Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

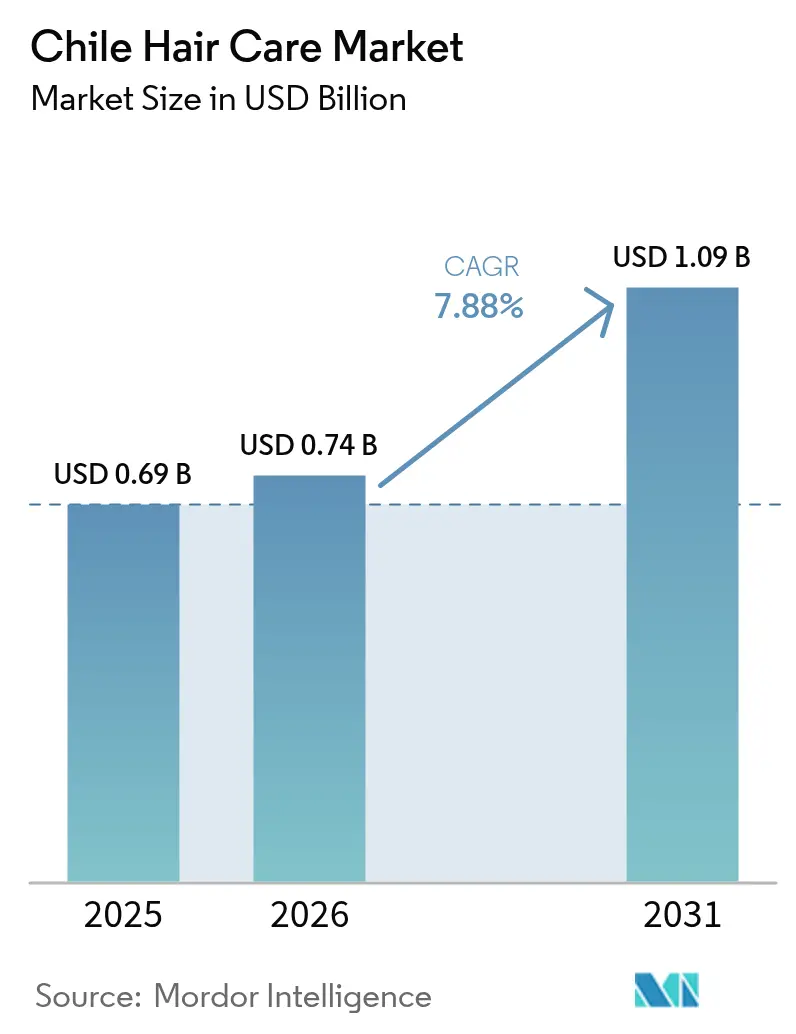

| Base Year Market Size (2025) | USD 0.69 Billion |

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 7.88% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chile Hair Care Market Analysis by Mordor Intelligence

The Chile Hair Care Market size was valued at USD 0.69 billion in 2025 and estimated to grow from USD 0.74 billion in 2026 to reach USD 1.09 billion by 2031, at a CAGR of 7.88% during the forecast period (2026-2031). Hair care products maintain a significant position in the personal care industry, as hair remains a key indicator of beauty. The market is experiencing growth as more consumers, particularly men, focus on their physical appearance and seek natural and traditional hair care solutions. This shift in consumer behavior has led to increased demand for products such as organic shampoos, natural conditioners, hair oils, and traditional hair treatments derived from botanical sources. The market growth is driven by multiple factors, including harsh climate conditions, poor water quality, and increasing adoption of hair coloring practices. These elements necessitate sophisticated hair care routines and regular treatments, strengthening market demand. Consumers are increasingly investing in deep conditioning treatments, hair masks, and protective styling products to combat environmental damage.

Key Report Takeaways

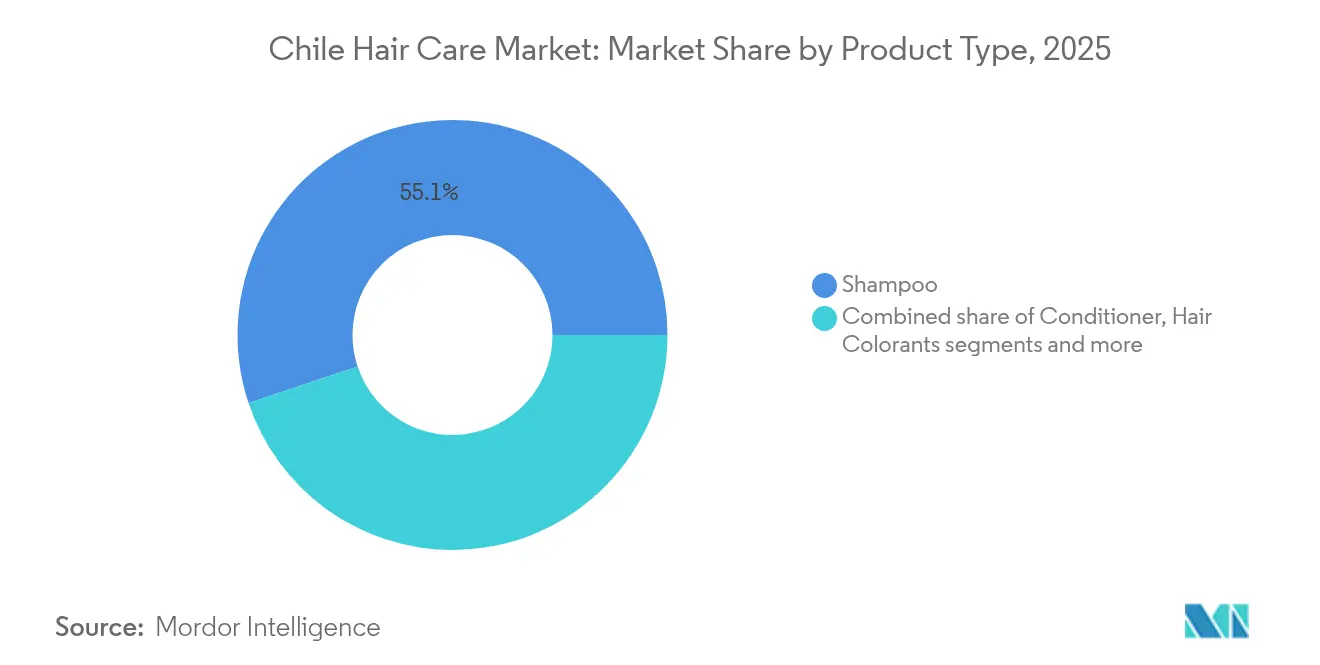

- By product type, shampoo led with 55.12% of the Chile hair care market share in 2025, hair styling products recorded the fastest 8.05% CAGR for 2026-2031.

- By category, mass products held 77.78% share in 2025, whereas premium products are set to advance at an 8.25% CAGR to 2031.

- By ingredient type, conventional/synthetic captured 73.95% Chile hair care market share in 2025, while natural and organic alternatives will expand at a 8.74% CAGR.

- By distribution channel, supermarkets and hypermarkets retained a 40.92% share in 2025, yet online retailing posts the strongest 9.1% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for eco-friendly, certified-organic products | +1.2% | National, with early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement | +1.8% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Demand for multi-functional and damage control products | +1.5% | National, with higher adoption in metropolitan areas | Medium term (2-4 years) |

| Technological innovations in product formulations | +1.1% | National, with premium segment focus | Long term (≥ 4 years) |

| Expansion of e-commerce and digital retailing | +2.1% | National, with strongest impact in Santiago region | Short term (≤ 2 years) |

| Rising male grooming segments | +0.8% | National, with urban concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preference for Eco-Friendly, Certified-Organic Products

Chilean consumers increasingly prioritize environmental sustainability, driving demand for certified-organic hair care formulations that align with the country's environmental consciousness. The preference extends beyond ingredient sourcing to packaging sustainability, with consumers favoring brands that demonstrate measurable environmental impact reduction. Chile's stringent environmental regulations and consumer awareness campaigns have elevated sustainability from a niche preference to a mainstream purchasing criterion. Natural ingredient sourcing from Chile's diverse ecosystems, including Patagonian botanicals and Atacama Desert minerals, presents opportunities for local and international brands to develop region-specific formulations that command premium pricing. Major retailers have established dedicated "natural beauty" sections in their stores, indicating the shift from niche to mainstream consumer demand. The Instituto de Salud Pública's regulatory oversight enhances consumer confidence in certified product claims.

Influence of Social Media and Celebrity Endorsement

Social media platforms drive hair care purchasing decisions among Chilean consumers, with Instagram and TikTok serving as primary discovery channels for new products and styling techniques. Chilean influencers and celebrities wield a significant impact on beauty trends, particularly in hair styling and color preferences that reflect seasonal fashion cycles. The phenomenon extends beyond traditional advertising to user-generated content and peer recommendations, creating authentic engagement that translates to purchase intent. Chile's high social media penetration rate amplifies brand messaging and product demonstrations. According to the StatCounter Global Stats data from 2024, 42.93% of people in Chile used Facebook, and 27.95% used Instagram [1]Source: StatCounter Global Stats, "Social Media Stats in Chile", statcounter.com . Digital marketing strategies that incorporate local cultural references and Chilean lifestyle elements demonstrate higher engagement rates compared to generic Latin American campaigns. The trend creates opportunities for brands to leverage micro-influencers and beauty professionals who maintain authentic connections with Chilean audiences while building trust through consistent product demonstrations and results sharing.

Demand for Multi-Functional and Damage Control Products

Chilean consumers seek hair care solutions that address multiple concerns simultaneously, reflecting time-conscious lifestyles and value-driven purchasing decisions. This demand stems from Chile's active outdoor culture and environmental factors, including UV exposure, wind, and seasonal climate variations that contribute to hair damage. Multi-functional products that combine cleansing, conditioning, and protective benefits appeal to consumers seeking efficiency without compromising hair health. The trend particularly resonates with working professionals who prioritize streamlined beauty routines while maintaining hair quality standards. Damage control formulations targeting heat styling, chemical processing, and environmental stressors address the specific needs of Chilean consumers who frequently use styling tools and hair coloring services. Product innovations that incorporate heat protection, UV filters, and strengthening agents within single formulations capture market share by delivering comprehensive hair care solutions that align with Chilean lifestyle demands.

Technological Innovations in Product Formulations

Advanced formulation technologies enable hair care brands to develop products specifically adapted to Chilean climate conditions and consumer hair types. These innovations include microencapsulation techniques that ensure sustained ingredient release, pH-balancing systems that work with Chile's varying water hardness levels, and climate-responsive formulations that adjust to seasonal humidity changes. The integration of biotechnology and sustainable chemistry creates opportunities for brands to differentiate through performance while meeting environmental standards. Chilean consumers demonstrate a willingness to pay premium prices for technologically advanced products that deliver measurable results, particularly in anti-aging and hair-strengthening categories. Research and development investments in formulation science enable brands to address specific concerns prevalent among Chilean consumers, including hair thinning, premature graying, and damage from frequent styling. The trend supports market premiumization as consumers recognize the value proposition of scientifically backed formulations over conventional alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over chemical ingredients | -0.9% | National, with higher impact in educated urban segments | Medium term (2-4 years) |

| Proliferation of counterfeit products | -0.6% | National, with concentration in informal retail channels | Short term (≤ 2 years) |

| Competition from home remedies and natural alternatives | -0.7% | National, with rural and traditional household focus | Long term (≥ 4 years) |

| Limited awareness in rural areas | -0.5% | Rural regions, particularly in northern and southern Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over Chemical Ingredients

Growing awareness of potentially harmful chemicals in conventional hair care products creates consumer hesitation and drives demand for ingredient transparency among Chilean consumers. This concern particularly affects products containing sulfates, parabens, and synthetic fragrances, leading to increased scrutiny of product labels and ingredient lists. Chilean health authorities and consumer protection agencies have heightened awareness through public education campaigns about cosmetic safety, influencing purchasing decisions toward perceived safer alternatives. The trend disproportionately affects mass-market products that rely on cost-effective synthetic ingredients, creating opportunities for premium and natural brands to capture market share through clean formulation positioning. Consumer education initiatives by health-conscious brands help address concerns while building trust through transparent communication about ingredient safety and efficacy. The restraint creates pressure on manufacturers to reformulate existing products and invest in safer alternative ingredients, potentially increasing production costs while improving long-term brand positioning.

Proliferation of Counterfeit Products

Counterfeit hair care products entering Chile through informal distribution channels undermine consumer confidence and create safety concerns that affect overall market growth. These products often contain harmful ingredients and fail to deliver promised results, leading to negative experiences that influence consumer perception of hair care categories. Chile's geographic position and trade relationships create vulnerabilities to counterfeit product infiltration, particularly through online marketplaces and informal retail networks. The presence of counterfeit products creates price pressure on legitimate brands while potentially causing health issues that generate negative publicity for the entire hair care category. Regulatory enforcement efforts by Chilean authorities help combat counterfeiting, but the challenge requires ongoing vigilance and consumer education to maintain market integrity. Brand protection strategies, including authentication technologies and authorized retailer networks, help legitimate manufacturers differentiate their products while building consumer trust through verified purchase channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoo Dominates Amid Styling Innovation

Shampoo maintains commanding market leadership with 55.12% share in 2025, reflecting its essential role in Chilean hair care routines and frequent repurchase cycles that generate consistent revenue streams. Hair styling products emerge as the fastest-growing segment at 8.05% CAGR through 2031, driven by increasing style consciousness and social media influence on appearance standards among Chilean consumers. Conditioner products capture significant market share through complementary positioning with shampoo purchases, while hair colorants benefit from Chile's fashion-forward culture and acceptance of hair color experimentation across age groups.

The product type segmentation reveals distinct consumer behavior patterns, with basic cleansing needs supporting shampoo dominance while aspirational styling drives growth in specialized products. Other product types, including treatments, masks, and leave-in products, gain traction as consumers develop more sophisticated hair care routines influenced by professional salon experiences and online beauty education. The segment dynamics reflect Chile's evolving beauty culture, where functional hair care expands into lifestyle and self-expression categories that command higher price points and stronger brand loyalty.

By Category: Mass Products Evolve Toward Premium Positioning

Mass products command 77.78% market share in 2025, reflecting price-conscious purchasing behavior and widespread distribution through supermarkets/hypermarkets across Chile's urban and rural markets. Premium products accelerate at 8.25% CAGR through 2031, indicating consumer willingness to invest in higher-quality formulations as disposable income increases and beauty awareness expands. This growth trajectory suggests market maturation where consumers graduate from basic functionality to performance-driven and experience-focused products that deliver superior results.

The category segmentation highlights Chile's economic development impact on consumer behavior, with rising middle-class purchasing power enabling premium product adoption without abandoning mass-market accessibility. According to the World Bank data from 2023, per capita Gross Domestic Product (GDP) at Purchasing Power Parity in Chile was USD 32,809.9 . Premium segment growth concentrates in metropolitan areas where consumers demonstrate higher beauty spending and brand consciousness, while mass products maintain relevance in price-sensitive segments and rural markets. The dual-track growth pattern creates opportunities for brands to develop portfolio strategies that capture both value-seeking and premium-aspiring consumer segments through differentiated product positioning and pricing strategies.

By Distribution Channel: Online Retail Disrupts Traditional Models

Supermarkets/Hypermarkets maintain a 40.92% market share in 2025, leveraging convenience, competitive pricing, and broad product selection that appeals to Chilean consumers' preference for one-stop shopping experiences. Online retail stores accelerate at 9.1% CAGR through 2031, driven by digital adoption, convenience preferences, and expanded product access that particularly benefits consumers in smaller cities and rural areas. Specialty stores provide expert consultation and premium product focus that supports higher-value transactions, while other channels, including pharmacies and direct sales, maintain niche market positions.

According to the International Telecommunication Union (ITU), 94% of Chile's population had internet access in 2023 . This digital connectivity allows businesses to expand their market reach through online channels, providing product specifications and consumer feedback to facilitate purchasing decisions. The multi-channel landscape creates opportunities for omnichannel strategies that combine physical retail experiences with digital convenience, potentially optimizing customer acquisition costs while maximizing market reach across Chile's diverse geographic and demographic segments.

By Ingredient Type: Natural Transition Reshapes Formulation Landscape

Conventional synthetic formulations maintain 73.95% market dominance in 2025, supported by cost-effectiveness, proven efficacy, and established consumer familiarity with traditional hair care ingredients. Natural and organic alternatives surge at 8.74% CAGR through 2031, reflecting environmental consciousness and health awareness trends that particularly resonate with younger Chilean consumers and educated urban demographics. This growth differential indicates a market transition toward cleaner formulations while maintaining synthetic ingredient relevance for performance-critical applications.

The ingredient type evolution reflects broader sustainability trends in Chilean consumer culture, where environmental protection awareness drives purchasing decisions across multiple product categories. Natural and organic positioning enables premium pricing strategies while appealing to consumers seeking authentic, environmentally responsible beauty solutions that align with personal values. The segmentation creates opportunities for hybrid formulations that combine natural ingredients with synthetic performance enhancers, potentially capturing consumers seeking both efficacy and environmental responsibility in their hair care choices.

Geography Analysis

The capital's cosmopolitan culture and professional workforce create demand for sophisticated hair care solutions that support personal branding and workplace appearance standards. Valparaíso and Concepción emerge as secondary growth centers, benefiting from university populations and cultural dynamism that drive beauty experimentation and trend adoption. Regional market dynamics reflect Chile's economic geography, with northern mining regions demonstrating strong purchasing power but limited product variety, while southern agricultural areas show growing interest in hair care investment as economic development expands.

The country's unique climate zones, from desert to temperate, create distinct hair care needs, with northern consumers requiring UV protection and moisture retention products, while southern regions focus on humidity control and seasonal adaptation formulations. E-commerce expansion particularly benefits smaller cities and rural areas where physical retail options remain limited, enabling national brands to achieve broader market penetration.

Chile's geographic market structure supports premium positioning strategies in urban centers while maintaining mass-market accessibility in smaller communities, creating opportunities for tiered product portfolios that address diverse economic and lifestyle segments. The country's strong logistics infrastructure and established retail networks facilitate efficient distribution, while cultural homogeneity enables national marketing campaigns that resonate across regional boundaries.

Regulatory Landscape

Hair care products in Chile are regulated under the national cosmetic control framework overseen by the Instituto de Salud Publica de Chile (ISP) within the Ministry of Health. A key compliance anchor is Decreto Supremo No. 239/2002 (Reglamento del Sistema Nacional de Control de Cosméticos), which defines sanitary control requirements, including the need for sanitary registration to market cosmetic products (including hair products) in Chile, with registrations valid for five years.

Market access and ongoing commercialization depend on meeting ISP requirements for product authorization pathways (including notifications where applicable), Spanish-language labeling requirements covering purpose and warnings, and digital processing through the ISP platform (GICONA). For brands selling mass-consumption hair care in consumer packaging, compliance is also shaped by obligations linked to Chile's extended producer responsibility approach for packaging and waste (Ley REP), which influences packaging design and material choices, along with take-back and recycling coordination across retail channels.

Competitive Landscape

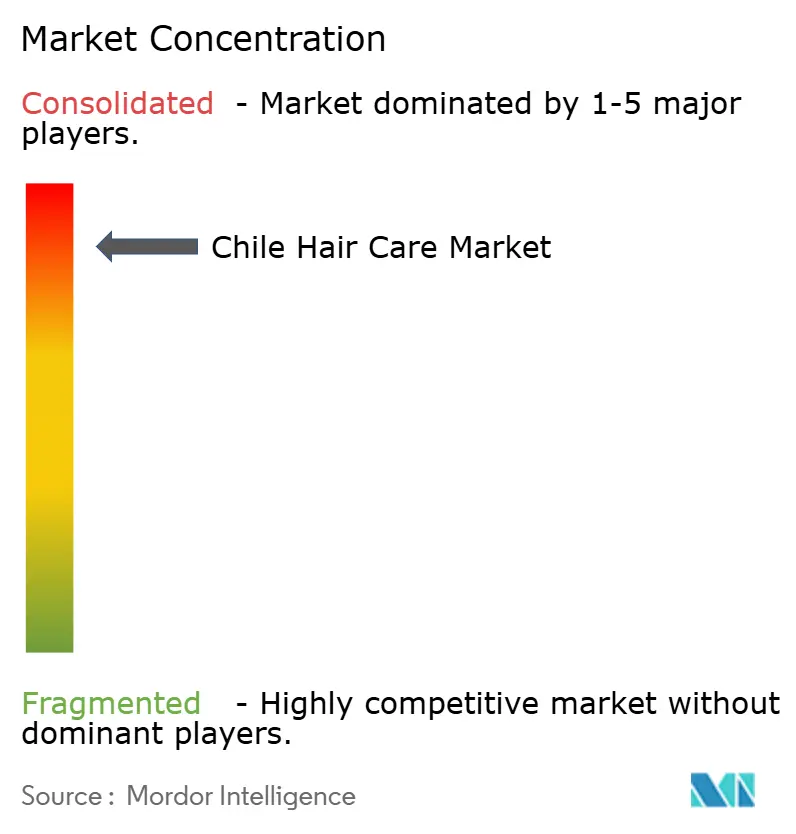

The Chile hair care market is highly consolidated. Major players in the market include Coty Inc., The Procter & Gamble Company, Unilever Plc, Laboratorio Ballerina Ltd, and L'Oreal SA. Technological innovation is reshaping the competitive landscape, with companies harnessing AI for tailored product recommendations and sophisticated formulation development. These advancements are driving product differentiation and enhancing consumer engagement, offering competitive edges while establishing entry barriers.

This is particularly evident in the premium segment, where efficacy claims demand rigorous scientific validation, making technological integration a critical factor for success. Moreover, the market is gravitating towards direct-to-consumer models. Brands like Nutrafol, specializing in hair growth supplements, underscore the potential of targeted strategies to generate significant value, even in a market dominated by a few players.

Moreover, the direct-to-consumer (DTC) distribution model is expanding in Chile's hair care market. This business strategy allows companies to establish direct consumer relationships and collect real-time purchasing data. Companies utilize this market intelligence to modify their product portfolio, target specific consumer segments like scalp treatments and sulfate-free products, and address the market demand for specialized hair care solutions.

Chile Hair Care Industry Leaders

-

Coty Inc

-

The Procter & Gamble Company

-

Unilever Plc

-

Laboratorio Ballerina Ltd

-

L'Oreal SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory execution creates room for companies that can operationalize compliance and shorten time to market in Chile. ISP-administered sanitary control under Decreto No. 239/02, together with import steps that may include certificates for customs destination and ISP-related use or disposal documentation, tends to favor manufacturers and importers that invest in strong regulatory dossiers, Spanish-compliant labeling, and traceable post-market processes. This also supports opportunities in claims-led segments such as natural and organic hair care, where formal safety and labeling processes help brands differentiate from informal and counterfeit supply.

Channel and packaging shifts add further opportunity. Supermarkets and hypermarkets continue to function as a major volume engine (40.92% share in 2025), while online retailing is the fastest-growing route-to-consumer (9.1% CAGR in the report outlook), expanding access to broader assortments across Chile. In-market programs that use refill and reusable-pack formats for mainstream hair care lines, including Unilever initiatives for TRESemme and Dove in 2024, create actionable avenues for refillable hair care formats and circular-packaging execution that align with consumer sustainability preferences and packaging-waste rule requirements.

Recent Industry Developments

- June 2026: Laboratorio Ballerina announced expansion beyond Chile through entry into the Peruvian household and personal care market. The company extended its regional route-to-market, which can support scale in procurement and manufacturing for adjacent categories, with potential spillover into hair care portfolio positioning across the Pacific coast.

- December 2025: Coty completed the divestiture of its remaining 25.8% stake in Wella to KKR for USD 750 million. The transaction further separates Coty from a major dedicated hair care manufacturer, signaling portfolio focus changes that can alter how the company allocates capital and partnerships in hair-related categories across markets.

- October 2024: Unilever launched a sustainable packaging initiative in Chile with refillable containers for TRESemme and Dove hair care products in partnership with major supermarket chains. The program linked hair care consumption to refill behavior in mainstream retail, reinforcing the strategic role of packaging formats and retailer collaboration in winning repeat purchases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Chile hair care market is measured as the value of hair cleansing, conditioning, treatment, coloring, and styling products sold to consumers in Chile across retail and professional channels, reported in USD.

Scope exclusions: We exclude hair accessories, electrical appliances, and salon service fees because they are not product sales.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Product Types

-

By Category

- Premium Products

- Mass Products

-

By Ingredient Type

- Natural and Organic

- Conventional/Synthetic

-

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame the demand environment and keep assumptions anchored to publicly visible signals in Chile. We reviewed official statistics and releases such as Chilean customs and trade data, Banco Central and inflation series, national statistics publications, and relevant health or consumer safety regulator updates that affect labeling and product movement.

To understand category direction and channel change, additional references were used such as company annual reports and investor presentations, retailer and distributor websites, trade association pages, patents and scientific journals on ingredients and formulation trends, and reputable press coverage. We also used an internal paid subscription for company financials and news context, plus a shipment-level trade database where it helped validate import intensity. These desk sources are illustrative only, and many other public references were checked for data capture, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with brand and category teams, distributors and importers, retail channel managers, and salon or professional channel stakeholders. Respondent input was used to confirm what is counted as hair care value in practice, validate the price ladder, and pressure-test channel splits and adoption trends before the final outputs were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 19% | |

| Mid tier: 41% | Functional/Unit leaders: 31% | |

| Smaller Players: 20% | Managers: 50% |

Market-Sizing & Forecasting

Market sizing used a top-down build that starts from Chile category spending signals and reconstructs hair care value by mapping product groups and channel availability, then converting to USD on a consistent timing basis. Those totals were corroborated with selective bottom-up approximations, including sampled price points by pack size, channel checks on promotional depth, and supplier or importer volume direction where data was observable.

Key model inputs included category price inflation versus real consumption, shifts between modern trade, pharmacy, and e-commerce, the mix change between mass and premium formats, import reliance for finished products, and the pace of treatment and colorant adoption versus basic shampoo and conditioner. Where bottom-up coverage was incomplete, gaps were handled using conservative penetration ranges validated in interviews, and then reconciled back to the top-down envelope.

For forecasting, scenario analysis was used, with scenarios tied to variables like expected inflation path, household consumption outlook, channel expansion rates, and expected promotional intensity. Assumptions were reviewed with primary respondents so the base case stayed realistic for planning and did not drift into overly aggressive price or volume growth.

Data Validation & Update Cycle

Outputs were triangulated across multiple checks, including year-over-year growth sanity tests, channel mix coherence, and price-versus-volume consistency, followed by an internal multi-step review before sign-off. When a variance was found, the model was reopened, and the related assumption was either corrected with source support or revalidated through follow-up outreach.

The report is refreshed annually, and interim updates are triggered when material events occur, such as sharp currency moves, tax or labeling changes, or notable channel disruptions. Before delivery, a final analyst pass is completed so clients receive the most current view aligned to the latest available indicators.

Mordor Intelligence's Chile Hair Care Market Market Sizing Compared With Other Published Estimates

Published market sizes for Chile hair care often do not match because the counting boundary is not the same across studies, and because prices and currency conversion are not applied on the same timing. Differences also show up when one estimate includes salon services or accessories, or when another uses a narrow product list that misses treatments, styling, or take-home professional items.

The refresh cycle is another common driver, since assumptions on price ladder movement and promotional intensity can change quickly in consumer categories, and a different currency conversion month can shift the USD value even if local spending is stable. By refreshing key ASP and FX timing inputs close to the publication window and then rechecking the totals against channel and trade signals, Mordor Intelligence keeps the 2025 value tied to what is being sold in-country.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.69 B (2025) | |

| Global Consultancy A | USD 0.78 B (2024) | Uses a different base year and mixes estimated-year pricing with a separate forecast window, which can lift the number if price progression is assumed before being validated through channel checks. |

| Industry Publisher B | USD 0.15 B (2024) | Likely applies a narrower category scope and definition of hair care, which can exclude parts of treatments, styling, and professional take-home products, thereby compressing the reported market value. |

The spread in the table is mainly explained by scope boundaries, base-year selection, and how price and FX timing are applied when translating local sales into USD. Using transparent product coverage and repeatable checks on price and channel signals helps keep the final market size practical for decision-making and easier to reconcile to real market movement.

Key Questions Answered in the Report

How big is the Chile hair care market today?

The Chile hair care market stands at USD 0.74 billion in 2026 and is on track to reach USD 1.09 billion by 2031 at a 7.88% CAGR.

Which product category is growing the fastest?

Hair styling products register the highest 8.05% CAGR for 2026-2031, driven by social-media trends and rising personal-style expression.

What drives premium segment expansion?

Higher disposable incomes, professional salon influence and demand for technology-backed performance push premium products ahead at an 8.25% CAGR.

Why is online retail important for hair-care brands in Chile?

Online sales grow at 9.1% CAGR, leveraging smartphone penetration and nationwide delivery networks that extend assortments to smaller cities and rural areas.

Page last updated on: