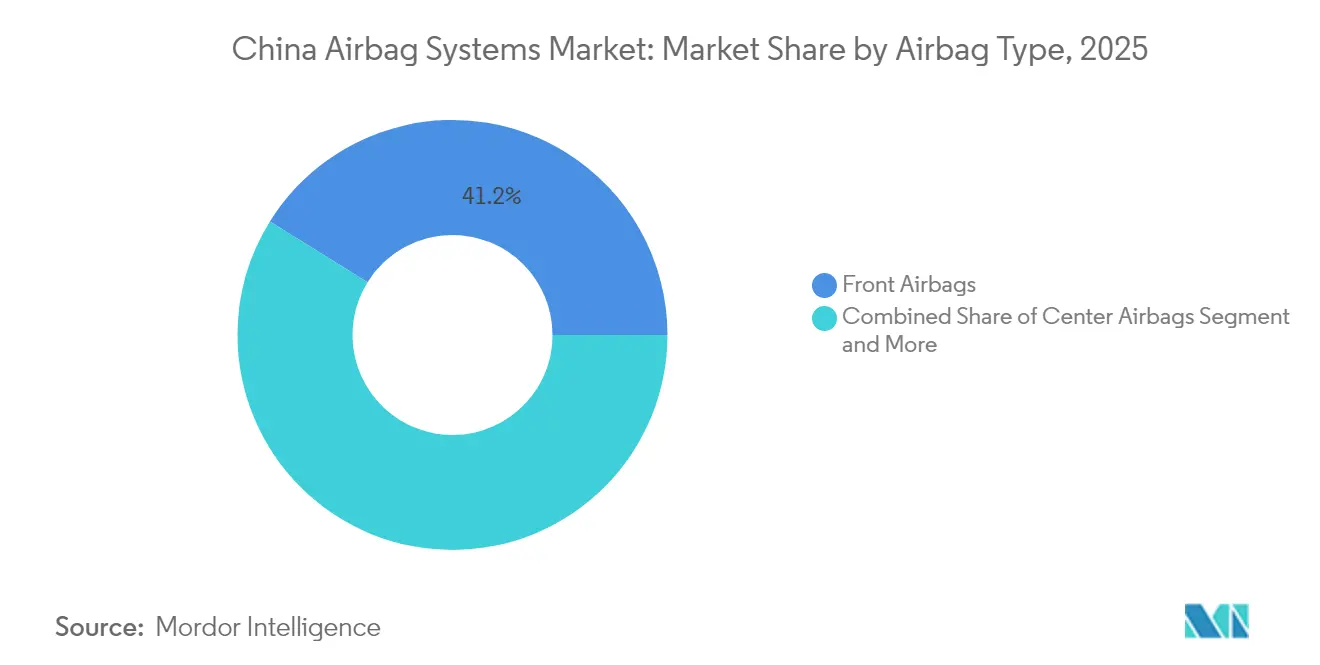

- By airbag type, front airbags led the China airbag systems market with 41.15% of the market share in 2025; center airbags are forecast to post a 6.45% CAGR through 2031.

- By vehicle type, passenger cars accounted for 83.10% of the China airbag systems market size in 2025, while buses and coaches are expected to expand at a 6.46% CAGR through 2031.

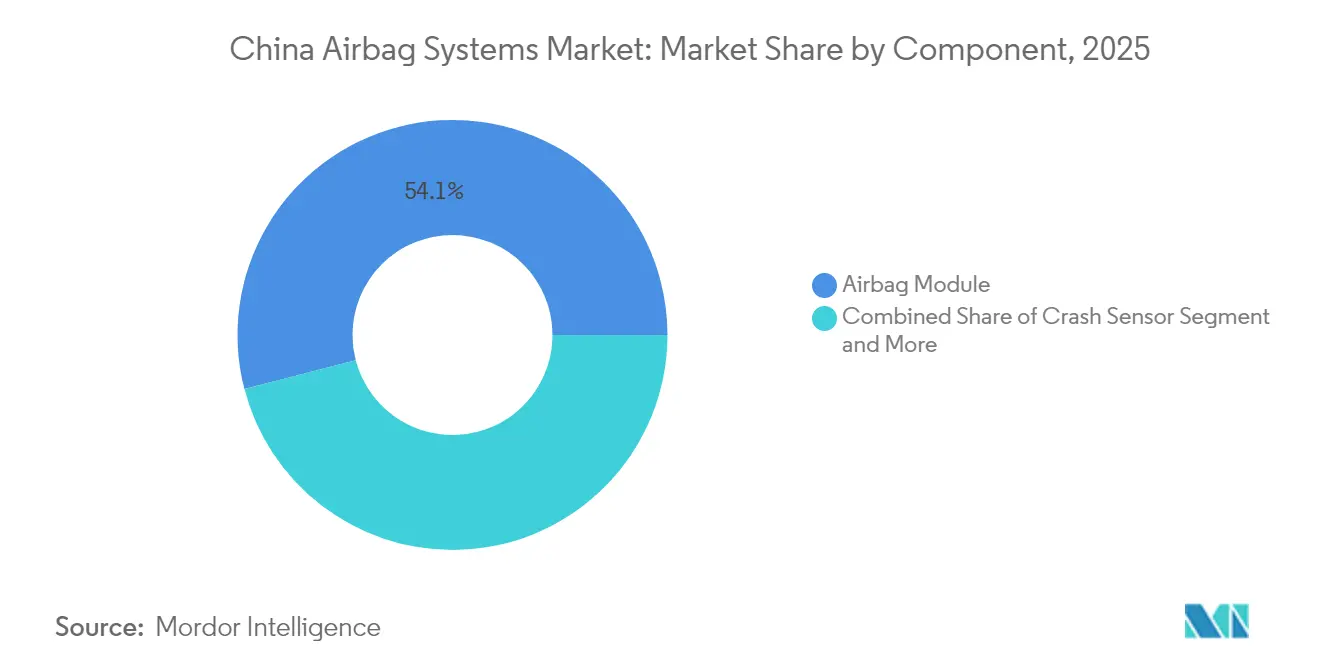

- By component, airbag modules held 54.05% revenue share of the China airbag systems market in 2025, whereas crash sensors recorded the fastest 6.50% CAGR through 2031.

- By sales channel, the OEM segment captured 86.85% of the China airbag systems market in 2025; aftermarket demand is advancing at a 6.43% CAGR as the national fleet ages.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Airbag Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory GB 15083 and GB 14166 Regulations | +1.6% | National, with enforcement across all provinces | Long term (≥ 4 years) |

| Rising Passenger-Vehicle Output | +1.2% | National, concentrated in manufacturing hubs | Medium term (2-4 years) |

| C-NCAP 2024 Star-Rating Upgrade | +1.1% | National, affecting all OEMs seeking ratings | Short term (≤ 2 years) |

| AI-Driven Occupant-Sensing Enables Adaptive Airbags | +0.9% | Premium vehicle segments, expanding to mass market | Long term (≥ 4 years) |

| EV/SUV Premiumization | +0.8% | National, with premium segments leading adoption | Medium term (2-4 years) |

| Localized Inflator and Propellant Supply Cuts Unit Cost | +0.6% | Manufacturing regions, particularly Wuhan and Xi'an | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory GB 15083 and GB 14166 Regulations

GB 15083 details multi-scenario crash performance tests, while GB 14166 governs inflator chemistry and timing. Suppliers must validate dual-stage deployment, side-impact integrity, and azide-free propellant stability through SAMR-accredited labs. Compliance increases engineering budgets by a minimal amount, but regulations ensure a predictable baseline for the production of multiple new vehicles each year [1]“GB 15083-2024 Performance Requirements for Automobile Safety Restraint Systems,” State Administration for Market Regulation, samr.gov.cn . Established players with certified test corridors, digital twins, and traceability software shorten validation cycles by one-fifth, gaining a time-to-market edge. Smaller domestic firms often partner with specialty labs in Jilin or Chongqing to avoid capital-intensive crash facilities, reinforcing collaborative innovation across the Chinese airbag systems market.

Rising Passenger-Vehicle Output

Volumes rebounded to pre-2020 levels in 2024 and are projected to track a steady annual increase through 2027. Production is heavily concentrated in Guangdong, Shanghai, and Hubei, allowing module suppliers to offset logistics costs by one-fifth compared to sea freight imports. Fleet renewal waves from 2018-2020 vintages stimulate aftermarket replacements, while government scrappage incentives maintain throughput at body-assembly plants. The predictable order books enable tier-ones to amortize the Wuhan mega-plant over a shorter horizon, reinforcing scale economics within the China airbag systems market.

C-NCAP 2024 Star-Rating Upgrade for Center and Far-Side Airbags

The revised protocol adds eight points for far-side protection, effectively requiring OEMs to include center airbags in every variant at a fair price. Suppliers have an 18-24-month window to refine folding patterns and minimize module thickness to fit narrow seat gaps. Validation costs rise one-third because each new module must pass 65 kph oblique-barrier tests plus torso-interaction simulations. Early adopters, mainly premium German-Sino joint ventures, secure price premiums and marketing leverage, reinforcing a virtuous cycle of safety-led differentiation in the China airbag systems market [2]“2024 Assessment Protocol Revision,” C-NCAP Management Center, c-ncap.org.

AI-Driven Occupant-Sensing Enables Adaptive Airbags

Leading automakers are integrating wide-angle infrared cameras into roof modules and combining the data with seat pressure mats. This innovation produces real-time 3-D avatars of vehicle occupants. Using advanced algorithms, they fine-tune gas generator outputs based on the occupant's stature, posture, and seatback angle. This adjustment has significantly improved safety performance during NCAP sled tests. Furthermore, with over-the-air updates, these algorithms are continuously refined, transitioning airbags from a passive to a semi-active role. In a notable trend, domestic electric vehicle disruptors in China are licensing these advanced models. This move not only shortens their in-house R&D cycles but also underscores the burgeoning trend of software monetization in China's airbag systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recall-Related Cost | -0.7% | National, with higher impact in premium segments | Medium term (2-4 years) |

| Counterfeit/Grey-Market Airbags Erode Trust | -0.5% | National, concentrated in aftermarket channels | Short term (≤ 2 years) |

| Tight Supply Of Azide-Free Propellant Chemicals | -0.4% | National, affecting all manufacturers | Long term (≥ 4 years) |

| Homologation Lag | -0.3% | National, concentrated in premium and EV segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recall-Related Cost and Liability Spikes

In a proactive move, SAMR has signed a data-sharing agreement with regulators in both the EU and the United States, leading to precautionary recalls even before any domestic incidents are reported. BMW's decision to recall a significant number of units in 2024 compelled its suppliers to set aside a substantial amount for remediation and legal expenses. As a result, product-liability insurance premiums surged considerably, putting financial pressure on mid-tier suppliers operating on slim margins. Original Equipment Manufacturer (OEM) contracts have evolved to incorporate punitive liquidated-damage clauses that effectively transfer the burden of recall risks downstream. This heightened scrutiny has led suppliers to adopt blockchain technology for part traceability. However, this move has also extended the duration of program quotations in the competitive Chinese airbag systems market.

Counterfeit/Grey-Market Airbags Erode Trust

Investigations uncovered inflators stamped with falsified lot codes and low-grade ammonium nitrate. Price gaps of up to four-fifths attract unsuspecting repair shops in tier-three cities. Fallout includes NHTSA warnings that tarnish the perception of legitimate Chinese makers and complicate export ambitions. Domestic e-commerce portals now require third-party authentication seals, but enforcement remains patchy beyond provincial capitals. Genuine suppliers invest in RFID-embedded logos and forensic inks, adding cost but restoring confidence in the aftermarket segment of the Chinese airbag systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Airbag Type: Center Airbags Drive Innovation

Front airbags retained the largest 41.15% slice of the China airbag systems market in 2025, yet center airbags are on track for a robust 6.45% CAGR through 2031. That surge stems from C-NCAP scoring rules that reward far-side protection, as well as from the increasing width of EV interiors, which creates space for mid-cabin modules. Driven by the launch of premium sedans and crossovers, the market for center airbags in China is expected to witness significant growth over the forecast period. Suppliers have refined burst-seam stitching techniques to eliminate seat-cover wrinkling, a cosmetic concern that previously hindered adoption. Meanwhile, regulatory mandates ensure consistent demand for side and curtain airbags, and knee airbags find their place as a niche feature in sports sedans.

Curtain modules are evolving into dual-chamber formats, offering simultaneous cushioning for both front- and rear-row occupants. To navigate this added complexity, industry leaders are turning to high-speed folding robots and laser-guided sewing tables, achieving notable improvements in production efficiency. While seatbelt-integrated airbags remain in the experimental phase, they're drawing R&D grants for autonomous-driving prototypes, hinting at a potential surge in interest in the long term. The center-airbag surge is not just a standalone event; its technological advancements, especially in novel fabrics and compact inflators, are permeating other module categories, amplifying the innovation momentum in China's airbag systems market.

By Vehicle Type: Commercial Segments Accelerate

Passenger cars commanded 83.10% of deliveries in 2025, translating to more than 21 million modules, but buses and coaches will outpace with a 6.46% CAGR. E-commerce logistics spur continuous light commercial-vehicle replacement cycles, while green-city mandates trigger electric bus tenders that specify side-rollover curtains as standard. Municipalities are prioritizing occupant safety for public fleets, driving the China airbag systems market for commercial passenger transport to experience significant growth over the forecast period.

In hazardous-materials corridors, trucks are now mandated to have dual-inflator driver bags and seatbelt pretensioners, leading to a notable increase in per-cab value. Freight operators, recognizing the benefits of reduced downtime and lower insurance rates, are elevating the bargaining power of premium safety vendors. With heavy-duty cabs accommodating thicker steering hubs, suppliers are now testing larger driver airbags, a significant upgrade from the standard found in sedans. This specialized engineering move underscores the diversification strategy many firms are adopting to counterbalance the cyclical demand for passenger cars in China's airbag systems market.

By Component: Crash Sensors Lead Technology Evolution

Airbag modules accounted for 54.05% of 2025 revenue, while crash sensors demonstrated the fastest 6.50% CAGR, as AI-based deployment logic relies on richer data streams. By the end of the forecast period, the market for crash sensors in China's airbag systems is anticipated to witness significant growth. Suppliers are now integrating triaxial accelerometers, micro-radar, and pressure transducers onto single boards, successfully reducing the wiring harness weight per vehicle. In response to the rising demand for high-tolerance chips, which are resilient to the vibrations in battery packs of electric vehicles (EVs), MEMS fabrication capacities in key manufacturing hubs have expanded.

While inflators continue to see consistent volume growth, there's a notable shift towards smokeless generants to comply with in-cabin VOC limits. Control units are now equipped with ASIL-D dual-core microcontrollers, enabling the simultaneous operation of airbag and autonomous driving systems. This integration has resulted in a noticeable reduction in latency during multi-stage deployments. Furthermore, diagnostic lines are now capable of providing real-time health reports through CAN-FD, paving the way for subscription-based predictive maintenance revenue. These technological advancements highlight a significant shift in the Chinese airbag systems market, moving from traditional commodity hardware to cutting-edge innovative systems.

By Sales Channel: Aftermarket Gains Momentum

OEM contracts captured 86.85% of 2025 shipments, yet the aftermarket is experiencing a 6.43% CAGR as multiple vehicle national fleets cross their 10-year average age milestone. Provincial inspection rules mandate the presence of functional airbags for roadworthiness, forcing owners to repair failed modules rather than de-register their vehicles. Tier-one suppliers pilot brick-and-click stores that bundle genuine modules with certified installation, slicing warranty claim rates by half. Authorized fitters rely on QR-coded calibration software that matches deployment thresholds to specific trim codes, assuring regulatory compliance and reducing liability.

Counterfeit deterrence strategies include NFC-tagged tamper-evident seals and mobile-app validation that empowers consumers to scan and verify authenticity. The promotion of certified service networks aims to capture revenue that was previously lost to unregulated workshops. Over time, data harvested from aftermarket diagnostics feeds machine-learning models that refine deployment algorithms for new-vehicle programs, forming a virtuous feedback loop that strengthens the China airbag systems market.

Geography Analysis

The coastal manufacturing belt of Guangdong, Shanghai, and Jiangsu accounts for approximately two-thirds of airbag capacity, leveraging the proximity of container ports and the density of automotive supply chains. Plants in Wuhan and Xi'an anchor central China’s emergent cluster, enjoying state subsidies that rebate up to one-fifths of fixed-asset investments . Tier-one city sales skew toward premium trims featuring 10-plus airbags, whereas inland regions favor value models with six-bag baselines, underscoring the complexity of product mix for supply planners. Infrastructure in Chongqing and Chengdu now supports high-speed crash-sled labs, shortening test logistics and fueling local R&D migration.

Export-oriented suppliers in North America face scrutiny following counterfeit scandals, prompting them to secure ISO 21434 cybersecurity certification to regain credibility. Government programs such as the Yangtze River Delta Innovation Fund co-finance safety-electronics startups that extend sensor fusion into mid-tier vehicles.

Western provinces, such as Xinjiang, are presenting new bus-safety tenders tied to Belt and Road passenger links, thereby widening geographic demand dispersion within the China airbag systems market. These regional nuances compel suppliers to adopt multi-site manufacturing footprints to hedge policy and logistics risks.

Competitive Landscape

In the Chinese airbag systems market, the top five brands—Autoliv, ZF LIFETEC, Continental AG, Joyson Safety Systems, and Yanfeng Automotive Systems—command a dominant presence, collectively accounting for a significant share of the market revenue. Autoliv operates multiple module plants, achieving rapid production cycles through fully automated sewing lines. Meanwhile, ZF enhances safety with vision-based occupant detection, a feature integrated from its tech center in Shanghai. Continental, harnessing its advanced software stack, synchronizes airbag deployment with electronic stability control events, bolstering crash-avoidance measures. Domestically, Joyson, a prominent player, offers cost-effective solutions to OEMs, providing vertically integrated inflator-through-module packages. This strategy not only reduces production costs but also ensures compliance.

Looking ahead to the near future, Autoliv is set to embark on a joint venture with HSAE, focusing on the integration of mechatronics. Concurrently, ZF is making a significant investment with a large-scale megasite in Wuhan, capable of producing a substantial volume of modules annually. In a nod to sustainability, Continental is piloting the use of recycled polyester fabrics, aiming for a notable reduction in cradle-to-gate CO₂ emissions, positioning itself ahead of impending carbon procurement regulations.

While smaller specialists are finding their footing in niche areas like crash sensors and adaptive algorithms, they steer clear of direct competition with larger module manufacturers. As local EV brands increasingly seek software-enhanced airbags, the distinction between passive and active safety is becoming increasingly blurred. This evolution is intensifying competition and sparking heightened M&A interest within the Chinese airbag systems landscape.

China Airbag Systems Industry Leaders

Autoliv Inc.

ZF Friedrichshafen AG

Joyson Safety Systems

TOYODA GOSEI Co., Ltd.

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Autoliv formed a joint venture with Hangsheng Electric (HSAE) in China to co-develop automotive safety electronics integrating mechatronic airbag control.

- June 2024: Autoliv introduced airbags fabricated from 100% recycled polyester, aiming to cut greenhouse-gas emissions across its China production lines.

China Airbag Systems Market Report Scope

By Airbag Type

| Front Airbags |

| Side Airbags |

| Curtain Airbags |

| Knee Airbags |

| Center Airbags |

| Seatbelt Airbags |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Buses & Coaches |

By Component

| Airbag Module |

| Crash Sensor |

| Inflator |

| Diagnostic Sensor |

| Control Unit |

| Others |

By Sales Channel

| OEM |

| Aftermarket |

| By Airbag Type | Front Airbags |

| Side Airbags | |

| Curtain Airbags | |

| Knee Airbags | |

| Center Airbags | |

| Seatbelt Airbags | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium & Heavy Commercial Vehicles | |

| Buses & Coaches | |

| By Component | Airbag Module |

| Crash Sensor | |

| Inflator | |

| Diagnostic Sensor | |

| Control Unit | |

| Others | |

| By Sales Channel | OEM |

| Aftermarket |

Key Questions Answered in the Report

How large will China’s airbag systems market be by 2031?

It is projected to reach USD 7.39 billion, expanding at a 6.42% CAGR from 2026.

Which type of airbag is growing the fastest in China?

Center airbags are forecast to post a 6.45% CAGR as C-NCAP rules make them essential for five-star ratings.

Why are buses and coaches attracting more airbag investment?

China’s public-transport electrification mandates enhanced passenger safety, propelling a 6.46% CAGR for airbag revenue in this segment.

What drives aftermarket demand for airbags in China?

The national fleet’s aging profile and annual safety inspections compel owners to replace faulty modules, lifting aftermarket growth to 6.43% CAGR.

How are suppliers curbing counterfeit airbag risks?

They deploy NFC authentication tags, RFID seals, and certified service networks to help buyers verify genuine parts and maintain compliance.

Which companies dominate China’s airbag systems landscape?

Autoliv, ZF LIFETEC, Continental, Joyson Safety Systems, and Yanfeng collectively account for around 65% of the market revenue.

Page last updated on: