Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

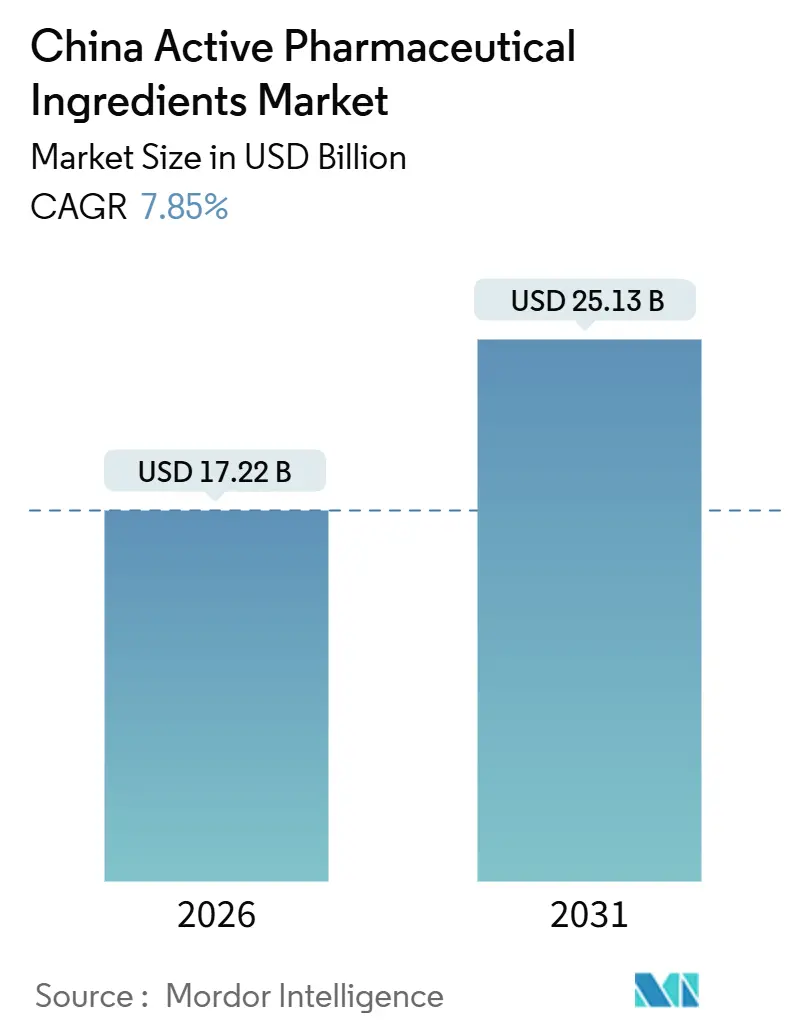

| Market Size (2026) | USD 17.22 Billion |

| Market Size (2031) | USD 25.13 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Active Pharmaceutical Ingredients Market Analysis by Mordor Intelligence

The China Active Pharmaceutical Ingredients Market size is estimated at USD 17.22 billion in 2026, and is expected to reach USD 25.13 billion by 2031, at a CAGR of 7.85% during the forecast period (2026-2031).

The market trajectory rides on expedited review pathways, vertically integrated cost advantages, and expanding merchant capacity that link upstream coal-based solvents to downstream crystallization. At the same time, national volume-based procurement (VBP) and U.S. security legislation are pressuring margins, forcing suppliers to pivot toward complex, high-value molecules. Biotech APIs are growing fastest, buoyed by a domestic biologics pipeline that moved 3,575 candidates into active development between 2015 and 2024. Currency depreciation strengthens export pricing, yet volatile coal and solvent costs offset part of that benefit. Competitive strategies now revolve around green manufacturing upgrades, regional satellite plants, and niche technologies such as peptide synthesis and antibody-drug conjugates.

Key Report Takeaways

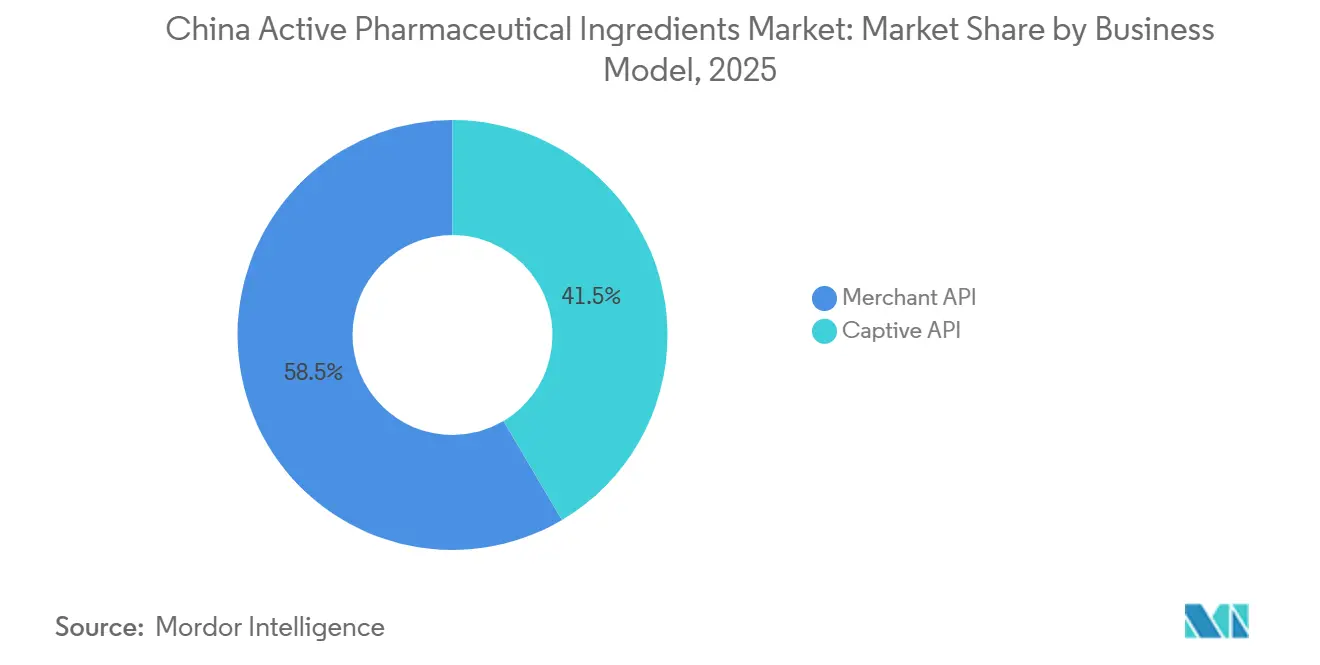

- By business model, merchant API operations led with 58.55% of the China active pharmaceutical ingredients market share in 2025; captive plants are projected to trail as merchant capacity expands at an 8.25% CAGR to 2031.

- By synthesis type, synthetic routes commanded 70.53% of the China active pharmaceutical ingredients market size in 2025, while biotech APIs are forecast to post the highest 11.85% CAGR through 2031.

- By drug type, generic molecules held 73.63% share of the China active pharmaceutical ingredients market size in 2025, but branded APIs are set to grow at 10.87% CAGR between 2026 and 2031.

- By application, oncology maintained a 24.3% revenue share in 2025; neurology APIs are advancing at a 12.81% CAGR through 2031 as Alzheimer’s and Parkinson’s prevalence climbs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Active Pharmaceutical Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & lifestyle diseases | +1.4% | Eastern provinces | Long term (≥ 4 years) |

| Growing domestic use of biologics & biosimilars | +1.8% | Beijing, Shanghai, Suzhou | Medium term (2-4 years) |

| Yuan depreciation widens export price advantage | +0.9% | Zhejiang, Jiangsu, Shandong | Short term (≤ 2 years) |

| Supply-chain friend-shoring boosts China CDMO orders | +1.2% | Global | Medium term (2-4 years) |

| Government policies favoring local manufacturing | +1.1% | National | Long term (≥ 4 years) |

| Rising demand for affordable generics | +1.0% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Chronic & Lifestyle Diseases

Cardiovascular disease, diabetes, and cancer account for more than 80% of Chinese mortality, and 75% of citizens aged 60 plus manage at least one chronic condition[1]Chinese CDC, “Chronic Disease Trends 2025,” chinacdc.cn. The burden guarantees sustained ordering of statins, metformin precursors, and oncology intermediates despite VBP price compressions. Diagnosed diabetes cases reached 140 million, locking in high baseline demand for antidiabetic APIs. Provincial cancer-screening mandates introduced under Healthy China 2030 further accelerate orders for PD-1 and kinase inhibitor intermediates. Because the population aged 65 plus will top 300 million by 2030, demand for neurology and osteoporosis APIs is projected to remain resilient across the forecast window.

Growing Domestic Use Of Biologics & Biosimilars

China initiated 4,382 innovative drug programs between 2015 and 2024, and 18 Chinese-origin products won overseas approvals, catalyzing local demand for monoclonal-antibody and recombinant-protein APIs[2]Nature Biotechnology Editors, “China’s Biologics Innovation Landscape,” nature.com. Kelun-BPC invested in ADC intermediates, while Luye Pharma advanced nanomedicine capabilities to retain more value margins that generic VBP has eroded. Streamlined biosimilar review rules introduced in 2020 helped trastuzumab follow-ons capture sizeable domestic share within 18 months. Cytiva’s 2025 index rated China 5.72 in biomanufacturing capacity and reported that 61% of surveyed sponsors plan to increase regional sourcing. These indicators underpin the 11.85% CAGR outlook for biotech APIs over 2026-2031.

Yuan Depreciation Widens Export Price Advantage

A gradual yuan weakening improved dollar-denominated unit costs for Zhejiang and Jiangsu exporters by 3-4% when currency slipped 5% versus the U.S. dollar. The benefit is strongest for high-volume pain and vitamin molecules, yet firms with dollar debt or imported catalysts experience offsetting cost inflation. Vertically integrated producers such as CSPC, which source acetone and methanol domestically, capture the full currency benefit. Buyers, however, increasingly insert quarterly price adjustment clauses, shifting FX risk back to suppliers.

Supply-Chain Friend-Shoring Boosts China CDMO Orders

Despite political rhetoric, friend-shoring has lifted near-term CDMO volumes because alternate regions lack equivalent reactor capacity. WuXi AppTec’s Taixing and Changzhou plants passed FDA inspections without observations in March 2025, reinforcing foreign client confidence. Asymchem opened a U.K. site in 2024, and Pharmaron purchased facilities in Cramlington and Coventry, offering Western domiciles while retaining core Chinese manufacturing. Yet the U.S. Biosecure Act introduced in 2024 caused sponsors to pause new orders, cutting WuXi Advanced Therapies revenue 17% through Q3 2024. The duality is expected to persist through 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Drug-price control & national volume-based procurement | -1.6% | Tier-1 and Tier-2 cities | Short term (≤ 2 years) |

| Fierce competition & stricter GMP / environmental rules | -1.1% | Coastal clusters | Medium term (2-4 years) |

| Emerging U.S./EU tariffs on critical-drug raw materials | -0.7% | Zhejiang, Jiangsu, Shandong | Short term (≤ 2 years) |

| Volatile coal & solvent prices squeezing small producers | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Drug-Price Control & National Volume-Based Procurement

The 2024 VBP extension to oncology triggered API cost-down requests that erased 1.6 percentage points from market CAGR projections. CSPC’s bulk-drug revenue dipped 1.6% year-over-year in 2024 despite higher volumes, illustrating margin erosion. The policy accelerates commoditization by neutralizing brand differentiation, forcing suppliers toward complex peptides and HPAPIs where VBP leverage is weaker.

Fierce Competition & Stricter GMP / Environmental Rules

The 14th Five-Year Plan mandates wastewater and emission upgrades that can cost RMB 50 million for a mid-size plant. Zhejiang Huahai’s June 2025 FDA warning letter for data-integrity lapses highlighted rising compliance scrutiny. Smaller firms face exit risks if they cannot recoup capital under compressed VBP pricing, accelerating consolidation in Jiangsu and Zhejiang clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Merchant Operations Secure Greater Volume Share

Merchant players captured 58.55% of 2025 revenue in the China active pharmaceutical ingredients market and are tracking an 8.25% CAGR to 2031. Western pharma is outsourcing to preserve R&D budgets, and multi-client portfolios help spread fixed costs. WuXi’s Taixing complex, spanning 169 acres with over 1,000 m³ reactors, demonstrates the scale advantage. Captive facilities risk low utilization whenever pipeline assets fail or patents expire, while merchant suppliers can redeploy capacity quickly. However, reliance on a concentrated foreign client base leaves merchant firms vulnerable to geopolitical shocks such as the Biosecure Act suspension wave that dented WuXi Advanced Therapies revenue in 2024.

The merchant model also eases geographic diversification. Asymchem’s U.K. acquisition and Pharmaron’s British sites allow Chinese CDMOs to list Western regulatory addresses while retaining low-cost mainland production. High-potency and peptide lines command premium pricing, insulating margins from VBP, and are the focal points of most new merchant CAPEX through 2031.

By Synthesis Type: Biotech Route Records Fastest Growth

Synthetic chemistry still holds 70.53% of the 2025 market value in the China active pharmaceutical ingredients market, yet biotech APIs are scaling at an 11.85% CAGR courtesy of an accelerated biologics pipeline. Mammalian cell-culture capacity is expanding in Suzhou and Shanghai parks, with Cytiva rating Chinese biomanufacturing at 5.72 in its 2025 index.

Biotech APIs earn 3-5 times the unit price of small molecules, cushioning suppliers against input price swings. Synthetic APIs face shrinking spreads as VBP covers more molecules, nudging chemistries toward chiral intermediates and HPAPIs where specialized containment justifies higher quotations.

By Drug Type: Branded Molecules Gain Momentum

Generic molecules represented 73.63% of the 2025 China active pharmaceutical ingredients market size, but branded APIs are advancing at 10.87% CAGR, lifted by a surge in in-licensed Chinese pipeline assets that hit 31% in 2024. Branded intermediates enjoy stronger pricing power under exclusivity and often include profit-sharing clauses.

Generic APIs continue to underpin cash flow; CSPC reported vitamin C sales of RMB 1,994 million in 2024, up 3.4% year-over-year. Nonetheless, suppliers are redirecting CAPEX toward continuous manufacturing and enzymatic synthesis platforms to defend margins on branded APIs as the NMPA’s expedited review compresses launch timelines.

By Application: Neurology Surges On Aging Demographics

Oncology maintained 24.3% revenue share in 2025, but neurology APIs are slated for a 12.81% CAGR as Alzheimer’s and Parkinson’s incidence grows with an aging base. Healthy China 2030 screening and therapy expansion underpin the oncology baseline.

Neurology growth reflects newfound product success abroad; disease-modifying treatments approved in the U.S. catalyze analogous Chinese trials, prompting Luye Pharma to invest in CNS-targeted nanomedicines. Pulmonology APIs remain stable, while cardiology stays volume heavy yet margin thin under VBP.

Geography Analysis

Provincial output is concentrated: Jiangsu, Zhejiang, and Shandong contribute significant percentage of national API volume by leveraging feedstock proximity, port logistics, and industrial-park incentives[3]Zhejiang Medicine Co., “Corporate Presentation 2025,” zmc.com.cn. Jiangsu’s Taizhou and Lianyungang plants specialize in analgesic and penicillin intermediates; Zhejiang’s clusters command vitamins E and biotin; Shandong leverages coal-chemicals for antibiotic precursors.

Export dynamics show a split strategy. High-value HPAPIs and peptides go to North America and Europe, while commodity APIs serve ASEAN, Latin America, and Africa. Yet 59% of Chinese plants await FDA inspection, a risk spotlighted in Wall Street Journal coverage. Section 301 tariffs and the U.S. Biosecure Act add uncertainty, prompting WuXi to plan a Singapore site for 2027 and Asymchem to establish capacity in the U.K..

Domestic consumption is diffusing into Tier-2 and Tier-3 cities as VBP penetrates county hospitals, widening API distribution grids. Cold-chain needs for biologics and provincial QC bottlenecks challenge logistics, yet the shift reduces reliance on volatile export revenue over the long term.

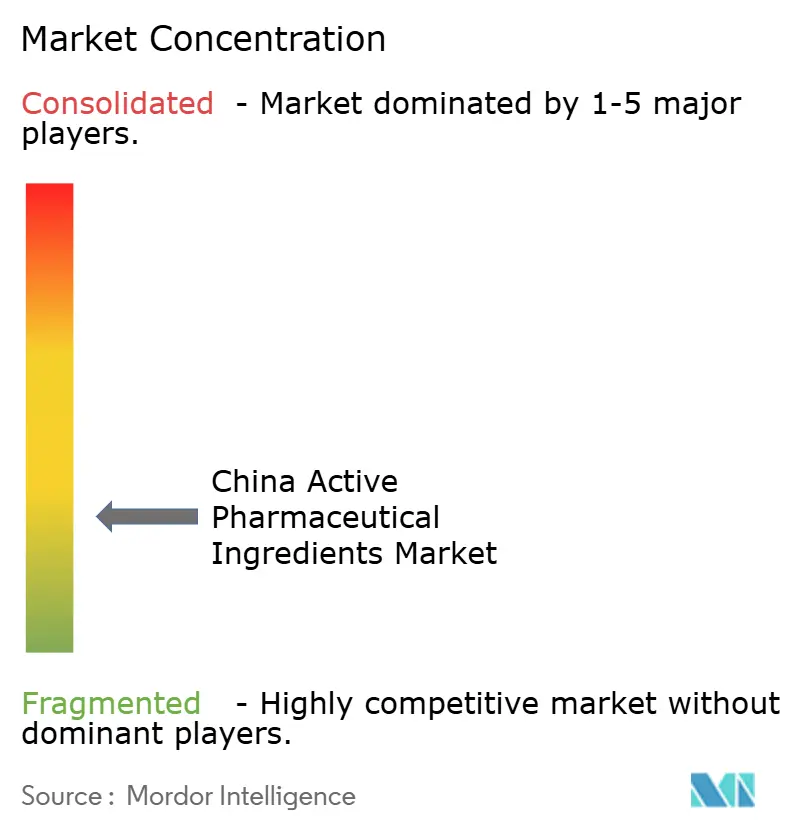

Competitive Landscape

China’s API arena is fragmented. The top 10 suppliers command a significant percentage of revenue, leaving a long tail of small firms focused on commoditized molecules. Leading CDMOs are capturing high-potency niches: Asymchem launched an OEB5 facility in Tianjin with 500 kg annual capacity in July 2025. WuXi AppTec raised HKD 7.7 billion in July 2025 to fund overseas expansion and green upgrades.

Strategy divides along scale lines. Large firms deploy satellite plants abroad to reassure Western clients, while specialists triple down on flow chemistry, controlled substances, or agrochemical adjacencies. Viva Biotech and Porton Pharma integrate CRO, CMC, and API services, shortening lead times for biotech sponsors.

Technology adoption remains uneven. Continuous manufacturing is concentrated among tier-one CDMOs, yet the 14th Five-Year Plan’s green mandates are pushing even smaller facilities to invest in closed-loop solvent recovery. Regulatory compliance is a decisive moat; Zhejiang Huahai’s FDA letter underscores reputational stakes and accelerates industry consolidation.

China Active Pharmaceutical Ingredients Industry Leaders

Reyoung Pharmaceuticals

Sandoz Group AG

CSPC Pharmaceutical Group Ltd.

WuXi AppTec (STA Pharmaceutical)

Lonza Guangzhou Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: WuXi AppTec’s Changzhou and Taixing API sites cleared consecutive FDA inspections with zero observations.

- February 2025: Chinese producers lowered export prices on 41 critical APIs by 40-50%, affecting India’s PLI-backed self-reliance push.

China Active Pharmaceutical Ingredients Market Report Scope

As per the scope of the report, an active pharmaceutical ingredient (API) is a part of any drug that produces its effects. Some drugs, such as combination therapies, have multiple active ingredients to treat symptoms or act differently. They are produced using highly technological industrial processes during the R&D and commercial production phases.

The China active pharmaceutical ingredients market is segmented by business mode, synthesis type, type of drug, and application. By business mode, the market is segmented into captive API and merchant API. By synthesis type, the market is segmented into synthetic and biotech. By drug type, the market is segmented into generic and branded. By application, the market is segmented into cardiology, oncology, pulmonology, neurology, orthopedics, ophthalmology, and other applications. The report offers the value (USD) for the above segments.

By Business Mode

| Captive API |

| Merchant API |

By Synthesis Type

| Synthetic |

| Biotech |

By Drug Type

| Generic |

| Branded |

By Application

| Cardiology |

| Oncology |

| Pulmonology |

| Neurology |

| Orthopedic |

| Ophthalmology |

| Other Applications |

| By Business Mode | Captive API |

| Merchant API | |

| By Synthesis Type | Synthetic |

| Biotech | |

| By Drug Type | Generic |

| Branded | |

| By Application | Cardiology |

| Oncology | |

| Pulmonology | |

| Neurology | |

| Orthopedic | |

| Ophthalmology | |

| Other Applications |

Key Questions Answered in the Report

How large is the China active pharmaceutical ingredients market in 2026?

It is valued at USD 17.22 billion and is projected to reach USD 25.13 billion by 2031, registering a 7.85% CAGR.

Which segment is expanding fastest by synthesis type?

Biotech-derived APIs are growing at an 11.85% CAGR thanks to a robust domestic biologics pipeline.

What share do merchant suppliers hold?

Merchant operations controlled 58.55% of 2025 revenue and are on track for an 8.25% CAGR through 2031.

Why is neurology API demand accelerating?

Rising Alzheimer's and Parkinson's prevalence in an aging population drives a 12.81% CAGR for neurology molecules.

How is VBP affecting API profitability?

National procurement demands price cuts of 30% or more, squeezing margins on generic APIs and pushing producers toward high-value niches.

What environmental rules shape future investments?

The 14th Five-Year Plan requires costly wastewater and emission upgrades, compelling smaller plants to consolidate or exit the market.

Page last updated on: