Methyl Methacrylate (MMA) Adhesives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

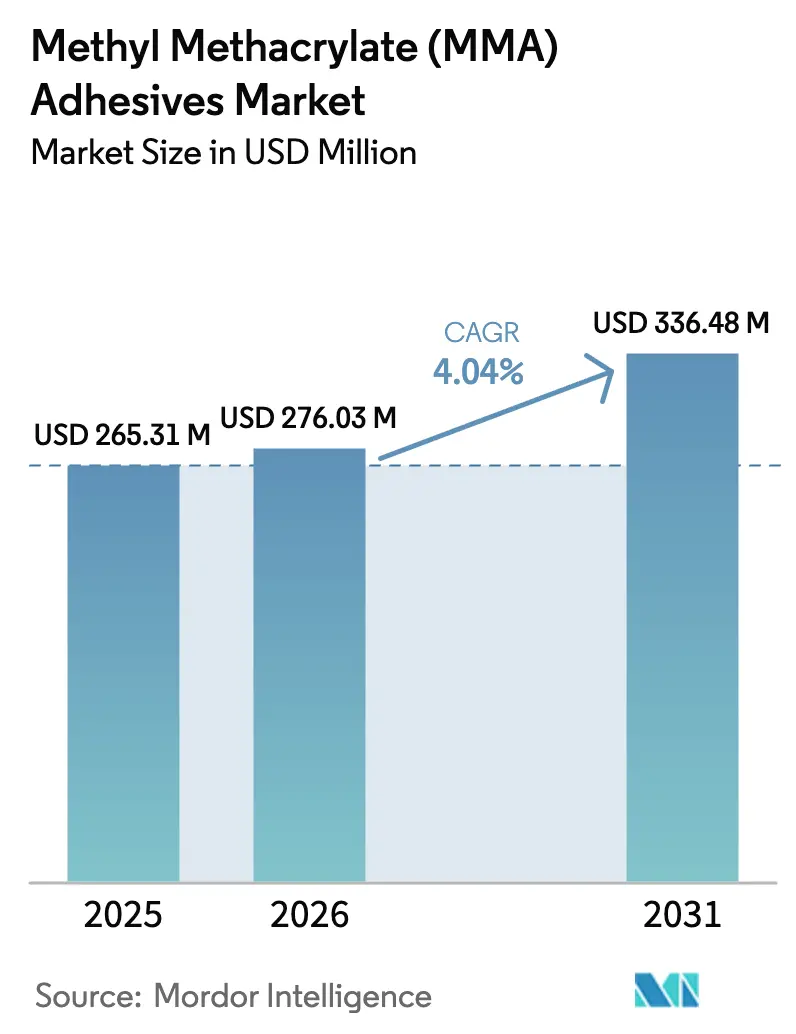

| Market Size (2026) | USD 276.03 Million |

| Market Size (2031) | USD 336.48 Million |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

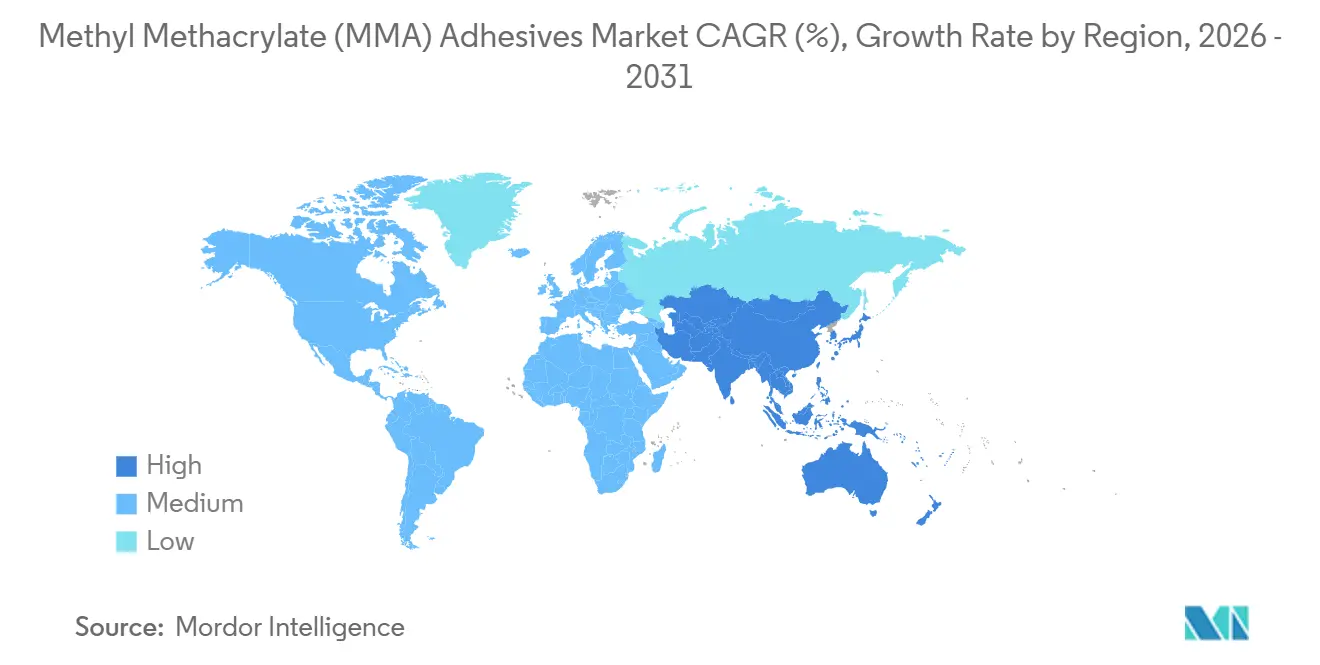

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

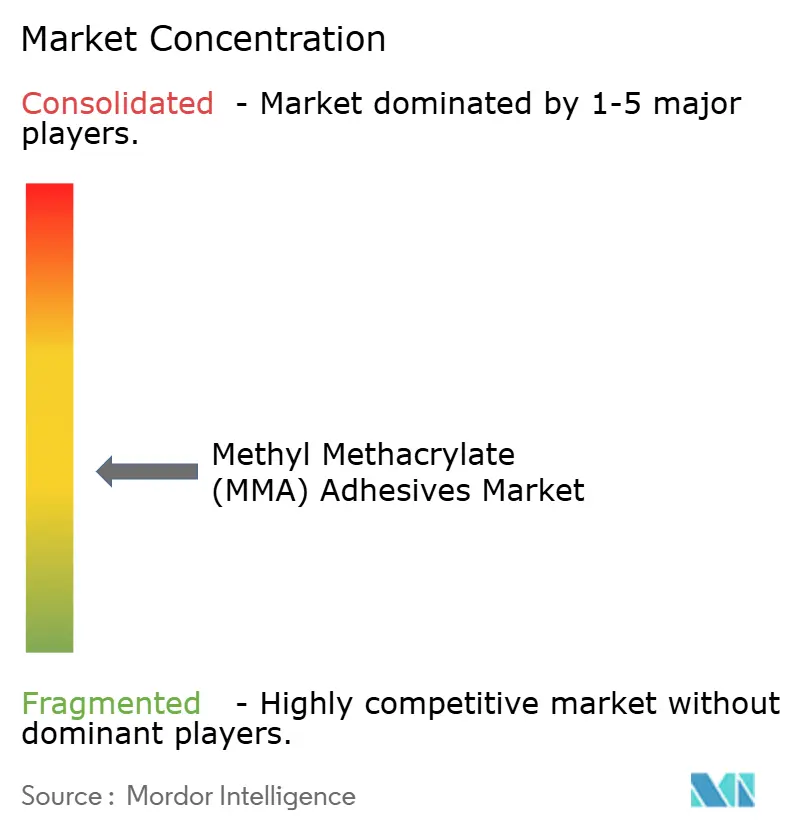

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Methyl Methacrylate (MMA) Adhesives Market Analysis by Mordor Intelligence

The Methyl Methacrylate Adhesives Market size is expected to increase from USD 265.31 million in 2025 to USD 276.03 million in 2026 and reach USD 336.48 million by 2031, growing at a CAGR of 4.04% over 2026-2031. Demand is shifting from mechanical fasteners toward structural bonding because MMA chemistry joins dissimilar substrates while cutting component weight, production time, and capital costs. Asia-Pacific leads current consumption, propelled by offshore wind blade manufacturing, ASEAN’s prefabricated construction projects, and regional shipbuilding. Metals hold a commanding but gradually eroding position as the primary substrate, while composites expand the addressable base by enabling carbon-fiber, aluminum, and thermoplastic hybrids in transportation and renewable-energy hardware. End-user priorities center on faster cure, lower odor, and compliance with tightening VOC limits, driving suppliers to roll out high-performance variants that reduce line takt time without jeopardizing joint integrity.

Key Report Takeaways

- By substrate, metals accounted for 42.19% of the methyl methacrylate (MMA) adhesives market share in 2025, while composites are poised for the fastest growth at a 6.15% CAGR through 2031.

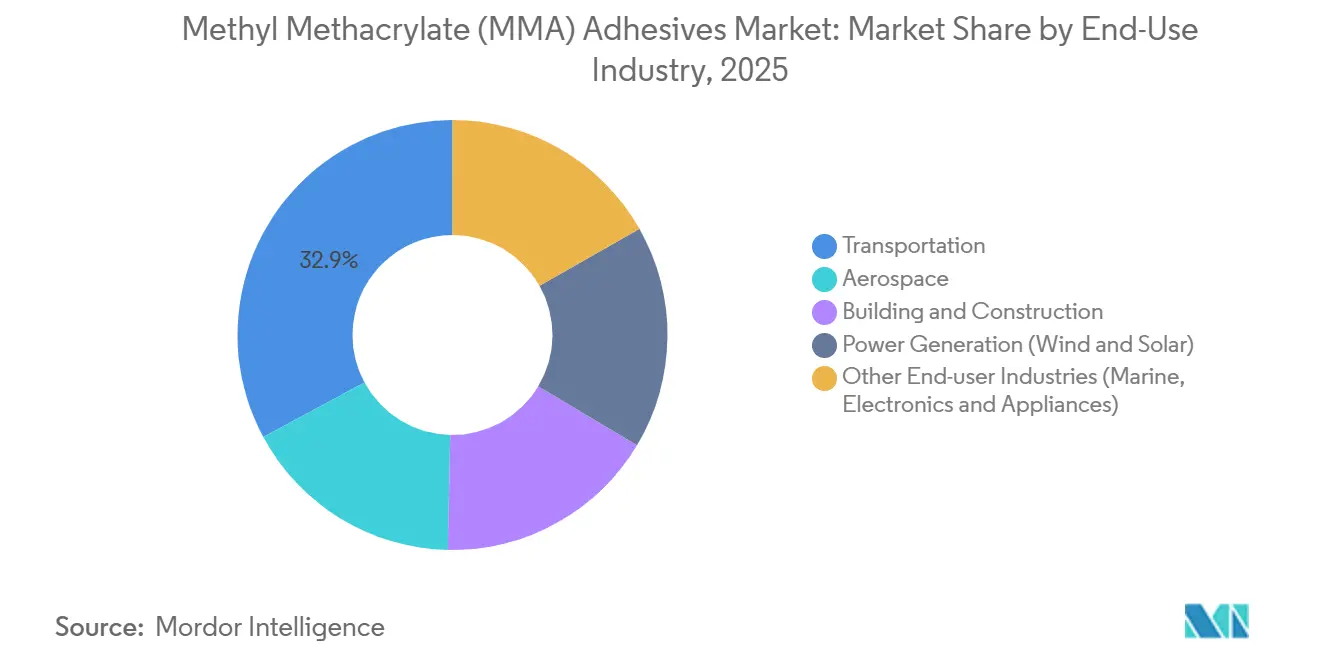

- By end-use industry, transportation led with 32.87% revenue in 2025; power generation is projected to expand at a 6.01% CAGR to 2031.

- By geography, Asia-Pacific led with 46.29% revenue in 2025 and the region is projected to expand at a 5.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Methyl Methacrylate (MMA) Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Light-Weighting Push Across Mobility Segments | +1.2% | Global, with concentration in North America, Europe, and China | Medium term (2-4 years) |

| Substitution of Welding/Riveting in Composite-Metal Joints | +0.9% | North America and Europe (aerospace), APAC (automotive) | Long term (≥ 4 years) |

| Growth of Offshore Wind-Turbine Blade Bonding | +1.1% | Europe (North Sea), APAC (China, Taiwan, South Korea), emerging in North America | Medium term (2-4 years) |

| Rapid Infrastructure Build-Out in ASEAN Prefab Construction | +0.7% | ASEAN core (Vietnam, Thailand, Indonesia, Malaysia) | Short term (≤ 2 years) |

| Increasing Demand from Marine Sector | +0.4% | Global, with early gains in Asia-Pacific shipbuilding hubs and European yacht manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Light-Weighting Push Across Mobility Segments

Automakers and aircraft OEMs are eliminating mechanical fasteners to remove mass, improve range, and meet CO₂ targets. Ford cut 47 kg from its 2025 F-150 Lightning by bonding aluminum to high-strength steel with MMA adhesives, realizing a 3.2% range gain. Airbus reported a 680 kg reduction on each A321neo after replacing rivets in secondary structures, saving 1.8% fuel over the aircraft life. Because every kilogram trimmed extends electric-vehicle range by roughly 20 m, MMA bonding’s premium over welding is economically justified, particularly when OEMs avoid the capital outlay for new spot-welding cells. Formulators are therefore focused on 15- to 30-minute fixture times that match paced assembly lines while meeting new 50 ppm workplace-exposure limits in the EU.

Substitution of Welding/Riveting in Composite-Metal Joints

Composite content exceeds 50% on the Boeing 787 and Airbus A350, yet drilling fastener holes degrades fatigue life. NASA’s 2024 test program found bonded joints extend composite fatigue life by 15%-25% compared with riveted equivalents[1]NASA, “Advanced Composites Project 2024 Findings,” nasa.gov . Spirit AeroSystems eliminated 1,200 fasteners per 737 MAX wing set, trimming USD 18,000 in build cost and 34% in assembly time after shifting to MMA adhesives in 2025. BMW achieved 28 MPa lap-shear strength when bonding carbon-fiber roofs to aluminum pillars on the iX M60, avoiding galvanic corrosion while tolerating differential thermal expansion. Aerospace certification under ISO 11003-2 keeps barriers high, locking in value once a formulation is approved.

Growth of Offshore Wind-Turbine Blade Bonding

Blade lengths topping 115 m impose cyclic loads approaching 1 billion stress cycles over 25 years. Vestas switched to MMA formulations for its V236-15 MW turbines after peel strength held 94% of baseline in accelerated marine aging, compared with epoxies’ 78%. Cure time dropped from eight hours to 90 minutes, boosting mold throughput without new capital. China’s 71 GW offshore pipeline under construction will consume an extra 145-218 t of MMA adhesive annually as each megawatt requires 8-12 kg in spar-cap and shell bonds. Low-temperature-cure grades are specified for the 2.9 GW Hornsea 3 project to accommodate winter assembly at 5 °C.

Rapid Infrastructure Build-Out in ASEAN Prefab Construction

The Asian Development Bank values ASEAN’s infrastructure backlog at USD 3.1 trillion through 2030, with modular building favored to speed delivery. Vietnam mandates prefab methods for 60% of new industrial parks, spurring MMA demand for steel-to-aluminum façade bonding where adhesives stop thermal bridging and support LEED certification. Thailand’s Eastern Economic Corridor specifies MMA for curtain walls because 45-minute open times fit humid-tropical field conditions. Indonesia’s 2024 code revision now allows structural MMA bonding up to eight stories, broadening the application space.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in MMA Monomer Feedstock Prices | -0.8% | Global, with acute impact in regions dependent on imported feedstock (Asia-Pacific non-producing nations, Latin America) | Short term (≤ 2 years) |

| Stringent VOC and Odor Exposure Limits | -0.5% | Europe and North America (strict enforcement), emerging in APAC urban centers (Japan, South Korea, Singapore) | Medium term (2-4 years) |

| Cartridge Waste-Disposal Regulations in Urban Plants | -0.3% | North America and Europe urban manufacturing zones, expanding to China Tier-1 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in MMA Monomer Feedstock Prices

Spot MMA prices jumped 18% to USD 2,340 /t FOB Asia in Q2 2025 after propylene outages in China and South Korea, squeezing formulators unable to lock long-term contracts. A 15% feedstock hike lifts finished-adhesive cost by 9%-11%, but competitive pressure caps pass-through at 4%-6%, clipping gross margins 300-500 bp. Mitsubishi Chemical’s 100 kt/yr Saudi plant, started in 2024, adds capacity yet still covers just 3.2% of global supply. Because only 4 of the top 15 suppliers run captive monomer production, the majority remain exposed to swings that showed a 32% coefficient of variation over 24 months.

Stringent VOC and Odor Exposure Limits

The EU cut the 8-h workplace limit for MMA to 50 ppm in January 2025, forcing manufacturers to reformulate or add ventilation systems costing USD 180,000-420,000 per line[2]European Chemicals Agency, “REACH Dossier Update 2025,” echa.europa.eu . South Coast AQMD capped VOCs in structural adhesives at 250 g/L in March 2025, driving a 25% solvent reduction that lengthens cure and trims green strength by up to 12%. Workers detect MMA odor at 0.2 ppm; a German IG Metall survey logged 23% more complaints versus polyurethane in 2024, prompting OEMs to pay USD 0.32-0.48/kg for odor-masking additives. Japan now mandates respiratory protection for enclosed-space application, raising compliance hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate: Metals Dominate, Composites Accelerate

Metals produced the largest slice of demand, accounting for 42.19% in 2025, because automotive and aerospace builders still rely heavily on aluminum-to-steel joints that require 18-24 MPa lap-shear strength and tolerate differing thermal expansion rates. In value terms, the metals slice of the methyl methacrylate (MMA) adhesives market size stood at USD 116.5 million in 2026. Composites are the clear growth engine, expanding at a 6.15% CAGR to 2031 as carbon-fiber wind-turbine spar caps and aircraft secondary structures proliferate. Adhesive joints eliminate galvanic-corrosion concerns while spreading loads over greater surface area, extending fatigue life in next-generation airframes.

The composites surge encapsulates a structural material shift rather than a cyclical rebound. Boeing raised composite content on the 777X to 54%, specifying MMA bonding for fuselage-panel integration that avoids the drilling damage seen with rivets. Wind turbines longer than 100 m require gap-filling adhesives that cure at ambient temperature in coastal factories lacking climate control, a niche where MMA chemistry surpasses epoxies. Plastics form a small yet rising cohort—especially ABS, polycarbonate, and acrylic in EV battery casings—because MMA joins them with minimal surface prep. Ceramics and wood remain niche uses, though ceramic-metal bonds in electronics heat sinks are attracting R&D attention.

By End-Use Industry: Transportation Leads, Power Generation Surges

Transportation absorbed 32.87% of global revenue in 2025 as OEMs deploy multi-material body structures to meet emission and range targets. Power generation will post the fastest 6.01% CAGR through 2031, powered by offshore wind blades that consume 8-12 kg of adhesive per megawatt and by glass-to-metal bonds in solar modules. Wind alone could lift annual demand by 200+ t by 2031 as 15 MW turbines move mainstream.

Aerospace commands premium pricing of USD 18-32/kg because every formulation faces ISO 11003-2 and OEM-specific test regimes. Building and construction adoption widens as architects pursue sleek façades without thermal bridging; Sika’s 45-minute open-time grade suits humid Southeast-Asian jobsites. The marine segment gains from composite superstructures that lower the center of gravity, cut fuel burn, and free interior volume. Electronics and appliances are emerging users; Samsung trimmed refrigerator build time by 28% after switching to MMA for stainless-steel-to-polymer bonding.

Geography Analysis

Asia-Pacific captured 46.29% of global demand in 2025 and is set to advance at 5.76% CAGR to 2031. China approved 18.2 GW of new offshore wind in 2025, each MW adding up to 12 kg of MMA usage, translating to an incremental 145-218 t per year. India built 5.9 million passenger cars in FY 2024-25, accelerating adhesive uptake to meet fuel-economy rules tightening to 118 g CO₂/km by 2027. Japan’s hydrogen-fuel-cell road map is spurring MMA use in carbon-fiber storage tanks that must hold 700 bar without micro-cracking. ASEAN’s USD 3.1 trillion infrastructure pipeline leans heavily on prefab modules bonded with MMA, with adoption climbing to 34% of new commercial starts in 2025.

In North America, Boeing’s plan to build 38 737 MAX jets per month consumes up to 11 t of adhesive monthly for secondary structures alone. The Inflation Reduction Act encourages local sourcing; Henkel’s USD 65 million expansion in Connecticut adds 12 kt of annual capacity for automotive and wind clients. Canada’s 5 GW offshore wind prospects will open a fresh channel when construction begins in 2027-29. Mexican auto hubs used about 3,200 t in 2025 as GM and Ford rolled out EV platforms that bond aluminum battery trays to steel underbodies.

Europe, though mature, is buoyed by 7.3 GW of offshore wind commissioned in 2025 and by OEM shifts toward adhesive bonding to trim welding costs. Volkswagen cut 340 welds on each ID.7 roof panel, saving EUR 18 per unit. The UK’s latest Contracts for Difference round awarded 6.4 GW of offshore projects entering build phase from 2026. Smaller yet promising, South America rides Brazilian wind expansions, while the Middle East benefits from Saudi Arabia’s NEOM city, which mandates adhesive-bonded façades in 80% of residential buildings.

Competitive Landscape

The top five suppliers—Henkel, Sika, 3M, Arkema, and H.B. Fuller—control roughly 48% of the methyl methacrylate (MMA) adhesives market. Competition pivots on performance innovation, not price, because aerospace, wind, and automotive OEMs cannot risk unqualified substitutes. Henkel’s 2024 buyout of Scheugenpflug integrates precision dispensers with Loctite chemistries, locking in customers through proprietary mixing protocols. Sika unveiled a cloud-linked viscosity-monitoring system in 2025 that flags degradation before bond strength drops, cutting scrap on high-value parts. 3M’s 2025 Scotch-Weld 7290 meets 45-minute handling targets for EV battery enclosures, while Arkema partners with Futerro to launch 40% bio-based monomers by 2027.

Niche specialists such as Permabond and Master Bond win aerospace and electronics contracts by offering on-site engineering; their AS9100D-certified plants support direct supply to primes wary of global freight snarls. Patent filings underline strategic thrusts: Henkel logged 14 low-odor MMA patents, while 3M submitted 11 on metal-surface interactions that extend durability in salt spray. Regulatory readiness is a moat: ISO 10365-certified formulations command 12%-18% price premiums in European aerospace because requalification for alternates can take up to 30 months.

Methyl Methacrylate (MMA) Adhesives Industry Leaders

3M

H.B. Fuller Company

Sika AG

Arkema

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Evonik Industries AG introduced VISIOMER Terra IPGMA monomers, specifically designed for high-performance, low-odor adhesives. This development addressed a longstanding concern regarding the strong odor associated with methyl methacrylate (MMA) adhesives.

- October 2024: IPS Corporation expanded its methyl methacrylate (MMA) adhesives portfolio by acquiring MMA/acrylate technology from L&L Products. It strengthened its capacity to serve the European and North American markets.

Global Methyl Methacrylate (MMA) Adhesives Market Report Scope

Methyl methacrylate (MMA) glue is a two-part structural adhesive designed to create strong and durable bonds between metals, composites, and plastics. It offers high resistance to impact, vibration, and chemicals, making it suitable for applications in automotive, marine, and industrial sectors as an alternative to welding or riveting. The adhesive cures through polymerization, hardening quickly at room temperature while delivering excellent strength and performance in demanding conditions.

The methyl methacrylate adhesives (MMA) market is segmented by substrate, end-use industry, and geography. By substrate, the market is segmented into metals, plastics, composites, and other substrates. By end-use industry, the market is segmented into transportation, aerospace, building and construction, power generation (wind and solar), and other end-use industries (marine, electronics, and appliances). The report also covers the market size and forecasts for methyl methacrylate adhesives (MMA) in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Metals |

| Plastics |

| Composites |

| Other Substrates |

| Transportation |

| Aerospace |

| Building and Construction |

| Power Generation (Wind and Solar) |

| Other End-user Industries (Marine, Electronics and Appliances) |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Substrate | Metals | |

| Plastics | ||

| Composites | ||

| Other Substrates | ||

| By End-Use Industry | Transportation | |

| Aerospace | ||

| Building and Construction | ||

| Power Generation (Wind and Solar) | ||

| Other End-user Industries (Marine, Electronics and Appliances) | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the methyl methacrylate (MMA) adhesives market?

The global market stands at USD 276.03 million in 2026 and is forecast to reach USD 336.48 million by 2031.

Which region leads consumption of MMA adhesives?

Asia-Pacific holds 46.29% of global demand, driven by offshore wind, prefab construction, and shipbuilding.

Which end-use sector will grow the fastest?

Power generation, especially offshore wind blades, will register a 6.01% CAGR through 2031.

Why are composites boosting MMA adhesive demand?

Composites need gap-filling, fatigue-resistant bonds that eliminate drilling and galvanic corrosion, advantages intrinsic to MMA chemistry.

Page last updated on: